Mega Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

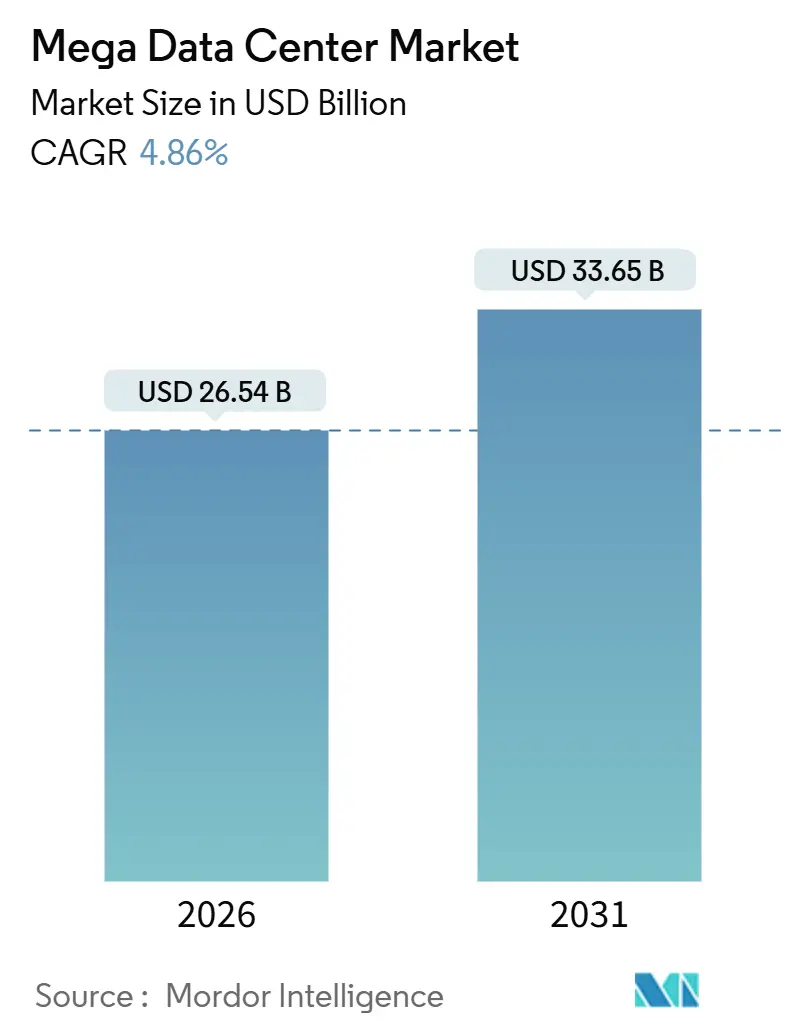

| Market Size (2026) | USD 26.54 Billion |

| Market Size (2031) | USD 33.65 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

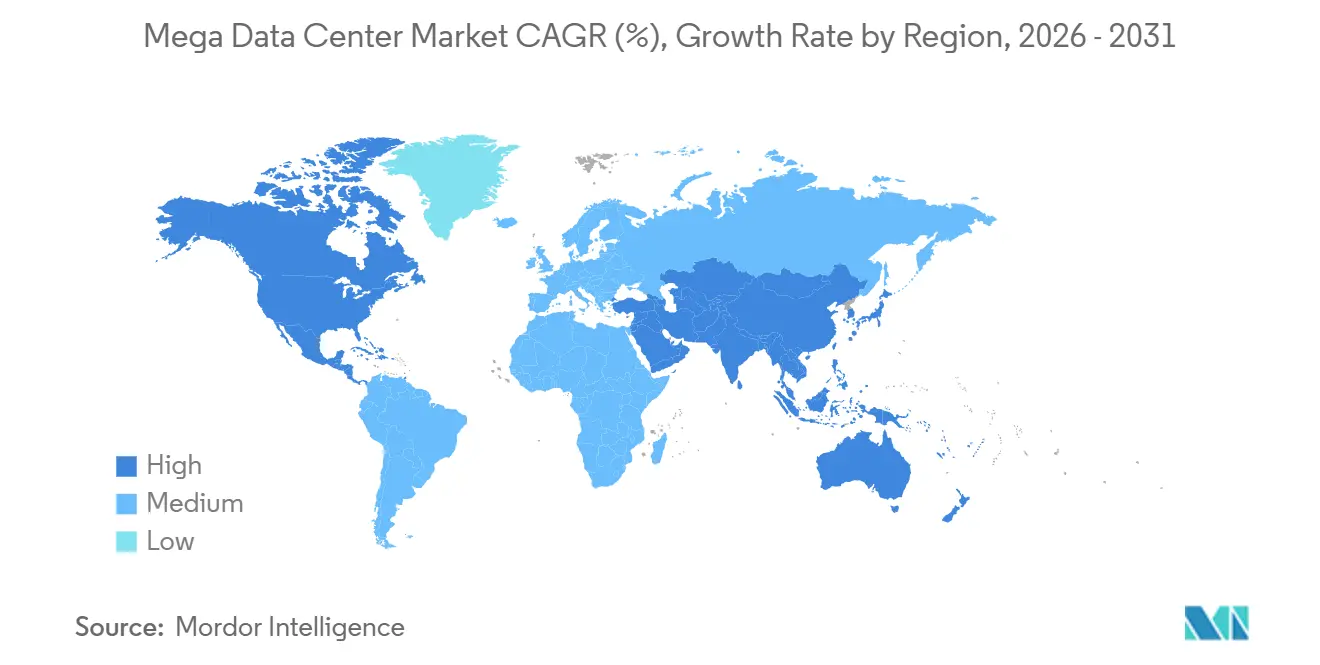

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

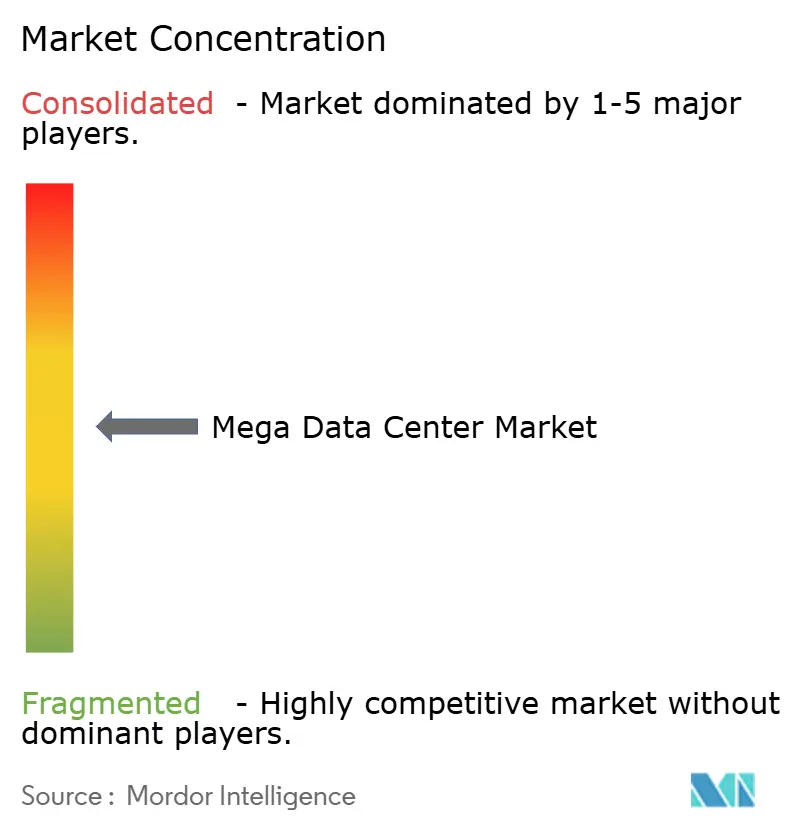

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mega Data Center Market Analysis by Mordor Intelligence

The mega data center market size reached USD 26.54 billion in 2026 and is projected to reach USD 33.65 billion by 2031, reflecting a 4.86% CAGR during the forecast period. This solid trajectory hides an underlying shift toward fewer, larger campuses that aggregate ever-denser AI clusters and demand unprecedented electrical and cooling capacity. Rising transformer lead times, grid congestion, and 30-month permitting cycles are compelling hyperscalers to front-load capital commitments and pre-purchase key components. Financial institutions accelerated workload migrations in 2025, favoring mega campuses that deliver certified zero-trust zones, while AI training operators paid a 60% premium for liquid-cooled racks to avoid thermal throttling. Suppliers of integrated power and cooling modules are consolidating, but tight manufacturing capacity for high-voltage equipment continues to constrain deployment schedules.

Key Report Takeaways

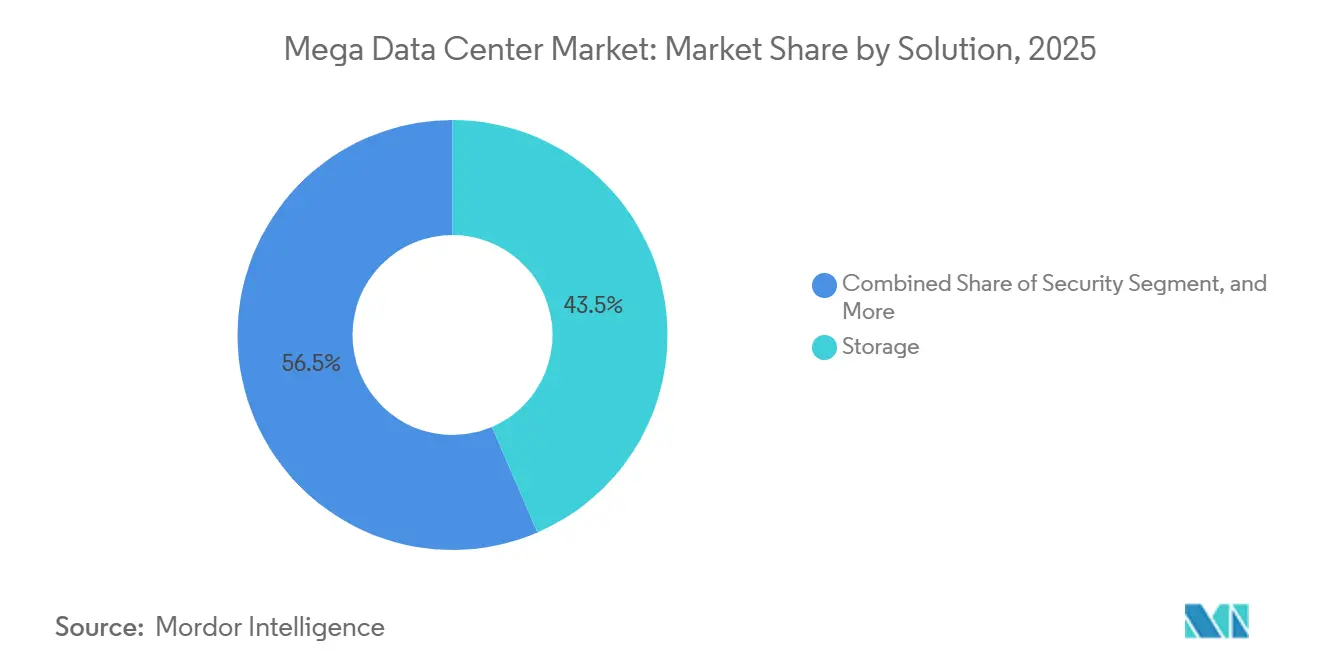

- By solution, storage held 43.54% of revenue in 2025, while security solutions are forecast to expand at a 5.67% CAGR through 2031.

- By data center type, hyperscale self-builds accounted for 61.65% of deployments in 2025, whereas hyperscale colocation is poised to grow at a 5.86% CAGR to 2031.

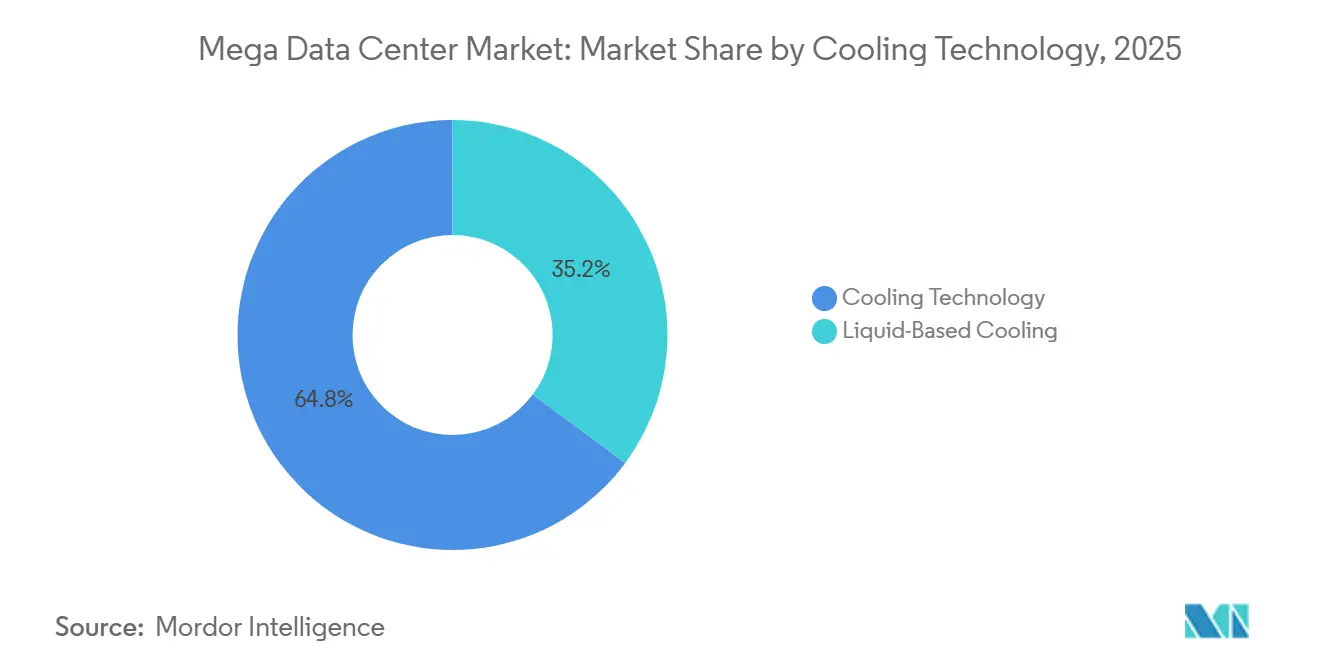

- By cooling technology, air-based systems retained a 64.84% share in 2025; liquid-based designs will advance at a 5.45% CAGR through 2031.

- By geography, North America commanded 39.74% revenue in 2025; Asia-Pacific is projected to record the fastest 6.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mega Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive AI and ML Compute Density Requirements | +1.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising BFSI Workload Placement in Mega Facilities | +0.9% | North America, Europe, Asia-Pacific financial hubs | Short term (≤ 2 years) |

| Accelerated Cloud-Service Capacity Buildouts | +0.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Energy-Efficient Liquid-Cooling Adoption Wave | +0.6% | North America, Europe, select Asia-Pacific metros | Medium term (2-4 years) |

| Increasing Demand for Data Center Consolidation | +0.5% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| On-Site Microgrid Generation to Bypass Grid Bottlenecks | +0.4% | North America, Middle East and select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive AI and ML Compute Density Requirements

Large-language-model training runs exceeded 20,000 GPUs per cluster in 2025, pushing individual rack loads to 120 kilowatts and driving operators toward rear-door heat exchangers and direct-to-chip cold plates.[1]Natalie Broughton, “GPU Heat Loads Force New Cooling Paradigms,” Reuters, reuters.com These liquid solutions went from niche status to 18% of new installs within a year, enabling single-site power contracts of over 200 megawatts. Shorter 24-month accelerator refresh cycles intensify capital turnover, so operators now optimize designs for three-year total cost of ownership. The result is a new equilibrium in which thermal design, electrical infrastructure, and upgrade cadence are co-engineered at the campus scale.

Rising BFSI Workload Placement in Mega Facilities

Updated cyber-resilience rules in the United States, European Union, and Singapore mandated hardware security modules at each transaction node and sub-second audit trails, making distributed architectures non-compliant for critical banking workloads. Consequently, leading financial groups moved 40% more core-banking processes into mega facilities in 2025, pursuing risk centralization and faster incident response. Regulators now hint that stress tests will examine underlying data-center resilience metrics, locking this migration pathway into strategic roadmaps.[2]Dan Reed, “EU Ecodesign Directive Alters Data Center Builds,” Financial Times, ft.com

Accelerated Cloud-Service Capacity Buildouts

AWS, Microsoft Azure, and Google Cloud collectively commissioned more than 5 gigawatts of new capacity in 2025, often pre-leasing entire campuses before final permits to outrun local opposition. Long-dated renewable power contracts and on-site generation are becoming standard hedges against grid volatility, while joint ventures with local telecom operators unlock land and spectrum advantages in India and Indonesia. Treating data-center inventory as a competitive moat, these firms accept near-term margin compression to secure scarce power entitlements.

Energy-Efficient Liquid-Cooling Adoption Wave

Rack densities above 50 kilowatts rendered chilled air largely obsolete for AI workloads, propelling a fleet-wide pivot toward immersion and direct-to-chip systems. Policy reinforced the shift, as the European Union’s 2025 Ecodesign update banned low-efficiency designs for builds above 20 megawatts. U.S. utilities introduced demand-response incentives that reward lower peak power draw, and ASHRAE updated thermal guidelines to normalize liquid-cooled environments. Supply-chain complexity increased, with coolant fluid and precision pump markets expanding 35% year-over-year.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Installation Costs | -1.0% | Global, especially in North America and Europe | Long term (≥ 4 years) |

| Escalating Utility Power Costs and Scarcity | -0.8% | Europe, North America, select Asia-Pacific | Medium term (2-4 years) |

| Community Backlash Over Water and Land Footprint | -0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| 30-Month Lead Times for HV Transformers and Switchgear | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Installation Costs

Typical mega campus budgets exceed USD 1 billion, with liquid cooling, redundant substations, and biometric security now mandatory line items.[3]Laura Schultz, “Inflation Pushes Mega Campus Budgets Past USD 1 Billion,” Reuters, reuters.com In Europe, tighter building codes and ESG certifications have added 15% to baseline costs since 2024, pushing many developers toward multi-phase campuses or sale-leaseback financing. Inflationary pressure on steel, semiconductors, and labor compounds risk, limiting participation to entities with deep capital market access.

Escalating Utility Power Costs and Scarcity

Wholesale electricity in Europe spiked more than 40% during renewable intermittency events in 2025, slashing project viability margins. In Northern Virginia and Texas, grid congestion forced several hyperscalers to delay energizing commissioned halls, prompting investments in on-site microgrids totaling USD 400 million per project. Energy procurement has become a board-level discipline, with operators hiring chief energy officers to secure long-dated hedges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Storage Anchors, Security Surges

Storage solutions accounted for 43.54% of 2025 revenue, yielding the single-largest market share for any solution type in the mega data center market. Object storage and NVMe-over-fabric architectures delivered 70% more IOPS than legacy SAN systems, enabling sub-millisecond access to petabyte-scale AI repositories. This performance uplift is critical for real-time inference, making storage a foundational pillar of the mega data center market. Security solutions are on track for the fastest 5.67% CAGR to 2031, propelled by zero-trust frameworks that bake hardware-rooted attestation into every server. Vendors now integrate intrusion detection and biometric access into unified platforms, reflecting a pivot from software-only models. Collaborative reference architectures between hyperscalers and storage leaders signal a procurement landscape that values pre-validated bundles, shortening deployment cycles and reducing engineering risk.

The performance edge of NVMe-over-fabric translates directly into operating income because higher throughput per watt reduces the cooling headroom required per transaction. On the security front, regulatory mandates such as NIST SP 800-207 and ISO 27001 certifications support premium pricing, cushioning margins against commoditization in server and networking segments. Hardware security modules embedded at board level eliminate latency overheads, appealing to BFSI and defense clients. Overall, solution providers that align with integrated storage-and-security demand are best positioned to capture incremental mega data center market revenue.

By Data Center Type: Self-Build Dominates, Colocation Accelerates

Self-build campuses accounted for 61.65% of total 2025 deployments, giving hyperscalers the lion’s share of the mega data center market at the facility level. These projects integrate bespoke liquid-cooling loops, on-site substations, and battery storage designed around proprietary AI workflows. The model suits operators able to absorb multi-billion-dollar commitments and manage construction risk. In parallel, hyperscale colocation is forecast to deliver a robust 5.86% CAGR through 2031. Colocation specialists have cut delivery timelines by 20% by using modular shells and prefabricated power trains, enabling cloud providers to secure capacity in congested metros without waiting 2 years for municipal permits.

A hybrid pattern is emerging in which hyperscalers lease entire buildings within a colocation campus, then retrofit custom power and networking, effectively blending the speed of colocation with the control of self-build. Compliance with ISO/IEC 22237 and Uptime Tier IV standards prominently features in RFP scoring, underscoring a mature buyer base that prioritizes resilience over cost. Joint ventures between smaller operators aggregate land and power entitlements, unlocking inventory in markets such as Singapore and Frankfurt that are restrictive. As the mega data center market evolves, the demarcation between self-build and colocation blurs into a continuum of risk-sharing models.

By Cooling Technology: Air Holds, Liquid Gains

Air-based cooling maintained a 64.84% revenue share in 2025, yet the threshold at which chilled air becomes thermally and economically untenable is fast approaching. Direct-to-chip liquid systems comfortably sustain racks at 150 kilowatts, enabling dense AI clusters while holding component temperatures within warranty envelopes. Immersion cooling offers even higher density, though the complexity of fluid management and server re-qualification slow adoption. Hybrid topologies that combine an air plenum for legacy gear and liquid loops for new AI trays create transition pathways. Across all variants, the mega data center market for liquid-cooled solutions is projected to expand at a 5.45% CAGR, far outpacing air-cooled solutions.

Regulatory forces drive the pivot. The European Union’s Ecodesign Directive and Uptime Tier standards penalize inefficient air systems for builds above 20 megawatts, while U.S. utilities grant demand-response credits that reward liquid-cooled peak-load profiles. Waste-heat recovery, mandated in parts of Scandinavia and Germany, strengthens the case that operators can earn revenue offsets by supplying captured heat to district networks. Collectively, these trends place liquid cooling at the center of next-generation facility blueprints, shaping equipment vendor roadmaps and influencing site selection.

Geography Analysis

North America accounted for 39.74% of 2025 revenue, securing the largest share of the mega data center market amid sustained hyperscaler capital outlays and a mature supply ecosystem. Northern Virginia remains the world’s densest cluster of compute, but emerging build zones in Texas, Oregon, and Arizona diversify risk and tap renewable portfolios. Canada and Mexico are benefiting from spillover demand and government incentives, while U.S. regulatory bodies maintain a favorable permitting environment. Grid congestion and community pushback over water use add friction, prompting operators to adopt closed-loop cooling and on-site generation.

Asia-Pacific is forecast to expand at a 6.02% CAGR through 2031, making it the fastest contributor to the incremental mega data center market. China’s national cloud program and India’s digital-public-infrastructure initiative anchor large deployments that localize AI workloads in line with data-sovereignty laws. Japan and South Korea invest in AI-focused campuses, while Australia positions itself as a disaster recovery hub for the region. Limited land and power in Singapore and Mumbai push developers toward tier-two cities and modular campuses designed for phased expansion.

Europe’s trajectory is moderated by electricity costs that averaged EUR 0.15 per kilowatt-hour (USD 0.17 per kilowatt-hour) in 2025. New capacity gravitates to Scandinavia and Ireland, where renewable penetration lowers marginal costs and cooler climates extend free-air-cooling windows. Germany, France, and the United Kingdom continue to attract steady investment, though local opposition extends permitting timelines. The European Union’s regulatory environment is the strictest globally, mandating waste-heat reuse and water-neutral designs, thereby influencing global best practices.

Regulatory Landscape

Regulatory requirements are tightening around sustainability disclosure, siting approvals, and resilience for large-scale data centers, which is pushing operators to standardize reporting and design choices across regions. In the European Union, Commission Delegated Regulation (EU) 2024/1364 operationalized a multi-phase sustainability rating and reporting framework, requiring operators with at least 500 kW IT power demand to communicate key performance indicators to an EU database on an annual basis, with early milestones starting in September 2024 and May 2025.

In the United States, policy signals reflect both acceleration and constraint. A July 2025 White House executive action targeted faster federal permitting for data center infrastructure, while 2026 introduced more transparency and local-control measures. At the federal level, the Data Center Water and Energy Transparency Act of 2026 (S. 4213, introduced March 2026) and H.R. 9372 (directing NIST to develop best practices for measuring data center energy and water use, including AI workloads) point to increasing scrutiny of energy and water intensity at scale. At the state level, New York issued Executive Order No. 62 in July 2026, establishing a temporary moratorium on data center development while the state develops higher development standards and a benefits blueprint, reinforcing how sub-national rules shape project sequencing and site selection.

Competitive Landscape

Competitive intensity is escalating as colocation giants Digital Realty and Equinix go head-to-head with hyperscaler self-builds, while GPU-focused challengers such as CoreWeave raise multi-billion-dollar war chests. Integrated cooling and power modules from Schneider Electric and Vertiv shorten construction cycles, giving early adopters a time-to-market edge. Patent filings on liquid cooling, power distribution, and AI-driven facility management increased sharply in 2025, reflecting a technology race to optimize for 200-megawatt campuses. Mergers, acquisitions, and joint ventures reconfigure market positions. Digital Realty’s expansion of its European portfolio and Equinix-led sovereign wealth partnerships epitomize the scramble for strategic land and power.

Vertical integration deepens, with hyperscalers signing 15-year renewable power purchase agreements and deploying on-site microgrids to mitigate grid volatility. Equipment vendors climb the value chain, bundling monitoring software with hardware to capture recurring revenue. Disruptors adopt specialized GPU clouds to bypass commodity compute and carve out high-margin niches. Regional diversification becomes a hedging strategy as operators strive to balance mature-market saturation with emerging-market growth potential.

Rising stakeholder scrutiny over environmental impact is pushing operators to embed sustainability metrics in competitive positioning. Closed-loop liquid cooling, district-heat reuse, and on-site renewable microgrids are no longer optional differentiators but baseline expectations for hyperscale RFPs. Vendors that can certify lower embodied carbon in switchgear, transformers, and prefabricated modules win procurement points, while facilities that negotiate water-offset agreements gain fast-track community approvals. As a result, sustainability officers now sit alongside chief technology and energy officers in deal negotiations, shaping everything from site selection to equipment bill-of-materials and redefining the parameters of competitive advantage.

Mega Data Center Industry Leaders

Cisco Systems Inc.

Intel Corporation

Dell Technologies Inc.

Fujitsu Ltd.

Hewlett-Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most compelling whitespace centers on power procurement, site approvals, and the integration of high-density AI infrastructure. Mega campuses are increasingly seeking turnkey pathways that bundle grid interface, on-site generation, and advanced cooling into repeatable designs. Build intensity supports this direction: U.S. data center construction spending reached USD 7.9 billion in May 2026 and USD 58.1 billion year-to-date, while the scale of AI build programs is shifting procurement from component-by-component purchases toward integrated power-and-cooling modules, microgrids, and standardized liquid-cooling architectures that reduce commissioning risk amid long transformer and switchgear lead times.

In Europe, the opportunity set is being shaped by policy-enabled capacity expansion alongside tighter energy obligations. The European Commission tabled the Cloud and AI Development Act in June 2026, setting out a program to expand EU data center capacity with measures such as acceleration zones and strategic projects. Industry coordination is also taking shape, with fourteen European industry associations signing a Declaration of Intent on June 3, 2026, to cooperate on an EU model for tripartite agreements among data center operators, energy stakeholders, and public authorities. Together, these dynamics increase demand for solutions that document energy and water performance, operationalize demand-side flexibility, and support waste-heat and efficiency requirements, particularly for campuses that often exceed 200 MW power contracts and increasingly rely on liquid-based cooling for rack densities beyond air-cooling limits.

Recent Industry Developments

- July 2026: Intel announced a EUR 5 billion capital investment at its Leixlip campus in Ireland to upgrade manufacturing capabilities for next-generation Xeon chips. Improving regional supply for server CPUs supports mega data center build schedules by reducing dependence on constrained supply chains. It also aligns with EU efforts to deepen strategic technology capacity.

- June 2026: Dell Technologies expanded its AI-optimized infrastructure portfolio under the Dell AI Factory with NVIDIA, including new PowerEdge platforms designed for very high GPU density at the rack level. Higher density server configurations increase demand for liquid-based cooling and integrated power distribution in mega campuses. This reinforces the shift toward fewer, larger sites built around AI clusters.

- December 2025: AWS commissioned a 500 MW campus in Virginia with on-site microgrid generation and water recycling. The project highlighted how mega data center developers are combining very large power blocks with resilience and sustainability features. It also reflects efforts to navigate grid congestion, community scrutiny, and tighter environmental expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is the spending tied to building and upgrading mega data centers, including core IT and facility systems used in very large sites that support hyperscale and high density workloads.

Scope exclusions: We exclude day to day colocation service revenue, telecom network services, and software-only subscriptions that are not part of the physical data center build or refresh cycle.

Segmentation Overview

- By Solution

- Storage

- Networking

- Server

- Security

- Other Solutions

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Cooling Technology

- Air-Based Cooling

- Liquid-Based Cooling

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public capacity and demand signals that can be tracked over time, which then guided what to test in interviews. We used sources such as the International Energy Agency for electricity demand context, the US Energy Information Administration for power price and generation mix, and ITU releases for traffic growth direction. For data center footprint indicators, we referred to public statistics and publications from the US Census Bureau, Eurostat, and national energy regulators where available.

To translate these signals into market inputs, we also reviewed company annual reports, investor presentations, sustainability reports, and reputable press coverage on new campus builds and expansion timelines. In parallel, we used paid subscriptions for company financials and intelligence, and for patent databases to understand where cooling and power innovations are moving. These named sources are illustrative only, and many other public documents were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what counts as a mega site in practice, how budgets are split across IT and facility layers, and what drives refresh timing once a campus is live. We spoke with a mix of operators, design and engineering advisors, component suppliers, and channel specialists across major build regions so assumptions on capacity additions, pricing, and deployment pace could be corrected when desk signals were less direct.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | APAC: 41% |

| Mid tier: 42% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 22% | Managers: 47% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the demand pool is reconstructed from large-campus capacity additions and upgrade cycles, and then mapped to spend per site across IT and facility systems. The totals were then checked with selective bottom-up approximations, including a sampled bill of materials logic for a typical mega build (server, storage, networking, security, and cooling), plus sense checks against supplier revenue exposure and channel feedback.

Inputs that matter in this market include announced and under-construction campus counts, estimated IT load and power density ranges, cooling mix shifts (air versus liquid), lead times for electrical and mechanical equipment, and indicative pricing movements for key hardware categories. For forecasting, scenario analysis was used, since build-outs move in waves and can shift with power availability, permitting timelines, and changes in hyperscale capex plans. Where a bottom-up check left gaps, we bridged them using conservative proxy ratios from comparable builds, then re-tested those ratios with interview feedback before finalizing the model.

Data Validation & Update Cycle

Outputs were validated by comparing implied spend per MW and per site against independent signals, and then rechecking any outliers that did not align with known build economics. A second analyst review was completed for key assumptions, and follow-up calls were triggered when a region showed a step change that could not be explained by capacity additions or price movement.

The report is refreshed annually, with interim updates when there are material events such as large campus announcements, policy changes affecting power access, or notable shifts in cooling or density adoption. Before delivery, a final pass is completed so the latest public updates and interview confirmations are reflected in the published view.

Mordor Intelligence's Mega Data Center Market Size Versus Other Published Estimates

Published numbers for the mega data center market often do not match because the term mega is not treated the same way, and because some studies mix build spend with service revenue. Differences also show up when one estimate uses IT load thresholds and another uses server-count rules, which changes what gets counted.

The main gap comes from whether colocation operating revenue and managed services are added on top of build and refresh spending, and then how the mega threshold is applied across regions. By using a consistent definition anchored to mega facilities (for example, 15,000+ servers) and counting only infrastructure spend, Mordor Intelligence keeps the totals tied to measurable build indicators like site additions, power and cooling configuration, and replacement cycles rather than broader data center revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 26.54 B (2026) | |

| Industry Publisher A | USD 26.50 B (2025) | Uses a different base year and often blends solution, support infrastructure, and service layers, which can shift totals when service revenue is counted alongside physical build spend. |

| Industry Publisher B | USD 26.92 B (2025) | Defines mega sites using a power-based threshold (for example, above a MW level) and may apply different regional inclusion rules, which changes which campuses qualify and how fast the counted pipeline expands. |

Overall, the spread in values is mainly explained by year alignment and what is included beyond the physical infrastructure stack. When scope is kept to infrastructure spend and checked against campus build signals and upgrade cycles, the result is easier to trace, reproduce, and update as new capacity announcements come in.

Key Questions Answered in the Report

How large is the current mega data center segment in monetary terms?

The segment reached USD 26.54 billion in 2026 and is projected to grow to USD 33.65 billion by 2031.

What is driving most new capacity additions after 2026?

Hyperscalers are consolidating AI clusters into fewer, larger campuses and pre-purchasing transformers and switchgear to overcome 30-month lead times.

Why are financial institutions moving workloads into mega facilities?

Updated cyber-resilience rules now require hardware security modules and sub-second audit trails that are easier to implement inside certified zero-trust zones.

Which geographic region is poised for the fastest expansion up to 2031?

Asia-Pacific is forecast to post a 6.02% CAGR, led by China’s sovereign cloud policy and India’s digital-public-infrastructure rollout.

How are operators addressing grid congestion and power scarcity?

Many are investing in on-site microgrids, signing 15-year renewable power contracts, and adopting liquid cooling to lower peak electricity demand.

What cooling technology is emerging as the standard for AI workloads?

Direct-to-chip and immersion liquid systems are gaining mainstream status, supporting rack densities above 150 kilowatts while keeping components within warranty limits.

Page last updated on: