LiDAR Drones Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

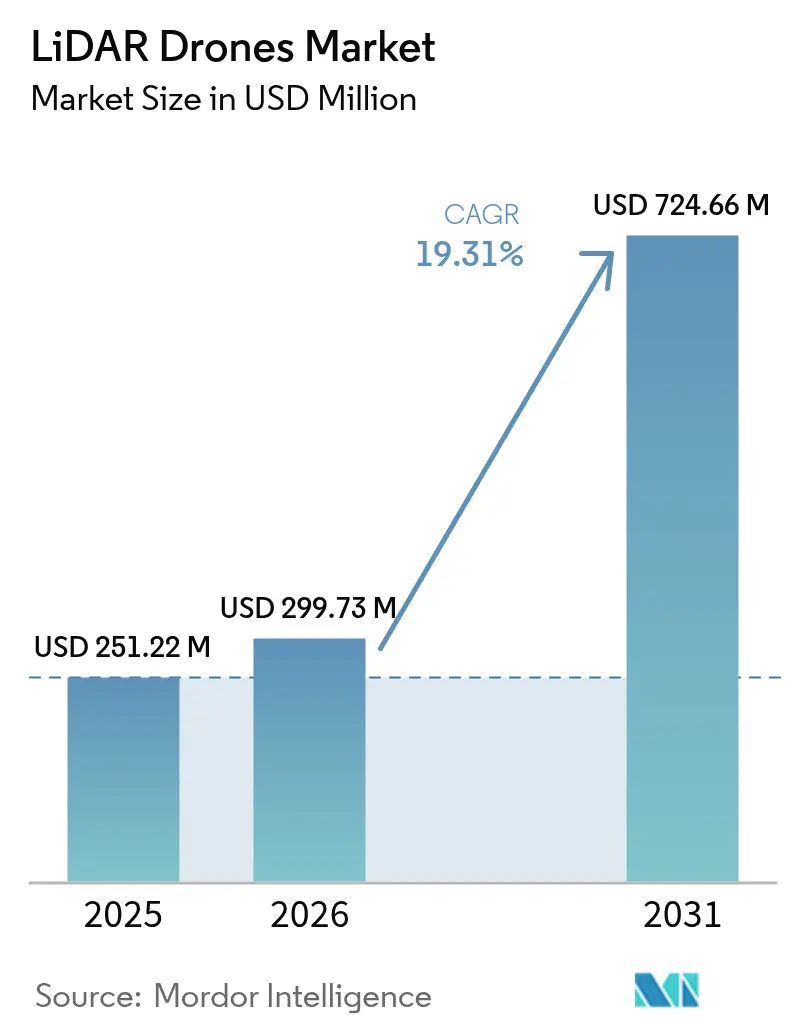

| Market Size (2026) | USD 299.73 Million |

| Market Size (2031) | USD 724.66 Million |

| Growth Rate (2026 - 2031) | 19.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

LiDAR Drones Market Analysis by Mordor Intelligence

LiDAR drone market size in 2026 is estimated at USD 299.73 million, growing from 2025 value of USD 251.22 million with 2031 projections showing USD 724.66 million, growing at 19.31% CAGR over 2026-2031. Solid-state cost breakthroughs below the USD 400 inflection point, supportive regulatory reforms in major air-space markets, and expanding demand for precision mapping across construction, agriculture, and energy underpin this expansion. Rotary-wing platform upgrades, cloud-native data pipelines, and integrated navigation units are widening the addressable user base, while lower-weight sensors are opening new urban and micro-mapping opportunities. Large infrastructure programs in North America, the European Union, and Asia-Pacific continue to allocate survey budgets toward unmanned systems, and methane-leak detection mandates are accelerating LiDAR payload uptake in the oil and gas sector. Hardware commoditization is steering value toward analytics software and LiDAR-as-a-Service offerings, reshaping competitive strategies and margins.

Key Report Takeaways

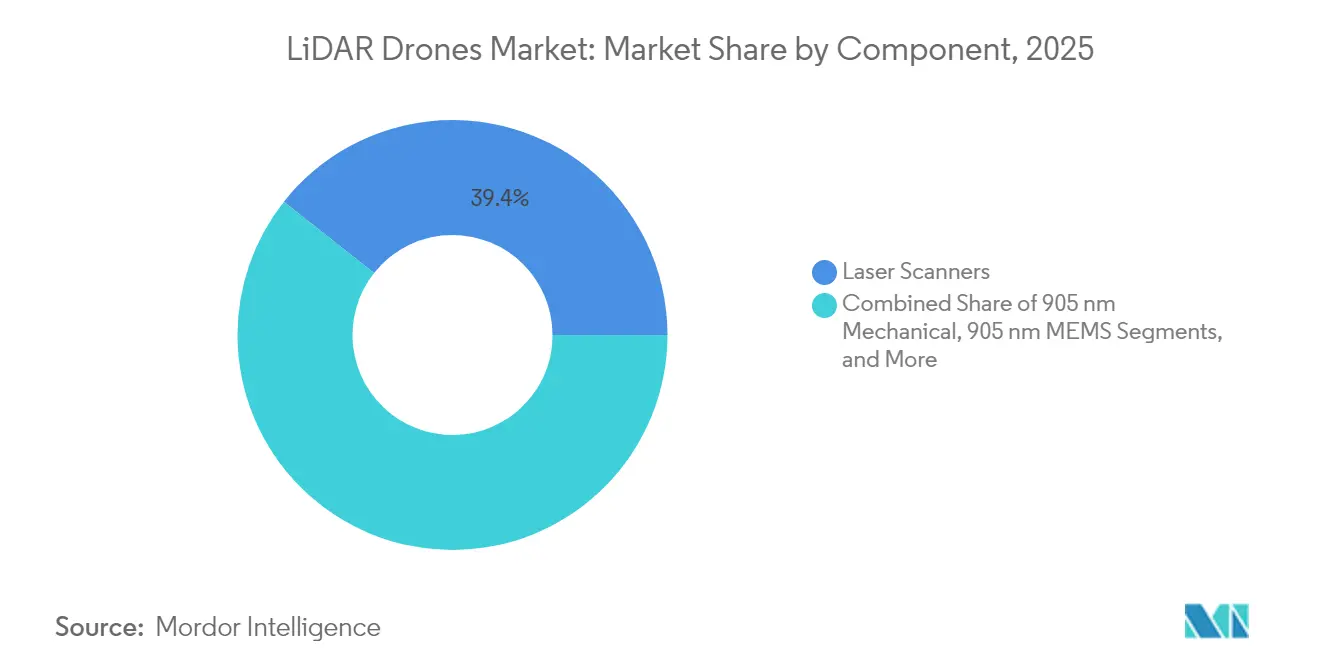

- By component, laser scanners led with 39.35% of LiDAR drone market share in 2025; navigation and positioning systems are on track to expand at a 21.1% CAGR to 2031.

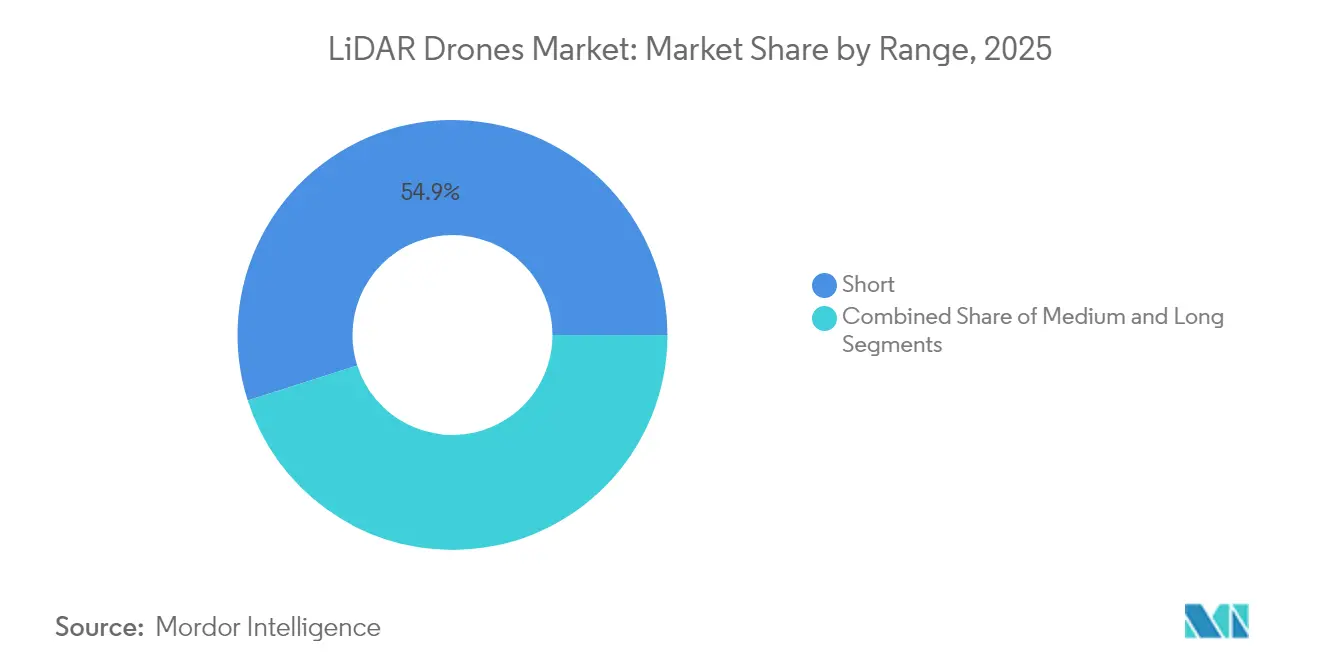

- By range, short-range systems accounted for 54.92% of the LiDAR drone market size in 2025, while long-range platforms are projected to rise at a 24.9% CAGR through 2031.

- By application, construction and infrastructure captured 29.45% of the LiDAR drone market size in 2025, whereas precision agriculture is forecast to grow at a 24.8% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global LiDAR Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Break-even of solid-state LiDAR cost < USD 400 enabling mass-market drones | +4.20% | Global, with early gains in North America & China | Medium term (2-4 years) |

| Surge in sub-250 g “micro-mapping” drones driven by EU Open-category rules | +3.10% | Europe core, spill-over to aligned regulatory regions | Short term (≤ 2 years) |

| Integration of bathymetric LiDAR on VTOL drones for shallow-water asset surveys | +2.80% | Coastal regions globally, Caribbean & Mediterranean focus | Medium term (2-4 years) |

| Cloud-native SLAM/AI point-cloud pipelines reducing post-processing lead-time | +3.50% | Global, concentration in tech-advanced markets | Short term (≤ 2 years) |

| Oil-and-gas methane-leak detection mandates in North America using LiDAR UAVs | +2.90% | North America, expanding to aligned regulatory jurisdictions | Medium term (2-4 years) |

| African corridor finance favoring drone-based topographical surveys over manned aircraft | +2.10% | Sub-Saharan Africa, corridor project concentrations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Break-even of Solid-state LiDAR Cost Below USD 400 Enabling Mass-market Drones

Photonics integration and scaled manufacturing have pushed solid-state unit prices below USD 400, removing the historical cost barrier that discouraged smaller contractors, farmers, and municipalities from adopting LiDAR-equipped aircraft. Hesai’s 300,000-unit annual volumes exemplify the economies of scale now possible. Mechanical parts elimination improves reliability and cuts maintenance, and patent filings show intense work on beam steering optimization. These shifts are expanding procurement beyond specialized survey firms into mainstream construction and environmental services, bolstering recurring upgrade cycles.

Surge in Sub-250 g Micro-mapping Drones Driven by EU Open-category Rules

Open-category regulations in Europe allow sub-250 g aircraft to be flown without a pilot license, spurring a wave of micro-LiDAR payloads engineered for class C0 drones. [1]European Union Aviation Safety Agency, “Open Category – Civil Drones,” easa.europa.eu Manufacturers now reach point densities near 50 pts/m² while staying under the weight ceiling. DJI’s Air 3S shows how consumer-grade craft now host forward-facing LiDAR for obstacle avoidance and basic mapping. Urban planners and heritage conservators benefit from affordable, quick-deployment tools, and similar frameworks are emerging in Canada and Japan, broadening the addressable base.

Integration of Bathymetric LiDAR on VTOL Drones for Shallow-water Asset Surveys

VTOL airframes couple helicopter-style vertical lift with fixed-wing cruise efficiency, offering the ideal platform for bathymetric LiDAR. Leica’s Chiroptera 4X achieves 140,000 pts/s at depths to 25 m, enabling coastal infrastructure and offshore wind inspections without boat mobilization. TOPODRONE’s AQUAMAPPER solution validated the method on mountainous construction corridors, delivering 2-3 cm accuracy in turbid rivers. Operators appreciate reduced safety risk and faster mobilization compared with crewed aircraft or sonar vessels.

Cloud-native SLAM/AI Point-cloud Pipelines Reducing Post-processing Lead-time

Advanced SLAM algorithms such as Voxel-SLAM combine inertial and LiDAR inputs to create real-time maps, cutting typical post-flight processing by 60%. [2]Voxel-SLAM Authors, “A Versatile LiDAR-Inertial SLAM System,” arxiv.org Edge processors handle initial alignment during flight, and cloud resources finish classification within hours. Machine-learning models now auto-detect vegetation, utilities, and terrain breaks, slashing manual editing requirements that previously consumed most project labor. Faster turnaround increases project throughput and enhances the value proposition of high-frequency monitoring.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EMI compliance hurdles for 1550 nm lasers | -2.30% | Global, strict in controlled airspace | Medium term (2-4 years) |

| Fragmented ASEAN BVLOS approvals | -1.80% | Southeast Asia | Long term (≥ 4 years) |

| Carbon-battery transport regulations | -1.40% | Global | Short term (≤ 2 years) |

| Limited GNSS correction in island nations | -0.90% | Caribbean and Pacific islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EMI Compliance Hurdles for 1550 nm Lasers on Multi-payload Rigs

FAA guidance AC 20-183 requires rigorous EMI, exposure, and ocular hazard calculations when high-power 1550 nm lasers share airframes with radios and radars. [3]Federal Aviation Administration, “AC 20-183 – Laser Airworthiness Installation Guidance,” faa.gov Shielding and wavelength-selective filters add 15-25% to system cost, slowing procurement for multi-sensor fleets. Certification backlogs extend lead times, particularly for oil-and-gas operators integrating methane spectroscopy, broadband comms, and GNSS on one rig.

Fragmented Air-traffic Management Delaying BVLOS Permits in ASEAN

Southeast Asian states apply divergent unmanned-traffic rules, forcing survey firms to pursue separate approvals for cross-border projects. Singapore’s reforms shortened local processing, yet Indonesia, Malaysia, and Thailand still rely on manual case-by-case clearances. Inconsistent flight corridor definitions and data-sharing rules hamper beyond-visual-line-of-sight adoption, delaying linear-infrastructure surveys that span multiple jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensor Integration Shapes System Evolution

Laser scanners retained 39.35% of LiDAR drone market share in 2025, reflecting their irreplaceable role in point-cloud generation. Navigation and positioning units are advancing at a 21.1% CAGR, as centimeter-grade inertial-GNSS fusion has become essential for tightly coupled SLAM workflows. These precise reference packages anchor the LiDAR drone market size for premium survey-grade deliverables. Second-tier components, including thermal regulation modules and edge processors, now incorporate AI accelerators to handle in-flight feature extraction. Manufacturers are rolling out common electrical and data interfaces that shorten development cycles and simplify field swaps, lowering total cost of ownership for fleet operators.

Standardization extends to open-source middleware that allows plug-and-play upgrades of camera, multispectral, or magnetometer units alongside the LiDAR core. Battery management systems gain sophistication as extended-endurance flights stress cell life and thermal limits. Design attention is shifting to shielding against electromagnetic coupling between high-frequency transmitters and light-amplification circuits, a theme amplified by growing 1550 nm deployment.

By Product Form-factor: Rotary-wing Dominance with Fixed-wing Momentum

Rotary-wing aircraft provided 62.4% of total shipments in 2025, favored for their hover stability, vertical takeoff, and precision positioning around structures. Hybrid VTOL craft, though newer, combine those control benefits with fixed-wing cruise efficiency, allowing operators to surveil corridors exceeding 50 km on a single battery. Fixed-wing designs now include modular nose cones and wing hardpoints capable of hosting dual-sensor payloads, expanding survey productivity per flight hour.

The LiDAR drone market continues to value rotary-wing versatility for cell-tower, façade, and confined-site mapping, yet rising insurance premiums tied to hover time encourage operators to consider fixed-wing sorties where terrain allows launch and recovery strips. Manufacturers answer with quick-swap airframe kits enabling crews to redeploy the same sensor stack across platform types within a single shift, blurring historical boundaries between product classes.

By Operating Altitude: Low-altitude Operations Remain the Safety-first Norm

Most commercial sorties occur under 120 m AGL, aligning with air-space rules that separate drones from manned traffic and streamline flight notices. This altitude bracket secures a plurality of the LiDAR drone market size, especially for construction, agriculture, and urban planning work. Operators obtain waivers for 120-300 m flights when larger footprints demand fewer ground control points, though compliance procedures add administrative overhead. Only niche projects such as mountainous corridor mapping justify 300-500 m profiles, where clearances must account for terrain elevation and radar line-of-sight.

Equipment suppliers tailor sensor eye-safe power levels and beam divergence to typical flying heights, simplifying regulatory submission packages. Some agencies are trialing performance-based risk frameworks that could unlock mid-altitude corridors, yet widespread adoption remains a long-term prospect.

By Service Model: Hardware Sales Give Way to Subscription Revenue

Fleet managers historically bought equipment outright, but budget-sensitive organizations increasingly favor LiDAR-as-a-Service subscriptions that bundle platform, pilot, and analytics deliverables into a single invoice. Cloud processing and AI classification allow vendors to turn raw data around overnight, appealing to clients who need rapid cycle times yet lack in-house geospatial staff. Analytics Software-as-a-Service logs recurrent revenues as users upload legacy data for comparative change detection. Hardware OEMs respond by offering trade-in programs and monthly leasing to retain customer relationships in the face of full-service competitors.

By Range: Short-range Systems Lead, Long-range Platforms Accelerate

Short-range craft (<100 m) held 54.92% of 2025 demand, reinforcing ease-of-use and quick-deployment priorities on construction and inspection sites. Long-range models (>500 m) are forecast to grow at a 24.9% CAGR as large-scale environmental monitoring, mining, and corridor projects seek coverage efficiencies. Software advances now calibrate target density automatically based on standoff distance, making long-range surveys viable without qualitative detail loss. Medium-range systems (100-500 m) bridge the gap, supplying municipalities with adequate reach for city-block mapping while retaining straightforward pilot training requirements.

By Application: Construction Leadership, Agriculture Momentum

Construction and infrastructure projects controlled 29.45% of 2025 revenue by applying LiDAR for earth-work measurement, clash detection, and incremental progress checks within BIM environments. Variable-rate agronomy and plant-health analytics position precision agriculture to expand at a 24.8% CAGR through 2031 as rural broadband and farm-management software converge. Forestry agencies value canopy-penetrating pulses to generate stem counts and biomass indices, while linear-infrastructure owners apply corridor mapping to plan maintenance, detect encroachment, and optimize asset lifecycles.

Geography Analysis

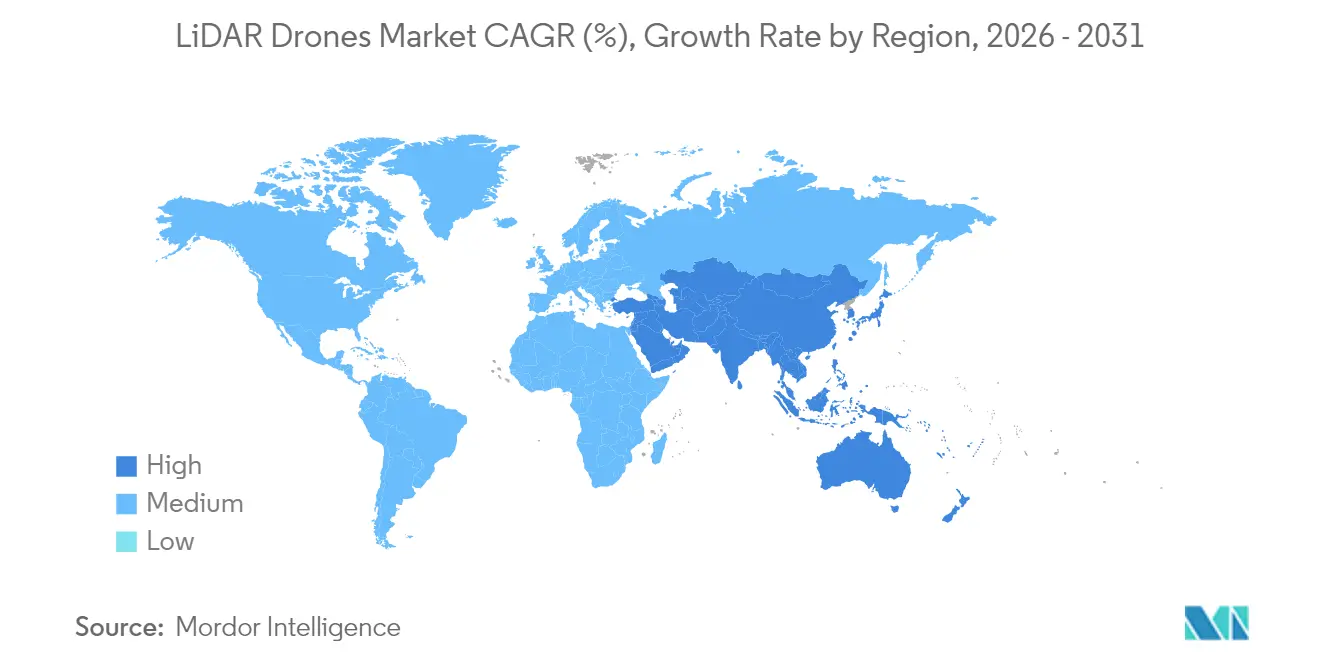

North America preserved 35.10% of global revenues in 2025, benefiting from established BVLOS waiver pathways, robust GNSS correction grids, and federal methane-leak rules that specify 100 kg/h detection thresholds. Energy majors fund fleet rollouts to meet EPA compliance, and state DOTs allocate capital to scan bridges and roads ahead of rehabilitation cycles. Trimble’s Q1 2025 USD 841 million earnings reveal sustained instrument demand tied to machine control and survey automation.

Asia-Pacific holds 22.80% share yet records the steepest growth slope, propelled by China’s LiDAR production scale and India’s infrastructure build-out. Hesai alone shipped 195,818 sensors in Q1 2025, underlining regional manufacturing muscle. India’s public-private corridors embrace drone mapping for land acquisition and progress tracking, while Japan subsidizes local government rice-field surveys. BVLOS harmonization lags across ASEAN, tempering offshore pipeline and power-line reconnaissance expansion.

Europe benefits from uniform air-space provisions under EASA’s Open-category, stimulating micro-platform uptake for urban surveying and cultural-heritage archiving. Hexagon reported EUR 564.9 million (USD 664.64 million) recurring revenue for Q3 2024, signaling strong digital reality adoption despite macro headwinds. Single-photon advances promise efficient national mapping, and the Green Deal’s biodiversity targets feed demand for forestry and habitat LiDAR baselines.

Competitive Landscape

The field remains moderate. Chinese volume leaders such as Hesai dominate automotive supply chains and leverage cost curves to enter adjacent aerial markets, while Western incumbents—Leica Geosystems, RIEGL, Trimble—retain brand preference in survey-grade work where accuracy and service networks command premiums. Ouster and Velodyne emphasize digital-architecture sensors that streamline firmware upgrades across vehicle and drone platforms, allowing cross-market reuse of R&D.

Strategic partnerships shape differentiation. GeoCue joined Clogworks to pair end-to-end software with rugged airframes, while Phase One and Carbonix integrate dual-sensor pods to address long-range linear infrastructure jobs. Suppliers invest in SLAM-enhanced firmware and AI-ready onboard compute, hedging against pure-hardware margin compression. Service vendors exploit subscription revenue, bundling data capture, processing, and analytics for construction clients who prefer outcomes over equipment.

White-space remains in shallow-water inspection, forestry carbon quantification, and live construction progress feeds. Firms able to integrate bathymetric scanning, multispectral imaging, and cloud analytics within a single operating dashboard may capture outsized share as end-users consolidate procurement toward turnkey providers.

LiDAR Drones Industry Leaders

-

Sick AG

-

Phoenix LiDAR Systems

-

Trimble Inc.

-

Velodyne / Ouster

-

DJI

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial scaling is increasingly tied to autonomy and repeatability rather than one-off survey flights, creating whitespace for integrated drone-in-a-box LiDAR workflows that deliver routine progress captures for construction and infrastructure owners. In March 2026, Skyports Drone Services deployed a BVLOS drone-in-a-box system for automated weekly surveying at the Rheinbruecke Leverkusen bridge project in Germany. The deployment illustrates how LiDAR capture can be operationalized as a scheduled service with faster turnaround and reduced field staffing.

Large, asset-owner procurement and public programs are also widening the addressable market for LiDAR payloads beyond traditional survey firms. In March 2026, DJI Enterprise secured a USD 250 million procurement contract from State Grid Corporation of China that included Zenmuse L2 LiDAR payloads and dock-based charging stations, indicating a shift toward fleet-scale, dock-enabled inspection deployments in utilities. In the United States, the FAA published a notice in April 2026 detailing the process for granting regulatory waivers under Section 927 of the FAA Reauthorization Act of 2024, complementing existing exemption pathways and supporting more standardized approvals for BVLOS operations where corridor mapping and recurring inspections demand longer ranges. India provides another opportunity corridor through government-sponsored river and drainage monitoring: Genesys International announced a National Mission for Clean Ganga contract in May 2026 for aerial LiDAR survey and geotagged videography across four states, expanding use cases in environmental monitoring, flood-risk planning, and infrastructure planning around waterways.

Recent Industry Developments

- June 2026: SICK integrated Aeva high-precision LiDAR-on-chip technology into its industrial sensing product line. The integration supports miniaturized, higher-performance LiDAR architectures that can transfer into lighter, more power-efficient aerial payload designs and autonomous inspection workflows where size, weight, and power are constraints.

- May 2026: Ouster announced a strategic agreement to supply digital LiDAR for integration into ARGUS Interception GmbH A1-Falke net-based counter-UAS interceptor drones. The partnership highlights defense and security demand for rugged, high-update-rate LiDAR sensing and points to continued investment in software-defined, upgradable LiDAR platforms for airborne deployments.

- September 2024: Trimble launched the APX RTX direct georeferencing portfolio for UAV mapping, integrating CenterPoint RTX to support centimeter-level positioning without base stations. The update supports field scalability for LiDAR drone operators working across distributed sites by reducing reliance on local GNSS correction infrastructure and simplifying deployment logistics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the LiDAR drones market covers revenue generated from drone platforms that are sold or deployed with LiDAR sensors for aerial mapping, surveying, inspection, and similar data-capture missions. This includes related integration and service delivery where it is bundled with the LiDAR drone offering.

Scope exclusions: We exclude stand-alone LiDAR sensors sold for non-UAV use, pure photogrammetry-only drone work, and general drone services that do not include LiDAR capture.

Segmentation Overview

-

By Component

- Laser Scanners

- 905 nm Mechanical

- 905 nm MEMS

- 1550 nm Fiber

- Navigation and Positioning Systems

- Inertial Measurement Units

- Cameras

- Power and Thermal Modules

- Other Components

-

By Product Form-Factor

- Rotary-Wing

- Fixed-Wing

- Hybrid VTOL

-

By Operating Altitude

- Very-Low (?120 m)

- Low (120-300 m)

- Medium (300-500 m)

-

By Range

- Short (<100 m)

- Medium (100-500 m)

- Long (>500 m)

-

By Service Model

- Hardware Sales

- Turn-key LiDAR-as-a-Service

- Analytics SaaS

-

By Application

- Construction and Infrastructure

- Environment and Forestry

- Precision Agriculture

- Corridor Mapping (Road, Rail, Pipeline)

- Mining and Quarrying

- Defense and Security

- Disaster Management and Insurance

-

Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia

-

Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to establish the factual base for the model and keep assumptions tied to what is feasible in flight operations. We reviewed public sources such as FAA drone rules and advisory material, EASA guidance, and other civil aviation publications that shape where LiDAR drones can be flown.

On the demand side, we leaned on sources such as USGS and other national mapping agency publications, infrastructure and transportation program documents, and forestry and environmental monitoring releases to understand where aerial LiDAR adoption is progressing. We also used company filings, investor presentations, association websites, and reputed press coverage to track product launches, typical payload capabilities, and common use cases. For cross-checks, paid subscriptions that compile company financials, patent activity, and shipment and trade indicators were referenced to confirm timelines and directional trends. The sources cited here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what portion of drone programs truly use LiDAR, and what is purchased as hardware versus delivered as a bundled service. We spoke with a mix of drone solution providers, surveying and mapping users, and technical specialists across APAC, EMEA, and the Americas to pressure-test pricing, replacement cycles, and adoption timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 21% | APAC: 51% |

| Mid tier: 52% | Functional/Unit leaders: 26% | EMEA: 30% |

| Smaller Players: 21% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where UAV adoption in mapping and inspection programs is translated into a LiDAR-equipped demand pool using penetration-rate logic, and then converted into value using typical system pricing and service mix. To keep the model grounded, selective bottom-up approximations were also run, where a sampled set of supplier revenues, channel checks, and average selling price (ASP) by drone class were used to validate totals and adjust outliers.

Key inputs include the share of projects shifting from ground surveys to aerial LiDAR, typical LiDAR payload weights and compatibility limits that influence platform choice, average flight time and coverage per mission (which affects how many systems are needed), and the hardware-versus-service split by buyer type. We also track regulatory readiness signals, such as BVLOS progress, sensor price trends, and replacement or upgrade cycles, since these drive annual purchasing patterns.

Forecasting was done using scenario analysis supported by trend smoothing, where the main drivers were varied in conservative, base, and high cases and then aligned to the consensus gathered from interviews. When bottom-up datapoints were missing for smaller markets, gaps were handled through proxy ratios such as drone fleet growth, application activity levels, and regional price normalization, and then rechecked through expert feedback before finalizing the forecast path.

Data Validation & Update Cycle

Validation is done in steps so that the final number is not dependent on one single assumption. Outputs are checked against independent signals such as drone registration and operations trends, mapping and infrastructure activity indicators, and visible shifts in LiDAR payload pricing. Where variances arise, they are traced back to the specific driver that caused them.

Before sign-off, the model goes through peer review, where input sources, unit logic, and conversion factors are rechecked and any abnormal jumps are challenged. If a variance cannot be explained cleanly, the related assumptions are revisited, and when needed, primary respondents are re-contacted for clarification. Reports are refreshed annually, and interim updates are triggered when material events occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Lidar Drones Market Size Versus Other Published Estimates

Published numbers for LiDAR drones often differ because each publisher anchors the market in a different year and then treats bundled services, analytics add-ons, and drone platform revenue in its own way. As a result, two estimates can sound similar in topic, yet still be counting different revenue streams and timing points.

In this market, the biggest drivers behind the spread are usually the base year selected, whether pricing is treated as hardware-only or as a project-delivered service value, and how fast ASPs are assumed to decline as lighter sensors and integration become more common. Currency timing and the cadence of assumption refreshes also matter, especially when adoption is shaped by aviation approvals and infrastructure spending cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 299.73 M (2026) | |

| Global Consultancy A | USD 254.42 M (2025) | Uses a 2025 base year and a faster growth setup, and it appears to lean more on a broad application expansion case and less on year-by-year checks of service versus hardware mix, which can shift the starting value. |

| Industry Publisher B | USD 264.54 M (2025) | Anchors the market in 2025 and presents 2026 as a forecast step, and differences can come from how bundled project delivery is priced and how quickly ASP declines are applied in early years. |

The table mainly shows a timing and scope treatment gap, with two estimates starting at 2025 and one starting at 2026. When service delivery is counted only where LiDAR capture is part of the contracted drone job, and the hardware-versus-service split is refreshed using interview checks, the 2026 starting point lands differently. That is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the LiDAR drone market?

The LiDAR drone market stood at USD 299.73 million in 2026 and is projected to reach USD 724.66 million by 2031.

Which component segment is growing fastest?

Navigation and positioning systems are expanding at a 21.1% CAGR, driven by demand for centimeter-level georeferencing.

Why are sub-250 g drones important for LiDAR adoption?

European Open-category rules exempt these light drones from pilot licensing, enabling rapid, low-cost mapping in dense urban areas.

How are methane regulations influencing demand?

EPA Super-Emitter mandates in North America require 100 kg/h leak detection, prompting oil and gas operators to deploy LiDAR-equipped UAVs.

Which region shows the highest growth potential?

Asia-Pacific exhibits the steepest growth trajectory, supported by Chinese manufacturing scale and India’s infrastructure programs.

What challenges limit wider deployment?

Electromagnetic interference certification for high-power lasers and fragmented BVLOS rules in ASEAN states continue to slow rollout timelines.

Page last updated on: