Colombia Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

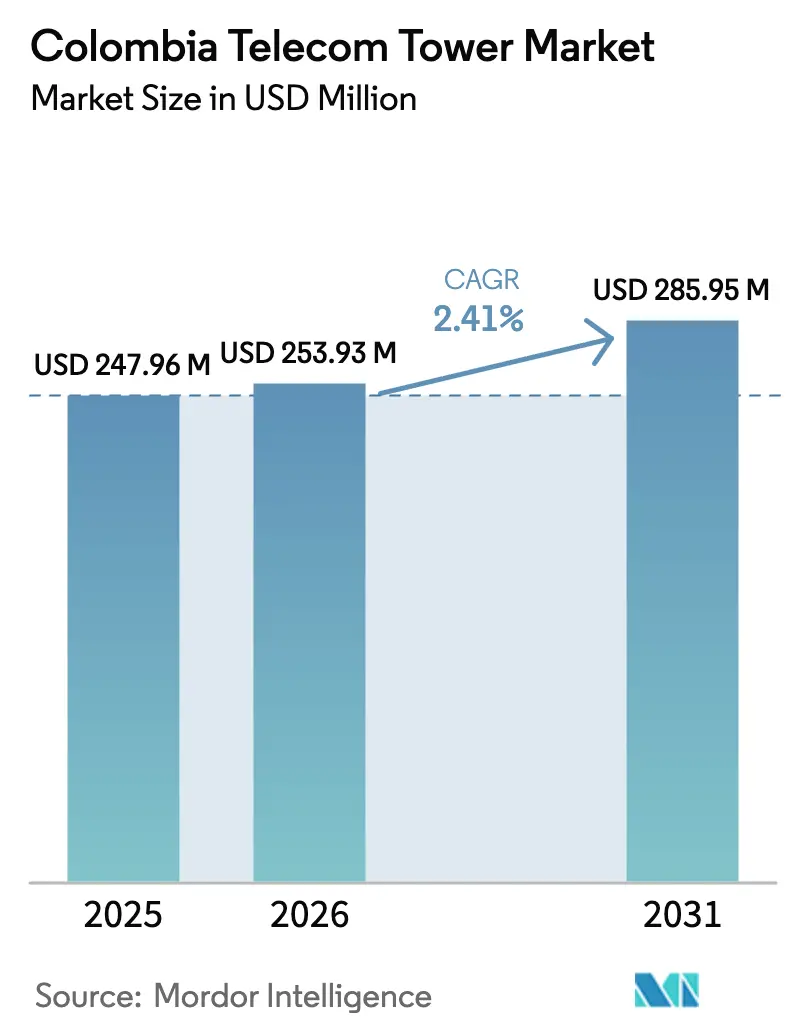

| Base Year Market Size (2025) | USD 247.96 Million |

| Market Size (2026) | USD 253.93 Million |

| Market Size (2031) | USD 285.95 Million |

| Growth Rate (2026 - 2031) | 2.41% CAGR |

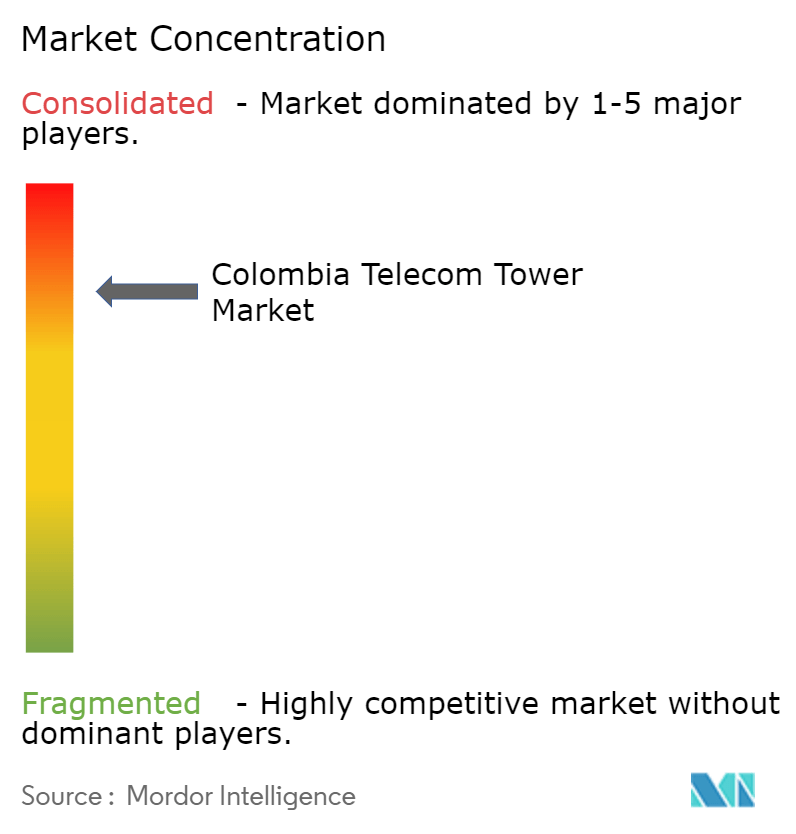

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Telecom Tower Market Analysis by Mordor Intelligence

Colombia Telecom Tower Market size in 2026 is estimated at USD 253.93 million, growing from 2025 value of USD 247.96 million with 2031 projections showing USD 285.95 million, growing at 2.41% CAGR over 2026-2031.

This trajectory reflects the incremental but steady monetization of passive infrastructure as operators pivot to 5G spectrum obligations, rural coverage targets, and carbon-reduction goals. Independent TowerCos already manage nearly two-thirds of active sites, while renewable-powered systems post double-digit growth that sharply contrasts with the grid-diesel status quo. Elevated mobile-data traffic, spectrum auctions that require dense antenna roll-outs, and network-sharing deals among carriers will support consistent tenancy additions. At the same time, peso depreciation pressures and complex municipal permitting act as near-term headwinds, prompting tower companies to refine hedging strategies and accelerate small-cell rooftops that shorten time to revenue. Overall, the Colombia telecom towers market continues to shift from an operator-owned footprint toward a neutral-host model that unlocks balance-sheet liquidity for 5G radio investments.

Key Report Takeaways

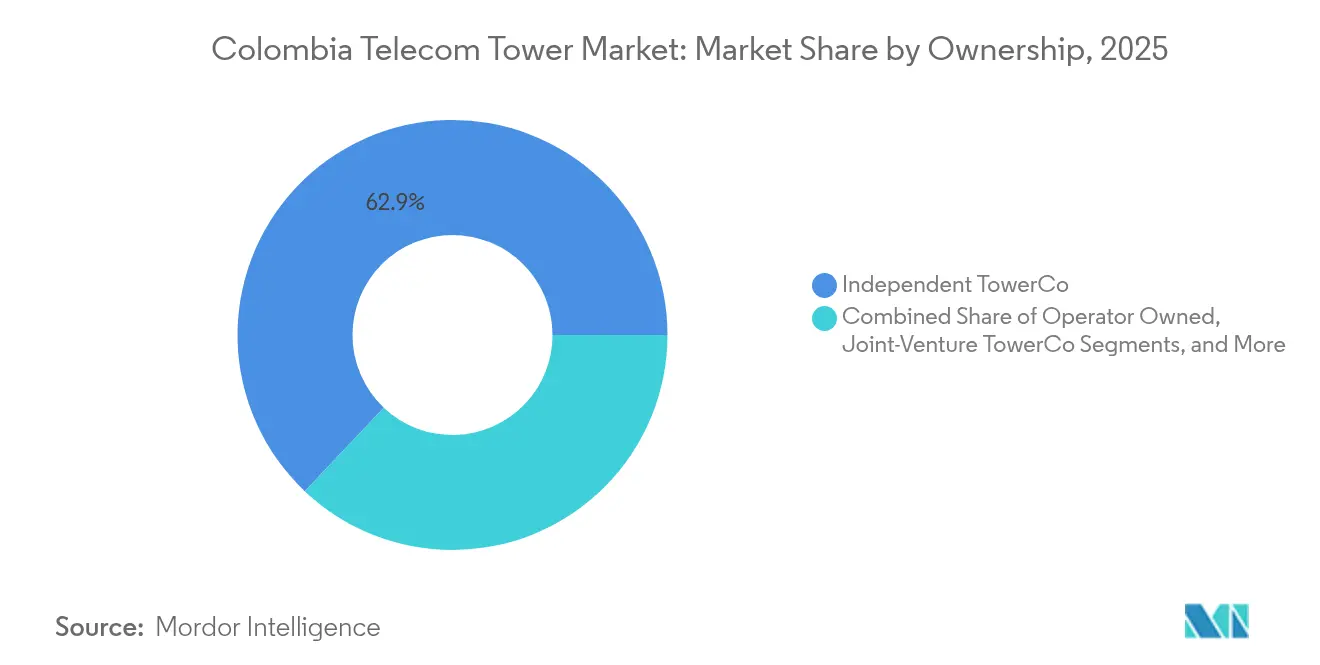

- By ownership, Independent TowerCos led with 62.94% Colombia telecom towers market share in 2025.

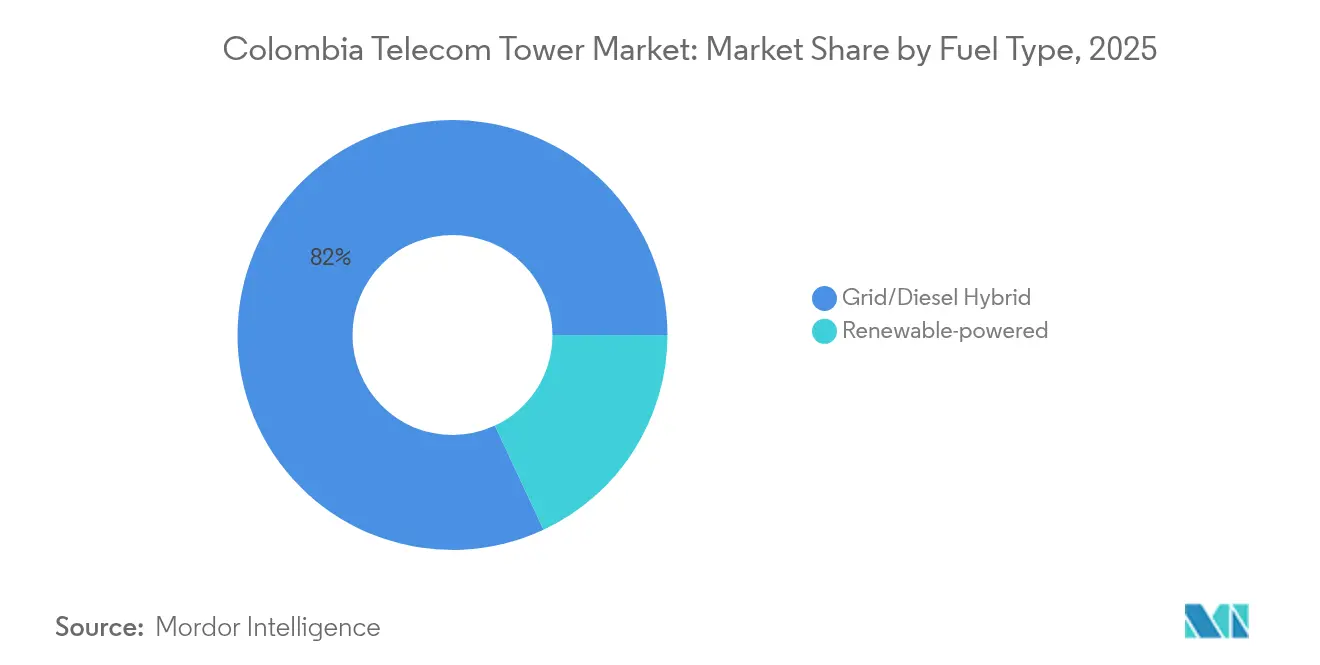

- By fuel type, renewable-powered sites are advancing at an 17.60% CAGR through 2031 and represent the fastest growing slice of the Colombia telecom towers market size.

- By installation, ground-based structures retained 54.86% revenue share in 2025, while rooftop sites are projected to expand at a 4.33% CAGR through 2031.

- By tower type, stealth and concealed solutions are progressing at a 5.36% CAGR as urban aesthetic norms tighten.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum auction accelerating tower densification | +0.6% | Major urban corridors nationwide | Medium term (2-4 years) |

| Rising mobile data consumption and subscriber growth | +0.8% | Nationwide, urban concentration | Long term (≥ 4 years) |

| Operator network-sharing and outsourcing to TowerCos | +0.4% | Nationwide | Medium term (2-4 years) |

| Government rural-connectivity mandates driving BTS roll-outs | +0.3% | Rural PDET zones | Long term (≥ 4 years) |

| Fixed-wireless access demand in underserved municipalities | +0.2% | Rural and peri-urban | Medium term (2-4 years) |

| Edge-computing co-location for agricultural IoT in coffee belt | +0.1% | Central Andes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Spectrum Auction Accelerating Tower Densification

The December 2023 5G auction raised USD 1.37 billion and handed 80 MHz blocks in the 3.5 GHz band to four licensees who must meet phased coverage mandates. [1]Europa Press Newswire, “Colombia Raises USD 1.37 Billion in 5G Auction,” europapress.esClaro alone activated 1,200 of its planned 1,400 5G antennas by October 2024 across 14 cities, reducing cell spacing to sub-kilometer intervals that favor rooftop and small-cell deployments. [2]BNamericas Staff, “Claro Reaches 1,200 5G Antennas,” bnamericas.comBecause millimeter-wave signals attenuate quickly, densification requirements multiply site counts versus legacy 4G grids, pushing neutral hosts to negotiate rapid municipal clearances and leverage existing vertical real estate. Nokia supplies core network gear, and the government estimates total 5G infrastructure investment at COP 25 trillion over the coming decade. These forces position the Colombia telecom towers market as a direct beneficiary of obligatory build-outs that guarantee long-term tenancies and incremental power-conversion upgrades.

Rising Mobile Data Consumption and Subscriber Growth

Mobile internet lines climbed to 44.9 million in 2023—12.07% above 2022—while data traffic reached 4.15 million TB, up 37.6%. [3]Comisión de Regulación de Comunicaciones, “Mobile Internet Statistical Report 2023,” crc.gov.co Despite heavy urban usage, nearly 80% of rural citizens still lack broadband, so operators extend footprints to satisfy universal-service quotas. WOM supports 6.4 million users on 5,100 antennas across 725 municipalities, underscoring the scale of coverage required for national parity. Average download speeds remain among Latin America’s slowest, stressing networks and calling for additional backhaul and edge nodes. With more than 29,000 mobile sites in place, the shift to 5G and fixed-wireless access continues to stimulate leasing demand in the Colombia telecom towers market.

Operator Network-Sharing and Outsourcing to TowerCos

MinTIC cleared the Movistar-Tigo unified RAN in January 2025, spotlighting co-build models that compress capital intensity and accelerate coverage. Millicom divested 1,100 towers to KKR entities in early 2024, and SBA Communications sold 206-site portfolios, illustrating monetization pressure on carriers. Independent TowerCos already control 63.51% of active sites and are expanding at a 5.09% CAGR through 2030 as multi-tenant economics unlock steady EBITDA margins. Shared infrastructure lowers duplication in rural zones and helps operators redirect capital into spectrum payments, directly fueling tenancy ratios and boosting the Colombia telecom towers market.

Government Rural-Connectivity Mandates Driving BTS Roll-outs

The “Conecta TIC 360” roadmap aims for 85% national internet coverage by 2026 and is backed by nearly USD 20 billion in blended public financing. Complementary initiatives—National Fiber Optic, Zonas Comunitarias para la Paz, and Centros Digitales—seed Wi-Fi points, fiber trunks, and community committees in PDET municipalities. These subsidies de-risk build-to-suit projects for tower companies that otherwise face thin economics in sparsely populated terrain. As a result, rural lattices and monopoles increasingly adopt renewable powerplants that mitigate diesel logistics. Mandatory service-level milestones continue to inject structural growth into the Colombia telecom towers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex municipal permitting and land-acquisition delays | -0.4% | Bogotá and main metros | Short term (≤ 2 years) |

| Peso depreciation hitting USD-linked lease rates | -0.3% | Nationwide | Medium term (2-4 years) |

| Tenant insolvency risk from financially distressed operators | -0.2% | Nationwide, higher in rural corridors | Medium term (2-4 years) |

| Regulatory enforcement of spectrum-payment defaults | -0.1% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Municipal Permitting and Land-Acquisition Delays

Bogotá’s Decreto 083-2023 requires engineering studies, EMF compliance, soil tests, and heritage reviews within a nominal 15-day window, yet multi-agency workflows often elongate approvals. National harmonization via Decreto 1031 is slated for 2026, but interim stamp-tax hikes elevate transaction costs and affect site economics. ANLA licensing adds layers for projects near protected habitats, and minimum 25 m radii between structures restrict viable plots. Combined, these hurdles delay launch timelines and temporarily cap new revenue streams, tempering short-term upside in the Colombia telecom towers market.

Peso Depreciation Hitting USD-Linked Lease Rates

American Tower models 4,300-4,410 COP/USD rates for 2025 and flags revenue drag above 6% from translation effects. Because most lease contracts are dollar-indexed, local-currency rents compress when the peso weakens, squeezing gross margins for TowerCos and dampening free-cash flow available for expansion. Operators with peso-denominated expenses benefit asymmetrically, compounding negotiation complexity. Volatility also reduces asset valuations, raising return hurdles for foreign investors exploring the Colombia telecom towers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Drive Market Consolidation

Independent TowerCos command 62.94% of the Colombia telecom towers market share in 2025, and the segment is expanding at a 4.92% CAGR through 2031. American Tower runs 4,951 sites, Phoenix Tower International oversees 2,500, and Andean Telecom Partners controls 1,600, with each leveraging national build-to-suit contracts that boost co-location ratios. Sale-leasebacks such as Millicom’s 1,100-tower divestiture to KKR exemplify operators’ shift toward asset-light models, while Movistar and Tigo rely on joint RAN frameworks to meet 5G timelines without duplicating passive capex.

Growth in this slice of the Colombia telecom towers market comes from economies of scale in permitting and energy procurement that elevate EBITDA margins. TowerCos bundle fiber backhaul and edge data-center pods, creating integrated offerings that carriers struggle to replicate internally. Competitive tendering for new PDET sites now features neutral-host stipulations, and capital markets reward their predictable cash flows with lower funding costs, reinforcing a flywheel that consolidates ownership even further.

By Installation: Ground-Based Dominance Faces Urban Rooftop Pressure

Ground-based lattices and monopoles accounted for 54.86% revenue in 2025, anchoring the Colombia telecom towers market size. Rooftop structures, however, are projected to climb 4.33% annually as city councils curb ground permits and millimeter-wave 5G forces denser grids. Claro’s initial 1,200 5G antennas relied heavily on commercial roofs in Bogotá and Medellín to sidestep 50 m separation rules on private land.

Tenancy yields remain higher on ground towers because of larger loading thresholds, yet rooftops accelerate time to revenue and lower site-acquisition capex. Landlords often demand inflation-indexed rents, so TowerCos implement standardized templates and invest in structural reinforcement to host multiple tenants. Together these factors will steadily reallocate incremental spending toward rooftops without materially undermining ground-based share through mid-decade.

By Fuel Type: Renewable Transition Accelerates Despite Grid Dominance

Grid-diesel hybrids still supply 81.96% of operational sites, mirroring Colombia’s hydropower-heavy generation matrix and legacy diesel backup norms. Renewable alternatives—primarily solar-battery systems—are advancing at an 17.60% CAGR, the fastest across any slice of the Colombia telecom towers market. Energy-as-a-Service contracts let TowerCos amortize solar arrays within four years, aided by tax exemptions on imported photovoltaic modules.

Off-grid rural projects under Conecta TIC 360 favor renewables because diesel transport adds cost and carbon penalties. TowerCos also lock in predictable OPEX, safeguarding IRR against fuel volatility. Despite higher upfront capex, declining battery prices and improved panel efficiency will lift renewable share well beyond 20% of the Colombia telecom towers market size before 2031.

By Tower Type: Stealth Solutions Gain Urban Acceptance

Lattice designs hold 21.12% market in 2025, valued for multitenant capacity and low cost per load. Stealth and concealed poles, however, are posting a 5.36% CAGR as city planners prioritize skyline aesthetics. Flagpoles, light standards, and artificial pines camouflage 5G small cells in historic districts, unlocking permits otherwise delayed by resident opposition.

Design premiums run 15-25% above standard monopoles, yet operators absorb the surcharge to meet timetable commitments and preserve community goodwill. In dense cores, stealth sites also leverage fiber back-haul for edge computing, making them strategic in the evolution of the Colombia telecom towers market toward latency-sensitive applications.

Geography Analysis

Site counts cluster in six metros—Bogotá, Medellín, Cali, Barranquilla, Cartagena, and Bucaramanga—where subscriber density and ARPU sustain multi-tenant economics. Claro’s 1,200 live 5G antennas by late 2024 are concentrated in these hubs, accelerating service differentiation and anchoring fresh lease revenues for rooftop landlords. American Tower’s 4,951-site footprint also aligns with highways that connect these cities, optimizing uptime and logistical support.

Rural divides remain stark: 79.8% of countryside residents lack mobile broadband versus 9.3% in urban zones. Government subsidy schemes, particularly in Amazon and Andean PDET municipalities, stimulate build-to-suit contracts that push the Colombia telecom towers market deeper into low-density areas. Environmental restrictions in páramo ecosystems demand creative camouflage and renewable powerplants, but EU-CAF funding packages mitigate risk and guarantee minimum revenue periods.

The coffee belt in the central Andes emerges as a secondary hotspot. Precision-agriculture pilots rely on edge nodes mounted on micro-lattices to relay sensor data and automate irrigation. AgrodatAi aims to connect 250,000 producers, illustrating latent demand that monetizes agricultural IoT traffic. Pacific coast ports like Buenaventura leverage CODISERT fiber for last-mile Wi-Fi hubs, but tower footprints still expand to backhaul satellite and microwave links, gradually enlarging the Colombia telecom towers market.

Competitive Landscape

The Colombia telecom towers market displays moderate concentration. American Tower leads with 4,951 sites, Phoenix Tower International ranks second with 2,500, and Andean Telecom Partners follows at 1,600. Combined, the top three players command just over 60% of active lattices and rooftops, leaving the balance to mid-tier specialists such as Towernex, Continental Towers, and Tower One Wireless.

Strategic moves center on portfolio swaps and renewable retrofits. SBA Communications acquired 7,000 regional sites from Millicom in October 2024 for USD 975 million, improving clustering in high-traffic corridors. Meanwhile, American Tower targets 1,950-2,550 global site additions in 2025, many slated for Colombia, but flags a 6% FX hit that tempers guidance. Neutral-host fiber integrators are also entering, pairing dark-fiber spurs from ISA’s 35,000 km network with monopole builds that enable edge colocation.

Tenant risk remains under the microscope. WOM Colombia’s rescue by SUR Holdings in January 2025 grants a three-year grace on spectrum obligations but forces TowerCos to reassess receivables. Telecall’s COP 41 billion default underscores exposure to smaller carriers. To diversify, tower owners negotiate long-term power-purchase agreements and bundle energy-as-a-service options that raise switching costs, cementing their role in the Colombia telecom towers market.

Colombia Telecom Tower Industry Leaders

American Tower Corporation

Phoenix Tower International

Andean Telecom Partners

QMC Telecom International

IHS Towers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Millicom completed acquisition of Telefónica’s Colombian operations for USD 400 million, teeing up tower rationalization.

- January 2025: WOM Colombia was acquired by SUR Holdings, securing a three-year grace period on spectrum fees.

- January 2025: Movistar and Tigo activated a unified RAN after MinTIC approval.

- December 2024: WOM Chile gained court confirmation for a USD 500 million recapitalization, easing regional spillover risk.

Colombia Telecom Tower Market Report Scope

Telecom towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Colombia telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO Captive sites), by installation (rooftop, and ground-based), and by fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of installed base (Thousand Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the 2026 valuation of the Colombia telecom towers market?

The market is valued at USD 253.93 million in 2026 and is expected to keep rising through 2031.

How fast is renewable power adoption among Colombian tower sites?

Renewable-powered locations are expanding at an 17.60% CAGR, the fastest growth across all infrastructure segments.

Which companies lead tower ownership in Colombia?

American Tower, Phoenix Tower International, and Andean Telecom Partners jointly operate about 60% of all active sites.

Why are rooftop sites gaining relevance?

5G millimeter-wave densification and stringent downtown zoning make rooftops quicker and more cost-effective to deploy than ground structures.

How does peso weakness affect tower leasing?

Most leases are dollar-indexed, so a weaker peso reduces local-currency revenue, squeezing TowerCo margins by roughly 6% on translation.

What government program targets rural coverage?

“Conecta TIC 360” seeks 85% national internet coverage by 2026 and channels nearly USD 20 billion into rural build-to-suit projects.

Page last updated on: