Laboratory Glassware Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

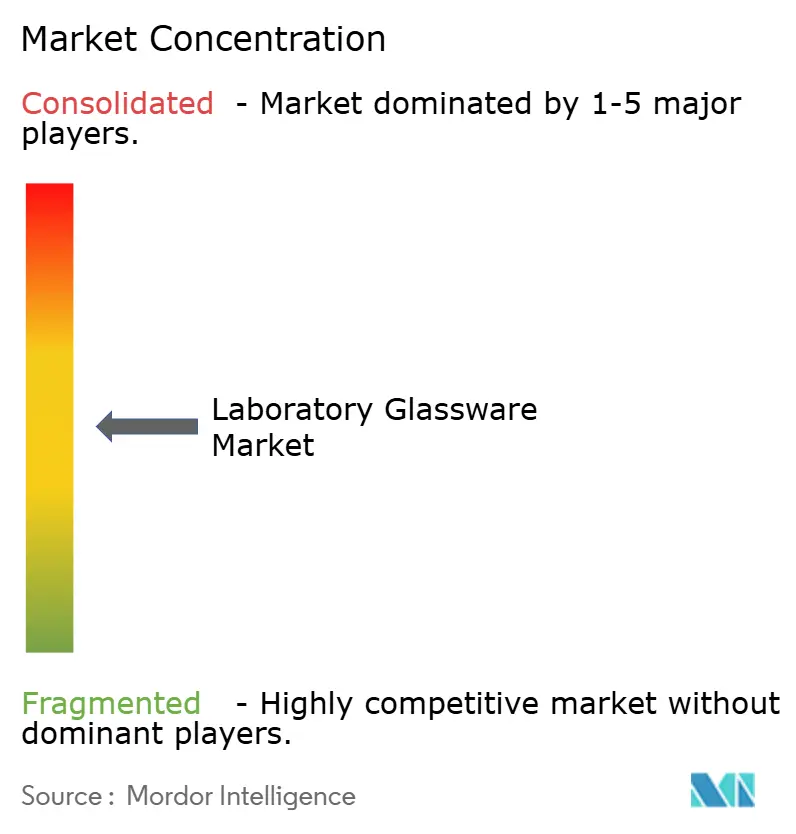

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Laboratory Glassware Market Analysis by Mordor Intelligence

The Laboratory Glassware Market size was valued at USD 2.72 billion in 2025 and is estimated to grow from USD 2.84 billion in 2026 to reach USD 3.56 billion by 2031, at a CAGR of 4.57% during the forecast period (2026-2031). Demand is increasing as serialized traceability, precision measurement requirements, and contamination control mandates converge across pharmaceutical, academic, and semiconductor laboratories. Regulatory alignment with United States Pharmacopeia (USP) 1058, European Union Good Manufacturing Practice (EU GMP) Annex 1, and national research and development (R&D) stimulus packages is extending replacement cycles for legacy soda-lime products while driving the adoption of borosilicate and quartz formats that can endure repetitive autoclave, thermal shock, and digital audit processes. Vendors integrating QR-coded batch records, wavelength dispersive X-ray fluorescence (WDXRF) elemental testing, and laser-etched calibration marks into their offerings are gaining market share as end users shift toward compliance-ready portfolios. The Asia-Pacific region leads in both absolute consumption and incremental growth, supported by China’s multi-trillion-yuan research budget and India’s expanding clinical trial activities. Additionally, sustainability metrics and Scope 3 reporting rules are emphasizing durability and life-cycle emissions in procurement evaluations, creating opportunities for premium reusable glassware.

Key Report Takeaways

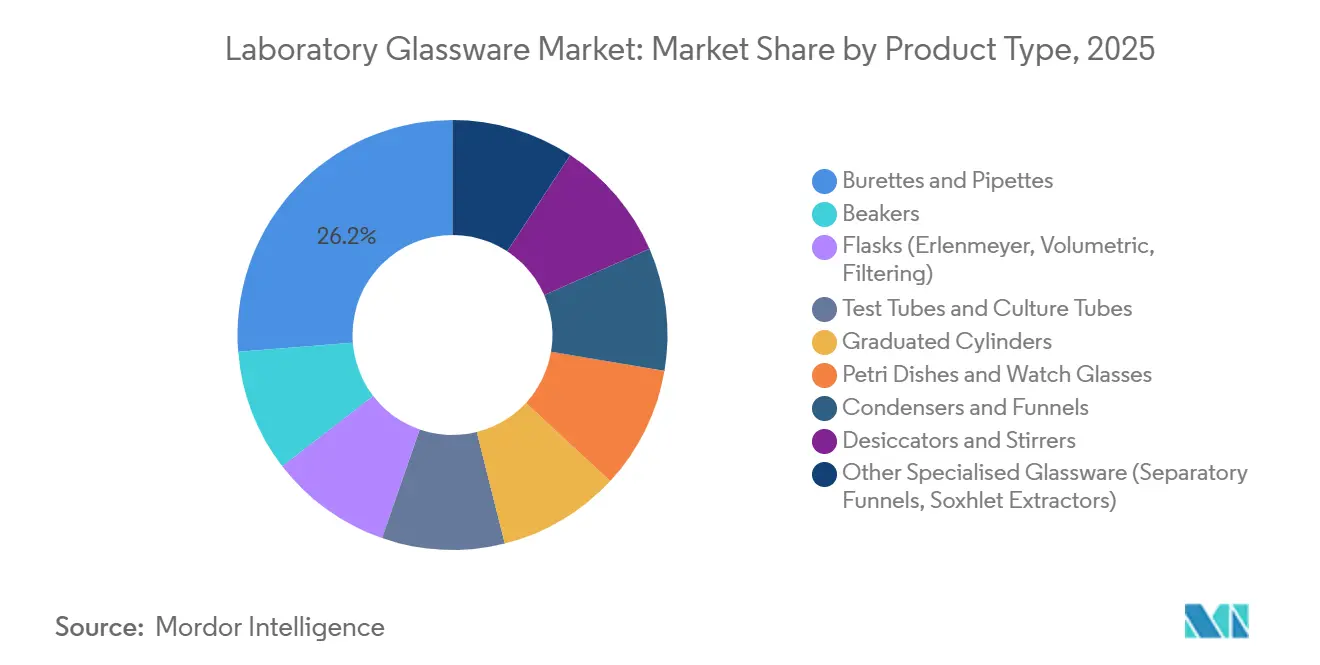

- By product type, burettes and pipettes led with 26.22% of the laboratory glassware market share in 2025 and are projected to advance at a 5.36% CAGR through 2031.

- By material type, borosilicate captured 65.24% revenue in 2025, whereas quartz is forecast to post the fastest 5.42% CAGR to 2031.

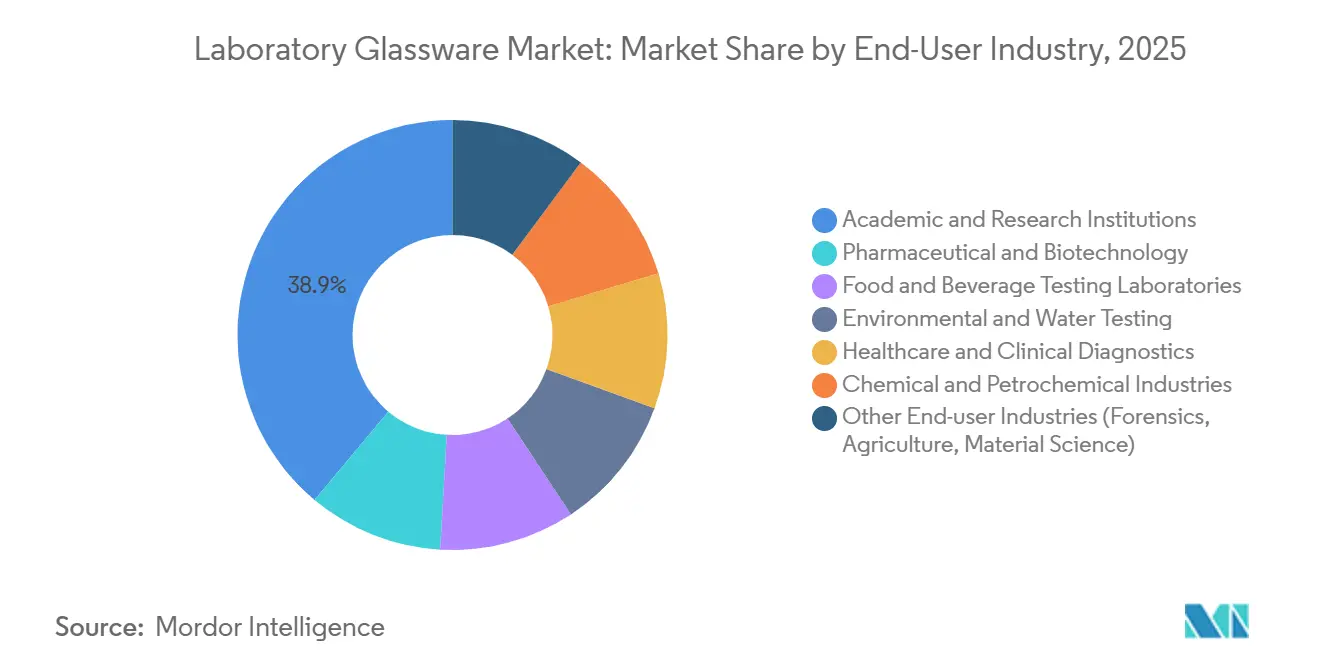

- By end-user industry, academic and research institutes accounted for 38.89% expenditure in 2025, but pharmaceutical and biotechnology laboratories hold the highest projected 5.88% CAGR over 2026-2031.

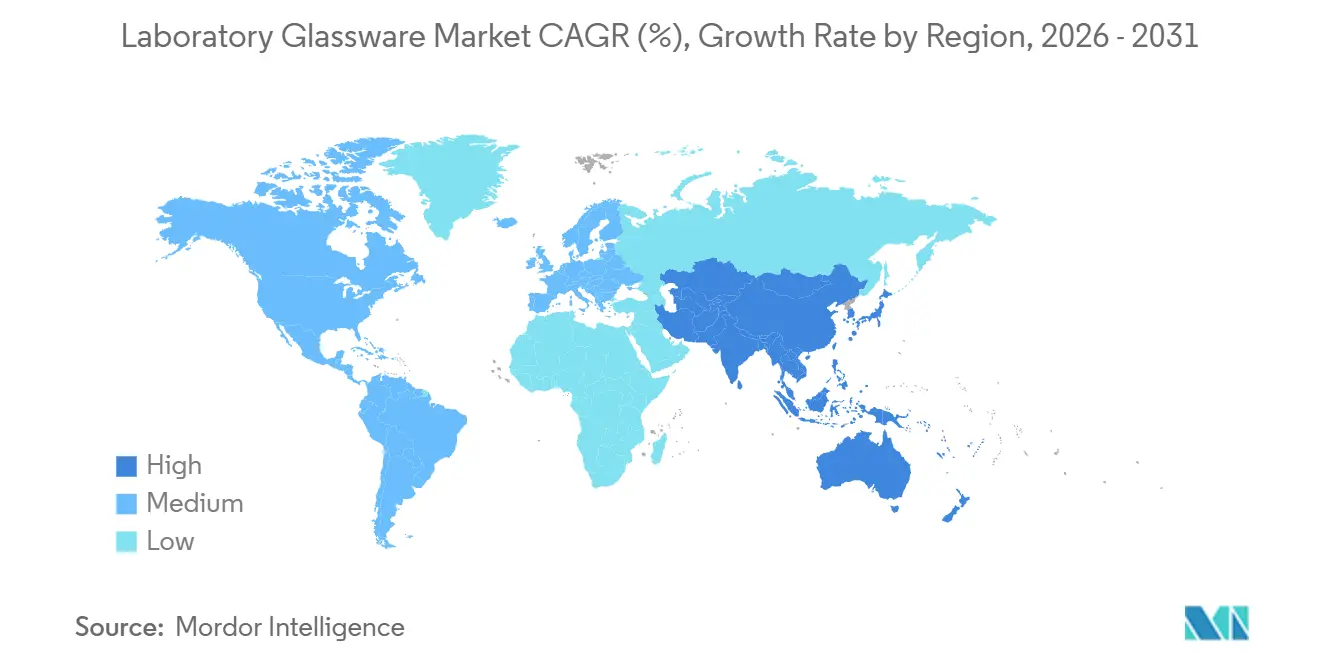

- By geography, Asia-Pacific secured 48.11% of 2025 spending and is on track for a 5.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory Glassware Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of academic and government research institutes | +1.2% | Global, with concentration in APAC (China, India) and Europe (Germany, UK, France) | Medium term (2-4 years) |

| Rising number of diagnostic and analytical laboratories | +1.0% | APAC core (India, ASEAN), spill-over to MEA and South America | Short term (≤ 2 years) |

| Shift toward precision-measurement, contamination-free labware | +0.9% | North America & EU pharmaceutical hubs, APAC semiconductor clusters | Medium term (2-4 years) |

| Stringent traceability rules (USP <1058>, EU GMP Annex 1) spurring serialized glassware demand | +1.1% | Global, led by North America and EU regulatory zones | Long term (≥ 4 years) |

| Microfluidics start-ups requiring ultra-thin custom glass chips | +0.5% | North America (Boston, San Francisco), EU (Cambridge, Munich), select APAC innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Academic and Government Research Institutes

Public-sector science funding is increasingly directed toward consumables essential for multi-omics, photonics, and quantum-sensing research. Ireland allocated EUR 100 million (USD 115.38 million) for photonics laboratories, emphasizing ultra-low-fluorescence quartz cuvettes. Concurrently, the United States National Science Foundation (NSF) set aside USD 160 million for biomanufacturing innovation engines, highlighting the need for serialized volumetric flasks compliant with National Institute of Standards and Technology (NIST) standards[1]National Science Foundation, “Regional Innovation Engines Awards,” NSF.GOV. China's CNY 3.9 trillion (USD 0.56 trillion) research budget requires provincial buyers to prioritize domestic borosilicate suppliers, driving capacity expansions in Jiangsu and Zhejiang. India's Department of Biotechnology is establishing 12 biotechnology clusters, centralizing bulk procurement of borosilicate and quartzware through unified tenders. These initiatives collectively extend the lifecycle of essential equipment and ensure consistent demand for premium glassware calibrated to meet United States Pharmacopeia (USP) 1058 standards.

Rising Number of Diagnostic and Analytical Laboratories

New reference laboratories across India and Southeast Asia are significantly increasing the demand for autoclavable borosilicate test tubes, capable of enduring 200 sterilization cycles. In response to 4,563 food-safety alerts from the Rapid Alert System for Food and Feed (RASFF) in 2024, European member states are enhancing their pesticide-analysis capabilities, leading to increased orders for borosilicate Erlenmeyer flasks and separatory funnels[2]European Food Safety Authority, “RASFF Food Safety Notifications 2024,” EFSA.EUROPA.EU. The Food Safety and Standards Authority of India (FSSAI) plans to expand India's accredited laboratory network to 400 sites by 2027 under International Organization for Standardization/International Electrotechnical Commission (ISO/IEC) 17025 standards, further amplifying the demand for volumetric ware. With clinical trials in India reaching 18,000 new protocols in 2024, there has been a significant increase in the consumption of culture tubes and pipettes, tripling their usage compared to standard diagnostics.

Shift Toward Precision-Measurement, Contamination-Free Labware

Pharmaceutical quality control (QC) teams are automating liquid handling, increasing the demand for tighter glass-tolerance specifications. Sartorius introduced a gravimetric pipette-calibration system capable of detecting sub-microliter drift, which has extended burette recertification intervals from six to eighteen months. In 2024, industry leaders Thermo Fisher, Eppendorf, and Gilson collectively shipped over 500,000 electronic pipettes, each equipped with borosilicate or quartz tips, known for their zero ion leaching in high-performance liquid chromatography (HPLC) solvents. The semiconductor industry's need for containers emitting less than 10 parts per billion (ppb) sodium led USP to incorporate aluminosilicate and high-purity quartz into its classification monograph. European Union (EU) regulations on water quality now mandate glass filtration funnels to prevent polymer contamination in microplastics assays, broadening the scope for precision-engineered glassware. Additionally, United States Environmental Protection Agency (EPA) guidelines under the Fifth Unregulated Contaminant Monitoring Rule (UCMR5) for per- and polyfluoroalkyl substances (PFAS) testing explicitly exclude soda-lime and lower-grade borosilicate options, reinforcing the industry's shift toward premium materials.

Stringent Traceability Rules Spurring Serialized Glassware Demand

USP 1058 has classified volumetric glassware as critical measurement infrastructure, requiring laboratories to maintain detailed records of autoclave cycles, cleaning agents, and calibration drifts. In alignment with these standards, EU Good Manufacturing Practice (GMP) Annex 1 mandates ready-to-use glass vials accompanied by batch-specific endotoxin certificates. This has led companies such as Gerresheimer and Corning to adopt automated serialization lines. Further supporting this trend, the United States Food and Drug Administration (FDA) guidance from July 2024 emphasizes the need for bridging studies when altering vial glass composition, effectively binding biologics producers to long-term borosilicate contracts. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) has harmonized its container standards with International Council for Harmonization of Technical Requirements for Pharmaceuticals for Human Use (ICH) Q3D, limiting extractable metals to thresholds achievable only with borosilicate Type I or quartz. However, smaller regional suppliers lacking digital traceability systems face challenges in competing for high-value tenders.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory limits on reusable glassware in clinical settings | -0.8% | North America, EU clinical diagnostics hubs | Short term (≤ 2 years) |

| Substitution threat from disposable/autoclavable plasticware | -0.6% | Global, with higher intensity in cost-sensitive APAC and South America markets | Medium term (2-4 years) |

| Rising insurance premiums linked to glass breakage losses | -0.3% | North America, EU, developed APAC markets (Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Limits on Reusable Glassware in Clinical Settings

Reusable glassware, despite its sustainability benefits, is being phased out in hospital laboratories due to the Occupational Safety and Health Administration’s (OSHA) Bloodborne Pathogens Standard and the Centers for Disease Control and Prevention (CDC) guidelines, which recommend single-use containers. BD’s Barricor tubes, an alternative to traditional glass serum-separator formats, reduce centrifugation times and eliminate the risk of glass-particle contamination. Cyclic-olefin-polymer hybrids are now widely used in hematology tubes, although research by Eppendorf indicates that recycled-plastic blends exceeding 20% fail United States Pharmacopeia (USP) 661 tests. Consequently, research laboratories continue to use borosilicate glass, while clinical settings increasingly adopt validated plastic solutions.

Substitution Threat from Disposable/Autoclavable Plasticware

Life-cycle assessments indicate that glass surpasses polypropylene in carbon dioxide (CO₂) emissions only after 40 reuse cycles. However, many laboratories in emerging markets face challenges in achieving this due to gaps in autoclave maintenance. The EcoLabWare tool suggests that in regions dependent on coal-based electricity or experiencing water scarcity, plasticware is a more sustainable option. Additionally, cost differences-up to 60% in favor of plastic make it a preferred choice for budget-conscious buyers, particularly in areas where import tariffs increase glass costs. In contrast, in the regulated pharmaceutical sector, the Food and Drug Administration (FDA) rules that discourage changes in vial materials support consistent demand for glass, providing a competitive advantage for premium glass suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Volumetric Precision Drives Burette and Pipette Leadership

Burettes and pipettes, commanding 26.22% of the 2025 laboratory glassware market share, are set to outpace their peers with a projected 5.36% CAGR through 2031. The rising demand for borosilicate tips is driven by electronic pipetting systems that feature on-demand calibration. In pharmaceutical quality control (QC) suites, flasks are preferred, especially with Annex 1's contamination-control clauses prioritizing ready-to-sterilize glass over soda-lime. While test tubes see steady use in microbiology and research teaching labs, their adoption in hospitals is limited by the increasing use of single-use alternatives. Mandates in food safety and environmental testing are increasing the throughput of sample preparation for graduated cylinders, condensers, and specialized Soxhlet apparatus. Across these categories, the adoption of QR-coded serial numbers and laser-etched volume marks is becoming standard, creating challenges for low-cost competitors.

As the forecast period progresses, burettes and pipettes are strengthening their leadership. This shift is supported by the transition of United States Pharmacopeia (USP)-compliant lifecycle records from traditional spreadsheets to laboratory information management system (LIMS) application programming interfaces (APIs). Vendors are leveraging this trend by bundling electronic pipette service contracts with serialized burettes to secure recurring revenue streams and increase switching costs. Standard items like beakers, watch glasses, and petri dishes typically follow a mature replacement cycle. However, there is demand for antistatic or low-autofluorescence variants, driven by workflows in semiconductors and cell imaging.

By Material Type: Quartz Gains Ground as Microfluidics and Semiconductor Labs Demand Ultra-Low Expansion

Borosilicate, with a 65.24% revenue share in 2025, owes its dominance to a favorable cost-performance ratio. However, quartz is charting a steeper growth trajectory with a 5.42% CAGR. This demand increase is driven by advancements in genomics fluorescence assays, research and development (R&D) in photonics, and stringent sub-parts per billion (ppb) metal contamination standards in semiconductor metrology. While Borosilicate 3.3 is essential for routine volumetric ware, surviving under 200 autoclave cycles without drift, soda-lime's thermal-expansion limits its use to teaching labs. Specialty aluminosilicate, on the other hand, finds its niche in high-energy radiation shielding.

Quartz's growing prominence is further supported by femtosecond-laser micromachining, streamlining the scale-up of microfluidic chips to over 10,000 units. As point-of-care diagnostics gain traction, vendors providing comprehensive supply chains for quartz wafers, bonding adhesives, and serialization are positioned for significant growth. The market for quartz-based laboratory glassware is set to double its 2025 figures by 2031, while borosilicate will grow in line with the market but lose some share.

By End-User Industry: Pharma and Biotech Outpace Academics as Biologics Investments Surge

In 2025, academic and research facilities accounted for 38.89% of spending, largely due to a significant installed base for routine replacements. However, pharmaceutical and biotechnology firms are on track to register the highest growth at a 5.88% CAGR. This growth is driven by major investments in biologics and cell-based therapies, with Novartis leading at USD 23 billion, followed by Eli Lilly at USD 11.5 billion, and substantial expansions from Roche and Genentech. In these facilities, serialized volumetric ware is essential for Food and Drug Administration (FDA) process validation, steering procurement towards comprehensive service suppliers. Under Rapid Alert System for Food and Feed (RASFF) pressure, food and beverage labs are expanding, and environmental agencies are turning to quartz funnels for monitoring per- and polyfluoroalkyl substances (PFAS) and microplastics. Clinical labs present a split: high-complexity reference centers still prefer borosilicate for trace-metal assays, but routine hospital testing is shifting towards single-use plastics.

Contract research organizations (CROs) in regions like India, Mexico, and Poland are emerging as key players, responding to demand spikes from global sponsors. Forecasts indicate a minimum 6% annual growth for the laboratory glassware market catering to CROs, supported by their flexible capacity and International Organization for Standardization/International Electrotechnical Commission (ISO/IEC) 17025 accreditation. Across all sectors, there is a noticeable shift towards premium options, driven by the increasing importance of traceability and sustainability, even in traditionally cost-sensitive regions.

Geography Analysis

Asia-Pacific, accounting for 48.11% of 2025 revenue, is projected to grow at a 5.67% compound annual growth rate (CAGR) through 2031. China's substantial research investments, combined with local sourcing mandates, are strengthening the domestic value chain for borosilicate ware. In India, growth in clinical trials and an expanding diagnostics network are driving demand for graduated cylinders and pipettes. Japan and South Korea are focusing on the premium market, exporting high-precision quartz cuvettes and microreactors designed for photonics and semiconductor laboratories. Meanwhile, Southeast Asia's efforts to comply with European Union (EU) food-export standards are increasing the demand for Soxhlet extractors and separatory funnels.

North America is leveraging stringent United States Pharmacopeia (USP) and Food and Drug Administration (FDA) regulations that emphasize serialized glassware. The United States is expected to introduce millions of volumetric flasks, primarily linked to biomanufacturing hubs in California, North Carolina, and Virginia. In Canada, clean-tech tax incentives are encouraging universities to invest in quartz photochemical reactors. Simultaneously, Mexico is benefiting from the near-shoring of analytical-testing centers catering to United States supply chains.

Europe's outlook is influenced by the enforcement of European Union Good Manufacturing Practice (EU GMP) Annex 1 and emerging climate-ledger reporting mandates. Germany, France, and the United Kingdom are allocating Horizon Europe funds into quantum-sensing and cell-therapy research, both of which require ultra-pure glass. Nordic countries, under the Water Framework Directive, are adopting quartz filtration assemblies for environmental monitoring. Meanwhile, Eastern Europe is gradually upgrading its quality systems, revealing a latent demand for International Organization for Standardization (ISO)-compliant borosilicate ware.

In South America, mid-single-digit growth is evident as Brazil expands its pharmaceutical fill-finish capabilities. Concurrently, Chile is investing in lithium battery research labs, specifically requiring borosilicate condensers for electrolyte testing. The Middle East and Africa are witnessing new orders driven by Saudi Arabia's Vision 2030 science parks and South Africa's water-quality monitoring initiatives, although a fragmented distribution network limits their full potential.

Competitive Landscape

The laboratory glassware market is moderately fragmented. Gerresheimer and Corning maintain comprehensive control, overseeing everything from sand sourcing to the delivery of sterilized vials, but they face the challenge of making significant investments in serialization Information Technology (IT). This is essential for compliance with the requirements of Annex 1 audit trails. Sartorius has partnered with Sanofi to integrate single-use bioreactors with QR-coded glass sensors, highlighting the increasing convergence of traditional glassware and bioprocess automation. Avantor's divestiture of Clinical Services for USD 650 million is a strategic decision aimed at reallocating resources toward high-margin serialized consumables, reflecting a shift in focus from lower-return logistics.

Patent filings have increased, particularly for laser-etched calibration marks designed to resist autoclave erosion and for Near Field Communication (NFC) tags embedded in batches that can directly upload data to Laboratory Information Management Systems (LIMS). In the Asia-Pacific (APAC) and Middle East and Africa (MEA) regions, Indian and Chinese manufacturers are leveraging cost-efficient borosilicate production and ISO/IEC 17025 certified testing laboratories to serve educational institutions. However, their inability to certify every lot using Wavelength Dispersive X-ray Fluorescence (WDXRF) technology limits their access to contracts with leading pharmaceutical companies. Sustainability considerations are becoming increasingly important in the industry. Suppliers that quantify cradle-to-grave carbon dioxide (CO₂) savings for reusable products are gaining an advantage in Requests for Proposals (RFPs), reducing the pricing competitiveness of generic imports.

Laboratory Glassware Industry Leaders

-

Corning Incorporated

-

DWK Life Sciences

-

Gerresheimer AG

-

Avantor, Inc.

-

Borosil Scientific Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gerresheimer has invested EUR 100 million (USD 115.38 million) to install an oxy-hybrid furnace at its Lohr facility. This initiative reduces natural gas consumption by 30% and increases the production capacity for serialized, ready-to-use vials that comply with Annex 1 contamination-control standards, aligning with the growing demand in the laboratory glassware market.

- October 2024: Avantor sold its Clinical Services business for USD 650 million, reallocating capital toward the production of serialized volumetric glassware, a key component in laboratory glassware, targeting the cell-and-gene-therapy segment. This strategic move aligns with the growing demand for precise and high-quality laboratory equipment in advanced therapeutic applications.

Global Laboratory Glassware Market Report Scope

Laboratory glassware refers to containers and instruments, often made from borosilicate glass, used in scientific laboratories for handling, mixing, heating, storing, and measuring chemicals. Designed for resistance to chemicals and thermal shock, common items include beakers, flasks, pipettes, and burettes.

The laboratory glassware market is segmented by product type, material type, end-user industry, and geography. By product type, the market is segmented into beakers, flasks (Erlenmeyer, volumetric, filtering), test tubes and culture tubes, burettes and pipettes, graduated cylinders, petri dishes and watch glasses, condensers and funnels, desiccators and stirrers, and other specialized glassware (separatory funnels, Soxhlet extractors). By material type, the market is segmented into borosilicate glass, quartz glass, soda-lime glass, and other speciality glass types. By end-user industry, the market is segmented into pharmaceutical and biotechnology, academic and research institutions, food and beverage testing laboratories, environmental and water testing, healthcare and clinical diagnostics, chemical and petrochemical industries, and other end-user industries (forensics, agriculture, material science). The report also covers the market size and forecasts for laboratory glassware in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Beakers |

| Flasks (Erlenmeyer, Volumetric, Filtering) |

| Test Tubes and Culture Tubes |

| Burettes and Pipettes |

| Graduated Cylinders |

| Petri Dishes and Watch Glasses |

| Condensers and Funnels |

| Desiccators and Stirrers |

| Other Specialised Glassware (Separatory Funnels, Soxhlet Extractors) |

| Borosilicate Glass |

| Quartz Glass |

| Soda-Lime Glass |

| Other Speciality Glass Types |

| Pharmaceutical and Biotechnology |

| Academic and Research Institutions |

| Food and Beverage Testing Laboratories |

| Environmental and Water Testing |

| Healthcare and Clinical Diagnostics |

| Chemical and Petrochemical Industries |

| Other End-user Industries (Forensics, Agriculture, Material Science) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Beakers | |

| Flasks (Erlenmeyer, Volumetric, Filtering) | ||

| Test Tubes and Culture Tubes | ||

| Burettes and Pipettes | ||

| Graduated Cylinders | ||

| Petri Dishes and Watch Glasses | ||

| Condensers and Funnels | ||

| Desiccators and Stirrers | ||

| Other Specialised Glassware (Separatory Funnels, Soxhlet Extractors) | ||

| By Material Type | Borosilicate Glass | |

| Quartz Glass | ||

| Soda-Lime Glass | ||

| Other Speciality Glass Types | ||

| By End-user Industry | Pharmaceutical and Biotechnology | |

| Academic and Research Institutions | ||

| Food and Beverage Testing Laboratories | ||

| Environmental and Water Testing | ||

| Healthcare and Clinical Diagnostics | ||

| Chemical and Petrochemical Industries | ||

| Other End-user Industries (Forensics, Agriculture, Material Science) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the laboratory glassware market expected to grow through 2031?

It is projected to expand at a 4.57% CAGR from 2026 to 2031, reaching USD 3.56 billion by the end of the period.

Which product category leads spending today?

Burettes and pipettes hold the top position with 26.22% 2025 share and remain the fastest-growing product group.

Why is Asia-Pacific the largest regional buyer?

China’s expansive Research and Development budget and India’s surge in clinical trials have created a sizable installed base that demands serialized, reusable glassware.

What drives quartz demand in the coming years?

Microfluidics, semiconductor analytics, and fluorescence-based genomics assays require ultra-pure substrates with near-zero thermal expansion.

How do new traceability rules affect procurement?

USP 1058 and EU GMP Annex 1 compel labs to buy glassware with QR-coded batch records and lifetime calibration histories, favoring suppliers that offer serialization.

Page last updated on: