UK Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

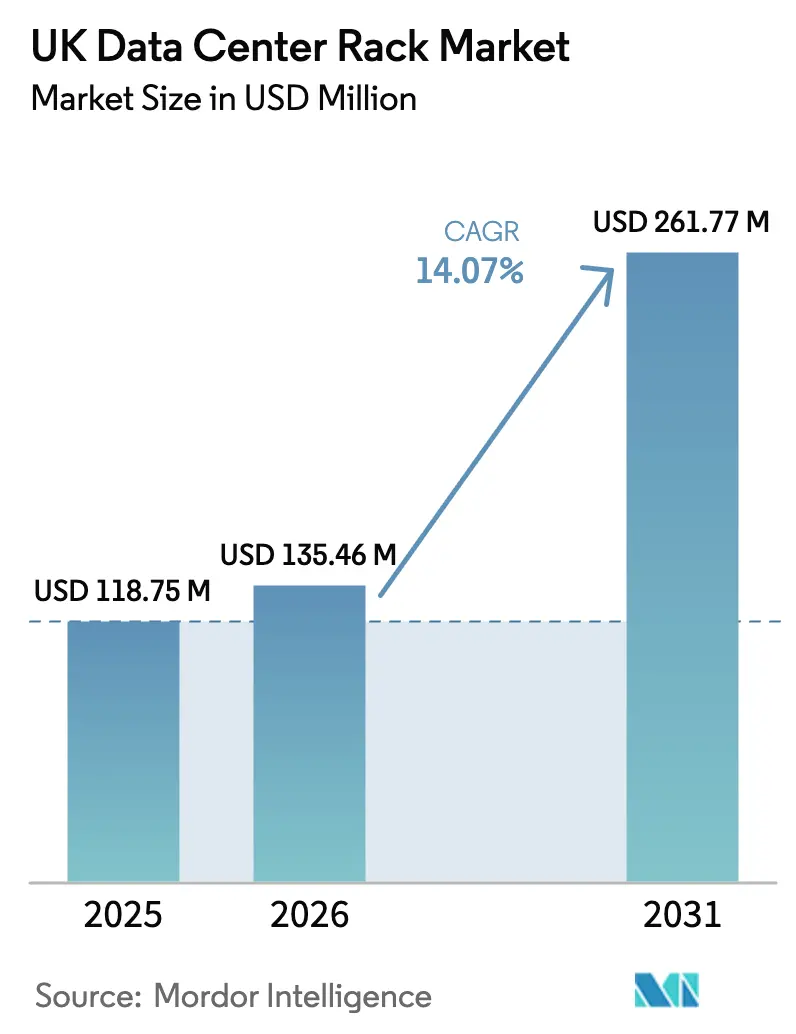

| Base Year Market Size (2025) | USD 118.75 Million |

| Market Size (2026) | USD 135.46 Million |

| Market Size (2031) | USD 261.77 Million |

| Growth Rate (2026 - 2031) | 14.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Data Center Rack Market Analysis by Mordor Intelligence

The United Kingdom data center rack market size is expected to grow from USD 118.75 million in 2025 to USD 135.46 million in 2026 and is forecast to reach USD 261.77 million by 2031 at 14.07% CAGR over 2026-2031. Current growth rests on the nation’s AI Opportunities Action Plan, which is unlocking private capital for digital infrastructure while fast-tracking planning approvals. Designation of data centers as Critical National Infrastructure in 2024 tightened cyber-security standards, lifting demand for cabinet-class enclosures that meet stricter physical-security rules. Sovereign-cloud deployments, accelerated by the Competition and Markets Authority’s probe into hyperscale concentration, are steering many enterprises toward domestically run facilities that favor the United Kingdom data center rack market. Meanwhile, AI workloads are driving a shift from 42U to 48U heights, with liquid-cool-ready frames gaining traction as rack power densities surpass 70 kW. Supply-chain pressure from power-grid connection queues is pushing operators into secondary metros and stimulating interest in on-site generation, modular designs, and material innovations such as aluminum alloys.

Key Report Takeaways

- By rack type, cabinet racks captured 64.02% of the United Kingdom data center rack market share in 2025; open-frame racks are projected to grow at 16.05% CAGR through 2031.

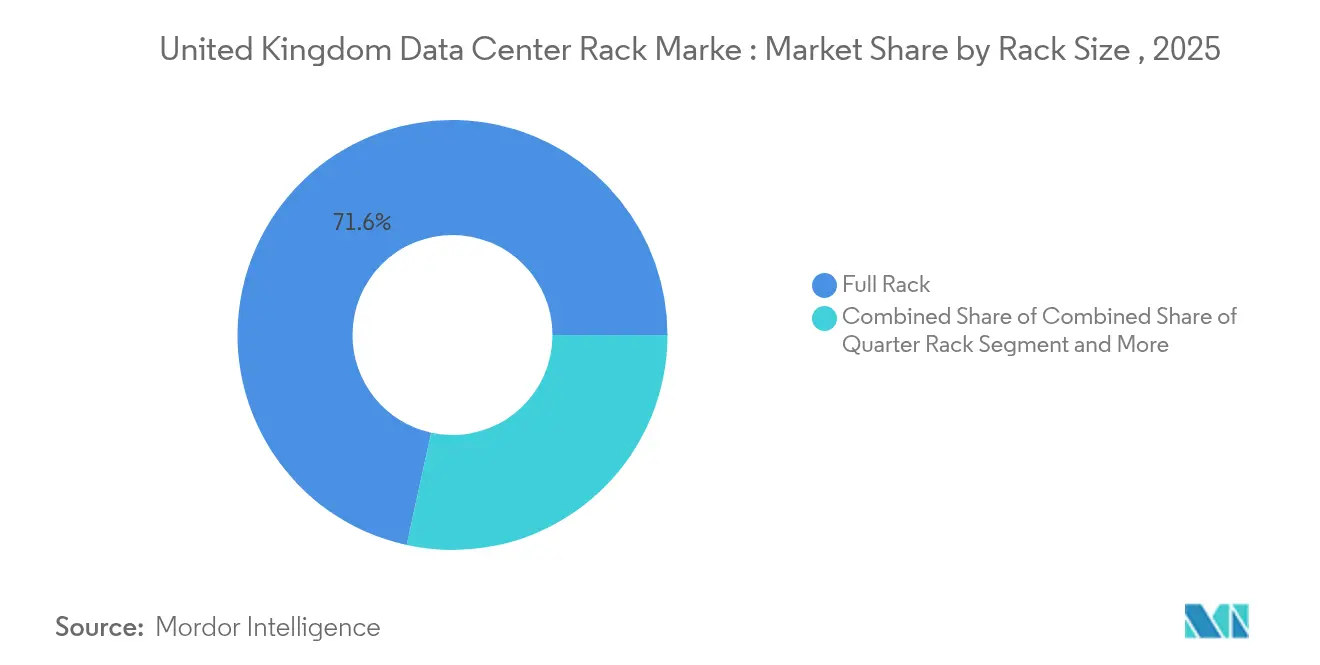

- By rack size, full racks led with 71.58% share of the United Kingdom data center rack market size in 2025, while quarter racks are forecast to advance at 16.12% CAGR to 2031.

- By rack height, 42U configurations accounted for 55.82% share of the United Kingdom data center rack market size in 2025; 48U racks exhibit the highest projected CAGR at 14.92% between 2026-2031.

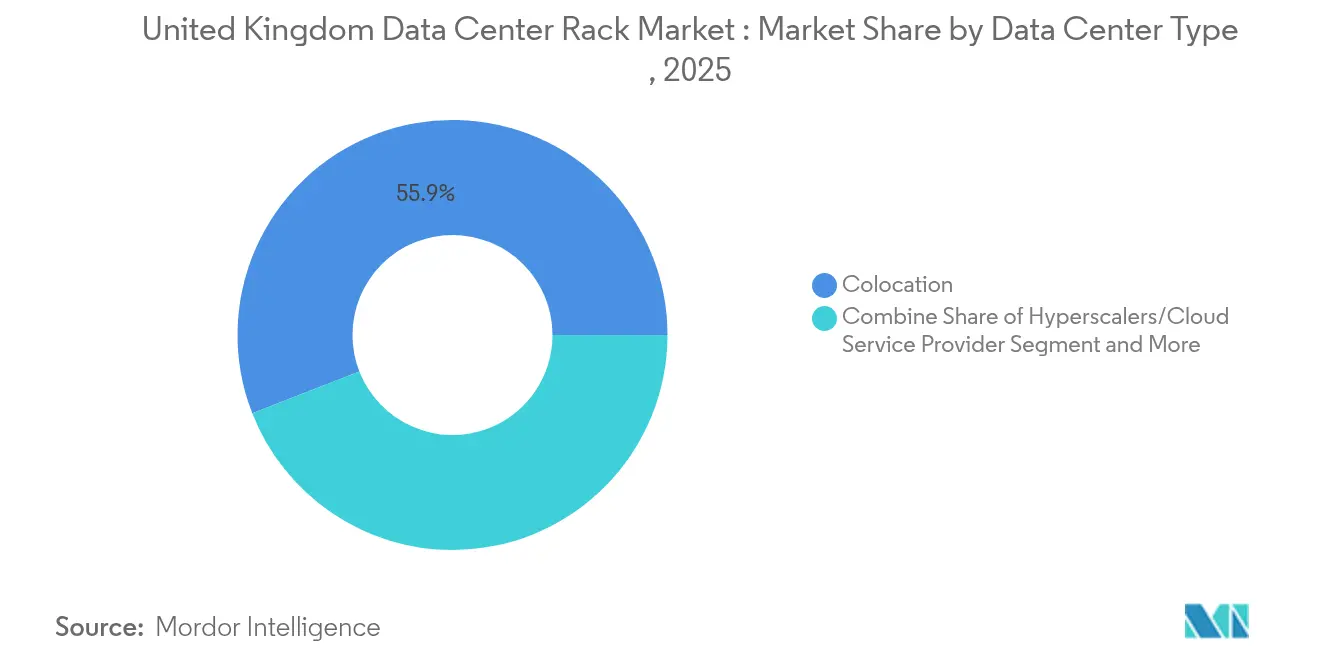

- By data-center type, colocation held 55.93% share of the United Kingdom data center rack market in 2025; hyperscale deployments are expanding at 16.98% CAGR to 2031.

- By material, steel dominated with 81.78% United Kingdom data center rack market share in 2025; aluminum racks are rising at 16.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The contribution of United kingdom may read different when placed against the full pool of global outputs. The worldwide data center rack market shares by Mordor Intelligence reflect that proportional balance.

UK Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of sovereign and hybrid cloud zones | +3.2% | National, with concentration in London, Manchester, Edinburgh | Medium term (2-4 years) |

| AI/ML rack-density upgrades across hyperscale and colocation | +4.1% | Global, with UK leading in financial services AI adoption | Short term (≤ 2 years) |

| Accelerated 5G edge build-outs needing micro-racks | +1.8% | Urban centers: London, Birmingham, Manchester, Glasgow | Medium term (2-4 years) |

| Government carbon-neutral mandates driving liquid-cool ready racks | +2.3% | National, with early adoption in Scotland and Wales | Long term (≥ 4 years) |

| Surge in fintech and Open-Banking transactions | +1.9% | London financial district, with spillover to Edinburgh | Short term (≤ 2 years) |

| Modular data-hall retrofits in listed U.K. real-estate trusts | +1.0% | Greater London, Manchester, Birmingham metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Sovereign and Hybrid Cloud Zones

The sovereign-cloud agenda is redrawing rack-deployment patterns as enterprises seek local data-residency compliance. AI Growth Zones streamline approvals, enabling faster cabinet installations with enhanced locking mechanisms that meet financial-sector audit trails. Hybrid architectures also mitigate vendor lock-in risk highlighted by the ongoing cloud-market investigation, spurring demand for racks with integrated cabling and power-distribution units that support multi-cloud switching.[1]Competition and Markets Authority, “CMA launches market investigation into cloud services,” gov.uk Financial institutions further accelerate deployments by specifying British-hosted racks that satisfy open-banking regulations.

AI/ML Rack-Density Upgrades Across Hyperscale and Colocation

AI training clusters are pushing per-rack loads above 90 kW, forcing operators to adopt 48U and custom heights to accommodate immersion trays, rear-door heat exchangers, and high-capacity busbars. Partnerships such as Telehouse’s liquid-cooling laboratory illustrate the convergence of rack, cooling, and monitoring domains, opening opportunities for suppliers able to offer pre-engineered, liquid-ready cabinets. [2]Telehouse, “Telehouse launches London liquid-cooling lab,” telehouse.net Hyperscalers standardize on taller frames to optimize compute-per-square-meter, strengthening volume demand for the United Kingdom data center rack market.

Accelerated 5G Edge Build-Outs Needing Micro-Racks

Nationwide 5G rollout requires edge nodes in shopping centers, stadiums, and roadside cabinets. Operators specify quarter and half-racks with ruggedized casings, vibration dampers, and remote-access sensors so they can manage unmanned sites. Wall-mount formats gain popularity because they fit retail backrooms and cell-tower shelters without structural reinforcements, broadening the customer base for specialized rack vendors.

Government Carbon-Neutral Mandates Driving Liquid-Cool Ready Racks

Net-zero rules and the Energy Efficiency Directive obligate data-center operators to capture waste heat and curtail water usage. Rack manufacturers respond with aluminum skeletons that integrate cold-plate manifolds and quick-disconnect piping, cutting installation labor and leak risk. Recent factory investments in Scarborough will shorten domestic supply chains and reduce embedded-carbon footprints for United Kingdom data center rack market buyers. [3]Schneider Electric, “Schneider Electric invests GBP 42 million in Scarborough facility,” se.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid connection queues (≥24-month delays) | -2.8% | London, Birmingham, Manchester metropolitan areas | Short term (≤ 2 years) |

| Tight labour pool for Tier 3/Tier 4 installers | -1.5% | National, with acute shortages in Scotland and Northern England | Medium term (2-4 years) |

| In-rack thermal hotspots above 70 kW challenging legacy sites | -1.2% | London financial district, established colocation facilities | Short term (≤ 2 years) |

| Rising insurance premiums on high-density halls | -0.8% | Greater London, with spillover to major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power-Grid Connection Queues (≥ 24-Month Delays)

Backlogs totaling 400 GW in the London region force developers to wait two years or more for grid hookups. Many operators redirect capital to Manchester or Cardiff, while others install on-site gas turbines, battery storage, or explore small modular reactors. The AI Energy Council’s formation underscores official urgency; however, long approval cycles still curb near-term rack deployments.

Tight Labour Pool for Tier 3/Tier 4 Installers

Liquid-cool technology demands plumbers, controls technicians, and commissioning engineers schooled in both IT and HVAC disciplines. Post-Brexit immigration constraints have narrowed the talent funnel, lengthening build schedules and inflating wages. Suppliers now ship pre-assembled busways and coolant loops to cut field labor, yet complex retrofits in legacy halls remain schedule-risk factors for United Kingdom data center rack market projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Racks Dominate Enterprise Deployments

Full racks held 71.58% of the United Kingdom data center rack market share in 2025, reflecting the preference for standardized 600 mm × 1,200 mm footprints that streamline airflow and cable management. The segment is projected to expand at 15.86% CAGR as hyperscalers and colocation landlords chase economies of scale. Quarter racks will persist in edge pods, but volume remains modest in the overall United Kingdom data center rack market.

Rising AI compute clusters further cement full-rack popularity because clustered GPU trays consume contiguous vertical and horizontal space, making partial frames inefficient for power and cooling loops. Therefore, suppliers concentrate R&D on strengthening frame rigidity, vibration isolation, and built-in coolant manifolds that serve rack-wide cold-plate grids—features easier to integrate when designing full-height enclosures.

By Rack Height: 42U Standard Faces AI-Driven Evolution

The 42U format still accounts for 55.82% of the United Kingdom data center rack market size, but its dominance is eroding as 48U systems grow 14.92% per year. Taller frames provide an extra 6U that operators allocate to in-rack UPS drawers, top-of-rack switches, or manifold headers for liquid loops. Taller enclosures also raise center-of-gravity considerations, prompting vendors to switch from mild steel to lighter aluminum frames that meet seismic standards without adding floor anchoring.

GPU clusters like NVIDIA DGX SuperPOD occupy multiple rack units per server sled, accelerating the shift to 48U and custom 52U configurations so operators can maximize nodes per kilowatt. Legacy 42U sites in London’s Docklands are therefore retrofitting with rear-door heat exchangers to squeeze incremental capacity until grid upgrades arrive

By Rack Type: Cabinet Security Drives Colocation Preference

Cabinet racks captured 64.02% of the United Kingdom data center rack market share, propelled by financial-services compliance requirements that demand lockable doors, CCTV integration, and differential-pressure containment. Growth remains strongest in cabinet designs because colocation providers rely on them to separate multi-tenant environments, and hyperscalers now adopt sealed racks for internal micro-segmentation of customer clusters.

Open-frame racks survive where cost minimization overrides security, chiefly in dedicated hyperscale halls. Still, even here, operators are adding side-panel kits and RFID-controlled doors, steadily nudging open-frame users toward hybrid or fully enclosed formats. Wall-mount cabinets gain share in roadside and retail deployments that anchor 5G edge applications.

By Data Center Type: Colocation Leads Multi-Tenant Growth

Colocation sites accounted for 55.93% of the United Kingdom data center rack market in 2025, thanks to enterprise outsourcing of non-core infrastructure. Hyperscale cloud operators, expanding at 16.98% CAGR, are building multi-building campuses in Northumberland and Greater Manchester, boosting large-volume rack orders that feature standardized busbar trunking, closed-loop coolant rails, and AI-optimized airflow.

Enterprise self-build facilities shrink as CIOs migrate workloads to OPEX-driven contracts. Edge data centers, though small per site, are proliferating in count, creating a tailwind for micro-rack suppliers that can pre-assemble units in local factories and ship to distributed cell-tower shelters.

By Material: Steel Dominance Faces Aluminum Challenge

Steel remains the default, anchoring 81.78% of the United Kingdom data center rack market size, yet aluminum racks rise 16.92% annually. Weight savings facilitate multi-story builds where floor loading is critical, and aluminum’s superior thermal conductivity improves liquid-cool efficiency. Operators embracing net-zero targets value aluminum’s recyclability, prompting some to stipulate minimum recycled content in procurement tenders.

Composite and copper-lined frames cater to electromagnetic shielding requirements inside classified government pods. Although niche today, these premium racks could expand if post-quantum encryption drives demand for secure enclaves that resist side-channel attacks.

Geography Analysis

Greater London retains the largest share of the United Kingdom data center rack market, fueled by proximity to financial hubs and undersea cables. However, 24-month grid queues and soaring land costs shift fresh investment toward Manchester, Birmingham, and Edinburgh. Scotland’s renewable energy surplus and cooler climate attract hyperscale projects aiming to lower Power Usage Effectiveness, while Wales offers inexpensive sites near the Western Power grid spine.

Northern England is ascending quickly: QTS’s proposal in Northumberland and Kao Data’s Stockport campus illustrate how brownfield industrial land, previously overlooked, is being repurposed for data-center campuses. These locations supply ample power headroom and enjoy improved fiber backhaul via recent rail-corridor conduit projects. As a result, the United Kingdom data center rack market size in northern regions is forecast to grow faster than the national average through 2031.

Edge computing reshapes geographic strategy by dispersing micro-data centers along 5G corridors. Latos Data Centres’ plan for 40 sites underscores the pivot toward regional hubs where latency-sensitive workloads require racks closer to users. Public-sector incentives under the “leveling-up” agenda should further diversify deployment, allowing the United Kingdom data center rack market to avoid over-reliance on the congested South-East.

The data center rack market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, South America, and North America. This is complemented by country-specific insights for Belgium, Ireland, Chile, Canada, Japan, and Mexico, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition remains moderate, with Schneider Electric, Vertiv, and Eaton facing specialized challengers in liquid-cool integration and edge form factors. Market consolidation accelerated in 2024, tallying 13 strategic transactions as players pursued integrated value chains. Schneider Electric’s USD 850 million Motivair acquisition shores up direct-to-chip cooling know-how, letting it bundle racks, busways, and coolant distribution as a single SKU.

Vertiv partners with immersion-tank makers to deliver hybrid solutions that retrofit legacy halls, while Eaton packages racks with lithium-ion UPS skids to shorten build cycles for colocation operators. Regional specialists such as Cannon Technologies differentiate on rapid lead times and bespoke cable-management accessories favored by telecom edge deployments. New entrants leverage aluminum fabrication and sustainable sourcing to win bids tied to ESG scoring, carving out niches inside the broader United Kingdom data center rack market.

Technology alliances increasingly decide market share: Telehouse coordinates a vendor ecosystem spanning pump-skids, coolant, and sensors to guarantee 90 kW-plus per rack. Similar ecosystems emerge at new Scottish campuses, indicating that rack suppliers able to certify end-to-end performance with cooling and power partners will capture premium segments.

UK Data Center Rack Industry Leaders

Eaton Corporation

Rittal GmbH & Co. KG

Schneider Electric SE

Hewlett Packard Enterprise Co.

Vertiv Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DataVolt and Supermicro teamed up to fast-track rack-scale liquid-cooling for AI clusters, targeting 100 kW-plus cabinets.

- April 2025: Schneider Electric reported 21% organic growth in its data-center division after integrating Motivair’s cold-plate product line.

- April 2025: Colt Technology Services divested its European data-center portfolio to NorthC to prioritize connectivity services.

- March 2025: Pulsant acquired SCC’s Birmingham and Fareham facilities, expanding its estate to 12 UK sites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom data center rack market as the annual sales revenue generated within the country from new, factory-built racks and cabinets that physically house IT, networking, and storage equipment inside purpose-built or retrofitted data centers. Solutions tailored for outdoor telecom shelters, desktop enclosures, or non-IT industrial cabinets fall outside this scope.

Scope exclusion: Telecom street-side or on-board equipment enclosures are not counted.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next interview UK-based colocation facility managers, hyperscale procurement leads, rack integrators, and edge-computing solution architects across London, Slough, Manchester, and Scotland. These conversations verify in-rack power densities, refresh cycles, and average selling price shifts, and they fill data gaps on liquid-cool-ready models that are not yet reported publicly.

Desk Research

We begin with an extensive scan of freely available tier-1 sources such as the Office for National Statistics power-use data, the Uptime Institute capacity tracker, the Digital Infrastructure Association build pipeline reports, HMRC customs codes for steel rack imports, and peer-reviewed thermal-management journals. Company filings and reputable press add recent contract values, while paid repositories like D&B Hoovers and Dow Jones Factiva sharpen revenue splits. Together, these references set boundary conditions for shipment volumes, prevailing rack heights, and typical selling prices. The sources cited above illustrate our approach and are not an exhaustive list of material consulted.

Market-Sizing & Forecasting

We employ a top-down reconstruction that starts with installed and planned data-center floor area, converts that metric into addressable rack slots through prevailing rack footprint ratios, and then multiplies by verified replacement rates. Select bottom-up checks, supplier roll-ups, and sampled ASP x volume calibrate the totals before finalizing. Key variables in the model include (1) average rack density in kW, (2) hyperscale capex announcements, (3) quarterly steel price movements, (4) new Tier III and IV build counts, and (5) edge facility counts under ten racks. An ARIMA forecast, tuned with scenario inputs from primary experts, projects each driver, after which currency normalization and vacancy adjustments close residual gaps.

Data Validation & Update Cycle

Outputs undergo multi-layer review. Analysts triangulate against independent colocation revenue dashboards, flag anomalies that breach +/-7 percent variance, and rerun interviews if needed. Every study is fully refreshed once a year, with interim mini-updates triggered by material events such as multi-megawatt hyperscale deals.

Why Mordor's UK Data Center Rack Baseline Commands Reliability

Published estimates often diverge because firms adopt different rack definitions, convert currencies at varied points, or freeze models for long spells before release.

Key gap drivers include scope choices that mix telco street cabinets with true data-center racks, reliance on global average selling prices instead of UK-specific figures, and the use of once-per-three-year refresh cadences that miss London's fast-moving build queue. Our disciplined annual cycle and dual-layer variable set mitigate those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 118.8 M (2025) | Mordor Intelligence | - |

| USD 239.2 M (2023) | Regional Consultancy A | Includes power-distribution units and refurb racks; older base year |

| USD 210 M (2024) | Global Consultancy B | Uses global ASP averages and a static 42U height assumption |

| USD 209 M (2024) | Industry Journal C | Projects straight-line growth without primary validation or currency realignment |

Taken together, the comparison shows that Mordor's numbers sit between aggressive and conservative peers, anchored by clear scope boundaries, UK-specific price checks, and a refresh cadence that keeps pace with the market's rapid expansion.

Key Questions Answered in the Report

What factors are driving growth in the United Kingdom data center rack market?

Robust AI investments, sovereign-cloud mandates, and 5G edge deployments combine to lift rack density needs and spur demand for liquid-cool-ready enclosures.

How large is the United Kingdom data center rack market today?

The market generated USD 135.46 million in 2026 and is forecast to reach USD 261.77 million by 2031.

Which rack type leads the market?

Cabinet racks dominate with 64.02% share in 2025 due to stringent physical-security requirements in colocation facilities.

Why are 48U racks gaining popularity?

They provide extra vertical space for AI servers and cooling hardware, enabling power densities above 70 kW per rack and supporting taller liquid-cool manifolds.

Page last updated on: