Market Overview

| Study Period | 2020 - 2031 |

|---|---|

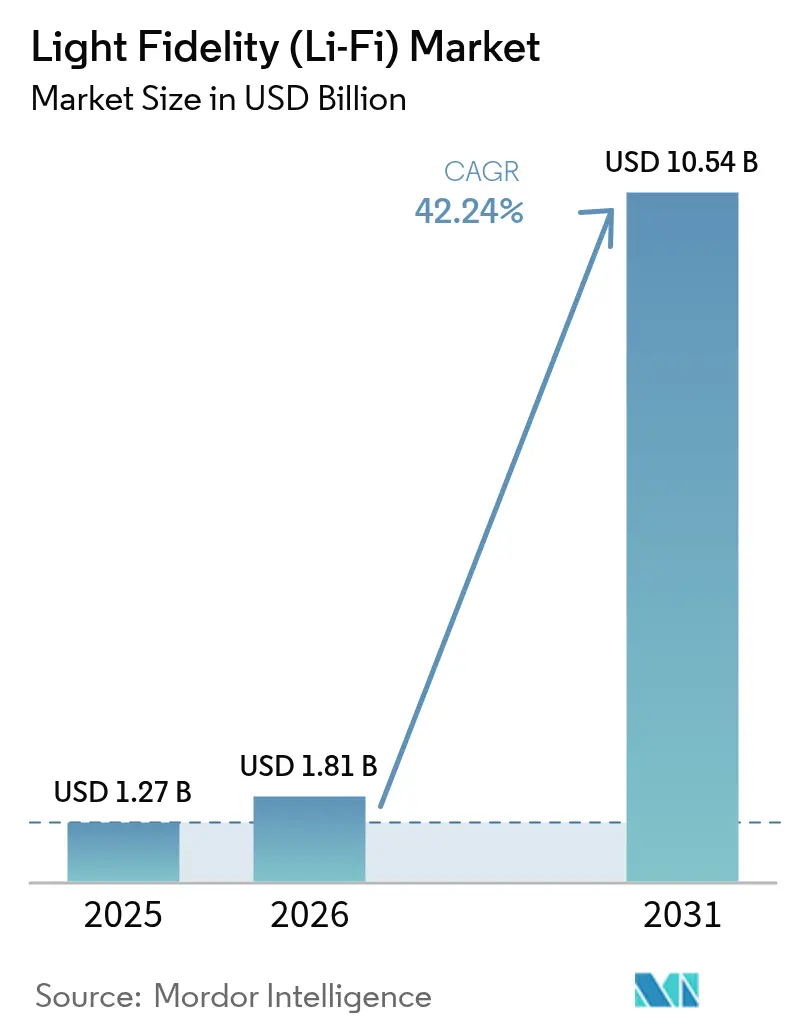

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 10.54 Billion |

| Growth Rate (2026 - 2031) | 42.24% CAGR |

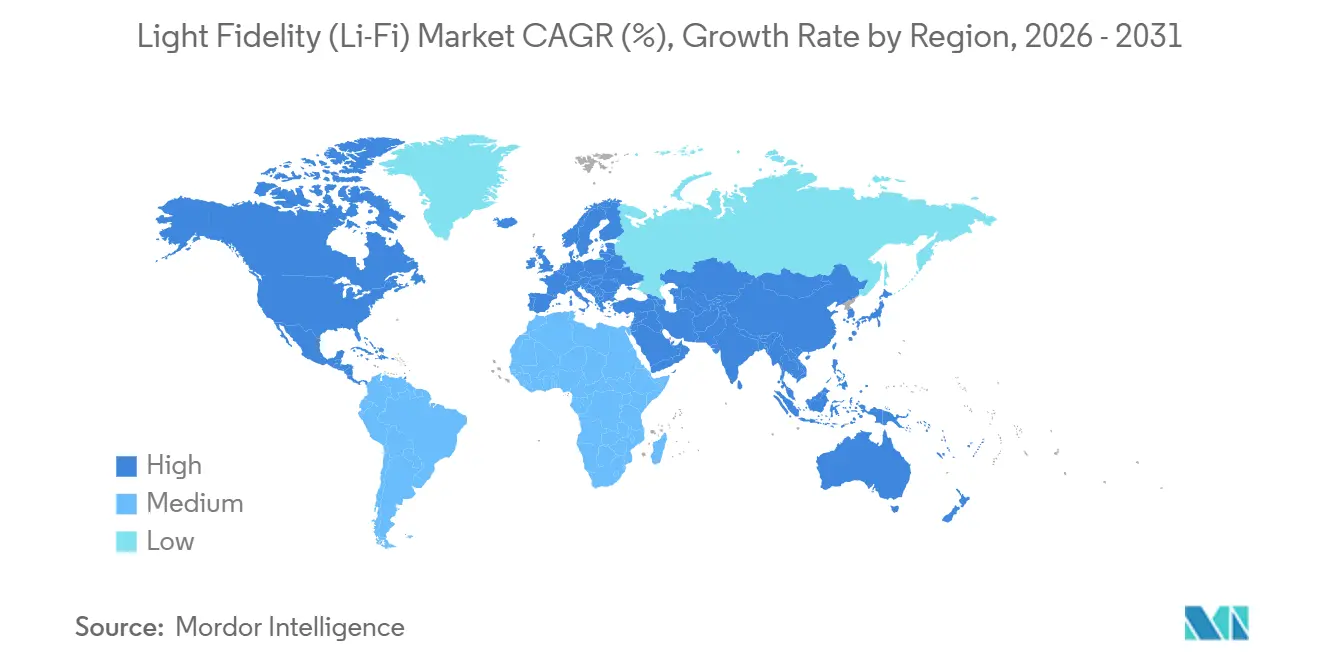

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Light Fidelity (Li-Fi) Market Analysis by Mordor Intelligence

The Light Fidelity (Li-Fi) market size is expected to increase from USD 1.27 billion in 2025 to USD 1.81 billion in 2026 and reach USD 10.54 billion by 2031, growing at a CAGR of 42.24% over 2026-2031. Commercial momentum accelerated after the IEEE 802.11bb interoperability standard removed vendor-lock risk, while large-scale U.S. Army deployments validated field resilience. Enterprises now view optical wireless as a secure overlay that complements Wi-Fi, especially in environments where spectrum congestion, electromagnetic interference, or espionage threats undermine radio solutions. Early adopters in healthcare, aviation, and industrial automation report fewer network outages, lower latency, and greater confidence in data security, creating peer-driven demand that extends beyond traditional lighting refurbishment cycles. The resulting uptick in pilot activity supports a robust pipeline of retrofit and green-field projects scheduled to start during 2026-2028.

Key Report Takeaways

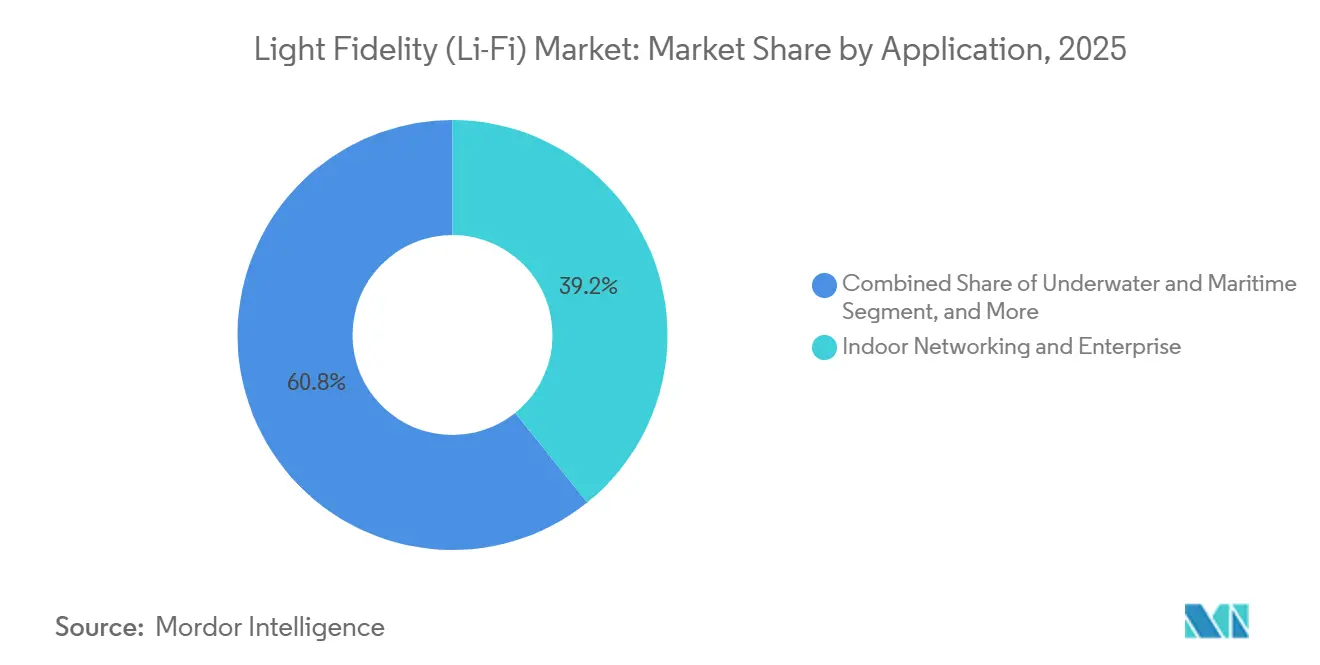

- By application, indoor networking and enterprise led with 39.21% of the Light Fidelity (Li-Fi) market share in 2025, while underwater and maritime applications are projected to expand at a 43.66% CAGR through 2031.

- By component, LEDs accounted for 47.38% of 2025 revenue, whereas photodetectors are forecast to grow at a 43.26% CAGR during 2026-2031.

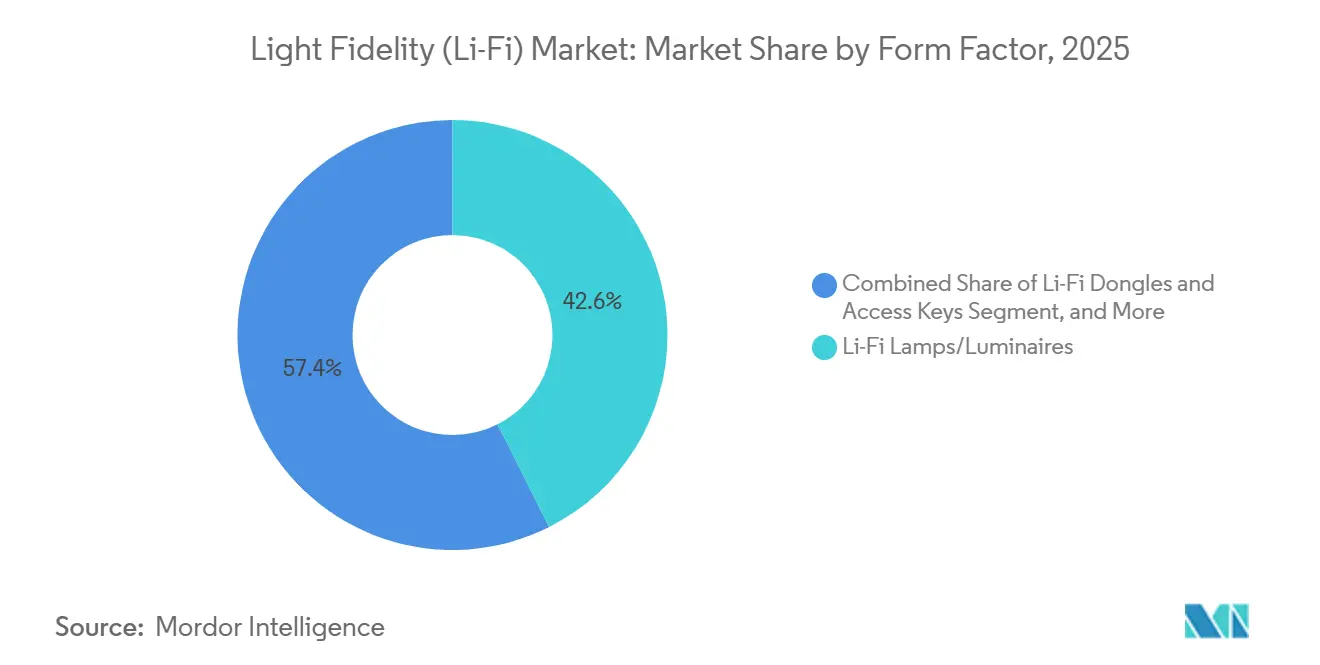

- By form factor, Li-Fi lamps and luminaires accounted for 42.57% of the Light Fidelity (Li-Fi) market share in 2025, while dongles and access keys are expected to grow at a 43.04% CAGR through 2031.

- By end-user, enterprises accounted for 36.89% of 2025 revenue, yet transportation and logistics is set to post the fastest growth with a 43.21% CAGR over the forecast window.

- By geography, North America dominated with 38.42% of 2025 revenue, whereas Asia-Pacific is poised for the highest regional expansion at a 43.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Light Fidelity (Li-Fi) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED-Lighting Retrofit Wave | +8.5% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| IEEE 802.11bb Interoperability Standard | +7.2% | Global | Short term (≤ 2 years) |

| Secure RF-Free Links for Defense and Healthcare | +6.8% | North America, Europe, Asia-Pacific (defense and healthcare hubs) | Medium term (2-4 years) |

| In-Flight Cabin Connectivity Adoption | +5.1% | Global, led by Europe and North America aviation markets | Medium term (2-4 years) |

| VCSEL-Based Above 10 Gbps Industrial Links | +4.3% | Asia-Pacific manufacturing hubs, North America, Europe | Long term (≥ 4 years) |

| RF-Restricted Clean-Room Mandates | +3.6% | Global, concentrated in semiconductor and pharmaceutical manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LED-Lighting Retrofit Wave

Organizations that replaced fluorescent fixtures with LEDs during 2020-2025 now view Li-Fi as an incremental upgrade rather than a green-field build. Wieland Electric demonstrated the model in 2025 by embedding optical modulators into existing luminaires, avoiding new cable pulls and bringing 250 Mbps links online in days.[1]Wieland Electric, “Wieland Electric Uses LiFi Technology in In-House Production,” wieland-electric.com Facility managers merge lighting and networking budgets, so the combined energy savings and connectivity gains shorten payback periods compared with separate wireless rollouts. As more lighting vendors ship “Li-Fi-ready” fixtures, procurement teams specify the capability up front, locking in future demand. The retrofit dynamic, therefore, converts a routine maintenance cycle into a large, addressable funnel for optical wireless.

IEEE 802.11bb Interoperability Standard

Formal ratification of IEEE 802.11bb in 2023, followed by government procurement notices that require compliant hardware, removed the multi-vendor risk that once stalled pilots.[2]Institute of Electrical and Electronics Engineers, “IEEE 802.11bb Standard,” ieee.org Enterprises now integrate Li-Fi access points into existing IP security and quality-of-service frameworks, eliminating the need for parallel IT stacks. Chipset makers have clear design rules that support volume production and narrow the cost gap with Wi-Fi. Standards alignment also eases global certification, enabling manufacturers to ship a single product family worldwide. The resulting confidence compresses sales cycles and lifts near-term shipment forecasts.

Secure RF-Free Links for Defense and Healthcare

Light signals stay inside defined coverage cones, preventing radio leakage that adversaries or eavesdroppers can exploit. The U.S. Army Europe and Africa’s 4,000-unit Kitefin deployment proved that optical wireless withstands contested environments while keeping RF signatures near zero.[3]British Broadcasting Corporation, “Light Technology Firm Strikes Deal With US Army,” bbc.com India’s Ministry of Defence followed with Navy trials that cite security benefits and lower spectral fees. Hospitals adopt the same principle to protect patient data and avoid electromagnetic interference with medical devices. Military and clinical endorsements carry high credibility, so adjacent industries such as finance and critical infrastructure are now piloting Li-Fi to harden their networks.

In-Flight Cabin Connectivity Adoption

Airlines need more bandwidth per passenger than satellite or air-to-ground links can economically supply. Integrating Li-Fi transmitters into overhead lighting provides each seat with a dedicated gigabit channel without introducing RF noise that complicates avionics certification. Early European trials report smoother streaming and fewer customer complaints, raising the likelihood of fleet-wide retrofits before 2030. Aircraft manufacturers explore factory-fit options that could embed optical backbones during assembly, saving weight and installation labor. Success in aviation elevates public awareness and demonstrates that Li-Fi operates safely in one of the most heavily regulated environments on Earth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost versus Wi-Fi | -5.8% | Global, particularly price-sensitive residential and small business segments | Short term (≤ 2 years) |

| Line-of-Sight Blockage and Short Range | -4.2% | Global | Medium term (2-4 years) |

| Fragmented Optical-Spectrum Rules | -2.7% | Global, with regional variations in photobiological safety limits | Medium term (2-4 years) |

| Hybrid Li-Fi and Wi-Fi Security Gaps | -1.9% | North America, Europe (enterprise and government sectors) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Cost Versus Wi-Fi

Li-Fi access points and USB receivers still cost three to five times as much as comparable Wi-Fi gear, a premium that deters schools, start-ups, and homeowners. Oledcomm’s LiFiMAX Compact kit reduces installation friction but remains priced for security-sensitive sites rather than mass adoption. The dual-hardware requirement transceivers in both lamps and client devices double the bill of materials. Until integrated chipsets appear in mainstream laptops and tablets, per-user dongle costs will keep total ownership high. Vendors are experimenting with leasing and subscription models, yet near-term uptake still hinges on applications where security or interference avoidance justifies the added spend.

Line-of-Sight Blockage and Short Range

Optical beams cannot penetrate walls or detour around obstacles, so users lose connectivity when they step outside illuminated zones. pureLiFi’s Bridge XC moves gigabit signals through windows, but the fix only helps fixed customer-premise equipment, not roaming devices. Large venues must install dense fixture grids to achieve full coverage, raising capital and energy costs compared with radio. Bright sunlight or high-intensity task lighting can overwhelm receivers, forcing adaptive modulation that cuts throughput at peak daylight hours. Hybrid Li-Fi and Wi-Fi designs mitigate some gaps, yet the added complexity challenges thinly staffed IT teams. These physical constraints temper enthusiasm for all-optical networking in cost-sensitive projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Defense Validation Accelerates Commercial Adoption

Indoor networking and enterprise deployments accounted for 39.21% of the Light Fidelity (Li-Fi) market share in 2025, confirming that secure conference rooms, executive suites, and trading floors form the largest current revenue pool. Hospitals, factories, and airports added steady pilot volume, boosting confidence that Li-Fi performs reliably outside laboratories. The underwater and maritime niche, although small today, is projected to expand at a 43.66% CAGR through 2031 as navies and offshore operators replace attenuated radio links with blue-green laser systems. Healthcare installations continue to gain favor because optical signals do not interfere with life-support equipment, enabling patient-care areas to become reliable, high-bandwidth zones. Overall, strong early performance in mission-critical settings validates Li-Fi for broader enterprise rollouts.

Defense endorsements create a ripple effect that speeds procurement in civilian industries. Military field tests demonstrated that optical links remain jam-resistant and free of detectable emissions, a finding that resonates with financial services and critical infrastructure operators who fear espionage. Aviation trials show passengers can receive gigabit content without adding RF noise to avionics, further widening the technology’s appeal. Smart home interest remains niche, yet gamers and home-office users already pay premiums for low-latency optical links, hinting at a gradual trickle-down to consumers. Taken together, diverse adoption paths diversify risk and underpin a strong outlook for the Light Fidelity (Li-Fi) market size tied to application breadth.

By Component: Photodetectors Pull Ahead in the Race for Speed

LEDs accounted for 47.38% of 2025 component revenue, as most organizations retrofit existing fixtures rather than invest in stand-alone emitters. Their dominance reflects the practical reality that ceiling lights already blanket offices and factories, so adding data modulation demands minimal extra hardware. Photodetectors, however, are on track to deliver the fastest growth, with a 43.26% CAGR from 2026 to 2031, as avalanche photodiodes and silicon photomultipliers extend range and unlock multi-gigabit throughput. Optical filters and precision lenses complement the new receivers by sharpening beam focus and blocking ambient light, essential for sunlit atria and glass-walled factories. Software and services revenue rises in tandem as enterprises need dashboards that orchestrate roaming between Li-Fi and Wi-Fi.

A transition toward laser-based vertical-cavity surface-emitting transmitters is underway, particularly in manufacturing environments that demand deterministic latency. While lasers still account for only a small share of the Light Fidelity (Li-Fi) market, their ability to reach 10 Gbps supports real-time machine vision and robotics, creating new demand for advanced detectors. Micro-controllers and modulators become more complex because adaptive coding keeps links stable during lighting variations, thereby increasing semiconductor content per fixture. As vendors chase eye-safety limits rather than raw brightness, receiver sensitivity improvements become the primary lever for coverage gains. This shift redirects value from commodity LEDs toward higher-margin photonics and signal-processing components.

By Form Factor: Dongles Bridge the Gap Until Native Chipsets Arrive

Li-Fi lamps and luminaires accounted for 42.57% of 2025 revenue, indicating that bundled illumination and connectivity remain the easiest entry point for building owners. Integrated fixtures reduce ceiling clutter and simplify power distribution, allowing engineers to specify a single device rather than separate access points and lights. Dongles and access keys, in contrast, are expected to post a 43.04% CAGR through 2031 because bring-your-own-device cultures require quick ways to connect existing laptops and tablets. Modules and chipsets attract original-equipment manufacturers eager to embed optical transceivers into notebooks, monitors, and industrial sensors, shrinking form-factor footprints. Each category supports a distinct adoption stage, ensuring that no single hardware type dominates the Light Fidelity (Li-Fi) market share across all use cases.

Early pilots typically start with USB-C sticks so IT teams can validate performance without opening sealed devices. Once results satisfy security and throughput criteria, facilities often shift toward ceiling fixtures that blanket entire rooms and require no user accessories. Integrated luminaires benefit from 10-15 year replacement cycles, locking in recurring software revenue as vendors push firmware updates. Dongle suppliers counter by adding driverless, plug-and-play features that reduce help-desk tickets and enable rapid desk-hotel reconfigurations. Over time, chipset integration in mainstream consumer electronics is expected to reduce dongle volumes, but the interim demand ensures a balanced revenue mix that stabilizes the overall Light Fidelity (Li-Fi) market size.

By End-User: Logistics Leads the Next Wave of Adoption

Enterprises accounted for 36.89% of 2025 revenue, underscoring that corporate offices, banks, and research labs currently pay the bills for Li-Fi vendors. These users prize optical links for protecting sensitive discussions and intellectual property while avoiding the RF congestion typical of dense urban campuses. Transportation and logistics are forecast to register the steepest climb, with a 43.21% CAGR through 2031, as automated guided vehicles and smart shelving require deterministic wireless connectivity in metal-rich warehouses. Government and defense customers remain strategic anchors because validated field resilience speeds internal approvals, even if order volumes fluctuate with budget cycles. Residential demand remains constrained by price, yet privacy-minded consumers are creating a growing niche for RF-free smart homes.

Industrial manufacturers install Li-Fi on production lines to connect robotic arms, sensors, and inspection cameras without spectrum licensing, improving uptime in noise-sensitive plants. Warehouse deployments also leverage visible-light positioning for centimeter-level accuracy, eliminating the need for separate real-time location tags and reducing capital outlay. Healthcare institutions, another high-trust customer class, deploy optical links in surgical suites to eliminate electromagnetic interference, reinforcing vendor credentials. Combined, these verticals spread risk and support incremental expansion of the light fidelity market share, ensuring that growth does not hinge on any single end-user category.

Geography Analysis

North America commanded 38.42% of 2025 revenue, placing the region at the top of the light fidelity market share leaderboard. Federal cybersecurity mandates and sustained defense funding continue to anchor demand in government and financial services. Vendors also benefit from wide LED penetration, which speeds Li-Fi retrofits across corporate campuses. Local manufacturing investments shorten supply chains and satisfy domestic-content rules, further reinforcing buyer confidence. The region’s growth outlook remains solid even though its forecast expansion trails that of the Asia-Pacific.

Asia-Pacific is projected to grow at a 43.29% CAGR through 2031, the highest regional growth rate recorded for the light fidelity market. Government-backed pilots in China, India, Japan, and South Korea channel grants into smart factories and smart city corridors, creating early anchor orders for domestic suppliers. Defense ministries fund secure fleet communications that avoid congested radio bands, and educational institutions install Li-Fi in research labs to protect intellectual property. Component ecosystems emerging around VCSEL arrays and photodetectors are expected to bring down costs and enable large-scale commercial launches. As standards alignment improves, cross-border deployments will allow Asian vendors to export turnkey solutions.

Europe follows closely behind, driven by stringent electromagnetic-compatibility codes and privacy regulations that favor optical confinement. Airlines retrofit cabins with Li-Fi lighting harnesses, while office landlords install secure meeting rooms to attract blue-chip tenants. Middle East and African governments pilot the technology at critical infrastructure sites, and Latin American logistics operators test it in high-bay warehouses where radio reflections degrade Wi-Fi reliability. Although these regions currently hold modest shares, successful trials could unlock pent-up demand, adding incremental volume to the global light fidelity market size during the forecast window.

Competitive Landscape

The light fidelity market remains moderately fragmented, with no single vendor controlling more than half of global revenue. Signify leverages its vast installed lighting base and now offers the FIPS 140-3-validated Trulifi 6004, a credential that opens doors to U.S. federal buyers. pureLiFi positions itself as the innovation leader, shipping chipsets that demonstrate 10 Gbps throughput and forging alliances with fixed wireless access providers. Oledcomm and Velmenni focus on aviation and industrial verticals, while Panasonic targets enterprise retrofits in Asia.

Recent strategic moves underscore intensifying competition. In 2025, Signify secured multiple agency contracts after receiving cryptographic certification, cementing its role as the default choice for secure indoor links. In March 2026, pureLiFi unveiled Connectivity DNA and the Bridge XC Flex window unit, a five-minute self-install product aimed at telcos seeking last-mile solutions. Terra Ferma opened a Colorado Springs plant to localize defense supply chains, and Latécoère integrated Li-Fi hardware into aircraft cabin structures to deliver seat-level gigabit service.

Component specialists such as KYOCERA SLD Laser, Broadcom, and Lite-On are bringing VCSEL arrays and high-sensitivity photodetectors to market, enabling second-tier integrators to enter without full optical R&D. Growing chipset availability is expected to lower hardware costs and shift competition toward software, security, and network-management features. As IEEE working groups extend standards from fixed infrastructure to mobile devices, the playing field will likely broaden, favoring firms that combine silicon expertise with scalable cloud orchestration.

Light Fidelity (Li-Fi) Industry Leaders

Signify N.V.

pureLiFi Ltd

Oledcomm SAS

LiFi Group

Panasonic Holdings Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: pureLiFi unveiled its 10 Gbps Connectivity DNA platform at Mobile World Congress, confirming deliveries of the Bridge XC Flex self-install window unit later in 2026.

- January 2026: Researchers at ISEL-IPL and CTS-UNINOVA-LASI demonstrated a visible-light AGV coordination system sustaining 500 vehicle arrivals per hour at SPIE Photonics West.

- November 2025: Terra Ferma confirmed a USD 1.3 million Li-Fi manufacturing facility in Colorado Springs, creating 120 jobs to serve defense and aerospace buyers.

- October 2025: Nav Wireless Technology completed the first commercial Li-Fi deployment in New York hospitals, transmitting patient records without RF interference.

Global Light Fidelity (Li-Fi) Market Report Scope

The Light Fidelity Market Report is Segmented by Application (Indoor Networking and Enterprise, Healthcare and Medical Devices, Vehicle and Transportation, Underwater and Maritime, Aerospace and Defense, Smart Home and Consumer Electronics, Industrial Automation and Warehouse), Component (LEDs, Photodetectors, Micro-Controllers and Modulators, Optical Filters and Lenses, Software and Services), Form Factor (Li-Fi Lamps/Luminaires, Li-Fi Dongles and Access Keys, Li-Fi Modules/Chipsets, Integrated Li-Fi Fixtures), End-User (Enterprises, Government and Defense, Residential, Transportation and Logistics, Industrial Manufacturing), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Application

| Indoor Networking and Enterprise |

| Healthcare and Medical Devices |

| Vehicle and Transportation |

| Underwater and Maritime |

| Aerospace and Defense |

| Smart Home and Consumer Electronics |

| Industrial Automation and Warehouse |

By Component

| LEDs |

| Photodetectors |

| Micro-Controllers and Modulators |

| Optical Filters and Lenses |

| Software and Services |

By Form Factor

| Li-Fi Lamps/Luminaires |

| Li-Fi Dongles and Access Keys |

| Li-Fi Modules/Chipsets |

| Integrated Li-Fi Fixtures |

By End-User

| Enterprises |

| Government and Defense |

| Residential |

| Transportation and Logistics |

| Industrial Manufacturing |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Application | Indoor Networking and Enterprise | ||

| Healthcare and Medical Devices | |||

| Vehicle and Transportation | |||

| Underwater and Maritime | |||

| Aerospace and Defense | |||

| Smart Home and Consumer Electronics | |||

| Industrial Automation and Warehouse | |||

| By Component | LEDs | ||

| Photodetectors | |||

| Micro-Controllers and Modulators | |||

| Optical Filters and Lenses | |||

| Software and Services | |||

| By Form Factor | Li-Fi Lamps/Luminaires | ||

| Li-Fi Dongles and Access Keys | |||

| Li-Fi Modules/Chipsets | |||

| Integrated Li-Fi Fixtures | |||

| By End-User | Enterprises | ||

| Government and Defense | |||

| Residential | |||

| Transportation and Logistics | |||

| Industrial Manufacturing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast can Li-Fi deliver data in real deployments?

Commercial systems now ship at 1-2 Gbps, and vendor demonstrations have reached 10 Gbps, supporting high-bandwidth enterprise and industrial applications.

What are the main cost drivers when adopting Li-Fi for offices?

Upfront spending centers on Li-Fi-enabled luminaires and per-user dongles, although retrofit projects offset some expense by reusing existing LED fixtures and wiring.

Which vertical is forecast to grow the fastest in Li-Fi adoption by 2031?

Transportation and logistics, fueled by automated guided vehicle coordination in warehouses, is projected to post the steepest CAGR through 2031.

How does Li-Fi enhance network security compared with Wi-Fi?

Optical signals stay within the illuminated area and cannot penetrate walls, creating a physically contained link that reduces eavesdropping and jamming risk.

When will native Li-Fi chipsets appear in mainstream laptops and phones?

Early integrations are scheduled to reach select commercial devices after 2026, with broader consumer rollout expected once 802.11bb volumes drive chipset cost down.

What region is projected to attract the most aggressive Li-Fi investment over the forecast window?

Asia-Pacific is set for the highest growth rate as government-backed pilots in China, India, Japan, and South Korea scale into full deployments.

Page last updated on: