Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

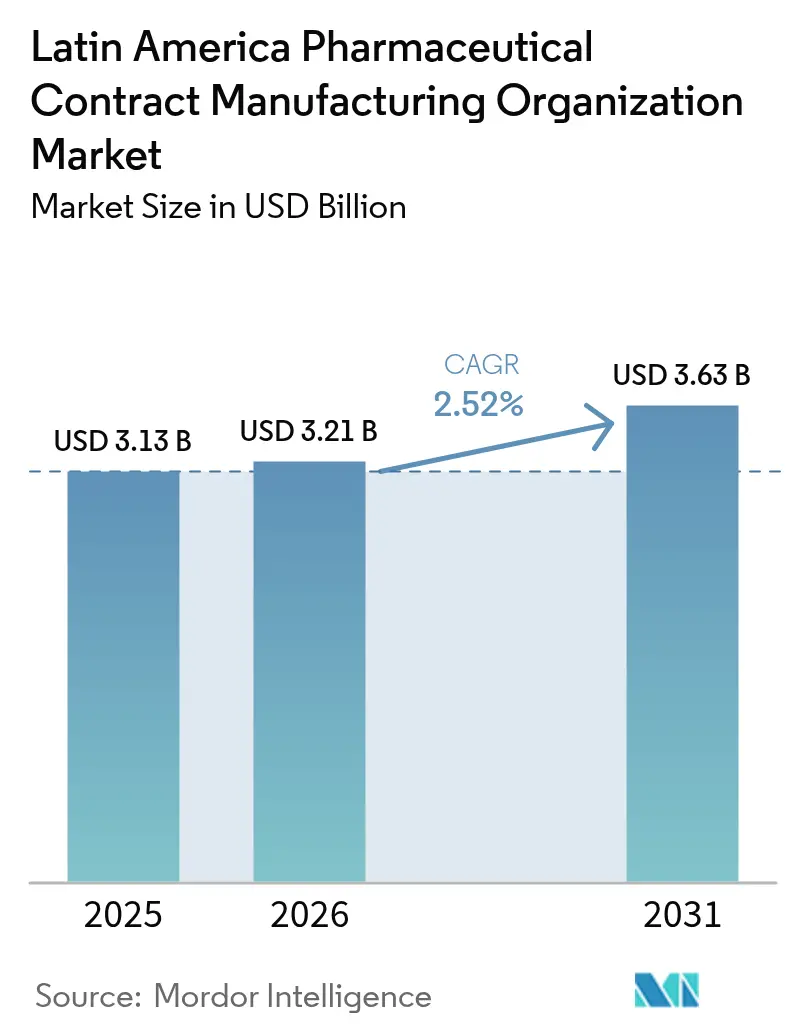

| Base Year Market Size (2025) | USD 3.13 Billion |

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 2.52% CAGR |

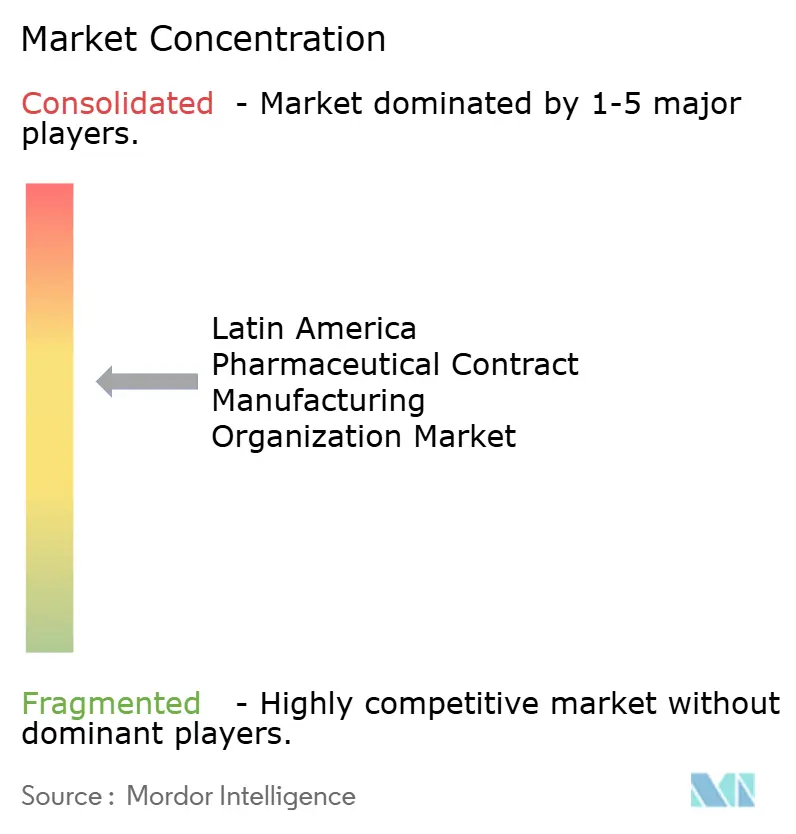

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Pharmaceutical Contract Manufacturing Organization Market Analysis by Mordor Intelligence

Latin America pharmaceutical contract manufacturing organization market size in 2026 is estimated at USD 3.21 billion, growing from 2025 value of USD 3.13 billion with 2031 projections showing USD 3.63 billion, growing at 2.52% CAGR over 2026-2031. Continuous nearshoring by North American drug makers, sizable green-field investments such as Novo Nordisk’s USD 1.09 billion GLP-1 facility in Brazil, and regional tax incentives for export-oriented plants underpin steady expansion. Rapid growth of biologics outsourcing, widening adoption of AI-enabled process optimization, and ESG-linked financing that lowers the cost of capital further reinforce competitiveness. At the same time, currency volatility, GMP-trained talent shortages outside primary hubs, and power-grid instability in Brazil’s Northeast temper momentum, yet do not derail the overall upward trajectory of the Latin America pharmaceutical contract manufacturing organization market.

Key Report Takeaways

- By service type, API manufacturing led with 42.10% of the Latin America pharmaceutical contract manufacturing organization market share in 2025, and the same service is forecast to advance at a 3.62% CAGR through 2031.

- By drug molecule, small molecules dominated at 56.85% share in 2025, while advanced therapies are expected to post the fastest 3.95% CAGR to 2031.

- By scale, commercial operations accounted for 61.70% of the Latin America pharmaceutical contract manufacturing organization market size in 2025, whereas clinical-phase manufacturing will grow the quickest at a 5.05% CAGR to 2031.

- By end user, Big Pharma captured a 45.80% share in 2025, yet emerging and virtual biotech companies are poised for the highest 4.45% CAGR over 2026-2031.

- By therapeutic area, oncology generated 38.05% revenue share in 2025, while CNS therapeutics are projected to accelerate at a 4.33% CAGR through 2031.

- By country, Brazil held 48.40% of the Latin America pharmaceutical contract manufacturing organization market share in 2025; Chile is estimated to register the fastest 4.82% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Pharmaceutical Contract Manufacturing Organization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising biologics outsourcing within LATAM | +0.6% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Growing near-shoring by North-American pharma companies | +0.8% | Mexico, Brazil, Colombia | Short term (≤ 2 years) |

| Expansion of local vaccine manufacturing post-COVID-19 | +0.7% | Brazil, Argentina, Mexico | Medium term (2-4 years) |

| Government tax incentives for export-oriented CMOs | +0.5% | Chile, Mexico, Colombia | Long term (≥ 4 years) |

| AI-enabled process optimization boosting CMO margins | +0.4% | Brazil, Mexico, Chile | Long term (≥ 4 years) |

| Regional ESG-linked financing unlocking CapEx | +0.3% | Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising biologics outsourcing within LATAM

Pharmaceutical firms are increasingly outsourcing biologics because the specialized bioreactors, purification skids, and validated cold-chain infrastructure required for large-molecule products demand steep capital expenditures. PAHO’s mRNA transfer hubs in Argentina and Brazil catalyze domestic know-how, while the Fiocruz–Boehringer agreement to localize Jardiance showcases how established CMOs pivot toward higher-margin biologics work. National policies that subsidize technology transfer amplify the trend, and regional CDMOs are now scaling single-use systems and 2,000 L stainless bioreactors. The shift helps the Latin America pharmaceutical contract manufacturing organization market secure larger, multi-year contracts from innovator companies that prefer variable cost models over owning dedicated biologics capacity. As a result, biologics now occupy a rising share of facility CapEx plans across Brazil’s primary clusters in São Paulo and Minas Gerais.

Growing near-shoring by North-American pharma companies

Heightened geopolitical friction and pandemic supply-chain bottlenecks have prompted U.S. and Canadian sponsors to relocate portions of their manufacturing portfolios nearer to the United States. Mexico’s proximity, bilingual workforce, and USMCA tariff advantages enable faster cycle times and simplified FDA audits, encouraging partnerships like Lupin–Huons for regional supply coverage. Flexible manufacturing lines inside Brazilian free-trade zones equally appeal to specialty drug makers aiming to hedge over-reliance on Asia. As these relocations mature, the Latin America pharmaceutical contract manufacturing organization market gains consistent baseline volumes that smooth production scheduling and heighten plant utilization.

Expansion of local vaccine manufacturing post-COVID-19

Pandemic-era consortia injected both public and private money into vaccine fill-finish suites, BSL-2 labs, and ancillary cold rooms. Eurofarma’s collaboration with Pfizer-BioNTech to supply mRNA doses across the region exemplifies the new export orientation of local vaccine lines. Beyond coronavirus inoculations, CMOs now produce routine immunizations such as pneumococcal and HPV antigens, capturing long-term contracts from health ministries. This activity stimulates ancillary segments-from glass vial makers to dry-ice providers-multiplying value capture for the Latin America pharmaceutical contract manufacturing organization market.

AI-enabled process optimization boosting CMO margins

Samsung Biologics’ generative-AI document automation and Pfizer CentreOne’s Pharma 5.0 toolkit highlight early successes of artificial intelligence inside regulated production.[1]Eunju Hong, “Case Study: Samsung Biologics Automates Generative AI-Based Works,” Samsung SDS, samsungsds.com Pattern-recognition algorithms predict batch deviations, slash deviations, investigations’ turnaround, and shrink waste. The productivity uplift allows CMOs to offer more competitive pricing without compromising quality, nurturing a reputation for digital maturity that attracts tech-savvy biotech clients to the Latin America pharmaceutical contract manufacturing organization market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent regulatory inspections causing project delays | -0.4% | Brazil, Mexico, Colombia | Short term (≤ 2 years) |

| Currency volatility impacting imported raw-material costs | -0.3% | Argentina, Brazil, Chile | Short term (≤ 2 years) |

| GMP-trained talent shortage in secondary cities | -0.5% | Brazil, Mexico, Argentina | Medium term (2-4 years) |

| Power-grid instability raising operating costs in Brazil’s Northeast | -0.2% | Brazil Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Frequent regulatory inspections causing project delays

ANVISA’s 2025 agenda heightened unannounced GMP audits, compelling plants to maintain perpetual inspection readiness and occasionally suspend production for remediation. COFEPRIS mirrored the stance, increasing cross-border dossier harmonization with the FDA, which widens the documentation burden. Smaller CMOs in the Latin America pharmaceutical contract manufacturing organization market divert engineers from process improvement to compliance firefighting, diluting resource focus and slowing tech-transfer launches.

Currency volatility impacting imported raw-material costs

Most APIs, filters, and disposable bioprocess bags are dollar-denominated, whereas CMO revenue often accrues in reais or pesos. Sharp swings, particularly in Argentina, erode margin visibility and force price-escalation clauses that some sponsors resist. Operators hedge through forward contracts, but the cost of financial instruments still compresses earnings, limiting reinvestment for advanced modalities in the Latin America pharmaceutical contract manufacturing organization market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: API Manufacturing Consolidates High-Value Chemistry

API lines accounted for 42.10% of the Latin America pharmaceutical contract manufacturing organization market share in 2025, and their 3.62% CAGR forecast underscores clients’ preference to outsource potent-compound synthesis. Brazilian and Mexican plants now operate dedicated HPAPI suites with occupant-protection barriers that meet EU Annex 1 revisions. Secondary packaging remains smaller yet benefits from serialization mandates that mandate line upgrades across the region. As regulatory confidence rises, innovators funnel more tech-transfers for complex steps toward Latin facilities, lifting dollar-denominated backlog for the Latin America pharmaceutical contract manufacturing organization market.

Growing biologics API work further enriches margins. Single-use assemblies and tangential flow filtration installations become common, while analytical laboratories adopt mass-spectrometry-based release testing. Consequently, service-mix evolution migrates revenue from low-margin tablet compression to higher-value chemical and biological ingredient production, propelling reinvestment cycles that reinforce regional competitiveness inside the Latin America pharmaceutical contract manufacturing organization market.

By Drug Molecule Type: Advanced Therapies Gain Momentum

Small molecules still anchor 56.85% of revenue thanks to entrenched generic demand and scalable chemistry. However, the 3.95% CAGR in cell and gene therapy manufacturing illustrates the shifting portfolio. CDMOs retrofit Grade B suites for viral-vector fill-finish, and regulators craft fast-track biologics guidelines. Biologics pipelines such as monoclonal antibodies drive stainless and single-use hybrid facilities that diversify risk and attract venture-backed biotech clients to the Latin America pharmaceutical contract manufacturing organization market.

Emerging modalities create network effects: as ex-U.S. sponsors secure reliable viral-vector supply, they also shift analytical and stability work. This virtuous cycle nudges more capital toward specialized platforms, gradually diluting small-molecule weight without displacing its dominant revenue role through 2031.

By Scale of Operation: Clinical Batches Accelerate

Commercial-scale lots represented 61.70% of the Latin America pharmaceutical contract manufacturing organization market size in 2025, reflecting decades of generic exports. Yet clinical-phase output registers a 5.05% CAGR as sponsors relocate Phase II and Phase III trials to leverage diverse patient cohorts. CMOs invest in flexible, small-batch isolators, rapid-microbial-method labs, and e-batch-record systems. Quick-turn capabilities allow them to win multi-study frameworks that translate into future commercial supply, cementing the long-term presence of sponsors in the Latin America pharmaceutical contract manufacturing organization market.

Continuous-manufacturing skids for oral solids illustrate how lessons from high-volume lines migrate into early-stage settings, compressing tech-transfer timelines. Sponsors consequently lock in regional partners early, reinforcing stickiness and inflating option value for capacity reservations.

By End User: Democratization through Virtual Biotech

Big Pharma still controls 45.80% of spend due to legacy blockbuster contracts and multi-country launches. However, virtual biotech entities-firms built around one or two assets with zero internal manufacturing-expand at a brisk 4.45% CAGR. These lean teams prize turnkey solutions that span toxicology lots to commercial vials, making integrated CDMOs custodians of the entire chemistry-to-clinic continuum in the Latin America pharmaceutical contract manufacturing organization market.

Generic manufacturers also outsource complex steps such as spray-drying or continuous coating, freeing their own capacity for core molecules. The rising client diversity stabilizes demand curves and reduces exposure to single-account renegotiations, bolstering financial resilience for regional CMOs.

By Therapeutic Area: Oncology Rules, CNS Surges

Oncology generated 38.05% of 2025 sales, fueled by rising regional cancer incidence and robust contract demand for HPAPI containment and aseptic fill-finish lines. Concurrently, CNS therapeutics exhibit the fastest 4.33% CAGR through 2031 as mental-health awareness climbs and innovators reposition neurology assets for emerging markets. Multi-chamber bags for injectable antiepileptics and depot microspheres for schizophrenia therapy enter tech-transfer pipelines, enriching the product diversity of the Latin America pharmaceutical contract manufacturing organization market.

Cardiovascular drugs sustain volume via chronic-care programs, while infectious-disease vaccines maintain baseline utilization of adjuvant mixing tanks installed during the pandemic. This therapeutic mosaic balances cyclicality and supports continuous workforce specialization.

Geography Analysis

Brazil wielded 48.40% of the Latin America pharmaceutical contract manufacturing organization market share in 2025, anchored by Eurofarma’s network that includes the Itapevi complex, turning out more than 411 million units yearly. ANVISA’s digital dossier platform, rolled out in 2025, cuts review bottlenecks, encouraging sponsors to lodge larger product portfolios. However, electrical instability in the Northeast and local-currency depreciation mandate robust risk-mitigation plans for plants reliant on uninterrupted utilities.

Chile, though smaller, is projected to outpace peers with a 4.82% CAGR, buoyed by predictable macro-fundamentals and pro-investment statutes that refund up to 50% of R&D expenses. Its Pacific Alliance ties open tariff-free corridors to Asia, enticing CMOs focused on export-heavy biologics to choose Santiago industrial parks. As a result, sponsors seeking dual-hemisphere diversification funnel clinical and small-volume commercial lots into Chilean lines, amplifying the Latin America pharmaceutical contract manufacturing organization market footprint in the Southern Cone.

Argentina supplies niche capabilities in plasma-fractionation and mRNA fill-finish under PAHO’s tech-transfer program, yet working-capital strains from peso volatility force elevated hedging costs. Mexico leverages USMCA rules of origin to host API synthesis for U.S.-bound generics, whereas Colombia’s INVIMA streamlining positions Bogotá as an emerging serialization-hub. Together, these secondary geographies furnish redundancy and client-specific risk portfolios, ensuring the Latin America pharmaceutical contract manufacturing organization market exhibits geographic dispersion that insulates revenue against country-level shocks.

Regulatory Landscape

Pharmaceutical contract manufacturing in Latin America is overseen by national health regulators that enforce Good Manufacturing Practices (GMP) across drug substance, finished dose, and conditioning (packaging) activities, led by ANVISA (Brazil), COFEPRIS (Mexico), and ANMAT (Argentina). Regional alignment efforts tied to PIC/S participation have increased expectations for internationally comparable inspection practices and documentation packages, which raises the compliance bar for CMOs serving multi-country supply.

Mexico reinforced the policy linkage between domestic production capability and public-sector demand through the Guidelines for the Promotion of Investment in National Territory in the Production of Medicines and Health Supplies, published in May 2026. These guidelines emphasize local manufacturing, fill-finish, and packaging infrastructure while linking to consolidated procurement preferences. In parallel, GMP frameworks such as NOM-059-SSA1-2015 remain central in Mexico for manufacturing, conditioning, and quality control, while Brazil has continued to tighten oversight through ANVISA-led inspection intensity and platform-driven dossier handling introduced in 2025, affecting project timelines and readiness costs for regional and export-focused CMOs.

Value Chain Analysis

The value chain starts with inputs that are often imported and dollar-denominated, including APIs for some programs, excipients, primary packaging components, and bioprocess consumables such as filtration membranes, chromatography resins, and single-use assemblies, where single-source dependencies remain a recurring bottleneck. CMOs then carry out tech transfer, analytical method validation, and scale-up into GMP manufacturing across API and finished dosage forms. Conditioning follows through secondary packaging and, where required, serialization or aggregation, with quality release and distribution handled through temperature-controlled logistics networks for vaccines, biologics, and other sensitive products.

Manufacturing operations are centered around established industrial corridors that connect production clusters with logistics infrastructure. In practice, the Sao Paulo-Campinas axis supports cold-chain routes linked to Viracopos International Airport, enabling regional distribution and export handling. Downstream, sponsors distribute through national wholesalers, hospital and retail pharmacy networks, and government procurement channels, while regulatory scrutiny from bodies such as ANVISA and COFEPRIS increases the share of volume handled by certified, well-capitalized facilities. This also lifts the role of specialized QA/QC labs and compliant packaging partners within the contract manufacturing ecosystem.

Competitive Landscape

Competition is moderately concentrated. Global giants such as Catalent, Lonza, and Thermo Fisher anchor premium biologics and sterile capabilities, while regional leaders like Eurofarma, Grifols, and Megalabs dominate high-volume solids and plasma derivatives. Catalent’s São Paulo site focuses on Zydis fast-dissolve technology transfers, whereas Lonza partners with local biotech incubators to co-develop cell-therapy analytical assays. These investments sharpen the technology gradient within the Latin America pharmaceutical contract manufacturing organization market.

Digitalization differentiates contenders: Samsung Biologics’ AI audit-automation compresses compliance cycles, giving it a time-to-market edge. Eurofarma couples MES-driven OEE dashboards with photovoltaic arrays that lower Scope 2 emissions, appealing to ESG-oriented sponsors seeking carbon-footprint disclosures. Megalabs channels its USD 70 million IDB Invest facility into modular clean-rooms that can toggle between penicillin and cephalosporin lines, upgrading flexibility for client pipelines.

White-space remains in viral-vector manufacturing and ultra-cold chain packaging. Firms that scale 2-8 °C logistics into −70 °C formats can capture upcoming gene-editing platforms. Similarly, clinical-trial supply-chain orchestration services-temperature-validated kitting and returns management-provide incremental stickiness. As sponsors bundle such adjunct services, integrated players secure multiyear master service agreements, reinforcing revenue visibility across the Latin America pharmaceutical contract manufacturing organization market.

Latin America Pharmaceutical Contract Manufacturing Organization Industry Leaders

Catalent, Inc.

Thermo Fisher Scientific Inc.

Lonza Group AG

Boehringer Ingelheim International GmbH

Pfizer Inc. (Pfizer CentreOne)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Named investment programs and capacity expansions across multiple countries are creating whitespace for CMOs and contract packagers that can support compliant scale-up, validation, and reliable release for both regional supply and export-oriented programs. Mexico is a clear example of industrial-policy-driven demand formation, with the May 2026 Health Investment Project announcement totaling 21 billion pesos of private-sector funding across seven pharmaceutical production ventures involving companies including Abbott, Bristol Myers Squibb, Sanofi, and Liomont. The rollout expands the partner base for local development, manufacturing, and packaging services that align with COFEPRIS requirements and procurement-linked localization criteria.

Brazil and smaller hubs add additional opportunity lanes in injectables, vaccines, and high-throughput solids. The federal plan to structure a Health Biotechnology Industrial Complex PPP in Rio de Janeiro (referenced at a USD 1.2 billion scale) targets higher regional vaccine output, while private capacity builds such as Novo Nordisk's April 2025 USD 1.09 billion investment for GLP-1 capacity and Adium's March 2026 USD 60 million Paraguay plant expansion (to 100 million units annually) increase demand for qualified tech transfer, QA/QC, and compliant packaging throughput. Together, these moves raise the need for cold-chain capable distribution and for packaging providers that can integrate serialization and aggregation when sponsors require multi-market traceability.

Recent Industry Developments

- July 2026: Thermo Fisher Scientific expanded its operations in Brazil by establishing a new research plant. The expansion increases in-region capabilities that support regulated manufacturing programs through applied development and analytics, supporting sponsors running tech transfers and scale-up work in Latin America.

- December 2025: AptarGroup acquired Sommaplast, a Brazil-based provider of oral dosing pharmaceutical packaging solutions. The acquisition adds specialized packaging capability and local capacity, supporting sponsor demand for integrated device-plus-packaging formats and more resilient regional supply for finished products.

- July 2024: Grunenthal announced an investment of over EUR 80 million to modernize its production sites in Chile and Ecuador, increasing capacity for solid dosage form manufacturing. The modernization expands qualified regional throughput and can translate into more outsourcing-ready capacity as plants upgrade systems aligned with GMP expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue earned from outsourced pharmaceutical manufacturing work delivered by specialized contract manufacturers for drug companies across Latin America. It covers contract activity from making active ingredients through finished dosage manufacturing and related secondary packaging services.

Scope exclusions: The sizing excludes in-house captive production done only for a parent company, and it also excludes pure research-only contracting that does not result in manufacturing revenue.

Segmentation Overview

- By Service Type

- API Manufacturing

- Small Molecule

- Large Molecule

- High-Potency API (HPAPI)

- FDF Development and Manufacturing

- Solid Dose

- Liquid Dose

- Injectable Dose

- Secondary Packaging

- API Manufacturing

- By Drug Molecule Type

- Small Molecule

- Biologics

- Advanced Therapies (Cell and Gene)

- By Scale of Operation

- Clinical-Phase Manufacturing

- Commercial-Scale Manufacturing

- By End User

- Big Pharma

- Generic Pharma

- Emerging / Virtual Biotech

- Specialty Pharma

- By Therapeutic Area

- Oncology

- Cardiovascular

- Central Nervous System (CNS)

- Infectious Disease

- Other Therapeutic Areas

- By Country

- Brazil

- Chile

- Argentina

- Rest of Latin America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model, with emphasis on drug output, trade flows, and the policy environment that shapes outsourcing decisions in Latin America. We pulled public statistics and reference points from sources such as PAHO and WHO publications, UN Comtrade trade tables for pharmaceutical inputs and medicines, World Bank macro indicators, national health and regulatory portals in Brazil and Mexico, and peer-reviewed journals covering pharmaceutical manufacturing trends.

To translate the context into usable sizing inputs, we also reviewed secondary material such as company annual reports, investor presentations, association websites, and reputable press to understand service mix and capacity additions. In a few cases, paid subscriptions that support company financials, patents, and shipment-level import and export checks were used to validate directionally important assumptions. These desk sources are illustrative only, and many other public and paid references were used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with contract manufacturers, pharma outsourcing managers, quality and regulatory specialists, and supply chain leaders who manage regional production and sourcing. The respondent input was used to confirm which services are routinely outsourced, how pricing moves by dosage form and molecule type, and which country markets are driving new contracts. We then used these clarifications to tighten assumptions where public disclosures were not specific enough for the Latin America service mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | |

| Mid tier: 48% | Functional/Unit leaders: 26% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

The core sizing logic is built using a top-down approach where production, outsourcing penetration, and service-mix shares are applied to a Latin America demand pool, then converted into service revenue using realistic price bands. Totals were corroborated through selective bottom-up approximations, including rolling up a sample of contract manufacturer revenues and checking implied volumes against typical plant throughput for key dosage forms.

Key model inputs included the split of outsourced work between API, finished dosage manufacturing, and secondary packaging, the share of clinical versus commercial manufacturing, average pricing progression by dosage form, and country-level demand signals tied to Brazil, Mexico, and the rest of the region. We also used export and import movement of pharmaceutical inputs, currency effects on reported revenues, and announced capacity expansions to avoid over-counting. For forecasting, scenario analysis was used around outsourcing intensity and pricing, with scenarios anchored to consensus views gathered in interviews on likely contract flow and utilization over the next few years. Where company-level disclosure gaps appeared, we applied ranges and then narrowed them using peer comparisons and the service mix respondents described as most common.

Data Validation & Update Cycle

Validation was handled through several layers of checks so that single-source bias did not drive the final number. We compared model outputs against independent signals such as trade movements for relevant pharma categories, known capacity changes, and the expected share split between API and finished dosage work, then investigated variances that appeared too large for local Latin America context.

Before sign-off, the model is reviewed in steps, including a second-analyst pass on assumptions, math checks, and sensitivity checks on pricing and outsourcing rates. If results moved outside expected ranges, respondents were re-contacted to clarify what changed, such as a large contract win, a regulatory shift, or a major currency swing. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so the client receives the latest view.

Mordor Intelligence's Latin America Pharmaceutical Contract Manufacturing Market Size Measured Against Other Published Estimates

Published market sizes for this topic can look far apart because groups define the service perimeter differently and also vary on the year used, currency handling, and what they treat as manufacturing revenue. Differences also come from how much weight is given to public production and trade signals versus interview-led assumptions on outsourcing rates.

Some estimates expand the scope beyond manufacturing into contract research and other supporting services, which naturally lifts the total. For Mordor Intelligence, the count is limited to contract manufacturing organization revenue across API manufacturing, finished dosage formulation development and manufacturing, and secondary packaging within Latin America. This keeps the number tied to manufacturing work that is actually outsourced and billed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.21 B (2026) | |

| Global Advisory A | USD 24.09 B (2026) | This figure rolls contract manufacturing together with contract research and related support services, so the total is not confined to manufacturing-only revenue. It also uses a longer-horizon growth arc that can embed more aggressive outsourcing and price assumptions. |

| Regional Consultancy B | USD 3.08 B (2024) | The estimate is anchored to an earlier base year and can differ due to currency timing and how service buckets such as secondary packaging and development work are treated. Limited transparency on how clinical-phase versus commercial work is weighted can also shift the total. |

The table shows that the main spread is explained by scope and timing, not by a single math choice. By keeping the inputs traceable to manufacturing services, country demand signals, and interview-confirmed outsourcing patterns, the resulting market size stays repeatable and easier to reconcile as new capacity and contracts appear.

Key Questions Answered in the Report

What is the current size of the Latin America pharmaceutical contract manufacturing organization market?

The Latin America pharmaceutical contract manufacturing organization market size stood at USD 3.21 billion in 2026 and is projected to reach USD 3.63 billion by 2031.

Which country holds the largest share of contract manufacturing in Latin America?

Brazil dominates with 48.40% market share owing to established infrastructure and supportive regulatory frameworks.

Which service segment is growing fastest in regional CMOs?

API manufacturing shows the highest growth, forecast to expand at a 3.62% CAGR through 2031 as sponsors outsource high-potency chemistry.

How quickly are clinical-phase manufacturing services expanding?

Clinical batch manufacturing is expected to grow at a 5.05% CAGR due to rising Phase II/III trial activity moving into the region.

Why are North-American firms shifting production to Latin America?

Near-shoring lowers logistics risk, benefits from USMCA trade terms, and keeps plants within similar regulatory regimes while reducing costs.

Which therapeutic area offers the highest growth potential for CMOs?

CNS therapeutics lead growth with a projected 4.33% CAGR, reflecting increased investment in mental-health treatment pipelines.

Page last updated on: