Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

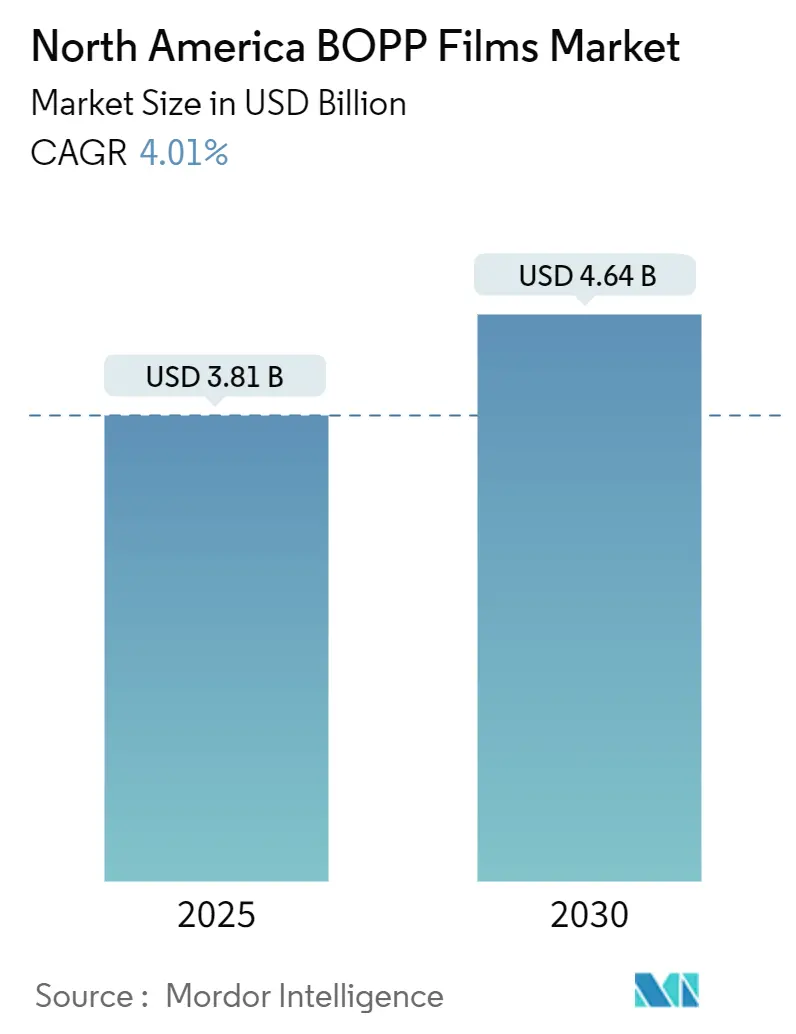

| Market Size (2025) | USD 3.81 Billion |

| Market Size (2030) | USD 4.64 Billion |

| Growth Rate (2025 - 2030) | 4.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America BOPP Films Market Analysis by Mordor Intelligence

The North America BOPP films market size stands at USD 3.81 billion in 2025 and is on course to reach USD 4.64 billion by 2030, translating into a 4.01% CAGR over the period. Robust e-commerce logistics, brand-owner commitments to recycle-ready mono-material laminates, and nearshoring of flexible-packaging operations into Mexico are reshaping demand in favor of higher-value grades while simultaneously expanding overall volumes. Rapid investments in wider tenter lines and hybrid BOPE-capable assets are lowering unit costs and improving gauge accuracy, creating new scope for downgauging without sacrificing mechanical integrity. Single-use plastics regulations in Canada and several U.S. states are nudging converters toward coated oxygen-barrier and metallization-free structures that still meet shelf-life targets, thereby widening the performance gap between commodity transparent film and specialty coatings. Meanwhile, polypropylene feedstock volatility has heightened the appeal of backward integration and resin-light formulations, prompting strategic partnerships across the value chain.

Key Report Takeaways

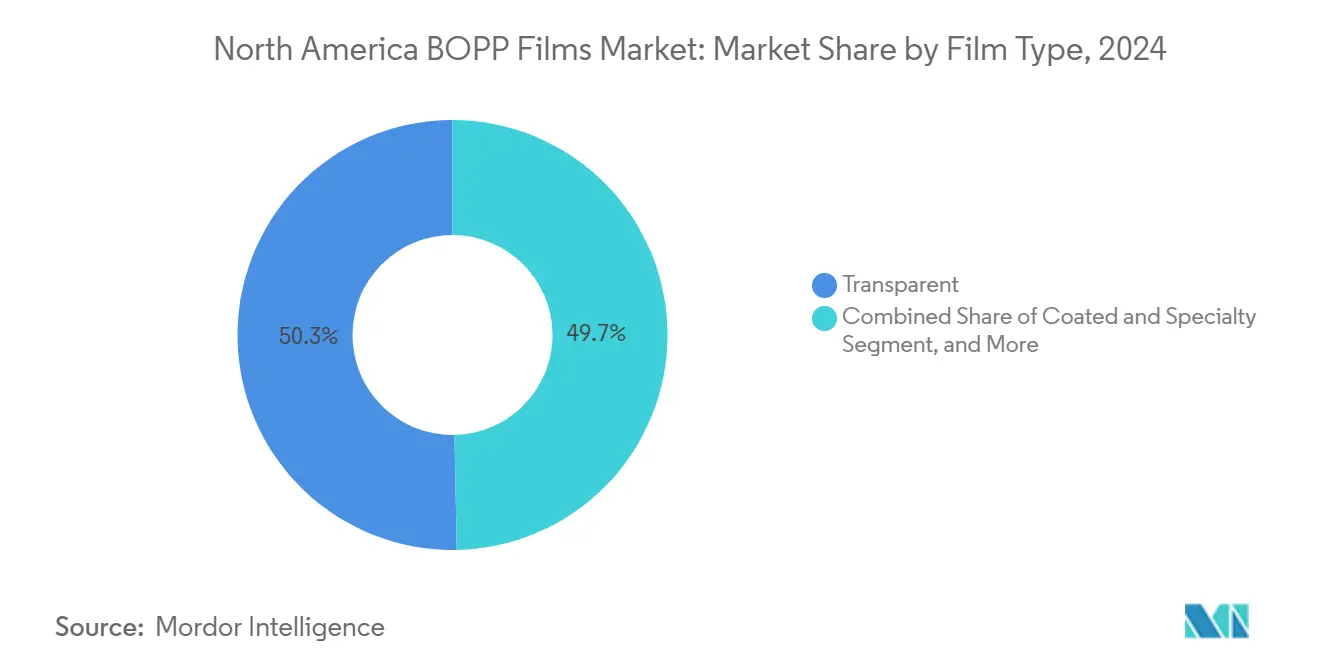

- By film type, transparent grades led with 50.32% revenue share in 2024; coated and specialty films are forecast to accelerate at 5.87% CAGR through 2030.

- By thickness, the 15-30 micron band captured 36.86% share in 2024 while films above 45 microns are projected to post a 4.83% CAGR to 2030.

- By production process, tenter lines held 72.43% output in 2024 and simultaneous biaxial stretching is anticipated to advance at 5.12% CAGR up to 2030.

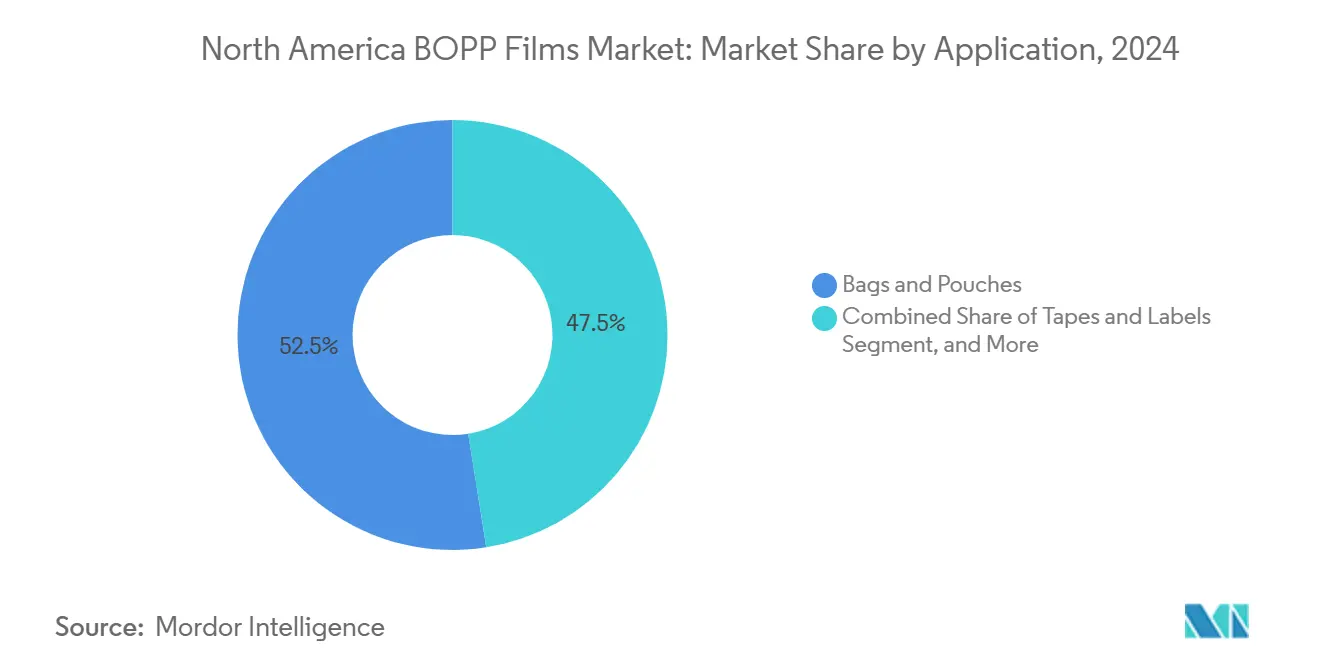

- By application, bags and pouches accounted for 52.53% share of the North America BOPP films market size in 2024 and tapes and labels are set for 4.74% CAGR through 2030.

- By end user, the food segment commanded 58.87% of the North America BOPP films market share in 2024 whereas pharmaceuticals are expected to expand at 6.12% CAGR by 2030.

- By country, the United States contributed 78.87 of % revenue in 2024, and Mexico is forecast to register the fastest 5.35% CAGR to 2030.

North America BOPP Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Sustainable Flexible Packaging Demand | +1.2% | United States, Canada, with spillover to Mexico | Medium term (2-4 years) |

| Growth of E-Commerce-Ready Lightweight Films | +1.4% | United States dominant, Canada secondary | Short term (≤ 2 years) |

| Conversion from Rigid to Flexible Packaging in Food Service | +0.9% | United States, Mexico QSR expansion zones | Medium term (2-4 years) |

| Rapid Capacity Expansions by North American Extruders | +0.8% | United States (Midwest, Southeast), Mexico (Querétaro, Monterrey) | Short term (≤ 2 years) |

| Adoption of BOPE-Ready Hybrid Production Lines | +0.6% | United States (early adopters), Canada pilot sites | Long term (≥ 4 years) |

| Brand Owner Commitments to Mono-Material Recyclable Laminates | +1.0% | United States, Canada (EPR-driven), Mexico (export-oriented converters) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Sustainable Flexible Packaging Demand

Brand owners are fast-tracking mono-material BOPP⁄PP laminates to avoid extended producer responsibility fees that penalize multi-layer mixes in California and Canada. Huhtamaki’s 2024 partnership with Siegwerk and Borouge yielded a digitally printable mono-PP pouch targeting food brands exposed to recycling levies of up to USD 0.10 per kilogram. Gualapack debuted a fully recyclable stand-up pouch for premium coffee and pet food, displacing PET⁄PE⁄aluminum composites. TOPPAN’s GL-SP vapor-deposited barrier film, released in April 2024, delivers an oxygen-transmission rate of 0.5 cc/m²/day yet remains compatible with polyolefin recycling streams.[1]TOPPAN Inc., “TOPPAN to Launch Indian Production of BOPP-based GL-SP Barrier Film for Sustainable Packaging,” holdings.toppan.com Federal support is evident: the U.S. Department of Energy granted USD 6 million in 2024 for recyclable film R&D, signaling official endorsement for mono-material innovation.

Growth of E-Commerce-Ready Lightweight Films

North American parcel volumes topped 17 billion units in 2024, pushing converters toward BOPP gauges below 20 microns that trim shipping weight without compromising puncture resistance. Howie Machinery noted in May 2025 that tape lines are running at elevated utilization to feed carton-sealing demand under VOC-compliant, water-based adhesive systems. H.B. Fuller’s Clarity PHL4150 adhesive ensures high tack on cold or damp corrugated boxes, supporting lines exceeding 600 m/min. Sealed Air’s 15 micron CRYOVAC lidding film cuts pack weight by 40% and improves throughput on high-speed tray lines. E-commerce majors therefore accelerate both volume and grade complexity, feeding specialty demand even as parcel growth moderates post-2026.

Conversion from Rigid to Flexible Packaging in Food Service

Multinational consumer-goods companies targeting 100% recyclability by 2025 have scaled investments in BOPP-centric laminates. The Sustainable Packaging Coalition recorded that 68% of U.S. flexible-packaging converters were installing mono-material capability by early 2025, up sharply from 42% in 2022. Taghleef’s acrylic-barrier films replace aluminum metallization in snack pouches, while Innovia’s Propafilm RCU blocks mineral-oil migration for up to 1.5 years, satisfying FDA and EU rules. Such re-tooling directly channels premium demand to specialty BOPP grades, reinforcing long-term profit pools even as commodity margins compress.

Rapid Capacity Expansions by North American Extruders

Quick-service restaurants across North America are phasing out rigid polystyrene clamshells in favor of recyclable BOPP pouches. Sealed Air documented a 60% material reduction and shelf-life extension from 21 to 45 days when Cucina Fresca switched to CRYOVAC vacuum-skin packs in 2024. Coesia’s Volpak Enflex F-17, shown at EXPO PACK México 2024, processes low-tension PP films without major line retrofits, easing adoption for contract packers. The most pronounced uptake is in Mexico, where food-service suppliers for U.S. chains align with sustainability scorecards and exploit tariff-free access under T-MEC.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polypropylene Feedstock Price Volatility | -0.7% | United States, Canada (integrated petrochemical hubs), Mexico (import-dependent) | Short term (≤ 2 years) |

| Stringent Single-Use Plastics Regulations | -0.5% | Canada (federal ban), United States (California, New York), Mexico (select municipalities) | Medium term (2-4 years) |

| Competition from Paper and Biodegradable Films | -0.4% | United States, Canada (premium dry-food segments) | Long term (≥ 4 years) |

| Overcapacity Pressuring Margins for Commodity Grades | -0.6% | United States (Midwest, Southeast production clusters) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Polypropylene Feedstock Price Volatility

North American polypropylene prices swung between USD 0.62 and USD 0.88 per pound during 2024 after refinery maintenance and geopolitical jitters disrupted propylene supply. BOPP extruders operating on 8-12% gross margins can seldom pass rising resin costs to converters locked into annual contracts. Integrated producers with captive propylene, such as ExxonMobil, secure a structural cost edge, whereas Mexico’s import-dependent converters absorb currency risk as 70% of national PP demand arrives from abroad.

Stringent Single-Use Plastics Regulations

Regional plastics and rubber capacity utilization slid to 76.6% in November 2024, reflecting excess starter-grade output even before Oben, Taghleef and Asian imports add fresh tonnage. Smaller merchant extruders lacking coating or metallization assets face intensified price competition, pushing them either toward consolidation or rapid specialty upgrades. Margin recovery hinges on e-commerce and food-service demand soaking up surplus rolls by late 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Specialty Coatings Capture Premium Segments

Transparent film anchored the North America BOPP films market with 50.32% share in 2024. Coated and specialty grades, however, are tracking 5.87% CAGR to 2030 as converters pivot toward oxygen-barrier, high-seal coatings that enable recycle-ready laminates. Metallized grades surrender ground because aluminum layers hinder polyolefin recycling, spurring brand owners to shift volumes to acrylic or AlOx coated BOPP. Price premiums of 20-40% encourage extruders to add online coaters despite higher capital intensity.

Pressured by regulations, transparent grades are now leveraging downgauging to retain cost advantage. Innovia’s Propafilm RCU and Taghleef’s EXTENDO lines showcase how barrier coatings replicate metallized oxygen performance while preserving sort-stream compatibility. Consequently, the North America BOPP films market sees a bifurcation: commodities serve tape and wrap where clarity rules, while functional coatings dominate barrier-critical snacks, coffee and pet foods.

By Thickness: Heavy-Gauge Films Serve Industrial Tapes

The 15-30 micron class holds the largest 36.86% slice but growth momentum shifts toward ≥45 micron gauges used in heavy-duty carton-sealing tapes and wraps registering 4.83% CAGR. E-commerce fulfillment centers favor 50-60 micron films for puncture resistance during robotic sortation. BagsOnNet markets 60 micron tapes with cold-weather acrylic adhesive, safeguarding seal integrity in refrigerated supply chains.

Below-15 micron films address twist-wrap and over-wrap but face processing limits on legacy tenter lines. Mid-range 30-45 micron films dominate printing and lamination but endure margin squeeze from downgauging at one end and high-performance industrial demand at the other. Jindal’s tight tolerance offerings (< ±5%) remain critical for high-speed die-cut label presses

By Production Process: Simultaneous Stretching Gains Traction

Tenter lines delivered 72.43% of 2024 output, favored for optical clarity and width versatility. Yet simultaneous stretching via bubble or hybrid systems is advancing 5.12% CAGR as Brückner’s switchable lines allow polypropylene and polyethylene runs on the same frame. Such flexibility helps producers hedge resin volatility and test BOPE without greenfield builds. Tubular double-bubble, accounting for roughly 11% capacity, retains a niche in shrink and specialty barrier film thanks to its balanced shrink ratios.

Oben’s 12-meter tenter commissioned in February 2025 underlines economies of scale, yielding jumbo rolls that slash downstream waste. Meanwhile, sequential producers are adding automated gauge control and inline coating to stave off simultaneous-stretch challengers. Over the forecast horizon, hybrid assets will likely lift their North America BOPP films market presence, though tenter lines stay dominant in ultra-wide commodity runs.

By Application: Tapes and Labels Ride the Parcel Wave

Bags and pouches controlled 52.53% of 2024 volume, but tapes and labels are set for 4.74% CAGR as logistics and omnichannel retail fuel carton-sealing and shipping-label demand. H.B. Fuller’s fast-setting acrylics permit 600 m/min coating on BOPP, aligning with converters chasing throughput gains. Inteplast supplies tailor-made facestock films offering moisture resistance and die-cut stability for beverage and personal-care labels.

Flow-wrap, confectionery twist films and lamination bases draw on BOPP’s stiffness and gloss but encounter substitution from PE/BOPE for soft-touch pouches. Capacitor and industrial films, though small in tonnage, command premium pricing tied to dielectric performance. Overall, rising parcel counts keep tapes and labels on a higher growth plane, cushioning the North America BOPP films market against softness in mid-range wrap demand.

By End-User Vertical: Pharmaceuticals Gain Momentum

Food retained a commanding 58.87% share in 2024 through bakery, snack and fresh-produce channels. Yet pharmaceuticals lead growth with 6.12% CAGR as blister lidding migrates from PVC/aluminum to recycle-compatible BOPP⁄PP structures meeting EU Packaging Waste Regulation targets for 2030. Jindal’s heat-seal-coated BOPP delivers tamper evidence and child-resistance while entering existing polyolefin reclaim streams.

Beverage labels, personal-care wraps and industrial tapes represent secondary pillars, each sensitive to macro consumption swings but generally aligned with BOPP’s clarity and machinability strengths. As medical packaging standards converge globally, the pharmaceutical push adds defensive diversification, further stabilizing aggregate demand for the North America BOPP films market.

Geography Analysis

The United States anchors the North America BOPP films market at 78.87% of 2024 volume. Inteplast, Toray Plastics and a newly operational 12-meter Oben line reinforce domestic self-sufficiency while e-commerce volumes topping 17 billion parcels annually sustain carton-sealing and protective-wrap runs.[2] Oben Group, “Oben Holding Group Commissions 12-Meter BOPP Line,” obengroup.com California’s EPR rules accelerate mono-material laminate deployment, lifting specialty-grade premiums even as overall plastics capacity utilization eased to 76.6% late in 2024. Federal R&D grants further prime innovation pipelines, strengthening the ecosystem of coating, metallization and converting suppliers that circle the U.S. Gulf and Midwest clusters.

Canada, albeit a smaller base, sets the regulatory tone through a federal single-use plastics ban effective 2022 and broadened in 2024. Converters in Ontario and Quebec now retrofit lines for acrylic-barrier BOPP to avoid producer-responsibility surcharges. Pharmaceutical demand clustered around Toronto and Montreal favors BOPP lidding films that satisfy Health Canada’s recyclability guidance, adding steady pull for specialty co-extrusions.

Mexico enjoys the region’s fastest 5.35% CAGR fueled by T-MEC tariff certainty and labor-cost arbitrage that attract packaging multinationals to Querétaro and Monterrey industrial corridors. Coesia’s low-tension form-fill-seal equipment exhibited at EXPO PACK México 2024 enables local converters to adopt mono-material PP pouches without prohibitive capex, thereby aligning with U.S. customer sustainability scorecards. While 70% of Mexican PP is imported, leading to resin price exposure, the nearshoring wave outweighs this disadvantage, positioning Mexico as the incremental growth engine for the North America BOPP films market.

Competitive Landscape

Market concentration is moderate: the top five suppliers, Inteplast, Toray Plastics, Oben, Taghleef, and Jindal, hold roughly 55-65% of installed capacity. Inteplast leverages vertical integration across BOPP extrusion, tape coating and distribution, granting a scale-driven cost edge in transparent grades. Oben’s new 12-meter tenter line showcases capital intensity as a strategic moat, targeting wide-web industrial segments where jumbo rolls curb downstream waste. Taghleef’s February 2025 acrylic-barrier coater expands premium capacity aimed at snack and confectionery pouches requiring a metallization-free oxygen barrier.

Mid-tier players Cosmo, Innovia, and Uflex intensify competition in coated niches, while hybrid BOPE-ready assets installed by early adopters create white-space advantage. Brückner’s switchable stretching frames and Nova’s machine-direction-orientable PE resins offer technical hedges against polypropylene volatility. Paper-based barrier films from Sappi and biodegradable PLA/PBAT structures are gaining traction in premium organic food channels, but remain cost-prohibitive for mass segments.[3]Sappi Packaging and Speciality Papers, “Focus on Barrier Papers,” sappi-psp.com

Strategic thrusts increasingly focus on full-solution platforms rather than commodity tonnage. Vapor deposition systems applying AlOx or SiOx on BOPP, exemplified by TOPPAN’s GL-SP, integrate resin formulation, extrusion and coating at one site, trimming lead times and reducing defect rates. As brand owners chase recycle-ready claims, technical service and rapid prototyping rise as pivotal differentiators, reshaping the competitive calculus within the North America BOPP films market.

North America BOPP Films Industry Leaders

Oben Holding Group

Taghleef Industries LLC

Dunmore Corporation

Inteplast Group Ltd.

Cosmo Films Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Oben Holding Group commissioned a 12-meter-wide BOPP production line, described as the world's widest, enabling production of jumbo rolls that reduce converting waste for wide-web applications such as industrial wraps and agricultural films, with capacity additions targeting North American demand for heavy-duty packaging.

- February 2025: February 2025 - Taghleef Industries installed a new coating line at its U.S. facility, expanding capacity for acrylic-barrier and heat-seal coatings that support mono-material laminate demand, with the investment targeting food and beverage converters seeking recyclable alternatives to aluminum metallization.

- September 2025: Pregis expanded North American film operations to meet e-commerce driven demand for BOPP-based air pillows and void-fill.

- April 2024: TOPPAN Inc. launched GL-SP, a vapor-deposited barrier film on BOPP substrate, delivering 0.5 cc/m²/day oxygen transmission and aimed at recyclable dry-food packs in North America, Europe and India.

North America BOPP Films Market Report Scope

The BOPP Films Market refers to the industry involved in the production, distribution, and application of Biaxially Oriented Polypropylene (BOPP) films, which are polypropylene films stretched in both machine (MD) and transverse (TD) directions to enhance mechanical, optical, and barrier properties.

The North America BOPP Films Market Report is Segmented by Film Type (Transparent, Metallized, White/Opaque, Coated and Specialty, Other Film Types), Thickness (Below 15 Microns, 15-30 Microns, 30-45 Microns, Above 45 Microns), Production Process (Tenter Process, Tubular Double Bubble Process, Simultaneous Biaxial Stretching), Application (Bags and Pouches, Wraps, Tapes and Labels, Printing and Lamination, Capacitor and Industrial Films), End-User Vertical (Food, Beverage, Industrial, Pharmaceuticals, Personal Care and Cosmetics, Other End-User Verticals), and Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Film Type

| Transparent |

| Metallized |

| White / Opaque |

| Coated and Specialty |

| Other Film Types |

By Thickness

| Below 15 Microns |

| 15-30 Microns |

| 30-45 Microns |

| Above 45 Microns |

By Production Process

| Tenter Process |

| Tubular (Double Bubble) Process |

| Simultaneous Biaxial Stretching |

By Application

| Bags and Pouches |

| Wraps |

| Tapes and Labels |

| Printing and Lamination |

| Capacitor and Industrial Films |

By End-User Vertical

| Food |

| Beverage |

| Industrial |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Other End-User Verticals |

By Country

| United States |

| Canada |

| Mexico |

| By Film Type | Transparent |

| Metallized | |

| White / Opaque | |

| Coated and Specialty | |

| Other Film Types | |

| By Thickness | Below 15 Microns |

| 15-30 Microns | |

| 30-45 Microns | |

| Above 45 Microns | |

| By Production Process | Tenter Process |

| Tubular (Double Bubble) Process | |

| Simultaneous Biaxial Stretching | |

| By Application | Bags and Pouches |

| Wraps | |

| Tapes and Labels | |

| Printing and Lamination | |

| Capacitor and Industrial Films | |

| By End-User Vertical | Food |

| Beverage | |

| Industrial | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Other End-User Verticals | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America BOPP films market?

It is valued at USD 8.81 billion in 2025 and is projected to reach USD 11.71 billion by 2030.

Which film type is growing fastest in North America?

Coated and specialty BOPP films are advancing at a 5.87% CAGR through 2030 as brand owners prioritize recycle-ready barrier structures.

Why are thicker BOPP gauges gaining traction?

E-commerce carton-sealing tapes and heavy-duty wraps need 50-60 micron films for puncture resistance in automated fulfillment centers.

How do single-use plastics rules affect BOPP demand?

Regulations in California and Canada penalize non-recyclable laminates, pushing converters toward mono-material BOPP structures to avoid fees.

Which country is the fastest-growing market for BOPP films within North America?

Mexico is expanding at 5.35% CAGR due to nearshoring under T-MEC and rising flexible-packaging capacity targeting U.S. brand owners.

What strategic technologies are reshaping competition?

Hybrid BOPE-ready stretching lines and vapor-deposited AlOx barrier coatings position extruders for both sustainability and cost leadership.

Page last updated on: