Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

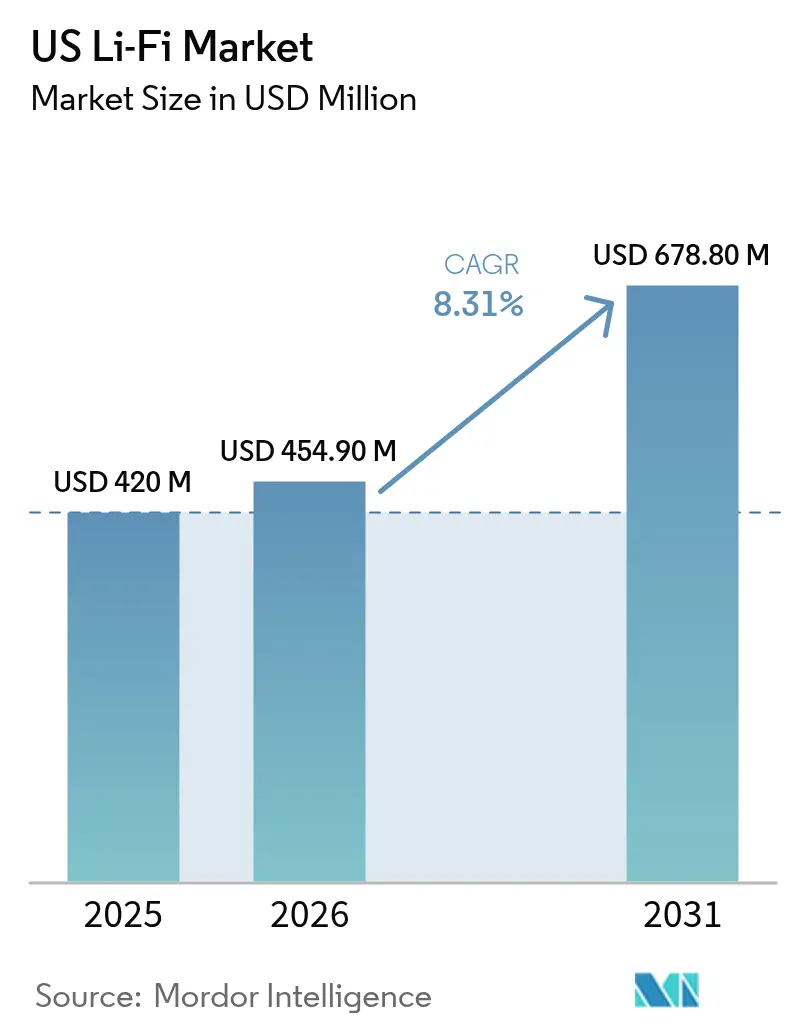

| Base Year Market Size (2025) | USD 420 Million |

| Market Size (2026) | USD 454.90 Million |

| Market Size (2031) | USD 678.80 Million |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Li-Fi Market Analysis by Mordor Intelligence

The US Li-Fi Market size is projected to be USD 420 million in 2025, USD 454.90 million in 2026, and reach USD 678.80 million by 2031, growing at a CAGR of 8.31% from 2026 to 2031.

Growth rests on three pillars: accelerated LED retrofits that turn lighting fixtures into data networks, federal incentives that expand domestic optical-component supply, and mounting RF congestion inside enterprise campuses that position Li-Fi as a complementary channel. Military spending, smart-building mandates, and Industry 4.0 automation each funnel fresh demand toward optical wireless links that handle high throughput without electromagnetic interference. Competitive activity concentrates on interoperability with Wi-Fi, smaller transceivers for consumer devices, and tight integration with power-over-Ethernet lighting so that deployment friction stays low.

Key Report Takeaways

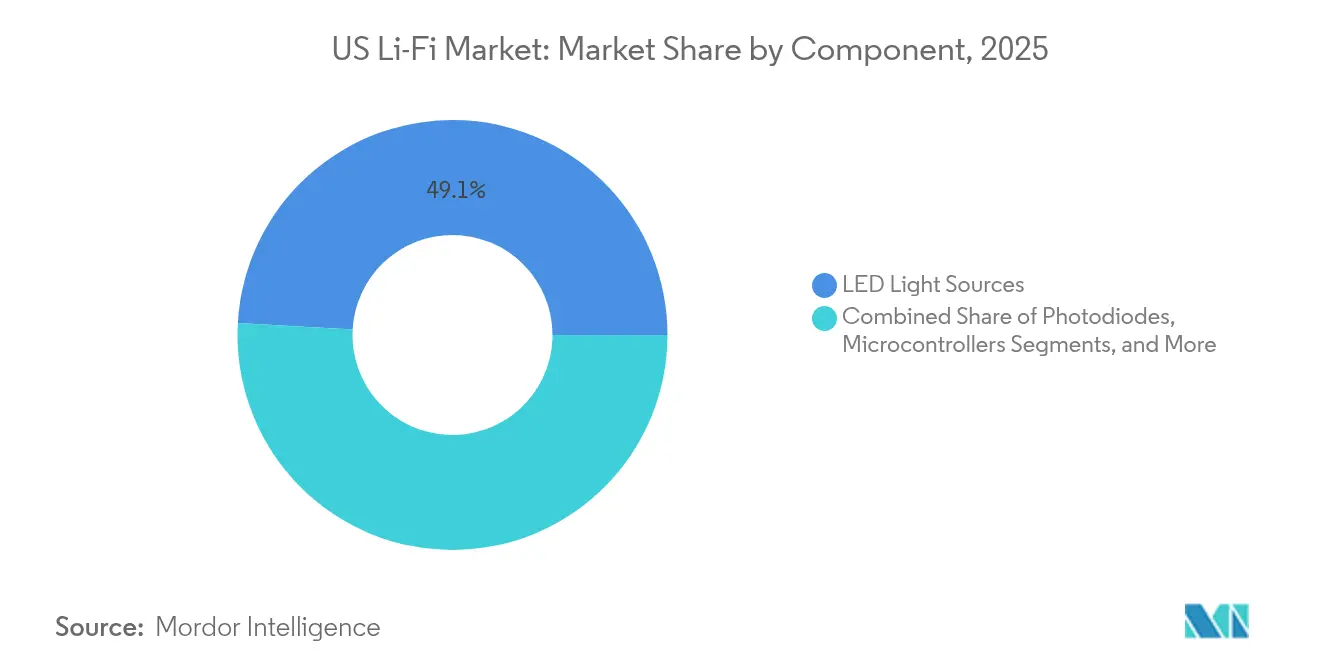

- By component, LED light sources captured 49.12% of the US Li-Fi market share in 2025, while software and firmware record the fastest 10.08% CAGR to 2031.

- By technology, LED-based Li-Fi (VLC) systems held 65.10% of the US Li-Fi market size in 2025; hybrid Li-Fi/RF systems expand at an 10.78% CAGR through 2031.

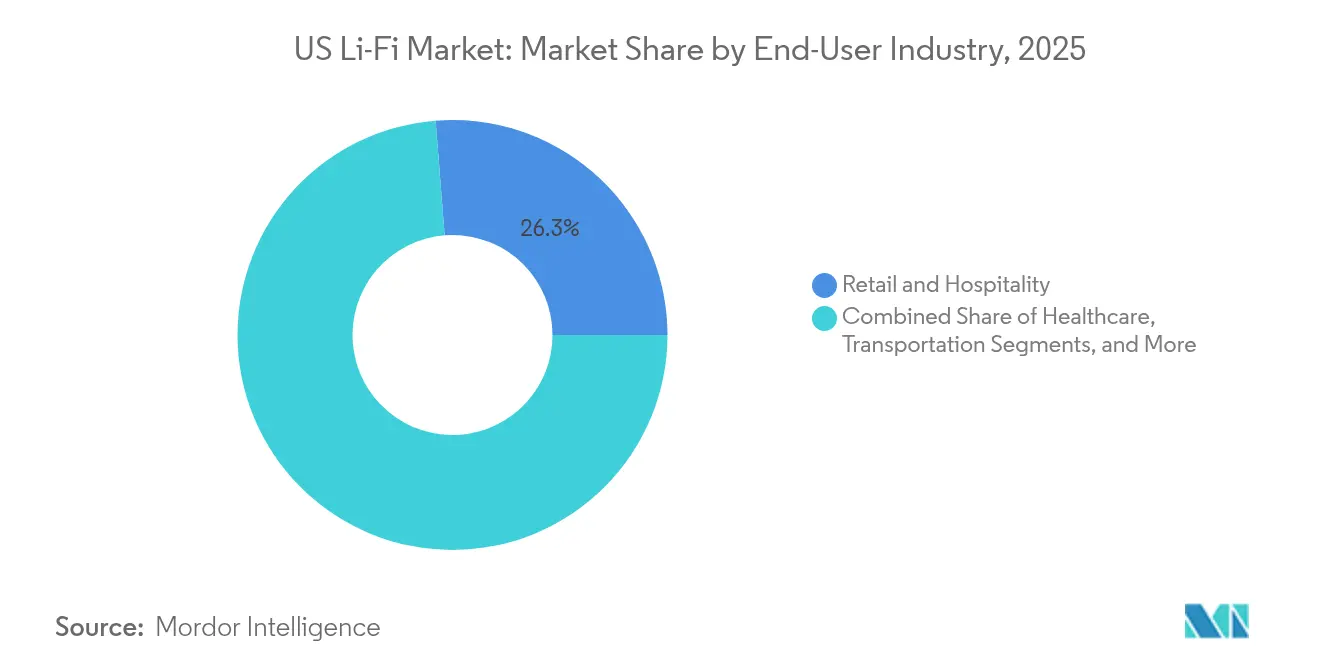

- By end-user industry, retail and hospitality led with 26.25% revenue share in 2025, whereas military and defense is projected to post the highest 11.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Li-Fi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated LED retrofit mandates in US commercial buildings | +1.8% | California, New York, Texas | Medium term (2-4 years) |

| RF spectrum congestion and secure indoor-wireless demand | +2.1% | US metro enterprise districts | Short term (≤ 2 years) |

| Federal funding for military/defense Li-Fi pilots | +1.2% | Defense installations | Medium term (2-4 years) |

| Industry 4.0 demand for deterministic low-latency links | +1.5% | Midwest and Southeast factories | Long term (≥ 4 years) |

| PoE-enabled smart-lighting backhaul economics | +0.9% | Commercial real estate clusters | Short term (≤ 2 years) |

| CHIPS-Act incentives for domestic optical-receiver supply | +0.8% | Arizona, Ohio, New Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated LED Retrofit Mandates Drive Infrastructure Foundation

California’s Title 24 codes and the IECC 2021 model elevate LED adoption, inadvertently wiring ceilings with transmitters that double as Li-Fi access points [1]David Manners, “Li-Fi Standard Released – IEEE 802.11bb,” Electronics Weekly, electronicsweekly.com. ASHRAE 90.1 pushes connected-lighting controls, letting building owners recover both energy savings and gigabit connectivity in a single investment. Power-over-Ethernet backhaul trims installation labor because low-voltage cable and data share the same run. Facility managers discover that every luminaire becomes a managed network node, so Li-Fi slips naturally into smart-building dashboards rather than standing alone. The outcome is a lower total cost per square foot compared with overlay Wi-Fi densification.

RF Spectrum Congestion Catalyzes Enterprise Adoption

Urban campuses already saturate 6 GHz Wi-Fi channels; Li-Fi escapes that bottleneck by moving up to the 400-800 THz band that offers 10,000 times the available spectrum. Light cannot leak through walls or ceilings, so floor-by-floor reuse multiplies throughput without coordination overhead. Banks and law firms appreciate the room-contained signal that curbs eavesdropping risk. Factories record cleaner machine telemetry because Li-Fi ignores electromagnetic interference that cripples RF near welders. Fraunhofer’s GigaDock demo hit 12.5 Gbps with sub-millisecond latency, proving deterministic links for Industry 4.0 workloads [2]Fraunhofer IPMS, “Real-Time Li-Fi for Industry 4.0,” Optics.org, optics.org .

Federal Defense Funding Accelerates Military Applications

In January 2025, Intelligent Waves and Signify formed a defense-focused joint venture that places optical wireless on the DoD’s modernization roadmap [3]OpenSystems Media, “Communication Pact for DoD,” Military Embedded Systems, militaryembedded.com. Field exercises indicate that adversaries cannot jam or intercept line-of-sight light unless they penetrate the secure perimeter. Contract dollars underwrite ruggedized transceivers that tolerate temperature swings, vibration, and battlefield dust. Lessons migrate back to civilian gear, leading to smaller photodiodes and adaptive beam steering that strengthen retail and healthcare use cases. As defense procurement absorbs initial non-recurring engineering costs, vendors gain scale economies that spill into commercial price lists.

Industry 4.0 Demands Deterministic Connectivity

Automated lines synchronize robots to tolerances measured in milliseconds; Li-Fi guarantees timetable integrity because light pulses do not fade under electromagnetic noise from motors. Each fixture can also triangulate asset location within centimeters, so a single network handles control and positioning. Automotive plants report faster tool-change routines when handheld scanners stay latency-free. Warehouses mount Li-Fi beacons on high-bay luminaires, guiding autonomous vehicles along dynamic paths while keeping Wi-Fi free for handheld terminals. The deterministic nature of light-based links appeals to safety auditors who insist on predictable packet delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited line-of-sight coverage range | -1.4% | Open office interiors | Short term (≤ 2 years) |

| Lack of native Li-Fi chipsets in mass-market devices | -1.8% | Consumer electronics channel | Medium term (2-4 years) |

| Fragmented local flicker and building-code compliance hurdles | -0.6% | Municipal jurisdictions | Short term (≤ 2 years) |

| Competitive threat from Wi-Fi 7 and 5G enterprise DAS | -1.1% | Enterprise campuses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Line-of-Sight Limitations Constrain Coverage Economics

Every cubicle wall and moving body can sever an optical path, forcing denser access-point grids than Wi-Fi needs. Reflective ceilings extend reach but cut throughput, so planners must balance redundancy with budget. Retailers find that seasonal aisle resets break line-of-sight maps, adding maintenance overhead. Although beam-steered lasers promise wider cones, the gear costs more than commodity LED lamps. Until automated coverage-mapping software matures, facilities weigh mobility risk against Li-Fi’s security upside.

Device Integration Barriers Limit Market Expansion

Smartphones, tablets, and laptops still ship without embedded Li-Fi transceivers, so users carry USB dongles that drain batteries and add bulk. System-on-chip vendors hesitate to redesign silicon before demand proves sustainable. As Wi-Fi 7 landlords provide gigabit speeds through existing antennas, purchasing teams question a second wireless stack that requires new inventory. The IEEE 802.11bb standard lets Li-Fi appear as another Wi-Fi band, but chipset integration remains in the pilot stage. Lack of native support pushes back consumer adoption timelines and slows economies of scale for component suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: LED Sources Anchor the Transmission Layer

LED light sources held 49.12% of the Li-Fi market share in 2025, demonstrating how illumination assets double as broadband gateways. Each lamp already draws power and occupies ceiling real estate, so incremental cost covers only modulation drivers and photodetectors. That synergy compresses payback periods for building owners who planned LED conversions to meet energy codes. Photodiodes follow as the next-largest hardware slice because every link needs a receive channel, and bidirectional traffic doubles diode counts in duplex installations. Microcontrollers oversee pulse-width modulation that exceeds 50 MHz yet stays flicker-free under IEEE PAR1789 guidance.

Software and firmware post a 10.08% CAGR, the fastest across component lines, because hybrid Li-Fi/Wi-Fi orchestration demands algorithms that decide which band carries which session. Network-management consoles now resemble lighting dashboards, merging lux level, occupancy sensing, and throughput graphs on a common pane. Modulator ASICs integrate signal conditioning that once lived on plug-in cards, trimming enclosure volume so transceivers fit inside desk lamps. System-integration services grow in lockstep, bundling photometrics with RF planning tools so architects can validate coverage and code compliance in one model. The Li-Fi market size allocation for services, therefore, rises faster than hardware outlays as early adopters seek guaranteed performance.

By Technology: VLC Dominance Faces a Hybrid Surge

LED-driven visible-light communication captured 65.10% of the Li-Fi market size in 2025 because commodity LEDs already sit in global supply chains. Safety regulators accept visible wavelengths for occupied spaces, so approvals flow smoothly. Laser-based near-infrared systems carve out specialist niches in warehouses and flight decks where users can wear protective goggles and justify higher costs for extended throw distances.

Hybrid Li-Fi/RF systems register the highest 10.78% CAGR by resolving mobility gaps. A worker can stream to a laptop under the desk lamp and then roam to the hallway as the session hands over to Wi-Fi without packet loss. The IEEE 802.11bb protocol treats optical channels as one more Wi-Fi band, so access-point controllers schedule traffic across light and radio in real time. Vendors now sell ceiling tiles that host both LED emitters and tri-band Wi-Fi antennas in a single enclosure. The convergence lets facilities upgrade on normal refresh cycles instead of running two separate projects.

By End-User Industry: Defense Growth Challenges Retail Leadership

Retail and hospitality claimed 26.25% of 2025 revenue because location-based services monetize shopper analytics while LED upgrades coincide with brand image renovations. Luxury hotels install Li-Fi desk lamps in executive suites so guests enjoy encrypted connectivity without sharing public Wi-Fi passwords. Grocery chains mount aisle-wide LED strips that push coupon data to handheld apps, reinforcing customer loyalty programs.

Military and defense, however, accelerate at a 11.64% CAGR as secure mission communications secure budget priority. The DoD partnership between Intelligent Waves and Signify validates Li-Fi for contested environments where RF jamming or detection jeopardizes operations. Command posts equip briefing rooms with ceiling nodes that isolate traffic to cleared personnel while avoiding electromagnetic leakage. Healthcare, transportation, education, and industrial automation follow with lower but steady adoption curves, each exploiting immunity to EMI or precise indoor positioning for their own workflows.

Geography Analysis

California leads Li-Fi rollouts because state energy codes mandate connected lighting, positioning the U.S. as one of the most advanced regions within the global Li-Fi market. and Silicon Valley firms pilot optical networking on new campuses. High-rise retrofits in Los Angeles adopt Li-Fi to offset Wi-Fi shadow zones created by Low-E window coatings. New York skyscrapers join the wave as landlords chase Title 24-style standards for their own sustainability pledges. Texas gains momentum in corporate campuses around Austin, where semiconductor fabs align with CHIPS Act grants for domestic optical receiver production.

Defense installations distribute Li-Fi nodes across more than a dozen states, clustering near major Air Force bases and shipyards. These projects seed local contractor ecosystems that then market the same skill sets to hospitals and universities. Midwest automotive plants in Michigan and Ohio add optical links alongside robot lines to dodge RF noise, while Southeast logistics hubs in Georgia and Tennessee equip distribution centers for centimeter-grade asset tracking.

Regional code variance slows uniform adoption. Cities like Seattle and Boston align lighting rules with IECC 2021, whereas smaller municipalities lag, forcing national retailers to juggle multiple compliance frameworks. For vendors, this patchwork inflates certification budgets and lengthens sales cycles. Yet once a jurisdiction upgrades electrical codes, the Li-Fi market responds swiftly because the cost of adding light-based networking is marginal against the mandatory LED switch. Thus, the Li-Fi market size in progressive states outpaces laggards by double-digit percentages within two years of code harmonization.

Competitive Landscape

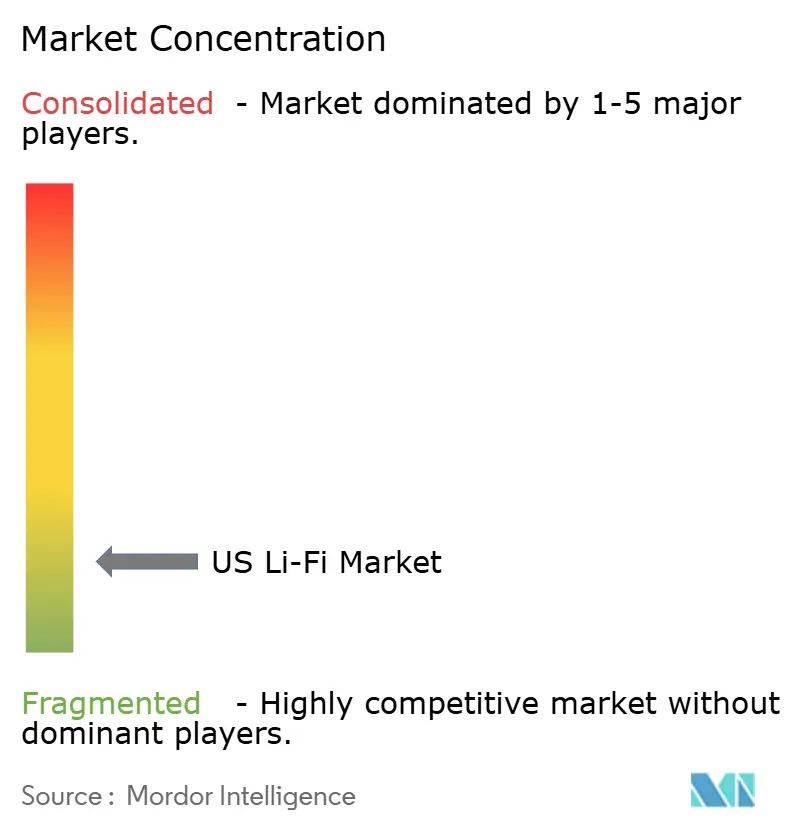

The studied market's concentration remains fragmented. Signify leverages its lighting portfolio but faces nimble rivals pureLiFi, VLNComm, and SaNoor that specialize in optical modulation. Each firm races to shrink receiver size so that laptop bezels host integrated photodiodes rather than USB dongles. Patent filings cluster around beam-steering micro-mirror arrays, adaptive dimming that maintains lux output while pushing higher data rates, and multi-band access-point algorithms.

Companies able to embed Li-Fi into conventional Wi-Fi chipsets gain cost leverage and instant user-base access. Lighting giants bundle optical access points with power-over-Ethernet luminaires, pitching a single invoice that covers energy savings and network upgrades. Startups counter with modular kits aimed at defense and heavy-industry buyers who value performance over volume pricing.

Mergers and joint ventures intensify as firms seek scale. Signify’s JV with Intelligent Waves attacks defense budgets, while component houses align with PCB assemblers in Ohio to meet CHIPS-Act domestic-content rules. Service integrators spring up to audit ceiling layouts, run photometric simulations, and guarantee both flicker compliance and throughput. Venture funding follows, yet investors scrutinize chipset roadmaps because native smartphone support is the final unlock for mass adoption. The Li-Fi industry, therefore, displays dynamic but disciplined capital flows.

US Li-Fi Industry Leaders

Signify Holding (Trulifi)

VLNComm Inc.

Qualcomm Technologies, Inc.

Panasonic Holdings Corporation

pureLiFi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Intelligent Waves and Signify formed a joint venture to advance Li-Fi for DoD use, focusing on jam-resistant optical links in contested environments.

- July 2024: Caltech researchers unveiled electrically tunable optical meta-surfaces that split a single pulse into multiple steerable beams, paving the way for agile Li-Fi beam steering.

- April 2024: Vibrint and pureLiFi launched a secure light-based network aimed at classified government operations, highlighting national-security demand for non-RF communications.

US Li-Fi Market Report Scope

Li-Fi is a wireless communication technology that uses the visible light spectrum or infrared spectrum for high-speed data communication. It offers significantly greater security and safety and ultra-fast data transmission rates to deliver unprecedented low latency and reliability. Li-Fi is a form of green communication method that salvages the existing lighting infrastructure for communication. The data is transmitted by varying the light intensity that is invisible to the human eye.

The United States Li-Fi market is segmented by cities (New York, Los Angeles, Chicago, Houston, Philadelphia, Washington, and Other Cities), estimated usage (house, corporate office, railways and airlines, airways, retail stores/supermarkets/hypermarkets, hotels, and other usages), types (led, photodiodes, microcontrollers, and other types). The market sizes and forecasts are provided in terms of value (USD ) for all the above segments.

By Component

| LED Light Sources |

| Photodiodes |

| Microcontrollers |

| Modulators/Signal-Processing ASICs |

| Software and Firmware |

| System Integration and Services |

By Technology

| LED-based Li-Fi (VLC) |

| Laser-based Li-Fi (NIR) |

| Hybrid Li-Fi/RF Systems |

By End-user Industry

| Healthcare |

| Transportation |

| Education |

| Military and Defense |

| Retail and Hospitality |

| Other End-user Industries (Aerospace, Industrial Automation,and others) |

| By Component | LED Light Sources |

| Photodiodes | |

| Microcontrollers | |

| Modulators/Signal-Processing ASICs | |

| Software and Firmware | |

| System Integration and Services | |

| By Technology | LED-based Li-Fi (VLC) |

| Laser-based Li-Fi (NIR) | |

| Hybrid Li-Fi/RF Systems | |

| By End-user Industry | Healthcare |

| Transportation | |

| Education | |

| Military and Defense | |

| Retail and Hospitality | |

| Other End-user Industries (Aerospace, Industrial Automation,and others) |

Key Questions Answered in the Report

How big is the US Li-Fi market in 2026?

The Li-Fi market stands at USD 454.9 million in 2026.

What is the forecast CAGR for Li-Fi through 2031?

The market is projected to grow at an 8.31% CAGR between 2026 and 2031.

Which component holds the largest share?

LED light sources captured 49.12% of Li-Fi market share in 2025.

Which technology segment is growing fastest?

Hybrid Li-Fi/RF systems post an 10.78% CAGR through 2031.

Why is defense spending important to Li-Fi adoption?

Military and defense applications drive secure, jam-resistant communication funding, accelerating innovation and growth at a 11.64% CAGR.

What limits consumer uptake today?

Lack of native Li-Fi chipsets in mass-market devices forces external dongles, slowing mainstream penetration.

Page last updated on: