Global Gene Delivery Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

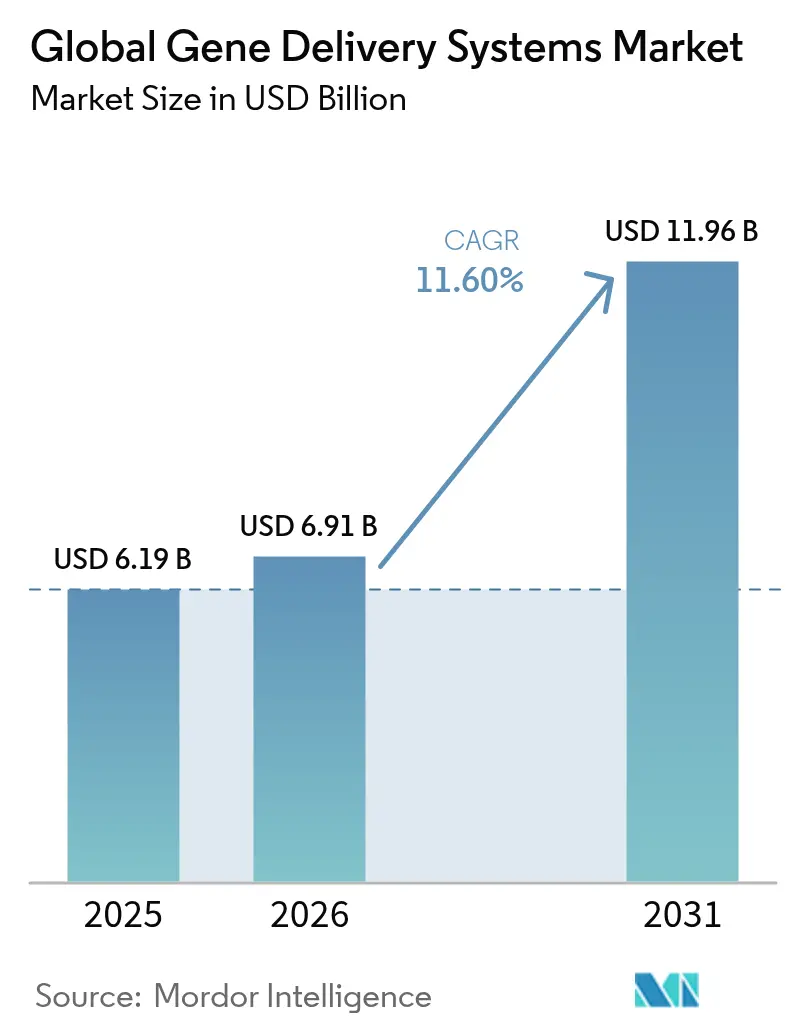

| Market Size (2026) | USD 6.91 Billion |

| Market Size (2031) | USD 11.96 Billion |

| Growth Rate (2026 - 2031) | 11.60% CAGR |

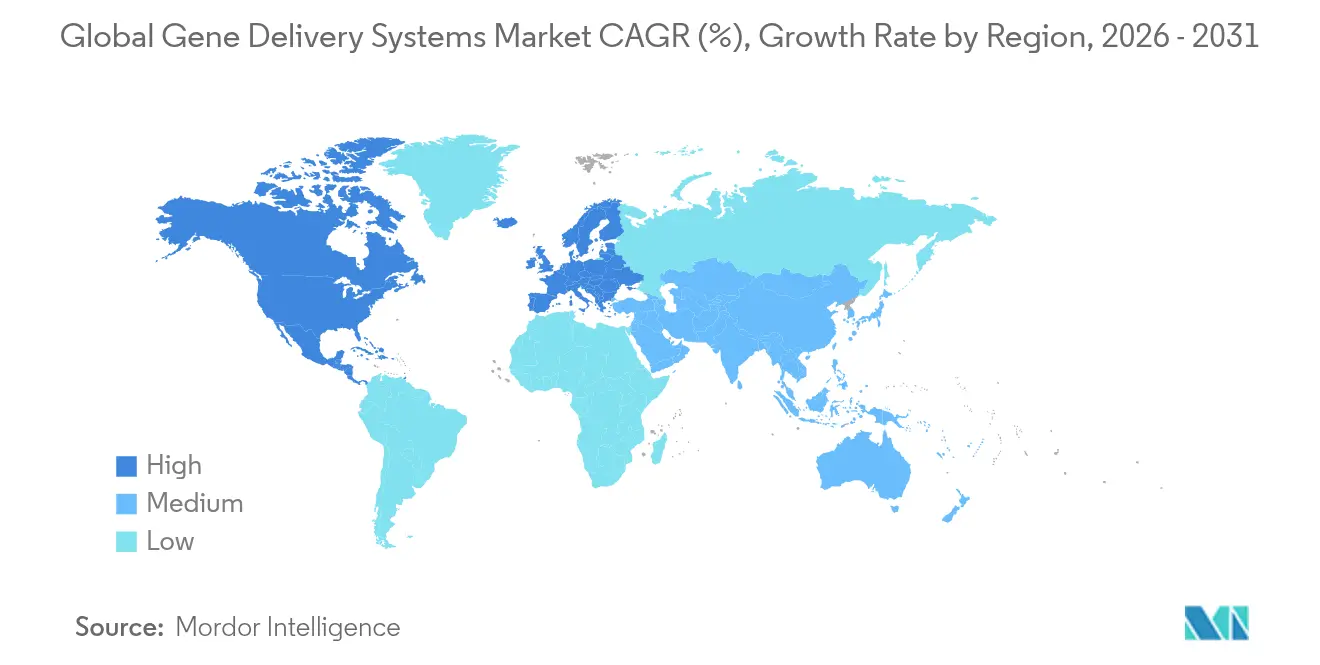

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Gene Delivery Systems Market Analysis by Mordor Intelligence

The gene delivery systems market size is expected to grow from USD 6.19 billion in 2025 to USD 6.91 billion in 2026 and is forecast to reach USD 11.96 billion by 2031 at 11.60% CAGR over 2026-2031. Momentum stems from the U.S. Food and Drug Administration’s clearances of transformative therapies such as CASGEVY and LYFGENIA for sickle cell disease, alongside large-scale capacity investments that reduce production bottlenecks. Demand is reinforced by oncology’s rapid adoption of viral vectors, infectious-disease programs leveraging novel lipid nanoparticles, and AI-enabled vector optimization that speeds candidate selection. Meanwhile, growing CDMO partnerships mitigate the 500% shortfall in commercial-scale plasmid and viral vector capacity, allowing developers to meet clinical timelines. Heightened venture funding, government incentives, and collaborative R&D hubs further enlarge the opportunity pool.

Key Report Takeaways

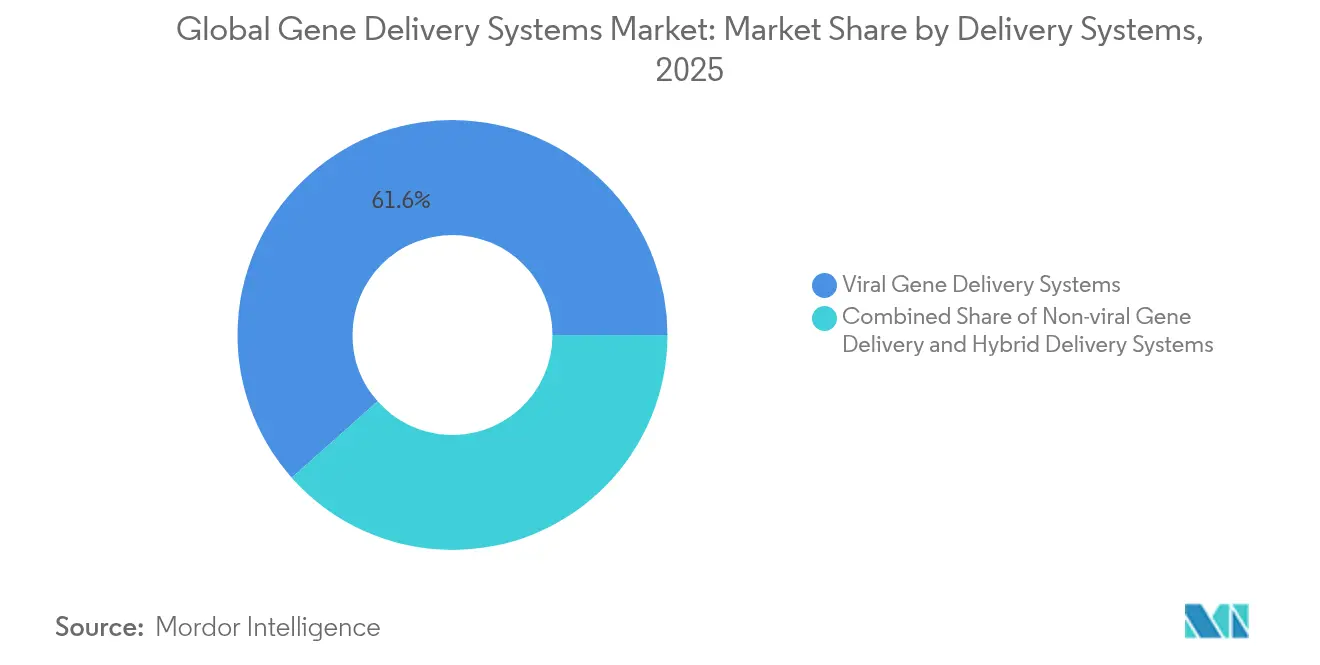

- By delivery system, viral vectors held 61.55% of 2025 gene delivery systems market share, whereas non-viral platforms registered the highest growth at a 12.98% CAGR to 2031.

- By application, oncology commanded 47.62% revenue share in 2025; infectious diseases are projected to advance at a 12.42% CAGR through 2031.

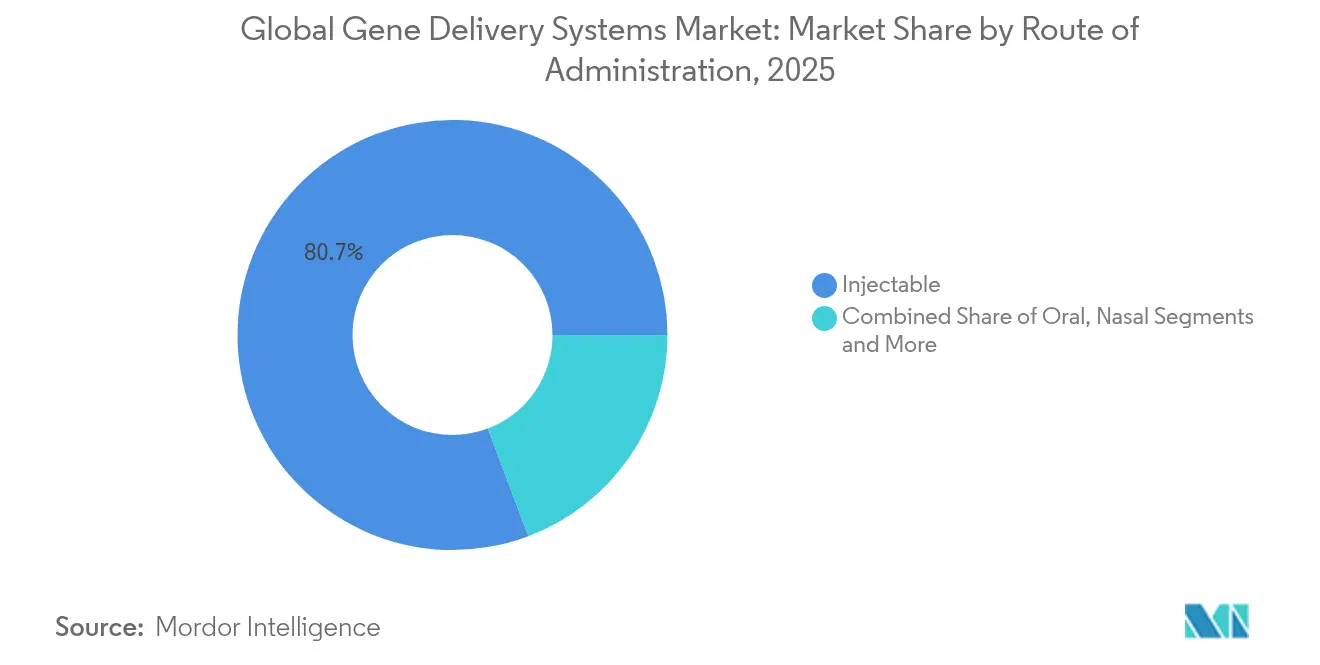

- By route of administration, injectable formats accounted for 80.74% of the gene delivery systems market size in 2025, while nasal delivery is set to grow at a 12.77% CAGR over the forecast period.

- By end user, biopharma and gene-therapy developers controlled 44.93% revenue share in 2025, with contract manufacturing & CDMOs recording the fastest expansion at 13.29% CAGR.

- By geography, North America led with 43.21% market share in 2025; Asia-Pacific is on track for the quickest rise at a 13.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gene Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic & lifestyle diseases | +2.8% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Rapid R&D advances by biopharma companies | +2.5% | North America, Europe, emerging Asia-Pacific hubs | Medium term (2-4 years) |

| Rising approvals of vector-based therapies | +2.2% | North America & EU leadership, Asia-Pacific following | Short term (≤ 2 years) |

| Venture and strategic funding inflows | +1.8% | Global biotech clusters | Medium term (2-4 years) |

| AI-driven vector design tools | +1.5% | Innovation centers in North America & Europe | Long term (≥ 4 years) |

| Regional CDMO build-out of plasmid capacity | +1.0% | Asia-Pacific expansion; North America & Europe modernization | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic & Lifestyle Diseases

Rising prevalence of genetic and chronic disorders fuels demand for curative gene therapies that replace lifelong symptom management with one-time molecular correction. Sickle cell disease affects 100,000 Americans, and hemophilia B impacts 1 in 40,000 males worldwide, motivating developers to pursue durable treatments. CASGEVY’s pivotal trial showed 96.7% of recipients free of vaso-occlusive crises for at least one year, validating the clinical and economic rationale for broader deployment. Success in hematologic indications accelerates exploration in cardiovascular, metabolic, and neurodegenerative diseases where conventional pharmacology offers limited long-term benefit.

Rapid R&D Advances by Biopharma Companies

Large pharmaceutical groups intensify gene-therapy pipelines through acquisitions and partnerships exceeding USD 1 billion each, such as Roche–Poseida and Novartis expansions in nervous-system disorders. AI-guided design shortens vector optimization cycles, enabling Regeneron, AstraZeneca, and CRISPR Therapeutics to progress multiple in-vivo programs simultaneously. This R&D velocity aligns with CDMO build-outs, ensuring production scalability for late-stage assets.

Rising Approvals of Vector-Based Gene Therapies

Regulatory momentum continues with 12 FDA-approved gene therapies as of 2024, including BEQVEZ for hemophilia B and Kebilidi for AADC deficiency. Europe’s EMA complements this trend through conditional authorizations and joint clinical assessments that harmonize evaluation across member states, accelerating multinational launches while preserving safety.

Venture and Strategic Funding Inflows

Despite macro-economic headwinds, deal activity remains robust; VectorBuilder raised USD 76 million for new GMP facilities, while Charles River Laboratories partnered with the Gates Institute on lentiviral production. Private-equity interest is evident in bluebird bio’s acquisition by Carlyle and SK Capital Partners, underscoring long-term confidence in commercial viability.

AI-Driven Vector Design Tools

Machine-learning platforms achieve 88-90% accuracy in predicting AAV capsid performance, dramatically improving selection of tissue-specific variants [1] Linus Meier, “Fit4Function Capsid Design,” nature.com . Stanford’s immune-safe zinc-finger proteins and the Broad Institute’s Fit4Function system showcase how computational approaches cut iteration cycles, potentially lowering manufacturing costs and enabling re-dosing strategies.

Regional CDMO Build-Out of Plasmid Capacity

Samsung Biologics, Fujifilm Diosynth, and GenScript collectively invest over USD 5 billion in large-scale plasmid and viral vector plants across Asia-Pacific and North America. Kaneka Eurogentec’s 1 kg GMP plasmid batch milestone and Takara Bio’s adoption of high-volume single-use bioreactors illustrate step-change throughput improvements that ease supply constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment & Reimbursement Costs | -2.5% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Safety / Immune-Response Concerns For Viral Vectors | -1.8% | Global regulatory oversight, clinical development | Medium term (2-4 years) |

| Complex Multi-Jurisdiction Regulatory Pathways | -1.2% | Global, particularly Europe-US-Asia coordination | Medium term (2-4 years) |

| Scarcity Of GMP-Grade Plasmid Manufacturing Slots | -0.8% | Global, concentrated in established manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment & Reimbursement Costs

Pricing peaks at USD 4.25 million for Lenmeldy and USD 2.2 million for CASGEVY, out-stripping payer budgets and slowing uptake despite lifetime health-economic benefits. Outcomes-based agreements and installment models offer relief but remain inconsistently adopted, creating access disparities, particularly in low- and middle-income countries.

Safety / Immune-Response Concerns for Viral Vectors

EMA’s pause of Elevidys trials after acute liver-failure events highlights ongoing immunogenicity challenges. Neutralizing antibodies limit AAV redosing and exclude patients with pre-existing immunity, pressuring developers to engineer stealth capsids and refine manufacturing controls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Systems: Viral Dominance, Non-Viral Acceleration

Viral platforms captured 61.55% of 2025 revenue, led by AAV vectors validated in recent approvals. Lentiviral systems grow in ex-vivo oncology and hemoglobinopathies despite production complexity. Non-viral approaches expand at 12.98% CAGR, propelled by lipid nanoparticles delivering CRISPR payloads with 90-100% encapsulation efficiency. Hybrid technologies blending viral precision with synthetic materials promise manufacturability and regulatory flexibility. Collectively, these dynamics sustain the gene delivery systems market’s transition toward diversified modalities.

Manufacturing capacity remains a pinch-point; industry surveys reveal potential lentiviral shortfalls without further scale-up. CDMOs respond with large-volume single-use bioreactors and continuous-flow purification that cut cycle times by 30%, narrowing the cost gap between viral and non-viral options.

By Application: Oncology Leads, Infectious Diseases Surging

Oncology held 47.62% of 2025 revenue, driven by CAR-T and solid-tumor gene therapies that demonstrably extend survival. Infectious-disease programs exhibit 12.42% CAGR through breakthroughs against HIV, herpes, and hepatitis B. Cardiovascular candidates advance with cBIN1 showing 30% functional improvement in large-animal models. Diabetes and pulmonary pipelines leverage inhaled and tissue-specific vectors that address longstanding delivery challenges. Orphan-disease portfolios benefit from accelerated review pathways, supporting a diverse set of rare-condition approvals.

By Route of Administration: Injectable Standard, Nasal Upswing

Injectable formats retained 80.74% share in 2025, reflecting regulatory familiarity and controlled dosing. Nasal delivery rises at 12.77% CAGR as AAV.CPP.16 and borneol-modified nanoparticles demonstrate high CNS penetration without systemic exposure . Oral, transdermal, and intra-ocular routes remain niche but evolve through protective coatings and device innovations that improve bioavailability.

By End User: Biopharma Core, CDMOs Scaling Fast

Biopharma developers commanded 44.93% revenue in 2025, retaining strategic control of IP and late-stage pipelines. CDMOs are the fastest-expanding cohort at 13.29% CAGR, buoyed by alliances such as Vertex–Lonza for CASGEVY and Catalent’s exclusive FDA-approved commercial AAV line . Academic institutes spearhead early discovery partnerships, while hospitals refine point-of-care manufacturing for autologous cell-based therapies.

Geography Analysis

North America led with 43.21% market share in 2025, backed by 12 FDA approvals in 2024 alone, deep venture capital pools, and cluster-based talent. Capacity additions like GenScript’s USD 224 million ProBio plant in New Jersey and Fujifilm Diosynth’s USD 1.2 billion North Carolina site underpin domestic manufacturing resilience. Europe follows with strong EMA oversight; Lonza’s Geleen facility supplies global CASGEVY demand, and 88% of approved ATMPs operate under additional monitoring, ensuring post-marketing safety.

Asia-Pacific posts the highest 13.46% CAGR to 2031 as Samsung Biologics invests USD 1.46 billion for 784,000 L of vector capacity and China’s biopharmaceutical sales could top 1.4 trillion yuan by 2029. Regulatory harmonization and local investment incentives attract multinational trials while fostering indigenous innovation.

Middle East & Africa and South America remain under-penetrated yet promising as vector costs fall and technology transfers expand. Only 5 of 32 approved therapies are currently accessible in LMICs, underscoring a need for collaborative financing and localized manufacturing to broaden treatment equity.

Competitive Landscape

Market concentration is moderate: established pharma leaders compete with specialized biotech innovators and AI-centric start-ups. Roche’s USD 1 billion Poseida acquisition and Novartis’ nervous-system investment reflect vertical expansion into delivery science.

Dyno Therapeutics and the Broad Institute’s machine-learning engines secure competitive edges by predicting capsid performance with 90% accuracy, enabling tailored vectors that improve efficacy while reducing dose-related toxicity.

Catalent’s status as the only CDMO with FDA-cleared commercial AAV lines positions it strategically amid soaring outsourcing demand. Meanwhile, Pfizer, Novartis, and Roche leverage patent exclusivities and manufacturing alliances to defend share. White-space opportunities persist in extra-hepatic targeting, cost-down process intensification, and combination therapies pairing gene editing with small-molecule modulation.

Global Gene Delivery Systems Industry Leaders

Pfizer, Inc.

Becton, Dickinson and Company

Takara Bio

Novartis AG

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: UniQure divested its Massachusetts gene-therapy plant to Genezen, which will manufacture Hemgenix, CSL Behring’s hemophilia B therapy.

- June 2024: Syncona merged Freeline and SwanBio into Spur Therapeutics and injected an additional USD 50 million to fund gene-therapy R&D.

- April 2024: Ascend Advanced Therapies acquired Beacon Therapeutics’ Florida CMC site, adding GMP capacity and process-development expertise.

- May 2023: Kytopen launched the Flowfect DiscoverTM early-access program, enabling high-throughput cell engineering for CRISPR, mRNA, and DNA at CDMOs and academic centers.

Global Gene Delivery Systems Market Report Scope

As per the scope of the report, gene delivery is the process of introducing foreign genetic material, such as DNA or RNA, into host cells.

The Gene Delivery Systems Market is segmented by Delivery Systems (Viral Gene Delivery Systems, Non-viral Gene Delivery Systems, and Combined Hybrid Delivery Systems), Applications (Oncology, Infectious Diseases, Cardiovascular Disorders, Diabetes, Pulmonary Disorders, Other Applications), Route of Administration (Oral, Injectable, Nasal, and Other Routes of Administration), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments

| Viral Gene Delivery Systems | Adenoviral Vectors |

| Lentiviral Vectors | |

| Retroviral Vectors | |

| Other Viral Vectors (AAV, HSV, etc.) | |

| Non-viral Gene Delivery | |

| Combined / Hybrid Delivery Systems |

| Oncology |

| Infectious Diseases |

| Cardiovascular Disorders |

| Diabetes |

| Pulmonary Disorders |

| Other Applications |

| Injectable |

| Oral |

| Nasal |

| Transdermal / Topical |

| Other Routes |

| Biopharma & Gene-therapy Developers |

| Contract Manufacturing & CDMOs |

| Academic & Research Institutes |

| Hospitals & Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Delivery Systems | Viral Gene Delivery Systems | Adenoviral Vectors |

| Lentiviral Vectors | ||

| Retroviral Vectors | ||

| Other Viral Vectors (AAV, HSV, etc.) | ||

| Non-viral Gene Delivery | ||

| Combined / Hybrid Delivery Systems | ||

| By Application | Oncology | |

| Infectious Diseases | ||

| Cardiovascular Disorders | ||

| Diabetes | ||

| Pulmonary Disorders | ||

| Other Applications | ||

| By Route of Administration | Injectable | |

| Oral | ||

| Nasal | ||

| Transdermal / Topical | ||

| Other Routes | ||

| By End User | Biopharma & Gene-therapy Developers | |

| Contract Manufacturing & CDMOs | ||

| Academic & Research Institutes | ||

| Hospitals & Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Global Gene Delivery Systems Market size?

The market is valued at USD 6.91 billion in 2026 and is projected to reach USD 11.96 billion by 2031.

Who are the key players in Global Gene Delivery Systems Market?

Pfizer, Inc., Becton, Dickinson and Company, Takara Bio, Novartis AG and F. Hoffmann-La Roche Ltd are the major companies operating in the Global Gene Delivery Systems Market.

Which is the fastest growing region in Global Gene Delivery Systems Market?

Infectious-disease programs are expanding at a 12.42% CAGR through 2031, powered by HIV and hepatitis B pipelines.

Which application segment is growing fastest?

In 2025, the North America accounts for the largest market share in Global Gene Delivery Systems Market.

Why are CDMOs becoming important in this market?

Developers face a 500% shortage in commercial-scale capacity; CDMOs fill the gap with specialized facilities and regulatory expertise.

Page last updated on: