Thailand Plastic Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

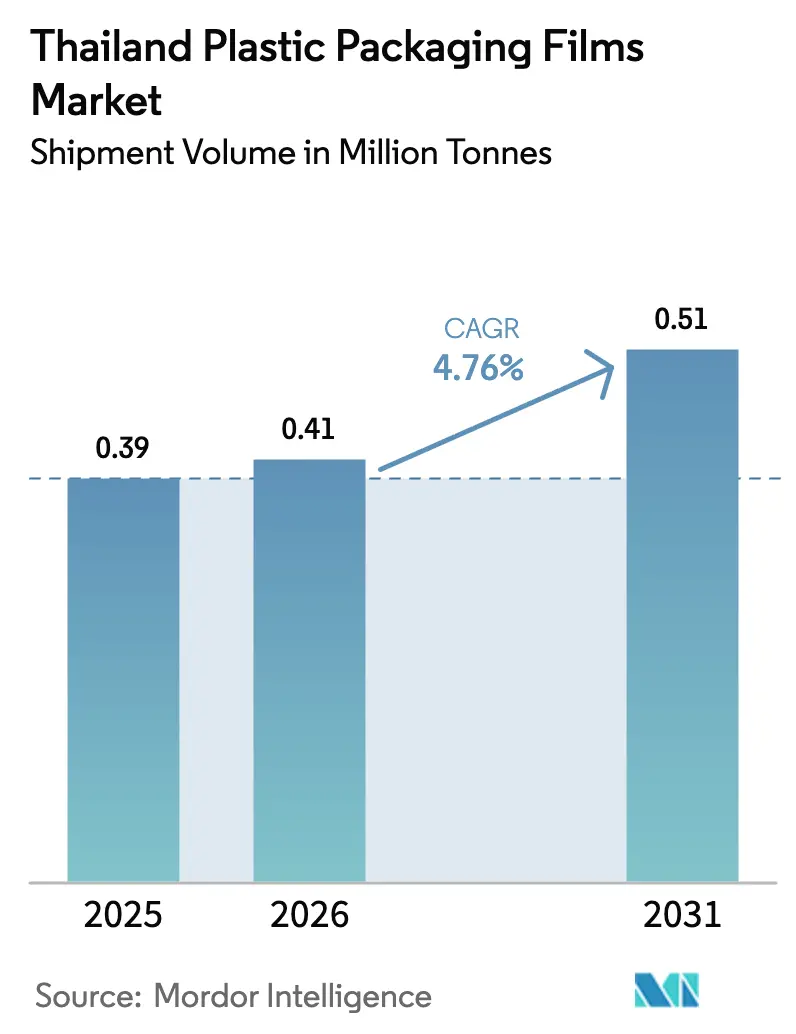

| Base Year Market Size (2025) | 0.39 Million tonnes |

| Market Volume (2026) | 0.41 Million tonnes |

| Market Volume (2031) | 0.51 Million tonnes |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Plastic Packaging Films Market Analysis by Mordor Intelligence

The Thailand plastic packaging films market size is projected to be 0.39 million tonnes in 2025, 0.41 million tonnes in 2026, and reach 0.51 million tonnes by 2031, growing at a CAGR of 4.76% from 2026 to 2031. Even with regulatory pressure and feedstock cost swings, converters continue to expand because Thailand is the largest packaging exporter in ASEAN, and plastics account for 78.2% of total packaging output. Growth rests on three structural pillars, entrenched polyethylene capacity that supplies low-barrier commodity films at competitive cost, rapid advances in bioplastic lines that address impending Extended Producer Responsibility (EPR) rules, and the country’s booming e-commerce sector that pivots retailers toward flexible secondary packs. Investment incentives under the Bio-Circular-Green Economic Model bolster margin-rich applications such as compostable mailers and antimicrobial pouches. Meanwhile, naphtha volatility compresses converters’ spreads, accelerating consolidation around vertically integrated groups with resin back-integration and precision extrusion technology.

Key Report Takeaways

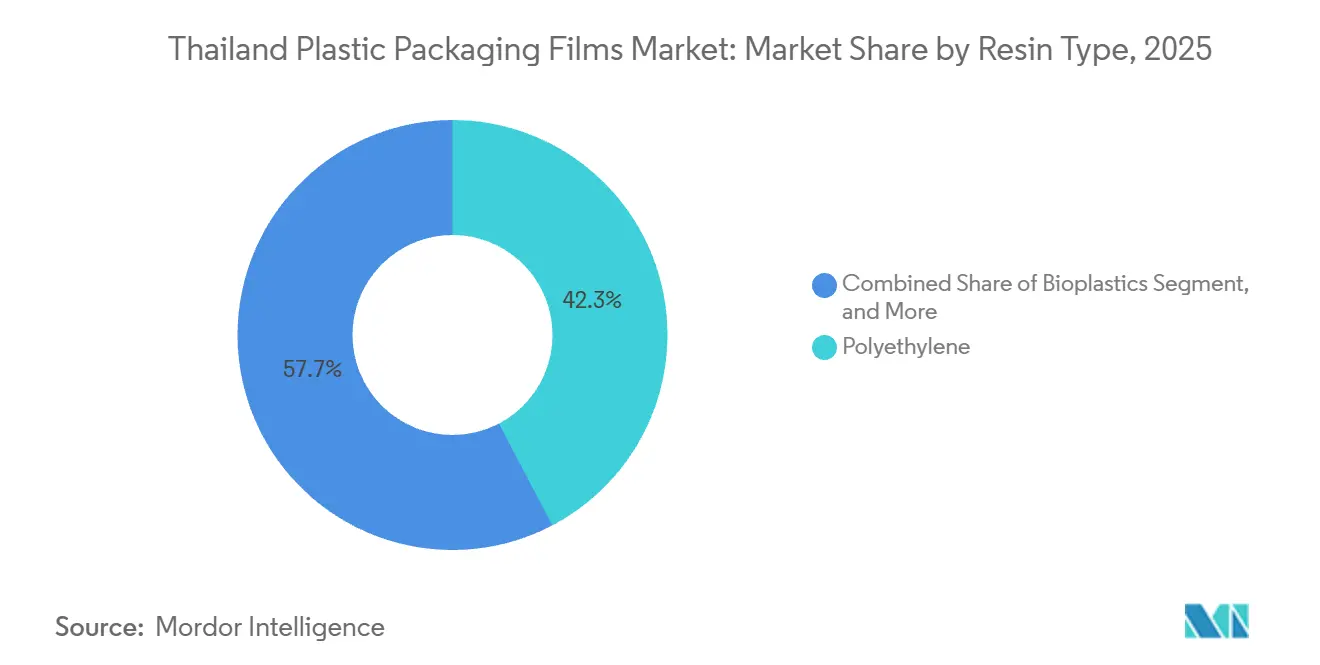

- By resin type, polyethylene commanded 42.31% of Thailand plastic packaging films market share in 2025 while bioplastics are forecast to post a 5.43% CAGR to 2031.

- By packaging format, pouches led with 48.54% of 2025 volume whereas wraps and overwraps are projected to expand at a 5.85% CAGR through 2031.

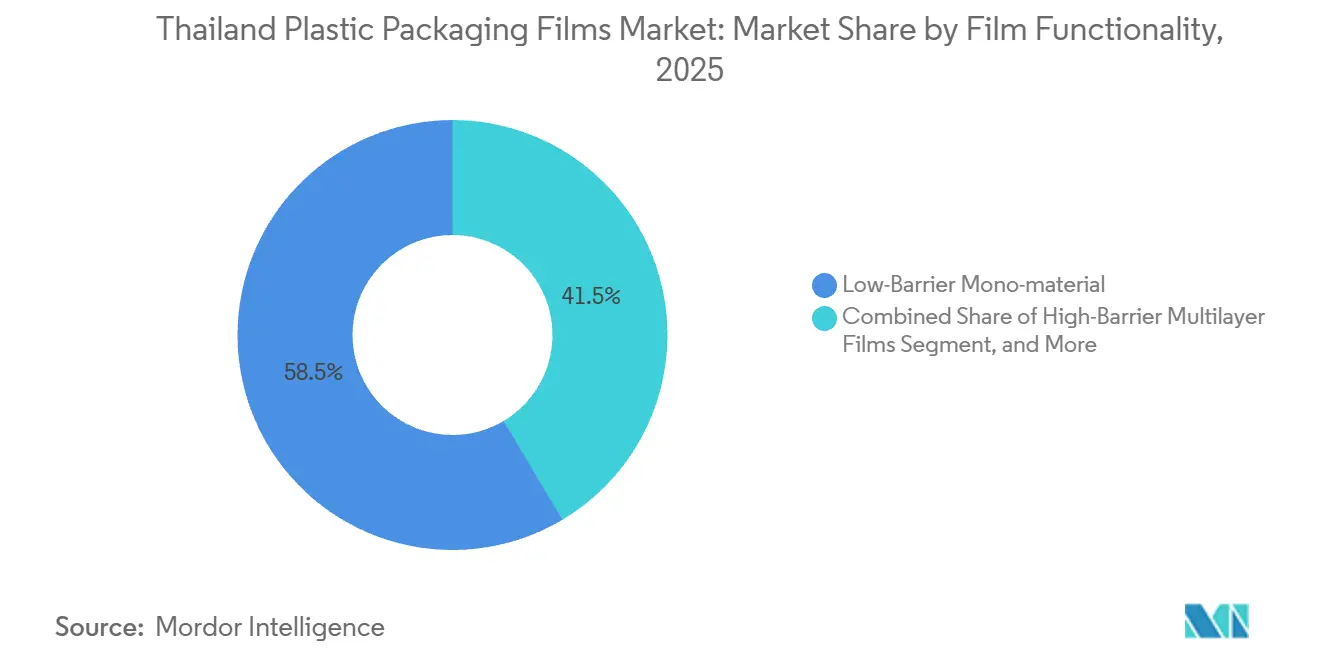

- By film functionality, low-barrier monomaterial structures held 58.54% share in 2025; high-barrier multilayer films will increase at a 5.12% CAGR to 2031.

- By end-use industry, food accounted for 32.43% of Thailand plastic packaging films market in 2025, yet healthcare and pharmaceutical packs are expected to grow fastest at a 6.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Plastic Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Lightweight Packaging Solutions | +0.8% | Bangkok, Samut Prakan, Rayong industrial zones | Medium term (2-4 years) |

| Surging Demand Across Diverse Consumer Goods Categories | +1.2% | Urban centers Bangkok, Chiang Mai, Phuket | Short term (≤ 2 years) |

| E-commerce Boom Accelerating Flexible Pack Adoption | +1.4% | Bangkok Metropolitan Region and provincial capitals | Short term (≤ 2 years) |

| Government-Backed Bio-Economy Roadmap Incentivising Bio-Based Films | +0.6% | Rayong and Chonburi under EEC initiative | Long term (≥ 4 years) |

| Quick-Service Restaurant Expansion Driving Portion-Pack Films | +0.3% | Bangkok, Pattaya, Chiang Mai, Hat Yai | Medium term (2-4 years) |

| Shift Toward Monomaterial Films for Circular Economy Compliance | +0.5% | Exporters serving EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight Packaging Solutions

Brand owners trimmed average pack weight 12% from 2022 to 2025 by swapping 80-micron multilayer laminates for 60-micron monomaterial PE that retains tensile strength through biaxial orientation and slip-additive chemistries.[1]SCG Packaging, “Technical Report 2024,” SCGPACKAGING.COM The change eliminated 4,800 tonnes of resin a year, easing EPR cost exposure while protecting shelf life for salty snacks and dry foods.[2]Pollution Control Department, “Plastic Waste Management Roadmap 2018-2030,” PCD.GO.TH Converters pumped THB 2.1 billion into precision extrusion lines capable of 40-micron cast polypropylene, generating coefficients of friction below 0.25, enabling 120-cycle-per-minute form-fill-seal runs for condiment sachets. Lightweight structures now occupy 38% of all flexible film output, up from 29% in 2020, as multinationals harmonize ASEAN specs for scale. Commodity film makers that cannot hold ±3% thickness tolerances face tightening margins and potential M&A as integrated peers dominate high-speed downgauging contracts.

Surging Demand Across Diverse Consumer Goods Categories

Thailand’s consumer goods turnover rose 6.8% in 2025, fueled by rising provincial incomes and a 14% jump in modern-trade stores, which now total 18,200 nationwide. Personal- and home-care pouches consumed 52,000 tonnes of flexible films in 2025, with refill packs for detergents and shampoos advancing 9.2% yearly as apartment dwellers favor space-saving packages. Pet food exports required 11,400 tonnes of high-barrier films, relying on oxygen permeability below 10 cc/m²-day to maintain kibble for 18 months. UHT milk pouches for school programs climbed 7.4% in 2025, specified with aluminum-foil/PE/EVOH laminates to keep milk shelf-stable for rural distribution. Confectionery twist-wrap OPP films hit 8,900 tonnes as Thailand shipped USD 1.2 billion of candy across ASEAN and the Middle East.

E-commerce Boom Accelerating Flexible Pack Adoption

Online GMV touched USD 21 billion in 2023, and every food-delivery order still needs a bag or pouch, pushing 18,600 tonnes of LDPE mailers and 6,700 tonnes of anti-fog produce films in 2025.[3]Electronic Transactions Development Agency, “E-commerce Report 2025,” ETDA.OR.TH E-tailers invested THB 840 million in algorithms that right-size packs, shaving 28% void fill and THB 340 million in film costs yearly. Cross-border e-commerce to Vietnam, Malaysia, and Singapore surged 31%, forcing converters to deliver compostable films that satisfy diverse landfill-diversion laws.

Government-Backed Bio-Economy Roadmap Incentivising Bio-Based Films

The 12th National Plan earmarked THB 15 billion for bioplastic infrastructure and set a 500,000-tonne capacity target by 2030. PTT Global Chemical’s 75,000-tonne PLA plant already supplies compostable resins for pouches and mailers and will lift output to 100,000 tonnes by 2027. Eight-year tax holidays lure converters that process cassava- and sugarcane-based feedstocks, pulling THB 6.2 billion of pledged capex in 2024. While bio-films held only 3.8% of 2025 volume, EU SUPD premiums of 15-20% entice exporters, and looming EPR rules mandating 30% recycled or bio content by 2028 will deepen local adoption once composting capacity expands beyond the current 14 industrial sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Government Regulations on Single-Use Plastics | -1.1% | Bangkok, Phuket, Chiang Mai tourist zones | Short term (≤ 2 years) |

| Volatile Feedstock (Naphtha) Prices Pressuring Margins | -0.9% | Nationwide | Short term (≤ 2 years) |

| Rising Adoption of Rigid Reusable Containers in Modern Trade | -0.4% | High modern-trade urban centers | Medium term (2-4 years) |

| Limited Post-Consumer Film Recycling Infrastructure | -0.3% | Provinces outside Bangkok Metropolitan Region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations on Single-Use Plastics

The Plastic Waste Management Roadmap outlawed Oxo-degradable films in 2021 and banned plastic waste imports in January 2025, removing 84,000 tonnes of low-cost feedstock for domestic recyclers. The draft EPR Act under Cabinet review will add roughly THB 2.40 per kilogram to brand owners’ costs, encouraging paper or reusable substitutes. Tourist provinces enacted stricter bans on plastic bags and straws, shifting 3,200 tonnes of film demand to higher-priced compostable options. Authorities levied THB 18.6 million in fines during 2025 crackdowns, pushing retailers toward certified monomaterial films for compliance.

Volatile Feedstock (Naphtha) Prices Pressuring Margins

Asian naphtha averaged USD 686 per tonne in Q1 2024, swinging 22% peak-to-trough, which cascaded through polyethylene and polypropylene pricing. HDPE fell from USD 1,029 to USD 946 per tonne over nine months, but converters locked into annuity contracts could not pass costs, slicing margins 8.1%. Twenty-two smaller converters shut in 2025 because they lacked hedging and working capital buffers. Forecasts for 2026 place HDPE between USD 850-950 per tonne, sustaining consolidation momentum as resin-integrated majors leverage cost immunity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyethylene Holds Sway as Bioplastics Accelerate

Polyethylene captured 42.31% of the Thailand plastic packaging films market in 2025, driven by LDPE stretch wraps and LLDPE stand-up pouches supplied through long-running extrusion assets clustered around Map Ta Phut. Biaxially oriented PET maintained 16.2% share, fed by Polyplex Thailand’s 42,000-tonne thin-gauge and 28,800-tonne thick-gauge lines. Polypropylene’s 22.8% slice reflects cast and BOPP expansions that target confectionery overwraps growing in double digits. Bioplastics, although only 3.8% of 2025 tonnage, will grow at a 5.43% CAGR on EPR quotas and EU export demand, flattening the cost gap as PLA capacity scales locally. Other high-barrier polymers such as EVOH and polyamide filled 14.6% of demand for seafood and pharma packs.

Rising sustainability premiums allow converters to extract healthy margins on bio-films while maintaining volume dominance in cost-effective PE. Strategic tie-ups with resin majors support agile grade switching during naphtha turbulence. To defend share against bio-polymers, PE suppliers roll out mono-PE structures with functional coatings that meet recyclability and barrier thresholds.

By Packaging Format: Wraps Surge Ahead of Pouches in Growth Stakes

Pouches retained top billing with 48.54% volume share in 2025 because form-fill-seal automation, spouts, and zippers cater to space-constrained households and export pet food. Yet wraps and overwraps will log the fastest 5.85% CAGR as e-commerce hubs escalate stretch-film and shrink-bundle consumption. Bags and linings at 32.7% now face bag-ban headwinds, but courier mailer demand partially offsets declines. A tail of wicketed bags, zipper formats, and vacuum-skin packs round out 18.8% of output.

Inventory buffers for e-commerce fulfillment centers drive larger production runs of blown LDPE, while pouch converters pivot toward high-barrier laminates for seafood and powdered beverages. As logistics operators push automated stretch-film systems that pre-stretch 250%, wrap makers embed metallocene resins to cut gauge without sacrificing pallet stabilization.

By Film Functionality: Monomaterial Trend Reshapes Barrier Economics

Low-barrier monomaterial designs accounted for 58.54% of the market in 2025, thanks to favorable recyclability narratives. High-barrier multilayers will, however, chalk up a 5.12% CAGR as seafood exporters must achieve oxygen rates below 5 cc/m²-day and pharma clients demand sub-0.5 g/m²-day moisture. Metallized films serve snack and coffee packs at 18.3% share, while active and antimicrobial variants, just 3.9% of tonnage, expand 6.8% annually on cold-chain rollout.

Policy shifts toward circularity push converters to combine mono-PE substrates with functional coatings and nano-clay fillers that meet EU and Japanese recyclability tests. Nevertheless, ultra-low oxygen specifications for tuna and sterile pharma packs still rely on EVOH or polyamide layers, anchoring multilayer growth and supporting specialized co-extrusion investments.

By End-Use Industry: Healthcare Races Ahead of Food

Food kept the lion’s share at 32.43% in 2025, spanning anti-fog produce films, high-barrier frozen shrimp pouches, and retail candy wraps. Healthcare and pharma volumes will rise the quickest at 6.03% CAGR, propelled by the EEC medical-hub strategy that boosts blister foil and sterile pouch demand. Beverage packs absorbed 14.6%, riding RTD coffee and milk growth. Personal- and home-care accounted for 19.8%, energized by pouch refills that slice unit price points. Industrial uses, chiefly stretch wrap and valve sacks, contributed 12.4% and tie into large public-works spending. Electronics, agriculture, and construction films made up the residual 20.8%.

Converter accreditation under ISO 15378 gives early movers an edge in high-value healthcare contracts, while food brands lean on recyclable mono-PE to satisfy export buyers. A diversified end-use mix shields the Thailand plastic packaging films market from single-sector downturns, but also raises technical demands across oxygen, moisture, and static-dissipative requirements.

Geography Analysis

Thailand’s Eastern Seaboard industrial belt houses 68% of flexible-film capacity, leveraging seamless resin supply from Map Ta Phut crackers and deep-sea export terminals. The Bangkok Metropolitan Region remains the single biggest demand node, accounting for 42% of consumption through dense modern-trade networks and 840 million e-commerce orders in 2025. The EEC has drawn THB 8.4 billion in film investments since 2022, largely for cleanroom conversion that serves medical-device and electronics exporters.

Southern provinces such as Songkhla, Phuket, and Surat Thani consumed 18.6% of output by feeding frozen-seafood processors that ship 620,000 tonnes abroad annually and require ultra-barrier laminates. The north around Chiang Mai and Lamphun took 12.4% as HDD and integrated-circuit clusters specify ESD films and moisture pouches. Government tax discounts for provinces beyond the main corridors lured THB 2.1 billion into facilities in Nakhon Ratchasima and Khon Kaen from 2023-2025.

Exports form a vital pressure valve, 22% of film shipments in 2025 crossed ASEAN borders, with Vietnam, Myanmar, and Cambodia together absorbing two-thirds. Zero tariffs under ATIGA spur scale, yet diverging plastic-waste laws force converters to juggle conventional and compostable SKUs for each destination.

Competitive Landscape

The market is reflecting moderate fragmentation. SCG Packaging led with THB 155.8 billion in 2024 sales and vertically integrates 40% of its resin needs, shielding it from naphtha swings. Polyplex Thailand leverages 106,050 tonnes of PET resin to feed 70,850 tonnes of BOPET film, securing 15-18% cost advantages and commanding premium metallized slots. The emerging space lies in ISO 15378-certified pharma films, where only four local converters can deliver moisture-barrier cold-form laminates, resulting in 8-12-month order backlogs.

Bioplastic expansion is the strategic battleground. PTT Global Chemical’s USD 150 million Rayong plant positions Thailand as ASEAN’s leading PLA supplier, yet pouch seal-strength hurdles remain. Global majors Amcor, Sealed Air, and Mondi each run Thai hubs that pioneer mono-PE with nano-clay barriers, hitting OTR below 50 cc/m²-day, trimming EVOH multilayer use by snack brands. Start-ups backed by the National Innovation Agency push antimicrobial films that cut food waste for premium retailers.

BOI tax breaks for lines using 30% recycled content are luring Japanese and Korean groups, promising 18,000 tonnes of value-added capacity by 2027. Competitive intensity is therefore highest in high-barrier and sustainable niches, while commodity LDPE sees exits by under-capitalized players. Consolidation looks set to continue as feedstock volatility favors resin-integrated and R&D-strong companies.

Thailand Plastic Packaging Films Industry Leaders

Amcor plc

Sealed Air Corporation

Huhtamäki Oyj

Mondi Group

Thai Future Incorporation Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Polyplex Thailand will commission a 6,000-tonne blown-film line targeting high-clarity produce packs, raising group capacity to 76,850 tonnes per year.

- November 2025: SCG Packaging partnered with a European technology firm to pilot recyclable mono-PE films featuring nano-clay oxygen barriers below 50 cc/m²-day.

- October 2025: PTT Global Chemical announced plans to expand its PLA facility from 75,000 to 100,000 tonnes annually by 2027.

- September 2025: The BOI approved three multilayer film projects worth THB 4.2 billion that must incorporate 30% recycled resin.

Thailand Plastic Packaging Films Market Report Scope

Plastic films are versatile, serving to wrap products, overwrap various packaging types (from individual packs to palletized loads), sachets, bags, and pouches, and are often part of laminates, where they are combined with other plastics and materials for packaging. The report also delves into the demand for these converted packaging films, analyzing them across essential resin and application categories. This broad scope mirrors the diverse needs of the market and the shifting preferences of consumers and businesses.

The Thailand Plastic Packaging Films Market Report is Segmented by Resin Type (Polypropylene, Polyethylene, Polyethylene-terephthalate, Polystyrene, Bioplastics, and Other Resin Types), Packaging Format (Wraps and Overwraps, Bags and Linings, Pouches, and Other Packaging Formats), Film Functionality (Low-Barrier Mono-material Films, Medium-Barrier Metallised Films, High-Barrier Multilayer Films, and Specialty Active and Antimicrobial Films), End-use Industry (Food, Beverages, Healthcare and Pharmaceutical, Personal Care and Home Care, Industrial Packaging, and Other End-use Industries). The Market Forecasts are Provided in Terms of Volume (Million Tonnes).

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyethylene-terephthalate (BOPET) |

| Polystyrene |

| Bioplastics |

| Other Resin Types |

| Wraps and Overwraps |

| Bags and Linings |

| Pouches |

| Other Packaging Formats |

| Low-Barrier Mono-material Films |

| Medium-Barrier Metallized Films |

| High-Barrier Multilayer Films |

| Specialty Active and Antimicrobial Films |

| Food | Candy and Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Meat, Poultry and Seafood | |

| Pet Food | |

| Other Food Products | |

| Beverages | |

| Healthcare and Pharmaceutical | |

| Personal Care and Home Care | |

| Industrial Packaging | |

| Other End-use Industries |

| By Resin Type | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Polyethylene-terephthalate (BOPET) | ||

| Polystyrene | ||

| Bioplastics | ||

| Other Resin Types | ||

| By Packaging Format | Wraps and Overwraps | |

| Bags and Linings | ||

| Pouches | ||

| Other Packaging Formats | ||

| By Film Functionality | Low-Barrier Mono-material Films | |

| Medium-Barrier Metallized Films | ||

| High-Barrier Multilayer Films | ||

| Specialty Active and Antimicrobial Films | ||

| By End-use Industry | Food | Candy and Confectionery |

| Frozen Foods | ||

| Fresh Produce | ||

| Dairy Products | ||

| Meat, Poultry and Seafood | ||

| Pet Food | ||

| Other Food Products | ||

| Beverages | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Home Care | ||

| Industrial Packaging | ||

| Other End-use Industries | ||

Key Questions Answered in the Report

How large is the Thailand plastic packaging films market in 2026?

It reached 0.41 million tonnes in 2026 and is set to hit 0.51 million tonnes by 2031.

Which resin dominates flexible film usage in Thailand?

Polyethylene leads with 42.31% share in 2025, backed by mature extrusion assets and competitive pricing.

What is driving growth in bioplastic films?

Eight-year BOI tax holidays and export premiums tied to EU single-use rules push bioplastics toward a 5.43% CAGR through 2031.

Why are wraps and overwraps growing faster than pouches?

E-commerce logistics need tamper-evident bundling and pallet stabilization, propelling wraps at a 5.85% CAGR.

How will EPR legislation affect film producers?

From 2028, packs must contain 30% recycled or bio-based content, favoring converters with mechanical recycling or PLA capacity.

Which end-use sector is expanding the fastest?

Healthcare and pharmaceutical packaging is forecast to rise at a 6.03% CAGR as Thailand positions itself as a regional medical hub.

Page last updated on: