Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

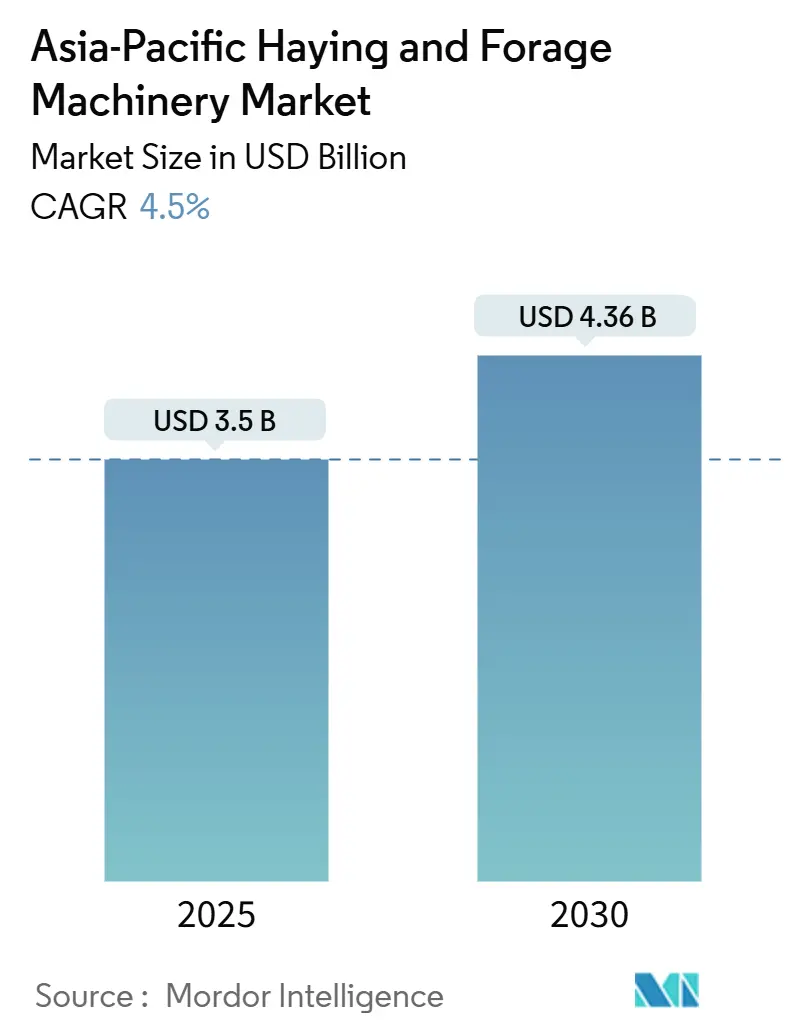

| Market Size (2025) | USD 3.5 Billion |

| Market Size (2030) | USD 4.36 Billion |

| Growth Rate (2025 - 2030) | 4.50% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Haying And Forage Machinery Market Analysis by Mordor Intelligence

The Asia-Pacific haying and forage machinery market size stands at USD 3.50 billion in 2025 and is forecast to reach USD 4.36 billion by 2030, progressing at a 4.50% CAGR. Escalating mechanization to counter rising labor costs, and sustained government subsidies underpin the steady expansion of the Asia-Pacific haying and forage machinery market. Large dairy deficits in Southeast Asia and accelerating feed demand in China continue to stimulate equipment purchases, while electrification initiatives signal a structural technology shift. Nevertheless, fragmented landholdings, commodity price volatility, and tighter diesel-emission rules moderate near-term momentum, making precision machinery and financing programs pivotal for equipment adoption across varying farm sizes. Competitive intensity remains moderate with the five largest suppliers holding the majority of revenue share, yet innovative entrants in autonomous and electric platforms are reshaping customer expectations.

Key Report Takeaways

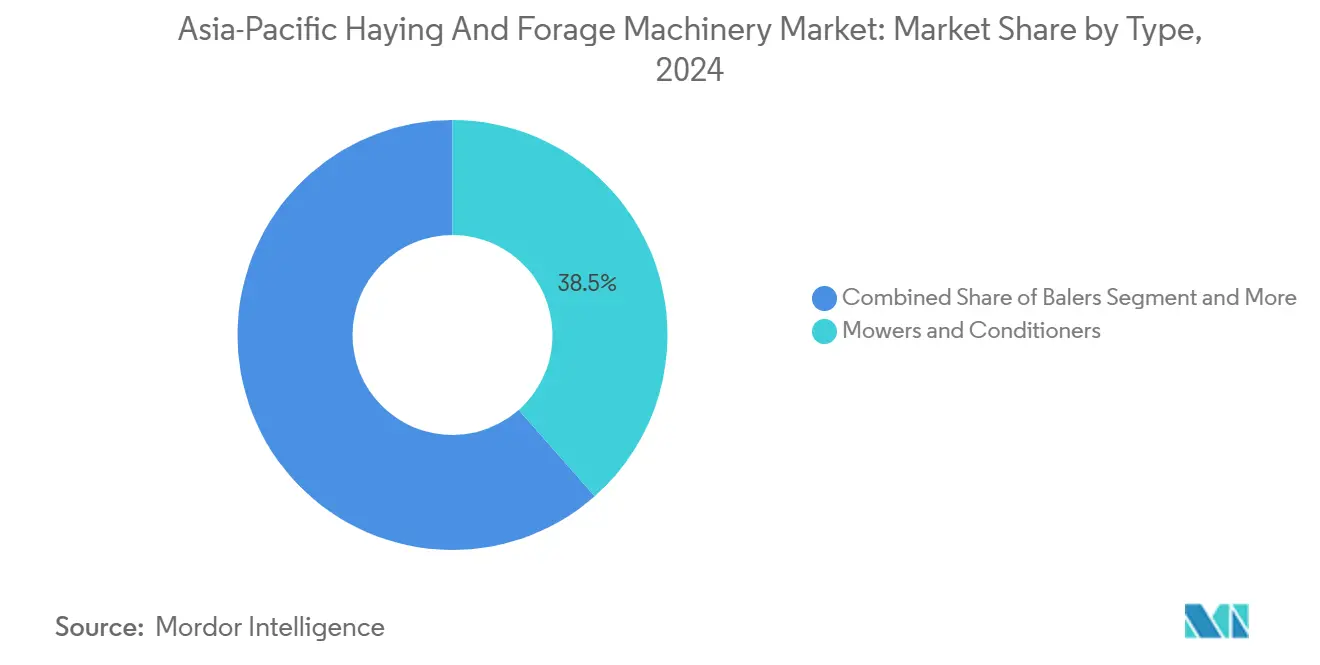

- By type, mowers and conditioners led with 38.5% of the Asia-Pacific haying and forage machinery market size in 2024, while forage harvesters are advancing at a 7.8% CAGR through 2030.

- By geography, China accounted for 40.2% of the Asia-Pacific haying and forage machinery market share in 2024, while Vietnam is poised to expand at an 8.6% CAGR to 2030.

Asia-Pacific Haying And Forage Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing farm mechanization rates in emerging Asian economies | +1.2% | China, India, Indonesia, and Vietnam | Medium term (2-4 years) |

| Rising agricultural labor costs | +0.8% | Japan, South Korea, Australia, and Thailand | Short term (≤ 2 years) |

| Government subsidies and zero-interest loan programs for farm equipment | +0.7% | India, Philippines, China, and Malaysia | Short term (≤ 2 years) |

| Rapid expansion of large-scale commercial dairy farms | +0.6% | China and India | Long term (≥ 4 years) |

| Rapid adoption of precision baling and IoT telematics | +0.4% | Japan, Australia, and South Korea | Medium term (2-4 years) |

| Early electrification of compact hay tools for smallholders | +0.3% | China, India, and Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising agricultural labor costs

Older workforces and climate stress amplify mechanization economics. Over 70% of Japanese farmers were 65 years or older in 2024, prompting policy reforms to recruit foreign farm workers beginning in 2027. South Korea lifted its 2025 seasonal foreign-worker quota to 22,000, 41% higher than 2024, yet still faces an 820,000-person farm-labor gap by 2033.[1]Government of the Socialist Republic of Vietnam, "FOREIGN WORKERS: Occupations that are in short supply in other countries (Period 3)," baochinhphu.vn China's agricultural labor force aging negatively impacts total factor productivity due to reduced technological adoption among older farmers, creating mechanization imperatives.

Government subsidies and zero-interest loan programs for farm equipment

Subsidy programs narrow payback periods. India funds 50-80% of equipment purchases under the Sub-Mission on Agricultural Mechanization. The Philippines’ Agri-Negosyo and Survival and Calamity programs offer loans up to PHP 300,000 (USD 5,300) and PHP 25,000 (USD 440), respectively, at concessional rates. Malaysia’s Agricultural Financing for Investment scheme via AGROBANK backs machinery acquisitions, while Australia’s AgriStarter loans provide up to USD 2 million at 5.18% variable interest.[2]Regional Investment Corporation, "AgriStarter Loan - Regional Investment Corporation," ric.gov.au

Rapid expansion of large-scale commercial dairy farms

China’s USD 626 billion dairy opportunity fuels the construction of high-capacity operations that integrate on-site silage bunkers and GPS-guided forage harvesters to secure consistent feed quality. Provincial authorities prioritize barn complexes exceeding 5,000 cows, raising annual forage requirements and accelerating purchases of mower-conditioners and high-horsepower balers. India complements this trend through national dairy parks and cooperative expansions that aim to double organized milk handling by 2030, a goal that depends on mechanized forage production and shared machinery banks.

Rapid adoption of precision baling and IoT telematics

Manufacturers integrate data analytics into haying workflows. New Holland’s Discbine 209/210 mower-conditioners boast quick-change knives and IoT readiness, enhancing field efficiency. AGCO Corporation introduced the Massey Ferguson SB1436DB baler capable of 90 strokes per minute with automated density control. RFID (Radio Frequency Identification)-enabled bale tracking platforms supply real-time inventory data, allowing farmers to optimize feed logistics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented land holdings limiting machinery ROI | -0.9% | India, China, Philippines, and Indonesia | Long term (≥ 4 years) |

| Volatility in forage crop prices | -0.6% | Australia, New Zealand, and Thailand | Short term (≤ 2 years) |

| Shortage of skilled technicians to service advanced machinery | -0.4% | Vietnam, Indonesia, and Philippines | Medium term (2-4 years) |

| Tightening diesel-emission rules increasing compliance costs | -0.3% | Japan, South Korea, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented land holdings limiting machinery ROI

Small plots curb utilization rates. India’s mechanization remains under 50%, far behind China’s 60%, due in large part to farm size averaging 1.08 hectares. China funds up to CNY 30,000 (USD 4,200) per hectare for land consolidation, but costs impede scale-up. Fragmentation increases travel time and lowers labor efficiency, constraining equipment upgrades across South Asia. Indonesia's agricultural land use dynamics show increasing pressure from urbanization and industrialization, particularly in Java, where food vulnerability is projected to increase by 2045 despite intensification efforts.

Volatility in forage crops prices

Frequent swings in hay, silage, and feed-grain prices complicate capital budgeting for equipment upgrades. Australia’s dairy value fell 7% in 2024-25 as higher hay costs erased margins, prompting farmers to defer mower-conditioner purchases.[3]Source: Department of Agriculture, Fisheries and Forestry, “Dairy,” Department of Agriculture, Fisheries and Forestry, agriculture.gov.au Global feed-grain balances remain tight, with Rabobank projecting stocks-to-use ratios below 2023/24 levels through 2033/34, adding uncertainty for forage-focused producers. Price volatility shortens planning horizons and raises perceived risk, resulting in slower adoption of high-ticket haying and forage machinery despite long-term efficiency benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Precision Technology Drives Equipment Evolution

Mowers and conditioners held 38.5% of the Asia-Pacific haying and forage machinery market share in 2024, due to their foundational role in forage workflows. The segment’s dominance stems from mid-sized dairy and beef farms prioritizing faster curing times and nutrient preservation. Upgrades such as quick-change cutterbars and adjustable conditioning rolls make new models attractive even for cost-conscious growers. Manufacturers bundle telematics modules to monitor acres per hour, further boosting adoption. The Asia-Pacific haying and forage machinery market size for mowers and conditioners is projected to rise at a steady clip as subsidy schemes favor energy-efficient designs.

Forage harvesters are the fastest-growing category with a 7.80% CAGR to 2030. High-horsepower machines paired with real-time dry-matter sensors improve ration quality, directly supporting the expanding regional dairy herd. The Asia-Pacific haying and forage machinery market share for forage harvesters remains modest today but will widen as custom-harvest contracting proliferates in Vietnam and Indonesia. Precision guidance and autonomous steering decrease operator fatigue, while remote diagnostics tackle service-skill shortages. Investments by Kubota Corporation and CLAAS KGaA mbH in self-propelled platforms illustrate the premium placed on throughput and data integration.

Geography Analysis

China controlled 40.2% of the Asia-Pacific haying and forage machinery market in 2024, reflecting its manufacturing scale and robust domestic replacement cycle. Local producers such as Weichai Lovol Intelligent Agricultural Technology Co. delivered USD 2.4 billion in 2024 sales despite broader industry softness, capitalizing on smart-tractor subsidies. Beijing’s pivot toward autonomous and electric equipment spurs incremental demand among progressive cooperatives. The Asia-Pacific haying and forage machinery market size in China expands steadily as dairy and beef complexes integrate feed self-sufficiency into their biosecurity strategies.

Vietnam is the regional growth pacesetter, advancing at an 8.6% CAGR through 2030. Rapid organic-land expansion targets 3% of farmland by 2030, encouraging forage crop rotation and mechanized haymaking. Rising exports of premium pork and poultry products necessitate quality roughage, spurring co-investment in balers and rakes. Government credit tied to sustainable practices lowers financing costs, enabling smallholders to adopt compact equipment.

India sits at an earlier mechanization phase, with tractor penetration still under 50% of cultivated land. Subsidies covering up to 80% of equipment costs, coupled with Farmer-Producer Organizations, foster pooled ownership models. The Asia-Pacific haying and forage machinery market share captured by India will expand as labor scarcity and electrification incentives converge. Japan and Australia, though mature, prioritize technology upgrades to offset aging labor and emission compliance. Custom-hire fleets and leasing products make self-propelled windrowers and forage harvesters financially viable for mid-size enterprises.

Competitive Landscape

Market concentration sits at a moderate level. Deere & Company, Kubota Corporation, CNH Industrial N.V., AGCO Corporation, and CLAAS KGaA mbH together control the majority share of 2025 revenue. Leaders invest heavily in precision platforms, cloud ecosystems, and in-region manufacturing. CLAAS connect provides machine analytics across 30 countries, including Australia and New Zealand, with an Asia roll-out slated for 2026. Kubota Corporation’s Smart Agri System serves 28,000 farmers, leveraging open APIs to aggregate crop-health, fuel, and maintenance data.

Electric and autonomous disruptors add competitive tension. China’s Honghu T70 and Vermeer Corporation’s ZR5 baler prototype highlight the convergence of robotics, battery storage, and telematics. Partnerships between research institutes such as the International Rice Research Institute and drone maker XAG introduce complementary automation layers. Regulatory forces shape differentiation. India’s Bharat Stage V non-road emissions and Japan’s post-2025 diesel limits elevate demand for compliant engines and retrofit kits.

Price competition remains contained, as currency volatility and component shortages elevate production costs. Vendors offset with service bundles, subscription software, and financing alliances with state-owned banks. Over the forecast horizon, vendors that fuse connected hardware with data-driven agronomy are poised to capture incremental wallet share among digitally curious producers.

Asia-Pacific Haying And Forage Machinery Industry Leaders

-

Deere & Company

-

Kubota Corporation

-

CNH Industrial N.V.

-

AGCO Corporation

-

CLAAS KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: New Holland is testing its IntelliSense bale automation system in Western Australia. The system incorporates LiDAR-based auto-steering and speed control technology to improve baling efficiency, reduce fuel consumption, and enhance operator comfort. The automation system is compatible with new BigBaler HD models and can be retrofitted to existing equipment.

- August 2025: CLAAS introduced four new Jaguar 1000 series forage harvesters that feature wider crop flow channels, V-Flex chopping cylinders, and artificial intelligence-enabled silage quality analysis to improve operational efficiency. The company plans to distribute these harvesters globally, including in Asia-Pacific markets.

- August 2024: Yanmar Holdings Co., Ltd. acquired CLAAS India, a manufacturer of agricultural machinery in India, through its group company Yanmar Coromandel Agrisolutions.

Asia-Pacific Haying And Forage Machinery Market Report Scope

Hay and forage harvesters also referred to as silage harvesters, foragers, or choppers, are agricultural implements used to harvest forage plants for livestock silage production. Tedder machines spread and turn loose hay in fields to facilitate drying. The Asia-Pacific haying and forage machinery market segments include mowers and conditioners, balers, forage harvesters, and other related equipment. The market analysis covers China, India, Japan, Indonesia, Vietnam, Australia, Thailand, and other Asia-Pacific regions, providing market estimations and forecasts in both value (USD) and volume (units) for each segment.

By Type

| Mowers and Conditioners |

| Balers |

| Forage Harvesters |

| Tedders and Rakes |

| Self-Propelled Windrowers |

| Other Haying and Forage Machinery (Forage wagons, Bale wrappers, etc.) |

By Geography

| China |

| India |

| Japan |

| Indonesia |

| Vietnam |

| Australia |

| Thailand |

| Rest of Asia-Pacific |

| By Type | Mowers and Conditioners |

| Balers | |

| Forage Harvesters | |

| Tedders and Rakes | |

| Self-Propelled Windrowers | |

| Other Haying and Forage Machinery (Forage wagons, Bale wrappers, etc.) | |

| By Geography | China |

| India | |

| Japan | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific haying and forage machinery market in 2025?

The market is valued at USD 3.50 billion in 2025 and is forecast to reach USD 4.36 billion by 2030.

Which equipment category is growing the fastest in Asia-Pacific?

Forage harvesters are expanding at a 7.8% CAGR due to precision sensors and autonomous steering.

Why is Vietnam considered the most dynamic geography?

Vietnam's sustainable farming push and organic-land expansion fuel an 8.6% CAGR through 2030.

What role do government subsidies play in equipment adoption?

Subsidies in India, China, the Philippines, and Malaysia cover up to 80% of equipment costs, reducing payback periods and increasing mechanization rates.

Page last updated on: