Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 43.48 Billion |

| Market Size (2026) | USD 44.37 Billion |

| Market Size (2031) | USD 50.44 Billion |

| Growth Rate (2026 - 2031) | 2.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Defense Market Analysis by Mordor Intelligence

The Japan defense market size is expected to grow from USD 43.48 billion in 2025 to USD 44.37 billion in 2026 and is forecast to reach USD 50.44 billion by 2031 at a 2.60% CAGR over 2026-2031. Heightened threats from China and North Korea, Cabinet-endorsed spending that rises toward 2% of GDP, and an accelerated shift toward counter-strike capabilities are reshaping the Japan defense market in ways unseen since the Cold War. The growing procurement of hypersonic interceptors, the fielding of private 5G networks for real-time command, and deeper integration into multilateral programs such as GCAP, as well as a prospective AUKUS Pillar II foothold, all broaden the market’s technology base. Foreign Military Sales remain indispensable for high-end systems even as yen weakness inflates dollar-denominated contracts, making cost-share partnerships more attractive. Domestic primes continue to capture sovereign programs, yet a wave of smaller firms is winning niche awards in counter-drone and directed-energy applications, intensifying competition across the Japan defense market.

Key Report Takeaways

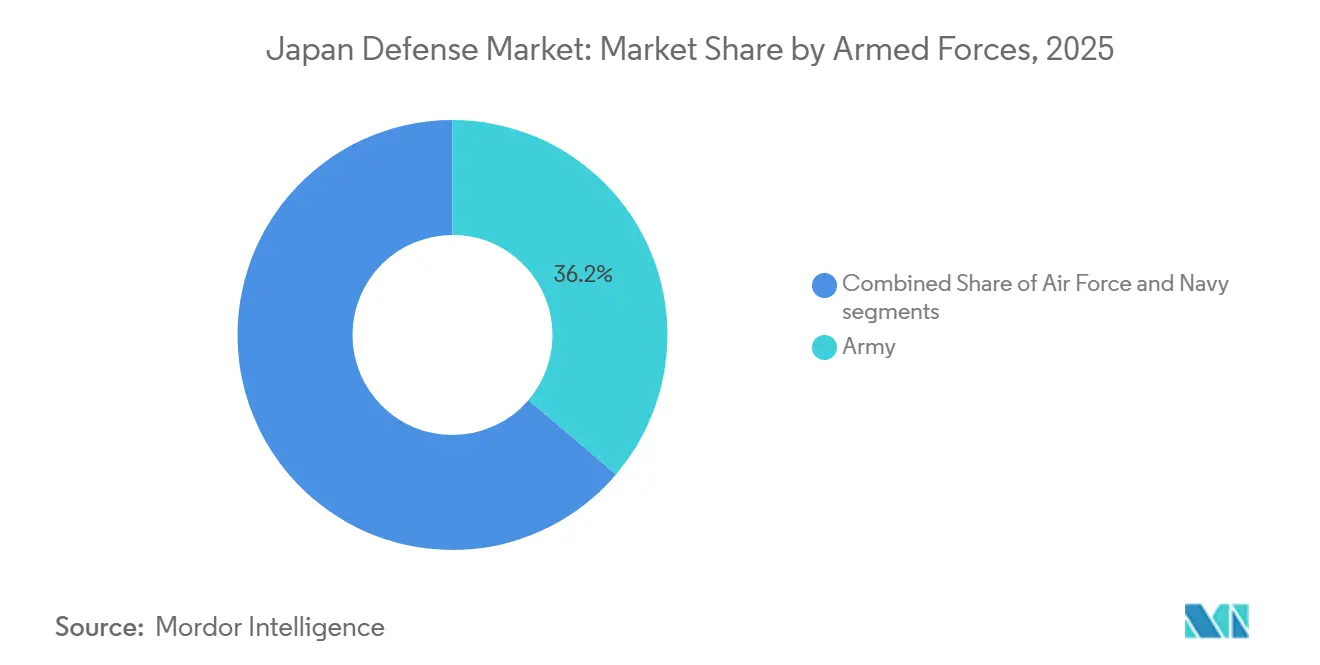

- By armed forces, the Army led with 36.24% of Japan defense market share in 2025, whereas the Air Force is forecast to grow at a 5.67% CAGR through 2031, the fastest among the services.

- By type, weapons and ammunition accounted for 32.11% of the Japan defense market size in 2025, while unmanned systems are forecast to grow at a 7.32% CAGR through 2031.

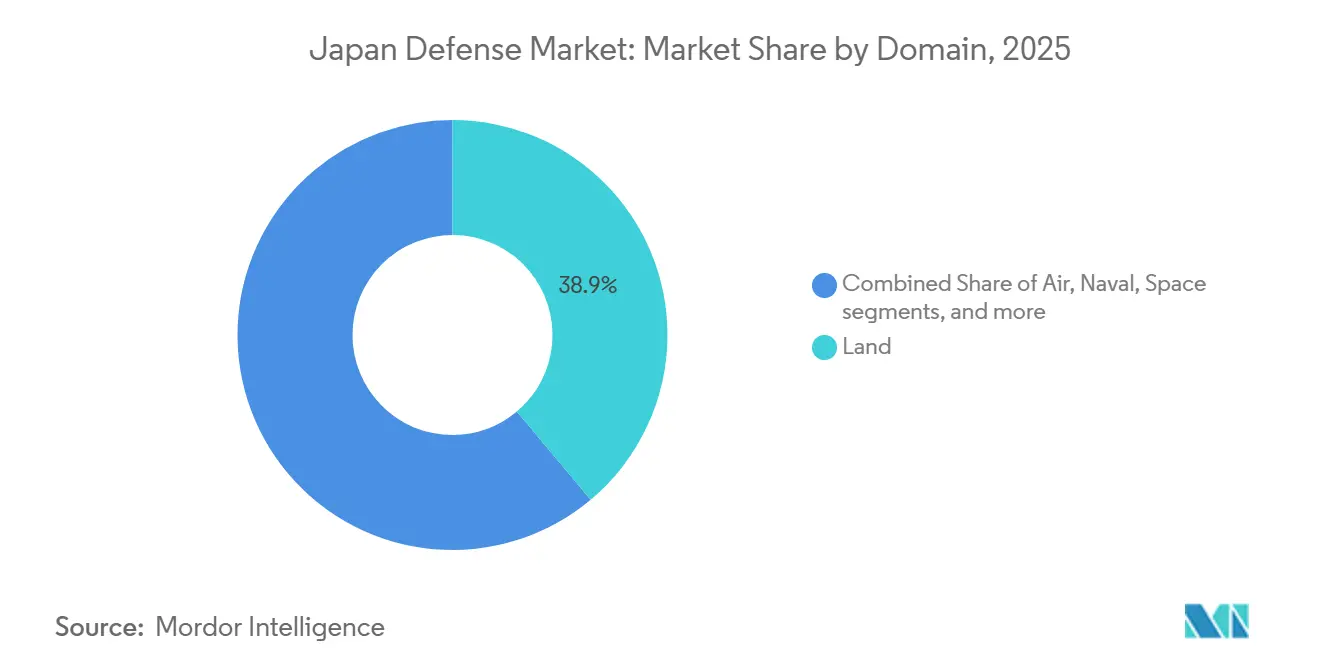

- By domain, land operations held a 38.89% share of the Japan defense market size in 2025, whereas space activities are projected to grow at a 6.57% CAGR through 2031.

- By procurement nature, indigenous production accounted for 60.10% of Japan's defense market share in 2025; foreign procurement is forecast to grow at a 3.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened security risks in the Indo-Pacific region | +0.8% | National, focused on southwestern approaches | Medium term (2-4 years) |

| Significant increase in long-term defense spending commitments | +0.6% | National with allied spillovers | Long term (≥ 4 years) |

| Rapid advancement of missile and hypersonic strike capabilities | +0.5% | National, stand-off ranges | Medium term (2-4 years) |

| Deepening participation in global defense collaboration initiatives | +0.4% | Global, led by US, UK, Italy, Australia | Long term (≥ 4 years) |

| Demographic pressures fueling growth in autonomous and unmanned systems | +0.3% | National, early use on remote islands | Medium term (2-4 years) |

| Deployment of private 5G networks across defense installations | +0.2% | National, key command centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Security Risks In The Indo-Pacific Region

China executed 1,200 incursions into Japan’s ADIZ during fiscal 2024, up 15%, while North Korea launched 23 ballistic missiles, some crossing Japanese airspace, prompting Tokyo to accelerate integrated air and missile defense architectures.[1]“Defense of Japan 2024,” Ministry of Defense Japan, mod.go.jp The National Security Strategy, revised in 2022, identifies China as “the greatest strategic challenge,” unlocking counter-strike options and underpinning a December 2024 purchase of 400 Tomahawk missiles. Taiwan-strait contingency planning places the Nansei chain at the front line, driving investments in hardened depots and distributed munitions. The sustained nature of these threats secures multi-year appropriations through 2031. Consequently, the Japan defense market records persistent demand for early-warning satellites, long-range fires, and mobile air-defense units.

Significant Increase In Long-Term Defense Spending Commitments

The FY2023-2027 plan allocates JPY 43 trillion (USD 272.34 billion), 56% above the prior quinquennium, backed by tax-linked financing that isolates the defense top line from annual fluctuations. Spending equal to 2% of GDP would increase annual outlays to JPY 11 trillion (USD 69.67 billion) by 2027. Institutional reforms, most notably the Acquisition, Technology & Logistics Agency, trimmed procurement lead times by 18 months and enabled serial production savings, as evidenced by a 12% per-hull cost drop for the Mogami-class frigate. These measures embed a funding trajectory that sustains the Japan defense market well into the 2030s.

Rapid Advancement of Missile and Hypersonic Strike Capabilities

Tokyo and Washington began co-developing the sea-based Glide Phase Interceptor in January 2025, aiming for IOC by 2030. Mitsubishi Heavy Industries delivered an extended-range Type-12 missile in March 2025, boosting the reach from 200 km to beyond 1,000 km. A Hypersonic Defense Unit stood up in Okinawa the following month, linking PAC-3 MSEs with Aegis-derived command networks. The Ministry’s 2024 white paper warned that pre-upgrade missile stocks could be exhausted within 72 hours of intense conflict, validating the need for deep-magazine procurement. These programs elevate the technology ceiling of the Japan defense market and draw sustained vendor interest.

Deepening Participation In Global Defense Collaboration Initiatives

Japan’s GCAP partnership with the UK and Italy advances a sixth-generation fighter slated for 2035, distributing cost and risk across three continents. Tokyo is also preparing to join selected AUKUS Pillar II streams following an invitation in February 2025. Exercise Malabar 2024 brought together Quad navies in their largest iteration, enhancing multi-domain interoperability. Shared development reduces per-unit costs and broadens export prospects, positioning the Japan defense market as a hub for collaborative high-technology programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High public debt levels constraining long-term budget expansion | -0.5% | National, central-government focus | Long term (≥ 4 years) |

| Limited industrial capacity and skilled workforce availability | -0.4% | National, precision manufacturing and software | Medium term (2-4 years) |

| Currency depreciation driving up import-related procurement costs | -0.3% | National, all foreign-sourced systems | Short term (≤ 2 years) |

| Environmental pushback against base development and live-fire training | -0.2% | Regional, Okinawa and dense prefectures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Public Debt Levels Constraining Long-Term Expansion

Government debt reached 264% of GDP in 2025, with debt service absorbing 23% of the general budget. Sustaining a 2% of GDP defense line post-2027 requires higher taxes or welfare cuts, both of which are politically delicate. Fitch revised Japan’s outlook to negative in August 2024, warning of “limited fiscal space to absorb additional spending shocks”. Although the current five-year program is funded, procurement beyond 2027 could be reduced, which would moderate growth in the Japan defense market.

Environmental Pushback Against Base Development And Live-Fire Training

Henoko’s replacement facility now faces a 2035 completion date and costs triple the 2018 plan, driven by lawsuits and seabed issues. The 2019 and 2024 Okinawa referendums recorded opposition above 60% to new construction. Higashi-Fuji reduced artillery exercises by 35% in 2024 following concerns from residents over noise and safety.[2]Ryusei Takahashi, “Japan Training Range Restrictions Reduce Artillery Exercises,” Asahi Shimbun, asahi.com Relocating drills to remote Hokkaido incurs higher logistics costs and reduces training tempo, thereby throttling readiness investments in the Japan defense market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armed Forces: Air Modernization Drives Outlays

The Japanese Air Self-Defense Force (JASDF) is on course for a 5.67% CAGR through 2031, eclipsing ground and maritime growth. It fields 147 F-35s, integrates 400 Tomahawk missiles, and co-develops the GCAP fighter, with each program contributing to the development of the Japan defense market, which is allocated to air modernization. A KC-46A tanker fleet further extends reach beyond 2,000 km, while the Hypersonic Defense Unit anchors missile-defense resources in Okinawa.

The Army retained a 36.24% stake in 2025 but shifted from tank-centric formations to agile island-defense brigades, slowing Type-10 production to eight units annually. Maritime forces commission Taigei-class submarines equipped with Li-ion batteries, which double submerged endurance. These reallocations reinforce a balanced yet air-skewed Japan defense market.

By Type: Automation Outpaces Munitions

Weapons and ammunition dominated the 2025 baseline at 32.11%; however, unmanned systems are set for a 7.32% CAGR, the swiftest ascent across categories. MQ-9B SeaGuardians deliver 30-hour patrol windows, while Subaru’s VTOL drone advances carrier-based ISR, tightening the loop between sensors and shooters.[3]Aaron Mehta, “Japan Procures MQ-9B SeaGuardian Drones,” Defense News, defensenews.com These gains push the Japan defense market toward autonomous operations.

C4ISR and EW enjoy steady inflows as private 5G and AI-powered fusion platforms proliferate. Personnel training and protection receive VR simulators and upgraded body armor, though their share remains modest. Space and cyber systems, buoyed by QZSS satellite launches, contribute incremental yet strategic value to the broader Japan defense market.

By Domain: Space Ascends From Support To Center Stage

Land retained 38.89% of 2025 outlays, but Space now carries the fastest growth trajectory at 6.57% CAGR. Eight-satellite QZSS arrays lift Japan’s autonomy from GPS dependence, and a 200-person Space Operations Group monitors orbital threats. These investments elevate Space from an enabler to a frontline domain within the Japan defense market.

Air domain budgets fund F-35, GCAP, and E-2D Hawkeye expansions, while naval allocations modernize Aegis destroyers and commission Taigei submarines with Li-ion propulsion. Cyber-electromagnetic initiatives add offensive tools and Five-Eyes partnerships, earning a growing slice of the Japan defense market.

By Procurement Nature: Balancing Sovereignty And Interoperability

Indigenous production led with 60.10% in 2025, buttressed by Type-12 missiles and Mogami-class frigates whose serial builds shave unit costs 12%. Foreign Procurement edges ahead at a 3.21% CAGR as interoperability demands F-35s, KC-46As, and Tomahawks despite yen-driven price surges. Revised transfer rules enabling licensed PAC-3 exports may allow domestic yards to scale, reinforcing the Japan defense market’s hybrid sourcing model.

Geography Analysis

Investment gravitates toward the southwestern Nansei chain, where new radar sites, Type-12 batteries, and replenishment depots harden defenses against a Taiwan-related contingency. The Hypersonic Defense Unit’s Okinawa activation signals the pivot’s intensity. Hokkaido’s role shifts to training and cold-weather drills as tank inventories are expected to fall by 30% from 2025 levels.

Tokyo hosts joint command hubs and the Bilateral Operations Coordination Center, which integrates US-Japan air-defense data in real-time. Exercise Malabar 2024 in the Philippine Sea highlights the region's reach, while anticipated AUKUS collaborations are expected to expand technology pipelines. Such alliances enlarge the Japan defense market beyond national borders into a multilateral ecosystem.

Regional politics impose uneven constraints. Okinawa, which holds 70% of US facilities, delays Henoko replacement until 2035 amid a projected cost tripling. Higashi-Fuji’s curtailed drills illustrate metropolitan pushback. These frictions add compliance costs and elongate project timelines across the Japan defense market.

Regulatory Landscape

Japan's defense policy and procurement environment is anchored by the 2022 National Security Strategy, National Defense Strategy, and Defense Buildup Program. The Ministry of Defense (MOD) and the Acquisition, Technology and Logistics Agency (ATLA) set acquisition priorities, program governance, and industrial participation rules. A key 2026 change was the April 21, 2026 amendment to the Three Principles on Transfer of Defense Equipment and Technology, which broadened permissible pathways for equipment and technology transfers tied to international joint development and production, and specified cooperation purposes. It strengthens the formal framework for export-linked collaboration while maintaining treaty and conflict-related restrictions.

Industrial and procurement rules increasingly treat the production and technology base as part of national defense capability. Measures under the Defense Production Base Strengthening Act (effective October 2023) and the ATLA industrial policy package (including the April 2023 profit-structure approach benchmarking corporate efforts against commercial-sector norms) support supplier investment, cost transparency, and life-cycle management. Within this framework, policy continues to prioritize domestic production for stable supply and security, while allowing international joint development when domestic-only acquisition is not viable, reinforcing the market's hybrid model of indigenous programs and allied interoperability-driven procurement.

Value Chain Analysis

Japan's defense value chain is organized around MOD requirements definition, ATLA-led acquisition and program management, and delivery by domestic primes supported by multi-tier subcontractors covering materials, precision machining, electronics, propulsion, and software. Industrial resilience measures have become more visible in the chain, including government support targeting critical products and capacity expansion at the supplier level. Oversight of prime-subcontractor relationships is also tightening, with new subcontracting guidelines released in March 2025 aimed at shaping transaction practices between major contractors and their supply base.

Upstream constraints and allied integration are shaping sourcing and throughput. Reuters reporting in 2024 highlighted bottlenecks in US-Japan Patriot PAC-3 related production plans linked to limited availability of key proprietary components. This illustrates how external dependencies can throttle output even when local assembly capability exists. At the same time, localized content pathways are expanding through collaborations such as Fujitsu's May 2025 move to manufacture power supply components for Lockheed Martin's AN/SPY-7(V)1 radar used for Japan's Aegis System Equipped Vessels (ASEV). Government funding for reinforcement of the defense production base, about JPY 99.6 billion in FY2025 and about JPY 101 billion in FY2026, also supports scaling of manufacturing, sustainment, and repair capacity across the chain.

Competitive Landscape

The top five domestic primes account for roughly 55% of indigenous orders, with no single firm exceeding 18%, placing the Japan defense market in a moderate-concentration band. Lockheed Martin, Boeing, and RTX dominate the market for imported high-end systems but rely on local partners. Notably, 40% of F-35 final assembly takes place at Mitsubishi Heavy Industries' Nagoya site, which sustains approximately 1,200 skilled positions.[4]“Lockheed Martin F-35 Final Assembly in Japan Sustains 1,200 Jobs,” Lockheed Martin, lockheedmartin.com

White-space niches emerge in counter-drone and directed-energy areas where Subaru and ShinMaywa secure initial contracts. Vendors now emphasize software-defined and open-architecture solutions, typified by NEC’s private 5G mesh and Mitsubishi Electric’s post-quantum encryption. Export-rule loosening allows PAC-3 interceptor sales abroad, yet 2026 export volumes remain modest, signaling room for growth in the Japan defense market.

Japan Defense Industry Leaders

Mitsubishi Heavy Industries, Ltd.

Kawasaki Heavy Industries, Ltd.

NEC Corporation

Toshiba Corporation

IHI AEROSPACE Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Active policy programs and budget lines are creating identifiable whitespace in unmanned and distributed defense architectures, missile production, and air-space integration. In the FY2026 initial budget, Japan allocated JPY 128.7 billion toward establishing a SHIELD posture using unmanned assets (including USVs and UUVs) by FY2027. This supports opportunities for domestic platforms, mission systems, autonomy software, and C2 integration. The same policy push is reinforced by July 2026 Liberal Democratic Party economic and fiscal guidelines that prioritized defense industry revival and drone mass production, which points to near-term demand for scalable manufacturing, testing, and supply-chain localization across small UAS and counter-UAS ecosystems.

Space and air-domain reorganization and program schedules provide additional near-term demand anchors for sensors, communications, and secure networking. The MOD's plan to reorganize the JASDF into an Air and Space Defense Force in FY2026 elevates requirements for space-domain awareness, resilient communications, and cross-domain data fusion. On the industrial side, preparations for Engineering Test Satellite 9 are underway for completion within FY2026, and development of the ship-type Type-12 surface-to-ship missile is scheduled for completion by the end of FY2026. Together, these timelines create procurement and integration opportunities across guidance, propulsion, test instrumentation, and naval fire-control interfaces, with ATLA and domestic primes positioned to pull specialized SMEs into certified supply roles.

Recent Industry Developments

- June 2026: Kawasaki Heavy Industries signed an MOU with Airbus Defence and Space to explore a Japanese anti-submarine warfare (ASW) variant of the Eurodrone. The step connects a European MALE UAV baseline with Japan-specific maritime mission requirements, widening options for long-endurance ISR and ASW support. It also signals a deeper pattern of cross-border platform adaptation that can pull Japanese sensors and C2 components into a partnered development path.

- April 2026: NEC Corporation signed a contract with the Commonwealth of Australia to supply nine types of defense equipment, including surface ship sonars and the UNICORN integrated communications antenna, for the SEA3000 frigate program. The award expands NEC's defense exports from domestic programs into allied naval production, supporting scale-up in certified manufacturing and long-term in-service support. It also strengthens Japan-Australia industrial linkages around shipboard C4ISR and integrated masts.

- July 2024: Reuters reported that the US-Japan Patriot missile production plan faced a component roadblock tied to Boeing-supplied parts, highlighting a bottleneck in scaling PAC-3 related output. The constraint underscored how limited availability of proprietary subcomponents can slow co-production ambitions even when assembly capacity exists. For Japan, it reinforced the value of supply-chain resilience measures and domesticization efforts for critical inputs where feasible.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan defense market is defined as the total value of Japan Self-Defense Forces-related spending on defense capabilities, mainly equipment procurement and modernization programs, including associated upgrades and technology development that supports those capabilities.

Scope exclusions: This sizing excludes purely civilian aerospace activity and non-defense public safety programs that are not funded and managed as defense procurement.

Segmentation Overview

- By Armed Forces

- Air Force

- Army

- Navy

- By Type

- Personnel Training and Protection

- C4ISR and Electronic Warfare (EW)

- Vehicles

- Weapons and Ammunition

- Unmanned Systems

- Space and Cyber Systems

- By Domain

- Land

- Air

- Naval

- Space

- Cyber and Electromagnetic Spectrum

- By Procurement Nature

- Indigenous Production

- Foreign Procurement

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with official budget and policy signals so the demand story stayed grounded in what Japan can actually fund and procure. We relied on public sources such as Japan Ministry of Defense budget materials and program documents, Cabinet level security strategy releases, parliamentary publications, and defense-related white papers.

To cross-check volumes and categories, we also used non-paywalled references such as SIPRI style defense-spend series, UN Comtrade trade statistics for relevant defense-linked categories (where applicable), patent databases for directional R&D activity, and peer-reviewed journals that discuss force structure and capability needs. Company filings, investor presentations, and reputable press reporting were then used to validate delivery timelines, upgrade cycles, and supplier and integrator capacity signals, supported by a paid subscription that provides company financials and news context, and another paid subscription focused on defense related market information. These sources are illustrative only, and many other public and paid references were used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with procurement and program stakeholders, supply chain participants, and domain specialists who track air, land, and maritime capability priorities in Japan. Their input was used to confirm which programs are counted in-market, align price and delivery assumptions, and pressure-test scenario choices against real procurement timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 50% | Functional/Unit leaders: 39% | |

| Smaller Players: 17% | Managers: 48% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where Japan defense budget direction and published procurement allocations are reconstructed into an addressable equipment and modernization pool, and then adjusted for timing and execution. To keep the totals realistic, results were corroborated with selective bottom-up approximations such as sampled program values, typical unit costs by platform class, and supplier and integrator channel checks, and then gaps were normalized where public details were incomplete.

Key model inputs included Japan defense budget growth and stated multi-year funding plans, procurement share versus operations share, delivery schedules for major platforms, upgrade and mid-life modernization cycles, and R&D intensity for areas like sensors, missile defense, and unmanned systems. Forecasting leaned on scenario analysis informed by expert views, since defense spending can shift with policy decisions, exchange-rate effects, and procurement slippage, and these drivers may not move in lockstep with historical trends.

Data Validation & Update Cycle

Outputs were checked against independent signals such as published defense spending totals, visible contract awards, and known delivery milestones, and then reviewed for year-to-year jumps that do not match procurement reality. When variances appeared, the assumptions behind unit pricing, program phasing, and inclusion boundaries were revisited, and respondents were re-contacted if the gap was material.

Before sign-off, the model and narrative go through multi-step internal reviews so calculation logic and scope decisions stay consistent across years. Reports are refreshed annually, with interim updates when major budget changes, strategy announcements, or large procurement decisions materially change the outlook, followed by a final pre-delivery pass to ensure clients receive the latest view.

Mordor Intelligence's Japan Defense Market Sizing Compared With Other Published Estimates

Published estimates for Japan defense can vary even when they use similar labels, because the counted items and the timing basis are often not the same. Differences typically come from whether the number represents defense expenditure, procurement value only, or a broader defense and security spend that mixes adjacent activities.

By tracking procurement-linked budget lines, program phasing, and currency timing, Mordor Intelligence keeps the estimate focused on equipment and modernization value rather than the full defense spend total, which reduces double counting when operations and personnel costs are blended into a single headline number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 44.37 B (2026) | |

| Industry Publisher A | USD 36.40 B (2025) | Uses a different base year and can apply a broader defense market framing that may blend categories differently, which shifts the procurement-only share and the implied pricing path. |

| Trade Media B | USD 54.20 B (2025) | Represents defense expenditure rather than an equipment and modernization market, so operating costs and personnel-related outlays can be included, which lifts the total versus procurement-focused sizing. |

The spread in the table is mostly explained by what is being counted and when it is being counted, not by small math differences. When the scope is kept tied to procurement and modernization signals, and then checked against program timing and visible awards, the market size becomes easier to trace and repeat year after year.

Key Questions Answered in the Report

How large is the Japan defense market in 2026?

The Japan defense market is valued at USD 44.37 billion in 2026 with a forecast 2.60% CAGR to 2031.

Which segment is growing fastest within Japan’s forces?

The JASDF, supported by F-35 expansion and GCAP development, is projected to rise at a 5.67% CAGR through 2031.

Why are unmanned systems gaining share in Japanese procurement?

Persistent demographic decline and recruitment gaps drive automation, lifting the unmanned systems segment at a 7.32% CAGR.

How does yen depreciation affect defense imports?

A weaker JPY raised Foreign Military Sales (FMS) costs by 28% between 2022 and 2025, delaying some tank and helicopter programs.

Page last updated on: