Ladder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

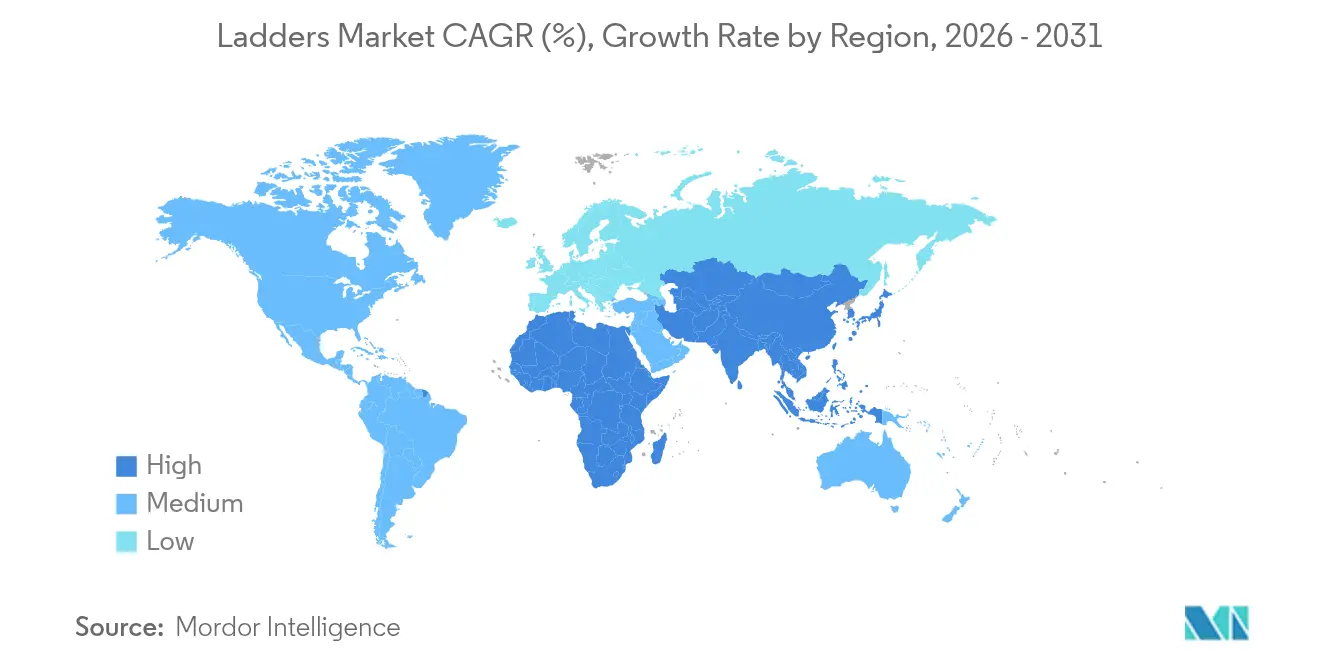

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

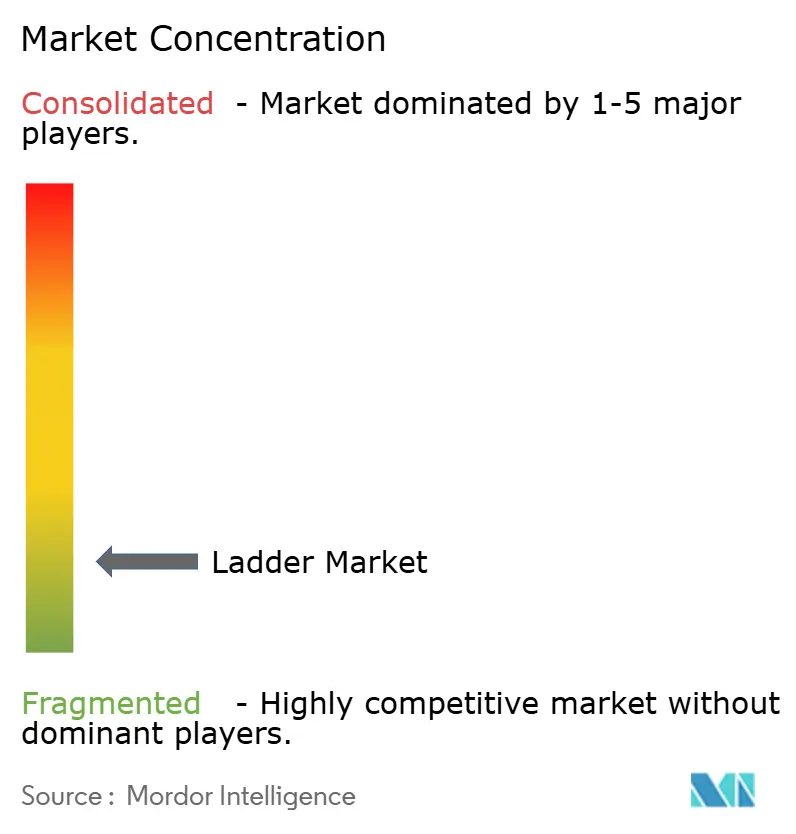

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ladder Market Analysis by Mordor Intelligence

The ladder market size was USD 2.37 billion in 2025, is set to reach USD 2.46 billion in 2026, and is forecast to rise to USD 3.21 billion by 2031, reflecting a 5.47% CAGR during 2026-2031. Purchase behavior continues to shift toward omnichannel, with online sales accelerating from a lower base and supporting premium product sales that feature enhanced safety and portability. North America held the largest regional position in 2025, while Asia-Pacific is the fastest-growing region through 2031, supported by construction, grid expansion, and telecom upgrades that require non-conductive access equipment. Market structure remains fragmented as localized production, varied duty ratings, and enforcement of safety standards shape product selection and distribution. Regulatory updates such as OSHA’s PPE fit rules and the ongoing alignment to EN 131 in Europe continue to raise compliance thresholds in professional settings[1]John Doe, “Personal Protective Equipment Standard 1926.95,” Occupational Safety and Health Administration, osha.gov .

Key Report Takeaways

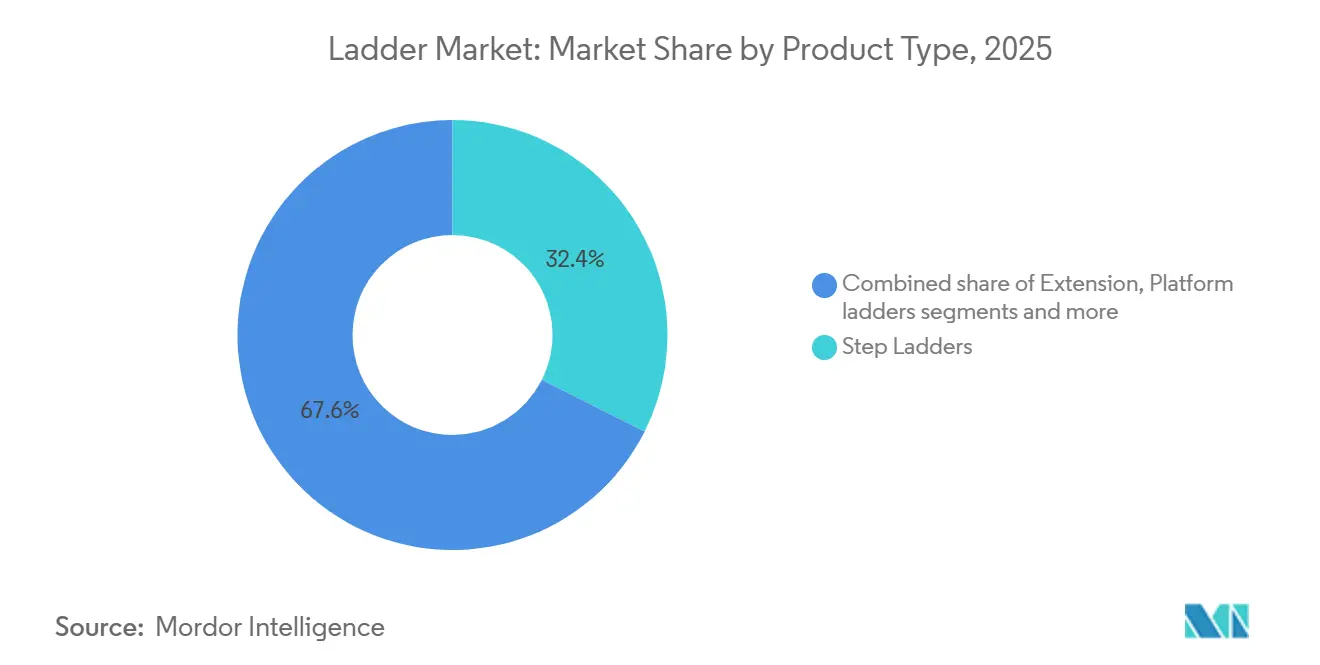

- By product type, step ladders led with 32.4% of the ladder market share in 2025, while telescopic ladders are projected to expand at a 6.86% CAGR to 2031.

- By material, aluminum held 48.6% of the ladder market share in 2025, while steel recorded the highest projected CAGR at 5.76% through 2031.

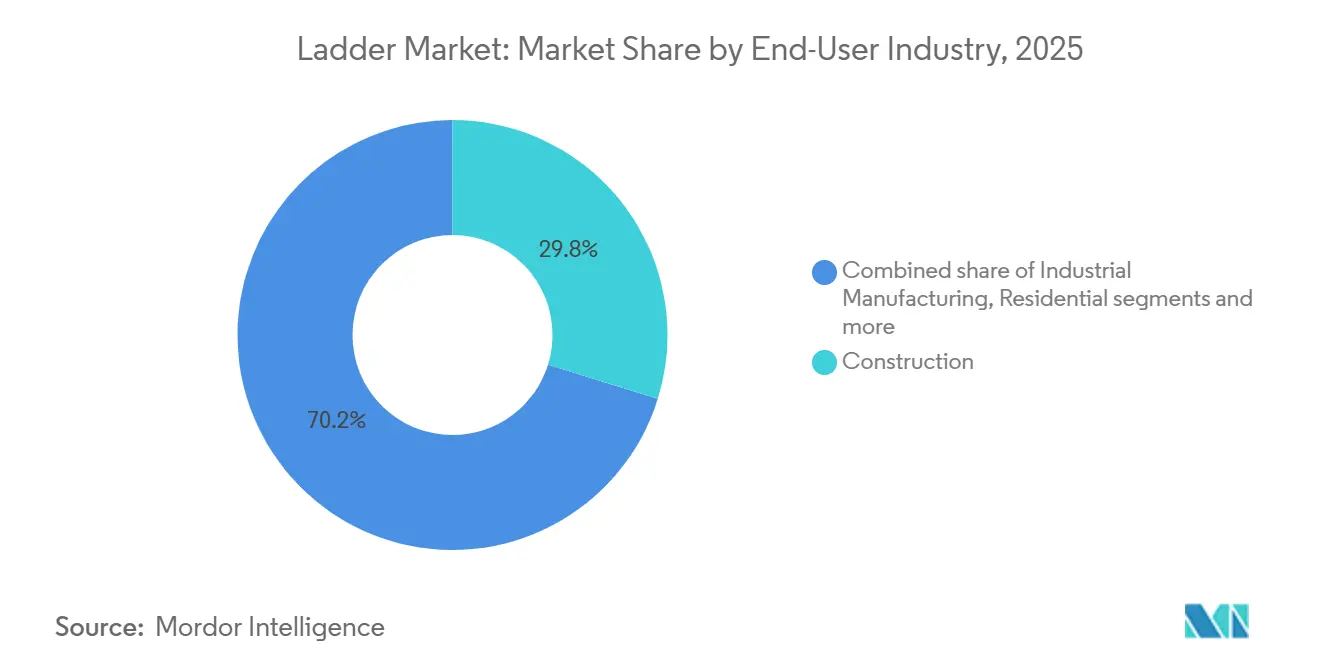

- By end-user, construction accounted for 29.8% of the ladder market share in 2025, while utilities and telecom are advancing at a 6.51% CAGR through 2031.

- By distribution channel, offline captured 71.5% of the ladder market share in 2025, while online is projected to expand at an 8.06% CAGR through 2031.

- By geography, North America held 34.7% of the ladder market share in 2025, while Asia-Pacific is the fastest-growing region at a 5.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ladder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction activity and site-access intensity | +1.2% | North America and Europe core, and Asia-Pacific is emerging | Medium term (2-4 years) |

| DIY and home renovation intensity | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| Safety standards, pushing platform, and fiberglass adoption | +1.1% | Global, with North America and the Europe leading the enforcement | Medium term (2-4 years) |

| E-commerce and multichannel distribution expansion | +0.8% | Global, Asia-Pacific accelerating | Short term (≤ 2 years) |

| Utility and telecom electrification favors non-conductive ladders | +0.7% | North America, Western Europe, India | Long term (≥ 4 years) |

| Warehouse ergonomics focuses on boosting platform or podium ladders | +0.5% | North America, and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction Activity and Site-Access Intensity

The United States construction spending reached USD 2,164.4 billion in 2025, a slight decline from 2024 levels, yet the residential base and public works categories sustained ongoing demand for access equipment used in installation, inspection, and maintenance tasks[2]U.S. Census Bureau Analysts, “Monthly New Residential Construction, December 2025,” U.S. Census Bureau, census.gov . New residential construction delivered 1,358,700 housing starts for the full year 2025, which supported periodic ladder purchases for trades and home improvement projects that follow handover cycles. Remodeling continues to be an anchor for the ladder market as households invested heavily in improvements during 2021 to 2023, reinforcing repeat-use categories like painting, lighting, and roofing that often require step and extension ladders. Public infrastructure outlays and jobsite rules related to ladder extension and landing heights shape procurement toward rated fiberglass and platform models designed for heavy-duty use in traffic-exposed settings. These dynamics support higher-value product adoption even when new-build cycles soften, which helps stabilize the ladders market through mixed economic conditions.

DIY and Home Renovation Intensity

Home improvement retailers signaled steady consumer activity in 2025 that aligns with ongoing DIY and small professional projects that favor step, folding, and multi-position ladders. The Home Depot reported fiscal 2025 revenue of USD 164.7 billion with digital channels maintaining high single-digit growth, which signals ongoing omnichannel engagement for tools and supplies that include ladders and ladder accessories[3]Investor Relations, “The Home Depot Announces Fourth Quarter and Fiscal 2025 Results,” The Home Depot, homedepot.com . Lowe’s reported positive comparable sales in mid-2025 with full-year guidance near USD 85 billion, which points to sustained demand for household maintenance solutions and supports retail availability of ANSI-rated ladder assortments in stores and online. The United States retail e-commerce sales increased year over year in Q3 2025 and reached 16.4% of total retail, which reinforces digital comparison behaviors where shoppers filter by duty rating, reach height, and certifications before placing orders or using buy online, pick up in store options. Premium models, such as podium ladders with integrated tops for tool storage and larger work zones, have gained traction as DIY users and pros trade up within categories that promise safety and convenience benefits. EU markets continue to align on EN 131 ladder standards, and the 2025 numbering update maintained technical requirements while prompting labeling updates, which helps filter out non-compliant imports in consumer channels.

Safety Standards Pushing Platform and Fiberglass Adoption

Falls from elevation remain a leading cause of severe injuries in construction, and regulators continue to focus on prevention through better equipment selection and fit requirements that affect how ladders and associated fall protection are used on-site. In January 2025, OSHA’s updated PPE fit rule, which became effective, requires all protective equipment to properly fit each worker, which raises compliance expectations on jobs that involve fixed ladders and elevating tasks. Platform and podium ladders certified under the A14.7 standard provide an enclosed standing area with guardrails and are being specified more often for tasks at height where stability, tool storage, and reduced overreaching are priorities. Fixed ladder rules and walking-working surface provisions reinforce the need for adequate landing heights, secure placement, and three-point contact, which direct buyers toward higher duty ratings and fiberglass models when work occurs around energized equipment. Grid modernization and telecom installations also pull demand toward non-conductive ladders in field conditions, which anchors growth in fiberglass categories where safety and compliance are central to product selection.

E-Commerce and Multichannel Distribution Expansion

Digital channels are gaining share in the ladders market from a smaller base as shoppers evaluate specifications online and retailers improve fulfillment for oversized items. The channel recorded a faster growth outlook than physical retail for 2026 to 2031, supported by the rise of mobile browsing, expanded marketplace assortments, and retailer investment in click and collect journeys. The Home Depot reported consistent online growth in 2025, which reflects customer use of digital tools to compare ladder duty ratings, heights, and compliance credentials before picking up orders in store. The United States retail e-commerce posted year-over-year gains in Q3 2025 and reached 16.4% of total retail, which sustains the shift of research and purchasing toward online platforms for categories including ladders. Marketplaces also matter since leading retailers in the United States continue to deepen their building materials and tools assortments, which helps grow ladder penetration in digital baskets for both DIY and trade customers. As omnichannel matures, manufacturers are balancing wholesale and direct-to-consumer approaches to reach buyers who want transparent testing, clear duty ratings, and compatibility with accessories like levelers and stabilizers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ladder fall injuries are prompting the substitution of MEWPs and training | -0.6% | Global, North America, and the Europe most affected | Short term (≤ 2 years) |

| Raw material price volatility, aluminum and fiberglass resins | -0.5% | Global, United States, tariff-driven | Short to Medium term |

| Warehouse automation reduces mobile ladder use in logistics centers | -0.4% | North America, Europe, China | Medium term (2-4 years) |

| Compliance burden and certification costs for OSHA and EN 131 standards | -0.3% | North America, Europe, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ladder Fall Injuries Prompting Substitution to MEWPs and Training

Falls remain a leading source of severe injuries in construction and related sectors, and this risk profile sustains interest in alternatives to traditional ladders for prolonged elevated tasks. Guidance from safety authorities highlights aerial lifts and scaffolds as safer options when tasks extend in duration or involve heavy tools, which reduces demand for commodity A-frame and straight ladders in commercial job scopes. Contractors also face a stronger emphasis on fit and selection of personal protective equipment, which raises expectations for training and inspection programs and may extend ladder replacement cycles when use is more controlled. Annual safety stand-downs reach hundreds of thousands of workers and reinforce correct ladder setup, inspection, and storage, which improves safety outcomes but can slow unit turnover as misuse-related damage declines. These factors reduce volumes in specific commercial applications while leaving residential and utility segments more reliant on ladders, where worksite constraints limit the use of mobile elevating equipment.

Raw Material Price Volatility, Aluminum and Fiberglass Resins

Aluminum input costs moved higher through late 2025 according to producer price data for mill shapes, which raised pressure on margins and wholesale price negotiations in aluminum-intensive ladder lines. Government materials summaries also flagged supply and pricing dynamics across aluminum markets into 2026, which complicates planning for manufacturers that rely on extrusions and stamped components. Volatility increases the difficulty of setting long-dated pricing with large retail partners, which can lead to shorter commitment windows or fewer forward buys that tighten working capital for producers. Fiberglass resin and synthetic fibers showed comparatively modest producer price changes into late 2025, yet these inputs still depend on petrochemical feedstocks and stable production capacity, which can tighten during shocks. Over time, manufacturers may adjust product mixes, tooling, and sourcing to balance input risk with safety and performance requirements, which influences the ladders market through 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Telescopic Ladders Drive Premiumization Amid Space Constraints

Step ladders held the lead with 32.4% share in 2025, while telescopic ladders are projected to expand at a 6.86% CAGR through 2031 as buyers value compact storage and adjustable reach in tight spaces. In residential maintenance, step ladders remain the first choice for interior tasks because self-supporting frames and modest reach heights address most rooms without wall support. Trade users adopt extension and multi-position designs for exterior work, yet telescopic designs have gained share as safer locks and stabilizers improve portability and setup in urban settings. Product innovation has focused on locking systems, safety indicators, and integrated tops that expand usable work zones and reduce overreaching in frequent repositioning tasks. The ladder market benefits when buyers trade up to premium models that combine reach, storage, and stability in one unit, where a basic ladder would be less productive.

Telescoping and platform designs have expanded retailer assortments as omnichannel search filters steer customers toward models that meet duty ratings for specific jobs. Premium telescoping models have moved up the ladder of consideration among pros who work from vans and compact trucks, where storage is limited, and job types vary by day. Facility managers are specifying podium ladders for fixed stations where elevated picking and maintenance recur, which shifts revenue toward higher-value units with enclosed platforms and guardrails. The ladder industry continues to respond with incremental safety and comfort features rather than radical new materials, which keeps product education focused on duty ratings, reach height, and platform size. As buyers choose models that reduce fatigue and improve throughput, the product mix tilts toward categories with better margins, which supports the ladders market during mixed construction cycles.

By Material: Steel Gains as Aluminum Economics Reset and Fiberglass Anchors Electrical Safety

Aluminum retained leadership at 48.6% share in 2025, valued for light weight, corrosion resistance, and transport convenience in frequent-use tasks where solo handling matters most. Steel posted the fastest growth outlook at a 5.76% CAGR as buyers seeking rigidity and high load ratings in industrial and warehouse settings opted for heavier frames that accommodate larger platforms and accessories. Producer price data signaled higher aluminum cost pressure into late 2025, which led some manufacturers and buyers to weigh steel or fiberglass alternatives in applications where weight is less critical. Fiberglass maintained momentum where non-conductive properties are essential, supported by safety standards for reinforced plastic ladders that address dielectric strength expectations in live-line proximity. Grid and telecom work continue to underpin fiberglass demand, a trend reinforced by elevated United States grid investment through 2025 that keeps line crews active on distribution and rooftop projects[4]EEI Editorial Team, “Electric Companies to Invest Nearly $208B in 2025 to Strengthen Grid and Drive Economic Growth,” Edison Electric Institute, eei.org .

Portfolio strategy across materials is shifting to balance input risk, safety mandates, and product performance. Fiberglass is increasingly prioritized in utility, telecom, and solar segments that operate near energized assets where OSHA rules limit conductive materials. Steel is specified in warehouses and plants where heavy loads and fixed stations favor rigidity and broader platforms, while aluminum continues to dominate in DIY and small contractor jobs that demand easy carry and frequent repositioning. These choices align with the ladder industry's focus on clear duty ratings, fit-for-purpose design, and compliance with ANSI or EN requirements, which buyers increasingly confirm online before purchase. Over time, material selection will continue to reflect end-use conditions and total cost of ownership rather than single-factor price comparisons, which supports resilience in the ladder market.

By End-User: Utilities and Telecom Fastest Growing as Grid Modernization Accelerates

Construction accounted for 29.8% of global ladder demand in 2025, reflecting the scale of projects that continue to require access equipment for finishing, repair, and inspection tasks across sites of varying complexity. Utilities and telecom are advancing at a 6.51% CAGR and form the fastest-growing end-user segment, driven by grid investments and distributed communications infrastructure that demand non-conductive ladders for field deployment. Construction spending in the United States remained high in 2025, which kept a baseline of ladder usage intact across residential and nonresidential scopes despite a marginal decline year over year. Electric company investment plans and forward capacity changes indicate a steady pipeline of work that requires compliant equipment and training, which ties procurement to ANSI and OSHA expectations.

Commercial and institutional maintenance teams continue to specify platform and podium ladders for safe, repeatable tasks that happen near people and inventory, which benefits designs with enclosed platforms and guardrails. Industrial users balance uptime and safety and are adopting heavier frames and larger platforms in high-traffic zones where stability and durability limit unplanned downtime. Residential DIY participation remains steady, supported by retailer results in 2025 that point to ongoing home maintenance projects where step and multi-position ladders are frequent purchases. Across end-users, non-conductive properties in fiberglass and ergonomic benefits in platforms unify procurement rationales that emphasize safety and productivity, reinforcing premiumization in the ladders market.

By Distribution Channel: Online Outpaces Offline as Omnichannel Reshapes Buyer Journeys

Offline channels captured a 71.5% share in 2025, while online is projected to expand at an 8.06% CAGR to 2031 from a smaller base, supported by search-led product discovery and improved fulfillment for bulky items. The ladder market benefits from product education at the shelf that shows reach height, duty rating, and stabilizer options for quick visual comparison in stores. At the same time, online journeys allow customers to filter by ANSI class, platform size, and material before choosing either direct delivery or store pickup. Leading home improvement retailers reported steady online growth in 2025, which validates the role of digital research and fulfillment in categories like ladders that require both specification checks and convenience at purchase.

The United States retail e-commerce penetration rose to 16.4% in Q3 2025, underscoring broader consumer comfort with ordering large-format items online when delivery speed and damage-free handling are reliable. Big marketplaces rank among the largest United States retailers, which helps bring ladder brands into fast-turn online categories where verified reviews and safety credentials influence final choice. Manufacturers now mix wholesale partnerships, marketplace presence, and direct-to-consumer channels to reach different buyer cohorts, which spreads risk and allows for premium accessory upsells. As omnichannel matures, data-driven merchandising aligns inventory with local project needs, which supports steady sell-through in the ladders market. In this environment, clear compliance labeling and stability features are a differentiator that supports repeat purchase and brand trust.

Geography Analysis

North America held 34.7% of global demand in 2025, supported by a large installed base of residential and nonresidential assets that require ongoing maintenance, along with steady investment in power and communications infrastructure. The United States construction spending remained high in 2025, which helped keep core ladder categories active across trades and DIY despite year-over-year moderation. Enforcement of OSHA standards continues to shape product selection toward ANSI-rated models, and updates to PPE fit rules in 2025 reinforced compliance expectations that extend to elevated tasks and fixed ladders. Utility work remains a support, given strong 2025 grid investment plans that rely on compliant non-conductive equipment for crews operating near energized assets. Retail infrastructure helps maintain access to in-store advice and online fulfillment, which together support category resilience in the ladders market.

Asia-Pacific is the fastest-growing region with a 5.91% CAGR through 2031, helped by urbanization, power capacity additions, and telecom densification that require frequent elevated access in construction and maintenance work. Planned capacity additions in the near term and growing electricity demand point to ongoing investment in distribution and rooftop installations, which anchor fiberglass usage for non-conductive work. Telecom infrastructure plans emphasize more distributed sites and edge nodes that increase the number of street-level installations, which favors compact, non-conductive ladders for safer work near live lines. As online platforms deepen assortments, buyers in space-constrained urban settings compare reach, duty ratings, and stabilizers before choosing brands that demonstrate standards compliance and after-sales support. With these structural drivers, the ladders market in Asia-Pacific continues to outpace mature regions.

Europe remains a significant share contributor with mature safety frameworks, professionalized maintenance sectors, and a harmonized ladder standard under EN 131 that saw an administrative numbering update in 2025. Buyers in commercial and institutional settings specify products against platform size, load capacity, and certification labels, which guide procurement toward premium brands that publish testing data and standards coverage. Industrial and warehouse facilities emphasize ergonomic upgrades, which support the use of podium platforms and enclosed standing areas aligned with ANSI and EN provisions, particularly in high-traffic or inventory-dense environments. Market access across the region remains tied to labeling accuracy and documentation, which continues to limit non-compliant imports. These factors stabilize demand patterns in Europe and support steady replacement and upgrade cycles in the ladder market.

Competitive Landscape

Market structure is highly fragmented, with the top five players collectively accounting for a very small percent of global revenue in 2025, which underscores regional manufacturing clusters and the influence of safety certification over pure scale. Competitive energy is visible in product refreshes that emphasize safer standing areas, tool organization, and portability for frequent repositioning on site. In September 2025, WernerCo introduced a compact fiberglass Ready Step to target jobsite efficiency, which reflects customer interest in lighter units that protect against electrical hazards while managing tools at height. WernerCo also continued to invest in telescoping ladders and platform solutions that move buyers up the value curve and integrate with training and safety programs for professionals. With buyers scrutinizing compliance and ergonomics, premium brands rely on standards alignment and retail presence to command price premiums in the ladder market.

Go-to-market strategies blend wholesale, marketplace, and direct channels as manufacturers seek reach and margin balance. Wholesale maintains scale and showroom validation for duty ratings and stability features, while marketplace presence expands selection breadth and review-based trust in brands that publish testing claims. Direct-to-consumer sites help brands upsell accessories such as stabilizers, levelers, and trays that elevate workflow at the jobsite and at home. In parallel, safety education has become part of the commercial offering, with manufacturers coordinating training that supports OSHA-aligned practices and on-site inspections that extend equipment life and reduce misuse. As these services expand, premium brands can capture value beyond the unit sale and differentiate through credible training and documentation.

Product development remains incremental and centered on safety and productivity. Larger work zones, enclosed platforms, and integrated storage are being adopted broadly where repetitive elevated tasks occur, particularly in warehouses and maintenance departments. Reinforced plastic and fiberglass remain the default for work near live electrical assets, and aluminum continues to dominate when frequent carry and setup drive the choice. Adjacent categories in access and storage show some players diversifying into premium equipment for regulated environments, which provides additional margin opportunities beyond commodity ladders. Given the fragmented base and the importance of regional logistics costs, no single player has achieved a dominant global position, and competition is expected to remain plural for the forecast period.

Ladder Industry Leaders

WernerCo

Louisville Ladder

Little Giant Ladder Systems (Wing Enterprises)

ZARGES GmbH

Hailo Werk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: WernerCo launched the WERNER Ready Step, a lightweight, compact fiberglass step ladder designed for enhanced jobsite efficiency, featuring integrated tool storage and ergonomic design.

- August 2025: The European Ladder Association announced administrative updates to EN 131 standards numbering without technical changes, requiring labeling updates for manufacturers and suppliers.

- April 2025: WernerCo introduced a new professional-grade telescoping ladder featuring enhanced locking mechanisms and extended reach capacity.

- January 2025: OSHA’s updated Personal Protective Equipment fit rule became effective, mandating that all construction PPE fit each worker properly.

Global Ladder Market Report Scope

The ladder market report focuses on the market dynamics, trends, and demand of ladders in the market. The report highlights key trends and factors that are driving the market, along with certain restraints imposed on the market. Moreover, the key profiles of the manufacturers in the global market are provided in detail.

The ladder market is segmented by product type, material, end-user, distribution channel, and geography. By product type, the market is sub-segmented into step, extension, platform, folding, telescopic, and specialty ladders. By material, the market is sub-segmented into aluminum, fiberglass, steel, wood, and plastic/composite. By end-user, the market is sub-segmented into residential/DIY, construction, industrial, utilities & telecom, commercial, and transportation/logistics. By distribution channel, the market is sub-segmented into offline and online. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts for the ladder market in value (USD) for all the above segments.

| Step Ladders |

| Extension Ladders |

| Platform Ladders |

| Folding Ladders |

| Telescopic Ladders |

| Specialty/Custom Ladders |

| Aluminum |

| Fiberglass |

| Steel |

| Wood |

| Plastic/Composite |

| Residential / DIY |

| Construction |

| Industrial Manufacturing |

| Utilities & Telecom |

| Commercial & Institutional |

| Transportation & Logistics |

| Offline (Home-Improvement Stores, Industrial Distributors) |

| Online (E-commerce Platforms, Direct-to-Consumer) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Step Ladders | |

| Extension Ladders | ||

| Platform Ladders | ||

| Folding Ladders | ||

| Telescopic Ladders | ||

| Specialty/Custom Ladders | ||

| By Material | Aluminum | |

| Fiberglass | ||

| Steel | ||

| Wood | ||

| Plastic/Composite | ||

| By End-User Industry | Residential / DIY | |

| Construction | ||

| Industrial Manufacturing | ||

| Utilities & Telecom | ||

| Commercial & Institutional | ||

| Transportation & Logistics | ||

| By Distribution Channel | Offline (Home-Improvement Stores, Industrial Distributors) | |

| Online (E-commerce Platforms, Direct-to-Consumer) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the ladder market growth outlook through 2031?

The ladder market size was USD 2.37 billion in 2025 and is projected to reach USD 3.21 billion by 2031 at a 5.47% CAGR over 2026 to 2031, supported by premiumization and omnichannel expansion.

Which regions lead demand and growth for ladders?

North America led with a 34.7% share in 2025, while Asia-Pacific is the fastest-growing region with a 5.91% CAGR through 2031, helped by construction, grid, and telecom investments.

Which product and material categories are most important for buyers?

Step ladders led with 32.4% share in 2025, and telescopic models are the fastest growing, while aluminum held 48.6% share and steel posted the highest material CAGR, with fiberglass prioritized for non-conductive safety needs.

How are safety rules shaping the procurement of ladders?

OSHA’s 2025 PPE fit update, walking-working surface rules, and EN 131 compliance in Europe steer buyers toward ANSI and EN certified models, including fiberglass and platform ladders near energized or high-traffic work.

What role does e-commerce play in ladder purchases?

Online sales are growing faster than offline from a smaller base and reached higher penetration alongside retail e-commerce gains in Q3 2025, as shoppers compare duty ratings and certifications online and use store pickup for convenience.

Which end-user segments are shaping future demand?

Construction remains the largest end-user, while utilities and telecom show the fastest growth due to grid modernization and distributed telecom sites, which push the adoption of non-conductive fiberglass ladders and platform solutions.

Page last updated on: