Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

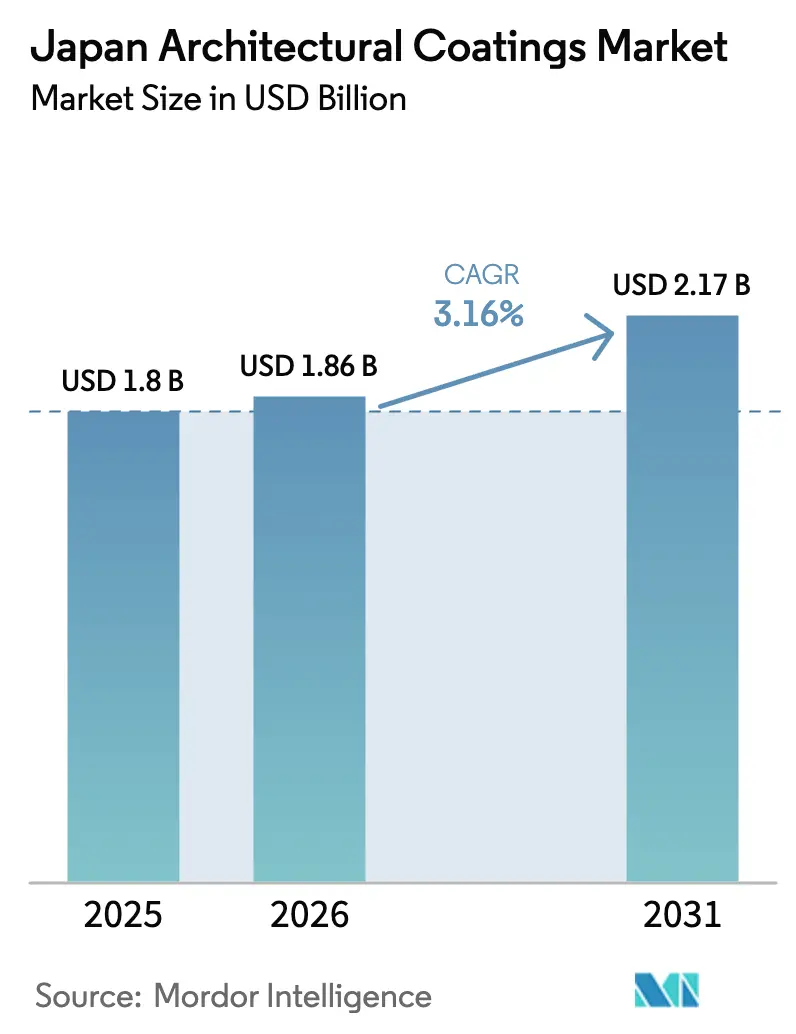

| Base Year Market Size (2025) | USD 1.8 Billion |

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Architectural Coatings Market Analysis by Mordor Intelligence

The Japan Architectural Coatings Market size is expected to grow from USD 1.8 billion in 2025 to USD 1.86 billion in 2026 and is forecast to reach USD 2.17 billion by 2031 at 3.16% CAGR over 2026-2031. Steady growth relies on resilient renovation demand, tightening energy- and VOC regulations, and municipal subsidies that favor heat-reflective technologies. Demographic shifts limit new construction, but an aging housing stock—now averaging 30 years in many suburbs—keeps maintenance spending elevated. The rapid adoption of water-borne coatings, now accounting for three-quarters of total demand, underscores a technology migration toward low-emission systems. Meanwhile, volatile titanium dioxide and acrylic monomer prices put pressure on margins, pushing manufacturers to secure raw material supplies through vertical integration and strategic alliances.

Key Report Takeaways

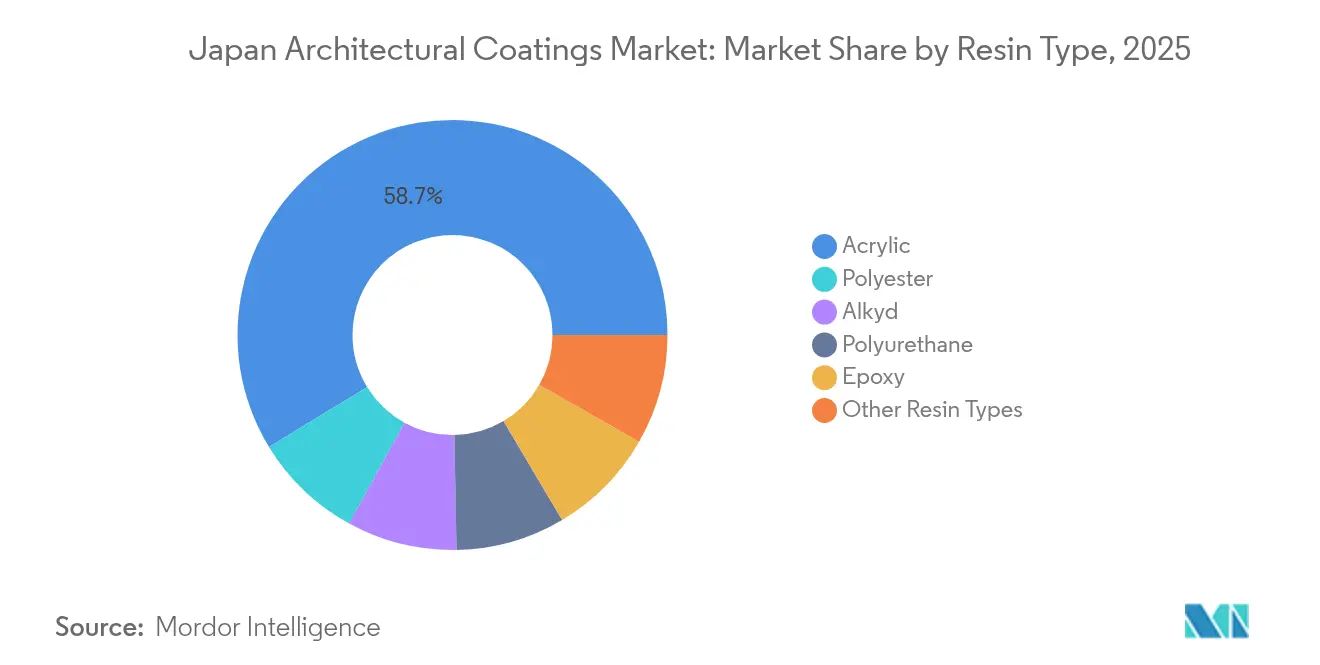

- By resin type, acrylic products led with 58.72% of the Japan architectural coatings market share in 2025 and are projected to advance at a 3.49% CAGR through 2031.

- By technology, water-borne systems commanded 76.05% of the Japan architectural coatings market size in 2025 and are projected to advance at a 3.27% CAGR through 2031.

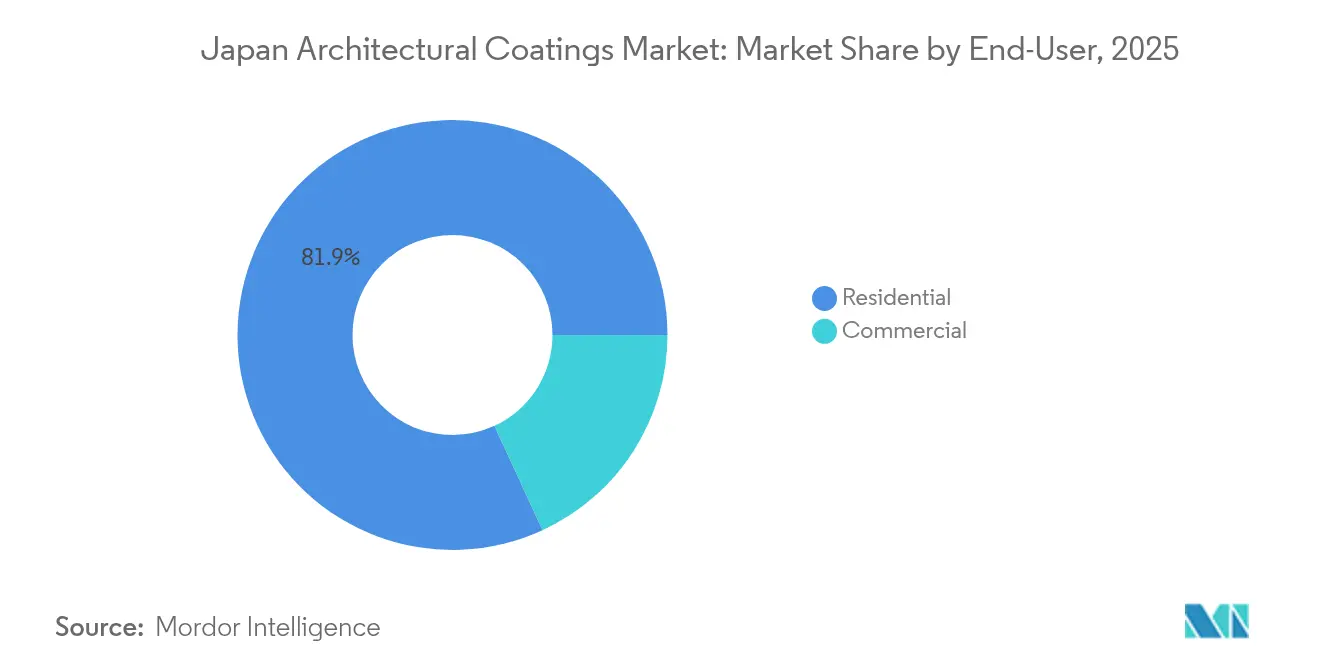

- By end-user, the residential segment accounted for 81.88% of demand within the Japan architectural coatings market in 2025, and is forecast to post the fastest growth at 3.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Energy-and-VOC Regulations accelerating water-borne adoption | +0.8% | National, with concentration in Tokyo, Osaka metropolitan areas | Medium term (2-4 years) |

| Surge in renovation of ageing housing stock post-1990s boom | +1.2% | National, with emphasis on suburban Tokyo, Kansai regions | Long term (≥ 4 years) |

| Maintenance spending ahead of Osaka-Kansai Expo 2025 commercial builds | +0.4% | Kansai region, spillover to Kyoto, Nara prefectures | Short term (≤ 2 years) |

| Digital DIY retail platforms expanding consumer reach in rural prefectures | +0.3% | Rural prefectures, northern Honshu, Kyushu regions | Medium term (2-4 years) |

| Municipal heat-island subsidies driving photocatalytic "cool-roof" demand | +0.5% | Urban centers: Tokyo, Osaka, Nagoya, Fukuoka | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Energy- and VOC-Regulations Accelerating Water-Borne Adoption

Japan’s Building Energy Conservation Act now applies performance standards to existing buildings, while the Air Pollution Control Law caps VOC content for architectural coatings at 400 g/L. These twin policies spur deeper penetration of water-borne formulations that inherently satisfy emission thresholds and improve envelope thermal performance. Ministry of Environment initiatives narrow the remaining use cases for solvent systems, driving suppliers to develop DMBA-based acrylic chemistries that match solvent-borne durability. Leading manufacturers secure a competitive advantage through proprietary water-borne resins and catalytic pigments, ensuring compliance without sacrificing lifetime performance[1]Ministry of Environment, “Chemical Management Initiatives,” Env.go.jp.

Surge in Renovation of Aging Housing Stock Post-1990s Boom

Roughly 13 million homes built during the 1990s boom now require major exterior upkeep as they cross the 25-year maintenance milestone. MLIT data show that renovation orders are expected to reach JPY 13.27 trillion (USD 94.8 billion) in 2024, a 14.9% increase from 2023, with residential projects contributing one-third of that value[2]Ministry of Land, Infrastructure, Transport and Tourism, “Construction Orders Statistics,” MLIT.go.jp . Suburban Tokyo and Kansai prefectures are focal points due to their dense, aging housing tracts. Owners are increasingly favoring premium acrylic and polyurethane coatings, which offer longer repaint cycles to counter rising labor costs, thereby channeling incremental value toward high-performance product tiers.

Maintenance Spending Ahead of Osaka-Kansai Expo 2025 Commercial Builds

The World Expo has triggered an uptick in pre-event building refresh across Osaka’s transit hubs, hospitality corridors, and surrounding prefectures. SK Kaken coatings feature on signature pavilions, reflecting heightened demand for aesthetics and durability fit for global scrutiny. Supply chains report compressed lead times and premium pricing for specialty membranes, with spillover orders extending to Kyoto and Nara. Though temporary, the event stimulates brand exposure and specification wins likely to translate into post-expo repaint cycles across regional commercial assets.

Digital DIY Retail Platforms Expanding Consumer Reach in Rural Prefectures

Home-center giants Cainz and Komeri leverage mobile apps to bridge inventory gaps in remote areas, allowing rural customers to source professional-grade finishes without traveling to urban stores. Tutorials, color simulators, and live chat support lower skill barriers, nudging do-it-yourself repaint activity among aging homeowners. The strategy expands the addressable audience of the Japan architectural coatings market outside metropolitan zones and shifts the revenue mix toward packaged water-borne kits, valued for their convenience and low odor.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining new-build housing starts amid demographic contraction | -0.9% | National, most severe in rural prefectures | Long term (≥ 4 years) |

| Raw-material price volatility (TiO₂, acrylic monomers) squeezing margins | -0.6% | National, affecting all market segments | Medium term (2-4 years) |

| Shortage of certified master-painters inflating application costs | -0.7% | National, acute in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining New-Build Housing Starts Amid Demographic Contraction

Japan’s population shrank by 644,000 in 2024, an accelerating trend that compresses demand for new dwellings. MLIT reports that annual housing starts have fallen below 800,000 units, the lowest level in half a century. Builder consolidation ensues, further reducing the consumption of fresh coatings tied to new construction. Suppliers pivot toward renovation-centric marketing and develop quick-dry, low-odor products suited for occupied dwellings, yet the structural headwind persists for the forecast horizon.

Raw-Material Price Volatility Squeezing Margins

Titanium dioxide is fluctuating, while acrylic monomer tightness followed Mitsubishi Chemical’s Hiroshima plant closure. Kaneka, DIC, and other feedstock providers raised modifier and pigment prices 5-10%, eroding coating-maker margins. Hedging strategies, backward integration—exemplified by Nippon Paint’s USD 4.5 billion AOC resin buy—and reformulation toward lower TiO₂ loads partially mitigate risk but do not fully neutralize cost pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Systems Underpin Climate Resilience

Acrylic products delivered 58.72% of Japan's architectural coatings market share in 2025 and are forecast to expand at a 3.49% CAGR through 2031. High UV resistance, moisture tolerance, and seismic flexibility make acrylics the default exterior finish, particularly along typhoon-prone coastlines. Nippon Paint’s next-generation DF fluororesin, introduced in March 2024, offers extended color retention of over 20 years on high-rise facades. Alkyds compete on a low upfront price for interior walls, while polyurethane captures premium storefronts that require chemical and abrasion resistance. As titanium-dioxide-based photocatalytic variants gain traction under heat-island grants, acrylics reinforce their technology moat. Continuous research and development efforts around self-cleaning surfaces and bio-based binders suggest that the segment will continue to outpace the overall Japanese architectural coatings market.

By Technology: Water-Borne Platforms Secure Regulatory Advantage

Water-borne systems controlled 76.05% of demand in 2025 and are projected to rise at 3.27% CAGR, cementing their dominance as VOC thresholds tighten. DMBA-modified acrylic emulsions now match solvent-borne hardness, enabling adoption in heavy-traffic corridors and commercial atria previously reserved for high-solid alkyds. Solvent-borne coatings persist in niche heritage restoration and marine-influenced installations, but their share falls each fiscal year. Regionally, water-borne penetration surpasses 80% in Tokyo due to stricter municipal ordinances. Reflective and photocatalytic water-borne topcoats qualify for subsidy programs, reinforcing momentum and enlarging the Japan architectural coatings market size attributed to eco-spec formulas.

By End-User: Residential Renovation Anchors Demand

Residential projects accounted for 81.88% of value in 2025 and are anticipated to post a 3.34% CAGR to 2031. MLIT’s renovation order book hit JPY 4.27 trillion (USD 30.5 billion) in 2024, underscoring sustained repaint cycles as condominiums built during the 1990s bubble age out of their original warranties. Homeowner preference shifts toward extended-life coatings to minimize repeat labor expenses in an era of skilled-worker scarcity. Digital DIY platforms from Cainz and Komeri widen access to mid-tier acrylic kits, supporting rural repaint activity. Commercial premises, while just 18.12% of the Japan architectural coatings market size, will log the briskest growth thanks to the Expo 2025 build-out and rising ESG-focused retrofits across office towers.

Geography Analysis

Demand in metropolitan Tokyo is driven by dense housing, stringent environmental regulations, and active subsidy programs that encourage the selection of premium products. Northern prefectures in Tohoku prize freeze-thaw durability, while Okinawa and Kyushu demand high UV-blocking pigments to counter subtropical sunlight. Salt-laden winds off the Sea of Japan propel demand for marine-grade epoxies with zinc-rich primers along coastal highways.

Digital retail adoption is narrowing urban-rural gaps; Komeri’s 1,220 outlets, paired with real-time inventory apps, serve depopulating inland towns, preventing a more severe decline in per-capita paint consumption. Meanwhile, rural depopulation continues to drag on per-capita demand, explaining why new-build volumes there fell faster than the national average. Local governments vary in their incentive pacing: Fukuoka has recently earmarked JPY 1.2 billion for reflective roof coatings, whereas Hokkaido focuses subsidies on insulation boards, indirectly influencing the choice of coating.

Competitive Landscape

Domestic champions capitalize on entrenched distributor ties and early-mover advantage in low-VOC science. International entrants lean on powder coatings and green-chemistry branding; its Interpon D superdurable line achieved a 40% lower carbon footprint by using bio-attributed raw materials in September 2025, appealing to LEED-focused developers. Niche suppliers differentiate through photocatalytic and moisture-adaptive membranes tailored to Japan’s humid summers. Labor shortages intensify competition for licensed applicators; several firms collaborate with trade schools to secure project capacity through joint certification programs. E-commerce and direct-to-site deliveries rewire sales channels. Paint majors experiment with subscription-based maintenance contracts that bundle product, labor, and periodic inspections, creating annuity revenue and deepening customer lock-in.

Japan Architectural Coatings Industry Leaders

Nippon Paint Holdings Co., Ltd.

Kansai Paint Co., Ltd.

SK KAKEN Co., Ltd.

Dai Nippon Toryo Co., Ltd.

FUJIKURA KASEI CO.,LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Akzo Nobel, Arkema, and BASF lowered the carbon footprint of Interpon D powder coatings by 40% using bio-attributed resins and NPG ZeroPCF.

- August 2025: Taisei, Dai Nippon Toryo Co., Ltd., and Nihon University launched “ZERO-e Coat,” delivering 40% better thermal insulation than conventional heat-shield paints.

Japan Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms