Livestock Cake And Meal Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

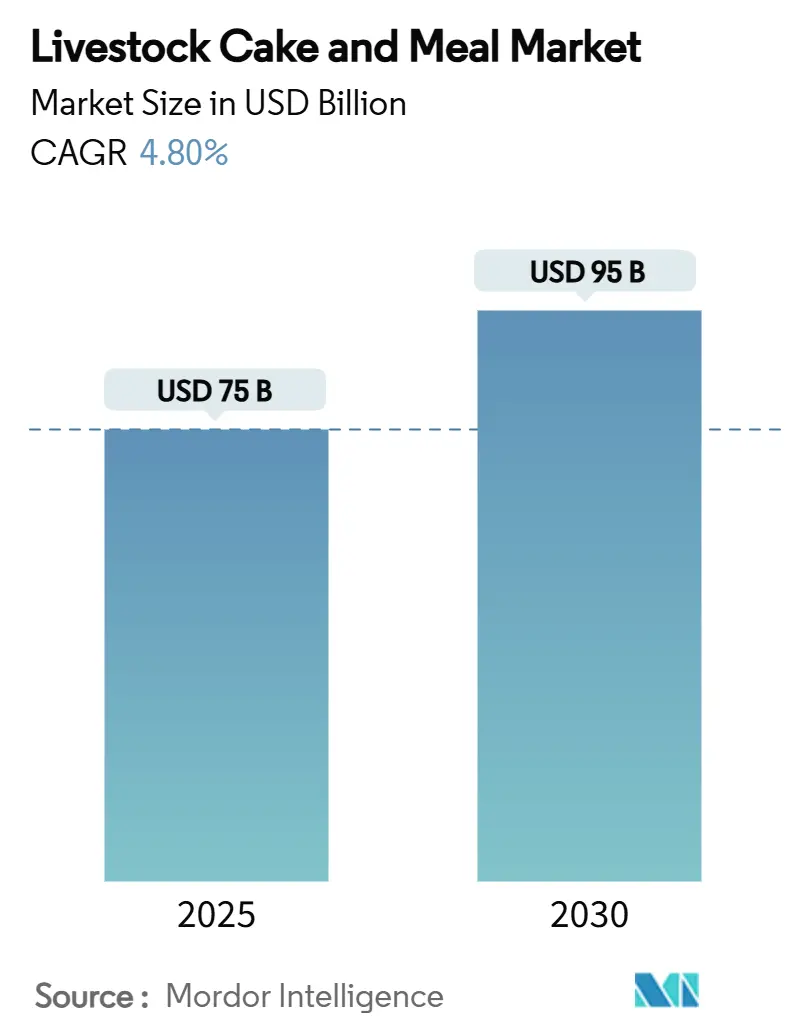

| Market Size (2025) | USD 75 Billion |

| Market Size (2030) | USD 95 Billion |

| Growth Rate (2025 - 2030) | 4.80% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Livestock Cake And Meal Market Analysis by Mordor Intelligence

The livestock cake and meal market size reached USD 75 billion in 2025 and is forecast to reach USD 95 billion by 2030, advancing at a 4.8% CAGR during the period. Strong protein demand in emerging economies, rapid expansion of global soybean crush capacity, and growing adoption of precision nutrition technologies underpin this momentum. Higher disposable incomes in Asia-Pacific drive poultry and aquaculture feed uptake, while sustainability-linked financing compels processors to shift toward certified, deforestation-free oilseed supplies. Anticipated regulatory tightening around antibiotic-free production in Europe and North America further accelerates substitution toward nutrient-dense cakes and meals. Meanwhile, innovations in extrusion and fermentation enhance the digestibility of specialty oilseed by-products, providing processors with cost-competitive alternatives. Market participants are also leveraging AI-enabled formulation tools to deliver targeted amino-acid profiles, reducing overall ration costs and improving feed-conversion ratios.

Key Report Takeaways

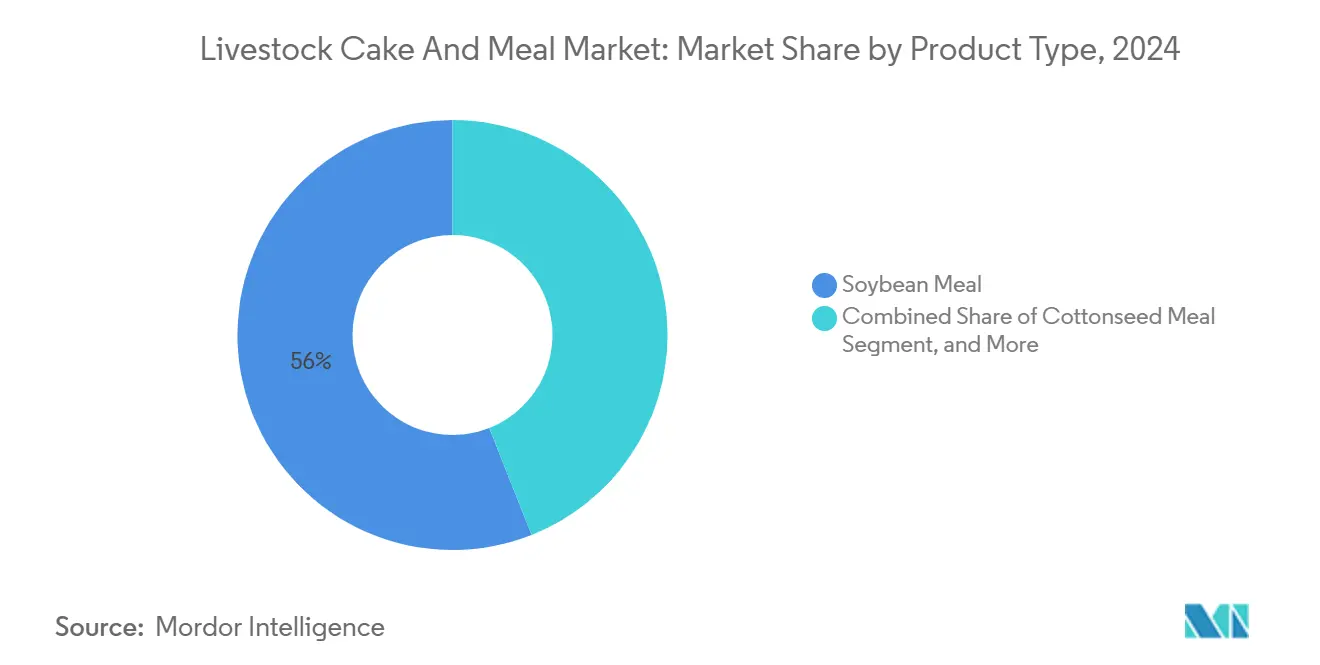

- By product type, soybean meal led with 56% revenue share in 2024, and sunflower meal is projected to advance at a 7.8% CAGR through 2030, the fastest among product categories.

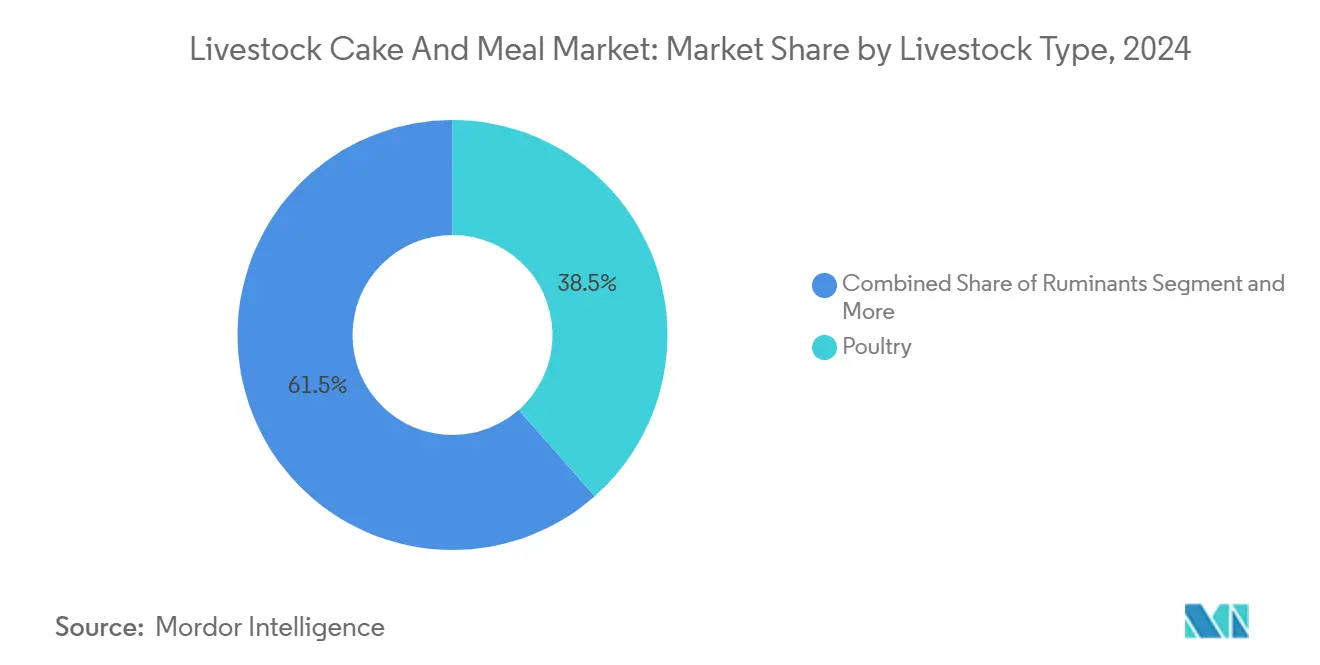

- By livestock type, poultry held a 38.5% share of the livestock cake and meal market size in 2024, and aquaculture is forecast to record the highest CAGR at 9.2% to 2030.

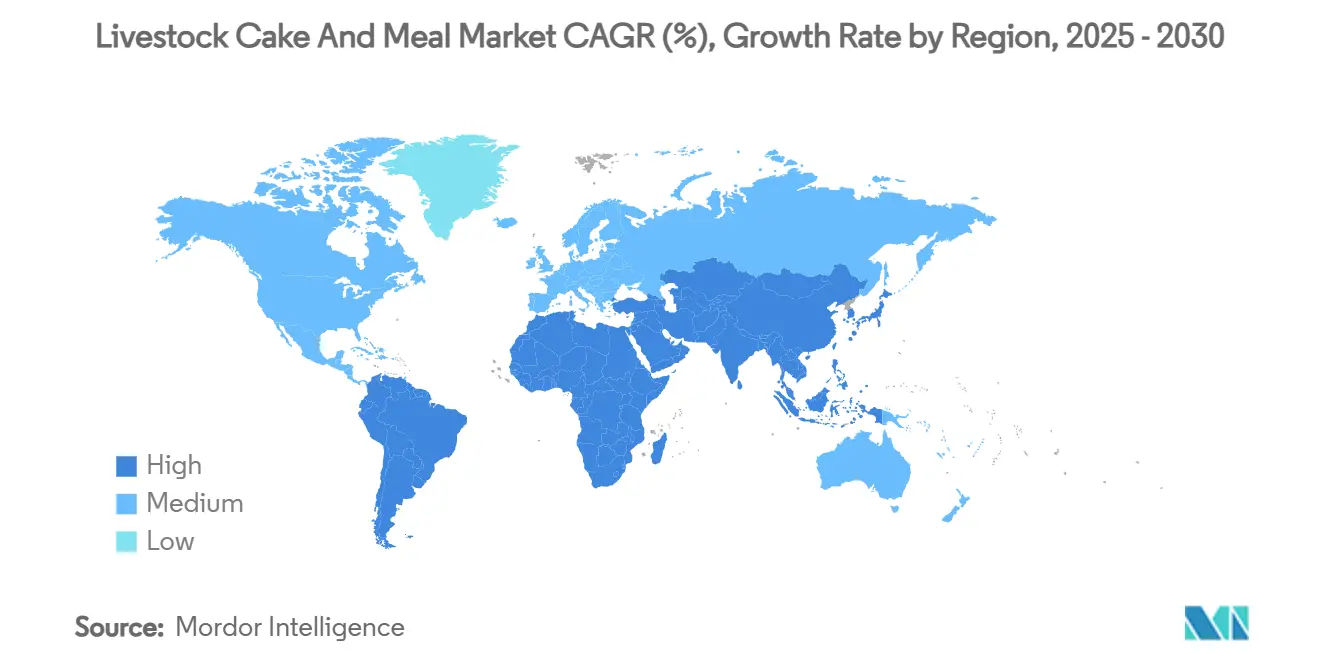

- By geography, Asia-Pacific captured 42% of the livestock cake and meal market share in 2024, and the Middle East is set to grow at a 7.5% CAGR through 2030, the most rapid among regions.

Global Livestock Cake And Meal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-protein feed from expanding meat consumption | +1.20% | Global (highest in Asia-Pacific, Middle East) | Medium term (2-4 years) |

| Expansion of global soybean crush capacity lowering meal cost | +0.80% | North America, South America, Asia-Pacific | Short term (≤ 2 years) |

| Stricter antibiotic-free feed rules boosting nutrient-dense meals | +0.70% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Rapid poultry sector growth in emerging economies | +0.60% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Surplus biodiesel co-products enabling higher meal inclusion | +0.40% | North America, Europe, South America | Short term (≤ 2 years) |

| AI-driven precision formulation favoring speciality oilseed cakes | +0.30% | Global (early adoption in North America, Europe) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Protein Feed From Expanding Meat Consumption

Escalating per-capita meat intake in Asia-Pacific and parts of the Middle East is transforming livestock nutrition requirements. India’s poultry consumption has climbed at 8% annually since 2024, pushing feed mills to upgrade amino-acid density and digestibility metrics in rations. Intensive broiler and layer operations increasingly substitute grain-heavy mixes with soybean and sunflower meals to hit aggressive feed-conversion benchmarks. Premium oilseed cakes now command price premiums as buyers prioritize consistent protein quality over crude percentages. Integrated processors capitalize on this shift by offering traceable, certifications-backed meals aligning with halal and antibiotic-free standards. Accelerating urbanization continues to draw consumers toward convenient poultry and aquaculture proteins, locking in structural demand for high-protein feed inputs.

Expansion of Global Soybean Crush Capacity Lowering Meal Cost

Brazil added 30% crushing capacity in 2024 and Argentina followed with 25% upgrades, generating sizeable soybean meal surpluses that eased prices worldwide. Biodiesel mandates incentivize higher oil extraction volumes, indirectly subsidizing livestock meal outputs. Locating new plants closer to feed hubs slashes freight costs and improves freshness, especially beneficial for Asia-Pacific poultry complexes. Modern extraction lines achieve higher throughput and lower energy consumption, narrowing production cost curves without sacrificing amino-acid integrity. Price declines have encouraged feed formulators to raise inclusion rates, boosting overall livestock cake and meal market demand. Simultaneously, forward-contracting mechanisms tied to crush margins help mills hedge cost risks.

Stricter Antibiotic-Free Feed Rules Boosting Nutrient-Dense Meals

The European Union fully enforced antibiotic-growth-promoter bans in 2024, forcing feed manufacturers to compensate via nutritional enrichment.[1]CFIA, “CFIA publishes new, updated Feeds Regulations,” inspection.gc.ca Soybean, rapeseed, and sunflower meals rich in bioactive peptides and natural antioxidants now replace pharmaceutical interventions in boosting gut health. Formulators blend functional oilseed cakes that supply balanced lysine, methionine, and threonine levels, sustaining growth performance without antimicrobials. Documentation of mycotoxin control, trace elements, and digestibility coefficients has become mandatory for import approvals, elevating entry barriers for undifferentiated commodity suppliers. North American producers pre-empt similar regulations, accelerating R&D in enzyme-treated cakes to unlock latent protein fractions.

Rapid Poultry Sector Growth in Emerging Economies

Organized poultry farming in India expanded 15% during 2024, while Indonesia’s broiler volumes jumped 12%, spurring steep feed demand. International genetics paired with automated housing require tightly balanced rations, elevating reliance on soybean meal with ≥48% protein and low urease activity. Vertical integrators often operate captive feed mills, guaranteeing consistent offtake for high-quality cakes. Suppliers offering technical advisory services on pellet durability, gut health enhancers, and precision amino-acid balancing gain preferred-vendor status. Rapid urban retail growth and quick-service restaurant penetration further cement poultry’s position, sustaining upward momentum in the livestock cake and meal market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in oilseed crop prices | -0.90% | Global (most acute in import-dependent regions) | Short term (≤ 2 years) |

| Competition from insect and microbial proteins | -0.50% | Europe, North America, emerging presence in Asia-Pacific | Long term (≥ 4 years) |

| Trade policy uncertainty on pesticide residues | -0.60% | Asia-Pacific, Middle East, Europe | Short term (≤ 2 years) |

| Sustainability-linked finance penalizing deforestation risk | -0.38% | Europe, North America, increasingly global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Oilseed Crop Prices

Climate-induced yield swings and shifting trade policies subjected soybean futures to 40% price fluctuations during 2024, straining feed manufacturers’ budgeting processes.[2]USDA, “Packers and Stockyards 2021-2022 Report to Congress,” usda.gov Import-dependent regions such as the Middle East experience amplified volatility due to freight and currency exposures. Hedge strategies involving futures, options, and diversified origin contracting have become critical but remain out of reach for smaller mills. Sporadic droughts in Argentina and logistics bottlenecks in Brazil periodically choke export flows, forcing spot-market purchases at elevated premia. The burden ultimately transmits to livestock producers, who confront thinner margins or must hike consumer prices, curbing growth in the livestock cake and meal market.

Competition From Insect and Microbial Proteins

The Food and Drug Administration's streamlined Animal Food Ingredient Consultation pathway, finalized in 2024, accelerated approvals for black soldier fly larvae meal and precision-fermented microbial proteins.[3]FDA, “Animal Food Ingredient Consultation; Draft Guidance,” federalregister.govThese alternatives attain ≥60% protein and appealing amino-acid profiles, attracting aquafeed formulators willing to pay premium prices for sustainability credentials. Large retailers pledging scope-3 emission cuts incentivize pet-food and laying-hen producers to pilot insect-based rations. Although current production volumes remain modest, cost curves are anticipated to converge with specialty oilseed meals, posing a tangible substitution threat. Traditional crushers counter by developing deforestation-free supply chains and nutrient-enhanced cakes to defend their share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Meals Gain Ground on Soybean Dominance

Soybean meal retained a 56% revenue share in 2024, underscoring its entrenched role as the global protein benchmark. Its widespread acceptance stems from predictable amino-acid composition, readily available global logistics, and decades of performance data. Sunflower meal’s forecast 7.8% CAGR signals a pivot toward specialty alternatives whose fiber profile supports gut integrity in antibiotic-restricted regimes. Rapeseed meal has consolidated presence in Europe, aided by low glucosinolate varieties and proximity to crushing facilities. Palm kernel cake continues to resonate with tropical ruminant systems, offering cost-effective energy-protein blends. AI-assisted formulation increasingly tailors specific lysine-to-methionine ratios, incentivizing feed mills to experiment with sesame, cottonseed, and niger meals. Extrusion preprocessing upgrades digestibility and palatability of these niche inputs, broadening supplier portfolios and deepening product differentiation within the livestock cake and meal market.

The market’s commodity-to-specialty transition aligns with sustainability imperatives. Certified deforestation-free soybean cake commands price premia in Europe and Japan, while non-GMO rapeseed meal appeals to brands pursuing clean-label credentials. Processors installing enzymatic treatment lines capture value by enhancing bypass protein fractions for dairy applications. Forward-looking crushers invest in fermentation steps that concentrate peptides and reduce antinutritional factors, allowing substitution levels to rise without compromising animal performance. Collectively, these developments diversify revenue streams and cushion margins against conventional crush-margin volatility.

By Livestock Type: Aquaculture Sets the Premium Bar

Poultry accounted for 38.5% of livestock cake and meal market demand in 2024, reflecting the species’ scale and standardized nutrition regimes. Nonetheless, aquaculture’s 9.2% forecast CAGR positions it as the marquee growth engine. Floating feeds for tilapia and shrimp require meals with precise water stability and oil-binding properties. Specialty suppliers engineer particle size distributions and thermal profiles to meet these parameters, selling at price points 20-30% above bulk soybean meal. Swine rations prioritize digestibility and lysine density, spurring demand for mechanically defatted cakes that limit fiber content. Ruminant nutrition maintains appetite for higher-fiber meals such as cottonseed cake, leveraging rumen microbes to unlock energy from complex carbohydrates.

Emerging segments include companion-animal diets, where hypoallergenic oilseed peptides fetch sizable premia. Functional ingredients, such as Omega-3-enriched rapeseed cake, resonate with pet-food formulating goals tied to coat health and cognitive development. The integration of near-infrared spectroscopy at feed plants ensures batch-level protein verification, strengthening quality assurance across species and sustaining buyer trust in the livestock cake and meal market.

Geography Analysis

Asia-Pacific dominated with a 42% share of global consumption in 2024, anchored by massive poultry and aquaculture sectors in China, India, and Southeast Asia. Continuous investments in domestic crushing capacity, coupled with port upgrades in Indonesia and Vietnam, are reducing reliance on imported meals and enhancing just-in-time delivery to feed hubs. Government-sponsored cold-chain rollouts further stimulate meat and fish output, magnifying downstream feed requirements for high-quality cakes.

The Middle East is forecast to grow at 7.5% CAGR to 2030, powered by sovereign food-security programs in Saudi Arabia, the UAE, and Qatar. Subsidized credit encourages private investors to co-locate crush plants with dairy and poultry mega-farms. Water scarcity elevates interest in palm kernel and sunflower cakes that deliver higher nutrient density per irrigation unit, aligning with resource-efficiency mandates. Traceability platforms documenting deforestation-free or non-irrigated origins help importers secure green-finance incentives, bolstering regional demand in the livestock cake and meal market.

North America’s established crushing infrastructure supports steady domestic demand while feeding export channels to Mexico and Southeast Asia. Adoption of precision-nutrition software and enzyme-treated meals yields incremental productivity gains, offsetting plateauing animal numbers. South America leverages biodiesel-driven soybean processing to export competitively priced meal volumes, yet rising domestic poultry and aquaculture ventures in Brazil capture a growing share internally, tightening export availabilities during peak demand seasons.

Competitive Landscape

The livestock cake and meal market exhibits moderate concentration. Cargill, Incorporated, is leveraging a globally integrated supply chain and proprietary risk-management platforms. Archer Daniels Midland Company is backed by process-technology leadership and long-term offtake contracts with integrated poultry giants. Bunge, Wilmar, and Louis Dreyfus also maintain strong market presence and origination strength with regional crushing footprints. Players such as COFCO and Viterra exploit captive domestic demand and targeted Asia-Pacific expansion to climb the rankings.

Strategic focus is shifting toward value-added meal grades tailored to antibiotic-free, non-GMO, and sustainability-certified niches. Firms are co-locating crush plants with biodiesel refineries to optimize shared logistics and capture glycerin co-products. AI-driven nutrient-profiling platforms offer embedded differentiation, binding clients into multi-year supply agreements. Partnerships with insect-protein startups hedge against future protein-source disruption.

Capital allocations increasingly favor energy-efficient solvent-extraction retrofits and enzymatic treatment lines that raise protein digestibility, enabling premium pricing structures in the livestock cake and meal market. Europe-based crushers fast-tracked carbon-footprint calculators to comply with anticipated border-adjustment charges, clinching preferred-supplier status with multinational food brands.

Livestock Cake And Meal Industry Leaders

Cargill, Incorporated.

Wilmar International Ltd

ADM (Archer Daniels Midland Company)

Bunge India Private Limited

Louis Dreyfus Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: California proposed emergency regulations for commercial feed ingredient definitions, establishing new nutritional guarantees and labelling requirements for cottonseed meal, alfalfa products, and various protein sources used in livestock nutrition.

- July 2024: The Canadian Food Inspection Agency published updated feed regulations governing safety and quality standards for animal feed products.

Global Livestock Cake And Meal Market Report Scope

| Soybean Meal |

| Cottonseed Meal |

| Rapeseed Meal |

| Sunflower Meal |

| Palm Kernel Cake |

| Other Oilseed Meals/Cake |

| Poultry |

| Ruminants |

| Swine |

| Aquaculture |

| Other Livestock |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| Product Type | Soybean Meal | |

| Cottonseed Meal | ||

| Rapeseed Meal | ||

| Sunflower Meal | ||

| Palm Kernel Cake | ||

| Other Oilseed Meals/Cake | ||

| Livestock Type | Poultry | |

| Ruminants | ||

| Swine | ||

| Aquaculture | ||

| Other Livestock | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current livestock cake and meal market size and its growth outlook?

The livestock cake and meal market size stands at USD 75 billion in 2025 and is projected to reach USD 95 billion by 2030 at a 4.8% CAGR.

Which product type dominates the livestock cake and meal market?

Soybean meal dominates with a 56% revenue share in 2024, owing to its consistent amino-acid profile and global availability.

Which region offers the highest growth potential for suppliers?

The Middle East shows the fastest regional growth at a 7.5% CAGR, supported by food-security investments and new crushing capacity.

What emerging proteins threaten traditional oilseed meals?

Insect-based and microbial proteins, now gaining regulatory approvals, present growing competition, particularly in high-value aquafeed and pet-food niches.

Page last updated on: