Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 623.16 Million |

| Market Size (2031) | USD 842.62 Million |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

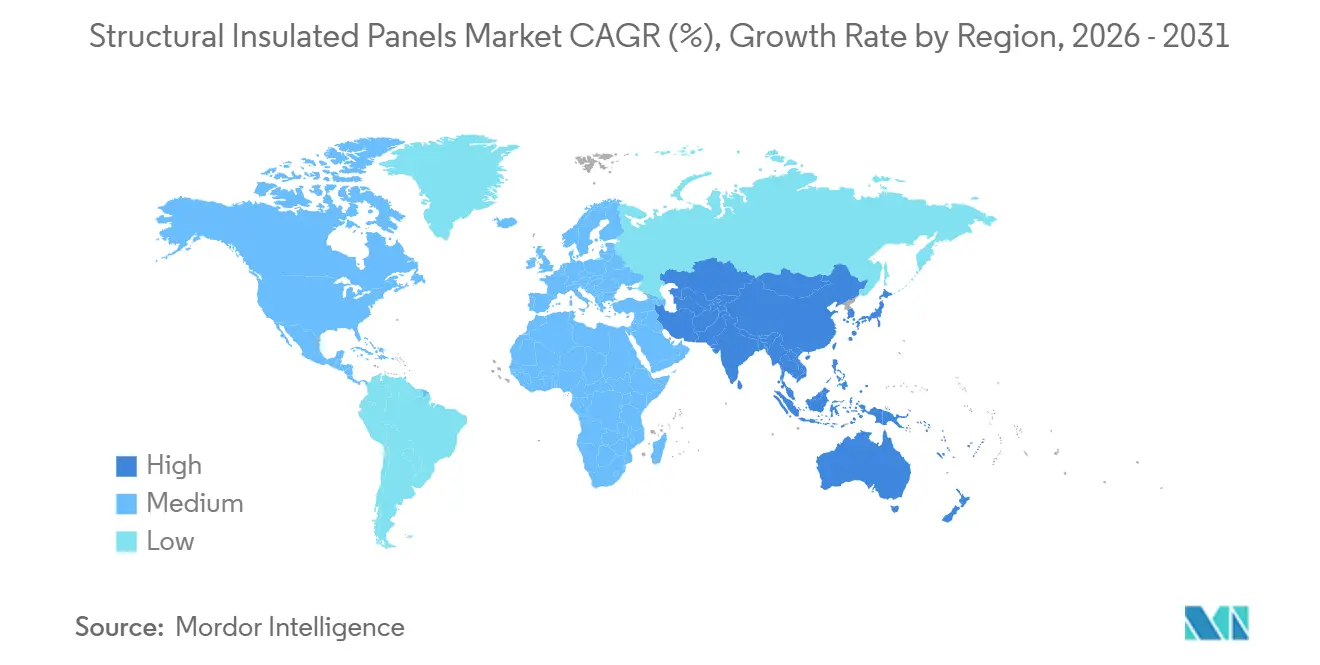

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Structural Insulated Panels Market Analysis by Mordor Intelligence

The Structural Insulated Panels Market size is estimated at USD 623.16 million in 2026, and is expected to reach USD 842.62 million by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Growth is powered by the convergence of tighter energy-efficiency rules, accelerating off-site construction, and mounting pressure to cut operational carbon. Cost premiums that once limited adoption are now counter-balanced by faster build schedules, reduced labor exposure, and measurable reductions in heating or cooling loads. Tight lumber supply in North America, cold-chain expansions in Asia-Pacific, and affordable-housing mandates across multiple regions continue to redirect capital toward high-R-value envelope systems. Competitive strategies are shifting as foam, steel, and glass-wool suppliers integrate forward into panel fabrication, while traditional lumber players diversify into noncombustible skins. Together, these forces reinforce a steady upward trajectory for the structural insulated panels market even in an environment of volatile commodity pricing.

Key Report Takeaways

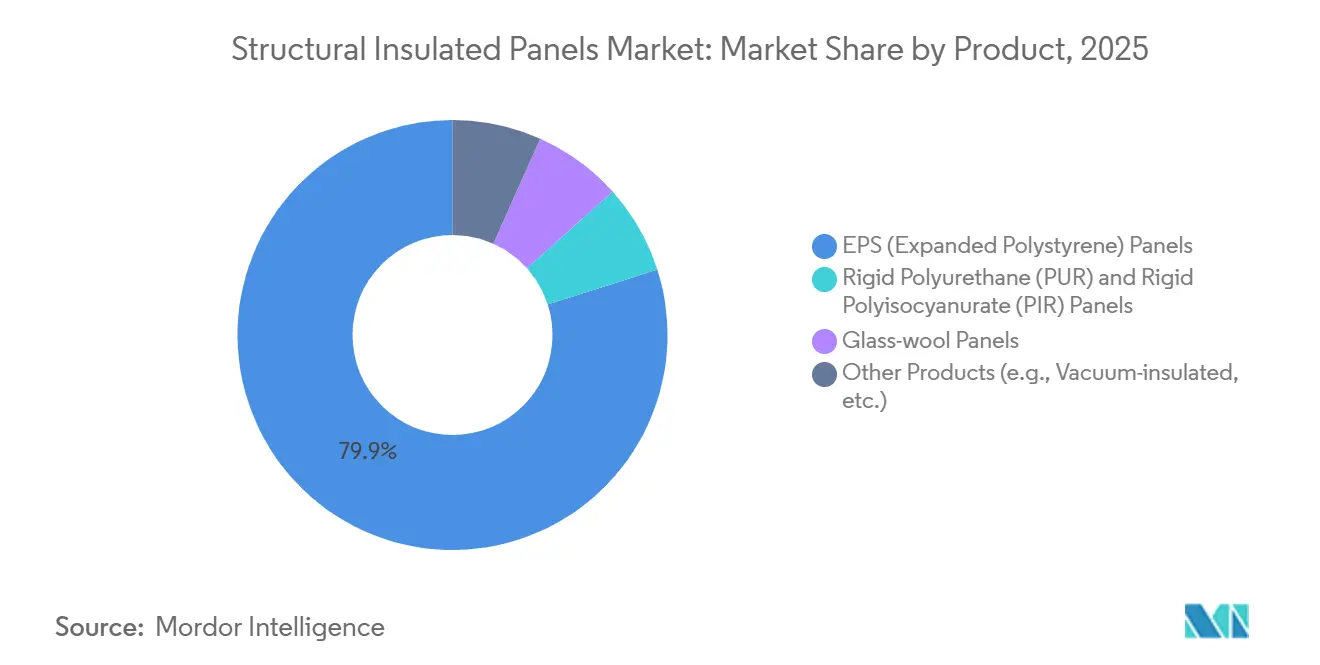

- By product, expanded polystyrene captured 79.94% of the structural insulated panels market share in 2025 and is forecast to grow at a 6.36% CAGR through 2031.

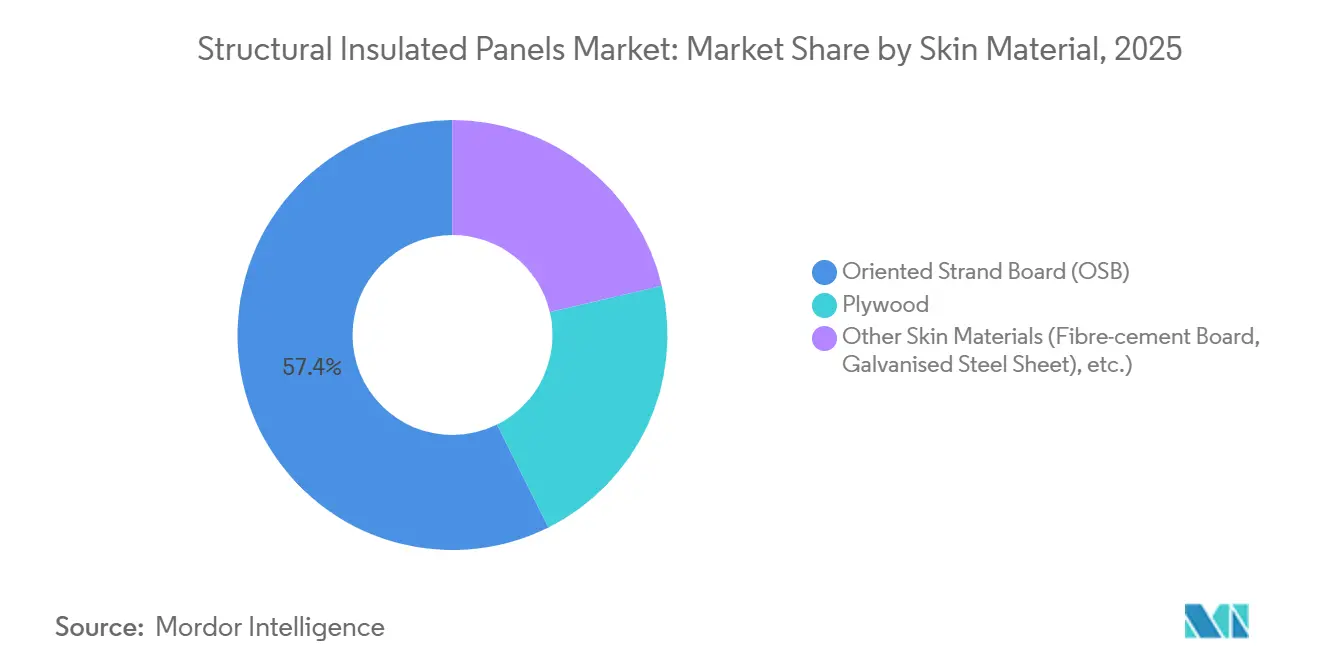

- By skin material, oriented strand board held 57.36% revenue share in 2025, while other skin materials are expected to advance at a 7.19% CAGR to 2031.

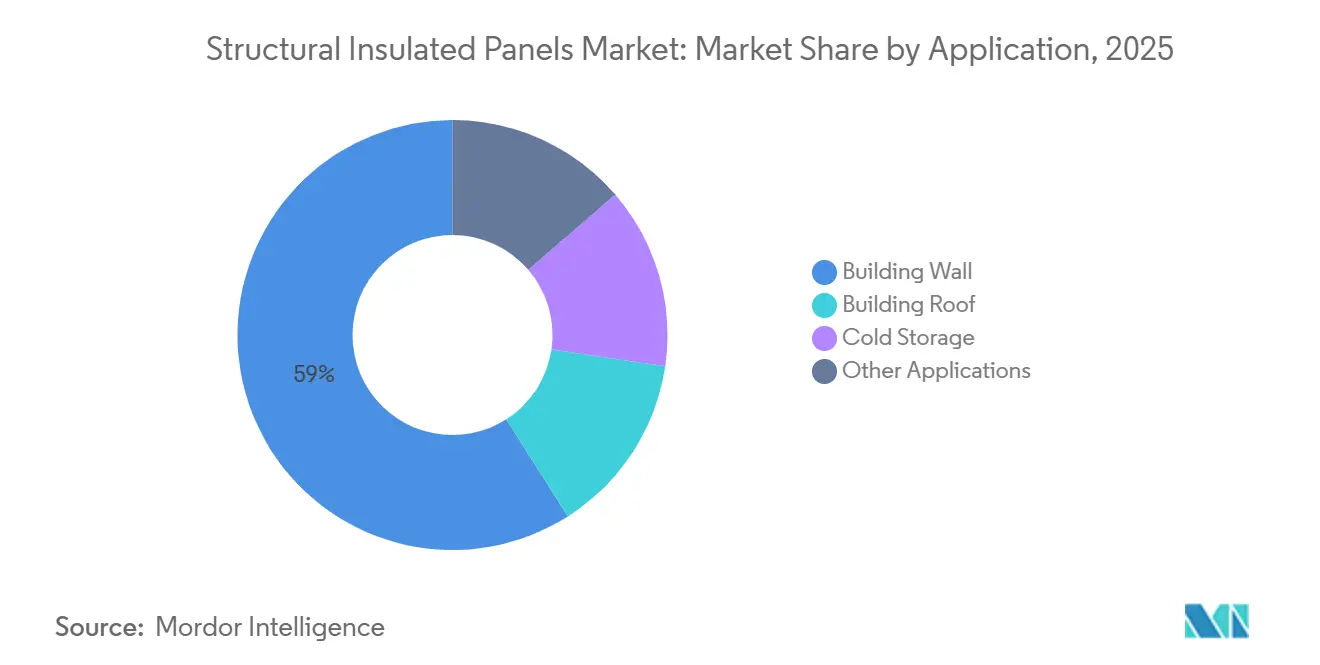

- By application, building-wall systems accounted for 59.02% of the structural insulated panels market size in 2025 and are expanding at a 6.75% CAGR to 2031.

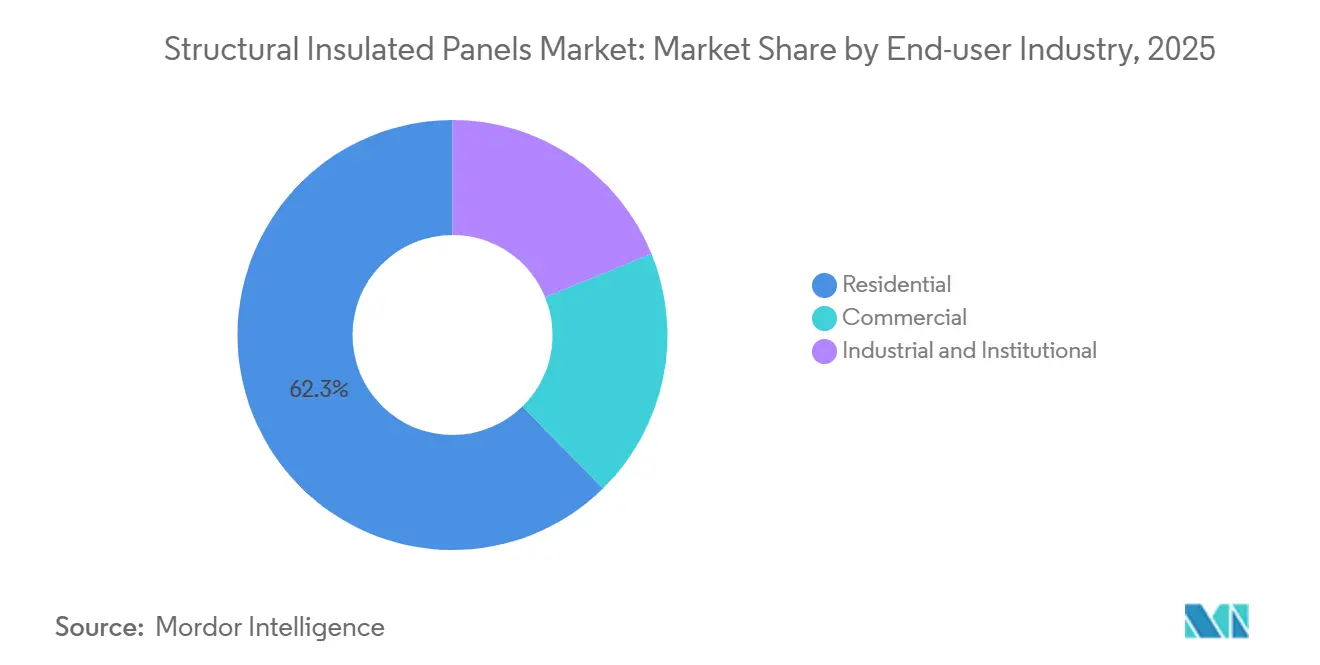

- By end-user industry, the residential segment controlled 62.35% of 2025 revenue and is on track to post the fastest 7.02% CAGR through 2031.

- By geography, North America led with 37.27% structural insulated panels market share in 2025, whereas Asia-Pacific is projected to climb at a 7.41% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Structural Insulated Panels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Efficiency Regulations Accelerating Adoption | +1.4% | Global, with concentrated enforcement in EU and select US states | Medium term (2-4 years) |

| Expansion of Global Cold-Chain Infrastructure | +0.9% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Rising Affordable-Housing and Residential Remodelling | +1.6% | North America and APAC, emerging in South America | Short term (≤ 2 years) |

| Growing Preference for Rapid, Off-Site Construction | +1.3% | Global, early gains in North America and Northern Europe | Medium term (2-4 years) |

| Carbon-Credit Monetisation for Timber-Based Structural Insulated Panels | +0.7% | EU, California, British Columbia, and select APAC pilot zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy Efficiency Regulations Accelerating Adoption

Multiple jurisdictions are tightening thermal-transmittance limits, driving builders toward high-R-value envelopes. The 2024 revision of the European Union’s Energy Performance of Buildings Directive phases out fossil-fuel heating in new dwellings by 2028, essentially mandating super-insulated exterior walls. The U.S. Department of Energy raised wall insulation requirements by 20% for climate zones 4-7 in 2025, pushing conventional stick framing to its practical limits. California’s updated Title 24 grants compliance credits for factory-built panels that test below 1.5 ACH at 50 Pa, a threshold routinely met by structural insulated panels but seldom achieved by site-built walls. Collectively, these rules reward upfront thermal investment, synchronize builder incentives with occupant energy costs, and add momentum to the structural insulated panels market.

Expansion of Global Cold-Chain Infrastructure

Pharmaceutical distribution and perishable-food logistics continue to add temperature-controlled space at a double-digit clip. The International Air Transport Association logged an 11% year-over-year rise in cold-chain capacity in 2025, with Asia-Pacific capturing 43% of new square footage. Hyperscale grocers such as Walmart adopted insulated-panel envelopes for 14 new facilities in 2025, citing a 22% refrigeration-load cut versus masonry and spray-foam walls. Because energy expenses account for up to 40% of warehouse operating costs, the payback on higher-performance panels is swift, supporting premium pricing for vacuum-insulated cores in the structural insulated panels market.

Rising Affordable-Housing and Residential Remodeling

Governments now regard off-site fabrication as a lever to close housing gaps. In 2025 the U.S. Department of Housing and Urban Development launched a USD 1.2 billion grant program prioritizing panelized construction that delivers units within 12 months of site acquisition[1]U.S. Department of Housing and Urban Development, “Innovation in Affordable Housing Grants,” hud.gov . India’s Pradhan Mantri Awas Yojana allocated INR 480 billion (USD 5.8 billion) for urban dwellings, with several states piloting insulated panels for 2026 completion targets. Remodeling also lifts demand; energy-efficiency projects reached 18% of U.S. renovation spend in 2025, up from 12% five years earlier. The residential channel therefore underpins both baseline volume and the steepest growth in the structural insulated panels market.

Growing Preference for Rapid, Off-Site Construction

Persistent labor shortages push contractors to industrialized building methods. Seventy-eight percent of U.S. general contractors ranked workforce availability as their top worry in 2025. The United Kingdom’s Construction Leadership Council aims for 25% off-site value by 2030, explicitly naming structural insulated panels as a key technology. When envelope erection drops from weeks to days, developers can shorten carrying costs and lock lower rates on construction loans, reinforcing demand in the structural insulated panels market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Costs Vs. Conventional Framing | -1.2% | Global, acute in cost-sensitive residential markets | Short term (≤ 2 years) |

| Substitution Threat from Advanced Prefab Wall Systems | -0.8% | North America and EU, limited penetration in APAC | Medium term (2-4 years) |

| OSB Supply Volatility (Beetle Infestation and Mill Outages) | -1.1% | North America, indirect impact on global pricing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Costs Versus Conventional Framing

Structural insulated panels carry a 15-25% material premium over stud walls with batt insulation, a hurdle for builders working on tight gross margins. A 2025 cost study by the National Association of Home Builders pegged the incremental outlay at USD 8-12 per square foot of wall area, stretching the payback period to 12-15 years in markets lacking utility rebates. Financial institutions that underwrite loans on first cost rather than lifecycle savings compound the burden, amplifying the near-term restraint on the structural insulated panels market.

Substitution Threat from Advanced Prefab Wall Systems

Cross-laminated timber, light-gauge steel panels, and autoclaved aerated concrete now compete head-to-head with foam-core assemblies. Changes to the International Building Code in 2024 lifted allowable timber heights to 18 stories, opening mid-rise opportunities formerly reserved for structural insulated panels. Prefabricated steel panels grabbed 9% of the U.S. commercial envelope market in 2025, up from 5% two years earlier, driven by noncombustible requirements in data centers and cold storage[2]American Institute of Steel Construction, “Commercial Envelope Market Report 2025,” aisc.org. These alternatives erode share in applications where fire resistance or exposed-wood aesthetics trump insulation depth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: EPS Secures Mass-Market Leadership

Expanded polystyrene panels dominated with 79.94% share in 2025 and are projected to climb at a 6.36% CAGR through 2031. EPS delivers R-3.6-4.2 per inch at 30-40% lower material cost than polyurethane, a differential central to volume adoption. Kingspan noted that EPS accounted for 62% of its insulated-panel revenue in 2025, a testament to deep residential penetration. Fire-code shifts and space constraints sustain niche demand for higher-R-value polyurethane and polyisocyanurate, but those chemistries remain secondary for commodity housing. Glass-wool cores serve fire-rated and acoustic-sensitive projects, while vacuum-insulated panels still sit at lower unit volume, confined to pharma cold chains and aerospace.

A regulatory edge also accrues to EPS because it already relies on pentane, a climate-compliant blowing agent. By contrast, polyurethane suppliers are still retooling to replace HFCs banned by the U.S. Environmental Protection Agency in 2024. That conversion introduces yield uncertainty and scrap risk, temporarily widening the cost gap in favor of EPS and further consolidating leadership in the structural insulated panels market.

By Skin Material: OSB Dominance Faces Noncombustible Tailwinds

Oriented strand board commanded 57.36% segment share in 2025, underpinned by its favorable weight-to-strength profile and compatibility with conventional fastening methods. Yet the structural insulated panels market is recording a notable pivot toward noncombustible skins. Other skin materials are forecast to rise at a 7.19% CAGR to 2031 as urban fire codes stiffen. Tata Steel reported that steel-faced panels captured 14% share in Indian commercial construction by 2025, driven by cold-storage and pharmaceutical demands.

OSB’s supply swings also nurture diversification. Beetle-driven log shortages pushed some manufacturers to plywood or hybrid steel laminates, each of which demands requalification under local codes but buffers raw-material risk. Digital design workflows accelerate change; architects now specify fire rating, impact resilience, and surface finish within BIM models, empowering project teams to evaluate multiple skin options early, compressing bid windows, and widening acceptance of nontraditional facings in the structural insulated panels market.

By Application: Wall Systems Anchor Volume while Cold Storage Commands Premiums

Building walls represented 59.02% of 2025 shipments and are advancing at a 6.75% CAGR through 2031. Independent testing by the U.S. Department of Energy in 2025 showed that panel walls reduced whole-building heating loads by up to 24% versus 2×6 studs with R-21 batts. That performance edge undergirds both new-build and retrofit momentum, especially in northern climates where heating bills materially influence payback. Roof panels secure the next-largest slice, favored on low-slope commercial buildings for their ability to integrate structure, vapor control, and insulation in a single component.

Cold-storage projects, though smaller in cubic meter terms, deliver outsized margin to panel suppliers. Global refrigerated capacity hit 730 million m³ in 2025, and most new builds default to panel envelopes to manage ±2 °C tolerances. Vacuum-insulated cores and stainless-steel facings—well beyond mainstream residential spec levels—fetch premium pricing yet win bids based on guaranteed temperature stability and hygiene compliance. As hyperscale grocers and biologics shippers expand, premium cold-chain requirements sustain a profitable niche inside the structural insulated panels market.

By End-user Industry: Residential Leads Both Volume and Growth

Residential absorbed 62.35% of 2025 demand and shows the swiftest 7.02% CAGR through 2031. Median build times for panelized homes in the United States compressed to 4.8 months in 2025, compared with 6.2 months for stick-frame houses. Millennials entering first-time homeownership and aging households pursuing energy-retrofit upgrades together propel volume. The 2026 tax-credit structure under the U.S. Inflation Reduction Act reimburses up to USD 1,200 for qualifying envelope improvements, a threshold panels readily exceed.

Commercial and institutional segments follow, leaning on panels to hit speed-to-occupancy targets in design-build arrangements. Industrial buyers, from manufacturers to data-center operators, look to airtight panelized envelopes to slash HVAC loads. The U.S. Army Corps of Engineers now specifies panels for forward-operating bases to achieve R-30 walls in one assembly, validating performance in extreme environments and strengthening credentials across the broader structural insulated panels market.

Geography Analysis

North America controlled 37.27% of global revenue in 2025, buoyed by U.S. and Canadian housing demand. Canada benefits further from provincial heat-loss caps that favor R-30 walls and airtightness below 2 ACH at 50 Pa. Nevertheless, beetle-induced OSB volatility and growing cross-laminated timber appeal temper North American expansion. Mexico remains an untapped frontier, where low energy costs and abundant skilled labor preserve conventional masonry, although nearshoring-driven industrial builds provide a niche opening for fast-tracked insulated envelopes.

Asia-Pacific is forecast to advance at a 7.41% CAGR, the quickest worldwide. China’s prefabricated-construction is growing with insulated panels surfacing in 18% of prefab housing starts, especially in northern provinces that enforce stringent heating-season energy caps. India’s market lifts off from a modest base but benefits from state-funded affordable-housing schemes and explosive cold-chain construction linked to pharmaceutical exports. Southeast Asian economies—from Vietnam to Indonesia—deploy panels in temperature-controlled warehouses that support rapidly expanding e-commerce grocery deliveries. Local manufacturing investments by Chinese, Indian, and multinational firms shorten lead times and buffer the structural insulated panels market against currency swings and freight costs.

Europe’s demand is anchored by Germany, the United Kingdom, and France. Strict near-zero-energy directives and incentive loans from Germany’s KfW bank push adoption toward Passive House-level performance. The United Kingdom targets off-site delivery to shrink its housing shortfall, explicitly including insulated panels in policy roadmaps. Eastern Europe, funded by EU structural packages, emerges as a fast-growing sub-region prioritizing deep-energy retrofits of socialist-era multifamily blocks. Southern Europe remains a relative laggard because milder climates dilute energy-savings economics, yet wildfire risk accelerates interest in fire-rated, noncombustible skins.

South America and the Middle East and Africa collectively form a small but strategic slice. Brazil mandates panel envelopes in vaccine storage under ANVISA regulations. Saudi Arabia integrates panels into data-center shells to lower cooling loads under 50 °C desert temperatures. South Africa’s social-housing pilots trial panelized retrofits to upgrade informal settlements. Limited local fabrication capacity, import duties, and volatile currencies restrict scale but also open investment windows for early entrants aiming to capture nascent demand in the structural insulated panels market.

Regulatory Landscape

Structural insulated panels (SIPs) are governed mainly through building-code acceptance pathways, with prescriptive recognition in the International Residential Code (IRC) Section R610 and use under the International Building Code (IBC) as alternative materials backed by third-party evaluation reports. In April 2026, the Structural Insulated Panel Association (SIPA) had its ICC-ES Master Code Report (ESR-4689) reissued, confirming code compliance across 2024, 2021, and 2018 IBC editions, and Ecopan Corporation had ICC-ES reissue ESR-5159 verifying compliance with 2024 IBC/IRC and alignment with 2025 CALGreen references.

State and country overlays also impose project-critical requirements tied to energy and resilience performance. California’s 2025 Building Energy Efficiency Standards (Title 24) took effect January 1, 2026, reinforcing performance-based compliance routes where tested airtightness and U-factor performance reward factory-built envelope systems. In hurricane-exposed markets, the Florida Building Commission issued an engineering evaluation report (FL28131_R3) in October 2024 for SIP wall compliance with the 8th Edition (2023) Florida Building Code, including High Velocity Hurricane Zone requirements, while product qualification for performance-rated SIP walls is increasingly standardized through ANSI/APA PRS 610.1-2023.

Value Chain Analysis

The SIP value chain begins with upstream inputs, primarily OSB/plywood facings and insulation cores (EPS, PUR/PIR, or mineral/glass wool), alongside adhesives and lamination consumables. SIP fabricators then convert these inputs using precision cutting and press-lamination equipment, and they supply panels through direct-to-builder channels, regional component distributors, and off-site construction partners that package design, engineering, and installation services. Standards such as ANSI/APA PRS 610.1-2023 and prescriptive recognition via IRC Section R610 shape manufacturers' quality assurance and documentation, reducing friction at permitting and inspection.

Cost and availability risks center on facing materials and petrochemical-derived resins, with OSB volatility and foam feedstock swings affecting panel pricing and lead times. These pressures have pushed some contract structures toward longer-term supply agreements and indexation clauses, and they reinforce nearshoring and localized fabrication where logistics costs and import duties materially affect delivered cost. High capital intensity for CNC, presses, and test and QA systems remains a barrier for new entrants, favoring scale players or fabricators integrated into established prefab and building-component networks.

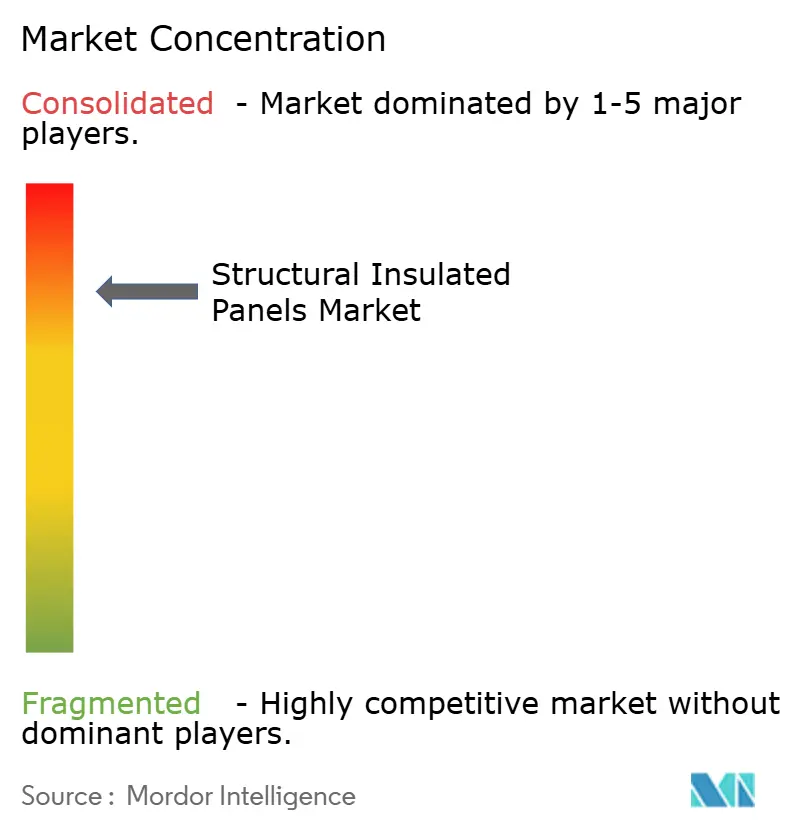

Competitive Landscape

Competition sits at a high concentration level as large global incumbents vie with agile regional fabricators. Kingspan and Owens Corning exploit fully integrated supply chains—from foam chemistry through lamination—to guarantee product availability and performance. Tata Steel and ArcelorMittal draw on in-house metalworks to tailor noncombustible facings for hygiene-sensitive and high-durability uses. Warranty terms evolve into differentiators; Kingspan now extends 30-year thermal guarantees, whereas Owens Corning issues third-party-verified R-value certificates. Smaller firms thrive on localized customization and faster lead times, vital where design-build contracts demand rapid iteration.

Digitalization boosts competitive reshuffling. Nucor’s BIM-enabled panel configurator, launched in 2025, trims bid-to-delivery from six to three weeks and directly links architects’ models to CNC cut lists. Start-ups leverage e-commerce to reach owner-builders with standardized kits. Innovation funnels into fire-safe hybrid skins marrying magnesium-oxide and steel, as well as vacuum-insulated cores infused with phase-change materials for temperature-sensitive logistics. Intellectual-property filings accelerate, yet commercialization remains concentrated in premium data-center and pharmaceutical cold chains, where the structural insulated panels market tolerates USD 200-plus per square meter pricing.

Structural Insulated Panels Industry Leaders

Owens Corning

Kingspan Group

Carlisle Companies Inc.

METECNO GROUP

ArcelorMittal

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Energy-code tightening and clearer compliance pathways create whitespace for SIP adoption in residential and light-commercial envelopes where builders want repeatable airtightness and thermal performance without extended on-site labor. A near-term catalyst is the California Energy Commission putting the 2025 Title 24 standards into effect on January 1, 2026, alongside broader normalization of third-party evidence packages, including ICC-ES evaluation reports and performance-rated qualification under ANSI/APA PRS 610.1-2023, which reduces approval friction for manufacturers and designers moving beyond one-off engineering judgments.

Consolidation and capability build-out in off-site construction also open room for integrated design-to-manufacture offerings and for regional capacity additions that shorten lead times. In June 2026, SIP Building Systems Ltd completed the acquisition of SIP Build UK (SBUK Group), consolidating multiple UK SIP providers to expand manufacturing and technical design capability, a model that can fit fragmented regional markets. Cold-chain and temperature-controlled logistics continue to support higher-spec panel demand, where vacuum-insulated cores and noncombustible skins can command premium pricing tied to operational energy savings and hygiene-driven specifications.

Recent Industry Developments

- July 2026: ZS2 Technologies received over USD 2.7 million from the Government of Canada through the Regional Homebuilding Innovation Initiative to scale advanced panel manufacturing capacity for modular housing. The funding supports expansion of industrialized building supply chains and helps move higher-performance envelope components closer to housing-delivery programs.

- June 2026: SIP Building Systems Ltd (SBS) completed a multi-million-pound acquisition of SBUK Group (SIP Build UK), consolidating UK SIP manufacturing and design resources. The combined footprint increases capacity and engineering depth, strengthening its ability to serve MMC and faster-turn housing projects.

- December 2024: All Weather Insulated Panels launched FASSADE with Bellara, an insulated panel system aimed at contemporary facade applications. The introduction broadened architectural options for metal-panel envelopes and supported higher-value specification work where aesthetics and performance need to be packaged together.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from newly manufactured structural insulated panels (SIPs) sold for building envelope uses, where a rigid insulation core is bonded between two structural skins and supplied as wall, roof, or floor panels.

Scope exclusions: The scope excludes non-structural insulated boards used mainly for refrigeration or generic cladding, and it also excludes curtain wall composite panels that do not provide structural load support.

Segmentation Overview

- By Product

- EPS (Expanded Polystyrene) Panels

- Rigid Polyurethane (PUR) and Rigid Polyisocyanurate (PIR) Panels

- Glass-wool Panels

- Other Products (e.g., Vacuum-insulated, etc.)

- By Skin Material

- Oriented Strand Board (OSB)

- Plywood

- Other Skin Materials (Fibre-cement Board, Galvanised Steel Sheet), etc.)

- By Application

- Building Wall

- Building Roof

- Cold Storage

- Other Applications (e.g., Data Centres, Floor and Deck, etc.)

- By End-user Industry

- Residential

- Commercial

- Industrial and Institutional

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping SIP use cases in residential and non-residential construction and then aligning them to public construction and energy-efficiency signals. We relied on sources such as the US Census Bureau (construction spending), US Energy Information Administration (heating and cooling intensity context), and the International Energy Agency for building energy and insulation direction at a high level.

To ground material and trade signals, references were taken from sources such as UN Comtrade for cross-border flows of relevant insulation and panel components, along with USITC data where applicable for import and tariff context. We also reviewed building-code and energy-standard references (such as IECC-related publications) to understand when SIP adoption becomes more likely, and then we cross-checked with company filings, investor presentations, and credible construction press to validate demand language and capacity additions. For company-level financial context and patent activity, paid subscriptions covering company intelligence and patent databases were used selectively. The desk sources listed here are not exhaustive, and many additional public documents were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how SIPs are priced and shipped in practice, and where adoption is concentrated by application (walls, roofs, floors) and by build type (new build vs retrofit). We spoke with manufacturers, distributors, building-envelope contractors, and design-side experts across APAC, EMEA, and the Americas so gaps from desk inputs could be closed and key assumptions could be sanity-checked before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 17% | APAC: 44% |

| Mid tier: 44% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 17% | Managers: 50% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where construction activity and building-envelope demand signals are translated into a realistic SIP addressable pool, and then converted into value using region-specific pricing and adoption rates. In practice, the model starts with indicators like new housing starts and commercial floor space additions, and then applies SIP penetration by application (wall, roof, floor) based on code push, prefab activity, and contractor availability.

To keep totals realistic, we corroborated the outputs with selective bottom-up approximations, such as sampled price per panel or price per square foot paired with estimated installed area, and manufacturer shipment and channel feedback gathered during interviews. Inputs that were tracked (illustrative) include OSB and foam insulation price direction, labor availability and off-site construction share, heating and cooling efficiency targets, and observed lead times for panel delivery, which typically move faster than general building materials when project cycles tighten.

Forecasts were developed using scenario analysis, where base, conservative, and faster-adoption cases were tied to a small set of drivers that primary respondents could comment on confidently, mainly construction starts, code enforcement intensity, and relative cost premium versus stick-built assemblies. When bottom-up signals were missing for smaller countries, gaps were handled through proxy penetration rates and regional price ladders, followed by a final check against construction spending directionality so the curve stays believable.

Data Validation & Update Cycle

Each major input was checked in at least two ways, first against an independent public signal and then against what respondents see in the field, which helps reduce single-source bias. Outliers were flagged when implied SIP spend per project or per square foot drifted away from typical ranges, and those cases were reworked before the market total was locked.

A multi-step internal review is followed, where assumptions, math, and year labels are checked by another analyst before sign-off. The report is refreshed annually, and if a material event happens (like a sharp swing in OSB or insulation pricing, a code change, or a visible capacity shift), an interim update is triggered. Before delivery, a final pass is completed so the latest inputs are reflected in the published numbers.

Mordor Intelligence's Structural Insulated Panels Market Sizing Compared With Other Published Estimates

Published estimates for SIPs can look far apart even when they use similar growth rates, because the counted products and use cases are not always the same. Differences usually come from what is treated as a SIP versus an insulated panel, which year is chosen as the base, and how pricing is converted across regions.

The main gap comes from mixing structural building-envelope SIPs with broader insulated panel categories used in cold storage or general cladding, and Mordor Intelligence counts value only when the panel is a load-bearing SIP supplied for wall, roof, or floor assemblies, which keeps the modeled demand tied to building activity and enclosure adoption patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 623.16 M (2026) | |

| Industry Research Portal A | USD 12.50 B (2024) | This figure appears to use a much wider product perimeter that likely blends SIPs with non-structural insulated panels, and it also anchors sizing to a different base year, which lifts totals before forecasting even starts. |

| Global Consultancy B | USD 12.65 B (2025) | The scope seems to include additional applications such as cold storage panels alongside building-envelope demand, and the use of a separate base year with a longer forecast window can compound currency timing and pricing assumptions. |

The spread in values is mainly explained by scope selection and base-year setup, rather than a disagreement that SIP adoption is growing. By keeping the definition limited to load-bearing SIPs used in building envelopes and by cross-checking penetration and pricing through field inputs, the estimate stays traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

How fast is global demand for structural insulated panels growing?

Global revenue is advancing at a 6.22% CAGR from 2026 to 2031, moving from USD 623.16 million to USD 842.62 million.

Which product core dominates insulated panel sales?

Expanded polystyrene commands 79.94% share because it offers the best cost-to-R-value balance for residential projects.

What drives adoption of panels in cold-storage facilities?

Panels tighten airtightness and cut refrigeration energy by more than 20%, delivering quick paybacks for grocers and pharmaceutical distributors.

Why are builders shifting toward noncombustible panel skins?

Urban fire-safety codes and wildfire exposure favor fiber-cement, steel, or magnesium-oxide facings that achieve Class A ratings without additional barriers.

Page last updated on: