Lawful Interception Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.47 Billion |

| Market Size (2031) | USD 14.98 Billion |

| Growth Rate (2026 - 2031) | 18.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lawful Interception Market Analysis by Mordor Intelligence

The lawful interception market size is expected to grow from USD 5.47 billion in 2025 to USD 6.47 billion in 2026 and is forecast to reach USD 14.98 billion by 2031 at 18.27% CAGR over 2026-2031. The surge reflects governments’ intensifying focus on national-security readiness, expanding regulatory mandates, and the technical complexity introduced by 5G, cloud, and encryption. Demand is accelerating as threat actors exploit digital ecosystems faster than legacy surveillance tools can adapt, prompting agencies to adopt AI-driven analytics for real-time pattern recognition. Vendors able to integrate mediation devices, decryption modules, and behavioural analytics on a single platform are well-positioned, especially as enterprises outside law enforcement face new compliance pressures. Competitive intensity is rising because telecom-equipment majors now bundle interception modules with 5G network gear, squeezing margins for stand-alone providers.

Key Report Takeaways

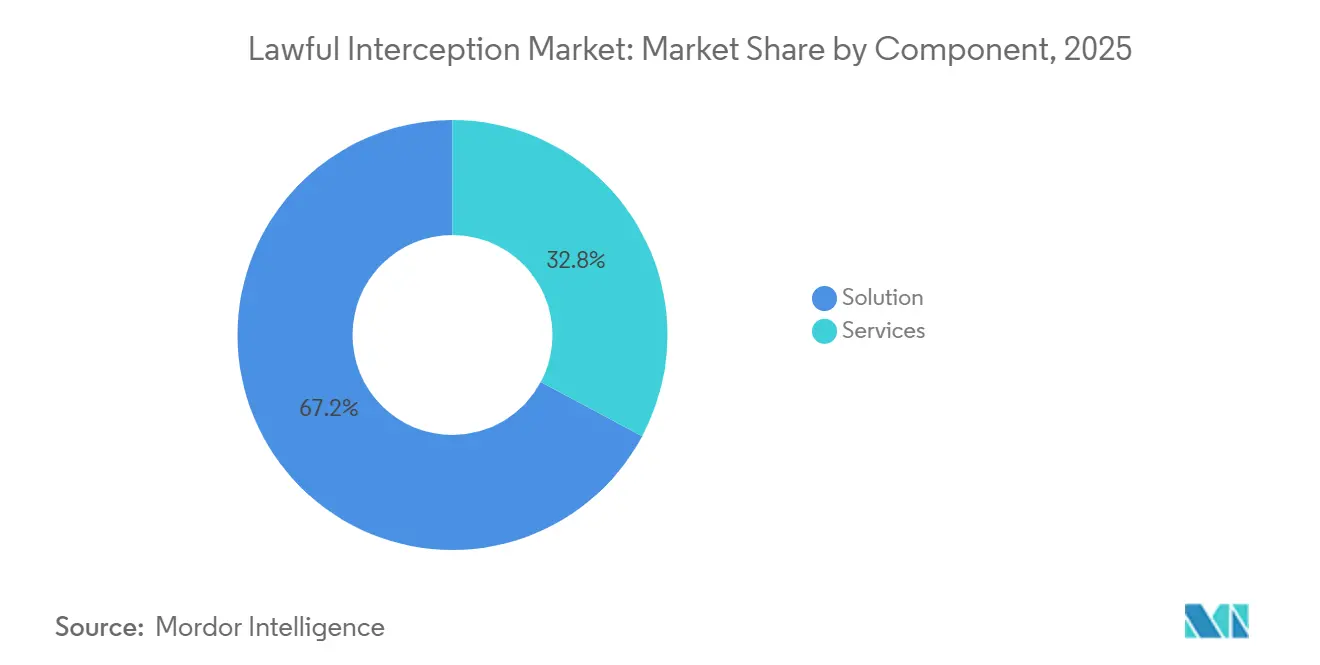

- By component, solutions captured 67.20% of the lawful interception market share in 2025, while services are expanding at a 18.62% CAGR through 2031.

- By network type, mobile networks led with 50.60% of the lawful interception market size in 2025; IP networks are projected to grow at a 19.05% CAGR to 2031.

- By communication channel, voice retained 44.90% revenue share in 2025, whereas social media and OTT messaging are poised for an 18.41% CAGR to 2031.

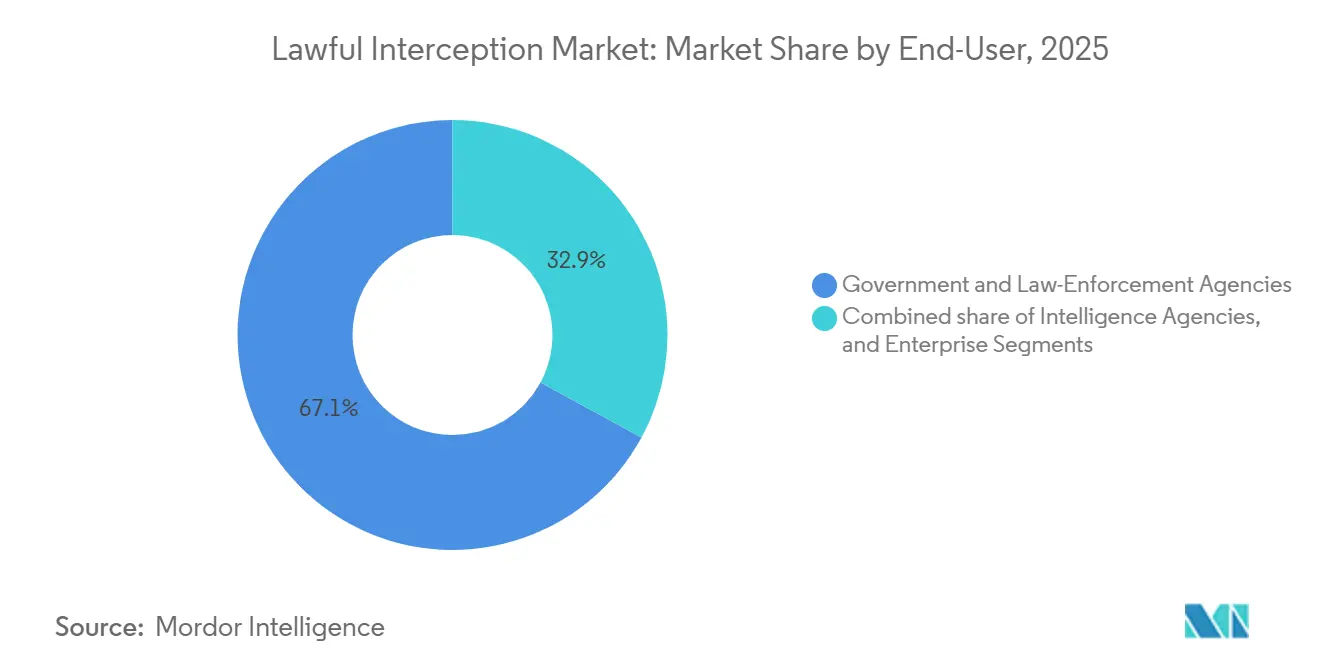

- By end-user, government and law-enforcement agencies held 67.10% share, but enterprises are advancing at a 19.30% CAGR through 2031.

- By deployment mode, on-premise solutions commanded 69.30% of the lawful interception market size in 2025, while cloud/hosted models are forecast to rise at a 19.12% CAGR.

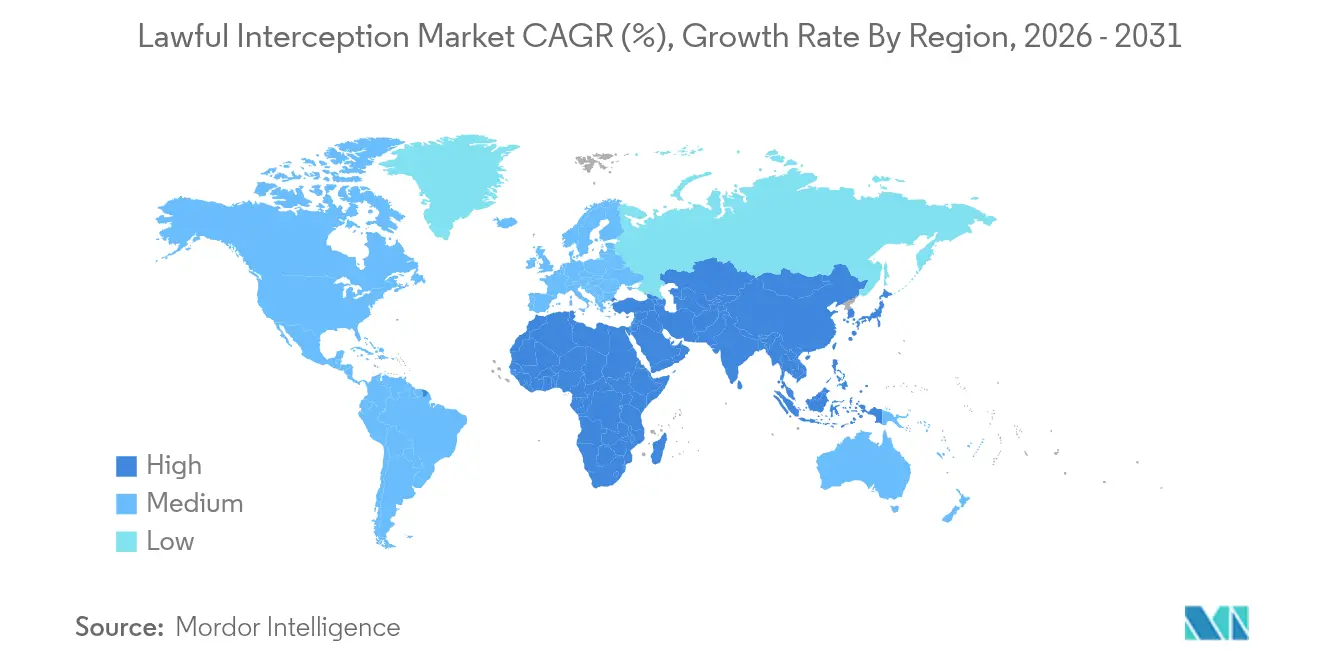

- By region, North America maintained 38.85% share in 2025 and Asia-Pacific is the fastest-growing region at a 19.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lawful Interception Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cyber-threats and national security concerns | +4.2% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Regulatory mandates and compliance requirements | +3.8% | EU, North America, global | Medium term (2-4 years) |

| Proliferation of IP-based and 5G communications | +3.5% | Asia-Pacific, North America, global | Medium term (2-4 years) |

| Shift toward cloud-hosted interception platforms | +2.9% | North America, Europe expanding to Asia-Pacific | Long term (≥ 4 years) |

| AI-driven real-time metadata analytics ROI | +2.1% | Initially North America and Europe, then global | Long term (≥ 4 years) |

| Digital-evidence admissibility frameworks | +1.5% | Global with regional legal-standard variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Threats and National Security Concerns

Geopolitical tensions and state-sponsored cyber operations are elevating interception budgets across North America, Europe, and Asia-Pacific. The U.S. Department of Defense’s 2024 assessment of China’s cyber-warfare posture underscores the urgency for advanced listening posts capable of simultaneous multi-channel surveillance.[1]U.S. Department of Defense, “Military and Security Developments Involving the People’s Republic of China 2024,” defense.gov MITRE’s December 2024 review of ubiquitous technical surveillance argues that AI-enabled analytics convert raw intercepts into actionable intelligence, driving agencies to upgrade beyond voice taps. Rapid detection of coordinated threat patterns now hinges on real-time correlation across 5G slices, satellite links, and encrypted messaging. Vendors offering integrated analytics suites rather than siloed probes therefore gain competitive traction. National-level procurement programs, particularly in the United States, United Kingdom, Australia, and Japan, continue to drive baseline demand.

Regulatory Mandates and Compliance Requirements

Governments worldwide are tightening legal frameworks that oblige telecom operators and digital platforms to furnish lawful-access capabilities. The EU’s 2024 dual-use export-control update demands enhanced due diligence for surveillance tools, favoring vendors with mature compliance documentation. India’s draft Telecommunication Bill and its 2024 National Cyber Coordination Centre (NCCC) specifications for 5G interception codify detailed technical blueprints, steering local carriers toward tested 3GPP-conformant solutions. Financial institutions must now align interception records with FinCEN’s cross-border funds tracing obligations, expanding enterprise spending on compliance monitoring. As regulators reference 3GPP TS 33.106/107 for architectural guidance, vendors embedded in standards committees enjoy accelerated adoption.

Proliferation of IP-Based and 5G Communications

Migration from circuit-switched voice to IP packets reshapes interception topologies. Cisco’s Service-Independent Intercept blueprint illustrates how packet flows require mediation, filtering, and lawful hand-over interfaces distinct from legacy voice environments. 5G network slicing and MEC deployments demand edge-based intercept points, as highlighted by ETSI’s 2024 guidance on multi-access edge computing. Juniper Networks’ user-plane lawful-intercept implementation confirms that vendors must marry deep-packet inspection with high-throughput scaling to sustain compliance under 5G traffic loads. Packetized data streams also unlock richer metadata for behavioural analytics, enabling agencies to pivot from retrospective searches to predictive monitoring.

Shift Toward Cloud-Hosted Interception Platforms

Cost, elasticity, and rapid deployment are pushing carriers toward cloud-native lawful interception market solutions. PertSol’s micro-services architecture supports containerized deployment in private or public clouds, demonstrating how interception can scale horizontally while preserving cryptographic integrity. Ribbon Communications’ November 2024 study shows that multi-tenant, cloud-native IMS platforms deliver carrier-grade uptime with 40% lower total cost of ownership versus fixed hardware. Emerging markets in Southeast Asia and Latin America use cloud licensing models to avoid heavy upfront capex. Cloud environments also integrate AI engines more readily, enabling real-time anomaly detection without on-premise GPU farms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy-rights backlash and data-protection laws | -2.8% | Europe, North America, global | Short term (≤ 2 years) |

| High cost and complexity of multi-network build-out | -2.1% | Global with pronounced effect in emerging markets | Medium term (2–4 years) |

| Vendor lock-in limits interoperability | -1.7% | Global enterprise and telecom ecosystems | Medium term (2–4 years) |

| “Encryption-by-default” policies in Over-The-Top (OTT) apps | -2.4% | Global, especially privacy-regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy-Rights Backlash and Data-Protection Laws

Civil-liberties pressure and stringent data-protection statutes temper the adoption of expansive surveillance tools, particularly in Europe and North America. The European Data Protection Board’s February 2025 guidance on AI privacy risks calls for algorithmic transparency and data minimisation, raising hurdles for blanket data collection in AI-enhanced interception[2]European Data Protection Board, “Guidelines on AI Privacy Risks,” edpb.europa.eu. Fragmented Member-State rules compel carriers to maintain disparate compliance workflows, adding cost. Advocacy groups continue to litigate algorithmic bias and mass-surveillance claims, forcing vendors to introduce selective targeting and robust oversight dashboards. In parallel, end-to-end encryption defaults on OTT platforms limit interception scope, intensifying the policy debate on exceptional-access mandates.

High Cost and Complexity of Multi-Network Build-Out

Operators must sustain simultaneous interception across legacy 2G/3G, 4G/LTE, 5G, fixed, and IP domains. 3GPP’s February 2025 Athens meeting advanced security-assurance requirements for 5G standalone deployments, compelling vendors to iterate hardware and software every release cycle. Smaller carriers face budget and skills shortages as they integrate diverse mediation devices, edge probes, and analytics engines. Interoperability challenges worsen when multi-vendor RAN and core elements lack uniform hand-over interfaces, inflating project timelines and cost overruns. These factors restrain lawful interception market uptake in emerging nations where capital allocation competes with basic coverage rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gaining Momentum Despite Solution Dominance

Solutions accounted for 67.20% of the lawful interception market share in 2025, underpinned by demand for mediation devices, interception access points, and analytics platforms. However, the services segment is projected to rise at a 18.62% CAGR as carriers and enterprises outsource integration, regulatory mapping, and lifecycle support. Consulting engagements that translate 3GPP specifications into actionable deployment blueprints remain in high demand, especially as 5G slicing adds architectural nuance. Managed interception services appeal to smaller operators lacking round-the-clock security staff. Within solutions, interception-management software enjoys the highest velocity because AI modules that parse encrypted payloads drive analytic value. Decryption engines and behavioural-analysis add-ons complement core probes, enabling proactive anomaly alerts. Mediation devices face commoditisation pressure from software-defined alternatives, yet they retain importance for legacy circuit-switched domains. The lawful interception market thus tilts toward platforms that bundle hardware abstraction with cloud-ready orchestration.

Rapid regulatory churn further elevates service value. Advisory teams guide carriers through export-control assessments and privacy-impact audits, minimising compliance risk. Continuous-integration support ensures that probe firmware aligns with quarterly 3GPP releases. Training services equip investigators to exploit AI dashboards, shortening mean-time-to-insight. As multi-tenant cloud deployments proliferate, vendors expand DevSecOps offerings to automate patching and verification. Consequently, although solutions remain dominant, recurring-revenue streams from professional and managed services increasingly stabilise vendor revenue profiles in the lawful interception market.

By Network: IP Networks Disrupting Traditional Mobile Dominance

Mobile infrastructure held 50.60% of the lawful interception market size in 2025, reflecting entrenched GSM, UMTS, and LTE monitoring foundations. Yet IP networks are advancing at a 19.05% CAGR because VoIP, VoLTE, and OTT traffic shift communications toward packet domains. Packet orientation unlocks metadata richness, allowing agencies to map social graphs and behavioural patterns unavailable in narrowband voice. Network slicing under 5G standalone creates virtual sub-nets that bypass legacy core probes, prompting demand for edge-resident intercept functions. Vendors able to merge user-plane probes with high-throughput packet brokers capture mindshare among tier-one carriers.

The fixed-network segment remains stable but slides slowly as copper retirements accelerate. Hybrid VoLTE deployments blur mobile and IP boundaries, forcing unified interception orchestration across RAN, core, and IMS domains. NEC’s certification of trans-Pacific lawful-intercept compliance with SS8 illustrates cross-ocean packet-intercept requirements for submarine routes. Within the mobile category, 3G/4G networks still generate majority probe volumes, but 5G traffic grows exponentially, pushing vendors to engineer 100 Gbps capture rates without packet loss. Consequently, investment tilts toward scalable, virtualised IP-intercept frameworks that future-proof carriers against surging encrypted traffic.

By Communication Channel: Social Media and OTT Messaging Driving Innovation

Voice interception contributed 44.90% revenue in 2025, yet social media and OTT messaging are forecast to expand at an 18.41% CAGR. Encryption-by-default on platforms such as WhatsApp and Signal challenges legacy lawful-access tactics, fuelling R&D in metadata analysis, endpoint interception, and lawful hacking. EU policy proposals to sanction non-cooperative providers increase pressure for traceability architectures, creating market openings for vendors offering compliance gateways within messaging stacks. Data communication channels, encompassing transactional messaging and IoT telemetry, form a stable mid-tier and benefit from exponential device growth.

OTT expansion compels analytics engines to correlate user, device, and application identifiers across layered protocols. Vendors integrate artificial-intelligence modules that infer intent from message frequency, contact patterns, and geolocation instead of decrypting content. Voice remains crucial for high-value targets in organised crime, but its relative share declines as younger cohorts prefer text and multimedia. Data-focused interception gains traction in financial crimes monitoring, where suspicious transaction routing often surfaces inside packet headers and payload metadata. The lawful interception market thus diversifies toward channel-agnostic platforms capable of ingesting heterogeneous data streams.

By End-User: Enterprise Adoption Accelerating Beyond Government Foundation

Government and law-enforcement bodies generated 67.10% of the lawful interception market revenue in 2025. Their spend remains anchored in national-security programmes, counter-terrorism, and organised-crime disruption. Even so, enterprise demand is set to rise at a 19.30% CAGR as sectors such as finance and healthcare face stricter communications-monitoring mandates. FinCEN’s cross-border fund-transfer rule compels banks to implement message-flow interception that maps wire-room instructions to customer profiles. The U.S. Department of Health and Human Services’ January 2025 HIPAA security proposal introduces obligations for healthcare providers to spot anomalous access, nudging them toward interception-enabled audit trails.

Intelligence agencies, while narrower in number, maintain premium-grade requirements for multilingual, multi-modal data fusion and long-range predictive analytics. Enterprises gravitate to software-as-a-service models that pivot government-grade capabilities into cost-effective compliance dashboards. Vendors package sector-specific rule libraries, such as BSA/AML for banking, reducing deployment times. However, price sensitivity and privacy concerns demand rigorous data minimisation and policy-based access control. As enterprise adoption scales, the lawful interception industry widens its addressable base beyond sovereign buyers, diversifying revenue.

By Deployment Mode: Cloud Migration Accelerating Despite On-Premise Dominance

On-premise platforms accounted for 69.30% of lawful interception market revenue in 2025, reflecting sovereignty mandates, classified-network isolation, and auditor confidence in local data control. Rising cybersecurity threats still persuade military and intelligence agencies to maintain air-gapped architectures. Yet cloud/hosted lawful-interception-as-a-service is predicted to grow at 19.12% CAGR because micro-service designs shorten installation cycles and cut capex. PertSol and Ribbon Communications offer Kubernetes-based probes that auto-scale on commodity hardware, attractive for tier-two carriers and mobile virtual-network operators.

Hybrid models are emerging as a pragmatic compromise. Sensitive payload decryption may remain on-premise, while non-classified metadata analytics burst into cloud GPUs for high-speed processing. Gorilla Technology’s late-2024 contracts in Taiwan demonstrate how law enforcement can leverage cloud AI engines without relinquishing raw payload custody. Managed-service options further address skills shortages by folding DevSecOps, patching, and compliance reporting into monthly fees. While on-premise will dominate high-security niches, the lawful interception market trajectory points toward elastic deployment frameworks that balance control with cost.

Geography Analysis

North America retained 38.85% of the lawful interception market size in 2025, supported by federal funding, mature telecom infrastructure, and vendor ecosystems that shape global standards. U.S. agencies continue to refine Communications Assistance for Law Enforcement Act provisions, bolstering domestic demand for upgraded probes. Canada’s 5G supply-chain security reviews add urgency for carriers to certify interception compliance amid geopolitical scrutiny. Regional leadership in AI research accelerates the adoption of advanced analytics modules, feeding virtuous cycles of innovation and procurement. Heightened ransomware and state-sponsored hacking incidents sustain budget allocations, ensuring steady platform refreshes.

Asia-Pacific is projected to post the fastest regional CAGR at 19.36% through 2031. Rapid 5G roll-outs require intercept mechanisms for network slices and edge clouds, tasks codified by India’s NCCC technical framework. Australia, Japan, and South Korea apply stringent critical-infrastructure rules, spurring proactive system upgrades. Meanwhile, Southeast Asian operators embrace cloud-hosted probes to avoid heavy capex, aligning with regional digital-transformation agendas. China’s expanding cyber-warfare doctrine is prompting neighbouring states to harden domestic surveillance capabilities, reinforcing demand for AI-driven analytics. The region, however, presents heterogeneous legal regimes, compelling vendors to tailor compliance packs per jurisdiction.

Europe exhibits a complex interplay of privacy safeguards and security imperatives. The European Commission’s High-Level Group recommendation to sanction non-cooperative OTT providers spotlights a regulatory tilt toward traceable communications. Yet GDPR obligations mandate data minimisation and lawful-purpose constraints, increasing deployment complexity. Fragmented member-state regulations mean that carriers often must maintain parallel mediation gateways to accommodate differing LI handover formats. Established vendors with extensive legal libraries, therefore, gain a competitive advantage. Elsewhere, Latin America, the Middle East, and Africa remain nascent yet promising; operators there balance interception investments against ongoing infrastructure build-outs, often turning to cloud services that circumvent heavy local hardware outlays.

Competitive Landscape

The lawful interception market is moderately fragmented but trending toward consolidation as 5G and encryption heighten technical barriers. Established niche specialists such as SS8, Verint spinoff Cognyte, and Utimaco (Now Nexburg) defend share through deep protocol expertise and long-standing government certifications. Cognyte reported USD 350.6 million revenue in fiscal 2025, underscoring the scale possible for software-centric players focused on AI-powered analytics. Telecommunications-equipment majors, Nokia, Ericsson, Cisco, embed interception hooks directly into network functions, leveraging their infrastructure footprint to cross-sell compliance options. This integration accelerates adoption but pressures pure-play probe vendors on pricing.

Strategic alliances proliferate as complexity rises. NEC’s partnership with SS8 for trans-Pacific lawful-intercept certification showcases co-development models that combine packet-broker hardware with analytics engines[5]NEC Corporation, “NEC and SS8 Announce Trans-Pacific Lawful Interception Certification,” nec.com. Thales’s Unified Lawful Interception Suite, deployed in 40 countries with 90 customers, demonstrates the edge enjoyed by companies offering end-to-end compliance toolkits. Smaller innovators pivot to cloud-native SaaS and AI specialisation, differentiating through real-time behavioural analytics rather than packet capture alone. Some are targets for acquisition by larger integrators seeking rapid capability uplifts.

Technology road-maps coalesce around virtualised probes, 3GPP compliance, and encryption-aware analytics. Vendors invest in GPU-accelerated processing, zero-trust architectures, and explainable AI to satisfy court admissibility tests. Standards participation offers first-mover insight into forthcoming hand-over definitions, a tactic leveraged by Ericsson and Nokia inside 3GPP working groups. Market success increasingly hinges on delivering scalable, hybrid deployment models that lower total cost while meeting location-based data-sovereignty rules.

Lawful Interception Industry Leaders

SS8 Networks, Inc.

Verint Systems Inc.

Vocal Technologies Ltd.

Aqsacom Inc.

Nexburg GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nexburg GmbH (Formerly Utimaco) announced its 5G ID Associator and S8HR solutions at ISS World Europe 2025, emphasising 3GPP compliance.

- February 2025: The European Data Protection Board issued AI privacy-risk guidance that impacts AI-enhanced interception platforms.

- February 2025: 3GPP SA WG3 meeting 120 advanced 5G security-assurance and lawful-interception specifications.

- January 2025: The U.S. Department of Health and Human Services proposed tougher HIPAA cybersecurity rules, raising healthcare compliance needs.

- January 2025: Cognyte Software reported USD 350.6 million revenue for FY 2025, driven by demand for AI-centric analytics platforms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the lawful interception market as all hardware, software, and managed platforms that enable communication service providers to deliver authorized real-time voice, data, and metadata to investigating agencies across fixed, mobile, and IP networks. We track solution revenues generated from mediation devices, intercept access points, gateways, management servers, and related analytics layers.

Scope exclusion: resale of legacy passive probes that do not feed a standards-based hand-over interface is not included.

Segmentation Overview

- By Component

- Solution

- Mediation devices

- Interception access points

- Interception management software

- Decryption and analytics modules

- Services

- Consulting

- Integration and deployment

- Support and maintenance

- Solution

- By Network

- Fixed networks

- Public Switched Telephone Network (PSTN)

- Broadband

- Mobile networks

- Global System for Mobile Communications (GSM)

- General Packet Radio Service (GPRS)

- 3G/4G/LTE

- 5G and future Radio Access Network (RAN)

- IP networks

- Voice over Internet Protocol (VoIP)

- Data-traffic monitoring

- Fixed networks

- By Communication Channel

- Voice communication

- Data communication

- Social media and OTT messaging

- By End-User

- Government and Law-Enforcement Agencies

- Intelligence agencies

- Enterprises

- By Deployment Mode

- On-premise

- Cloud/Hosted LI-as-a-Service

- By Geography

- North America

- United States

- Canada

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed network-security officers at tier-1 operators, compliance leads in law-enforcement units, and regional system integrators across North America, Europe, and Asia. These conversations validated price bands, typical port densities, and the pace at which 5G core upgrades embed interception hooks.

Desk Research

We began by mapping demand signals using publicly available sources such as ETSI and 3GPP standards releases, ITU mobile-subscription dashboards, U.S. CALEA compliance filings, European Council cyber-crime directives, and import data scraped from Volza for interception-ready routers. Financial notes from listed telecom operators, annual budgets for domestic security agencies, and patent volumes retrieved through Questel helped us size addressable spend. Internal paid feeds, Dow Jones Factiva for deal news and D&B Hoovers for supplier financials, filled historic gaps. Country-level telecom traffic from the World Bank, spectrum-auction disclosures, and regional trade association statistics refined adoption curves. The sources named are illustrative; many additional documents were consulted to cross-check numbers and definitions.

Market-Sizing & Forecasting

A top-down demand pool was built from active broadband and mobile connections, applying penetration factors for intercept-enabled sites that vary by regulation strictness and GDP. Select bottom-up checks, supplier roll-ups and sampled average selling price per mediation port, tuned totals. Key variables include the number of 4G/5G subscriptions, average lawful-intercept requests per million subscribers, mandated retention periods, national security spending, and median solution ASP. Forecasts use multivariate regression blended with ARIMA to project how traffic growth, encryption rates, and policy amendments shape equipment refresh cycles. Where bottom-up samples were thin, we interpolated using regional analogs before reconciling with primary insights.

Data Validation & Update Cycle

Outputs pass variance screens against independent indicators (e.g., carrier capex, security-software revenues). Senior reviewers probe anomalies, and figures are refreshed annually; extraordinary events trigger mid-cycle updates. A last-mile analyst review occurs just before publication, ensuring clients receive the freshest view.

Why Mordor's Lawful Interception Market Baseline Stands Reliable

Published estimates often diverge because firms pick different device mixes, base years, and refresh cadences, and they rarely rerun models when regulations shift.

Key gap drivers include wider scopes that fold network analytics tools, reliance on supplier revenue roll-ups without traffic calibration, older base years kept constant through straight-line growth, and currency conversions frozen at announcement dates, whereas we rebalance for exchange swings and statute changes every year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.47 B (2025) | Mordor Intelligence | - |

| USD 5.14 B (2024) | Global Consultancy A | Includes network analytics and DPI licenses beyond lawful intercept mandate |

| USD 3.50 B (2021) | Industry Association B | Uses legacy voice-tap hardware only and keeps 2021 base frozen |

These comparisons show that our disciplined scope selection, annual refresh, and dual-layer validation deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the projected value of the lawful interception market by 2031?

The market is expected to reach USD 14.98 billion by 2031, expanding at an 18.27% CAGR.

Which region is growing fastest in the lawful interception market?

Asia-Pacific is forecast to grow at a 19.36% CAGR through 2031, driven by rapid 5G deployment and evolving cybersecurity regulations.

Why are services gaining traction within the lawful interception industry?

The complexity of 5G architectures and shifting regulatory mandates require specialised integration, compliance, and managed-service support, resulting in a 18.62% CAGR for the services segment.

How is cloud adoption impacting lawful interception solutions?

Cloud-hosted interception platforms offer scalability and lower capex, driving a 19.12% CAGR for cloud deployments while enabling AI-driven real-time analytics.

Which network type will grow fastest for lawful interception deployments?

IP networks are set to expand at a 19.05% CAGR as communications migrate from circuit-switched voice to packet-based services.

What are the main restraints limiting lawful interception market growth?

Strong privacy-rights regulation and the high cost of multi-network build-outs reduce growth by an estimated 2.8% and 2.1% respectively over the forecast period.

Page last updated on: