Global Laboratory Informatics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

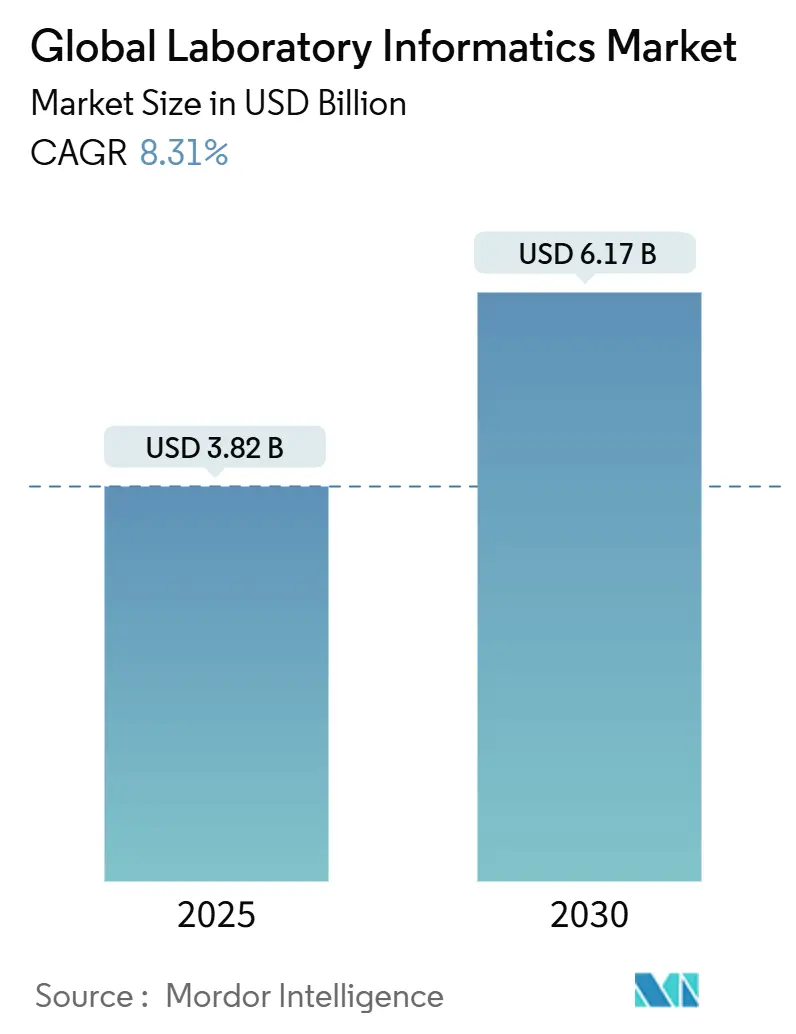

| Market Size (2025) | USD 3.82 Billion |

| Market Size (2030) | USD 6.17 Billion |

| Growth Rate (2025 - 2030) | 8.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

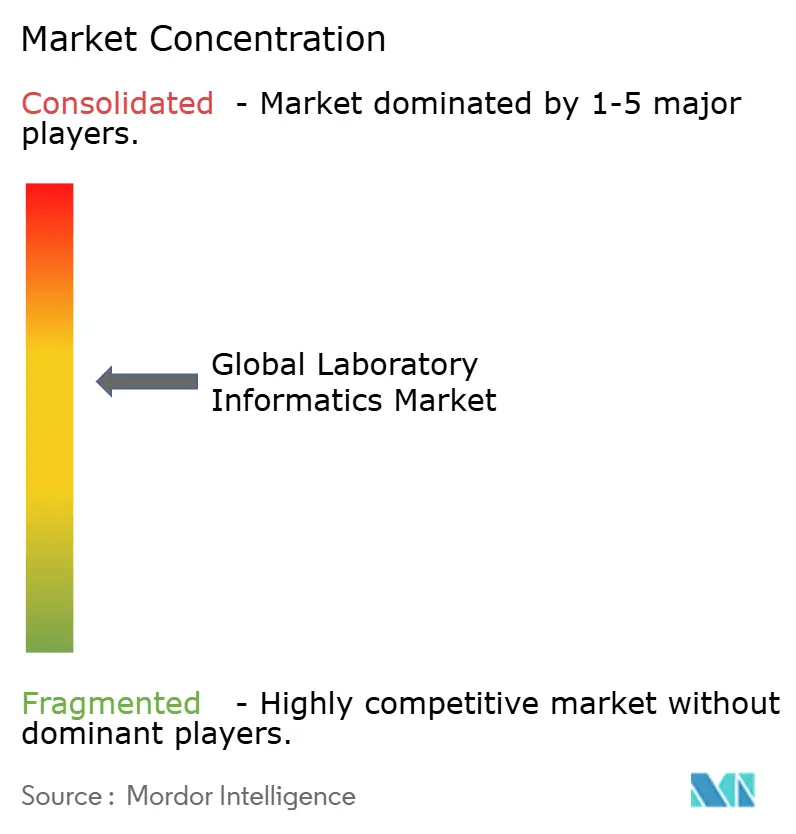

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Laboratory Informatics Market Analysis by Mordor Intelligence

The laboratory informatics market is valued at USD 3.82 billion in 2024 and is projected to reach USD 6.17 billion by 2030, advancing at an 8.31% CAGR over 2025-2030. Growth is underpinned by laboratories shifting to cloud deployment, the rising pace of outsourced drug discovery, and the expansion of precision-medicine biobanks that demand robust multi-omics data management. Cloud delivery already controls the largest revenue pool and is widening its lead because remote-access workflows have become standard in pharmaceutical R&D. Data-integrity mandates from regulators accelerate the replacement of legacy Laboratory Information Management Systems (LIMS) with modern platforms that embed compliance by design. Simultaneously, artificial-intelligence modules are being folded into informatics suites to shorten analysis cycles and surface predictive insights, especially in oncology and rare-disease research.

Key Report Takeaways

- By product, Laboratory Information Management Systems led with 48.6% of 2024 laboratory informatics market share, while Electronic Lab Notebooks are forecast to expand at a 12.5% CAGR to 2030.

- By component, services commanded 60.0% share of the 2024 laboratory informatics market size; software is the fastest mover, growing 11.2% annually through 2030.

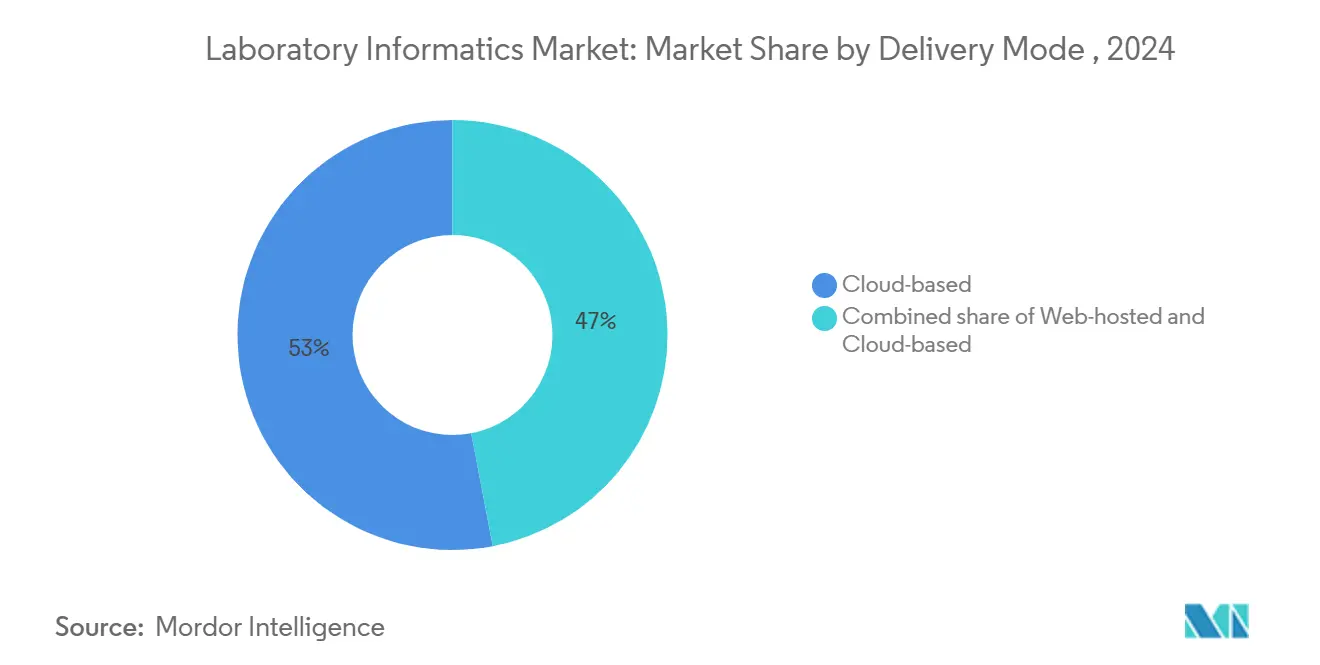

- By delivery mode, cloud solutions captured 53.0% of the laboratory informatics market in 2024 and are set to compound at 13.4% a year to 2030.

- By end user, pharmaceutical and biotechnology companies held 40.0% of 2024 revenue, whereas Contract Research Organizations are climbing fastest at a 12.8% CAGR.

- By geography, North America retained 43.0% of 2024 revenue; Asia Pacific is the highest-growth region, progressing at 9.0% a year between 2025-2030.

Global Laboratory Informatics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory-mandated data-integrity upgrades | +5% | North America | Short term (≤ 2 years) |

| CRO outsourcing boom to Asia | +4% | Asia Pacific | Medium term (2-4 years) |

| Precision-oncology biobank expansion | +3% | Europe | Long term (≥ 4 years) |

| AI-enabled analytics integration | +2% | Japan, South Korea | Medium term (2-4 years) |

| Remote & hybrid R&D policies accelerate web-hosted ELN uptake across global pharma labs | +2% | Global | Short term (≤ 2 years) |

| EU Green Deal Digital Product Passport pilots requiring SDMS for chemical traceability | +1% | Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Regulatory-Mandated Data Integrity Upgrades Driving LIMS Replacement Cycle

Legacy LIMS cannot satisfy today’s audit-trail, chain-of-custody, and electronic-signature requirements, propelling a wave of rip-and-replace projects across pharmaceutical and clinical laboratories in the United States and Canada. The U.S. Food and Drug Administration adopted Abbott’s STARLIMS across its testing sites, illustrating the regulatory preference for platforms that automate compliance workflows. Hospitals are following suit as infectious-disease reporting moves from manual logs to mandated electronic laboratory reporting that integrates with state surveillance networks[1]Ohio Department of Health, “Electronic Laboratory Reporting,” odh.ohio.gov. In practical terms, the upgrade cycle tightens vendor selection to systems with granular audit trails, validated instrument interfaces, and support for 21 CFR Part 11, pushing the laboratory informatics market toward higher annual maintenance revenue and longer multi-year support contracts.

Outsourcing Boom to Asian CROs Hikes Demand for Cloud-First Laboratory Informatics

Contract Research Organizations in China, India, and South-East Asia are winning a larger slice of early-stage drug development, lifting regional CRO revenue toward USD 46 billion in 2025. Sponsors demand real-time visibility into outsourced assays, forcing CROs to install cloud-architected LIMS that stream data to client portals. LabVantage expanded its professional-services footprint in Asia and South America by 80% between 2020-2023 to meet this need. Because cloud hosting sidesteps the capital outlay of on-premise data centers, smaller biotech firms can onboard CRO partners faster, contributing to sustained double-digit segment growth within the laboratory informatics market.

Precision-Oncology Biobank Expansion Necessitating High-Throughput Data Management

European research networks are building imaging-genomics repositories such as PRIMAGE and CHAIMELEON to refine cancer prognostics[2]Michela Gabelloni et al., “Bridging gaps between images and data: a systematic update on imaging biobanks,” European Radiology, procancer-i.eu. Handling multi-terabyte radiomics and whole-exome data requires laboratory informatics platforms that fuse biobanking, image archiving, and clinical data-warehouse functions. The Allegheny Health Network Cancer Institute’s Moonshot program showcases how multi-omics LIMS underpin predictive models linking tumor genotype with therapy response. As organoid and patient-derived xenograft workflows scale, throughput pressure escalates, reinforcing demand for elastic cloud storage paired with high-performance compute pipelines.

AI-Enabled Analytics Integration for Personalized-Medicine Workflows

Japanese and South Korean precision-health initiatives embed artificial-intelligence modules within laboratory informatics suites to accelerate biomarker discovery. Jefferson Lab demonstrates how deep-learning architectures interpret complex collider data, a blueprint being repurposed for high-dimensional omics analysis[3]Jefferson Lab, “Artificial Intelligence and Machine Learning,” jlab.org. ONCare Alliance partnered with Ovation.io in January 2025 to create a longitudinal multi-omics database combining electronic-medical-record data with serial blood biomarkers for cancer cohorts. Integrating AI directly into LIMS and Electronic Lab Notebooks (ELNs) shortens the feedback loop between data acquisition and insight generation, shifting the laboratory informatics market toward platforms with embedded machine-learning workbenches.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy instrument fragmentation | -2% | Latin America | Medium term (2-4 years) |

| GDPR-driven validation & cybersecurity costs | -3% | Europe | Short term (≤ 2 years) |

| Vendor lock-in concerns owing to proprietary data standards among public research institutes | -2% | Global | Medium term (2-4 years) |

| Skills gap in API scripting across LATAM food-safety labs impeding LES integration | -1% | Latin America | Medium term (2-4 years) |

Source: Mordor Intelligence

Legacy Instrument Fragmentation Hampers LIMS Integration in Latin America

Many Latin American laboratories rely on heterogeneous benchtop instruments acquired over decades, each running proprietary file formats and outdated firmware. The scarcity of local reagent suppliers and the elevated cost of importing consumables compound the challenge, as highlighted in Science’s 2024 coverage of the Reagent Collaboration Network[4]Rodrigo Pérez Ortega, “Scientists in Latin America struggle to get key chemicals,” Science, science.org. Although initiatives that teach labs to manufacture reagents locally reduce consumable costs, they do not solve the core integration problem. Consequently, new LIMS rollouts must include custom driver development and interface validation, raising project budgets and elongating timelines, which tempers the expansion pace of the laboratory informatics market in the region.

EU GDPR-Driven Validation & Cyber-Security Costs Limit Cloud-Migration Budgets

Europe’s General Data Protection Regulation raises data-hosting expenditures by roughly 20% and compute costs by 15% for life-science companies processing personal health data. Laboratory informatics vendors must embed encryption-at-rest, fine-grained role controls, and auditable access logs that comply with GDPR and national healthcare statutes. Validation documentation alone can lengthen cloud-migration projects by six months, effectively imposing a 25% cost premium on deployments. These added overheads persuade some mid-size European research centers to defer cloud adoption even when operational benefits are clear, cooling near-term uptake within the laboratory informatics market.

Segment Analysis

By Product: ELN Adoption Accelerates Digital Transformation

LIMS retained the lion’s share with 48.6% of 2024 revenue, yet ELNs are closing the gap, expanding at 12.5% a year. In revenue terms, ELNs contributed USD 1.17 billion in 2024, but their share of the laboratory informatics market size is projected to double by 2030. The rise stems from hybrid work models where scientists alternate between lab benches and remote data analysis sessions. Modern ELNs such as eLabNext embed real-time collaboration, tamper-evident audit trails, and drag-and-drop protocol builders. Integration with LIMS means experimental narratives automatically link to raw-data files and quality-control checkpoints, reinforcing data integrity and accelerating regulatory submissions. Over the forecast horizon, converged ELN-LIMS bundles will become the default architecture as organizations pursue single-vendor ecosystems that minimize validation overhead.

Combining ELN functionality with instrument-control modules improves compliance with GxP and 21 CFR Part 11, appealing to contract research labs courting pharmaceutical sponsors. LabWare’s embedded ELN within its LIMS platform permits guided execution of standardized test methods while capturing contextual data such as reagent lot numbers and calibration status. Because the laboratory informatics market share tied to LIMS is already high, growth among incumbent LIMS vendors will depend on cross-selling ELN and analytics add-ons. Meanwhile, pure-play ELN suppliers continue to differentiate through user-experience design and pre-built scientific templates that shorten onboarding time.

By Component: Services Dominance Reflects Implementation Complexity

Services generated 60.0% of 2024 revenue because most laboratories lack internal resources to map workflows, configure instrument interfaces, and validate systems under regulatory guidance. Accenture’s Scientific Informatics Services practice illustrates the breadth of demand, covering everything from requirements gathering to Quality Management System integration. Given the multiyear nature of transformation programs, service providers lock in annuity revenue through managed-service contracts that cover system maintenance, change control, and periodic re-validation.

However, software is catching up. The software slice of the laboratory informatics market is expanding at an 11.2% CAGR as vendors pivot to Software-as-a-Service packages that bundle hosting, updates, and basic support. LabVantage’s SaaS edition reduces infrastructure spend and enables click-to-deploy upgrades. Over time, automated interface libraries and low-code configuration tools will temper service revenues, but the need for specialized data-migration and validation skills ensures services remain the single largest component of the laboratory informatics industry through 2030.

By Delivery Mode: Cloud Solutions Dominate Growth Trajectory

Cloud deployment captured 53.0% of 2024 revenue, reflecting laboratories’ appetite for scalable infrastructure that supports globally distributed research teams. Cloud vendors emphasize SOC2, ISO 27001, and FedRAMP compliance to overcome security hesitations. Agilent’s OpenLab ECM XT offers end-to-end encryption, object-level versioning, and pay-as-you-grow storage. Because the CAGR for cloud delivery is 13.4%, the laboratory informatics market size attributable to cloud could surpass USD 4.5 billion by 2030.

On-premise deployments persist chiefly in nuclear, defense, and some European clinical settings where data-sovereignty rules impede external hosting. Hybrid models are gaining traction as labs combine local instrument capture with cloud analytics engines. LabWare’s cloud LIMS illustrates this pattern, offering browser-based access while allowing data buffering behind the firewall for instruments that lack reliable bandwidth. The pandemic-driven normalization of remote work entrenches cloud as the default procurement model, tilting vendor R&D budgets toward web-native interfaces and microservices architectures.

By End User: CROs Outpace Traditional Research Organizations

Pharmaceutical and biotechnology companies contributed 40% of 2024 revenue, but CROs form the fastest-growing constituency at a 12.8% CAGR. Small and mid-cap biotech firms lean on CRO partners for assay execution, genomic sequencing, and regulatory documentation, pushing CROs to invest in informatics stacks that provide transparent, audit-ready data flows. The Siemens-Thermo Fisher molecular-testing alliance bundles Thermo Fisher’s PCR instruments with workflow automation in Siemens’ kPCR solution, exemplifying how CROs can deliver turnkey testing pipelines.

Because CRO contracts often stipulate data-ownership clauses, vendors that offer flexible tenant models score higher in RFP evaluations. Unified platforms combining LIMS, ELN, and Scientific Data Management Systems (SDMS) lower integration friction and help CROs differentiate. The net effect is a widening revenue gap between digitally mature CROs and laggards, reinforcing double-digit expansion within this end-user slice of the laboratory informatics market.

Geography Analysis

North America contributed 43.0% of 2024 revenue, reflecting the confluence of stringent regulatory oversight and high R&D intensity. The U.S. Centers for Disease Control and Prevention embedded electronic-laboratory-reporting infrastructure long before the COVID-19 emergency, giving public-health labs a head start in rapid data exchange. Pharmaceutical majors based in the region routinely earmark digital-transformation budgets for AI-enabled data analytics, ensuring steady refresh cycles for informatics platforms. Federal grants for pandemic preparedness and antimicrobial-resistance surveillance further fuel demand, maintaining North America’s lead within the laboratory informatics market.

Asia Pacific is advancing at a 9.0% CAGR, the fastest worldwide. China and India dominate installation counts as domestic CROs scale capacity to service global sponsors. Governments are deploying national quality-infrastructure programs that subsidize laboratory automation and staff training, compressing adoption timelines. LabVantage’s decision to bolster its local implementation teams signals a pivot from export-led service models to in-region support structures, a move that lowers language and time-zone friction for clients. The absence of entrenched legacy systems in many new labs allows direct leapfrogging to cloud deployment, magnifying the growth momentum of the laboratory informatics market across Asia Pacific.

Europe balances advanced precision-medicine initiatives with strict data-protection regimes. Cancer-image biobanks and multi-omics repositories mandate platforms that seamlessly integrate imaging, genomic, and clinical data while safeguarding personal identifiers. Compliance with GDPR drives vendor investment in encryption, tokenization, and cross-border data-transfer controls. Although the regulatory overhead trims short-term budgets, national health services and Horizon funding streams are earmarking grants for digital-infrastructure upgrades, ensuring a solid mid-term pipeline for vendors servicing the European segment of the laboratory informatics market size.

Competitive Landscape

The laboratory informatics market features a moderate concentration, with the top five vendors controlling roughly 55.0% of 2024 revenue. Thermo Fisher Scientific stands out for breadth, spanning LIMS, chromatography data systems, and scientific-cloud storage. Its February 2025 acquisition of Solventum’s filtration business for USD 4.1 billion enhances upstream sample-prep capabilities that dovetail with Chromeleon CDS connectivity features. Abbott divested the STARLIMS suite to Francisco Partners, a move expected to inject dedicated R&D capital and accelerate product-road-map delivery.

Competition is shifting from point solutions to unified suites that combine LIMS, ELN, and SDMS under a single schema. Vendors such as Uncountable and Scispot emphasize low-code configuration and AI-driven workflow suggestions, appealing to fast-growing biotech startups that lack in-house IT staff. Traditional suppliers respond by publishing open-API libraries to entice third-party developers and foster ecosystem lock-in.

Strategic alliances complement acquisitions. Siemens Healthineers and Thermo Fisher combined molecular instruments with informatics readout modules to create end-to-end diagnostic workflows that shorten time-to-result for virology assays. These collaborations demonstrate how hardware vendors seek informatics partners to add analytical value, blurring boundaries between instrumentation and data-management suppliers and intensifying competitive dynamics inside the laboratory informatics market.

Global Laboratory Informatics Industry Leaders

-

Thermo Fisher Scientific Inc.

-

LabWare

-

Abbott (STARLIMS Corporation)

-

LabVantage Solutions Inc.

-

Agilent Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ONCare Alliance and Ovation.io formed a partnership to construct a multi-omics database for precision oncology, demonstrating how LIMS providers are aligning with clinical consortia to secure specimen-level data rights.

- November 2024: UL Solutions expanded laboratory capacity in Mexico to address regional testing demand, reflecting the pull effect that regulatory harmonization under USMCA exerts on informatics investments.

- March 2024: Precisio Biotix Therapeutics announced a Mayo Clinic collaboration on precision antibacterials, providing a case study of how high-throughput screening relies on fully integrated data pipelines.

- March 2024: Precisio Biotix Therapeutics acquired CC Bio, adding the ZEUS lysin platform, which illustrates how therapeutic-platform acquisitions often carry an informatics stack that must be swiftly harmonized post-deal to retain data continuity.

Global Laboratory Informatics Market Report Scope

As per the scope of this report, laboratory informatics is the specialized application of information with the help of a platform consisting of equipment, software, and data management tools that allow scientific data to be captured, migrated, processed, and interpreted for immediate use, as well as for future use.

The laboratory informatics market is segmented by product (laboratory information management system (LIMS), electronic lab notebooks (ELN), enterprise content management (ECM), laboratory execution system (LES), chromatography data system (CDS), scientific data management system (SDMS), and electronic data capture (EDC) & clinical data management system (CDMS)), by component (services and software), by delivery mode (On-premise, Web-hosted, and Cloud-based), by end user (pharmaceutical & biotechnology companies, contract research organizations (CROs), and other end users) and by geography (North America, Europe, Asia Pacific, South America, and Middle East & Africa). The report offers the value (in USD million) for the above segments.

| By Product | Laboratory Information Management System (LIMS) | ||

| Electronic Lab Notebooks (ELN) | |||

| Enterprise Content Management (ECM) | |||

| Laboratory Execution System (LES) | |||

| Chromatography Data System (CDS) | |||

| Scientific Data Management System (SDMS) | |||

| Electronic Data Capture (EDC) & Clinical Data Management System (CDMS) | |||

| By Component | Services | ||

| Software | |||

| By Delivery Mode | On-premise | ||

| Web-hosted | |||

| Cloud-based | |||

| By End User | Pharmaceutical & Biotechnology Companies | ||

| Contract Research Organizations (CROs) | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Laboratory Information Management System (LIMS) |

| Electronic Lab Notebooks (ELN) |

| Enterprise Content Management (ECM) |

| Laboratory Execution System (LES) |

| Chromatography Data System (CDS) |

| Scientific Data Management System (SDMS) |

| Electronic Data Capture (EDC) & Clinical Data Management System (CDMS) |

| Services |

| Software |

| On-premise |

| Web-hosted |

| Cloud-based |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organizations (CROs) |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the projected revenue of the laboratory informatics market by 2030?

The laboratory informatics market is forecast to reach USD 6.17 billion by 2030.

Which delivery model is growing fastest, and why?

Cloud deployment is expanding at a 13.4% CAGR because it supports remote access, lowers infrastructure costs, and simplifies global data-sharing.

How are regulatory requirements influencing purchasing decisions?

Data-integrity mandates from agencies such as the FDA compel laboratories to replace legacy LIMS with modern platforms that feature complete audit trails and electronic-signature controls.

Why are Contract Research Organizations investing heavily in informatics?

CROs need real-time data exchange with biotech sponsors; advanced LIMS and ELN systems provide transparent, audit-ready workflows that strengthen client partnerships.

What key restraint slows adoption in Europe?

GDPR compliance raises hosting and validation costs by up to 25%, delaying cloud migrations despite their operational advantages.

Which product segment is expected to grow most rapidly?

Electronic Lab Notebooks are set to rise at a 12.5% CAGR because they facilitate real-time collaboration and integrate seamlessly with modern LIMS platforms.