Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

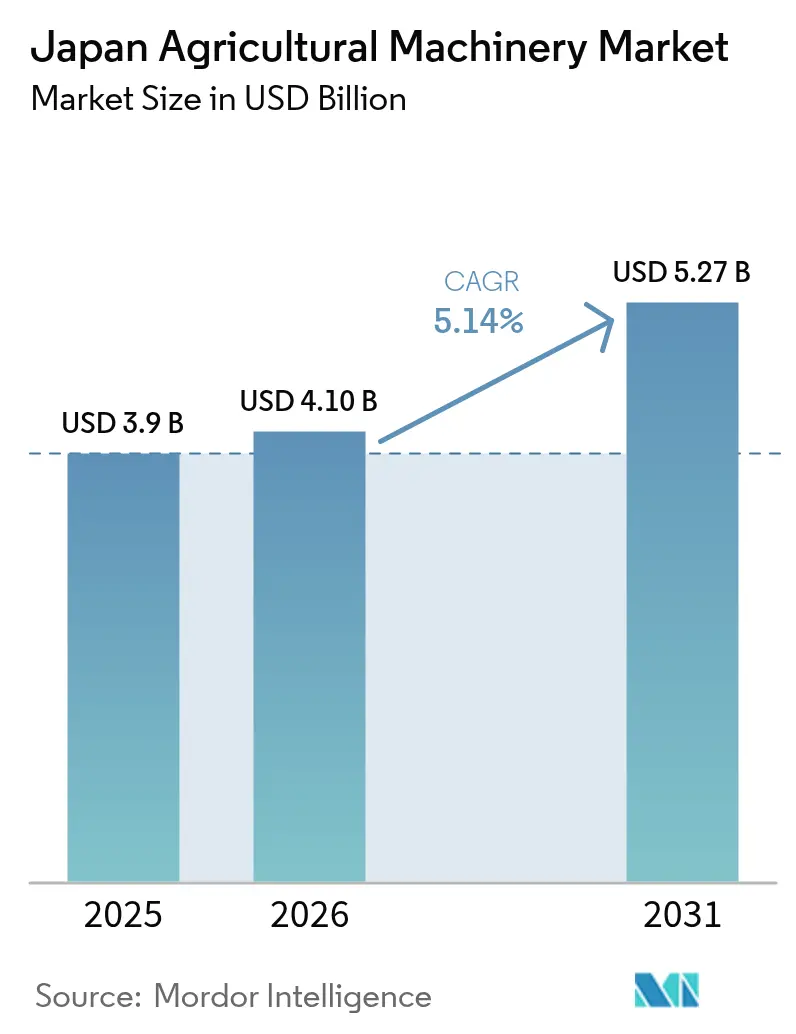

| Base Year Market Size (2025) | USD 3.9 Billion |

| Market Size (2026) | USD 4.1 Billion |

| Market Size (2031) | USD 5.27 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

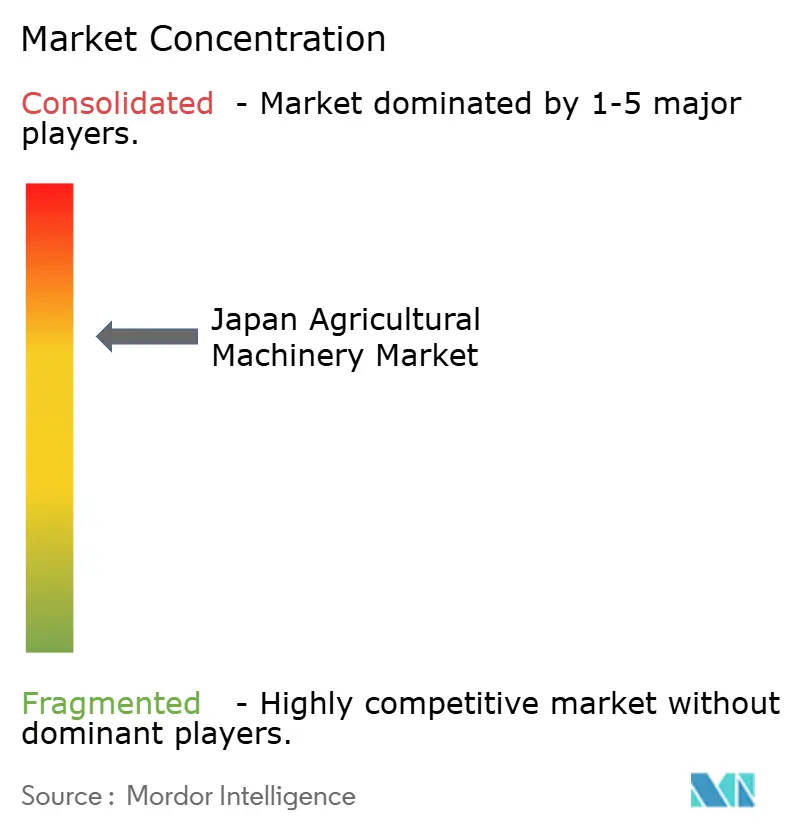

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Agricultural Machinery Market Analysis by Mordor Intelligence

The Japan agricultural machinery market size was valued at USD 3.9 billion in 2025 and estimated to grow from USD 4.1 billion in 2026 to reach USD 5.27 billion by 2031, at a CAGR of 5.14% during the forecast period (2026-2031). Government support, technological advancements, and an aging agricultural workforce drive market growth.[1]Ministry of Agriculture, Forestry and Fisheries, “2025 Budget Outline,” maff.go.jp The increasing adoption of digital solutions and precision farming equipment influences purchasing decisions, while collaborations between international and local manufacturers enhance technology adoption. The market demonstrates strong demand for tractors, smart irrigation systems, and autonomous farming robots as farmers address labor shortages and environmental challenges. While diesel-powered machinery remains dominant, government subsidies support the initial adoption of electric agricultural equipment, indicating an emerging shift in the market.

Key Report Takeaways

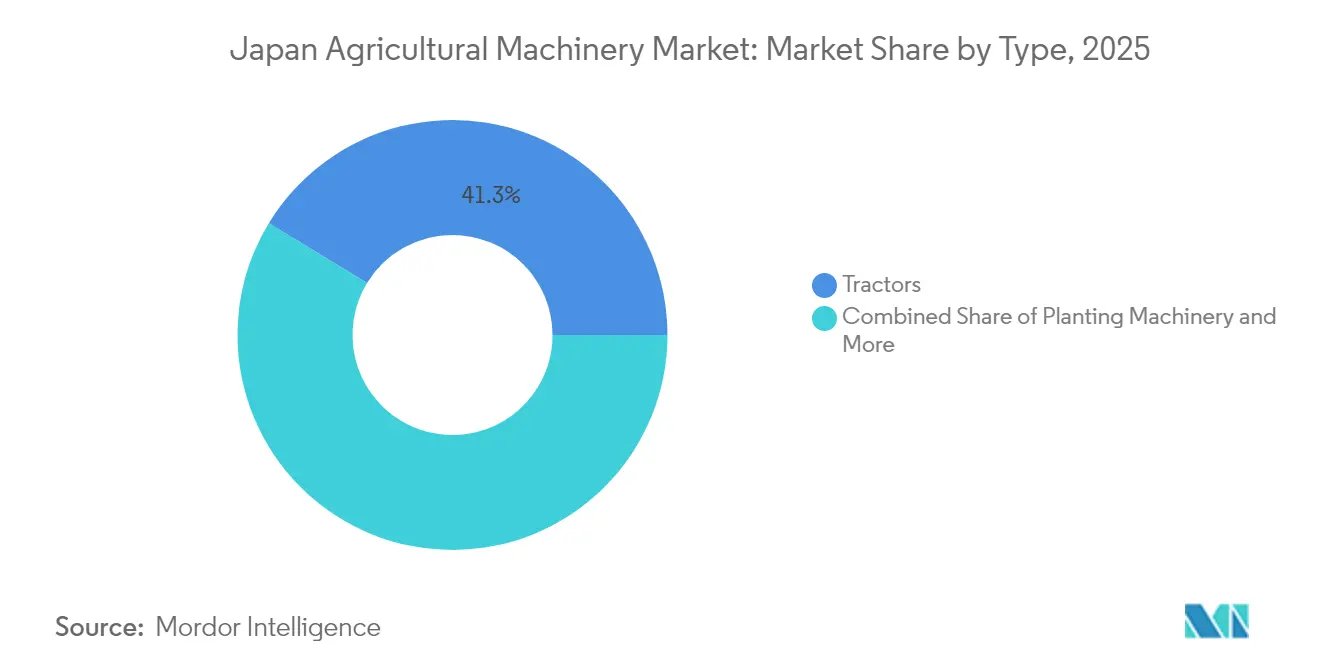

- By product type, tractors held 41.30% of the Japan agricultural machinery market share in 2025, while irrigation machinery is advancing at an 8.17% CAGR through 2031.

- By automation level, manual and conventional equipment commanded 71.25% revenue share in 2025, while fully autonomous systems are moving at a 11.68% CAGR to 2031.

- By drive type, diesel platforms represented 88.20% of the Japan agricultural machinery market size in 2025, and fully electric solutions are growing at a 9.05% CAGR through 2031.

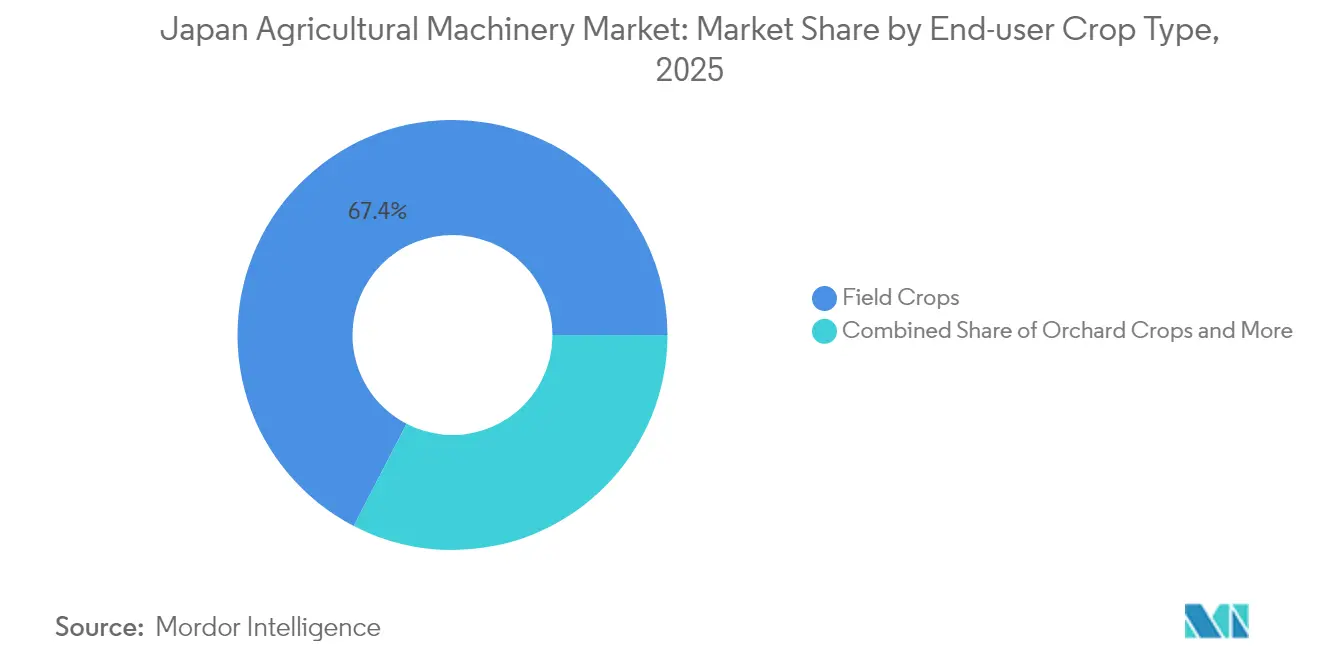

- By crop type, field crops accounted for 67.40% of the Japan agricultural machinery market size in 2025, yet protected cultivation is expanding at an 7.92% CAGR.

- By sales channel, authorized dealerships dominated with a 91.10% share in 2025, while online and mobile app platforms are rising at an 10.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Agricultural Labor Force | +1.8% | National, with acute impact in rural prefectures | Long term (≥ 4 years) |

| Government Purchase Subsidies and Tax Incentives | +1.2% | National, concentrated in designated agricultural zones | Medium term (2-4 years) |

| Rapid Tech Advances in Precision and Automation | +1.5% | National, early adoption in Hokkaido and Tohoku regions | Medium term (2-4 years) |

| Climate-resilient Rice Varieties Needing New Planters | +0.7% | National, priority in heat-affected southern prefectures | Long term (≥ 4 years) |

| Adoption of Electric Power-trains | +0.5% | National, pilot programs in urban-adjacent areas | Long term (≥ 4 years) |

| AI-driven Predictive-maintenance Service Bundles | +0.3% | National, concentrated in large-scale operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Agricultural Labor Force

Japan's farming population is declining rapidly, with most remaining workers being elderly. This demographic shift necessitates mechanization and digital tools to maintain productivity. Farms are adopting automation to address labor shortages, and equipment manufacturers now focus on developing user-friendly and autonomous features. The demand for efficient machinery is increasing across farms of all sizes as manual labor becomes scarce. This demographic transition is transforming the machinery market and changing agricultural practices across the country.

Government Purchase Subsidies and Tax Incentives

The Japanese government supports smart farming through comprehensive financial incentives. National-level grants and tax breaks support farmers' investments in advanced machinery, complemented by regional subsidies. These programs enable mid-size and small farms to acquire advanced equipment. The funding programs incorporate energy efficiency requirements to support environmental objectives. The reduction in initial investment costs and promotion of sustainable practices is facilitating the transition to precision agriculture, enabling farms of all sizes to modernize their operations.

Rapid Tech Advances in Precision and Automation

Japan's agricultural machinery industry is integrating robotics, AI, and IoT technologies. Kubota's Smart Agri System integrates satellite, sensor, and machinery data into a unified platform to reduce costs and improve grain quality.[2]Kubota Corporation, “Precision Farming According to Kubota,” kubota.com GPS-equipped harvesters and autonomous tractors operate with high precision, enhancing yield mapping capabilities and reducing labor requirements. These technologies are now operational in practical farming conditions to optimize farm management. The integration of smart technologies creates comprehensive systems where data analytics improve productivity.

Climate-resilient Rice Varieties Needing New Planters

Farmers are adopting heat-tolerant rice varieties that require modified planting methods due to changing climate conditions. Direct seeding is replacing traditional transplanting methods, requiring specialized equipment for accurate seed placement. Equipment manufacturers are modifying planters to accommodate different grain sizes and provide variable seeding rates. These equipment adaptations help farmers manage changing weather patterns while maintaining crop yields. Modern planters are becoming crucial for rice production as they accommodate variations in soil conditions, temperature, and rainfall patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Cost | -1.3% | National, particularly acute in small-scale operations | Short term (≤ 2 years) |

| Fragmented Landholdings Reduce ROI | -1.1% | National, concentrated in traditional farming regions | Long term (≥ 4 years) |

| Complex Operation / Maintenance Skills Gap | -0.8% | National, severe in aging farming communities | Medium term (2-4 years) |

| Farmer Data-privacy and Cyber-security Concerns | -0.4% | National, heightened in tech-forward operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost

Smart agricultural machinery requires substantial upfront capital investment, representing a significant portion of total farm expenditure. This poses a major challenge for smallholders managing modest plots. The high acquisition costs often exceed the financial capacity of individual farmers, making ownership impractical. Equipment-sharing stations have emerged as a solution, allowing farmers to rent machines by the hour and reduce initial investment. Custom hiring services are effective, particularly for harvesters operating across multiple farms, improving cost efficiency and utilization. While these collaborative models offer alternatives to direct ownership, their widespread adoption depends on infrastructure, awareness, and trust within farming communities.

Fragmented Landholdings Reduce ROI

Average farm plot sizes remain insufficient to justify investment in large-scale machinery, limiting mechanization returns. Approximately 60% of farmland consists of small, irregular fields that impede machine operations, reducing efficiency and increasing equipment wear.[3]National Chamber of Agriculture, “Skill Assessment Test,” asat-nca.jp This fragmentation requires operators to either consolidate land through cooperative arrangements or adopt compact, modular platforms suitable for small spaces. Without changes in landholding patterns or increased access to adaptable technologies, mechanization struggles to achieve consistent profitability. Addressing land fragmentation is crucial for maximizing agricultural machinery value and improving productivity across diverse farming landscapes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractors Remain Core While Smart Irrigation Accelerates

Tractors maintained a 41.30% of the Japan agricultural machinery market share in 2025, serving as the primary mechanization tool for field operations. Farmers invest in compact models suitable for narrow paddy fields while maintaining power requirements. Government depreciation policies support regular fleet updates, maintaining tractors' central role in mechanized farming. Plowing and cultivating equipment benefit from soil conservation programs promoting reduced tillage, while planting machinery adoption increases through direct seeding of climate-resilient rice. Haying and forage equipment serve livestock operations in Hokkaido, where larger herd sizes necessitate mechanical feeding systems.

Irrigation machinery leads market growth with an 8.17% CAGR through 2031. Manufacturers offer variable-rate drip and micro-sprinkler systems designed for small fields, with remote sensors optimizing water schedules. This shift emphasizes resource efficiency over raw power. Harvesters incorporate auto-steering and grain loss monitoring, while emerging technologies like drones and autonomous robots provide service-based solutions that reduce initial investment costs. These developments indicate a trend toward integrated automation systems capable of multiple field operations.

By Automation Level: Semi-Autonomous Systems Bridge Skill Gaps

Manual and conventional equipment accounted for 71.25% of revenue in 2025, indicating continued dependence on operator expertise and basic mechanical reliability. GPS retrofit kits enable farmers to upgrade existing tractors, facilitating digital adoption. Semi-autonomous systems combining GPS guidance with manual controls gain acceptance by maintaining familiar operation methods. Combined operations using auto-steering for field tasks with remote monitoring for maintenance provide a practical transition between traditional and automated farming.

Fully autonomous robots represent the fastest-growing automation segment at 11.68% CAGR. Initial adoption occurs in large rice estates and greenhouses where labor shortages are most acute. Specialized harvesters and robots accommodate delicate crops and enclosed orchards. Government testing facilities in Hokkaido demonstrate autonomous tractor systems, while agricultural cooperatives develop shared fleet programs to improve utilization and distribute costs. These developments attract technology companies and investors to Japan's agricultural machinery market.

By Drive Type: Diesel Stronghold Faces Measured Electrification

Diesel equipment retained 88.20% of Japan agricultural machinery market size in 2025, supported by established supply chains and maintenance networks. Service technicians specialize in combustion engines, with extensive parts availability across rural areas. Hybrid systems combine diesel generators with lithium-ion batteries to optimize fuel usage and power delivery. Fuel cell models show potential for heavy tillage operations but require hydrogen infrastructure development.

Electric equipment grows at a 9.05% CAGR, particularly in orchard sprayers, compact loaders, and greenhouse vehicles, where battery capacity meets operational requirements. Electric adoption concentrates near urban areas with existing charging infrastructure. Manufacturers address weight and cost challenges through exchangeable batteries and performance-enhancing software updates. Government initiatives explore special electricity rates for agricultural charging facilities to encourage sustainable equipment adoption.

By End User Crop Type: Field Crops Dominate While Greenhouse Yields Surge

Field crops generated 67.40% of revenue in 2025, primarily from rice, wheat, soybean, and feed corn production. Large farms invest in high-capacity planting and harvesting equipment, while soybean machinery demand increases due to protein crop incentives. Field crop operations implement strip tillage and residue management equipment to reduce costs while maintaining productivity. Rice farmers adopt direct seeding technology to address labor requirements, increasing demand for specialized planting systems.

Protected cultivation grows at 7.92% CAGR as urban-proximity farmers focus on greenhouse vegetables and premium fruits. Greenhouse operations utilize automated transplanting, aerial spraying, and mechanized harvesting to reduce manual labor. Orchard equipment demand increases for precision spraying and automated fruit handling. Greenhouse investments prioritize efficient climate management, while orchards implement robotic systems for maintenance and harvesting to improve produce quality.

By Sales Channel: Omnichannel Models Blend Click and Dealer Support

Authorized dealers provided 91.10% of the unit value in 2025 through established service networks and financing options. Major equipment purchases require demonstrations, negotiations, and maintenance agreements. Manufacturers integrate online platforms with dealer operations for direct parts distribution. Cloud-based software subscriptions indicate a combined approach using virtual and physical service locations.

Online platforms show 10.74% CAGR, driven by tech-savvy farmers utilizing mobile transactions. Digital marketplaces facilitate equipment research and configuration, though many complete purchases at dealerships. Video consultations continue supporting routine maintenance following pandemic adoption. This integration of digital and traditional channels strengthens customer relationships while expanding market reach in Japan's agricultural machinery sector.

Geography Analysis

Northern Hokkaido's agricultural landscape features expansive fields and cereal crop rotations, supporting large-scale equipment operations. Farmers in the region adopt auto-steering tractors and precision seeding technologies to enhance fuel efficiency and crop uniformity. The Tohoku region implements smart irrigation systems to optimize water usage and reduce operational costs. The central mountainous regions' terrain constraints necessitate compact tractors and modular implements. In Nagano, agricultural cooperatives use pesticide drones for efficient labor management and reduced chemical exposure.

Southern Kyushu's rice farms adapt to increasing temperatures by implementing climate-resilient varieties and advanced planters with dynamic seed depth adjustment. Coastal farms use electric sprayers to comply with environmental regulations in residential areas. In the Kanto region, urban farmers implement electric compact loaders for greenhouse operations, utilizing existing charging infrastructure. Japanese local governments provide subsidies for automation and emission-reduction technologies, accelerating equipment adoption in areas affected by environmental and climate challenges.

Agricultural cooperatives in Saitama and Chiba implement equipment sharing models to address small farm sizes, enabling cost-effective access to advanced machinery. Digital platforms facilitate equipment booking and maintenance scheduling. Technology development centers in Osaka and Kagoshima serve as testing grounds for agricultural robotics startups. These regional innovation hubs enable rapid development and implementation of agricultural technologies. Japan's agricultural machinery market reflects the need for region-specific solutions due to diverse geographical conditions and farm structures.

Competitive Landscape

Kubota Corporation, Deere & Company, Yanmar Holdings Co., Ltd., CNH Industrial N.V., and Iseki & Co., Ltd. hold the maximum share of the Japan agricultural machinery market in 2024. The industry remains moderately concentrated, built on established expertise and regional specialization. Kubota maintains market leadership through extensive dealer networks and diverse product offerings. Deere & Company specializes in high-powered tractors and combines for northern grain farms. CNH Industrial operates through Case IH and New Holland brands, while Yanmar and Iseki maintain strong domestic positions through their rice mechanization expertise.

The industry's competitive landscape is evolving through collaborations and pilot programs. Kubota Corporation partners with technology companies to develop AI systems for improved machine reliability and route efficiency. Yanmar Holdings Co., Ltd. implements automation features in harvesters to address labor shortages. CNH Industrial N.V. develops hydrogen-powered prototypes for alternative fuel solutions. Specialized companies like FieldWorks and AGRIST focus on specific tasks such as weeding and harvesting, presenting potential acquisition or licensing opportunities. The involvement of logistics companies in agri-tech investments indicates a growing emphasis on food system resilience and supply chain modernization.

Manufacturers enhance their competitive position through integrated digital systems. Equipment packages now include connectivity tools, software platforms, and insurance services to strengthen customer relationships. Predictive analytics support maintenance optimization and create continuous revenue streams. Dealers now provide comprehensive services, including fleet operations, data compliance, and technical support. Environmental performance metrics influence procurement decisions, with emissions reduction targets affecting subsidy eligibility and contract awards. The convergence of technology, service offerings, and environmental regulations is transforming Japan's agricultural machinery market through comprehensive business models.

Japan Agricultural Machinery Industry Leaders

Kubota Corporation

Deere & Company

Yanmar Holdings Co., Ltd.

CNH Industrial N.V.

Iseki & Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kubota Corporation partnered with Microsoft to incorporate generative AI into its agricultural machinery. The collaboration aims to improve precision farming and operational efficiency, addressing labor shortages and increasing productivity through digital technology.

- March 2025: Yanmar Holdings Co., Ltd. expanded an Electrification Unit to develop zero-emission solutions for compact off-highway machinery, including agricultural equipment. The unit focuses on e-powertrain systems, including batteries and electric drives, advancing carbon neutrality and innovation in industry.

Japan Agricultural Machinery Market Report Scope

Agricultural equipment/machinery can be defined as machines that are used to perform agricultural operations such as harvesting, plowing, irrigation, planting, and other agricultural operations. The Japan Agricultural Machinery Market is segmented by type into tractors (Tractor by Horsepower {below 20 HP, 21-30 HP, 31-50 HP, and above 50 HP}), (Tractor by Type {utility tractor, row crop tractor, compact utility tractor, and other types}, ploughing and cultivating machinery (ploughs, harrows, cultivators and tillers, and other ploughing and cultivating machinery), planting machinery (seed drills, planters, spreaders, and other planting machinery), harvesting machinery (mowers, balers, and other harvesting machinery), haying machinery, and irrigation machinery. The report offers the market size and forecasts for agricultural machinery in value (USD) for all the above segments.

By Product Type

| Tractors | Horse-Power | Below 20 HP |

| 21 - 30 HP | ||

| 31 - 50 HP | ||

| Above 50 HP | ||

| Type | Utility | |

| Row-Crop | ||

| Compact Utility | ||

| Speciality / Vineyard | ||

| Ploughing and Cultivating Machinery | Ploughs | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Plowing and Cultivating Machinery | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Harvesting Machinery | Combine Harvesters | |

| Other Harvesting Machinery | ||

| Haying and Forage Machinery | Mowers | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Irrigation Machinery | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Other Irrigation Machinery | ||

By Automation Level

| Manual / Conventional |

| Semi-autonomous (Guidance, Telematics) |

| Fully Autonomous / Robotics |

By Drive Type

| Diesel |

| Hybrid |

| Fully Electric |

By End-user Crop Type

| Field Crops |

| Orchard Crops |

| Protected Cultivation Crops |

By Sales Channel

| Authorized Dealerships |

| Online and Mobile-App-Based Platforms |

| By Product Type | Tractors | Horse-Power | Below 20 HP |

| 21 - 30 HP | |||

| 31 - 50 HP | |||

| Above 50 HP | |||

| Type | Utility | ||

| Row-Crop | |||

| Compact Utility | |||

| Speciality / Vineyard | |||

| Ploughing and Cultivating Machinery | Ploughs | ||

| Harrows | |||

| Cultivators and Tillers | |||

| Other Plowing and Cultivating Machinery | |||

| Planting Machinery | Seed Drills | ||

| Planters | |||

| Spreaders | |||

| Other Planting Machinery | |||

| Harvesting Machinery | Combine Harvesters | ||

| Other Harvesting Machinery | |||

| Haying and Forage Machinery | Mowers | ||

| Balers | |||

| Other Haying and Forage Machinery | |||

| Irrigation Machinery | Sprinkler Irrigation | ||

| Drip Irrigation | |||

| Other Irrigation Machinery | |||

| By Automation Level | Manual / Conventional | ||

| Semi-autonomous (Guidance, Telematics) | |||

| Fully Autonomous / Robotics | |||

| By Drive Type | Diesel | ||

| Hybrid | |||

| Fully Electric | |||

| By End-user Crop Type | Field Crops | ||

| Orchard Crops | |||

| Protected Cultivation Crops | |||

| By Sales Channel | Authorized Dealerships | ||

| Online and Mobile-App-Based Platforms | |||

Key Questions Answered in the Report

What is the current value of the Japan agricultural machinery market?

The market is USD 4.1 billion in 2026 and will reach USD 5.27 billion by 2031.

Which product category leads sales in Japan agricultural machinery?

Tractors account for 41.30% of revenue in 2025 followed by cultivating and harvesting equipment.

How fast is protected cultivation equipment growing?

Protected cultivation systems expand at an 7.92% CAGR through 2031 in the Japan agricultural machinery market.

Why are autonomous machines gaining attention among Japanese farmers?

Labor shortages and government incentives make autonomous units attractive by lowering labor input while sustaining yields.

Page last updated on: