Mono-material Plastic Packaging Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

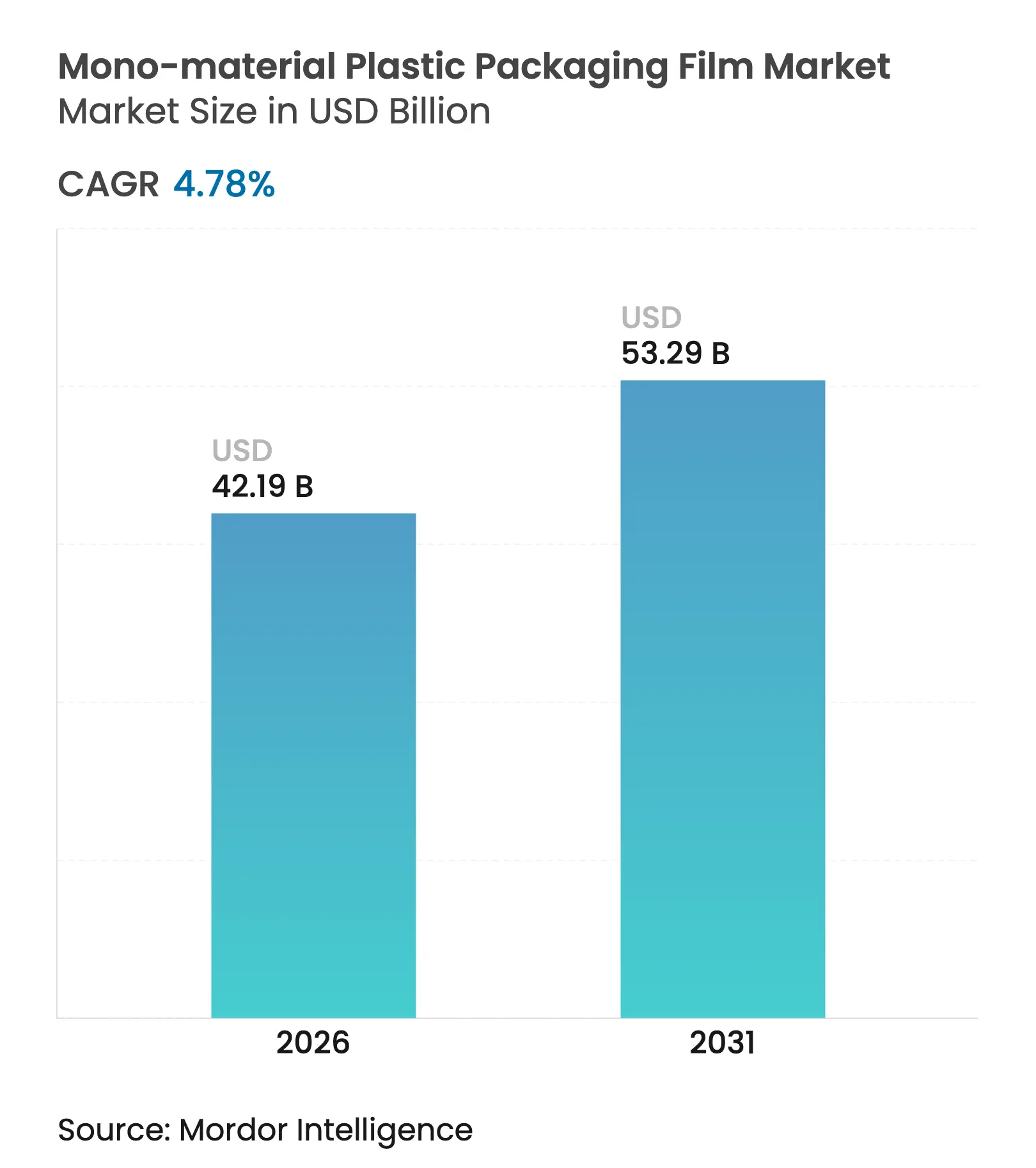

| Market Size (2026) | USD 42.19 Billion |

| Market Size (2031) | USD 53.29 Billion |

| Growth Rate (2026 - 2031) | 4.78 % CAGR |

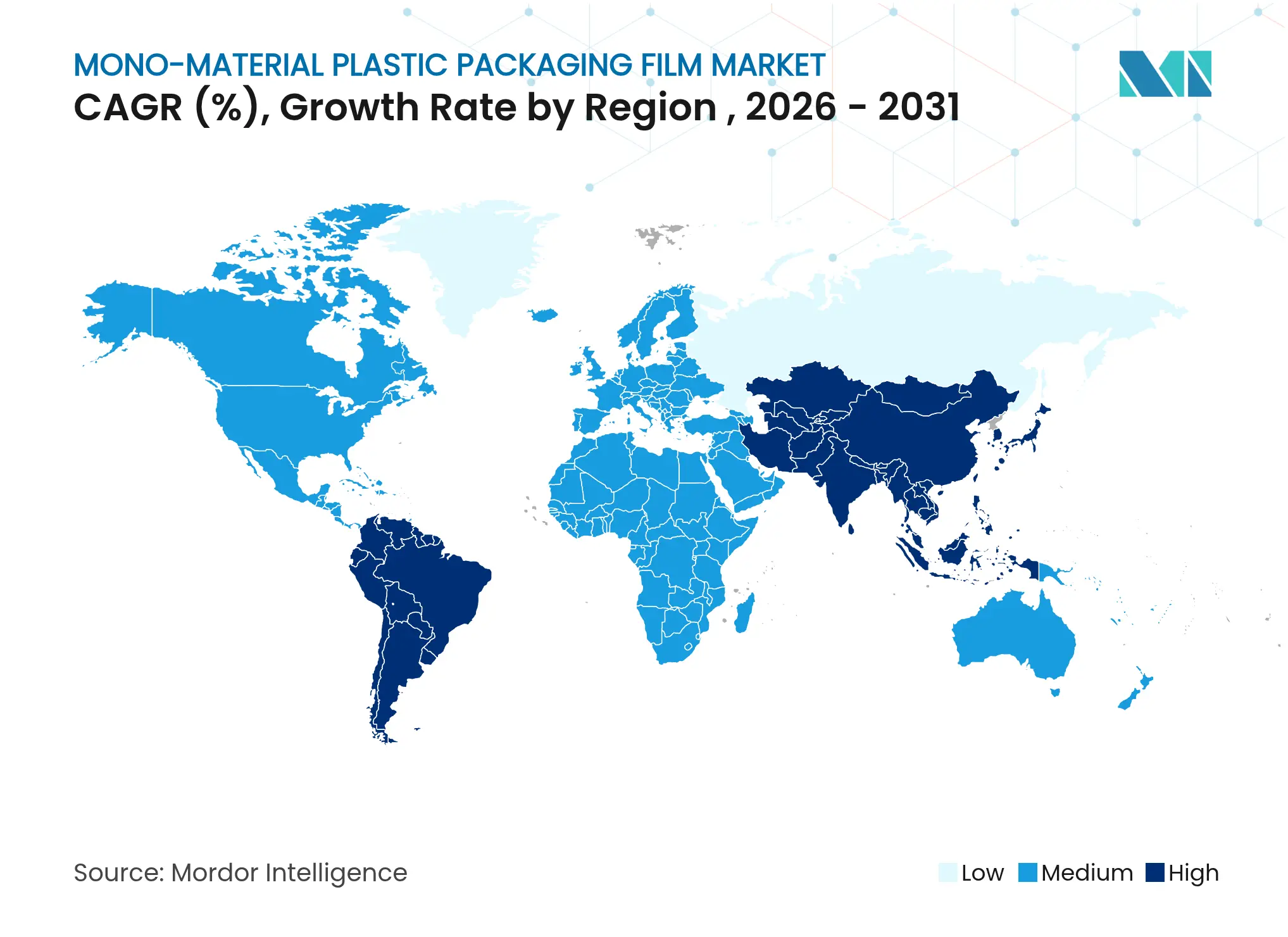

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Mono-material Plastic Packaging Film Market Analysis by Mordor Intelligence

The mono-material plastic packaging film market size is expected to grow from USD 40.26 billion in 2025 to USD 42.19 billion in 2026 and is forecast to reach USD 53.29 billion by 2031 at 4.78% CAGR over 2026-2031. Much of that momentum stems from regulators who now require meaningful recycled-content thresholds, forcing brand owners to replace multi-layer laminates with single-polymer structures that stay compatible with mainstream recycling streams. Polyethylene’s broad processing window gives it a head start, yet polypropylene’s optical clarity and hot-fill stability are prompting many converters to qualify PP mono structures for premium applications. Capital spending on machine-direction-oriented (MDO) assets continues across North America, Europe, and Asia-Pacific because the technology yields thinner films with higher stiffness, attributes that lower shipping weight in e-commerce channels. Added to that, large retailers have embedded “design-for-recycling” scorecards in private-label tenders, redirecting high-volume SKUs toward recyclable mono-material alternatives. Collectively, these factors position the mono-material plastic packaging film market for dependable mid-single-digit growth through the decade.

Advanced compatibilizers, PFAS-free processing aids, and oxygen-scavenging masterbatches are closing the historic barrier-performance gap versus aluminum-foil and EVOH-based laminates, thereby unlocking high-value food formats that once relied on multi-layer structures. Although ethylene and propylene price swings compress converter margins, vertical integration and long-term resin contracts are helping leading film makers protect profitability. Regionally, North America leads on market share thanks to state-level recycled-content rules, while Asia-Pacific posts the fastest growth on the back of new extrusion lines and expanding consumer-goods demand. Standard films still dominate, but high-barrier grades are multiplying at nearly double the aggregate CAGR as compatibilizer chemistry matures. At the same time, brand-owner experiments with bio-based PP and chemically recycled PE suggest that the sustainability narrative will broaden from “recyclable” to “low-carbon” over the forecast period.

Key Report Takeaways

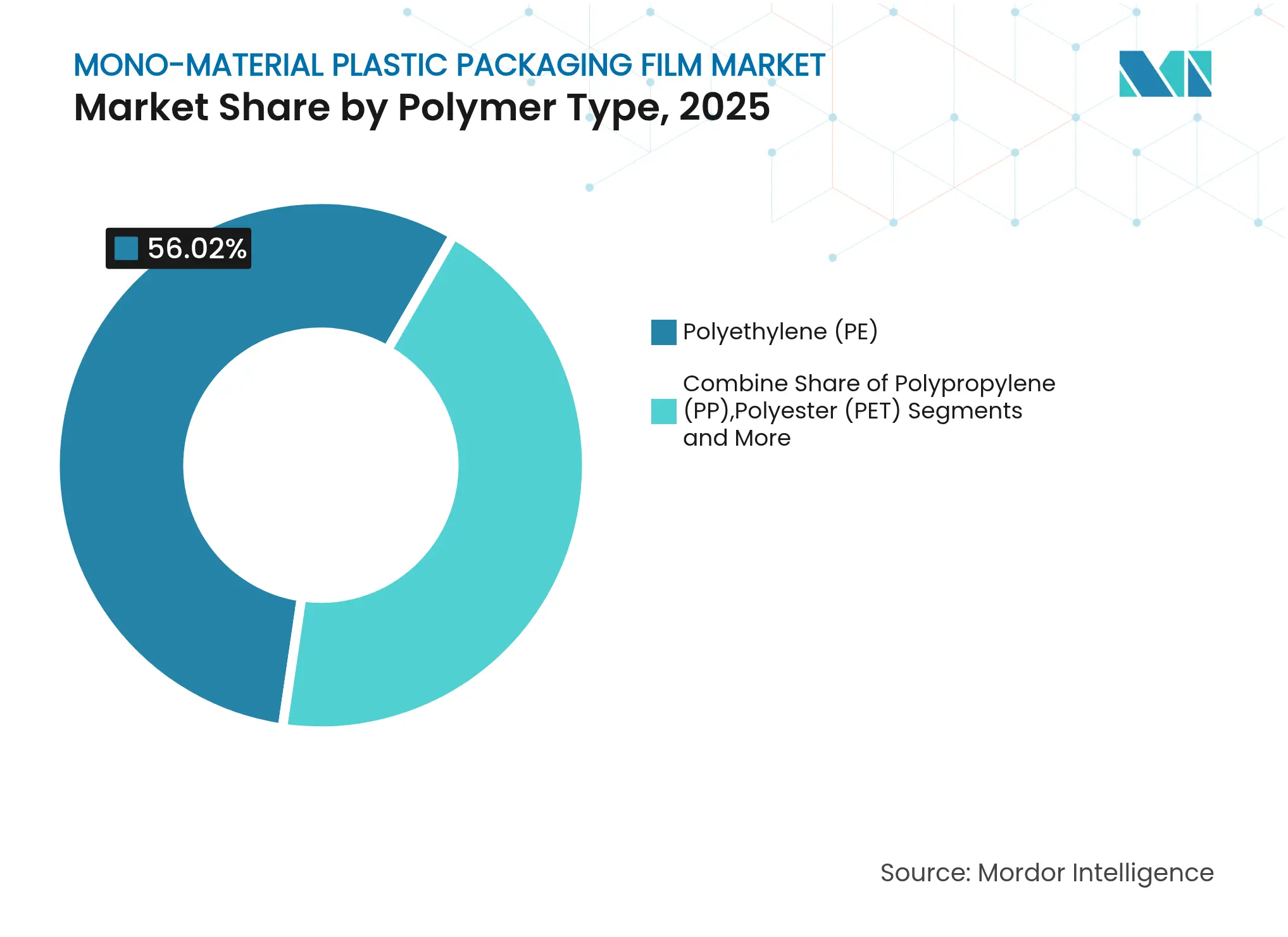

- By polymer type, polyethylene captured 56.02% of the mono-material plastic packaging film market share in 2025, whereas polypropylene is projected to post the quickest 6.56% CAGR to 2031.

- By film manufacturing process, blown film retained 48.21% revenue share in 2025; MDO film, however, is forecast to expand at 8.02% through 2031.

- By packaging format, pouches commanded 41.03% share of the mono-material plastic packaging film market size in 2025, while wrappers and overwraps are advancing at a 5.51% CAGR.

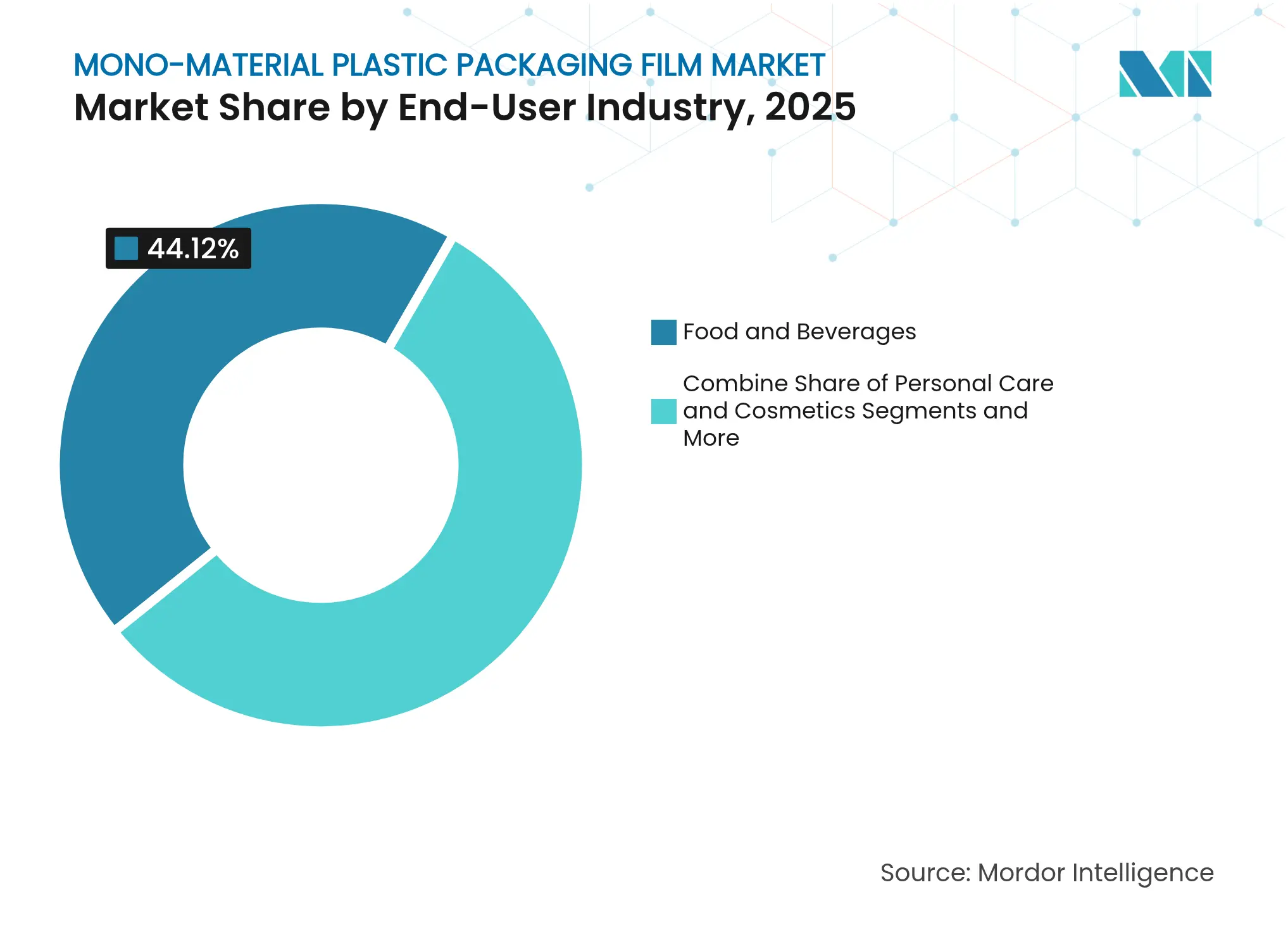

- By end-user Industry, the food and beverage segment held 44.12% share in 2025; personal care and cosmetics is slated to rise at a 6.62% CAGR between 2026-2031.

- By barrier property, the standard films segment held 62.77% share in 2025; High-Barrier Films is slated to rise at 8.58% CAGR between 2026-2031.

- By geography, North America led with 34.52% share in 2025 as Asia-Pacific registers the highest 8.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mono-material Plastic Packaging Film Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory mandates targeting >30% recycled content by 2030 Regulatory mandates targeting >30% recycled content by 2030 | +1.2% | EU, Canada, select US states | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:EU, Canada, select US states | Impact Timeline:Medium term (2-4 years) |

CPG shift to mono-PE/PP pouches for e-commerce-ready lightweighting CPG shift to mono-PE/PP pouches for e-commerce-ready lightweighting | +0.8% | Global, early adoption in North America & EU | Short term (≤ 2 years) | |||

Rapid scale-up of MDO PE film lines Rapid scale-up of MDO PE film lines | +0.6% | APAC core, spill-over to North America | Medium term (2-4 years) | |||

Advanced compatibilizers enabling high-barrier mono structures Advanced compatibilizers enabling high-barrier mono structures | +0.5% | Global | Long term (≥ 4 years) | |||

Retailer “design-for-recycling” scorecards Retailer “design-for-recycling” scorecards | +0.4% | North America & EU | Short term (≤ 2 years) | |||

Food-waste-reduction policies favouring breathable mono films Food-waste-reduction policies favouring breathable mono films | +0.3% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory Mandates Targeting >30% Recycled Content by 2030

The European Union’s Packaging and Packaging Waste Regulation that entered into force in March 2025 obliges every plastic pack to contain at least 30% recycled resin by 2030, rising to 50% in the following decade, and parallel rules in Canada and California mirror that ambition. [1]European Commission, “Regulation (EU) 2025/40 on packaging and packaging waste,” eur-lex.europa.euMechanical recyclers have reacted by commissioning high-throughput wash-lines dedicated to flexible films; NOVA Chemicals’ 100-million-lb plant in Indiana exemplifies this pivot toward post-consumer PE streams. Because mono-material films flow cleanly through optical sorters, brand owners view them as the lowest-risk route to compliance across multiple jurisdictions with staggered timelines. As compliance penalties outstrip the cost premium of recycling-grade resins, the regulatory driver materially lifts demand for single-polymer pouches, labels, and overwraps in the mono-material plastic packaging film market.

CPG Shift to Mono-PE/PP Pouches for E-commerce-Ready Lightweighting

Online retail’s escalating parcel volumes make every gram of packaging a cost variable. Lightweight mono-PE stand-up pouches can reduce total pack weight up to 75% relative to rigid PET jars, trimming dimensional-weight charges while passing ISTA drop-tests. Klöckner Pentaplast’s kp FlexiFlow EH 155 R—composed of more than 95% polyethylene—runs at 120 packs per minute on existing form-fill-seal lines, proving that mono structures can hit the cycle-time targets demanded by fulfillment centers. ExxonMobil’s high-barrier PE recipes now reach oxygen-transmission rates below 0.1 cm³/m²·day, enabling roast-and-ground coffee or nutraceutical powders to stay fresh through elongated supply chains. This convergence of shipping efficiency and shelf-life parity has encouraged personal-care brands to swap multi-layer PET/foil laminates for transparent mono-PP pouches that showcase product color while maintaining recyclability.

Rapid Scale-Up of Machine-Direction-Oriented (MDO) PE Film Lines

Announced MDO PE capacity adds more than 250 kilotons per year between 2025-2027, spearheaded by converters in Malaysia, China, and the Gulf states seeking thinner gauges without strength penalties. ExxonMobil’s Exceed S performance PE grades let converters like Scientex produce films that are 25% thinner yet 40% stiffer than conventional blown alternatives, widening the down-gauging window while maintaining dart impact. Mid South Extrusion’s twin USD 17 million and USD 12.5 million projects in Louisiana highlight North America’s readiness to replicate the MDO model for domestic food and courier-bags. [2]Louisiana Economic Development, “Mid South Extrusion announces investment for film growth,” opportunitylouisiana.gov As energy and resin expenditures dominate cost-of-goods, the productivity gains and material savings inherent in MDO processing strengthen the competitive position of the mono-material plastic packaging film market relative to legacy laminates.

Advanced Compatibilizers Enabling High-Barrier Mono Structures

Clariant’s PFAS-free AddWorks. PPA and other next-generation processing aids reduce die-build-up, improve gloss, and sharpen seal integrity, minimizing off-spec scrap that historically penalized mono-PE barrier structures. Academic work on stearic-acid-grafted starch as a compatibilizer in PE/TPS blends shows tensile-strength gains of 18% and water-vapor-permeability cuts of 22%, hinting at bio-based paths toward barrier uplift.[3]WASET Publications, “Interfacial adhesion improvement of PE/TPS blends,” publications.waset.org Oxygen-scavenging nano-iron add-ins and advanced coatings have already allowed polypropylene mono-films to hit sub-0.05 cm³/m²·day OTR, which is opening high-fat snack and retort-pouch uses once dominated by aluminum foil. As these chemistries scale, they remove the final functional hurdle that limited mono-material film adoption in the highest-value applications.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile C2/C3 monomer prices squeezing converter margins Volatile C2/C3 monomer prices squeezing converter margins | -0.7% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:Global | Impact Timeline:Short term (≤ 2 years) |

Functional barrier trade-offs in high-fat foods Functional barrier trade-offs in high-fat foods | -0.4% | Global | Medium term (2-4 years) | |||

Limited sortation capacity for flexibles in North-America MRF network Limited sortation capacity for flexibles in North-America MRF network | -0.3% | North America | Long term (≥ 4 years) | |||

OEM reticence to re-qualify pharma packaging OEM reticence to re-qualify pharma packaging | -0.2% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile C2/C3 Monomer Prices Squeezing Converter Margins

Ethylene and propylene transactions spiked 22% quarter-on-quarter in early 2025 after unplanned cracker outages and feedstock tightness, lifting raw-material cost share to almost 70% of finished-film COGS for independent converters.[4]Hapco Inc., “Resin shortage and supply-chain disruptions,” hapcoincorporated.com Smaller players with limited hedging latitude face margin compression that delays capital projects for MDO or recycled-content integration. Converters tied into long-term offtake with integrated resin producers fare better, but the sector overall remains sensitive to upstream volatility, creating an operational headwind within the mono-material plastic packaging film market.

Functional Barrier Trade-offs in High-Fat Foods

Oxygen-transmission rates below 0.01 cm³/m²·day are still the benchmark for vacuum-fried snacks and single-origin coffee; mono-PE and mono-PP films typically register an order of magnitude higher unless multi-layered with tie-layers that disrupt recyclability. High-fat matrices accelerate rancidity, so brand owners hesitate to compromise shelf life for sustainability messaging, especially in premium price tiers. While compatibilizer progress is notable, extensive validation—microbial challenge tests, accelerated aging, and regulatory migration studies—extends pilot-to-launch timelines, capping near-term penetration into these protective niches.

Segment Analysis

By Polymer Type: PE Dominance Faces PP Innovation Challenge

Polyethylene accounted for 56.02% of the mono-material plastic packaging film market share in 2025, cementing its role as the processing workhorse for grocery, courier, and industrial liners. Polypropylene, aided by bio-based pilot plants such as Braskem’s feasibility project in the United States, is riding a 6.56% CAGR on the back of clarity, stiffness, and hot-fill endurance advantages. That pace narrows PE’s historical lead, but mechanical recyclability and lower melting temperature keep PE entrenched where broad seal-window flexibility outweighs optics.

Bio-based and chemically recycled grades provide additional traction. PP resins synthesized from renewable ethanol offer identical mechanical properties while embedding a negative carbon footprint, resonating with premium beauty brands that elevate sustainability storytelling. Niche entrants—such as starch blends or PLA—are making headway in compostable produce bags, yet cost-per-kilogram gaps and limited collection infrastructure curb large-scale substitution. Over the outlook, new metallocene catalysts that push PE clarity and stiffness upwards will sustain polyethylene’s majority position, even as PP gathers increments in clear-barrier sachets and retortable pouches.

Note: Segment shares of all individual segments available upon report purchase

By Film Manufacturing Process: MDO Technology Disrupts Traditional Methods

Blown film still supplied 48.21% of all mono-material plastic packaging film market output in 2025 because its asset base is depreciated and well-understood by operators. That said, MDO’s 8.02% CAGR dwarfs other processes. By stretching oriented PE in the machine direction, converters can drop thickness from 50 µm to 37 µm while driving modulus gains, which in turn cuts material usage and shipping costs. Cast film retains relevance where gauge control and ultra-flatness are paramount, for instance in barrier lidding; extrusion coating serves T-shaped applications requiring paper-film laminates despite recyclability drawbacks.

AI-enabled thickness monitoring and closed-loop gravimetric dosing mitigate the learning curve on newer MDO assets, lowering scrap rates from 6% to 2% in greenfield plants. Even legacy blown lines receive retrofit kits that permit in-line MDO sections, indicating that process demarcations will blur as converters marry the familiarity of blown film with oriented-film performance.

By Packaging Format: Pouches Lead While Wrappers Accelerate

Pouches held 41.03% of the mono-material plastic packaging film market size in 2025, propelled by stand-up formats that combine billboard area with resealable spouts. Consumer loyalty programs delivered through QR codes on pouch surfaces further entrench the format in snack, pet-food, and personal-care aisles. Wrappers and overwraps, however, exhibit the fastest 5.51% CAGR because high-porosity mono-PE wraps prolong shelf life of berries and leafy greens under modified-atmosphere conditions. Bags and sacks maintain dominance in fertilizer and resin-pellet logistics where puncture resistance is critical.

Designers are experimenting with shaped-spout pouches and recyclable zipper profiles made entirely from HDPE, removing multi-material fitments that once blocked curbside recycling. Fresh-produce wraps employ micro-perforation and anti-fog coatings to manage respiration rates, illustrating how functional-plus-recyclable design is no longer mutually exclusive.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End-User Industry: Food Sector Dominance with Personal Care Growth

Food and beverage applications controlled 44.12% of 2025 volume as supermarkets pushed for mono-PE bread bags and cheese flow-wraps that match existing collection streams. Personal care and cosmetics, growing at 6.62% CAGR, lean on transparent mono-PP sachets and refill-pouch programs that align with brand ESG scorecards while preserving fragrance integrity. Pharmaceutical uptake stays cautious because blister formats still depend on aluminum for moisture barriers, and stability studies to validate mono structures span multi-year horizons.

Non-food industrial wraps—think insulation, lubricants, and hygiene—add baseline tonnage yet rarely require high-barrier chemistries, positioning recycled-content PE as the feedstock of choice. Across categories, “mass-balance” certified resins let brand owners book decarbonization credits even before physical recycled volumes scale, underscoring how carbon accounting techniques influence material decisions inside the mono-material plastic packaging film market.

Note: Segment shares of all individual segments available upon report purchase

By Barrier Property: Standard Films Dominate Despite High-Barrier Growth

Standard films represented 62.77% of total sales in 2025 because many dry-goods and courier envelopes need only moisture exclusion and scuff defense. High-barrier variants, though only 37.23% today, advance at an 8.58% CAGR thanks to nano-clay coatings, EVOH replacement tie-layers, and reactive oxygen scavengers that push OTR below 0.1 cm³/m²·day. Double-coated PP films with plasma-enhanced silicon oxide layers now challenge foil/SURLYN laminates for roasted-coffee demand, validating the technical ceiling of mono structures.

Future iterations may combine chem-loop recycling compatibility with barrier coatings that volatilize under controlled temperatures, ensuring both shelf life and end-of-life sortability. If proven at commercial scale, these solutions could tip the balance toward high-barrier mono films across meat, dairy, and nutraceutical use cases by the second half of the decade.

Geography Analysis

North America accounted for 34.52% of global revenue in 2025, anchored by California’s recycled-content mandate and robust collection infrastructure that captures 74% of flexible plastic packaging once specialized optical sorters are installed. Mid South Extrusion’s twin expansions in Louisiana and NOVA Chemicals’ Indiana recycling plant reflect a regional ecosystem that now spans virgin resin, post-consumer reclaim, and high-output film conversion. Nonetheless, flexible-film recovery still lags rigid PET due to contamination and bale economics, suggesting that policy-driven grants for MRF up-grades will dictate throughput of reclaim suitable for the mono-material plastic packaging film market.

Asia-Pacific registers the highest 8.64% CAGR through 2031 as rising middle-class incomes fuel packaged-food demand in China, India, and Indonesia. LyondellBasell’s Lupotech-T license to Levima for a 200 kt EVA plant exemplifies multinational technology transfer aimed at capturing regional growth. Local governments offer tax holidays for chemical recycling ventures, such as Dow’s MOU with SCGC that targets 200 kt of waste-to-polymer feedstock by 2030. Although waste-management infrastructure remains inconsistent, emerging EPR frameworks in Malaysia and Thailand signal future improvements in collection and aggregation.

Europe, backed by the Packaging and Packaging Waste Regulation, continues to punch above its weight in innovation. Finland’s VTT demonstrated cellulose-based films with moisture-barrier parity to oriented PP, while Fortum’s CO₂-based biodegradable polymer pilot showcases how carbon capture intersects with packaging. The region’s high disposal fees for non-recyclable packs expedite the shift to mono materials, yet energy-intensive recycling tariffs under the EU ETS could nudge converters toward lower-carbon bio-PP or chemical-recycling pathways to balance compliance costs.

The Middle East and Africa plus South America together represent a moderate but rising demand node. Gulf Cooperation Council members leverage feedstock advantage to export high-purity PE rolls, while Brazil’s state-level plastic-bag bans catalyze demand for heavier-gauge, reusable mono-PE carriers. Infrastructure constraints—limited curbside pickup and informal recycling networks—temper immediate volume, but multilateral green-bond financing for waste-to-energy and sorting centers is closing the gap. Collectively, geography-specific regulatory and infrastructure conditions will determine the pace at which each region contributes incremental tonnage to the mono-material plastic packaging film market.

Competitive Landscape

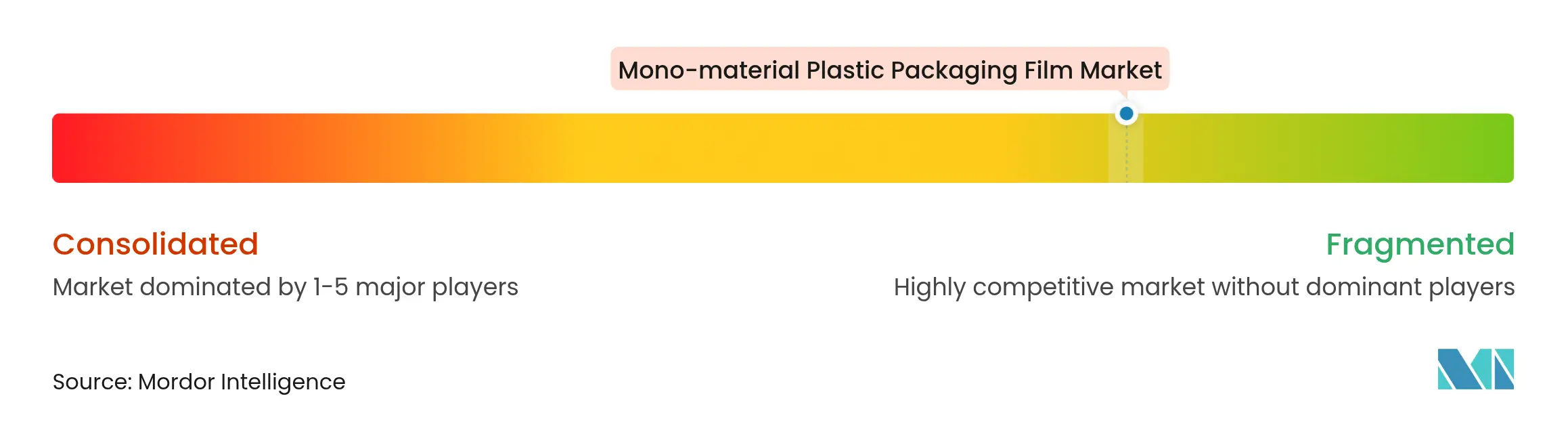

Market Concentration

The field is fragmented. Amcor’s USD 8.4 billion acquisition of Berry Global exemplifies how scale buys resin leverage, R&D bandwidth, and cross-selling synergies, with management targeting USD 650 million in annual cost savings by 2027. Novolex’s merger with Pactiv Evergreen further consolidates North American food-service films, signaling a defensive play against private-label power and resin volatility.

Technology leadership is a second axis of competition. ExxonMobil, Dow, and Borealis continue to release metallocene PE grades tuned for MDO orientation, while additive suppliers such as Clariant race to commercialize PFAS-free processing aids that remain compliant under tightening chemical legislation. Patent filings cluster around compatibilizer recipes that enhance interlayer adhesion without compromising melt-flow for recycling. AI-driven quality monitoring is emerging as a differentiator; lines equipped with machine-vision defect detection report scrap drops of 35%, bolstering margin resilience.

Strategic partnerships traverse the value chain: Amcor’s supply deal with NOVA Chemicals locks in mechanically recycled PE feedstock, ensuring the company can hit its 30% recycled-content promise by 2030. Dow’s tie-up with New Energy Blue to source bio-ethylene from corn stover highlights resin makers’ pursuit of carbon-negative inputs that dovetail with Scope 3 reduction targets. Overall, competition now hinges equally on cost position, technology breadth, and verifiable sustainability claims within the mono-material plastic packaging film market.

Mono-material Plastic Packaging Film Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amcor signed a multi-year collaboration with ExxonMobil to scale a new high-barrier, >95% PE mono-material film platform for coffee and snack pouches, with commercial volumes slated for Q3 2025.

- February 2025: Berry Global unveiled ClarityGuard™ shrink film, a mono-PE collation wrap containing 50% post-consumer resin that meets the Association of Plastic Recyclers’ design-for-recycling guidelines.

- January 2025: Mondi launched RetortPouchMono—a fully recyclable mono-PP retort pack that withstands 121 °C sterilization—initially targeting wet pet-food lines in Germany and Austria.

- November 2024: Constantia Flexibles opened a EUR 17 million Packaging Excellence Center in Weiden, Germany, to accelerate development of PE- and PP-based mono-material laminates for pharma blisters and flow-wraps.

Table of Contents for Mono-material Plastic Packaging Film Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Regulatory mandates targeting more than 30 % recycled content by 2030

- 4.2.2CPG shift to mono-PE/PP pouches for ecommerce-ready lightweighting

- 4.2.3Rapid scale-up of machine-direction-oriented (MDO) PE film lines

- 4.2.4Advanced compatibilizers enabling high-barrier mono structures

- 4.2.5Retailer “Design for Recycling” scorecards redirecting private-label SKUs

- 4.2.6Food waste–reduction policies favouring breathable mono films for fresh produce

- 4.3Market Restraints

- 4.3.1Volatile C2/C3 monomer prices squeezing converter margins

- 4.3.2Functional barrier trade-offs vs. multi-layer laminates in high-fat foods

- 4.3.3Limited sortation capacity for flexibles in North-America MRF network

- 4.3.4OEM reticence to re-qualify pharma packaging due to regulatory burden

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Polymer Type

- 5.1.1Polyethylene (PE)

- 5.1.2Polypropylene (PP)

- 5.1.3Polyvinyl Chloride (PVC)

- 5.1.4Polyester (PET)

- 5.1.5Other Polymer Type

- 5.2By Film Manufacturing Process

- 5.2.1Blown Film

- 5.2.2Cast Film

- 5.2.3Machine-Direction-Oriented (MDO) Film

- 5.2.4Extrusion-Coated Film

- 5.3By Packaging Format

- 5.3.1Pouches

- 5.3.2Bags and Sacks

- 5.3.3Wrappers and Overwraps

- 5.3.4Other Packaging Type

- 5.4By End-User Industry

- 5.4.1Food and Beverage

- 5.4.2Personal Care and Cosmetics

- 5.4.3Pharmaceutical

- 5.4.4Industrial and Household

- 5.4.5Other End-User Industry

- 5.5By Barrier Property

- 5.5.1High-Barrier Films

- 5.5.2Standard Films

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1United Kingdom

- 5.6.2.2Germany

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Netherlands

- 5.6.2.7Poland

- 5.6.2.8Russia

- 5.6.2.9Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2India

- 5.6.3.3Japan

- 5.6.3.4South Korea

- 5.6.3.5Australia and New Zealand

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1Middle East

- 5.6.4.1.1Turkey

- 5.6.4.1.2United Arab Emirates

- 5.6.4.1.3Saudi Arabia

- 5.6.4.1.4Rest of Middle East

- 5.6.4.2Africa

- 5.6.4.2.1South Africa

- 5.6.4.2.2Kenya

- 5.6.4.2.3Nigeria

- 5.6.4.2.4Rest of Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Amcor plc

- 6.4.2Mondi plc

- 6.4.3Sealed Air Corp.

- 6.4.4Saudi Basic Industries Corp. (SABIC)

- 6.4.5Huhtamaki Oyj

- 6.4.6Jindal Poly Films Ltd.

- 6.4.7Cosmo Films Ltd.

- 6.4.8CCL Industries Inc.

- 6.4.9Uflex Ltd.

- 6.4.10Toray Industries Inc.

- 6.4.11Innovia Films Ltd.

- 6.4.12Toppan Inc.

- 6.4.13Dow Inc.

- 6.4.14BASF SE

- 6.4.15DS Smith Plc

- 6.4.16Klockner Pentaplast

- 6.4.17AR Packaging Group AB

- 6.4.18Zotefoams plc

- 6.4.19Nurel S.A.

- 6.4.20Avery Dennison Corp.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Polymer Type

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polyester (PET)

- Other Polymer Type

- Polyethylene (PE)

- By Film Manufacturing Process

- Blown Film

- Cast Film

- Machine-Direction-Oriented (MDO) Film

- Extrusion-Coated Film

- Blown Film

- By Packaging Format

- Pouches

- Bags and Sacks

- Wrappers and Overwraps

- Other Packaging Type

- Pouches

- By End-User Industry

- Food and Beverage

- Personal Care and Cosmetics

- Pharmaceutical

- Industrial and Household

- Other End-User Industry

- Food and Beverage

- By Barrier Property

- High-Barrier Films

- Standard Films

- High-Barrier Films

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Poland

- Russia

- Rest of Europe

- United Kingdom

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- China

- Middle East and Africa

- Middle East

- Turkey

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Turkey

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- South Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Mono-Material Plastic Packaging Film Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 40.26 bn (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 10.9 bn (2024) | Global Consultancy A | excludes food wrap films; narrow regional scope | ||

USD 4.24 bn (2024) | Industry Journal B | counts only PE mono-film; omits PP volumes and ASP premiums | ||

USD 55.7 bn (2023) | Trade Organization C | bundles rigid and flexible formats, inflating value |