Market Overview

| Study Period | 2020 - 2031 |

|---|---|

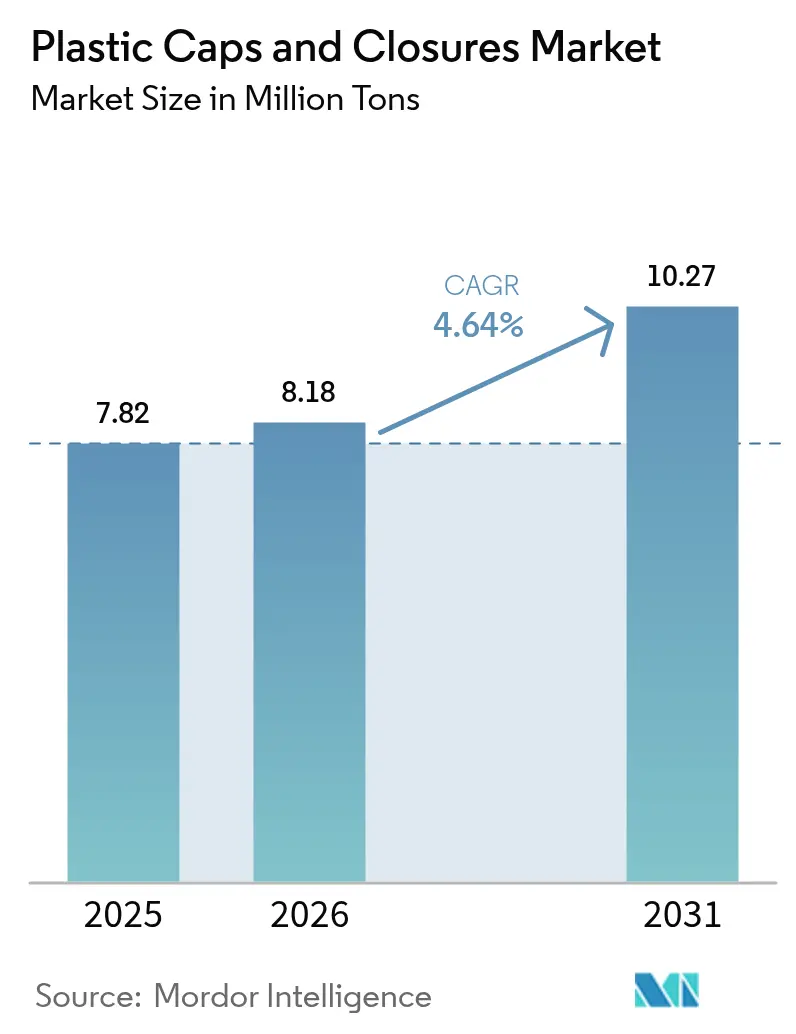

| Market Volume (2026) | 8.18 Million tons |

| Market Volume (2031) | 10.27 Million tons |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

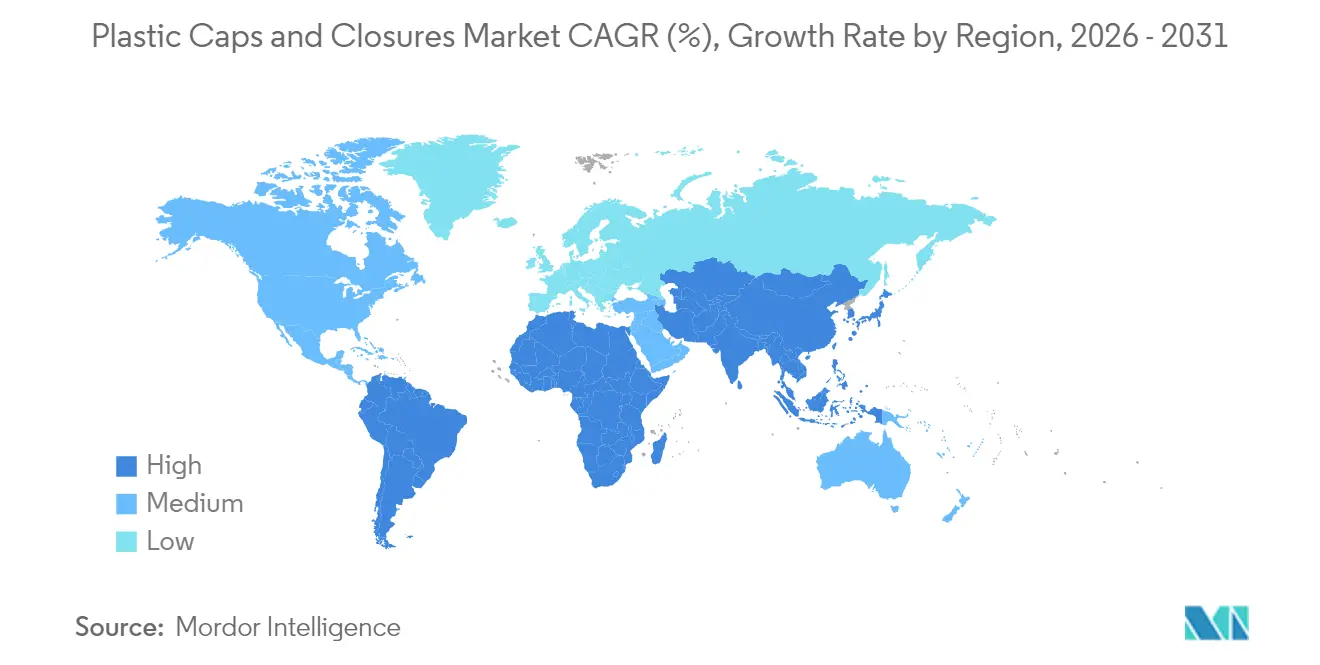

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Caps And Closures Market Analysis by Mordor Intelligence

The plastic caps and closures market size was valued at 7.82 million tons in 2025 and estimated to grow from 8.18 million tons in 2026 to reach 10.27 million tons by 2031, at a CAGR of 4.64% during the forecast period (2026-2031). Growth stems from tethered-cap mandates in Europe, surging aseptic PET bottling lines across ASEAN, and rapid pharmaceutical demand for child-resistant polypropylene closures. Consolidation, led by the Amcor–Berry Global combination, is reshaping competitive dynamics while manufacturers race to meet tougher Extended Producer Responsibility (EPR) fee structures. Raw-material volatility for propylene and ethylene remains a near-term headwind, yet sustained investment in compression-molding automation and recycled content is mitigating cost pressure. Across geographies, Asia-Pacific holds the largest share, Middle East and Africa records the fastest CAGR, and North America capitalizes on stringent safety regulations that favor high-value closure formats.

Key Report Takeaways

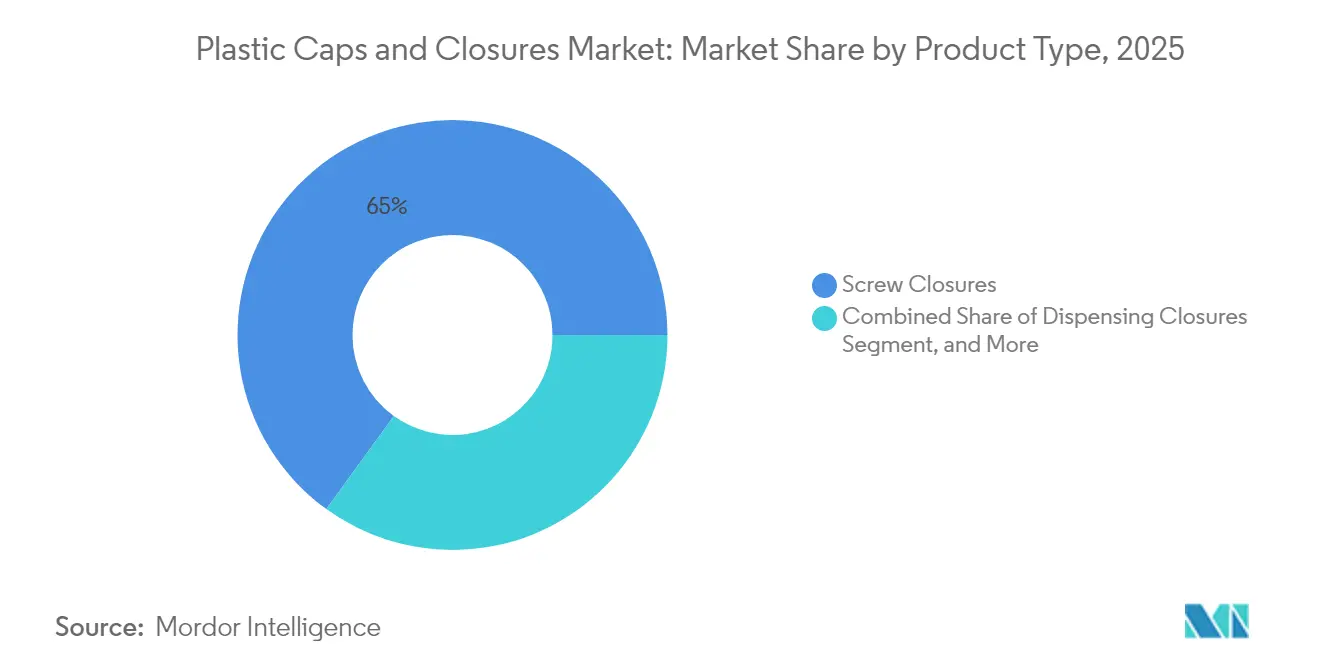

- By product type, screw closures held 65.02% of plastic caps and closures market share in 2025.

- By raw material, polypropylene accounted for 55.71% share of the plastic caps and closures market size in 2025.

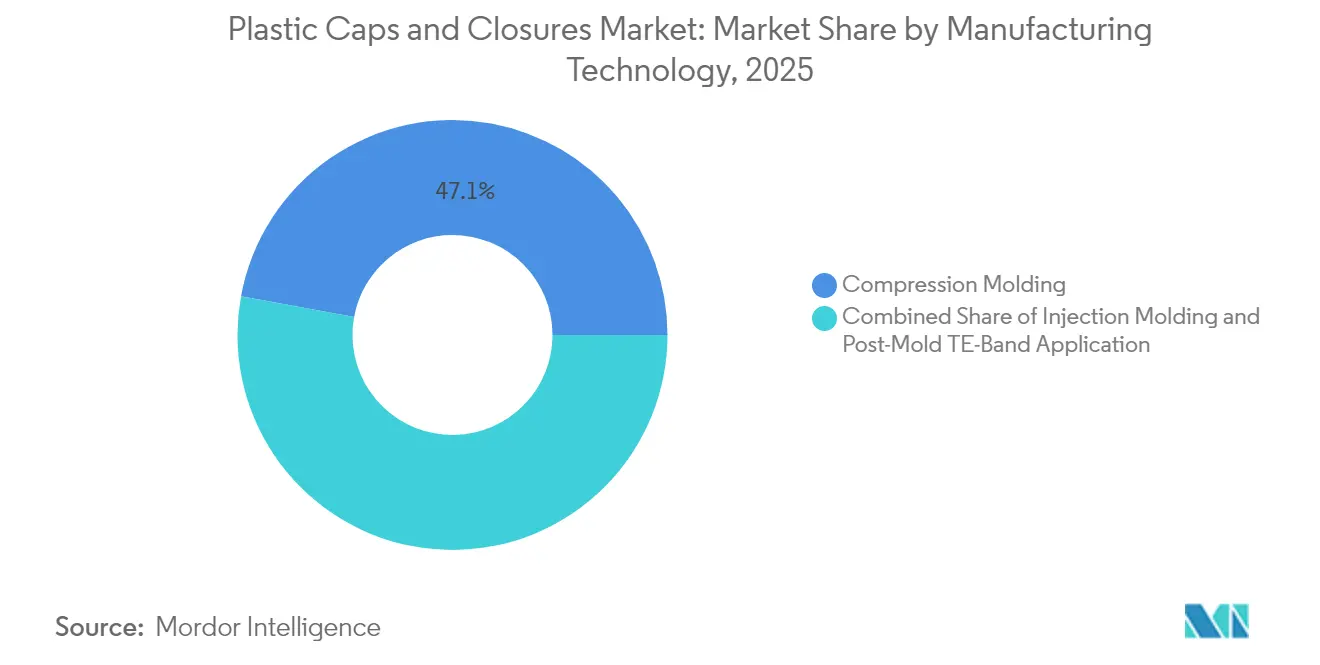

- By manufacturing technology, compression molding led with 47.12% plastic caps and closures market share in 2025.

- By end-use, beverages commanded 48.03% of the plastic caps and closures market size in 2025.

- By geography, the Middle East and Africa post the fastest 7.78% CAGR between 2026-2031 for the plastic caps and closures market size.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Caps And Closures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Single-Use Plastics Directive Mandating Tethered Caps Adoption | +1.2% | Europe, with spillover to North America | Medium term (2-4 years) |

| Surge in Aseptic PET Bottling Lines Across ASEAN Beverage Plants | +0.8% | ASEAN core, spillover to broader Asia-Pacific | Long term (≥ 4 years) |

| Pharma Shift to Child-Resistant PP Closures in U.S. and Canada | +0.6% | North America | Short term (≤ 2 years) |

| Latin American Dairy Pivot Toward Gable-Top Cartons with Screw Caps | +0.4% | Latin America | Medium term (2-4 years) |

| Craft Beer Exports Fueling Crown-Closure Demand in Europe | +0.3% | Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Single-Use Plastics Directive Mandating Tethered Caps Adoption

The July 2024 EU requirement that beverage containers below 3 liters carry tethered closures rewired design norms and forced widespread capital upgrades. Leading system suppliers introduced multiple attachment concepts that keep caps connected without compromising line speeds, enhancing litter-reduction goals while safeguarding consumer ergonomics. Brand owners in North America are trialing the same solutions ahead of pending Californian rules, signalling a global pivot toward attachment technology.

Surge in Aseptic PET Bottling Lines Across ASEAN Beverage Plants

New aseptic fillers extend shelf life up to 12 months and use 60.1% less plastic, driving demand for lightweight yet sterile closures. Projects in Vietnam and Indonesia illustrate the scale, with single facilities adding more than 20,000 tons of annual closure demand tied to recycled PET initiatives that back circular-economy targets.

Pharma Shift to Child-Resistant PP Closures in U.S. and Canada

Updated poison-prevention standards require 85% child-resistance without demonstration, prompting a migration toward precision-molded polypropylene designs that balance safety with adult accessibility. Regulatory synchrony between the United States, Canada, and Australia accelerates adoption across over-the-counter drug lines, boosting premium closure volumes.[1]Source: U.S. Consumer Product Safety Commission, “16 CFR 1700.15 — Poison prevention packaging standards,” ecfr.gov

Latin American Dairy Pivot Toward Gable-Top Cartons with Screw Caps

Regional processors embrace reclosable screw caps on gable-top formats to deliver convenience and sustainability. Investments exceeding USD 166 million in packaging upgrades underscore rising demand for closures that integrate recycled content and extend product freshness, aided by draft MERCOSUR standards on food-grade recycled PET.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Propylene and Ethylene Contract Prices Impacting PP/PE Margins | -1.1% | Global | Short term (≤ 2 years) |

| Rising Aluminum ROPP Substitution in Premium Spirits, Cannibalising Plastic | -0.7% | Europe, North America | Medium term (2-4 years) |

| Tethered-Cap Retrofitting Costs for Legacy PET Lines | -0.5% | Europe, with spillover to other regions | Short term (≤ 2 years) |

| Intensifying EPR Fees on Multilayer Plastic in OECD Markets | -0.4% | OECD countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Propylene and Ethylene Contract Prices Impacting PP/PE Margins

Feedstock swings erode margin stability for closure manufacturers that rely heavily on polypropylene and polyethylene. Firms counter the cost shock through hedging, recycled-resin blends, and ongoing automation programs that compress conversion costs.[2]Source: OECD, “Extended producer responsibility and economic instruments,” oecd.org

Rising Aluminum ROPP Substitution in Premium Spirits, Cannibalising Plastic

Premium spirits brands favor aluminum for barrier performance and perceived quality, siphoning share from plastic closures in high-margin segments. Plastic suppliers respond with improved barrier coatings and premium aesthetics to protect value pools in Europe and North America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Screw Closures Dominate Through Versatility

Screw closures captured 65.02% of plastic caps and closures market share in 2025 thanks to universal compatibility with high-speed beverage, food, and pharmaceutical lines. Their low unit cost and dependable seal underpin enduring dominance, even as dispensing variants post a 6.18% CAGR through 2031. Dispensing formats gain favor in condiments and personal-care SKUs where portion control and hygiene boost consumer appeal. Tamper-evident and child-resistant formats benefit from stricter safety regulations that reshape over-the-counter drug packaging.

Crown and ROPP closures retain relevance in beer and premium spirits where tradition and shelf presence matter. Snap-on designs serve household chemicals seeking quick reclose functionality. Rising tethered-cap requirements are catalyzing redesign projects across all screw variants, linking closure innovation directly to compliance. End-users adopting light-weight bottles favor advanced thread profiles that cut resin use without compromising seal integrity, supporting the long-term outlook for screw formats in the plastic caps and closures market.

By Raw Material: Polypropylene Leadership Amid Bio-Based Innovation

Polypropylene held 55.71% share of the plastic caps and closures market size in 2025. Its chemical resistance, heat stability, and processability secure its place in food and pharmaceutical applications. High-density polyethylene supports industrial chemical packs that need impact tolerance, while low-density polyethylene is used in flexible snap closures. PET variants grow as single-material packages simplify recycling systems and enable tethered designs compliant with EU rules.

Bio-based and chemically recycled resins expand at 7.62% CAGR. Brands invest to meet EPR fee modulation and consumer sustainability expectations. Early commercial lines running plant-based polypropylene highlight the pathway to lower-carbon closures. Supply chain qualification, color stability, and cost parity remain hurdles, yet scaling chemistry improvements portend faster adoption beyond 2030 in the plastic caps and closures industry.

By Manufacturing Technology: Compression Molding Efficiency Drives Market Share

Compression molding generated 47.12% plastic caps and closures market share in 2025 because it delivers tight dimensional tolerances and low scrap rates. Multi-cavity presses now integrate in-mold slitting and camera vision, raising uptime and reducing labor. Injection molding keeps importance for intricate child-resistant and dispensing formats that require multi-component builds.

Post-mold tamper-evident band application advances at 5.71% CAGR. The retrofit-friendly method lets producers comply with new safety norms without full tool replacements. Continuous improvements in servo-controlled band applicators deliver cycle-time parity with legacy systems, pushing adoption across medium-volume pharmaceutical and food lines. The result is broader technology diversity serving distinct performance and cost envelopes in the plastic caps and closures market.

By End-Use Industry: Beverage Applications Lead Amid Pharmaceutical Growth

Beverages drove 48.03% of global volumes in 2025 and rely on lightweight screw, crown, and tethered formats to secure carbonated drinks, water, juice, and beer. High-speed fillers demand closures with precise torque retention and oxygen barrier properties, supporting the beverage segment’s scale economics.

Pharmaceutical closures register a 7.06% CAGR to 2031, propelled by aging demographics and stringent child-resistant laws. Updated U.S. and Canadian regulations heighten demand for torque-controlled polypropylene components with liner compatibility and traceable resin sourcing. Food, personal-care, and household chemical segments round out demand with tailored needs for dosing, fragrance retention, and chemical resistance. Collectively, varied application profiles sustain robust innovation pipelines and stable growth in the plastic caps and closures market.

Geography Analysis

Asia-Pacific accounted for 40.12% of global volumes in 2025, anchored by China’s scale, Japan’s quality standards, and India’s expanding beverage and pharma sectors. ASEAN’s aseptic investment wave further intensifies regional closure consumption, while circular-economy policies fast-track recycled PET uptake. Australia’s alignment with international pharma safety rules harmonizes regional trade and drives demand for specialized child-resistant formats.

Middle East and Africa post the fastest 7.78% CAGR to 2031. Diversification initiatives in Saudi Arabia and the United Arab Emirates invite foreign investment in packaging, while Turkey leverages its strategic export location. Nigeria’s population growth and South Africa’s manufacturing base increase closure demand for beverages and household products. Regional reforms encouraging local value addition support future capacity builds in the plastic caps and closures market.

Europe balances regulatory headwinds and sustainability opportunities. Tethered-cap rules enforce expensive line retrofits yet unlock design differentiation. Germany leads technical compliance projects, France drives premium design, and the United Kingdom’s EPR fee schedules reshape cost models. Spain and Italy utilize established food and beverage exports to sustain closure demand. Collective emphasis on circular-economy targets accelerates the shift toward mono-material and recycled-content caps, preserving market relevance despite slower macro growth.

Competitive Landscape

Amcor’s 2025 stock merger with Berry Global created the world’s largest rigid and flexible packaging supplier, unlocking USD 650 million in synergy savings and USD 180 million in annual R&D spending.Silgan Holdings, Crown Holdings, and AptarGroup follow with targeted acquisitions and capacity upgrades to deepen technology breadth and regional presence. Silgan’s purchase of Weener adds dispensing and specialty closure lines with EUR 20 million in anticipated synergies.

Players differentiate through tethered-cap intellectual property, compression-molding enhancements, and bio-based resin partnerships. Automation, inline vision inspection, and energy-efficient tooling dominate capital budgets, supporting margin preservation amid feedstock volatility. Strategic pursuit of EPR-driven material innovation and local-for-local production in emerging markets signals a competitive pivot toward resilience and sustainability in the plastic caps and closures market.

Plastic Caps And Closures Industry Leaders

Silgan Holdings Inc.

Aptar Group Inc.

BERICAP GmbH & Co. KG

Closure Systems International

Amcor PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MERCOSUR issued draft rules on post-consumer recycled food-grade PET, mirroring EU chemical-recycling provisions.

- January 2025: Amcor closed its all-stock merger with Berry Global, targeting USD 650 million annual synergies.

- August 2024: Origin Materials unveiled tethered PET caps for PCO 1881 necks, launch slated Q4 2024.

- July 2024: Silgan completed the Weener acquisition, forecasting EUR 20 million annual synergies.

Global Plastic Caps And Closures Market Report Scope

The plastic caps and closures market aims to study the various segments of the manufacturing process of plastic caps and closures and the end consumers. End-users of plastic caps such as pharmaceuticals, cosmetics, and toiletries offer vast opportunities. The plastic material used to manufacture plastic caps & closures is thermoplastic and thermosets. Plastic caps & closures are recyclable and lightweight, making them ideal for packaging a variety of carbonated & non-carbonated beverages and industrial goods.

The Plastic Caps and Closures Market is segmented by Application (Food, Pharmaceuticals, Beverages, Cosmetics, and Toiletries), Raw Material (PP, HDPE, LDPE), and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Product Type

| Screw Closures |

| Dispensing Closures |

| Child-Resistant Closures |

| Tamper-Evident Closures |

| Crown Closures |

| ROPP (Roll-On Pilfer-Proof) |

| Snap / Press-on Closures |

By Raw Material

| Polypropylene (PP) |

| High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) |

| Polyethylene Terephthalate (PET) |

| Polyvinyl Chloride (PVC) |

| Other Raw Material |

By Manufacturing Technology

| Compression Molding |

| Injection Molding |

| Post-Mold TE-Band Application |

By End-Use Industry

| Beverages |

| Food |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Household and Industrial Chemicals |

| Other End-Use Industry |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Screw Closures | ||

| Dispensing Closures | |||

| Child-Resistant Closures | |||

| Tamper-Evident Closures | |||

| Crown Closures | |||

| ROPP (Roll-On Pilfer-Proof) | |||

| Snap / Press-on Closures | |||

| By Raw Material | Polypropylene (PP) | ||

| High-Density Polyethylene (HDPE) | |||

| Low-Density Polyethylene (LDPE) | |||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride (PVC) | |||

| Other Raw Material | |||

| By Manufacturing Technology | Compression Molding | ||

| Injection Molding | |||

| Post-Mold TE-Band Application | |||

| By End-Use Industry | Beverages | ||

| Food | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Household and Industrial Chemicals | |||

| Other End-Use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the plastic caps and closures market?

The market reached 8.18 million tons in 2026 and is forecast to hit 10.27 million tons by 2031, reflecting a 4.64% CAGR.

Which product type leads global demand?

Screw closures dominate with 65.02% share in 2025 thanks to versatility and compatibility with high-speed filling lines.

Why are tethered caps becoming mandatory in Europe?

EU rules aim to reduce litter by keeping caps attached to beverage containers under 3 liters, effective July 2024.

Which region grows fastest through 2031?

Middle East and Africa records the highest CAGR at 7.78% as governments diversify economies and expand consumer-goods production.

How will the Amcor–Berry Global merger affect competition?

The deal creates the sector’s largest supplier, unlocking USD 650 million in annual cost savings and intensifying R&D investment.

What challenges do manufacturers face from raw-material pricing?

Volatility in propylene and ethylene feedstocks pressures margins, prompting greater use of recycled resins and cost-efficient molding technologies.

Page last updated on: