Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Intelligent Flow Meter Market is Segmented by Type (Coriolis, Magnetic, Ultrasonic, and More), Communication Protocol (HART, Modbus, PROFIBUS, and More), Offering (Hardware, Software, and Services), End-User Industry (Oil and Gas, Water and Wastewater, Pharmaceuticals and Life Sciences, Power Generation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

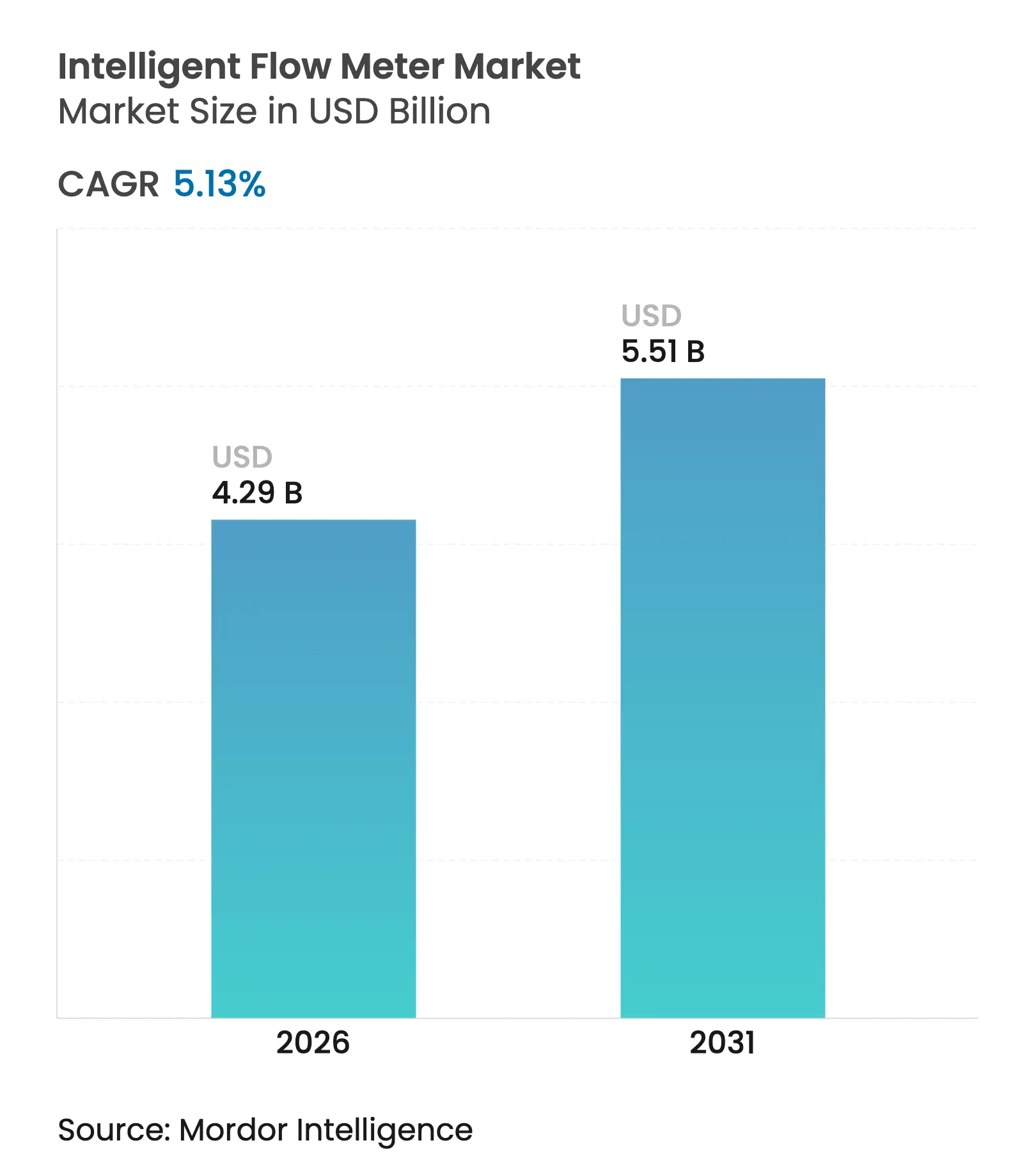

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 5.13 % CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Intelligent Flow Meter market size in 2026 is estimated at USD 4.29 billion, growing from 2025 value of USD 4.08 billion with 2031 projections showing USD 5.51 billion, growing at 5.13% CAGR over 2026-2031. Accelerated deployment of Industry 4.0 projects, coupled with stricter custody-transfer rules, is pushing operators to replace legacy mechanical meters with digitally connected alternatives. Continuous investment in desalination, hydrogen, and renewable-energy infrastructure is widening the technology’s addressable base, while edge analytics functions are allowing plants to shift from time-based to data-driven maintenance. At the same time, component shortages and heightened cybersecurity requirements are rewarding suppliers that can guarantee resilient supply chains and robust software support.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing penetration in oil and gas plus water and wastewater-management industries Growing penetration in oil and gas plus water and wastewater-management industries | +1.2% | Global, with concentration in APAC and MEA | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with concentration in APAC and MEA | Impact Timeline:Medium term (2-4 years) |

Rapid integration of IoT-enabled diagnostic functions Rapid integration of IoT-enabled diagnostic functions | +0.9% | North America and EU leading, APAC following | Short term (≤ 2 years) | |||

Stricter custody-transfer regulations and energy-efficiency mandates Stricter custody-transfer regulations and energy-efficiency mandates | +0.7% | Global, particularly North America and EU | Long term (≥ 4 years) | |||

Shift toward predictive-maintenance-ready digital twins Shift toward predictive-maintenance-ready digital twins | +0.6% | Developed markets initially, expanding globally | Medium term (2-4 years) | |||

Hydrogen-economy pipeline instrumentation demand Hydrogen-economy pipeline instrumentation demand | +0.4% | EU, Japan, Australia, select US regions | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Penetration in Oil and Gas Plus Water and Wastewater-Management Industries

Decarbonization targets and aging pipeline networks are prompting utilities to accelerate meter modernization programs. Electromagnetic units with embedded leak-detection logic are helping cities cut non-revenue water that still exceeds 30% in many large metros. In upstream operations, Coriolis and ultrasonic devices now deliver ±0.1% accuracy, reducing custody-transfer disputes. Operators handling shale and deepwater wells are turning to multiphase meters that quantify oil, gas, and produced water simultaneously, which helps optimize artificial-lift settings and comply with flare-reduction rules. [1]Baker Hughes, “Vortex Flow Meters,” bakerhughes.com

Rapid Integration of IoT-Enabled Diagnostic Functions

Modern transmitters feature edge processors that flag sensor drift, cavitation, or coating build-up before performance degrades. The Ethernet-APL physical layer moves both power and data in a single twisted pair, simplifying upgrades and lowering brownfield retrofit costs. Real-time alerts sent to L1/L2 support teams allow maintenance crews to act during planned shutdowns rather than scrambling after failures.

Stricter Custody-Transfer Regulations and Energy-Efficiency Mandates

The EU Renewable Energy Directive II compels refiners to verify biofuel blending ratios with higher-accuracy meters that remain stable across temperature swings. Growing carbon-capture investments also require volumetric proof of stored CO₂, boosting demand for multivariable Coriolis units that compensate for pressure and density changes.

Shift Toward Predictive-Maintenance-Ready Digital Twins

Biopharma producers now couple flow data with soft sensors to predict ideal harvest points in cell-culture reactors, elevating batch yields and cutting scrap. Chemical companies feed live meter readings into plant-wide models that tweak feed ratios every few seconds, improving selectivity and lowering specific energy consumption.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Higher CAPEX versus mechanical and differential-pressure meters Higher CAPEX versus mechanical and differential-pressure meters | -0.8% | Price-sensitive markets, particularly APAC and MEA | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Price-sensitive markets, particularly APAC and MEA | Impact Timeline:Short term (≤ 2 years) |

Complex calibration and skilled-labour requirements Complex calibration and skilled-labour requirements | -0.5% | Global, more pronounced in emerging markets | Medium term (2-4 years) | |||

Volatility of raw-material prices affecting sensor electronics Volatility of raw-material prices affecting sensor electronics | -0.4% | Global supply chains, semiconductor-dependent regions | Short term (≤ 2 years) | |||

Cyber-security vulnerabilities in connected meters Cyber-security vulnerabilities in connected meters | -0.3% | Connected infrastructure, critical utilities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Higher CAPEX Versus Mechanical and Differential-Pressure Meters

An intelligent Coriolis meter may cost four times more than a basic turbine device, stretching public-utility budgets. Yet total cost-of-ownership models, which include pump-energy savings and lower recalibration spend, increasingly swing decisions in favor of smart meters. [2]Badger Meter, “Vortex Flow Meters,” badgermeter.com

Complex Calibration and Skilled-Labour Requirements

Smart meters demand technicians who grasp both fluid dynamics and industrial networking. In many emerging markets, labs traceable to international standards remain scarce, leading to longer service disruptions whenever custody-transfer instruments are recalibrated. [3]KROHNE Messtechnik GmbH, “Flow Measurement,” krohne.com

By Type: Magnetic Dominance Challenged by Multiphase Innovation

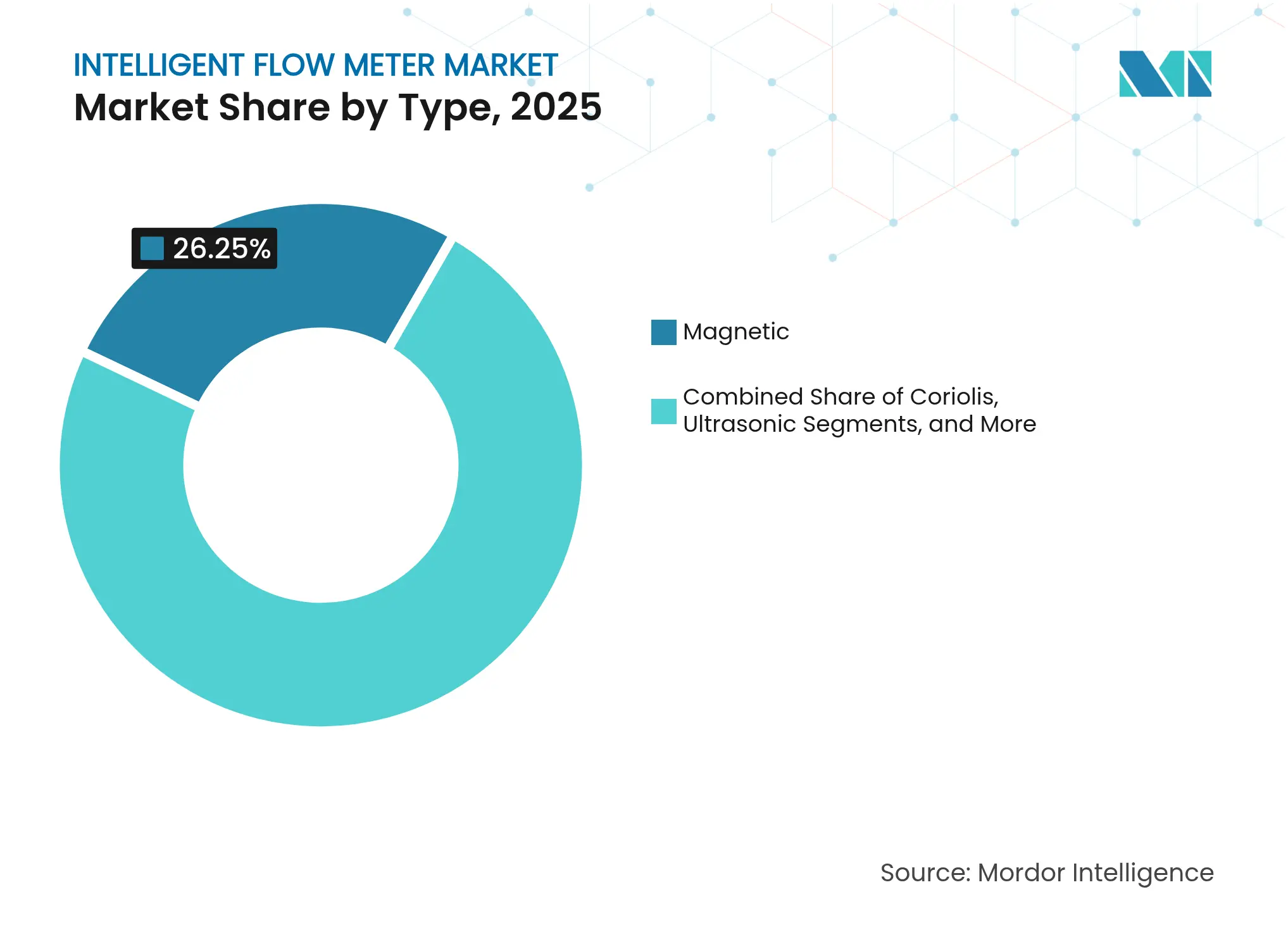

Magnetic devices generated 26.25% of 2025 revenues, benefitting from a rugged build that tolerates abrasive slurries without pressure loss. Utilities continue to standardize on magmeters for potable-water billing and wastewater aeration basins. Meanwhile, the agile multiphase category is logging an 7.75% CAGR as offshore operators push to eliminate bulky separators. The intelligent flow meter market size for multiphase instruments is forecast to reach USD 852 million by 2031, reflecting their ability to measure three-phase streams accurately at the wellhead. Coriolis designs hold shares in custody-transfer skids where mass flow, density, and temperature must be recorded simultaneously, saving space and minimizing leak paths. Vortex products serve steam loops and superheated gas lines thanks to a wide 30:1 turndown and built-in pressure, temperature, and energy calculations. Thermal, DP, and turbine variants continue in niche duty cycles, such as leak-detection loops or clean-liquid batching, preserving a diversified supplier ecosystem.

A secondary wave of innovation is combining complementary sensing principles in one body, for example, hybrid mag-ultrasonic designs that maintain accuracy under both laminar and turbulent flows. Suppliers are also embedding MEMS-based vibration sensors to detect early fouling, enabling operators to clean piping before flow coefficiencies slip.

Note: Segment shares of all individual segments available upon report purchase

By Communication Protocol: HART Legacy Meets Ethernet-IP Future

HART retained a 30.90% share in 2025, because brownfield facilities can add diagnostics over existing 4-20 mA loops without rewiring. That installed base means millions of devices speak HART, and migration is gradual. Nonetheless, Ethernet-IP links are gaining an 8.05% CAGR as factories flatten their networks and feed contextualized data directly into enterprise resource-planning suites. Modbus and PROFIBUS remain popular in legacy European chemical hubs where intrinsic-safety barriers have already been certified. Foundation Fieldbus still serves complex distributed-control arrangements, although additional crew training sometimes deters new adopters. The upcoming Ethernet-APL specification is poised to tip new project bids toward IP-native connections, given its 10 Mbit/s bandwidth and intrinsic-safety compliance in Zone 0 hazardous zones. As a result, the intelligent flow meter market is expected to see hybrid protocol stacks that auto-switch from HART to Ethernet to support phased upgrade paths.

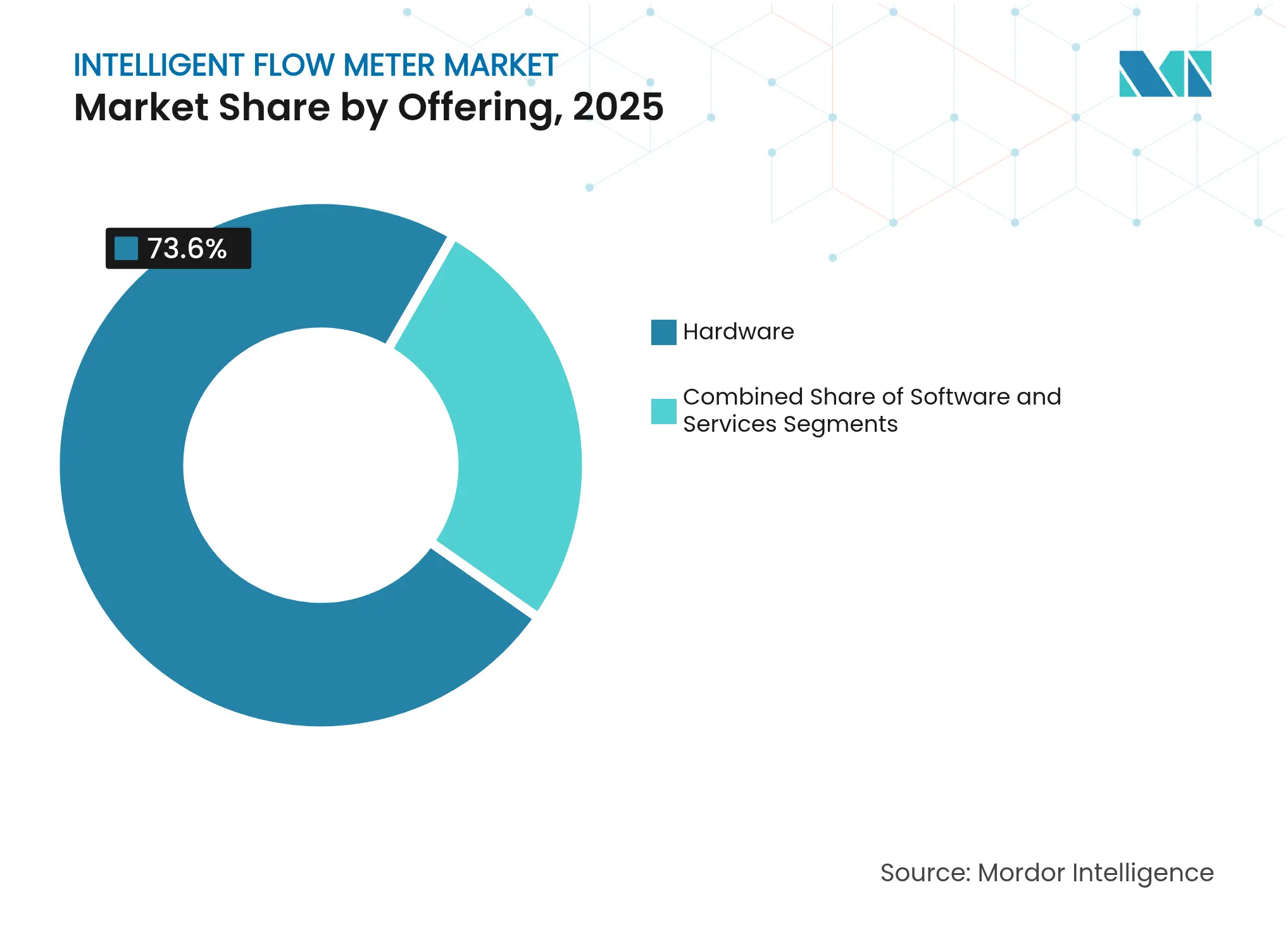

By Offering: Hardware Foundation Supports Software Growth

Hardware accounted for 73.60% of 2025 revenue, reflecting the capital nature of meter bodies, sensors, and primary elements. Customers typically keep these assets for 10-15 years, while swapping electronics every three to five years to capture new diagnostics. Software, however, is posting the strongest 8.72% CAGR. Cloud dashboards now harvest high-frequency samples, apply machine-learning scripts, and issue predictive-maintenance orders. For custody-transfer contracts, flow-computer applications reconcile meter readings with contractual tolerances, improving revenue assurance. Lifecycle services—remote calibration, spare-parts bundling, and performance-based service-level agreements—are gaining traction as plant managers outsource instrumentation upkeep. Accordingly, the intelligent flow meter market is tilting toward subscription-style revenue even as hardware remains indispensable.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Water Leadership Faces Power Generation Challenge

Water and wastewater operators held 25.30% of 2025 spending, driven by leak-loss programs and stricter discharge limits. Many utilities now link electromagnetic meters directly to GIS platforms that highlight abnormal consumption zones. The power-generation segment, growing at 7.42% CAGR, is installing multivariable vortex and ultrasonic meters in combined-cycle plants to fine-tune steam flows, maximize condenser vacuum, and support hydrogen-ready turbines. In the intelligent flow meter market, size growth linked to renewables is also materializing as pumped-storage schemes and green-hydrogen electrolyzers require tight flow control to safeguard membranes. Oil and gas firms continue to enhance custody-transfer skids, while pharmaceutical clean-rooms adopt single-use Coriolis probes that avoid cross-batch contamination.

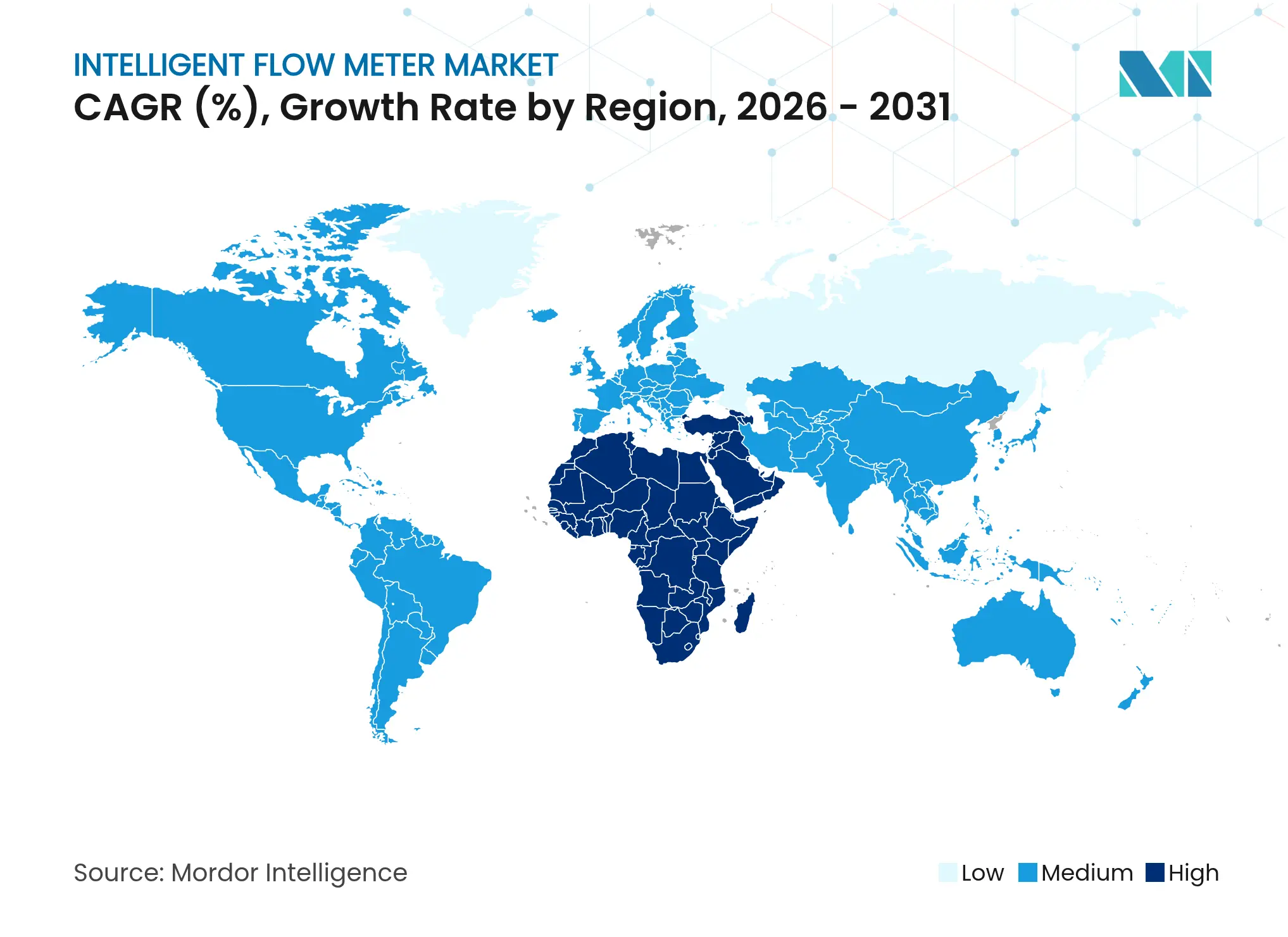

Asia-Pacific contributed 37.85% of global revenue in 2025, buoyed by rapid industrial build-outs and government-funded refinery upgrades across China and India. National water-quality frameworks are compelling municipalities to install non-intrusive ultrasonic meters that avoid service interruptions.

The Middle East and Africa region, boosted by Saudi Arabia’s NEOM and the UAE’s desalination pipeline, is advancing at 7.63% CAGR. Local EPC firms increasingly specify Ethernet-APL-ready vortex meters to future-proof new plants. North America and Europe together accounted for just under 44.60% of the 2025 value, with replacement demand dominated by process-safety upgrades and energy-efficiency retrofits. Europe’s push for net-zero manufacturing is spurring investments in multiparameter Coriolis units that calculate real-time carbon intensity.

Market Concentration

The intelligent flow meter market hosts a moderately fragmented ecosystem, with the top five suppliers together holding roughly 55% of 2024 revenue. ABB, Endress+Hauser, Emerson, Siemens, and Yokogawa deploy global support teams, in-house ASIC production, and vertically integrated service divisions to fend off challengers. Each also markets multiparameter platforms that combine flow, density, and pressure sensing to lock in higher per-meter value. Honeywell moved decisively in March 2025 by paying USD 2.2 billion for Sundyne, adding high-speed pump and compressor lines that bundle flow-meter spares under a single maintenance contract. [4]Honeywell International Inc., “Honeywell to Acquire Sundyne,” investor.honeywell.com

Start-ups focused on wireless clamp-on ultrasonic probes are differentiating through battery lives exceeding 10 years and cloud-native dashboards that spin up in minutes. Because procurement officers increasingly consider cybersecurity-by-design as a tender requirement, incumbents are pouring R&D into secure bootloaders and IEC 62443-certified firmware. Patent filings show a surge in sensor-fusion and AI-driven self-calibration, underscoring the sector’s drift toward software-defined measurement.

Supply-chain resilience is a new battleground. During the 2024 microcontroller shortage, vendors with dual-sourcing agreements and regionalized PCB assembly plants met delivery windows, winning multiyear framework agreements. Others responded by redesigning boards around widely available 32-bit MCUs, reducing lead times from 52 weeks to under 20. Aftermarket service packages that guarantee 98% fleet availability are gaining traction, further blurring lines between hardware, software, and services.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Flow control is a very important process in any industry since control of many parameters in the industry is achieved by control of flow. An Intelligent flow meter works by measuring the amount of liquid, gas, or steam flowing through or around the flow meter sensors.

The Intelligent Flow Meter Market is Segmented by Type (Coriolis, Magnetic, Ultrasonic, Multiphase, Vortex, Variable Area, Differential Pressure, Thermal, Turbine), Communication Protocol (Profibus, Modbus, Hart), End-user Industry (Oil and Gas, Pharmaceuticals, Water and Wastewater, Paper and Pulp, Power Generation, Food and Beverages), and Geography.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.