Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

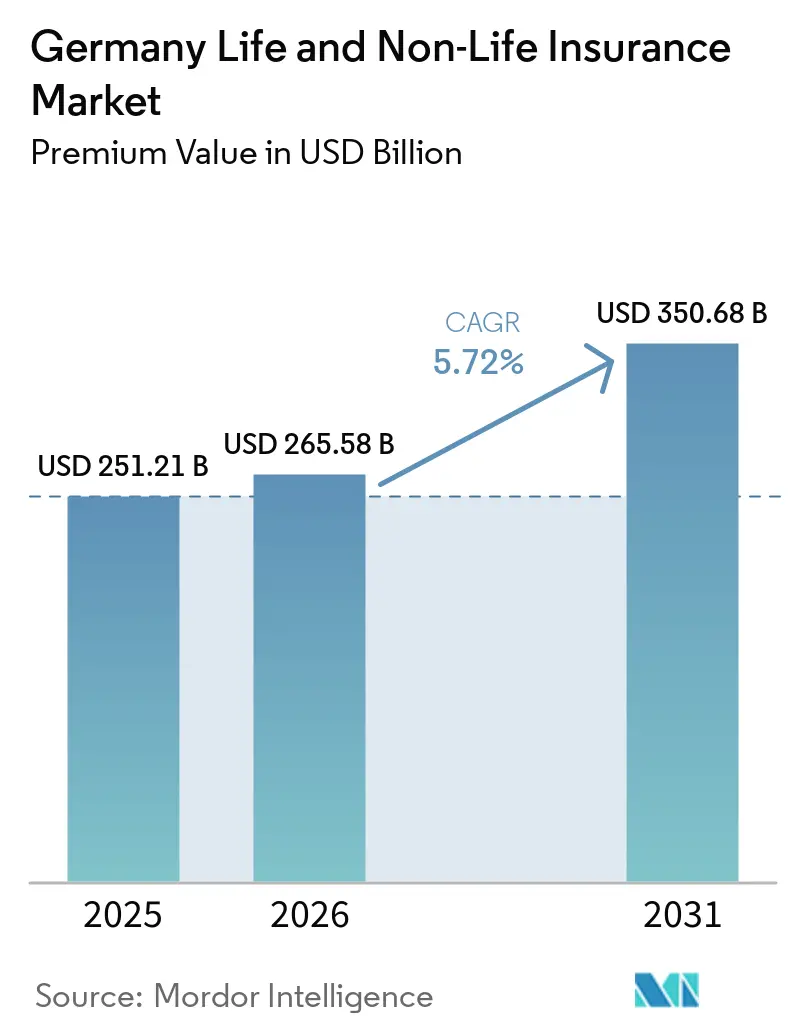

| Base Year Market Size (2025) | USD 251.21 Billion |

| Market Size (2026) | USD 265.58 Billion |

| Market Size (2031) | USD 350.68 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

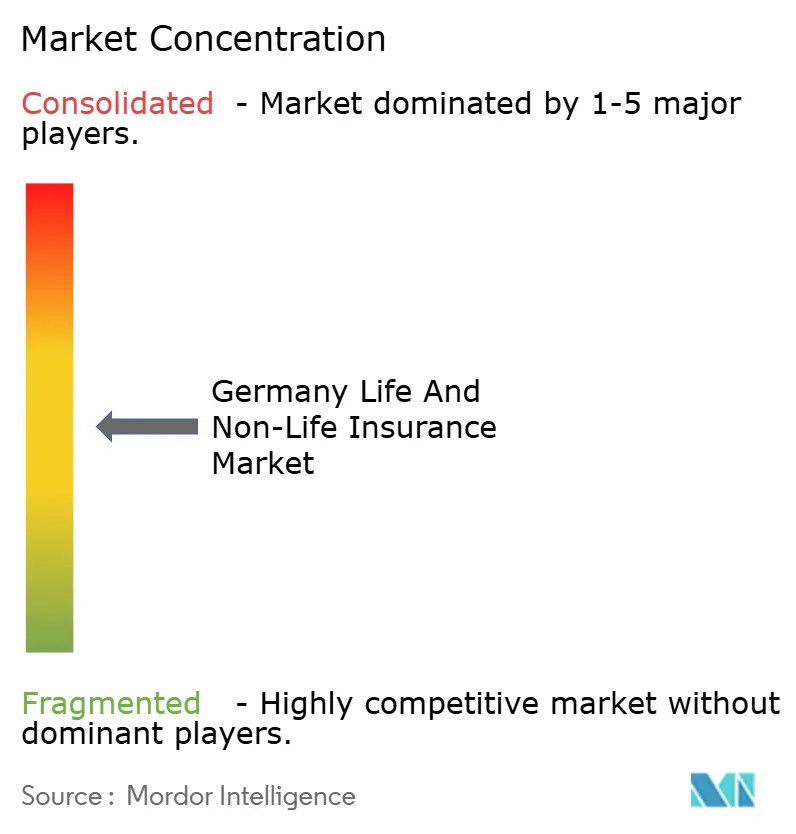

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Germany Life And Non-Life Insurance Market size in terms of premium value is projected to expand from USD 251.21 billion in 2025 and USD 265.58 billion in 2026 to USD 350.68 billion by 2031, registering a CAGR of 5.72% between 2026 to 2031.

The market’s expansion continues despite muted economic growth, supported by strong household balance sheets, mandatory social reforms, and sustained demand for risk-transfer products. Annuity and unit-linked life policies are gaining momentum as households look for inflation-resilient retirement solutions, while property and motor lines post solid premium gains in response to climate risk, higher repair costs, and elevated catastrophe losses. Growing digital engagement is reshaping distribution, with online aggregators, bancassurance portals, and embedded-insurance platforms steadily capturing premium share from traditional agents. Heightened regulatory focus on sustainability and capital efficiency under the revised Solvency II regime is accelerating the migration toward hybrid products with lower capital charges. Competitive intensity stays high because the market remains relatively unconcentrated, giving midsize carriers and InsurTech entrants room to grow.

Key Report Takeaways

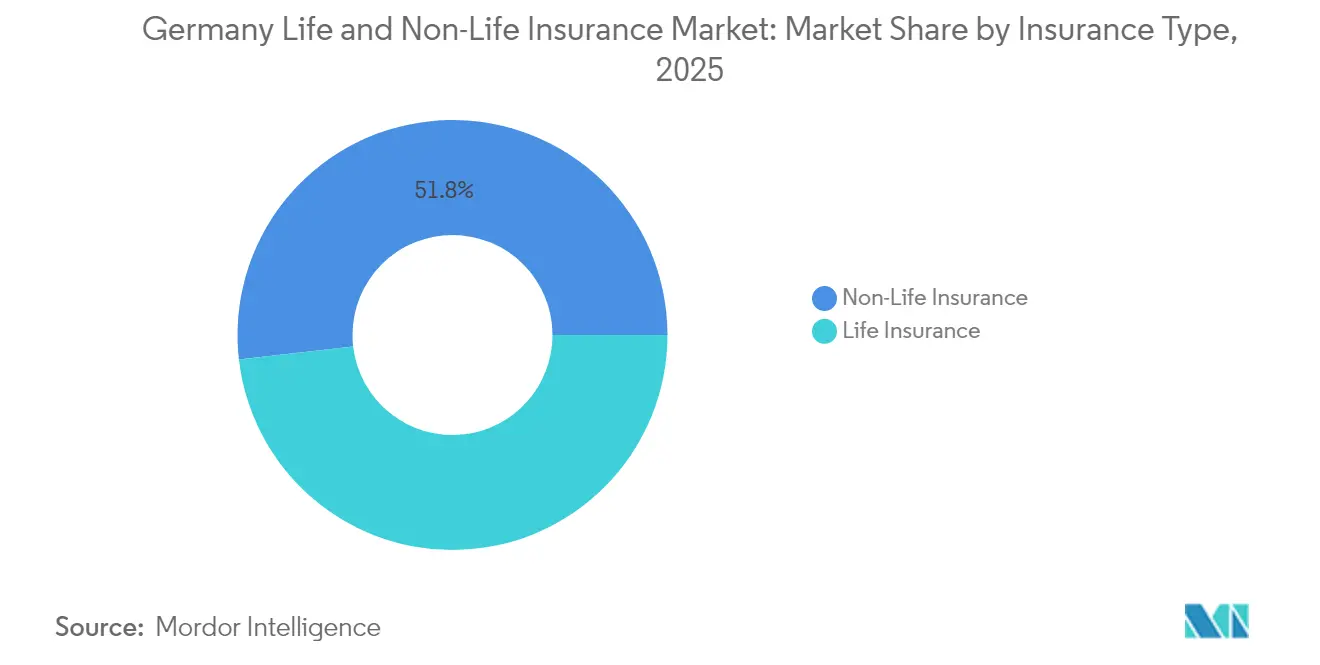

- By insurance type, non-life lines held 51.82% of the Germany life and non-life insurance market share in 2025, while annuity and unit-linked life products are projected to advance at a 5.88% CAGR to 2031.

- By distribution channel, independent agents and brokers led with 44.65% revenue share in 2025; digital-only and aggregator channels record the fastest growth at a 9.05% CAGR through 2031.

- By end user, retail households accounted for 59.25% share of the Germany life and non-life insurance market size in 2025, whereas the SME segment is expanding at a 5.06% CAGR over 2026-2031.

- By geography, West Germany captured 34.38% of the Germany life and non-life insurance market size in 2025, and East Germany shows the highest regional growth at a 4.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population boosting retirement & annuity demand | +1.8% | National, stronger in West and South Germany | Long term (≥ 4 years) |

| Solvency II capital optimisation influencing product mix | +1.2% | National, emphasis on major insurers | Medium term (2-4 years) |

| Digital adoption & InsurTech partnerships accelerating D2C | +1.5% | National, early gains in urban centres | Short term (≤ 2 years) |

| Increasing NatCat events elevating property-cat insurance penetration | +1.1% | National, higher impact in flood-prone regions | Medium term (2-4 years) |

| Mandatory long-term care reform expanding private supplementary health insurance | +0.9% | National, stronger uptake in high-income regions | Long term (≥ 4 years) |

| ESG & SFDR fueling green-insurance investment products | +0.7% | National, institutional focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Boosting Retirement & Annuity Demand

Germany's ageing population is driving growth in both life and non-life insurance markets, especially in the demand for retirement and annuity products. The statutory pension system, with a replacement rate capped at just 48% of average salaries, is widening the pension gap. This gap is pushing households towards private annuity solutions. Insurers are responding to the inadequacy of traditional guaranteed policies, once deemed sufficient but now falling short of inflation-adjusted income needs. They've introduced hybrid annuities, which ease capital strain by limiting guarantees and channeling remaining premiums into diversified asset portfolios[1]European Insurance and Occupational Pensions Authority, “Digitalisation Market Report 2025,” eiopa.europa.eu. This shift is bolstered by the forthcoming Generationenkapital fund, a state-backed initiative. This fund not only introduces public equity exposure but also paves the way for insurers to engage through administrative and longevity risk services. With the 67+ demographic on the rise, particularly in affluent western regions facing significant pension shortfalls, retirement-centric products are poised to lead the market, fundamentally altering Germany's insurance landscape.

Solvency II Capital Optimisation Influencing Product Mix

The January 2025 Solvency II refresh requires insurers to embed sustainability metrics, stricter look-through rules, and proportional reporting thresholds. A direct consequence is the pivot away from high-guarantee savings contracts toward unit-linked policies that attract lower solvency capital. Top carriers such as Munich Re display solvency ratios above 260%, using freed-up capital to price competitively and underwrite higher-yielding green assets[2]Munich Re, “Solvency and Financial Condition Report 2024,” munichre.com. Smaller mutuals benefit from proportional relief, enabling continued service of regional communities while still introducing ESG-labelled riders. Over the medium term, capital-light products will dominate the Germany life and non-life insurance market and reinforce a shift in investment strategy toward infrastructure debt, green bonds, and diversified equity mandates.

Digital Adoption & InsurTech Partnerships Accelerating D2C

Consumer preference for seamless digital journeys has prompted nearly every major insurer to integrate AI-enabled underwriting, automated claims triage, and personalized dashboards. The acquisition of finanzen.de by Allianz X signaled an arms-race for digital distribution capabilities. Urban customers increasingly initiate insurance purchases via price portals such as Check24, forcing incumbents to refine pricing algorithms and introduce real-time quotation APIs. Embedded insurance within retail checkouts and mobility apps is widening the addressable premium pool, while policy administration costs decline. As InsurTech capital inflows remain buoyant, partnership models proliferate, accelerating the speed at which new products reach market and enhancing customer experience across the Germany life and non-life insurance market.

Increasing NatCat Events Elevating Property-Cat Insurance Penetration

Floods in 2021 exposed Germany’s protection gap, prompting public debate over compulsory natural-hazard cover and intensifying household risk awareness. BaFin’s “Risks in Focus 2025” flags physical climate risk as a top supervisory concern. Uptake of extended building cover has risen, aided by improved risk zoning under the ZÜRS system and the launch of parametric solutions for quick flood-payouts. Reinsurers offer aggregate stop-loss treaties, enabling primary carriers to write additional capacity without breaching risk appetites. Consequently, property-cat premiums rise faster than GDP, and catastrophe reinsurance pricing power strengthens, affecting the non-life portion of the Germany life and non-life insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently low interest rates squeezing life-guarantee margins | -1.4% | National, stronger impact on traditional life insurers | Long term (≥ 4 years) |

| Intense motor-insurance price competition driven by telematics & portals | -0.8% | National, concentrated in urban markets | Short term (≤ 2 years) |

| BaFin commission caps constraining traditional intermediary channels | -0.6% | National, affecting all distribution channels | Medium term (2-4 years) |

| Shrinking young-adult cohort limiting pure-risk life-coverage growth | -0.5% | National, stronger impact in eastern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistently Low Interest Rates Squeezing Life Guarantee Margins

Long-dated guarantees continue to erode profitability, as reinvestment yields remain below legacy promise levels. Although ECB policy is beginning to normalize, average bond yields still trail the 2.25% [3]Geneva Association, “Low Interest Rate Environment and Life Insurance,” genevaassociation.orgaverage guarantees on older German contracts. Insurers mitigate strain through in-force management actions, back-book transfers, and surrender-value optimization . Yet, the drag on return on equity drives structural migration toward products where investment risk is partially borne by policyholders. Larger groups with strong asset-management arms diversify into private markets, but smaller mutuals face thinner buffers, constraining new-business growth within the Germany life and non-life insurance market.

Intense Motor-Insurance Price Competition Driven by Telematics & Portals

Price comparison engines have lowered switching frictions, turning motor insurance into a commodity. Direct writers and mutuals display combined ratios well below listed peers by leveraging agile IT and lean operations. Telematics programs, while improving risk segmentation, invite aggressive discounting that squeezes underwriting margins. Demand for advanced driver-assistance systems coverage and usage-based insurance grows, but average premiums trend down in competitive metropolitan areas. To offset erosion, carriers cross-sell roadside assistance and mobility-service subscriptions, yet margin recovery remains elusive in the motor slice of the Germany life and non-life insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Unit-Linked Products Drive Life Transformation

Life lines are reshaping rapidly. Annuities and unit-linked contracts together are expected to generate a 5.88% CAGR that outpaces overall market growth. Within the Germany life and non-life insurance market size of the life business, hybrid policies featuring partial guarantees attract risk-averse savers while easing capital strain on insurers. The non-life segment, which accounted for 51.82% of total premiums in 2025, enjoys support from rising property-cat and liability demand prompted by ESG compliance and evolving cyber threats.

Traditional endowment and whole-life products are redesigned with lower interest guarantees, allowing carriers to release capital under Solvency II. Growth pockets in non-life include cyber and environmental liability, both expanding at double-digit CAGRs as German corporates digitalize and face stricter disclosure mandates. Motor retains volume leadership but faces soft pricing, whereas commercial multi-risk and specialty engineering lines benefit from Germany’s advanced manufacturing sector. Consequently, the Germany life and non-life insurance market will remain balanced, with opportunities spread across both broad product buckets.

By Distribution Channel: Digital Aggregators Disrupt Traditional Models

Independent agents and brokers still wrote 44.65% of premiums in 2025, underscoring the importance of advisory services in complex pension and commercial lines. Nevertheless, digital-only and aggregator platforms are projected to lift their revenue share to nearly 16.4% by 2031 on the back of a 9.05% CAGR. This acceleration is visible in metropolitan areas, where consumers compare quotes on mobile devices before finalizing purchases.

Bancassurance gains momentum as retail lenders integrate insurance modules within online banking, giving them an edge in cross-selling term life, disability, and simple property cover. Embedded-insurance use cases—from airline ticket cancellation to smartphone warranties—are widening the premium base captured online. As a result, the Germany life and non-life insurance market will exhibit a dual-track distribution architecture: high-tech, automated flows for standardized risks, and advice-intensive channels for bespoke solutions.

By End User: SME Segment Accelerates Commercial Growth

Retail households remained the dominant buyer group with a 59.25% share of the Germany life and non-life insurance market size in 2025, reflecting Germany’s tradition of private provision for retirement, health co-payments, and household cover. Nonetheless, the SME customer base is the fastest-expanding, delivering a 5.06% CAGR through 2031 as companies confront cyber risk, supply-chain disruption, and ESG-linked liability exposures.

The Mittelstand’s digital transformation elevates demand for professional indemnity, cyber, and directors' & officers' liability policies. Government programmes encouraging industrial decarbonization spur interest in parametric weather cover and green-building insurance. Public institutions and non-profits adopt resilience frameworks, procuring catastrophe and climate-risk solutions. Overall, SME uptake enriches premium diversification and cements commercial lines’ importance to the Germany life and non-life insurance market.

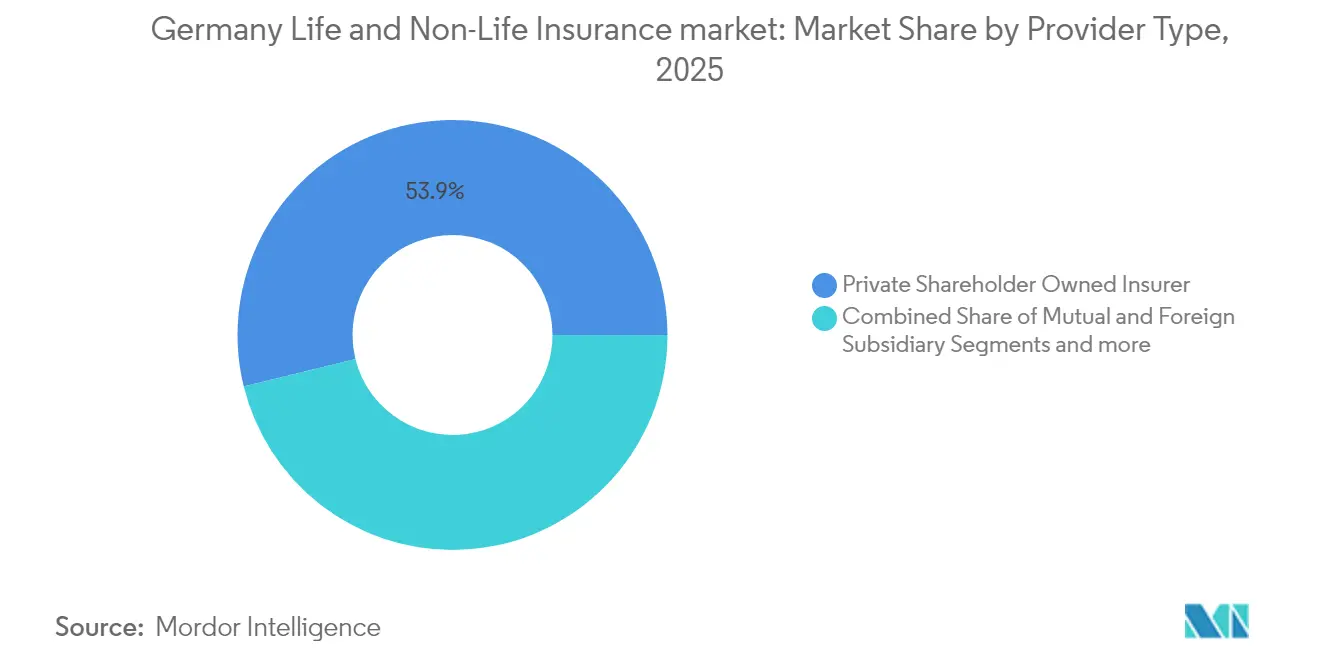

By Provider Type: Mutual Insurers Leverage Cost Advantages

Private shareholder-owned groups command scale, brand strength, and international diversification; however, regional mutuals and public-law insurers demonstrate lower expense ratios and strong community ties. Studies show mutual carriers’ average claims costs and operating expenses sit 2-3 percentage points below those of listed peers, translating into competitive motor and household rates.

Foreign subsidiaries such as Generali and Zurich bring specialized underwriting expertise, especially in specialty commercial lines and reinsurance. Cooperative banks’ insurance arms exploit cross-selling synergies, while digital natives focus on narrow product sets delivered via mobile apps. This provider diversity keeps margins tight and innovation high inside the Germany life and non-life insurance market.

By Premium Type: Regular Premiums Dominate Amid Flexibility Demand

More than 70% of life and long-term health contracts are written with regular premiums, matching household budgeting habits and providing insurers with reliable cash flow for asset-liability management. Single-premium sales rise in the run-up to retirement as affluent clients invest lump sums into immediate annuities or inheritance-planning wrappers.

Insurers introduce hybrid contribution options that allow ad-hoc top-ups without surrender penalties, appealing to self-employed professionals with fluctuating incomes. Flexible premium holidays and dynamic sum-assured riders improve retention, stabilizing lapse ratios. These product features embed versatility within the Germany life and non-life insurance market while preserving traditional risk-pooling economics.

Geography Analysis

West Germany, with its dense population and concentration of financial hubs, generated 34.38% of total premiums in 2025. The region boasts a sophisticated buyer base that favors customizable retirement and private-health products, sustaining higher average premiums per policy than any other area. Strong corporate clusters around Frankfurt and Cologne require complex commercial covers, including global programs and trade credit policies. Digital uptake is highest in these urban centres, enabling carriers to pilot AI underwriting and instant-issue motor products that later roll out nationwide.

East Germany is the fastest-growing territory, posting a 4.72% CAGR through 2031 as disposable incomes converge with Western levels. Rising vehicle ownership and increased mortgage activity spur motor and property demand. Insurers anchor new service centres in Leipzig and Dresden to serve expanding customer bases and leverage lower operating costs. Demographic differences—specifically an older average population—shape product mixes toward supplementary health and long-term care coverage, expanding regional relevance within the Germany life and non-life insurance market.

South Germany, encompassing Bavaria and Baden-Württemberg, benefits from a high concentration of industrial exporters, advanced automotive manufacturers, and technology leaders. These firms require sophisticated supply-chain risk, cyber, and environmental liability programmes, fostering demand for tailored specialty and engineering lines. Household wealth in Munich, Stuttgart, and Nuremberg supports strong penetration of capital-linked life products, often distributed via bancassurance channels of Landesbanks and cooperative banks.

North Germany, anchored by Hamburg’s maritime economy, exhibits elevated need for marine hull, cargo, and logistics liability cover. The large port ecosystem attracts international underwriters and reinsurers who inject competition into specialty lines. Low-lying areas near the North Sea face heightened flood risk, increasing uptake of extended natural-hazard endorsements and parametric flood products. Collectively, these regional nuances sustain balanced growth across the Germany life and non-life insurance market and limit over-reliance on any single state.

Competitive Landscape

Competition in the Germany life and non-life insurance market remains fierce because premium concentration is moderate. Allianz leads property-and-casualty with a high share, yet no single player dominates life, health, or commercial segments, leaving room for midsize specialists and Insurtech challengers. Large incumbents deploy sizeable digital budgets, modernizing core systems and building data lakes to enhance customer journeys and underwriting accuracy. Generali’s acquisition of Liberty Mutual’s European portfolio illustrates consolidation aimed at scaling and portfolio diversification.

Mutual groups such as Versicherungskammer and Debeka leverage local knowledge and low expenses to defend regional strongholds, while publicly listed Talanx pursues international expansion to mitigate domestic margin pressure. Insurtech entrants introduce usage-based micro-policies, embedded cover, and AI-driven claims automation that raise customer expectations market-wide. Reinsurers like Munich Re provide capital-efficient quota-share deals, enabling direct carriers to write additional catastrophe cover without breaching solvency limits. Competitive advantage increasingly hinges on access to granular data, algorithmic pricing, and ESG-aligned investment resources, rather than solely on scale.

Strategic plans in 2024-2025 include the rollout of parametric flood solutions, partnerships with telematics-data providers, and platform integrations with e-commerce merchants. Carriers embark on ecosystem initiatives that bundle insurance with home-automation devices, health-monitoring wearables, and mobility-subscription packages. The pivot beyond traditional risk transfer toward prevention and service monetization reshapes margins and aligns with regulators’ consumer protection agendas. Over the forecast period, players able to combine prudent capital management with customer-centric digital models will outpace rivals in the Germany life and non-life insurance market.

Germany Life and Non-Life Insurance Industry Leaders

Allianz SE

Munich Re

Talanx AG (HDI)

R+V Versicherung AG

Debeka Gruppe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BaFin released “Risks in Focus 2025,” listing climate hazards and geopolitical tensions as top concerns for insurers.

- January 2025: The revised Solvency II framework entered into force, tightening sustainability requirements and simplifying low-risk-undertaking reporting.

- November 2024: EIOPA’s digitalization report showed 50% AI uptake in non-life and rapid cyber-insurance adoption

- March 2024: BaFin issued a new Circular on the Prudent Person Principle, mandating double-materiality ESG assessments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German life and non-life insurance market as the combined direct gross written premiums collected by domestic and foreign carriers on policies covering life protection, savings, annuity, motor, property, liability, health supplemental, accident, marine, aviation, and transport risks. Values are expressed in current-year US dollars.

Scope Exclusion: Reinsurance transactions, cross-border covers booked outside Germany, and micro-credit guarantee schemes are not counted.

Segmentation Overview

- By Insurance Type

- Life Insurance

- Term Life

- Endowment & Whole Life

- Unit-Linked / Investment-Linked

- Annuity & Pension

- Others

- Non-Life Insurance

- Motor

- Comprehensive

- Third-Party Liability

- Property

- Residential

- Commercial & Industrial

- Liability (General)

- Health Supplementary

- Accident & Disability

- Marine, Aviation & Transport

- Others

- Motor

- Life Insurance

- By Distribution Channel

- Agents

- Brokers

- Bancassurance

- Direct Online

- Aggregators / Comparison Portals

- Affinity & Partnerships

- By End User

- Individuals

- Corporates & SMEs

- Public Institutions & Non-Profits

- By Premium Type

- Single Premium

- Regular Premium

- By Provider Type

- Private Shareholder-Owned Insurers

- Mutual & Cooperative Insurers

- Foreign Subsidiary Insurers

- By Region

- North Germany (HH, SH, HB, NI)

- West Germany (NW, HE, RP, SL)

- South Germany (BY, BW)

- East Germany (BE, BB, MV, SN, ST, TH)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriters, tied-agent heads, online aggregators, and pension consultants across Bavaria, North Rhine-Westphalia, Saxony, and Hamburg. Insights on lapse behavior, digital channel uptake, and emerging cyber or green covers helped us fine-tune distribution shares and growth assumptions reflected in surveys with policyholders and brokers.

Desk Research

We gathered baseline numbers from BaFin Jahresberichte, the German Insurance Association (GDV) Jahrbuch, Eurostat macro indicators, Bundesbank interest-rate data, and Swiss Re sigma plus Insurance Information Institute digests, which together outline premium pools and economic context. Carrier 10-Ks, rating reports, and D&B Hoovers snapshots revealed firm-level trends, while Bundestag papers on Solvency II updates and long-term-care reform clarified regulatory inflections. The sources cited are illustrative; many additional documents informed data collection, validation, and clarification.

Market-Sizing & Forecasting

We rebuilt the 2024 premium pool using a top-down approach that layers GDV line totals onto BaFin carrier disclosures, then confirmed results with selective bottom-up checks drawn from sampled average premium multiplied by policy counts in motor, supplemental health, and unit-linked life. Key variables such as real GDP growth, long-term Bund yields, the share of residents aged sixty-five and above, new-car registrations, and digital sales penetration feed a multivariate regression to project values through 2030. Scenario analysis captures interest-rate and catastrophe-loss swings, and any gaps in line-level data are bridged with three-year moving averages from Volza shipment proxies or Marklines vehicle sales where relevant.

Data Validation & Update Cycle

Outputs move through variance checks against GDV quarterly flashes, cross-analyst peer review, and a fresh sanity pass before release. Models refresh each year, with interim updates triggered by material events such as tax changes or severe natural catastrophes.

Why Mordor's Germany Life & Non-Life Insurance Baseline Commands Reliability

Published estimates differ because firms adopt varied premium definitions, currency bases, and refresh cadences. By flagging these drivers, we let users see why totals move.

Divergences typically stem from whether annuity flows sit inside life tallies, if accident and health ride within non-life, the treatment of reinsurance cessions, and the choice between net or direct premiums. Some publishers extend simple linear trends or single-currency conversions, whereas our team pairs real-time macro updates with expert-validated regression paths.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 251.21 B (2025) | Mordor Intelligence | |

| EUR 250 B (2024) | Regional Consultancy A | Excludes annuities, applies straight-line GDP uplift, lacks bottom-up checks |

| USD 245.46 B (2023) | Trade Journal B | Uses direct premiums before reinsurance, folds accident and health into non-life, provisional data set |

| USD 182.40 B (2022) | Global Consultancy C | Reports only general insurance, omits life lines, restated for IFRS 17 |

The comparison shows that shifts in scope or data vintage can swing totals by tens of billions. By grounding every assumption in transparent public sources and dual-track validation, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can trust year after year.

Key Questions Answered in the Report

What is the current size of the Germany life and non-life insurance market?

The market stands at USD 265.6 billion in 2026 and is forecast to reach USD 350.7 billion by 2031 at an 5.72% CAGR.

Which product segment is growing fastest?

Annuity and unit-linked life policies show the highest momentum, expanding at a 5.88% CAGR as savers seek inflation-resilient retirement options.

How are digital channels affecting distribution?

Digital-only and aggregator platforms post a 9.05% CAGR, steadily eroding the share of traditional agents and brokers, especially for motor and simple life policies.

Why are property catastrophe premiums rising?

More frequent floods and storms plus heightened public awareness have boosted demand for natural-hazard cover, lifting property-cat premium growth ahead of GDP.

Page last updated on: