Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

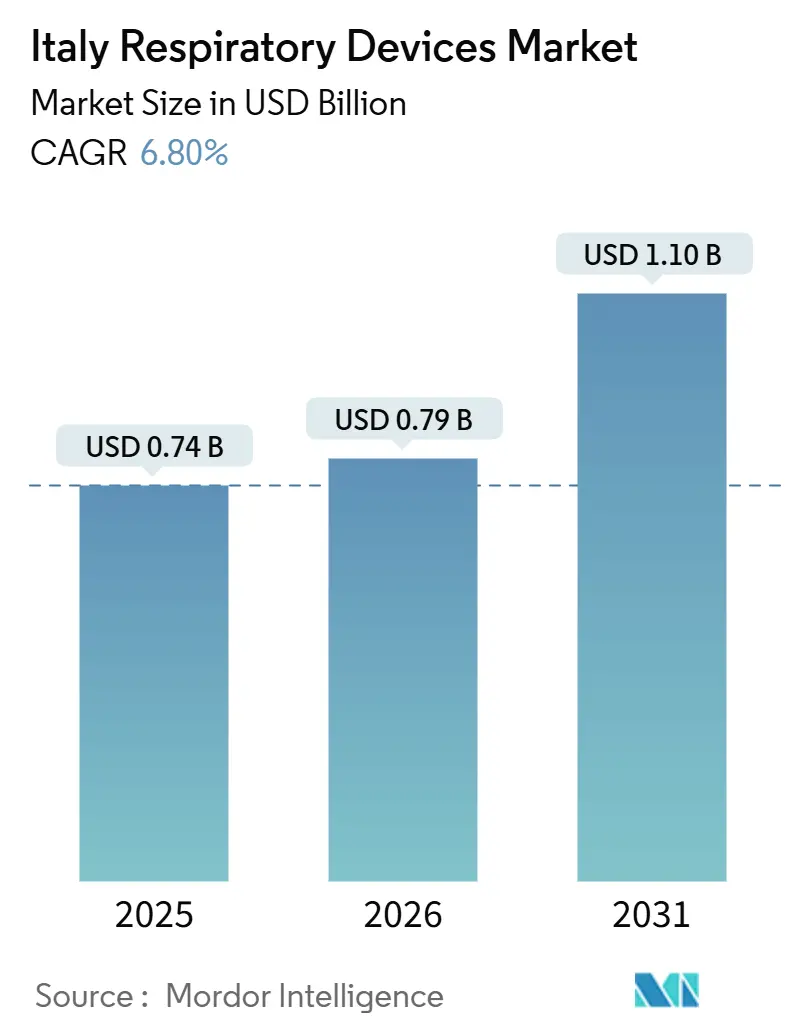

| Base Year Market Size (2025) | USD 0.74 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.10 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

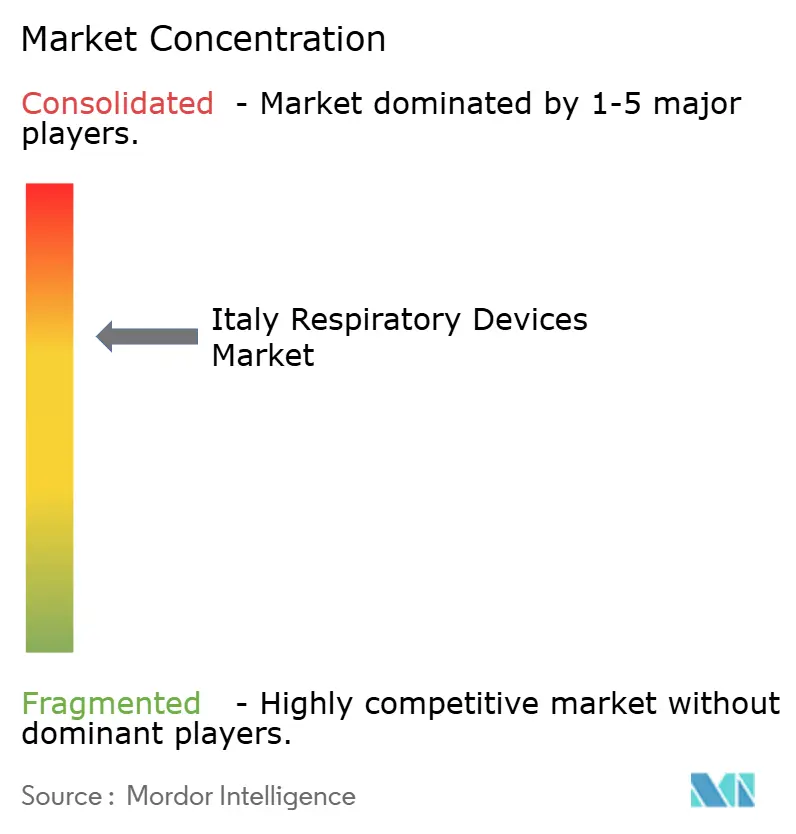

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Respiratory Devices Market Analysis by Mordor Intelligence

The Italy Respiratory Devices Market size is projected to be USD 0.74 billion in 2025, USD 0.79 billion in 2026, and reach USD 1.10 billion by 2031, growing at a CAGR of 6.80% from 2026 to 2031.

A rapidly aging population, high smoking prevalence, and persistent underdiagnosis of obstructive sleep apnea are expanding the pool of Italians who require chronic respiratory support. Hospitals continue to upgrade intensive-care ventilators, while primary-care clinics adopt portable spirometers that feed data into regional tele-health dashboards. Public funding from the National Recovery and Resilience Plan accelerates procurement cycles for home ventilators, connected pulse oximeters, and digital inhaler trackers, narrowing regional access gaps. At the same time, European Union climate legislation is forcing a pivot toward low-GWP inhalers, giving domestic champion Chiesi Farmaceutici a first-mover advantage in propellant reformulation. Multinational suppliers ResMed, Philips, Fisher & Paykel Healthcare, and Medtronic leverage global manufacturing scale yet must localize service contracts to compete with agile Italian SMEs that tailor disposables to hospital-fleet specifications.

Key Report Takeaways

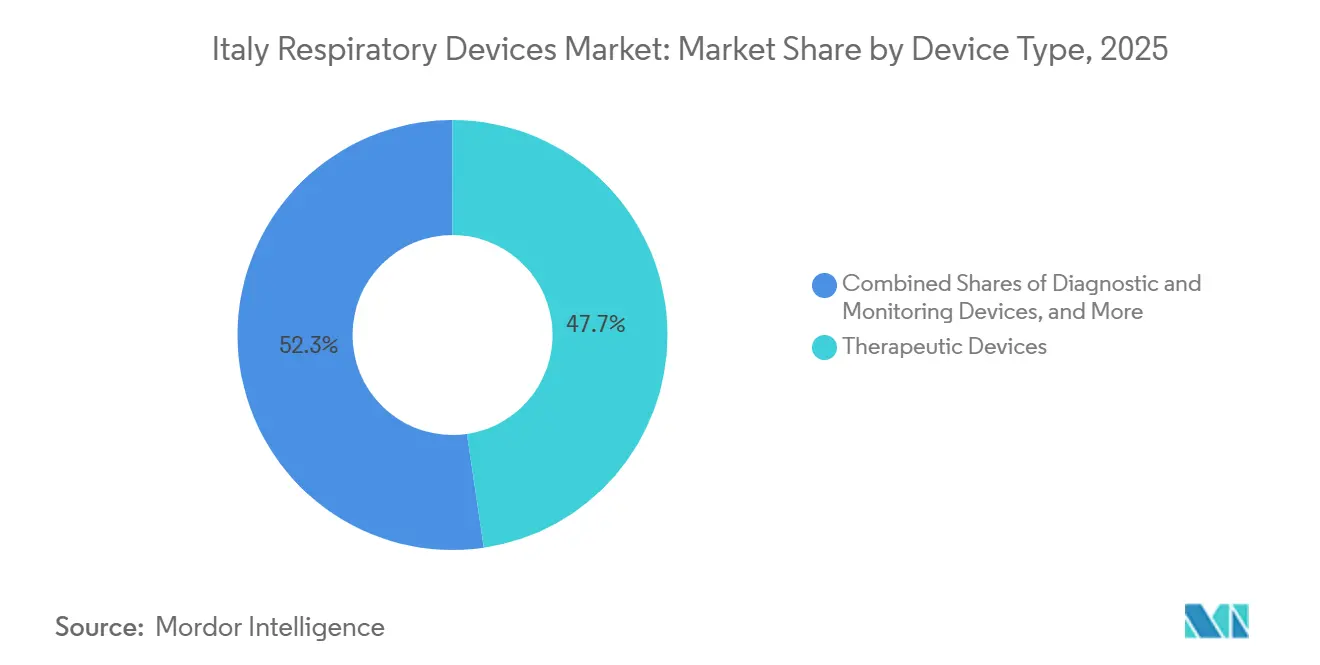

- By device type, therapeutic equipment led with 47.67% of the respiratory devices market share in 2025.

- By disease indication, COPD accounted for 33.34% of 2025 revenue, while sleep apnea is forecast to post the highest segment CAGR of 9.58% to 2031.

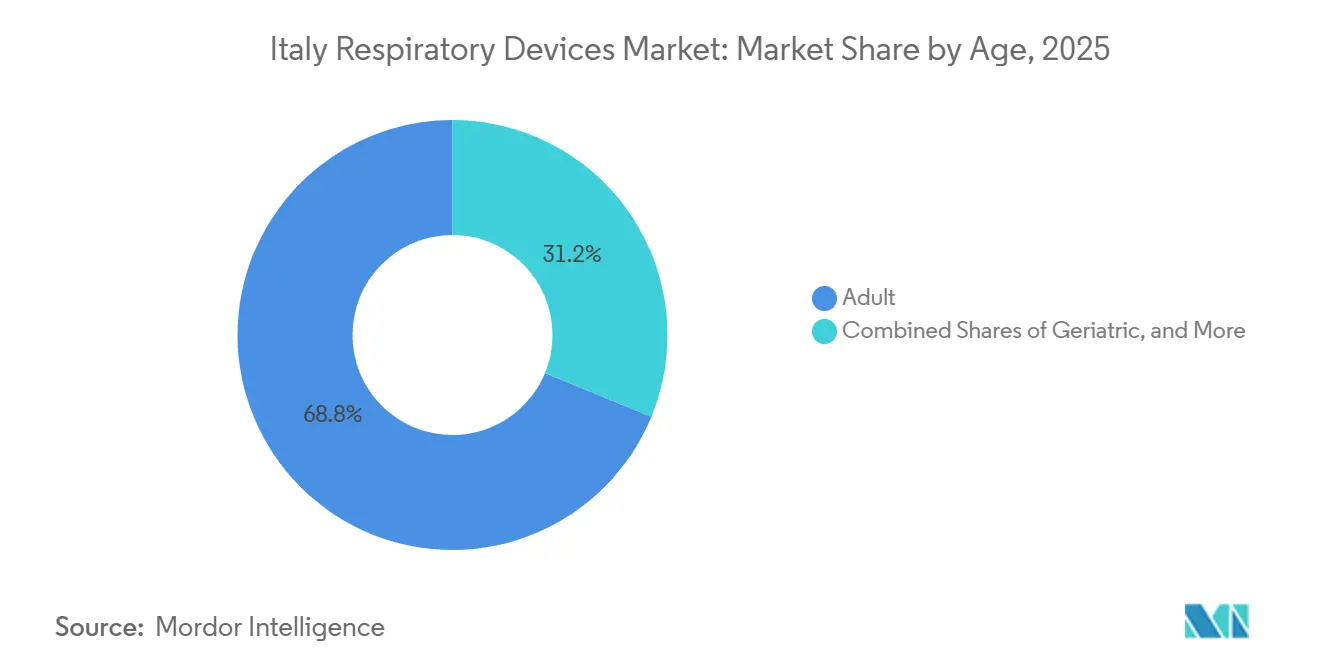

- By age, the pediatric cohort is set to rise at a 10.9% CAGR through 2031, outpacing all other age groups in the respiratory devices market.

- By end-user, home healthcare settings are expanding at a 9.4% CAGR to 2031, the fastest among care settings in the respiratory devices market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Respiratory Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | ( ~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing prevalence of chronic respiratory diseases | +2.1% | National, higher COPD burden in northern regions | Long term (≥ 4 years) |

| Rising adoption of home-care respiratory support & tele-monitoring | +1.8% | National, early leadership in Lombardy and Emilia-Romagna | Medium term (2-4 years) |

| EU climate policy driving switch to low-GWP inhalers | +0.9% | EU-wide, Italy as major inhaler market | Medium term (2-4 years) |

| Regional tele-health pilots accelerating digital uptake | +1.2% | Lombardy core, replication in Veneto and Piedmont | Short term (≤ 2 years) |

| Technological shifts toward non-invasive & portable devices | +1.8% | National | Medium term (2-4 years) |

| Aging population & high smoking rates | +2.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Respiratory Diseases (COPD, Asthma, OSA)

A combined 6.5 million Italians live with COPD or asthma, and an estimated 80% of moderate-to-severe sleep-apnea cases remain undiagnosed. During the 2023/2024 winter, co-circulating SARS-CoV-2 and influenza viruses led to a spike in hospital admissions for acute exacerbations among older adults. RSV alone drives roughly 26,000 hospitalizations and 1,800 deaths each year in citizens aged 60+, underscoring the need for early detection tools and ventilatory support systems.[1]Istituto Superiore di Sanità, “Prevalenza BPCO e Asma in Italia,” iss.it Expanding home-sleep testing and broader reimbursement of CPAP devices are expected to surface latent demand, lifting unit shipments of diagnostic polysomnography recorders and auto-adjusting positive airway pressure devices across the respiratory devices market.

Rising Adoption of Home-Care Respiratory Support & Tele-Monitoring

The National Recovery and Resilience Plan earmarks EUR 4.75 billion (USD 5.1 billion) for primary-care hubs equipped with digital monitoring platforms that push real-time oximetry, spirometry, and CPAP-adherence data to pulmonologists.[2]European Commission, “Recovery and Resilience Facility,” ec.europa.eu Lombardy’s COD19 project showed a 20% cut in COPD readmissions by deploying connected pulse oximeters and chat-based nurse triage. A 2025 survey of 150 Italian payers highlighted reimbursement ambiguity and privacy compliance as leading obstacles, signaling that national procurement standards and clear data-governance rules will unlock faster scale-up.

EU Climate Policy Driving Switch to Low-GWP Inhalers

Regulation 2024/573 mandates a 98% reduction in HFA-134a quotas by 2036, compelling inhaler manufacturers to migrate toward propellants such as HFA-152a, whose global-warming potential is 90% lower. Chiesi Farmaceutici completed Phase III safety trials of an HFA-152a pMDI in 2025 and plans a commercial launch in 2027, positioning itself for early volume gains as competitors scramble for reformulation approvals. While dry-powder inhalers avoid propellants altogether, coordination and dexterity requirements limit adoption in older and pediatric patients, allowing metered-dose formats to retain share if sustainability hurdles are met.

Regional Tele-Health Pilots Accelerating Digital Device Uptake

Lombardy’s TELEMACO and MIRATO programs deliver algorithm-guided care pathways that integrate Bluetooth spirometers, smart inhalers, and AI-driven notification engines. Early data indicate a 15-point improvement in medication adherence among patients with severe asthma. Regional authorities in Veneto and Piedmont have committed to replicating the model by 2027, driving incremental demand for cloud-enabled diagnostic devices across the respiratory devices market. Vendors that secure HL7-FHIR interoperability and ISO 27001 certification enjoy preferred-bidder status in these tenders.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront cost of advanced devices & limited reimbursement | -1.3% | National, stronger impact in southern regions | Medium term (2-4 years) |

| Stringent EU-MDR compliance timelines | -0.8% | EU-wide, affecting Italian SMEs | Short term (≤ 2 years) |

| Consolidation of hospital tenders squeezing SME margins | -0.8% | National | Short term (≤ 2 years) |

| Cyber-security & data-privacy hurdles for connected devices | -0.8% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Devices & Limited Reimbursement

Portable oxygen concentrators, adaptive servo-ventilation systems, and connected nebulizers cost EUR 1,500-8,000 but receive partial reimbursement only for narrowly defined indications under Servizio Sanitario Nazionale. Patients with moderate disease often self-finance or delay therapy, dampening unit growth in the respiratory devices market. Administrative complexity, multi-form authorization, specialist referrals, and annual recertification discourage uptake among elderly users with limited digital literacy, perpetuating a two-tier device landscape.

Stringent EU-MDR Compliance Timelines

Full enforcement of EU-MDR in October 2024 obliged manufacturers to overhaul technical files, clinical-evidence dossiers, and post-market surveillance protocols. Notified-body backlogs now exceed 18 months for Class IIb ventilators and Class III implantables, delaying new-product launches by Italian SMEs such as Siare Engineering. Resource diversion from R&D to regulatory tasks slows innovation velocity and temporarily restrains the respiratory devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Disposables Outpace Therapeutics on Infection-Control Mandates

Therapeutic equipment generated 47.67% of 2025 revenue as hospitals renewed ICU ventilator fleets and home-care providers expanded CPAP rental programs. Disposables, however, are projected to grow at an 8.8% CAGR, the highest among product lines in the respiratory devices market. Single-patient breathing circuits, antibacterial HME filters, and CPAP masks require quarterly replacement, creating a predictable consumables annuity. Diagnostic products, portable spirometers, pulse oximeters, and capnographs capture the remainder but gain relevance as tele-monitoring pilots transition from proof-of-concept to reimbursed standard of care.

Rising awareness of ventilator-associated pneumonia is driving stricter hospital protocols that favor single-use circuits, propelling volume for local converters that customize tubing lengths and connectors. At the same time, connected disposables embed RFID chips that track change intervals, enabling predictive reordering. Multinationals bundle disposables with equipment leases, locking customers into contracts for three to five years. Italian SMEs defend their market share through rapid prototyping and customization, helping the respiratory devices market maintain a competitive balance between global and domestic suppliers.

By Disease Indication: Sleep Apnea Surges as Under-Diagnosis Narrows

COPD still accounted for 33.34% of 2025 sales, reflecting over 3.5 million clinically diagnosed cases that require long-term oxygen therapy, nebulized bronchodilators, and pressure support ventilators. Sleep apnea is projected to grow 9.58% annually to 2031, the fastest rate among indications. Expanded reimbursement for home polysomnography and auto-titrating CPAP devices is boosting the market size for this category. Seasonal spikes in pneumonia and viral infections also drive purchases of ventilators and high-flow oxygen, an episodic driver that peaks during winter but has plateaued after COVID-19 ICU upgrades.

Improved awareness campaigns by pulmonology societies and general practitioners lead to earlier referrals, raising CPAP initiation rates within six months of diagnosis. Meanwhile, emerging niche indications such as bronchiectasis and pulmonary fibrosis receive attention through compassionate-use programs that seed future demand for portable oxygen concentrators and oscillatory PEP devices.

By Age: Pediatric Segment Leads Growth on Innovation and Screening

Adults accounted for 68.80% of 2025 consumption, driven by COPD and sleep apnea prevalence that spikes between 50 and 70 years. Yet pediatric demand is on track for a 10.9% CAGR, reflecting guideline-backed use of spacer-plus-metered dose inhalers and ultralight mesh nebulizers that cut dosing time by 50%. Italian schools increasingly stock emergency salbutamol inhalers, further expanding unit volumes.

Geriatric users require devices attuned to comorbidities, cognitive decline, and manual dexterity limits. Features such as low-noise output below 26 decibels and auto-humidification modes improve adherence. Hybrid non-invasive ventilation modes target complex sleep-disordered breathing common in elderly patients with heart failure, but limited clinical evidence in pediatric cohorts tempers cross-segment application. Both the oldest and youngest patients converge on a shared need for connected devices that alert caregivers to therapy lapses, sustaining demand momentum across the respiratory devices market.

By End-User: Home Healthcare Gains on National Recovery Plan Funding

Hospitals and clinics retained 62.05% of 2025 revenue due to large installed bases of ventilators, anesthesia machines, and lung-function labs. However, home-care settings are forecast to advance at 9.4% CAGR, the fastest among end-users, as EUR 4.75 billion in Recovery Plan grants bankroll digital platforms and nurse-led mobile teams. Connected CPAPs with cloud dashboards satisfy reimbursement requirements for remote adherence verification, shifting procurement toward subscription models.

Ambulatory surgical centers, nursing homes, and emergency services represent smaller slices but require portable ventilators and suction devices that integrate with ambulance telemetry. Equipment rental firms expand fleets of battery-operated oxygen concentrators to serve medical tourism and seasonal migration in southern seaside towns, widening the geographic reach of the respiratory devices market.

Geography Analysis

Regional disparities shape both access and procurement velocity in the respiratory devices market. Lombardy, Emilia-Romagna, and Veneto spend 15% more per capita on healthcare than the national average, enabling rapid adoption of connected ventilators and digital inhalers. Lombardy alone accounts for nearly 22% of national COPD hospitalizations but reduced readmissions by 12% after rolling out TELEMACO tele-health, generating a benchmark for southern regions. Emilia-Romagna prepares to issue a EUR 120 million umbrella tender for portable oxygen concentrators and spirometers in 2026, creating a procurement bulge that favors suppliers with local warehousing.

Southern regions such as Calabria, Campania, and Sicily face budget shortfalls that extend reimbursement decisions by up to 12 months and limit access to connected devices. National Recovery Plan monies earmark infrastructure upgrades and digital platforms to narrow these gaps, but implementation hurdles procurement expertise, vendor vetting, and staff training delay adoption. Manufacturers must navigate 21 autonomous regional health authorities, tailoring value dossiers to local clinical pathways and budgeting cycles. Cross-border e-commerce further complicates geography segmentation, as Italian patients increasingly purchase CE-marked CPAP masks from Spanish and German portals, adding gray-market price pressure.

Competitive Landscape

Competitive intensity in the respiratory devices market is moderate, with the top five players accounting for the majority of 2025 revenue. ResMed leads CPAP and cloud-software ecosystems, holding an estimated 18% share. Philips follows, regaining traction after 2024 recall setbacks by offering remediation rebates. Fisher & Paykel Healthcare dominates hospital humidification, while Medtronic leverages turbine patents to capture upgrades in critical-care ventilators. Domestic champion Chiesi Farmaceutici differentiates by bundling inhaled therapies with electronic-dose counters and low-GWP propellants, consolidating its 12% slice in inhalers.

Private-equity activity signals renewed consolidation potential. Quadrivio Group’s 2025 acquisition of Medical International Research added portable spirometry and tele-monitoring IP, improving scale economies in disposables. BTL’s purchase of Medisoft RAM Italia strengthened engineering talent and diversified into diagnostic treadmills. SMEs respond by focusing on niches, offering customizable disposables and region-specific service contracts.

Strategic partnerships accelerate market evolution. ResMed collaborates with Telecom Italia to integrate CPAP compliance data into national digital health platforms, thereby expediting reimbursement audits. Philips partners with Lombardy’s MIRATO to automate ventilator weaning protocols using AI-driven analytics. Such alliances intensify switching costs and create ecosystem lock-in, reinforcing competitive moats in the respiratory devices market.

Italy Respiratory Devices Industry Leaders

GE Healthcare

Fisher & Paykel Healthcare Ltd

Medtronic PLC

Invacare Corporation

Chiesi Farmaceutici S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: VoiceMed, a Rome-based digital health company, completed its first funding round, raising EUR 1 million (approximately USD 1.1 million). The company focuses on developing voice-based solutions for the remote monitoring of chronic respiratory conditions.

- September 2025: Chiesi Group announced positive Phase III TRECOS safety results for its low-GWP HFA-152a pMDI, a milestone toward commercial launch by 2027.

- August 2025: BTL purchased Medisoft RAM Italia from CAIRE, retaining Padua manufacturing and integrating treadmill diagnostics into its global rehabilitation portfolio.

Italy Respiratory Devices Market Report Scope

As per the scope of the report, respiratory devices include respiratory diagnostic devices, therapeutic devices, and breathing devices for administering long-term artificial respiration. It may also include a breathing apparatus used for resuscitation by forcing oxygen into the lungs of a person who has undergone asphyxia.

The Italian respiratory devices market is segmented by device type, disease indication, age, and end user. By device type, the market is segmented into diagnostic & monitoring devices, therapeutic devices, and disposables. By diagnostic & monitoring devices, the market is segmented into spirometers, sleep test devices, peak flow meters, pulse oximeters, capnographs, and other diagnostic & monitoring devices. By therapeutic devices, the market is segmented into CPAP devices, BIPAP devices, humidifiers, nebulizers, oxygen concentrators, ventilators, inhalers, and other therapeutic devices. By disposables, the market is segmented into masks, breathing circuits, and other disposables. By disease indication, the market is segmented into COPD, asthma, sleep apnea, pneumonia & acute respiratory infections, and others. By age, the market is segmented into adult, geriatric, and pediatric. By end-user, the market is segmented into hospitals & clinics, home healthcare settings, ambulatory surgical centers, and others. The report offers all values in (USD) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | |

| Peak Flow Meters | |

| Pulse Oximeters | |

| Capnographs | |

| Other Diagnostic & Monitoring | |

| Therapeutic Devices | CPAP Devices |

| BiPAP Devices | |

| Humidifiers | |

| Nebulizers | |

| Oxygen Concentrators | |

| Ventilators | |

| Inhalers | |

| Other Therapeutic Devices | |

| Disposables | Masks |

| Breathing Circuits | |

| Other Disposables |

By Disease Indication

| COPD |

| Asthma |

| Sleep Apnea |

| Pneumonia & Acute Respiratory Infections |

| Others |

By Age

| Adult |

| Geriatric |

| Pediatric |

By End-User

| Hospitals & Clinics |

| Home Healthcare Settings |

| Ambulatory Surgical Centers |

| Others |

| By Device Type | Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | ||

| Peak Flow Meters | ||

| Pulse Oximeters | ||

| Capnographs | ||

| Other Diagnostic & Monitoring | ||

| Therapeutic Devices | CPAP Devices | |

| BiPAP Devices | ||

| Humidifiers | ||

| Nebulizers | ||

| Oxygen Concentrators | ||

| Ventilators | ||

| Inhalers | ||

| Other Therapeutic Devices | ||

| Disposables | Masks | |

| Breathing Circuits | ||

| Other Disposables | ||

| By Disease Indication | COPD | |

| Asthma | ||

| Sleep Apnea | ||

| Pneumonia & Acute Respiratory Infections | ||

| Others | ||

| By Age | Adult | |

| Geriatric | ||

| Pediatric | ||

| By End-User | Hospitals & Clinics | |

| Home Healthcare Settings | ||

| Ambulatory Surgical Centers | ||

| Others | ||

Key Questions Answered in the Report

How large is the respiratory devices market in Italy today?

The respiratory devices market size stands at USD 0.79 billion in 2026 and is projected to reach USD 1.10 billion by 2031.

Which product group leads sales?

Therapeutic equipment, including CPAP machines and ventilators, generated 47.67% of 2025 revenue.

What segment is growing the fastest?

Disposables, such as single-use breathing circuits and CPAP masks, are expanding at an 8.8% CAGR through 2031.

Why is sleep apnea an attractive opportunity?

Under-diagnosis is high, and expanded reimbursement now covers severe cases, driving a 9.58% CAGR for sleep-apnea devices.

How will EU climate rules affect inhalers?

Regulation 2024/573 forces a shift to low-GWP propellants, benefiting early reformulators like Chiesi Farmaceutici.

Which end-user channel is gaining share?

Home healthcare settings are advancing at 9.4% CAGR as national funding supports remote monitoring platforms.

Page last updated on: