Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.25 Billion |

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 5.55 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Pharmaceutical 3PL Market Analysis by Mordor Intelligence

The Japan pharmaceutical 3PL third-party logistics market size is projected to expand from USD 4.25 billion in 2025 and USD 4.43 billion in 2026 to USD 5.55 billion by 2031, registering a CAGR of 4.59% between 2026 and 2031. Mandatory GS1 serialization, the rollout of cloud-based e-prescriptions, and the surge in cell and gene therapy trials are prompting manufacturers to shift distribution from in-house models to specialized providers with deep regulatory expertise. Investments in cryogenic networks, warehouse robotics, and carbon-neutral fleets are reshaping cost structures while last-mile demand rises as patients opt for home delivery. Capacity constraints at Narita and Haneda airports, multi-layer prefectural licensing for GDP warehouses, and semiconductor-related equipment delays remain key bottlenecks. Providers able to blend nationwide coverage with advanced temperature control, track-and-trace technology, and compliance support are best positioned to win bundled hospital contracts and cross-border clinical-trial work.

Key Report Takeaways

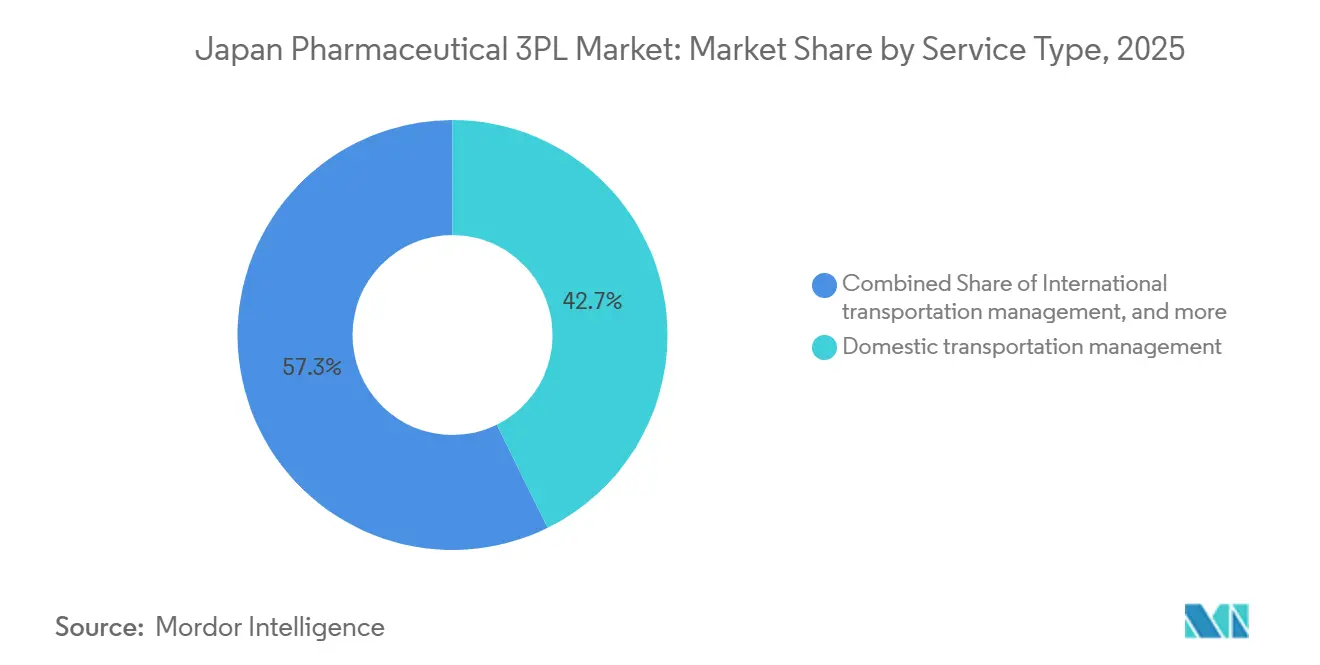

- By service type, domestic transportation management led with 42.69% of the Japan pharmaceutical 3PL third-party logistics market share in 2025, while International Transportation Management is projected to expand at a 5.05% CAGR through 2031.

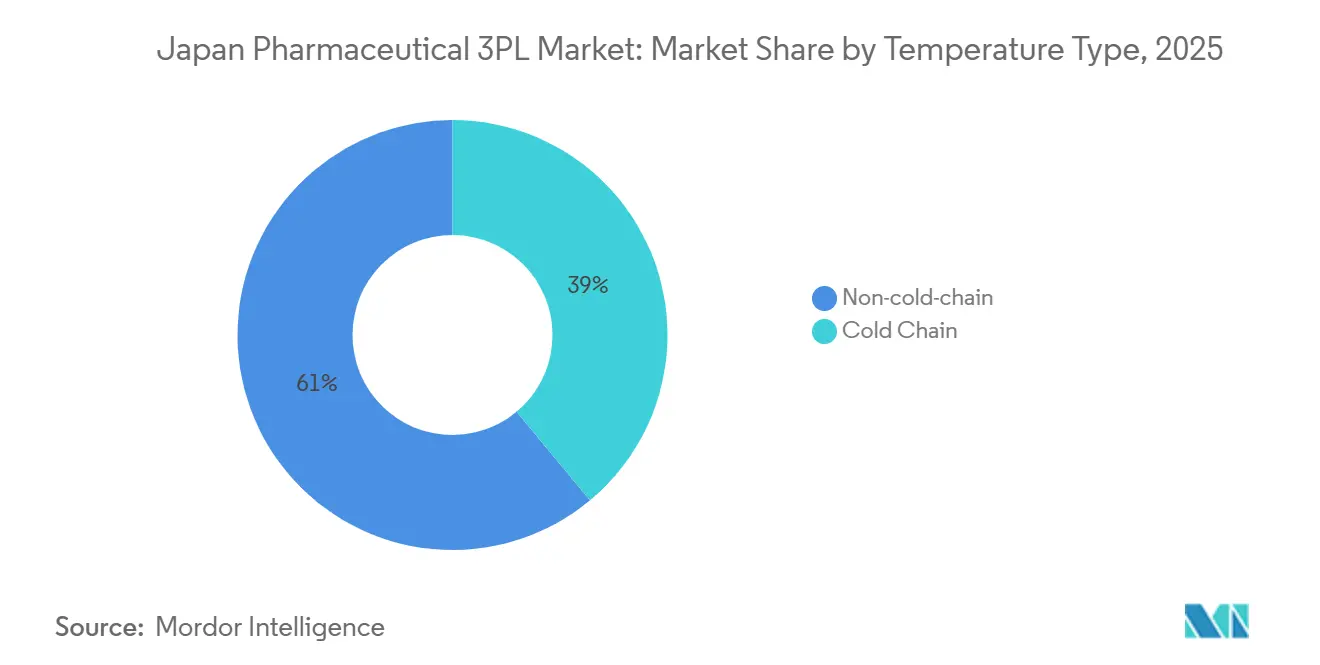

- By temperature type, Non-Cold Chain accounted for 61.05% of the Japan pharmaceutical 3PL third-party logistics market size in 2025, and cold chain is advancing at a 5.95% CAGR to 2031.

- By end user, pharmaceutical manufacturers held 44.52% share in 2025, whereas iotech and biosimilar manufacturers record the highest projected CAGR at 6.62% through 2031.

- By product type, prescription drugs captured 31.70% share in 2025, and cell and gene therapies are set to grow at a 7.10% CAGR between 2026 and 2031.

- By geography, Kanto represented 30.37% of the Japan pharmaceutical 3PL third-party logistics market size in 2025, while Kyushu and Okinawa are forecast to climb at a 5.47% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Pharmaceutical 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of cryogenic chains for advanced-therapy clinical trials | +1.1% | National, concentrated in Kanto and Kansai research hubs | Medium term (2-4 years) |

| Nationwide roll-out of cloud-based e-prescriptions boosting last-mile demand | +0.8% | Urban centers first, expanding to rural prefectures | Short term (≤ 2 years) |

| Hospital-group purchasing consolidation driving bundled logistics outsourcing | +0.7% | National, led by major metropolitan hospital networks | Long term (≥ 4 years) |

| Mandatory GS1 serialization spurring value-added tracking services | +0.5% | National, with early compliance in export-oriented manufacturers | Medium term (2-4 years) |

| Warehouse robotics adoption amid aging logistics workforce | +0.6% | Urban distribution centers, expanding to regional hubs | Long term (≥ 4 years) |

| Localization of API supply chains increasing domestic haul volumes | +0.4% | Manufacturing regions, particularly Kanto and Chubu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Cryogenic Chains for Advanced-Therapy Clinical Trials

Ultra-low temperature logistics operating at -196 °C is becoming mission-critical as regenerative medicine sponsors scale domestic trials. Mitsubishi Logistics’ Tonomachi Bio Logistics Center offers validated ranges from -150 °C to +70 °C and real-time monitoring, proving that premium pricing offsets high capital costs. METI’s backing of AGC Biologics’ JPY 50 billion (USD 320.09 million) Yokohama site further anchors domestic demand for cryogenic corridors. Marken’s first commercial CAR-T shipment between the United States and Japan illustrates the customs complexity and chain-of-custody rigor that generic freight players cannot match. Cryoport’s alliance with Mitsubishi Logistics couples global cryogenic know-how with a nationwide network, creating a high barrier to entry for smaller firms. Demand now extends beyond cell therapies to mRNA vaccines and emerging nucleic-acid drugs, reinforcing a multiyear investment cycle in dry-vapor shippers and liquid-nitrogen storage[1]Ministry of Health, Labour and Welfare, “電子処方箋,” MHLW.go.jp.

Nationwide Roll-out of Cloud-based E-Prescriptions Boosting Last-Mile Demand

The Ministry of Health, Labour and Welfare’s e-prescription system lets patients transmit scripts to any pharmacy and request home delivery, disrupting the historical wholesale-to-pharmacy flow. Sagawa Express has responded with same-day “dispensing pharmacy” routes that include temperature monitoring and tamper-evident packaging. Compliance layers covering patient privacy and prescription authenticity add documentation tasks that favor experienced 3PLs. Rural prefectures gain disproportionate access to urban pharmacies, yet sparse road networks force providers to rethink hub-and-spoke models. As penetration exceeds 70% in 2026, wholesalers must either retrofit last-mile fleets or relinquish volume to third-party specialists[2]“PHC Launches Specialty Drug Management System,” PHC Corporation, phchd.com.

Hospital-Group Purchasing Consolidation Driving Bundled Logistics Outsourcing

Centralized procurement by organizations such as the Japan Community Health Care Organization is shrinking price spreads and exposing bid-rigging, as highlighted by the JFTC’s high-profile 2020 case. Consolidated hospital networks now demand integrated deliveries across temperature zones and product classes to cut on-site inventory. Logistics partners must comply with GDP, medical-device tracking, and narcotics regulations while guaranteeing 99.9% order accuracy. Long-term contracts enable investment in dedicated docks, pick-to-light systems, and multi-compartment vehicles, yet transparent tenders cap margins and require constant productivity gains. Early movers that prove bundled capability can lock in multi-year volumes ahead of slower rivals.

Mandatory GS1 Serialization Spurring Value-Added Tracking Services

GS1 serialization obliges each package to carry a unique identifier scanned at every node. PHC Corporation’s RFID-based specialty-drug platform showcases the IT and IoT depth needed for compliance. Suzuken’s Cubixx system layers temperature alerts onto serialized data, turning compliance into a premium analytics service. Upfront spending on scanners, cloud storage, and staff training discourages small entrants, steering manufacturers toward seasoned 3PLs. Early adopters enjoy a first-mover advantage as full enforcement looms in 2027, while laggards face both deadline pressure and entrenched competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CO₂-emission caps raising replacement cost of cold-chain truck fleets | -0.7% | National, most acute in urban delivery zones | Short term (≤ 2 years) |

| Limited air-cargo slots at Narita and Haneda constraining temperature-controlled capacity | -0.5% | Kanto region, affecting international pharmaceutical trade | Medium term (2-4 years) |

| Multi-layer prefectural licensing slowing GDP warehouse expansion | -0.4% | National, particularly complex in rural prefectures | Long term (≥ 4 years) |

| Semiconductor shortage delaying delivery of reefer trucks and ULT freezers | -0.3% | National, concentrated in cold-chain infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

CO₂-Emission Caps Raising Replacement Cost of Cold-Chain Truck Fleets

Japan’s 46% emissions-reduction target for 2030 forces 3PLs to retire diesel reefers early, yet electric alternatives cost up to 40% more and suffer range constraints when refrigeration loads batteries. Urban low-emission zones accelerate compliance deadlines, compelling staged fleet swaps despite sparse charging infrastructure. Smaller carriers with limited capital may exit or be acquired, setting the stage for consolidation. Interim solutions, such as biodiesel blends and retrofit insulation, delay full electrification but add operational complexity. Fleet transition costs weigh on margins even as biologics volumes rise[3]“Efforts Toward Achieving Carbon Neutrality in Japan's Pharmaceutical Industry,” Health and Global Policy Institute, hgpi.org.

Limited Air-Cargo Slots at Narita and Haneda Constraining Temperature-Controlled Capacity

Slot allocation favoring passengers limits pharma cargo lift at Japan’s primary gateways, just as biologics and clinical-trial flows rise. Even CEIV-certified carriers struggle to secure space during peak periods, prompting price spikes and schedule volatility. Diversion to Kansai or Chubu reduces transit speed and adds trucking distance, eroding product shelf life. Airport expansion is slow due to land scarcity and community opposition, meaning structural shortfall lingers through 2031. Forwarders that pre-book block space or operate dedicated charters gain reliability advantages[4]“GMP Compliance Inspection,” Pharmaceuticals and Medical Devices Agency, pmda.go.jp.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Domestic Dominance Meets Global Momentum

Domestic Transportation Management accounted for 42.69% of the Japan pharmaceutical 3PL third-party logistics market share in 2025, supported by 206 Suzuken branches dispatching daily to 240,000 healthcare points. Extensive archipelago routing underpins scale economies, yet low margin per kilometer spurs automation and route-optimization software deployment. International Transportation Management, though smaller, is projected to grow 5.05% CAGR, buoyed by cross-border clinical-trial materials and biologics imports that demand CEIV-certified handling. Nissin’s 24-country network and four decades of pharmaceutical brokerage exemplify capabilities bridging customs, GDP, and temperature assurance. Blended providers such as ITOCHU Logistics knit inbound airfreight to nationwide truck lattices, selling seamless visibility and single-invoice simplicity. Over the forecast horizon, multinationals will outsource more investigational product flows, ensuring this global corridor continues to punch above its weight.

The Japan pharmaceutical 3PL third-party logistics market size attached to domestic services remains substantial, yet margin headroom lies in international premium lanes where high unit values justify active container leasing, data loggers, and real-time intervention teams. With serialization extending to export markets, 3PLs that integrate track-and-trace between airports and regional depots can monetize compliance dashboards. Conversely, domestic incumbents risk commoditization absent differentiation in analytics, sustainability, or bundled hospital contracts.

By End User: Biotech Complexity Commands a Growth Premium

Pharmaceutical Manufacturers retained 44.52% of the Japan pharmaceutical 3PL third-party logistics market share in 2025 thanks to stable prescription-drug pipelines and long-standing wholesaler contracts. Their distribution patterns are predictable, favoring route lock-ins and high trailer turns, yet price negotiations tied to national reimbursement reviews curb logistics fee escalation. Established 3PLs focus on service reliability and regulatory audit readiness to preserve incumbent positions.

Biotech and Biosimilar Manufacturers are projected to post a 6.62% CAGR through 2031, outpacing all other end-user groups as regenerative-medicine pipelines scale and CDMOs multiply. These firms outsource almost every logistics touchpoint, from cryogenic tissue collection to clinical-trial drug return, lifting the Japan pharmaceutical 3PL third-party logistics market size tied to specialist services. Providers must demonstrate chain-of-custody integrity, rapid deviation response, and redundant power for ULT freezers to win contracts. Success with biotech cargo often seeds follow-on work in commercial distribution once products receive approval, making early engagement critical.

By Temperature Type: Cold Chain Emerges as Value Engine

Non-Cold Chain still comprises 61.05% of the Japan pharmaceutical 3PL third-party logistics market size in 2025, driven by high-volume oral solids and OTC lines. Freight rates in this segment face deflationary pressure as hospital buyers squeeze wholesalers. Cold Chain revenue, however, is forecast to rise at 5.95% CAGR thanks to biosimilar launches and the widening pool of temperature-sensitive biologics. Cryogenic lanes supporting cell therapies command surcharges exceeding 200% of ambient tonnage, offsetting lower volumes. Shibamata Unyu’s GPS-enabled -196 °C service underlines the specialized infrastructure newcomers must replicate

Market leaders invest in multi-compartment trucks, phase-change material totes, and predictive maintenance for ULT freezers. Nippon Express’s tie-up with Otsuka on CO₂-reduced isothermal containers indicates that sustainability will differentiate bidders in cold chain tenders. As biologics penetration tops 40% of prescription spend by 2031, a bifurcation emerges: scale operators double down on cold chain centers of excellence, whereas small carriers gravitate toward ambient regional routes.

By Product Type: Regenerative Medicine Reshapes Infrastructure Strategy

Prescription Drugs accounted for 31.70% of the Japan pharmaceutical 3PL third-party logistics market share in 2025, reflecting continued reliance on small-molecule therapies under government price controls. Logistics for this class emphasize cost efficiency, high drop density, and serialization compliance at the case level. Margin pressure encourages route optimization and robotics-enabled picking to shave labor minutes per order.

Cell and Gene Therapies are forecast to expand at a 7.10% CAGR over 2026-2031, transforming the Japan pharmaceutical 3PL third-party logistics market size dedicated to ultra-low temperature lanes. Each shipment can be patient-specific, time-critical, and valued in the six-figure-USD range, demanding liquid-nitrogen dry shippers, active dataloggers, and 24 / 7 intervention teams. Only a handful of providers run validated -196 °C corridors today, allowing them to price services at substantial premiums. As regenerative-medicine capacity in Yokohama and Kobe ramps up, the supporting cryogenic network will widen, spurring fresh CapEx cycles in storage dewars, vapor shippers, and GMP packaging suites.

Geography Analysis

Kanto generated 30.37% of the Japan pharmaceutical 3PL third-party logistics market size in 2025, anchored by Tokyo-area manufacturing plants, research universities, and the PMDA headquarters. Mitsubishi Logistics alone operates more than 100,000 m² of GDP-compliant space in Misato and Shin-Kiba, feeding 24-hour hospital demand. Yet premium land prices, chronic highway congestion, and stricter emission zones inflate the cost per pallet. Airport slot scarcity at Narita and Haneda further complicates biologics exports, nudging shippers toward port-based sea-air combinations via Yokohama.

Kyushu and Okinawa post the fastest 5.47% CAGR as manufacturers seek lower real-estate costs and improved proximity to China and ASEAN markets. Otsuka’s new Tokushima syringe plant underscores the southward drift, while Fukuoka’s port accelerates cold chain imports from Korea and Singapore. Logistics providers respond by adding cross-docks in Kitakyushu and Miyazaki, leveraging land availability to build large-footprint GDP warehouses with solar-powered HVAC.

Kansai remains Japan’s second hub, sustained by Osaka-Kobe manufacturing clusters and LOGISTEED’s 2024 GDP center that enhances throughput for biopharma exporters. Chubu functions as a transit corridor, with Nagoya's road junctions linking eastern and western networks. Hokkaido and Tohoku gain resilience investments such as earthquake-proof racking and dual-power backup, learning from the 2011 disaster. Chugoku and Shikoku stay niche, served via spoke routes radiating from Kansai depots to balance service coverage against truck utilization.

Competitive Landscape

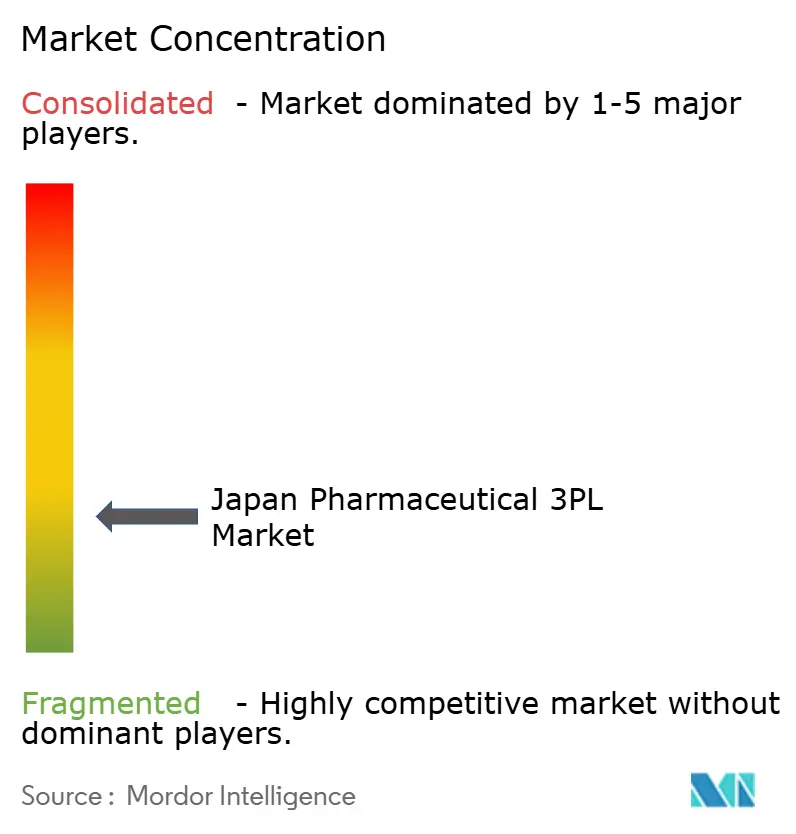

The Japan pharmaceutical 3PL third-party logistics market hosts a moderately fragmented field where the top five players control just under 55% of revenue, yielding a competitive yet consolidating arena. Nippon Express, Yamato Transport, and Sagawa Express leverage nationwide depots and proprietary IT to compete for hospital tenders, while Mitsubishi Logistics, LOGISTEED, and ITOCHU target high-margin cells-to-patient corridors through cryogenic capacity and serialization dashboards. Regulatory barriers, such as GDP accreditation, prefectural warehouses licenses, and serialization data platforms, impose six-figure entry costs, sheltering incumbents.

Technology adoption is quickly separating leaders from laggards. DHL Supply Chain’s robotics rollout cuts pick times by 30%, and Suzuken automates case sorting to offset labor scarcity. Sustainability also drives differentiation; Nippon Express fields hybrid reefers and biodegradable coolants under CO₂-reduction contracts with pharma sponsors. Competitive intensity heightens around bundled hospital contracts where the lowest compliant bid wins, compressing ambient margins but fortifying volume streams. Specialized niches CAR-T cryo-logistics, trial material export, and direct-to-patient e-pharmacy fulfillment offer double-digit margins but demand multi-million-dollar CapEx that only scale players can underwrite.

Looking ahead, acquisitions of regional cold-chain fleets and vertical alliances with CDMOs are expected as players chase end-to-end control. The 2020 JFTC penalties for bid collusion signal heightened antitrust oversight, pressing firms to strengthen compliance cultures while refining price-to-value narratives to hospital consortia and biotech upstarts alike.

Japan Pharmaceutical 3PL Industry Leaders

Suzuken Group

DHL Group

Kuehne+Nagel

SF Express (KEX-SF)

Nippon Express Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TOHO Pharmaceutical launched the Haneda Packaging Center near Tokyo’s airport to streamline one-stop supply chains.

- February 2025: Mitsubishi Logistics’ United States unit, Cavalier Logistics, opened a GMP warehouse in North Carolina, extending end-to-end support for Japanese biopharma exporters.

- November 2024: Nippon Express added GDP-certified nodes in Philadelphia and Budapest, lifting its global pharma network to 36 sites across 25 countries.

- May 2024: LOGISTEED opened the Kansai III Medical Distribution Center, a GDP-compliant hub boosting capacity for biologics and trials in western Japan.

Japan Pharmaceutical 3PL Market Report Scope

By Service Type

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing and Distribution (VAWD) |

By Temperature Type

| Cold Chain |

| Non-cold Chain |

By End User

| Pharmaceutical Manufacturers |

| Biotech and Biosimilar Manufacturers |

| Clinical Research and Trial Sponsors |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| E-pharmacies and Direct-to-Patient Services |

| Others |

By Product Type

| Prescription Drugs |

| OTC and Consumer Health Products |

| Biopharmaceuticals and Biosimilars (ex-CGT) |

| Cell and Gene Therapies |

| Vaccines and Blood-derived Products |

| Veterinary Pharmaceuticals and Animal Health Products |

| Medical Devices, Diagnostics and Combination Products |

| Clinical-trial Materials (Investigational Medicinal Products) |

| Others |

By Region (Japan)

| Hokkaido and Tohoku |

| Kanto |

| Chubu |

| Kansai |

| Chugoku and Shikoku |

| Kyushu and Okinawa |

| By Service Type | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing and Distribution (VAWD) | ||

| By Temperature Type | Cold Chain | |

| Non-cold Chain | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotech and Biosimilar Manufacturers | ||

| Clinical Research and Trial Sponsors | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| E-pharmacies and Direct-to-Patient Services | ||

| Others | ||

| By Product Type | Prescription Drugs | |

| OTC and Consumer Health Products | ||

| Biopharmaceuticals and Biosimilars (ex-CGT) | ||

| Cell and Gene Therapies | ||

| Vaccines and Blood-derived Products | ||

| Veterinary Pharmaceuticals and Animal Health Products | ||

| Medical Devices, Diagnostics and Combination Products | ||

| Clinical-trial Materials (Investigational Medicinal Products) | ||

| Others | ||

| By Region (Japan) | Hokkaido and Tohoku | |

| Kanto | ||

| Chubu | ||

| Kansai | ||

| Chugoku and Shikoku | ||

| Kyushu and Okinawa | ||

Key Questions Answered in the Report

What is the current value of the Japan pharmaceutical 3PL third-party logistics market?

The market is valued at USD 4.43 billion in 2026.

How large will Japan’s pharmaceutical 3PL outsourcing spend be by 2031?

It is forecast to reach USD 5.55 billion by 2031, reflecting a 4.59% CAGR from 2026.

Which logistics segment is growing fastest?

International Transportation Management is forecast at a 5.05% CAGR as Japanese firms move more clinical-trial materials and APIs across borders.

Why is cold chain attracting disproportionate investment?

Biosimilars and cell-based therapies require strict 2-8 °C or cryogenic conditions, driving cold-chain revenue growth at 5.95% CAGR despite lower shipment volumes.

What regulation is reshaping last-mile delivery models?

The nationwide rollout of cloud-based e-prescriptions enables direct-to-patient shipping, increasing demand for flexible, GDP-compliant home-delivery networks.

How are emission targets affecting logistics fleets?

CO₂ caps require accelerated replacement of diesel reefers with electric or hybrid units, raising capital costs and encouraging fleet consolidation.

Page last updated on: