Roofing Membranes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.87 Billion |

| Market Size (2031) | USD 13.86 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

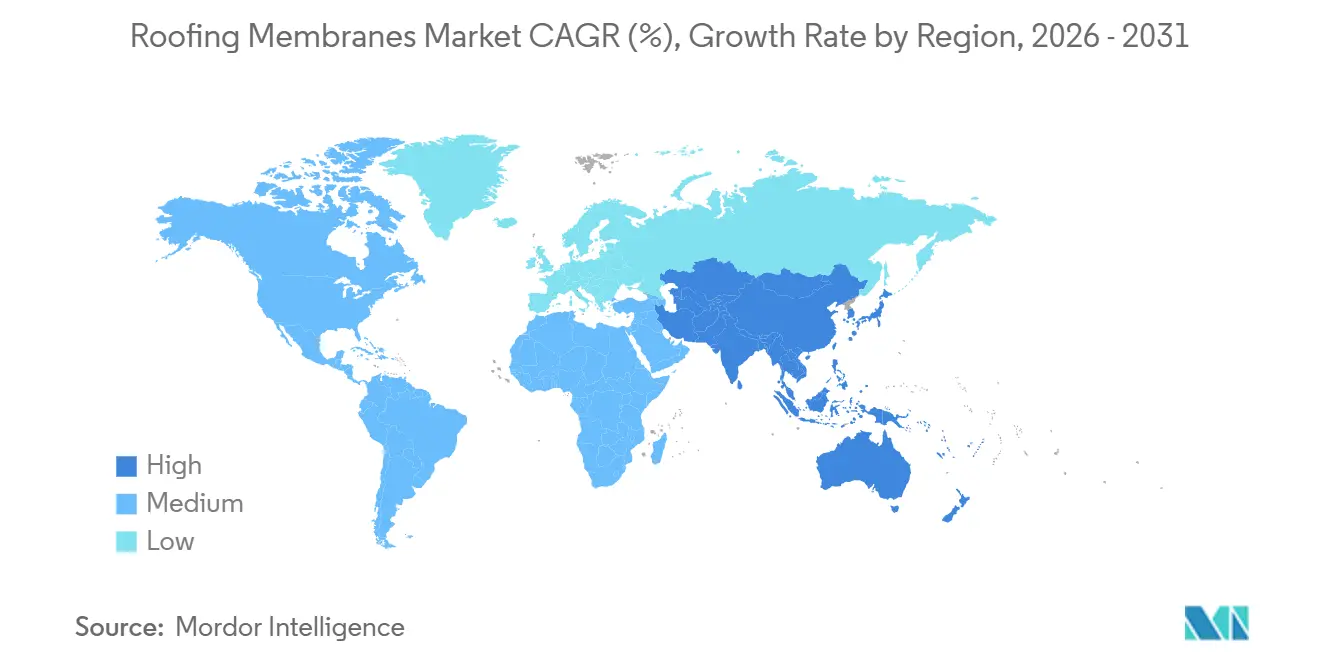

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Roofing Membranes Market Analysis by Mordor Intelligence

The Roofing Membranes Market size was valued at USD 10.36 billion in 2025 and is estimated to grow from USD 10.87 billion in 2026 to reach USD 13.86 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Rising code-mandated cool-roof reflectance, growth in modular construction, and the accelerating shift toward solar-ready rooftops are keeping demand for single-ply sheets and fluid-applied systems on a steady upward trajectory. Liquid-applied acrylic and silicone chemistries keep gaining share because they deliver seamless coverage, comply with volatile-organic-compound limits, and can be sprayed over existing substrates without full tear-offs, trimming project schedules across constrained labor markets. Fully adhered assemblies are displacing ballast in hurricane- and seismic-prone corridors, driven by insurers that reward higher wind-uplift ratings with premium discounts. Asia-Pacific leads volume growth, supported by China’s Belt and Road construction pipeline and India’s smart-city housing surge, while North America benefits from data-center, warehouse, and cold-storage investment that prioritizes reflective membranes to lower HVAC loads. Stringent fire and chemical regulations in Europe and parts of Asia are widening the gap between global formulators that control polymer R&D and smaller converters that rely on toll-blended resins.

Key Report Takeaways

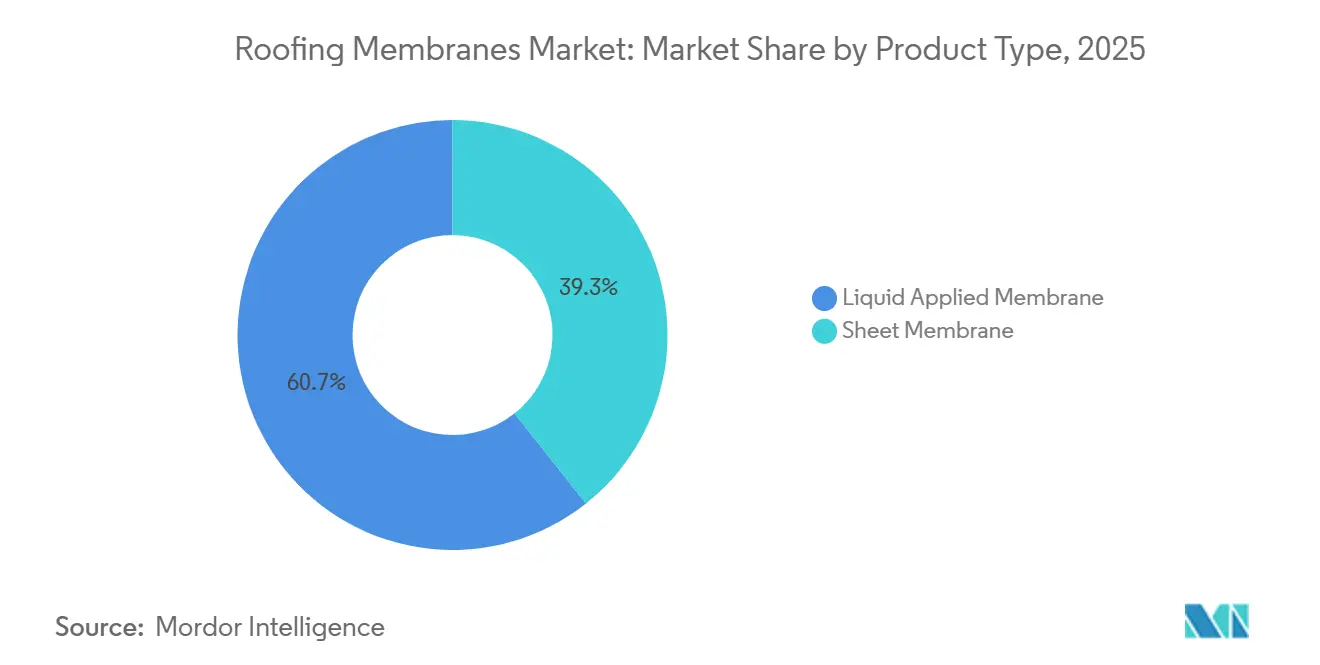

- By product type, the liquid-applied membranes segment held a 60.66% revenue share in 2025 and is expected to expand at a 5.34% CAGR during the forecast period (2026-2031).

- By installation type, fully adhered systems accounted for 46.78% of 2025 revenue and are projected to grow at a 5.22% CAGR during the forecast period (2026-2031).

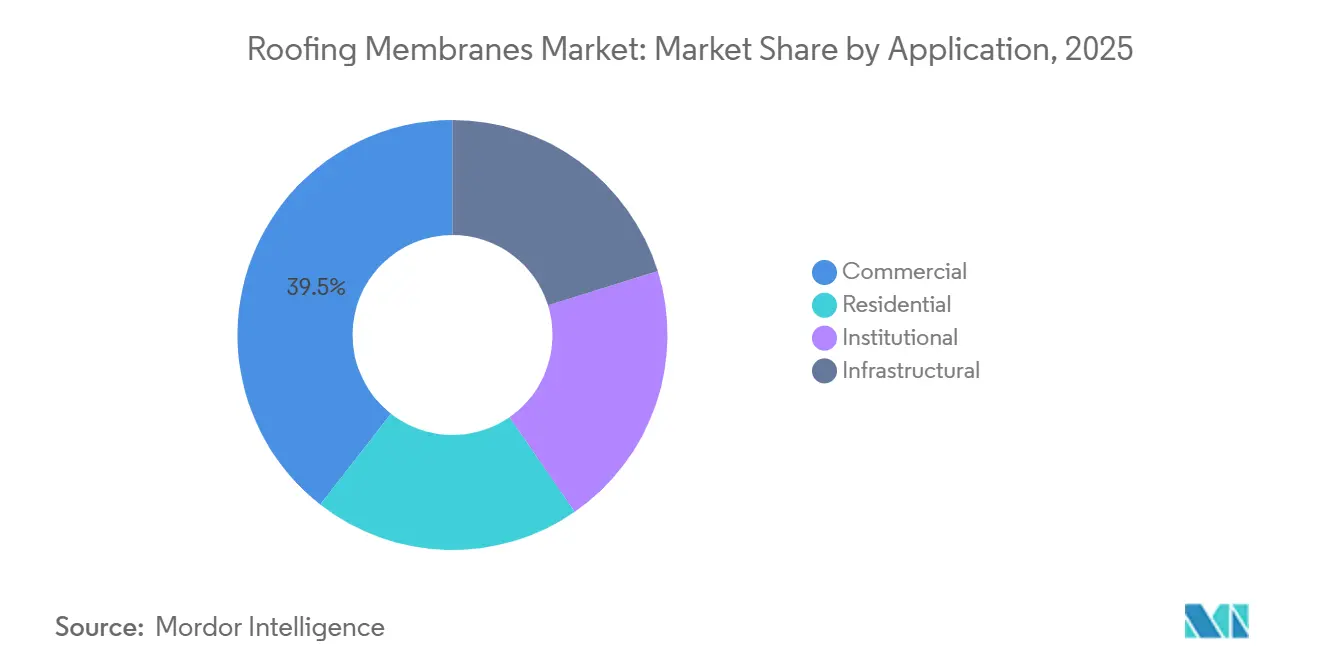

- By application, the commercial buildings segment accounted for a 39.45% share of the global roofing membranes market in 2025, growing at a 5.57% CAGR during the forecast period (2026-2031).

- By geography, the Asia-Pacific region commanded 45.56% of the revenue in 2025 and is expected to grow at a rate of 6.33% annually during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Roofing Membranes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for cool-roof compliance and energy-code stringency | +0.8% | North America, Europe, APAC (China, Japan, South Korea) | Medium term (2-4 years) |

| Expansion of green-building certification programs | +0.7% | Global, with concentration in North America, Western Europe, and APAC urban centers | Long term (≥ 4 years) |

| Construction boom in emerging economies | +1.2% | APAC (India, ASEAN, China), Middle East (Saudi Arabia, UAE), South America (Brazil) | Short term (≤ 2 years) |

| Rooftop-solar retrofit creating need for reflective membranes | +0.6% | Europe (Germany, Spain, Italy), North America (California, Texas), APAC (China, India) | Medium term (2-4 years) |

| Prefabricated modular roof-kit adoption accelerating membrane demand | +0.5% | North America, Western Europe, APAC manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Cool-Roof Compliance and Energy-Code Stringency

Building-energy standards in California, the International Energy Conservation Code, and China’s GB 55015-2021 are tightening reflectance thresholds, effectively disqualifying darker elastomeric products and shifting specifications toward white TPO, PVC, and high-albedo liquid coatings. Title 24’s 2025 update raised minimum aged solar reflectance, prompting rapid adoption of acrylic and silicone systems that achieve Solar Reflectance Index scores above 100 while sidestepping costly tear-offs[1]California Energy Commission, “2025 Title 24 Building Energy Efficiency Standards,” energy.ca.gov. Similar mandates in Sun Belt U.S. states and hot-summer Chinese provinces are sustaining premium pricing for reflective chemistries. Compliance deadlines have forced distributors to widen inventories of light-colored rolls and low-VOC primers to avoid project delays during permitting. Manufacturers that market CRRC-listed products with documented aged-value retention now win close-rate advantages on public-bid work in schools, hospitals, and government offices.

Expansion of Green-Building Certification Programs

LEED v5, BREEAM International 2024, and India’s GRIHA v5 have moved beyond reflectance, layering in credits for embodied-carbon reduction and verified environmental product declarations. Specifiers increasingly demand membranes containing recycled content, bio-based polyols, or water-blown foams, creating a dual metric of cool-roof performance plus life-cycle transparency. Global chemical majors that publish ISO 14025-aligned EPDs are qualifying for preferred-supplier status on multinational corporate campuses. The convergence of rating systems is standardizing submittal formats, cutting consultant costs, and accelerating bid evaluations because comparable LCA data are now available across most single-ply and liquid lines[2]U.S. Green Building Council, “LEED v5 Technical Guide,” usgbc.org.

Construction Boom in Emerging Economies

Saudi Arabia’s Vision 2030 giga-projects, the UAE pipeline, India’s National Infrastructure Program, and ASEAN industrial-park development triggered spot shortages for polyolefin films, polyester scrims, and polyisocyanurate insulation during 2025. Global producers responded by debottlenecking lines in China, Indonesia, and India, yet lead times for specialty cool-roof grades stretched to eight weeks at peak. Regional governments are bundling energy-efficiency and waterproofing mandates in public tenders, pushing even budget-sensitive housing segments to specify reflective EPDM or cost-optimized acrylic top-coats.

Rooftop-Solar Retrofit Creating Need for Reflective Membranes

The EU’s Energy Performance of Buildings Directive and California’s updated Solar Equipment Lists require solar-ready substrates, reinforcing white TPO and PVC as the default membranes in retrofit PV installations. Field studies confirm 10°C-15°C reductions in module operating temperature, boosting array output by up to 4%, which offsets the 5%-10% premium these membranes command versus black EPDM. Ballasted roofs now face structural constraints when overlaid with crystalline-silicon panels, spurring conversions to fully adhered sheets that distribute weight evenly. Reflective membranes, therefore, serve both energy and structural compliance, a dual benefit resonating with asset-management firms that must meet ESG targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent fire-safety and VOC/REACH regulations | -0.4% | Europe, North America, APAC (Japan, South Korea) | Medium term (2-4 years) |

| Shortage of certified single-ply installers | -0.5% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Competition from spray-applied continuous-roof coatings | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Fire-Safety and VOC/REACH Regulations

European Broof(t1) fire classifications, California’s 50 g/L VOC cap for roof coatings, and the EU REACH PFAS restrictions are driving reformulation costs upward and fragmenting product portfolios. Manufacturers must finance multiple full-scale EN 13501-1 tests for each membrane-insulation-deck combination, hampering cross-border product portability. Shifts to non-fluorinated surfactants have raised raw-material input costs up to 18%, prompting selective price surcharges across polyurethane and acrylic lines. Fast-to-market regional converters lacking in-house R&D are increasingly sourcing from multinational toll blenders, shrinking margins.

Shortage of Certified Single-Ply Installers

North America and Western Europe face an aging installer base and insufficient apprenticeship enrollments. The median U.S. roofing mechanic age reached 48 years in 2025, while certification enrollment for programs such as RCI’s Registered Roof Observer declined by 14%. Tight labor is inflating fully adhered TPO installation costs to USD 9-12 per square foot, eroding the delta between sheet systems and spray polyurethane foam. In response, manufacturers are rolling out self-adhered rolls and induction-weld protocols that reduce skilled-labor minutes per square, yet productivity gains have only partly offset wage escalation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Formulations Dominate Retrofit Applications

Liquid-applied systems secured 60.66% revenue in 2025 and are projected to advance at a 5.34% CAGR through 2031. That scale translates into the single largest portion of the Roofing Membranes market size because acrylic and silicone coatings can be installed over existing substrates, satisfy VOC rules, and achieve CRRC-listed reflectance without seams. Acrylics remain the volume leader due to low cost and UV stability, while polyurea’s rapid 15-second set time is unlocking plaza-deck and parking-garage use cases where fast return to service is critical. Sheet membranes claimed the remaining revenue, still favored for new-build logistics halls where large planes allow efficient roll-out. Thermoplastic polyolefin is steadily eroding legacy PVC share in North America, supported by formulations such as Carlisle’s Sure-Weld TPO that deliver ASTM D5034 tensile strengths beyond 350 lbf/in. EPDM maintains relevance in sub-zero climates, though its dark surface conflicts with cool-roof rules. Specialty self-adhesive bitumen rolls are expanding among European residential re-roofing, while high-density polyethylene films are carving green-roof niches due to root-barrier properties.

Premium HDPE and light-weight TPO variants, such as IKO’s 1.2 kg/m² fleece products, are positioned to capture structural-capacity constrained retrofits. Price differentials will remain narrow as higher polymer costs are offset by reduced labor minutes per roof, preserving lifecycle cost parity across product families.

By Installation Type: Fully Adhered Systems Lead Wind-Uplift Performance

Fully adhered assemblies captured 46.78% share in 2025 and are on track for a 5.22% CAGR during the forecast period (2026-2031), giving them the largest single slice of the Roofing Membranes market share in hurricane-exposed coastal corridors. Factory Mutual Class 1-90 ratings obtained with low-rise polyurethane adhesives drive insurer acceptance for logistics hubs and data centers. Water-based acrylic bonding agents are gaining popularity in VOC-regulated states because they cure through evaporation and permit rapid trades handoff. Mechanically attached roofs are attractive in retrofit scenarios where deck conditions or budget preclude adhesives. Electromagnetic induction welding is cutting leak incidence by eliminating fastener penetrations, a feature showcased in GAF’s EverGuard Extreme TPO that achieved FM 1-120 ratings at 12-inch plate spacing. Ballasted assemblies suffer headwinds from wind-code tightening and PV load constraints. Hybrid configurations, the remaining 7%, are expanding in seismic zones because perimeter adhesion paired with mechanically fastened fields affords building-movement tolerance.

Demand dynamics favor fully adhered growth inside both new construction and retrofit solar markets, yet mechanically attached systems will remain indispensable where structural, moisture, or cost hurdles override adhesive benefits. All installation formats are converging on digital fastening-layout software and on-deck pull-test verification, tightening construction quality control and reducing warranty claims frequency.

By Application: Commercial Buildings Drive Volume Growth

Commercial facilities held a 39.45% share of the Roofing membranes market size in 2025 and are projected to grow at 5.57% during the forecast period (2026-2031). Warehouse and data-center developers favor white TPO or PVC sheets to comply with LEED v5 credits and to temper roof-surface temperatures; Microsoft’s Azure campuses in Arizona and Texas documented 18°C drops compared with gray membranes, cutting chiller loads. Cold-storage build-outs demand high-R-value assemblies exceeding R-30, supporting upselling of polyisocyanurate insulation laminates. Residential use is split between liquid-applied acrylic restorations on existing asphalt shingle roofs and self-adhesive bitumen rolls for low-slope multifamily complexes. Institutional facilities represented 18%, buoyed by US federal energy-upgrade budgets that earmark USD 1.2 billion for cool-roof retrofits. Infrastructure and industrial sites made up the remaining 15%, with polyurea and polyurethane liquid systems preferred for chemical resistance on water-treatment plants and process-facility decks.

Commercial demand will stay foremost as e-commerce logistics footprints expand, hyperscale cloud operators race to commission capacity, and cold-chain players retrofit older warehouses to higher insulation values. Residential share growth hinges on rebate programs for cool-roof shingle restoration, while institutional uptake will follow public-sector energy-performance mandates that dovetail with renewable-energy procurement strategies.

Geography Analysis

Asia-Pacific generated 45.56% of 2025 global revenues and is expected to rise at a 6.33% CAGR during the forecast period (2026-2031), adding the largest incremental Roofing membranes market size among regions. China’s Belt and Road contracts worth USD 66.2 billion and India’s USD 120 billion smart-city housing allocation underpin near-term demand for cost-effective EPDM and reflective TPO. Seismic-resilient mechanically attached assemblies secured 58% of Tokyo’s 2025 commercial reroof activity, reflecting heightened risk awareness after the 2024 Noto event. ASEAN public-private partnerships are driving fungal-resistant polyurethane coatings on industrial parks where humidity exceeds 80% year-round.

North America’s revenue in 2025 was held up by re-roofing cycles, hurricane-code dictate, and a wave of data-center and cold-storage jobs. Warehouse builders across Florida, Texas, and the Carolinas specify FM-rated fully adhered TPO to qualify for insurance credits. California’s Title 24 cool-roof rule sustains white membrane volume in the state’s USD 12 billion annual roofing spend. Mexico’s near-shoring manufacturing drive is pivoting to rapid-cure polyurea membranes in Nuevo León industrial zones, while Canadian residential refurbishments are switching to low-VOC acrylic coatings that postpone full tear-offs by a decade.

In Europe, the Renovation Wave aims to upgrade 35 million buildings by 2030, with rooftop solar mandates pushing reflective sheets. Germany installed 14.1 GW of rooftop PV in 2025, 62% on commercial roofs that needed TPO substrates to match 25-year PV warranties. France’s RE 2020 carbon caps are channeling interest toward bio-based liquid polyurethane, while Eastern European Cohesion Fund projects rely on EPDM and bitumen rolls for affordable housing. Turkish seismic reconstruction is boosting uptake of flexible mechanically attached systems.

In the Middle East and Africa, Saudi Vision 2030 giga-projects, the UAE's USD 792 billion pipeline, and South Africa’s renewable-energy facilities all prefer reflective membranes to moderate ambient heat. Saudi mass-housing uses peel-and-stick bitumen for rapid construction, whereas Dubai’s Estidama Pearl standards are driving TPO and PVC adoption. South America’s share is paced by Brazil’s Minha Casa Minha Vida housing, though macroeconomic volatility continues to constrain import supply, leaving local EPDM makers to meet budget-driven demand.

Mordor Intelligence provides coverage of the roofing membranes market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The Roofing Membranes market is moderately fragmented. Strategic differentiation rests on the formulation of intellectual property that meets evolving cool-roof, VOC, and fire codes; vertical integration into installation or service programs; and verifiable sustainability credentials such as closed-loop take-back schemes. White-space plays center on ultra-light sheets for structural-capacity-constrained retrofits, integrated photovoltaic membranes that eliminate racking, and circular-economy service models that sell leak-free uptime rather than material.

Roofing Membranes Industry Leaders

Carlisle SynTec Systems

GAF Materials LLC

Sika AG

Soprema Group

Standard Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Dencoat India, a player in building materials and surface coatings, introduced a new type of waterproofing membrane for roofs and other surfaces. The product, launched under the name Dencoat DPM, is aimed at industrial, commercial, and residential building applications.

- February 2025: Sika launched the Sarnafil AT FSH self-healing PVC membrane and SikaShield HB79 hybrid modified bitumen sheet for North American re-roofing applications.

Global Roofing Membranes Market Report Scope

Roofing membranes are flexible, watertight membranes or sheets crafted to seal flat or low-slope roofs. By offering a durable, seamless barrier, they shield structures from water damage, mold, and leaks. These systems play a crucial role in both commercial and select residential applications.

The Roofing Membranes market is segmented by product type, installation type, application, and geography. By product type, the market is segmented into liquid-applied membrane and sheet membrane. By installation type, the market is segmented into mechanically attached, fully adhered, ballasted, and other installation types. By application, the market is segmented into residential, commercial, institutional, and infrastructural. The report also covers the market size and forecasts for the market in 23 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Liquid Applied Membrane | Acrylic |

| Polyurethane | |

| Polyurea | |

| Others | |

| Sheet Membrane | Polyvinyl Chloride (PVC) |

| Ethylene Propylene Diene Monomer (EPDM) | |

| Thermoplastic Polyolefin (TPO) | |

| Self-adhesive Bitumen | |

| High-density Polyethylene (HDPE) | |

| Others |

| Mechanically Attached |

| Fully Adhered |

| Ballasted |

| Other Installation Types |

| Residential |

| Commercial |

| Institutional |

| Infrastructural |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Romania | |

| Poland | |

| Serbia | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Liquid Applied Membrane | Acrylic |

| Polyurethane | ||

| Polyurea | ||

| Others | ||

| Sheet Membrane | Polyvinyl Chloride (PVC) | |

| Ethylene Propylene Diene Monomer (EPDM) | ||

| Thermoplastic Polyolefin (TPO) | ||

| Self-adhesive Bitumen | ||

| High-density Polyethylene (HDPE) | ||

| Others | ||

| By Installation Type | Mechanically Attached | |

| Fully Adhered | ||

| Ballasted | ||

| Other Installation Types | ||

| By Application | Residential | |

| Commercial | ||

| Institutional | ||

| Infrastructural | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Romania | ||

| Poland | ||

| Serbia | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global size of roofing-membrane demand by 2031?

Spending is forecast to reach USD 13.86 billion in 2031, expanding from USD 10.87 billion in 2026 at a 4.97% CAGR over 2026-2031.

Which product category is expected to add the most square meters through 2031?

Liquid-applied acrylic, silicone, polyurethane, and polyurea systems will add about 760 million m² thanks to seamless installation over existing roofs and easy compliance with VOC limits.

Why are fully adhered assemblies gaining share over ballasted roofs?

Insurers favor their Factory Mutual wind-uplift ratings, and they avoid the structural dead-load penalties that ballast imposes on PV-ready retrofits, especially in hurricane and seismic zones.

Which region will contribute the largest incremental revenue between 2026 and 2031?

Asia-Pacific, led by China’s Belt and Road projects and India’s smart-city housing, is forecast to grow at a 6.33% CAGR and already accounts for 45.56% of 2025 revenue.

How are new regulations shaping membrane formulation trends?

Title 24, REACH PFAS restrictions, and Broof(t1) fire tests are forcing a switch to chlorine-free TPO, non-fluorinated surfactants, and low-VOC water-based adhesives, rewarding suppliers with strong in-house polymer R&D.

Page last updated on: