Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

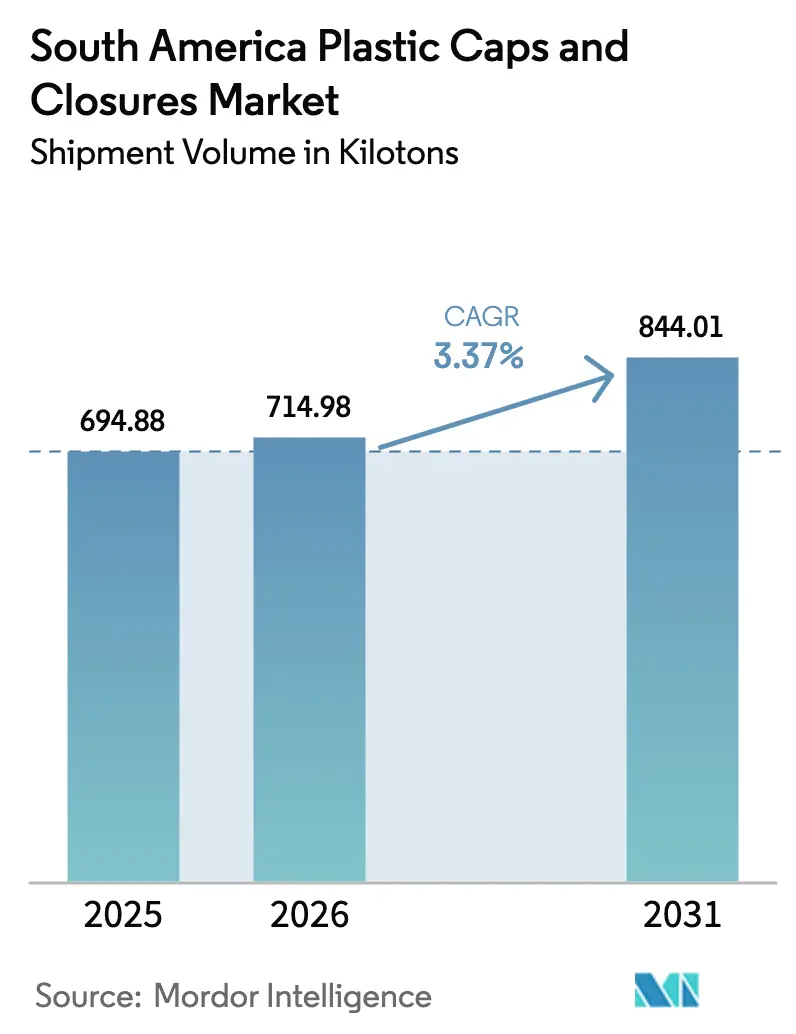

| Base Year Market Size (2025) | 694.88 kilotons |

| Market Volume (2026) | 714.98 kilotons |

| Market Volume (2031) | 844.01 kilotons |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

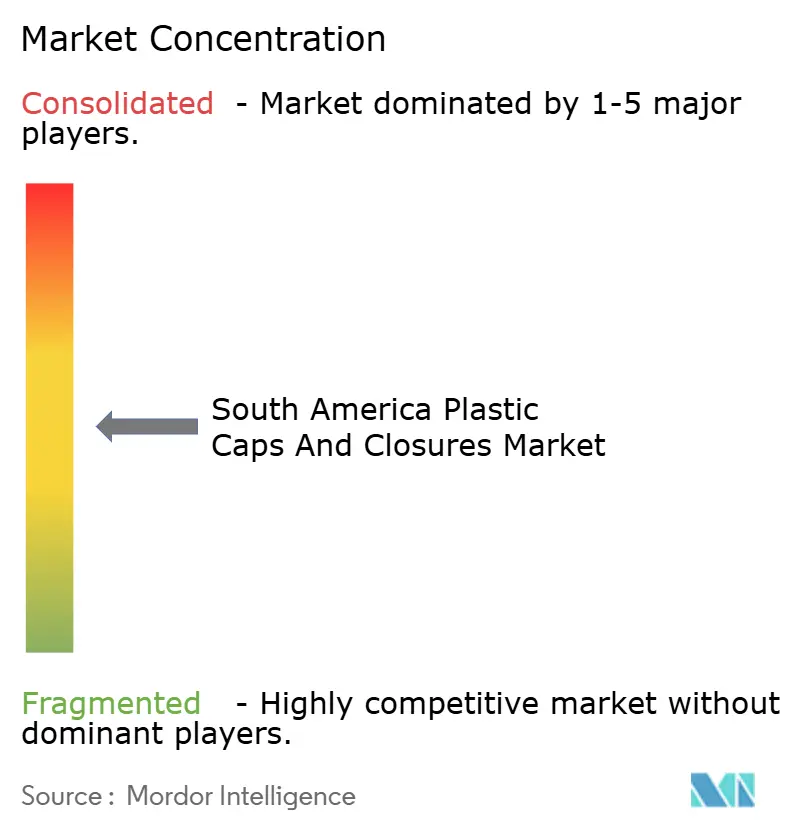

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Plastic Caps And Closures Market Analysis by Mordor Intelligence

The South America plastic caps and closures market size was valued at 694.88 kilotons in 2025 and estimated to grow from 714.98 kilotons in 2026 to reach 844.01 kilotons by 2031, at a CAGR of 3.37% during the forecast period (2026-2031). Favorable recycled-content mandates, the rapid uptick in e-commerce fulfillment, and exporter alignment with the European Union tethered-cap rule are redefining product specifications and sourcing strategies. Regional resin producer Braskem has accelerated the shift toward mechanically and chemically recycled grades, while premium personal-care and spirits brands are installing smart closures that validate authenticity at the point of consumption. Converters able to blend virgin and post-consumer resin, integrate tamper-evident functionality, and offer short print runs for promotional campaigns are winning new contracts. At the same time, closure lightweighting is becoming a cost-of-entry requirement as brand owners pursue carbon-reduction targets and seek relief from volatile polypropylene prices.

Key Report Takeaways

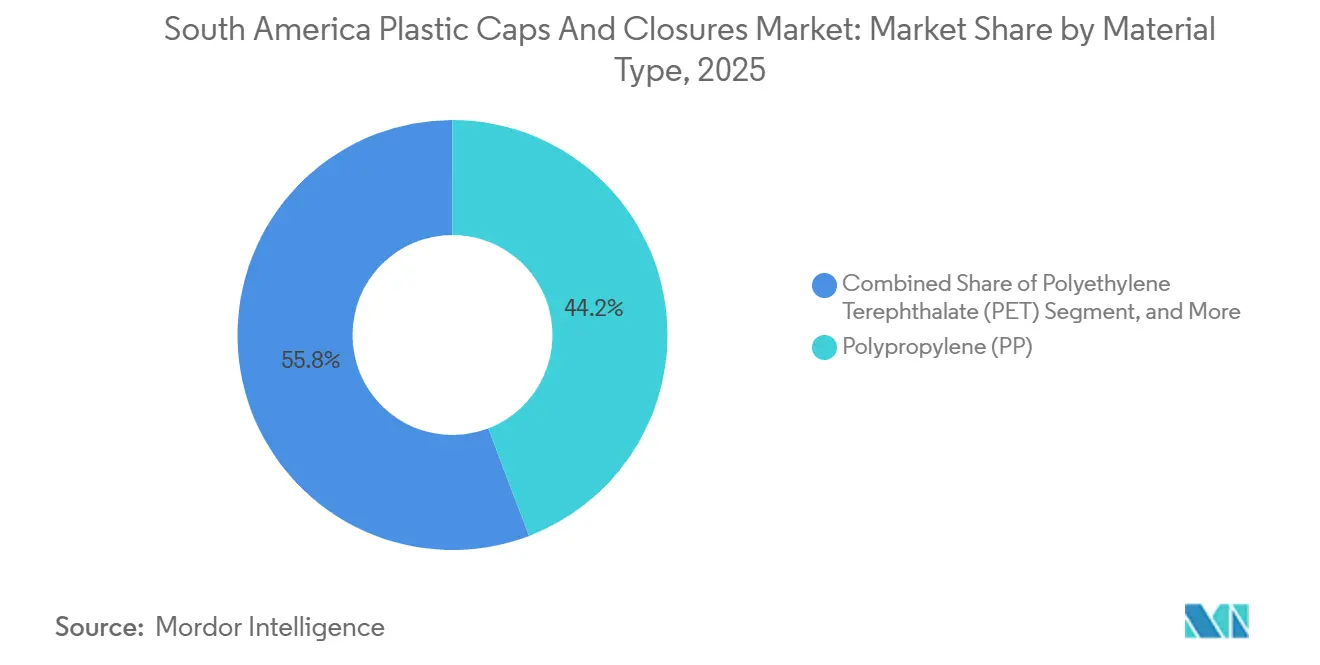

- By material, polypropylene led with 44.20% of the South America plastic caps and closures market share in 2025, while Other Materials are projected to expand at a 4.33% CAGR through 2031.

- By end-user industry, beverage closures commanded 49.32% share of the South America plastic caps and closures market size in 2025, and cosmetics and toiletries are forecast to advance at a 4.52% CAGR to 2031.

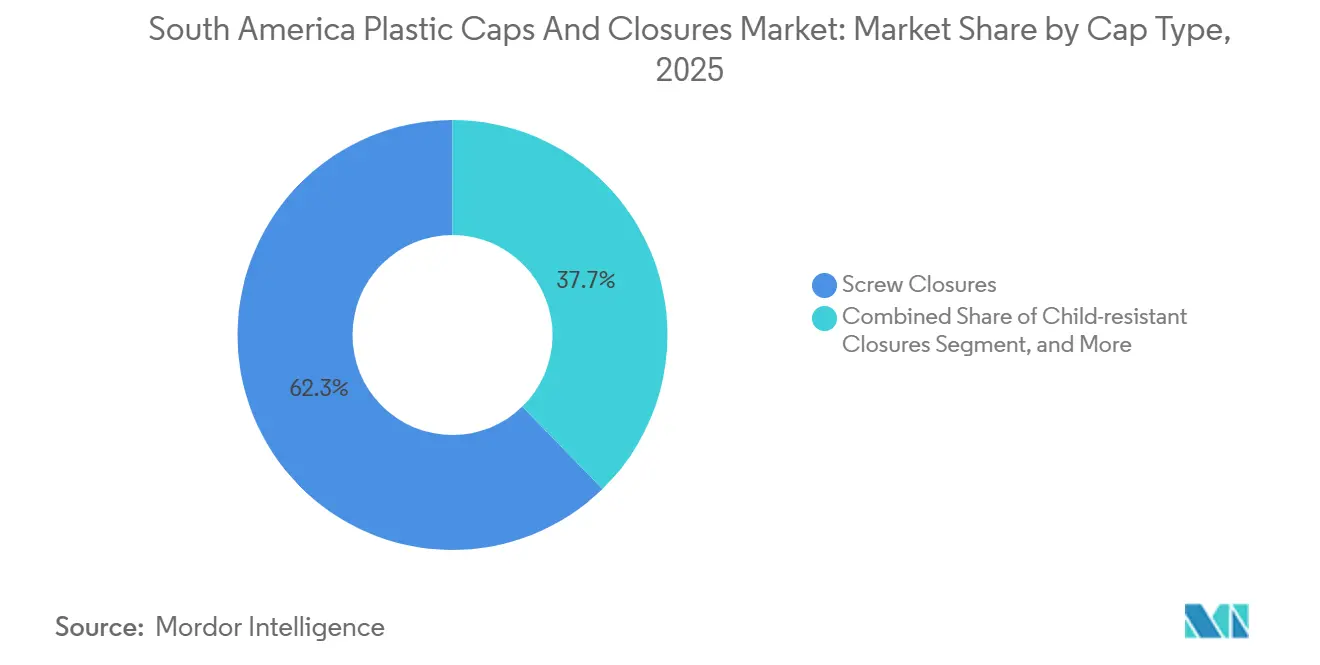

- By cap type, screw closures accounted for 62.30% of the South America plastic caps and closures market share in 2025, whereas tethered caps are expected to register a 4.49% CAGR during 2026-2031.

- By manufacturing technology, compression molding represented 47.78% of volume in 2025 and digitally printed smart closures are set to grow at a 4.18% CAGR over the same period.

- By geography, Brazil held 57.33% of regional volume in 2025, while Peru is projected to post the fastest 4.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Plastic Caps And Closures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging On-The-Go Beverage Consumption | +0.8% | Brazil, Argentina, Colombia, Spillover To Peru And Chile | Medium Term (2–4 Years) |

| Rising Penetration Of PET Bottled Dairy Drinks | +0.6% | Brazil, Argentina, Uruguay, Expansion Into Peru And Colombia | Long Term (≥ 4 Years) |

| Booming E-Commerce Demand For Tamper-Evident Packaging | +0.5% | Brazil, Argentina, Chile, Rapid Growth In Colombia And Peru | Short Term (≤ 2 Years) |

| Private-Label Expansion Among Regional FMCG Players | +0.4% | Brazil, Argentina, Chile, Early Gains In Urban Centers | Medium Term (2–4 Years) |

| Refill-And-Reuse Pilots By Large Beverage Brands | +0.3% | Brazil, Colombia, Pilot Programs In Argentina And Chile | Long Term (≥ 4 Years) |

| Adoption Of Tethered-Cap EU Directive By Exporters | +0.4% | Brazil, Argentina, Chile (Export-Oriented Producers) | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Surging On-The-Go Beverage Consumption

Urban commuters are favoring single-serve PET bottles that can be consumed on the move, pushing brands to specify closures that maintain carbonation, resist leakage, and open smoothly. Retail data show soft-drink and energy-drink volumes rising in Brazil and Colombia, and sports-drink lines are adopting flip-top and push-pull designs that enable one-handed use. Converters are responding with tamper-evident bands, pressure-relief vents, and stronger hinge designs that add up to 8% to unit cost yet reduce shrinkage for retailers. Investment in high-cavity compression molds supports the volume surge, while lightweighting offsets part of the added feature cost. The net effect is a positive mix shift toward value-added closures that lift average selling prices.

Rising Penetration of PET Bottled Dairy Drinks

Dairy processors in Brazil and Argentina are switching from cartons to chilled PET bottles, driving demand for closures that protect flavor and signal premium positioning. Sugarcane-based tethered caps introduced by Tetra Pak demonstrate that bio-attributed materials can meet both sustainability targets and performance needs. Dual-seal designs combining foil liners with tamper rings are gaining traction, though their co-injection tooling requirements limit production to larger converters. Cold-chain expansion in Peru and Colombia will unlock additional volume once infrastructure matures, making PET dairy drinks a key long-term growth pocket. Closure makers able to co-mold dissimilar resins and manage small color runs hold a strategic edge.

Booming E-Commerce Demand For Tamper-Evident Packaging

MercadoLibre and grocery delivery platforms are normalizing online orders for beverages, condiments, and household chemicals.[1]MercadoLibre, “Investor Presentation 2024,” investor.mercadolibre.com To mitigate liability, brands now insist on closures with breakaway bands or induction seals that cannot be resealed. Pharmaceutical and infant-nutrition categories face the strictest rules under ANVISA and ANMAT, spurring converter upgrades to machine-vision inspection that verifies 100% of band integrity. The capital intensity of these systems favors scale players, accelerating consolidation. As fulfillment speeds climb, automated packing lines also reward closures that run flawlessly at 1,200 pieces per minute, putting lagging converters at risk of delisting.

Private-Label Expansion Among Regional FMCG Players

Carrefour Brasil and Chilean retailers are rolling out price-fighter private-label SKUs that must look comparable to national brands while costing 15-20% less.[2]Carrefour Brasil, “Private-Label Expansion 2024,” carrefour.com.br Converters meet this brief by modularizing closure platforms, swapping only top inserts or embossing while keeping base molds constant. The approach lowers tooling amortization and gives retailers faster design refreshes, but it also squeezes margins. Success hinges on digital color management and tight logistics coordination to avoid stock-outs of specific hues or finishes. Medium-term growth will be strongest in Brazil and Argentina, where modern retail penetration tops 60%.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Stand-Up Pouches In Household Cleaners | -0.4% | Brazil, Argentina, Chile, Early Adoption In Cities | Medium Term (2–4 Years) |

| Growing Anti-Plastic Regulations In Pacific Alliance | -0.5% | Chile, Peru, Colombia, Spillover To Ecuador | Short Term (≤ 2 Years) |

| Price Volatility Of Virgin Polypropylene | -0.3% | Regionwide, Acute In Import-Dependent Markets | Short Term (≤ 2 Years) |

| Consumer Preference For Metal Crowns In Premium Beer | -0.2% | Argentina, Brazil, Chile Craft Segments | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Shift Toward Stand-Up Pouches In Household Cleaners

Flexible refill pouches now dominate detergent and fabric-softener aisles in Brazil and Chile, reducing demand for rigid-bottle closures. Unilever’s South America revenue rose 6.0% in 2024, helped by pouch formats that weigh 70% less and sell at a lower cost-per-use.[3]Unilever, “Annual Report 2024,” unilever.com Closure suppliers are exploring spouted pouches with flip-tops, yet the subformat still accounts for less than 5% of flexible-pack volume. As concentrated pods gain traction, closures could lose further relevance unless converters pivot to dispensing heads for refill stations or design resealable spouts compatible with film laminates.

Growing Anti-Plastic Regulations In Pacific Alliance

Chile, Peru, and Colombia have enacted non-aligned bans, recycled-content targets, and extended producer responsibility schemes, raising compliance complexity and costs. Peru now requires PET recycling certification, while Chile mandates 25% recycled content in packaging by 2030.[4]Chilean Ministry of Environment, “Packaging Regulations,” mma.gob.cl Multinationals can absorb the legal overhead, but small converters risk non-compliance penalties or lost contracts. The patchwork slows new product launches by up to six months and accelerates the exit of under-capitalized players, contracting the supplier base in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Resins Reshape Sourcing

Other Materials, mainly recycled PET, bio-based polyethylene, and advanced bioplastics, are forecast to outpace the overall South America plastic caps and closures market at a 4.33% CAGR, benefiting from Brazil’s 22% mandatory recycled content in PET packaging beginning in 2026. Polypropylene retained 44.20% volume share in 2025, but volatile offer prices at USD 840 per tonne have prompted converters to blend in 20-30% post-consumer resin, safeguarding margins while meeting client sustainability commitments.

Braskem’s FDA-compliant PCR PP launched in June 2025 removed the last technical barrier to using recycled PP in food-contact closures. Meanwhile, bio-attributed sugarcane PE qualifies for Bonsucro certification and cuts life-cycle carbon emissions by 70%. Limited food-grade rPET capacity in Peru and Colombia, however, constrains PET closure growth. Across the region, converters now qualify four resin streams, virgin, mechanically recycled, chemically recycled, and bio-based, raising inventory costs yet providing supply resilience..

By End-User Industry: Cosmetics Outpace Beverage

Beverage closures delivered 49.32% of volume in 2025 thanks to Ambev’s breweries and Coca-Cola FEMSA’s bottling footprint. Even so, cosmetics and toiletries closures will grow faster at 4.52% CAGR as premium skincare and hair-care lines adopt soft-squeeze and airless pumps that improve dosing precision. The South America plastic caps and closures market size for cosmetics commands higher average selling prices, offsetting lower tonnage.

Food closures advance in lockstep with rising per-capita income, while household-chemical closures suffer from refill pouches. Pharmaceutical and healthcare remain niche but highly profitable because of child-resistant and desiccant-integrated features demanded by ANVISA and ANMAT. Brand owners in Chile and Brazil, markets with stricter quality regulation, already pay 3-5 times the price of commodity screw caps for these advanced formats.

By Cap Type: Tethered Designs Gain Export Traction

Screw closures held a commanding 62.30% share of the South America plastic caps and closures market in 2025, maintaining entrenched leadership across beverage and food categories. However, tethered caps are poised for faster growth, posting a 4.49% CAGR through 2031 as exporters adopt EU attachment rules to avoid dual SKUs. This segment benefits from hinge investments by players like Guala Closures and Bericap, which are positioning tethered solutions as both regulatory-compliant and operationally efficient.

Flip-tops and snap-ons continue to play a vital role in personal care packaging, where convenience and user experience are paramount. Yet their relatively high unit costs limit penetration in price-sensitive food segments, where screw closures remain dominant. Luxury decorative closures, though representing just 3% of total volume, exert an outsized influence by setting brand differentiation standards that gradually filter down into mainstream packaging. This premium tier underscores the importance of aesthetics and tactile quality in shaping consumer perceptions. Converters are also innovating with functional enhancements, such as living hinges that withstand 50-plus open-close cycles.

By Manufacturing Technology: Digital Printing Enables Customization

Compression molding covered 47.78% of the 2025 volume due to its low scrap rate and large-cavity economics. Injection molding retains its dominance for complex child-resistant and multi-component assemblies that require tight tolerances. Digitally printed smart closures, though still below 5% of tonnage, will grow 4.18% a year as NFC tags and serialized QR codes migrate from premium spirits to mid-range cosmetics.

Hybrid sequential molding, combining compression for shells and injection for liners in a single cycle, is gaining traction in Brazil and Argentina as a next-generation packaging innovation. The process is designed to balance lightweighting objectives with scrap reduction, addressing two critical cost and sustainability pressures in regional beverage and dairy packaging markets. By merging two traditionally separate molding stages, manufacturers can streamline production, reduce material waste, and improve product quality consistency.

Geography Analysis

Brazil accounted for 57.33% of regional volume in 2025 on the back of its 212 million consumers, integrated resin supply, and dense brewery and bottling networks. National Solid Waste Policy requirements are prompting vertically integrated converters to double down on recycled-content sourcing, bolstered by private-equity consolidation of rPET plants. However, overcapacity has already forced one PET recycler shutdown as low virgin prices eroded spreads, hinting at cyclical risk. Closure demand is skewed toward beer, where metal crowns dominate premium craft lines and marginally displace plastic twist-offs.

Peru is the fastest-growing country, set to deliver a 4.52% CAGR, catalyzed by surging polypropylene and HDPE imports that fuel packaged food and beverage output. Free-trade agreements covering 60 countries support agricultural exports that need tamper-evident closures, while a government-mandated PET recycling certificate layers in compliance cost that smaller suppliers struggle to meet. Limited domestic closure capacity opens a window for regional entrants to install compression lines and capture share.

Argentina, Colombia, and Chile each exhibit mid-single-digit growth but divergent risk profiles. Argentina’s currency depreciation crimps converter capital budgets even as IRAM-aligned standards facilitate cross-border mold movement. Colombia’s new EPR law forces brands to document 30% packaging recovery by 2027, accelerating closure lightweighting and recyclability initiatives. Chile’s 25% recycled-content target by 2030 positions it as a test market for bio-based materials, but scale constraints keep manufacturing volumes small. The rest of South America, Ecuador, Bolivia, Paraguay, and Uruguay, remains fragmented, yet rising modern retail is laying the groundwork for future volume gains.

Competitive Landscape

The South America plastic caps and closures market is moderately fragmented. Global leaders Silgan, Guala, and Bericap leverage multiyear supply contracts with beverage multinationals, but regional converters gain ground by locking in circular polyethylene from Braskem under long-term offtake agreements. Amcor’s rigid-packaging unit booked USD 785 million in South American sales in 2025 and is rolling out lightweight screw-cap platforms that trim resin use by up to 15%, lowering cost and carbon footprints.

Technology is sharpening the competitive divide. AptarGroup’s NFC-enabled smart closures secure contracts in premium spirits and pharmaceuticals at unit prices five to ten times those of commodity caps. Converters that invested early in machine-vision inspection now offer 100% tamper-band verification, winning e-commerce volumes at the expense of rivals relying on manual checks.

Market entry barriers are climbing. ISO 15378 certification is becoming non-negotiable for healthcare projects, while capital outlays for high-cavity compression molds or inline assembly robotics exceed USD 2 million per line. Simultaneously, flexible-film suppliers erode share in household chemicals with pouch formats, pressuring closure demand. Consolidation in the rPET chain may help stabilize recycled-resin pricing long term, yet near-term overcapacity remains a risk that only well-capitalized players can absorb.

South America Plastic Caps And Closures Industry Leaders

Silgan Holdings Inc.

AptarGroup Inc.

Albéa S.A.

Guala Closures S.p.A.

Bericap GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Braskem completed the first commercial sale of circular polyethylene in South America, enabling converters to meet the 22% recycled-content rule for PET packaging.

- June 2025: Braskem introduced FDA-compliant PCR polypropylene with 25% recycled content for food-contact closures.

- November 2024: Origin Materials formed a strategic relationship with Berlin Packaging to supply 100% PCR-PET 1881 caps, addressing recyclability objectives in the USD 65 billion global closures space.

- May 2025: Amcor reported USD 785 million in South American rigid-packaging revenue, highlighting 10-15% resin savings from new lightweight closure designs.

- January 2025: Peru’s National Institute of Statistics confirmed 92.5% growth in polypropylene imports and a 34.4% jump in HDPE imports versus January 2024.

South America Plastic Caps And Closures Market Report Scope

The South America Plastic Caps and Closures Market Report is Segmented by Material (Polyethylene Terephthalate, Polypropylene, Low Density Polyethylene, High-Density Polyethylene, Other Materials), End-user Industry (Beverage, Food, Pharmaceutical and Healthcare, Cosmetics and Toiletries, Household Chemicals, Other End-user Industries), Cap Type (Screw Closures, Tethered Caps, Flip-top and Snap-on Caps, Child-resistant Closures, Luxury/Premium Decorative Closures, Dispensing Caps), Manufacturing Technology (Injection Molding, Compression Molding, 3-Piece and In-line Assembly, Digitally Printed Smart Closures), and Geography (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Volume (Kilotons).

By Material

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP) |

| Low Density Polyethylene (LDPE) |

| High-Density Polyethylene (HDPE) |

| Other Materials |

By End-user Industry

| Beverage |

| Food |

| Pharmaceutical and Healthcare |

| Cosmetics and Toiletries |

| Household Chemicals |

| Other End-user Industries |

By Cap Type

| Screw Closures |

| Tethered Caps |

| Flip-top and Snap-on Caps |

| Child-resistant Closures |

| Luxury/Premium Decorative Closures |

| Dispensing Caps |

By Manufacturing Technology

| Injection Molding |

| Compression Molding |

| 3-Piece and In-line Assembly |

| Digitally Printed Smart Closures |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Material | Polyethylene Terephthalate (PET) |

| Polypropylene (PP) | |

| Low Density Polyethylene (LDPE) | |

| High-Density Polyethylene (HDPE) | |

| Other Materials | |

| By End-user Industry | Beverage |

| Food | |

| Pharmaceutical and Healthcare | |

| Cosmetics and Toiletries | |

| Household Chemicals | |

| Other End-user Industries | |

| By Cap Type | Screw Closures |

| Tethered Caps | |

| Flip-top and Snap-on Caps | |

| Child-resistant Closures | |

| Luxury/Premium Decorative Closures | |

| Dispensing Caps | |

| By Manufacturing Technology | Injection Molding |

| Compression Molding | |

| 3-Piece and In-line Assembly | |

| Digitally Printed Smart Closures | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the forecast growth rate for the South America plastic caps and closures market?

The market is projected to advance at a 3.37% CAGR between 2026 and 2031, reaching 844.01 kilotons by the end of the period.

Which material segment is growing fastest in South America?

Closures made from Other Materials, especially recycled PET, bio-based polyethylene, and bioplastics, are expected to post a 4.33% CAGR through 2031.

How will EU regulations affect South American closure suppliers?

Exporters are pre-emptively adopting tethered caps to comply with the EU Single-Use Plastics Directive, driving a 4.49% CAGR in this cap type.

Why is Peru considered the most attractive growth market?

Robust polypropylene and HDPE import growth, expanding food processing, and trade agreements supporting packaged exports position Peru for a 4.52% CAGR.

Which end-user sector is set to outpace beverage closures?

Cosmetics and toiletries closures are forecast to grow 4.52% a year as premium skincare and hair-care packaging demands dispensing functionality and upscale aesthetics.

What is driving investment in smart closures?

Brand needs for product authentication and consumer engagement are pushing premium spirits and pharmaceutical companies toward NFC-enabled closures, despite higher unit costs.

Page last updated on: