Japan Plastic Packaging Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

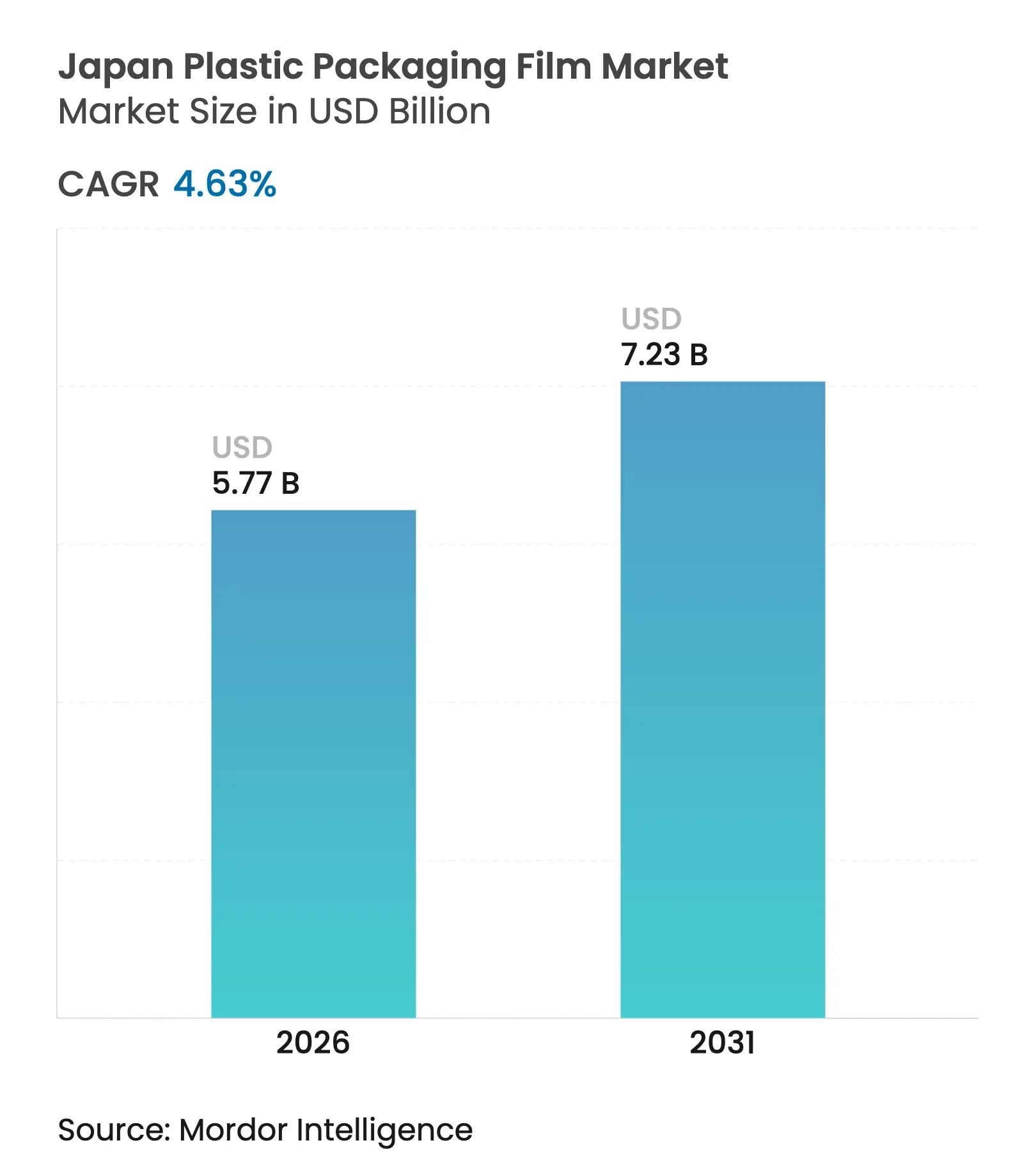

| Market Size (2026) | USD 5.77 Billion |

| Market Size (2031) | USD 7.23 Billion |

| Growth Rate (2026 - 2031) | 4.63 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Japan Plastic Packaging Film Market Analysis by Mordor Intelligence

Japan plastic packaging film market size in 2026 is estimated at USD 5.77 billion, growing from 2025 value of USD 5.51 billion with 2031 projections showing USD 7.23 billion, growing at 4.63% CAGR over 2026-2031. Demand accelerates as national recycling quotas, introduced under the 2024 Plastic Resource Circulation Act, push converters toward lighter, mono-material solutions. Pharmaceutical growth linked to a super-aging society is widening the application base for high-barrier and tamper-evident films, while food processors rely on ultra-thin gauges to curb rising resin costs. Producers are also capitalizing on government subsidies for chemical-recycling infrastructure that reward designs meeting closed-loop criteria. At the same time, export-oriented automotive and electronics suppliers specify protective films that maintain product integrity over long sea routes, underpinning steady industrial demand.

Key Report Takeaways

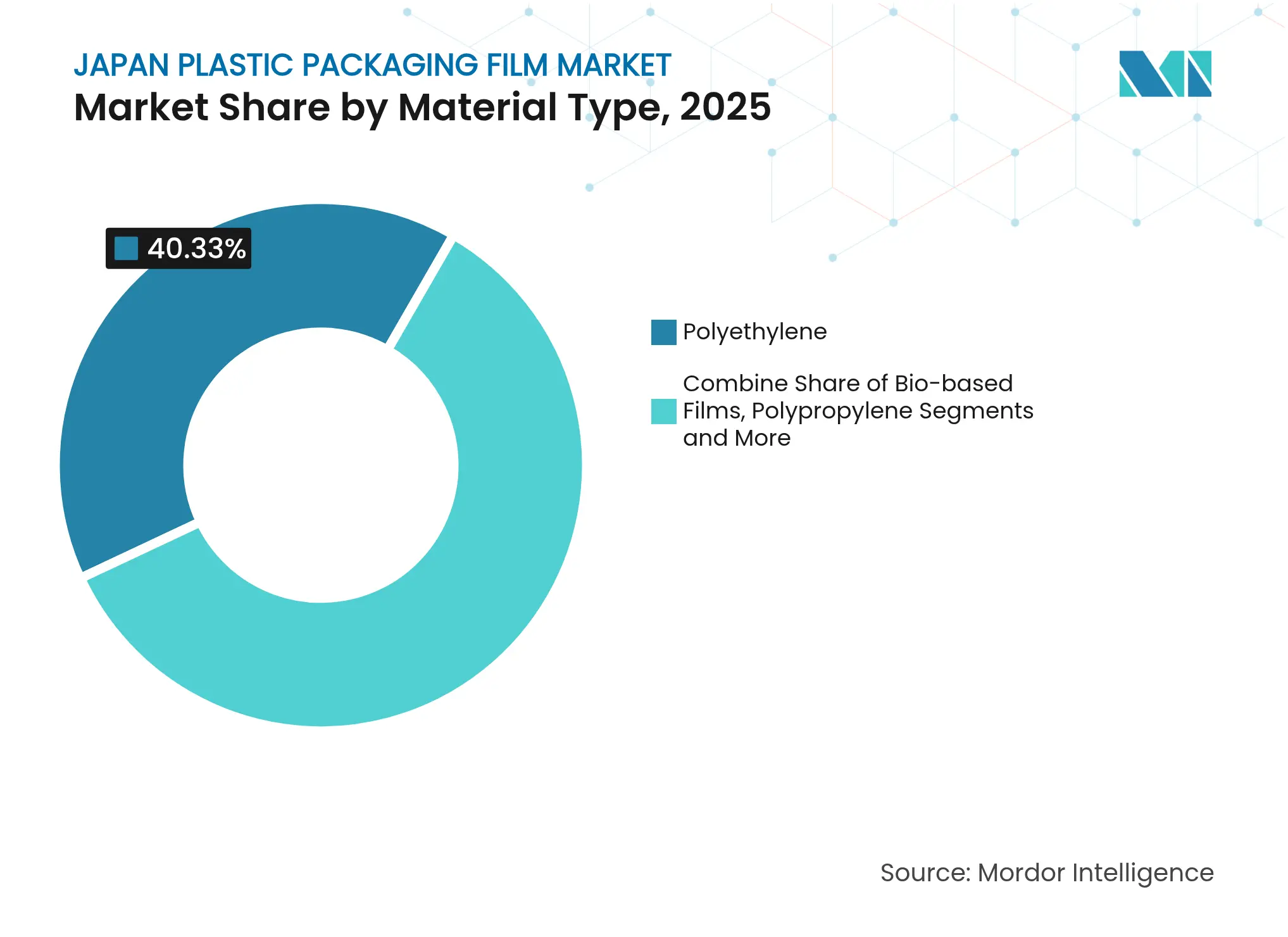

- By material type, polyethylene led with 40.33% of Japan plastic packaging film market share in 2025; bio-based films are poised for the fastest 8.78% CAGR to 2031.

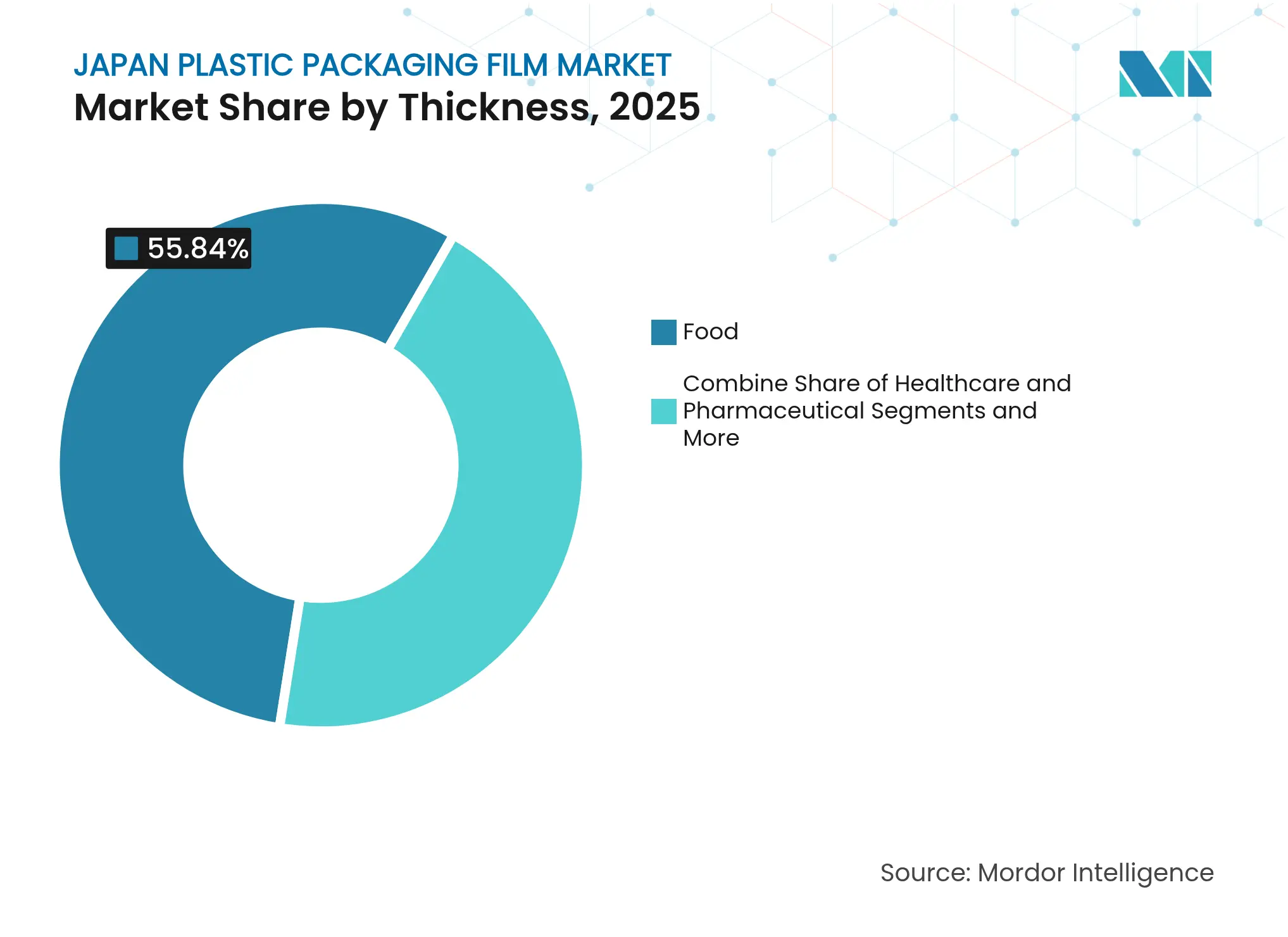

- By end-use industry, the food segment held 55.84% revenue share in 2025, while healthcare and pharmaceuticals are set to expand at an 7.86% CAGR through 2031.

- By thickness, 21-40 µm films commanded 44.10% of Japan plastic packaging film market size in 2025; ultra-thin films (≤20 µm) will climb at a 7.14% CAGR to 2031.

- By functionality, barrier films accounted for a 39.12% share of Japan plastic packaging film market size in 2025 and other functional films are growing at 8.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Plastic Packaging Film Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for lightweight and sustainable packaging across industries Rising demand for lightweight and sustainable packaging across industries | +1.2% | National, with concentration in Tokyo-Osaka industrial corridor | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:National, with concentration in Tokyo-Osaka industrial corridor | Impact Timeline:Medium term (2-4 years) |

Growth in processed food and ready-to-eat meal consumption Growth in processed food and ready-to-eat meal consumption | +0.8% | National, with higher penetration in urban centers | Short term (≤ 2 years) | |||

Pharmaceutical packaging demand due to ageing population Pharmaceutical packaging demand due to ageing population | +0.9% | National, with aging concentration in rural prefectures | Long term (≥ 4 years) | |||

Government subsidies for advanced recycling facilities driving adoption of recyclable mono-material films Government subsidies for advanced recycling facilities driving adoption of recyclable mono-material films | +0.7% | National, with priority in industrial zones | Medium term (2-4 years) | |||

Surge in e-commerce grocery cold-chain requiring high-barrier films Surge in e-commerce grocery cold-chain requiring high-barrier films | +0.6% | National, with urban logistics hubs leading adoption | Short term (≤ 2 years) | |||

Automotive export packaging shift to protective films Automotive export packaging shift to protective films | +0.4% | Regional, concentrated in automotive manufacturing clusters | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Lightweight and Sustainable Packaging Across Industries

Manufacturers are reallocating R&D budgets toward biomass-derived polyethylene and polypropylene after Tokyo signaled mandatory recycled-content targets for 2027. Dow-Mitsui Polychemicals commercialized ISCC PLUS-certified biomass LDPE in late 2024, showing that drop-in resins can satisfy toughness and sealability requirements without retooling lines. DNP’s mono-material PE laminate replaces traditional PET/PE composites, giving brands a route to claim 100% recyclability while meeting barrier specifications.[1]As resin taxes tighten, converters find that thinner gauges combined with plasma coatings deliver equal oxygen protection at 20% lower weight. The upshot is a Japan plastic packaging film market increasingly defined by lifecycle accounting rather than price per kilogram.

Growth in Processed Food and Ready-to-Eat Meal Consumption

Urban households continue to replace scratch cooking with chilled and retort pouches, lifting demand for high-barrier microwaveable films that lengthen shelf life to 18 months. Kansai-based co-packers now specify antifog shrink films so retailers can showcase freshly prepared meals without condensation. Price-sensitive brands adopt 25 µm OPP instead of 30 µm, trimming resin use by 17% while keeping dart impact strength constant. Government reforms allowing strategic food reserves heighten interest in transparent aluminum-oxide coatings, which cut both weight and permeation. These dynamics keep the Japan plastic packaging film market aligned with quick-turn production and cold-chain efficiency.

Pharmaceutical Packaging Demand Due to Ageing Population

Japan’s over-65 cohort surpassed 29% in 2025, lifting prescriptions filled outside hospitals and driving demand for child-resistant, senior-friendly blister webs. Kanae’s recyclable mono-material PTP sheet removes PVC while retaining push-through strength, helping pharmacies reduce landfill fees. Toppan’s GL BARRIER transparent film lowers aluminum usage by 40% and still achieves <0.1 cc/m²·day oxygen transmission, critical for biologics. Home-health delivery firms pair these packs with QR-coded labels that monitor ambient humidity, improving adherence. Such specialized needs reinforce premium-priced niches within the Japan plastic packaging film market.

Government Subsidies for Advanced Recycling Facilities

The NEDO Green Innovation Fund allocated JPY 11.8 billion to Resonac to commercialize mixed-plastic pyrolysis into ethylene, ensuring domestic supply of circular feedstock. Japan Environmental Association issued new eco-label criteria for chemical recycling output in April 2025, giving brands a recognized claim for “recycled in Japan” statements. Asahi Soft Drinks and nine partners launched a non-food PET-to-food-grade loop, underscoring the national pivot toward closed-loop design. These policy moves guide the Japan plastic packaging film market toward easier-to-sort mono-layers and trigger line upgrades that favor converters ready to certify traceability.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent government policies against plastic use Stringent government policies against plastic use | -0.8% | National, with stricter enforcement in metropolitan areas | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:National, with stricter enforcement in metropolitan areas | Impact Timeline:Short term (≤ 2 years) |

Volatile petrochemical raw-material prices Volatile petrochemical raw-material prices | -0.6% | National, with higher impact on import-dependent regions | Short term (≤ 2 years) | |||

Limited domestic recycling infrastructure for multilayer films Limited domestic recycling infrastructure for multilayer films | -0.4% | National, with rural areas facing greater challenges | Medium term (2-4 years) | |||

Competition from paper-based flexible packaging alternatives Competition from paper-based flexible packaging alternatives | -0.3% | National, with higher adoption in environmentally conscious segments | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Government Policies Against Plastic Use

The positive list for food-contact polymers, enforced from June 2025, limits converters to 21 approved resins and 827 additives, prompting costly reformulations. A proposed ban on 138 PFOA-related substances removes certain fluorinated barrier grades from multilayer laminates. Brand owners pay higher compliance fees under the updated Container and Packaging Recycling Act, as municipal PRO charges now cover 18% of local waste budgets.[2]OECD iLibrary, “The Packaging Recycling Act: Application of EPR to Packaging Policies in Japan,” oecd-ilibrary.orgSmaller firms risk margin compression while retrofitting extruders to handle certified resins. These hurdles temper near-term expansion in the Japan plastic packaging film market.

Volatile Petrochemical Raw-Material Prices

Japan imports nearly all naphtha feedstock, making domestic LDPE and LLDPE prices sway with Brent crude swings. Cosmo Energy’s plan to consolidate ethylene crackers in Chiba reflects structural overcapacity that could restrict spot supply during maintenance turnarounds. Meanwhile, Asahi Kasei’s pilot to synthesize ethylene from captured CO₂ and water shows promise but carries a cost premium until scale improves. The resulting price volatility encourages brand owners to hedge with thinner gauges or bio-resins, yet sudden spikes still squeeze EBITDA across the Japan plastic packaging film market.

Segment Analysis

By Material Type: Bio-based Films Accelerate While Polyethylene Retains Scale

The polyethylene segment accounted for 40.33% of Japan plastic packaging film, reflecting the resin’s versatility in food pouches, stretch wrap, and heavy-duty sacks. Polyethylene grades benefit from established supply, seal integrity and low-temperature toughness favored by frozen-food brands. LLDPE’s high elongation supports downgauging, letting converters hit <20 µm without sacrificing puncture resistance. Yet regulatory focus on fossil-carbon reduction nudges buyers toward emerging drop-in bio-PE streams certified under ISCC PLUS. Producers with in-house compounding lines adapt quickly, co-extruding bio-based layers with traditional resins to manage cost.

Bio-based films segment is set for 8.78% CAGR through 2031, outpacing every other resin group. Toray’s sugar-from-inedible-biomass program signals an end-to-end domestic value chain that may decouple pricing from crude oil. BOPP and CPP retain stronghold positions in snack and retort applications where optical clarity and heat-seal range matter. BOPET captures niche pharma and electronics packs needing dimensional stability. Scientists advancing ocean-degradable polyester derivatives hint at future carve-outs, yet commercial readiness remains post-2030. Together, these developments ensure the Japan plastic packaging film market continues balancing performance with environmental credentials.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Mature Food Demand Meets Rapid Healthcare Upswing

Food applications generated accounted for 55.84% of Japan plastic packaging film market share. Meat, seafood and ready-meal brands specify high-barrier coextrusions that lock in flavor over extended chill-chain routes. Convenience stores favor peelable lidding films that enable microwaving without puncturing, while confectioners rely on metallized BOPP for gloss and aroma retention. Price inflation in raw ingredients pushes processors toward thinner gauges paired with anti-fog coatings that preserve shelf appeal.

Healthcare and pharmaceuticals will grow at 7.86% CAGR as tablet, transdermal and specialty-injectable volumes climb. Child-resistant push-through webs meld PET and PP within a single recycle stream, meeting the 2025 positive-list mandate. Hospitals transitioning to home-care kits require moisture-proof secondary wraps that survive parcel deliveries. These trends weave a dual-track narrative in the Japan plastic packaging film market: the food category protects volume, while medical growth underpins margin expansion.

By Thickness: Mid-Gauge Films Dominate While Ultra-Thin Gauges Gain Pace

Films measuring 21-40 µm captured 44.10% of segment revenue in 2025, driven by their balance of puncture strength and cost for everyday pillow packs and stand-up pouches. Converters exploit multi-layer dies to embed EVOH or plasma coatings without thickening structure. The 41-70 µm class supports freezer bags and industrial liners, where tear resistance outweighs material savings.

Ultra-thin films no thicker than 20 µm should post 7.14% CAGR through 2031, lifted by resin-tax incentives and advances in torque-balanced blends. Polyplastics’ cellulose-fiber-reinforced PP demonstrates how bio-fillers restore stiffness lost to downgauging, slicing carbon footprint by 30%. As converters aim for <15 µm snack webs, tighter gauge-control systems become procurement criteria. The thickest category, above 70 µm, stays relevant for medical equipment wraps and electronics tray liners. Collectively, these shifts reveal a Japan plastic packaging film market using precision engineering to cut grams while safeguarding performance.

Note: Segment shares of all individual segments available upon report purchase

By Functionality: Barrier Films Anchor Value as Niche Functions Multiply

Barrier films accounted for 39.12% of Japan plastic packaging film market size, securing critical oxygen and water vapor resistance for chilled produce and biologics. Transparent oxide coatings let brands replace foil, aiding recyclability and metal-detector performance. Heat-shrink sleeves preserve tamper evidence across beverages, yet growth is modest as paper sleeves emerge.

Other functional films—anti-fog, anti-static, scratch-shield and UV-cut—will advance at 8.99% CAGR. KIMOTO’s direct-coated liquids can eliminate separate plastic overlays in electronics, foreshadowing material displacement. Auto exporters demand corrosion-inhibiting stretch wraps that protect components during trans-Pacific voyages. E-commerce grocery players specify breathable bags that vent CO₂ from cut produce while preventing dehydration. These specialized asks keep the Japan plastic packaging film market layered with high-margin micro-segments.

Geography Analysis

Japan’s plastic packaging film ecosystem clusters along the Tokyo-Osaka industrial belt, where integrated petrochemical, converting and printing facilities shorten lead times between resin production and end-use packing lines. Kansai processors collaborate with local food brands to beta-test ultra-thin retort webs, accelerating national roll-outs once performance targets are met. Central Honshu hosts automotive hubs that buy heavy-duty export wraps, anchoring demand for puncture-proof stretch hoods. Hokkaido, with strong dairy output, sources moisture-barrier bags tailored for chilled milk logistics.

Domestic island geography poses unique temperature swings that spur innovation in cold-chain packages. Nippon Express’ Protect BOX Thermal, proven to hold 5 °C for 72 hours without gel packs, depends on multi-layer inflation films with low thermal conductivity.Coastal prefectures leverage port access to re-export electronics sealed in static-dissipative PE, emphasizing salt-spray resistance. Rural regions face sparse recycling coverage, explaining higher adoption of mono-material PE pouches that fit existing mechanical-recycling streams.

Regulatory nuance also varies. Tokyo levies stricter disclosure on recycled-content percentages, nudging brand headquarters located there to champion PCR resins nationally. Meanwhile, Fukuoka subsidizes chemical-recycling pilot plants, attracting startups focused on depolymerization. These regional policies converge toward one outcome: a Japan plastic packaging film market that exports best-practice solutions once local validation is achieved.

Competitive Landscape

Market Concentration

The Japan plastic packaging film market is fragmented.Toray, Toppan and Futamura extend value chains into resin compounding, coating and printing, enabling turnkey offerings for brand owners seeking compliant mono-material structures. Each allocates 3–5% of sales to R&D, well above global averages, underpinning steady patent filings in barrier chemistry.

New entrants target niches ignored by incumbents. West One commercialized a two-year-compostable stretch wrap meeting EU EN 13432 requirements, positioning itself as a regulatory hedge for export shippers. Resonac leverages its pyrolysis investment to guarantee feedstock security for clients committing to recycled-content quotas. Strategic alliances mirror this collaborative landscape: DNP codesigns drop-in laminates with beverage groups, while Mitsui Chemicals pairs bio-based resins with converters that pledge ISCC chain-of-custody audits.

Pricing competition remains disciplined because performance claims need third-party verification under the 2025 positive-list regime. As a result, buyers judge offers on total compliance cost, supply stability and carbon-footprint metrics rather than resin price alone. This environment keeps innovation velocity high and cements the Japan plastic packaging film market as a bellwether for sustainable flexible-pack advances.

Japan Plastic Packaging Film Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: West One began domestic sales of GraDrop biodegradable stretch film that fully decomposes within two years, giving exporters a ready solution for stricter EU and ASEAN plastic-waste rules.

- January 2025: Resonac won JPY 11.8 billion from NEDO’s Green Innovation Fund to scale pyrolysis technology that converts mixed plastic waste into virgin-grade ethylene and propylene feedstocks for film production.

- September 2024: Dow-Mitsui Polychemicals began marketing ISCC PLUS-certified biomass EVA and LDPE, offering film converters drop-in resins that match conventional performance while lowering cradle-to-gate emissions.

- April 2024: Asahi Kasei, Mitsui Chemicals and Mitsubishi Chemical launched a joint feasibility study to decarbonize domestic ethylene crackers, aiming to supply low-carbon feedstock for next-generation packaging films by 2030.

Table of Contents for Japan Plastic Packaging Film Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising demand for lightweight and sustainable packaging across industries

- 4.2.2Growth in processed food and ready-to-eat meal consumption

- 4.2.3Pharmaceutical packaging demand due to ageing population

- 4.2.4Government subsidies for advanced recycling facilities driving adoption of recyclable mono-material films

- 4.2.5Surge in e-commerce grocery cold-chain requiring high-barrier films

- 4.2.6Automotive export packaging shift to protective films

- 4.3Market Restraints

- 4.3.1Stringent government policies against plastic use

- 4.3.2Volatile petrochemical raw-material prices

- 4.3.3Limited domestic recycling infrastructure for multilayer films

- 4.3.4Competition from paper-based flexible packaging alternatives

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Recycling and Sustainability Landscape

- 4.8Porter's Five Forces Analysis

- 4.8.1Bargaining Power of Buyers

- 4.8.2Bargaining Power of Suppliers

- 4.8.3Threat of Substitutes

- 4.8.4Threat of New Entrants

- 4.8.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material Type

- 5.1.1Polypropylene

- 5.1.1.1Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.2Cast Polypropylene (CPP)

- 5.1.2Polyethylene

- 5.1.2.1Low-Density Polyethylene (LDPE)

- 5.1.2.2Linear Low-Density Polyethylene (LLDPE)

- 5.1.2.3High-Density Polyethylene (HDPE)

- 5.1.3Biaxially Oriented PET (BOPET)

- 5.1.4Polystyrene

- 5.1.5Bio-based Films

- 5.1.6Other Material Type

- 5.2By End-Use Industry

- 5.2.1Food

- 5.2.1.1Candy and Confectionery

- 5.2.1.2Frozen Foods

- 5.2.1.3Fresh Produce

- 5.2.1.4Dairy Products

- 5.2.1.5Dry Foods

- 5.2.1.6Meat, Poultry and Seafood

- 5.2.1.7Pet Food

- 5.2.1.8Other Food Products

- 5.2.2Healthcare and Pharmaceutical

- 5.2.3Personal Care and Home Care

- 5.2.4Industrial Packaging

- 5.2.5Other End-use Industries

- 5.3By Thickness

- 5.3.1≤20 µm

- 5.3.221–40 µm

- 5.3.341–70 µm

- 5.3.4More than 70 µm

- 5.4By Functionality

- 5.4.1Barrier Films

- 5.4.2Heat-Shrink Films

- 5.4.3Twist-Wrap Films

- 5.4.4Anti-Fog and Anti-Static Films

- 5.4.5Other Functionality

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Toray Advanced Film Co., Ltd.

- 6.4.2Futamura Chemical Co., Ltd.

- 6.4.3Toppan Packaging Products Co., Ltd.

- 6.4.4Cosmo Films Limited

- 6.4.5Rengo Co., Ltd.

- 6.4.6Gunze Limited

- 6.4.7Unitika Ltd.

- 6.4.8Kingchuan Packaging

- 6.4.9KISCO Ltd.

- 6.4.10GSI Creos Corporation

- 6.4.11Toyobo Co., Ltd.

- 6.4.12Mitsui Chemicals Tohcello, Inc.

- 6.4.13Mitsubishi Chemical Corporation

- 6.4.14Dai Nippon Printing Co., Ltd.

- 6.4.15Takigawa Corporation

- 6.4.16Sumitomo Bakelite Co., Ltd.

- 6.4.17Sealed Air Japan

- 6.4.18Amcor Flexibles Japan

- 6.4.19Uflex Ltd.

- 6.4.20Showa Denko Packaging

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Material Type

- Polypropylene

- Biaxially Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Biaxially Oriented Polypropylene (BOPP)

- Polyethylene

- Low-Density Polyethylene (LDPE)

- Linear Low-Density Polyethylene (LLDPE)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Biaxially Oriented PET (BOPET)

- Polystyrene

- Bio-based Films

- Other Material Type

- Polypropylene

- By End-Use Industry

- Food

- Candy and Confectionery

- Frozen Foods

- Fresh Produce

- Dairy Products

- Dry Foods

- Meat, Poultry and Seafood

- Pet Food

- Other Food Products

- Candy and Confectionery

- Healthcare and Pharmaceutical

- Personal Care and Home Care

- Industrial Packaging

- Other End-use Industries

- Food

- By Thickness

- ≤20 µm

- 21–40 µm

- 41–70 µm

- More than 70 µm

- ≤20 µm

- By Functionality

- Barrier Films

- Heat-Shrink Films

- Twist-Wrap Films

- Anti-Fog and Anti-Static Films

- Other Functionality

- Barrier Films

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Japan Plastic Packaging Film Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 5.51 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 3.50 B (2024) | Regional Consultancy A | Bundles shrink-wrap with labels yet omits medical barrier films | ||

USD 6.70 B (2023) | Industry Journal B | Combines bio-based and non-plastic films; uses revenue-to-volume extrapolation | ||

USD 1.05 B (2025) | Global Consultancy C | Focuses on polypropylene only and relies solely on customs codes |