Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

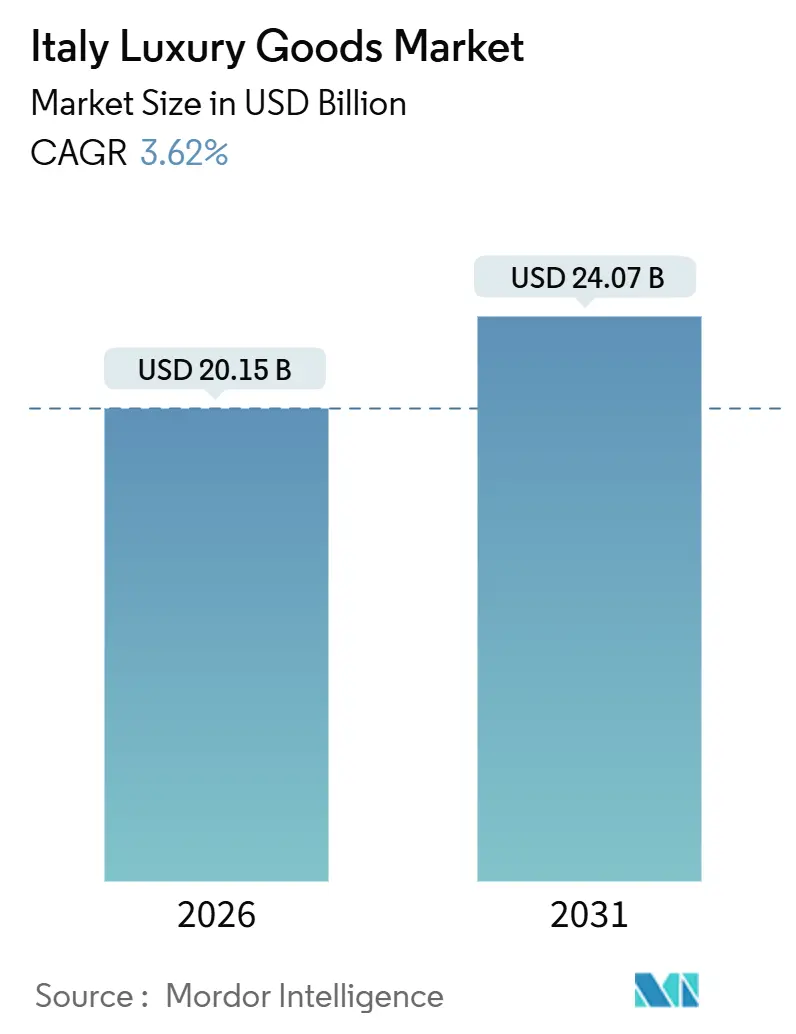

| Market Size (2026) | USD 20.15 Billion |

| Market Size (2031) | USD 24.07 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

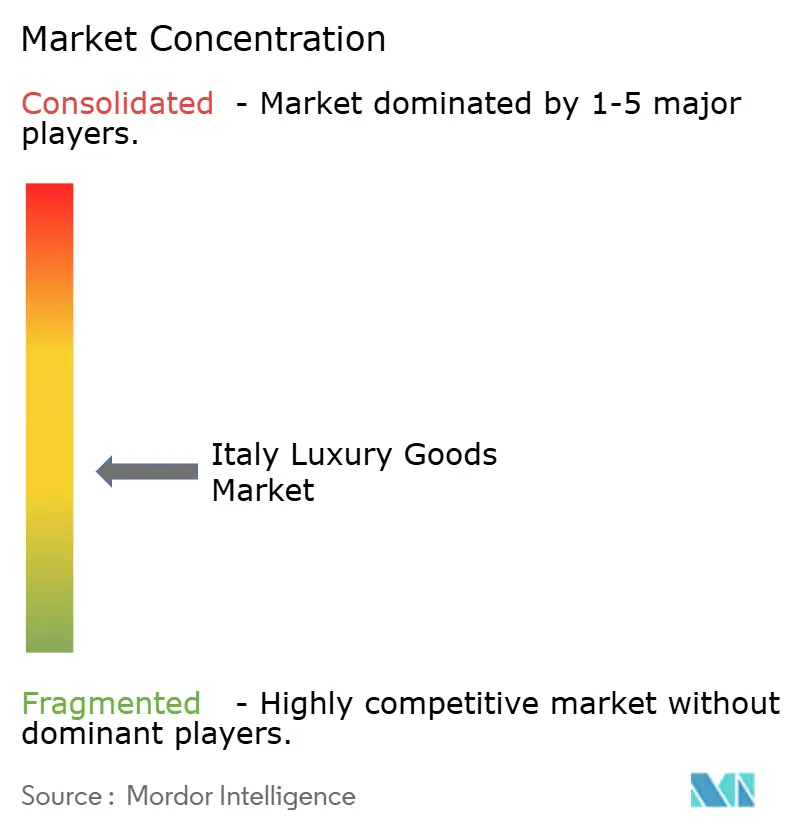

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Luxury Goods Market Analysis by Mordor Intelligence

Italy's luxury goods market is expected to reach USD 20.15 billion by 2026 and grow further to USD 24.07 billion by 2031, with a steady CAGR of 3.62%. This growth is driven by changes in how brands operate, focusing more on verifying product origins, adopting sustainable practices, and using digital marketing. Global demand is rising, mainly due to spending by international tourists. The watch segment is expected to grow the fastest, while clothing and apparel remain the top revenue generators. Companies are combining traditional brand values with innovative products to stay competitive. In terms of distribution, single-brand retail stores generate the most revenue, but online platforms are growing the fastest, showing the importance of omnichannel retail in Italy's luxury market. Government policies, such as Italian manufacturing certification and updates to the tourist VAT refund system, are supporting market growth. Stronger anti-counterfeiting measures are also helping by reducing illegal trade and protecting intellectual property.

Key Report Takeaways

- By product type, clothing and apparel captured 47.85% of the Italy luxury goods market share in 2025, whereas watches are forecast to expand at a 3.75% CAGR to 2031.

- By end user, women accounted for 58.45% of the Italy luxury goods market in 2025, while the men’s segment is advancing at a 4.24% CAGR through 2031.

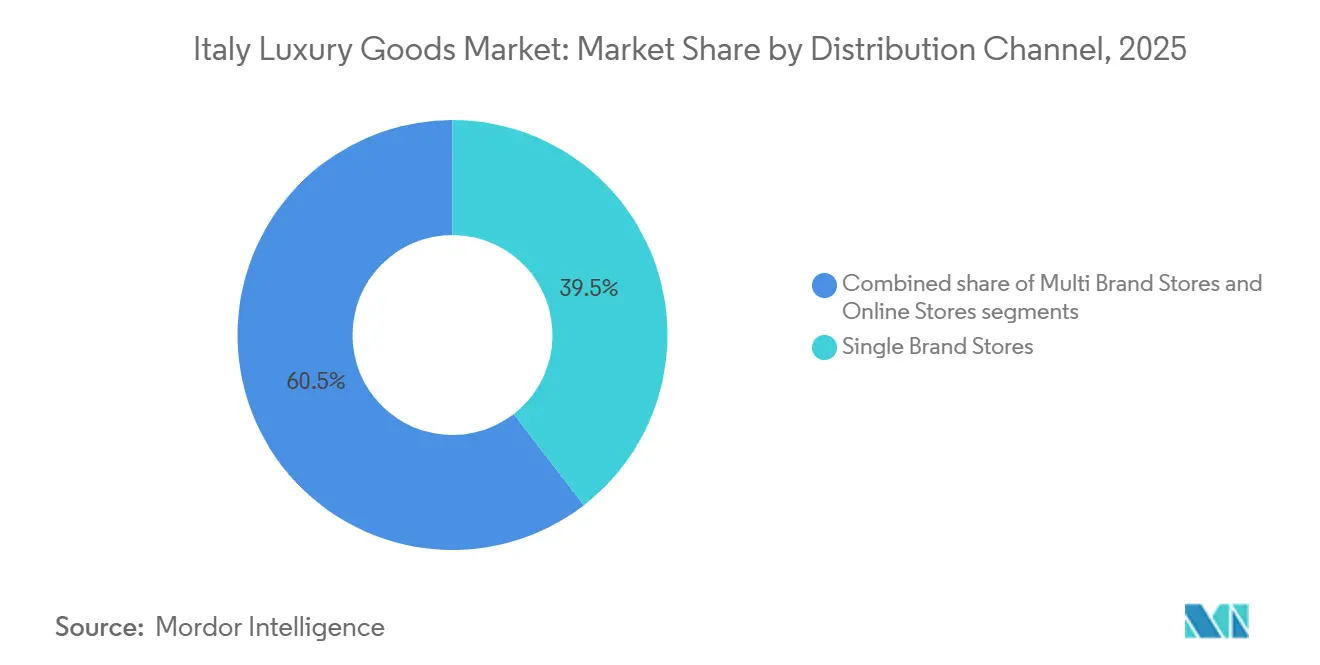

- By distribution channel, single-brand stores held 39.53% revenue share in 2025; online stores are growing fastest at a 4.73% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Italian craftsmanship in luxury goods being perceived as a status symbol | +1.2% | Global, with strongest effect in China, Middle East, and North America | Medium term (3-4 years) |

| Growing demand for sustainable high-end materials | +0.8% | Europe, North America, with emerging influence in Asia-Pacific | Long term (≥ 5 years) |

| Influence of social media and celebrity endorsement | +0.7% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Aggressive marketing by reputed brands | +0.5% | Global, with concentration in major luxury markets | Medium term (3-4 years) |

| Product innovation in terms of raw material and design | +0.9% | Global, with particular strength in European and North American markets | Medium term (3-4 years) |

| Technology integration in luxury retail improves shopping experiences | +0.6% | Global, with faster adoption in Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Italian Craftsmanship in Luxury Goods Being Perceived as a Status Symbol

Italian craftsmanship has transitioned from merely a hallmark of quality to a pivotal competitive edge in the global luxury arena. This is especially evident in the watch segment, where Italian design now stands toe-to-toe with Swiss manufacturing. Italy's manufacturing ethos prioritizes handcrafted nuances, design innovation, and a rich cultural legacy over sheer technical engineering. The "Made in Italy" label has transcended its geographical roots, now symbolizing heritage, exclusivity, and unparalleled craftsmanship. Luxury brands leverage this prestigious positioning through four primary strategies: anchoring in Italian locales, sourcing premium materials, emphasizing meticulous manufacturing, and forging ties with Italy's culinary and cultural landmarks. The Italian government reinforced this market position by implementing an official certification seal in 2023 for Italian-manufactured products, aiming to ensure product authenticity and differentiate genuine Italian luxury items from unauthorized replicas [1]Source: University of Parma, "The 'Made In Italy State Seal' To Promote Italian Excellences", foodforfuture.unipr.it. Domestically, luxury clothing and apparel emerge as key differentiators for affluent consumers. Italian shoppers, valuing premium quality, gravitate towards apparel that resonates with both local tastes and global trends. This segment is witnessing robust growth, largely fueled by the millennial and Gen Z demographics. These younger consumers are not only more attuned to seasonal launches and digital marketing but also demand corporate transparency. Their evolving consumption patterns are reshaping market dynamics, pushing manufacturers to marry product excellence with sustainability, ethical practices, and a touch of cultural authenticity.

Growing Demand for Sustainable High-end Materials

Italian luxury brands are prioritizing sustainability, largely due to the European Union's Digital Product Passport (DPP), which becomes mandatory by 2030. This regulation mandates comprehensive documentation of products' environmental credentials, pushing brands to guarantee transparency in their material sourcing and production. While navigating these compliance challenges is daunting, it presents Italian luxury houses with a chance to stand out in a crowded marketplace. The DPP aligns with the EU's Circular Economy Action Plan, which aims to make textiles durable, recyclable, and sustainably produced by 2030. Italy, as the fourth-largest apparel market in the European Union, reported an import value of EUR 18.2 billion in 2023, highlighting its pivotal role in the European textile industry [2]Source: Government of Netherlands, "The European Market Potential for Sustainable Materials", cbi.eu. In light of these developments, Italian brands are channeling investments into traceable supply chains and embracing circular economy principles. Yet, the Italian market grapples with hurdles. While there's a push for sustainable apparel, consumer awareness lags, and many hesitate to pay extra for these products. Instead, decisions lean more towards price, fit, and quality. This gap highlights the urgency for brands to not only pioneer sustainable practices but also to educate consumers, aligning market demand with sustainability efforts.

Influence of Social Media and Celebrity Endorsement

Italian luxury brands are balancing exclusivity with a growing presence on social media. These brands roll out targeted content strategies, especially during major events like Milan Fashion Week. Their marketing now weaves in strategic narratives and cultural relevance, moving beyond just premium visuals. Celebrities and influencers have shifted from mere endorsements to collaborative content roles, helping convey brand heritage and values. This approach resonates with Generation Z, who value genuine communication over conventional luxury markers. Moreover, partnerships with influencers are now central to brand strategies, aiding in market growth while preserving brand identity. A case in point: Gucci named BTS member Jin as its global ambassador in August 2024. Jin's presence in GG monogram designs not only highlighted Gucci's product quality but also its appeal to younger audiences. In tune with market dynamics, Italian luxury brands are ramping up their digital investments, honing in on content marketing, strategic messaging, and influencer collaborations. This pivot signals a broader industry evolution, blending digital strategies with age-old manufacturing prowess for a richer market experience.

Aggressive Marketing by Reputed Brands

Italian luxury brands are evolving, adopting sophisticated, consumer-centric marketing strategies that transcend traditional advertising. This evolution is especially pronounced in the men's luxury segment, which is set to grow at a CAGR of 4.24% from 2026 to 2031. In light of this growth, brands are increasingly embracing direct-to-consumer (DTC) models, placing a premium on personalized service, curated experiences, and brand-led storytelling. Zegna exemplifies this trend, reporting a notable 10.2% year-on-year revenue increase, reaching EUR 953.6 million in 2024. Much of Zegna's success is attributed to its DTC strategy, which seamlessly integrates physical retail with digital touchpoints, enhancing customer loyalty and lifetime value. Furthermore, Italy's tax-free shopping incentives bolster these brands' successes. In 2024, tax-free sales surged by 20%, driven by a rebound in international tourism, especially from the U.S., Canada, China, and the Middle East – all pivotal markets for Italian luxury. Germany generated the highest number of tourist arrivals in Italy during 2023, accounting for 12.5 million visitors. The United States recorded 4.1 million arrivals, while Canada and Australia reported 0.9 million and 0.6 million arrivals, respectively, as per Banca d'Italia [3]Source: Banca d'Italia, “International Tourism Survey – June 2024”, bancaditalia.it. This stark contrast emphasizes the need for Italian luxury brands to adopt hyper-personalized marketing strategies, catering to this elite group, ensuring exclusivity, and driving high-margin growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products | -0.9% | Global, with concentration in Southern Italy, particularly Naples | Medium term (3-4 years) |

| Lesser demand from price sensitive consumers | -0.6% | Global, with particular impact in emerging markets | Short term (≤ 2 years) |

| Brexit-related trade barriers increase operational costs and retail prices | -0.4% | Europe, with spillover effects to global operations | Medium term (3-4 years) |

| Labor shortages in specialized craftsmanship | -0.7% | Italy, with particular impact in traditional manufacturing regions | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit Products

In 2024, the Italian Ministry of Enterprises intensified its battle against counterfeiting, seizing nearly 9,000 counterfeit products, shutting down 354 websites, and issuing over 2,000 fines. These actions stemmed from the enforcement measures of the "Made in Italy" law, designed to safeguard the integrity of Italian luxury goods. Counterfeiting remains a significant economic challenge, with repercussions that extend beyond mere financial losses. A study by the European Union Intellectual Property Office highlighted that counterfeiting has led to a loss of 160,000 jobs in Europe's clothing sector, with Italy bearing a substantial brunt. In response, 2023 amendments to the Code of Industrial Property bolstered protections for unregistered trademarks and trade secrets, reinforcing legal safeguards for intellectual property. Furthermore, the Italian Customs Agency has enhanced border control operations, leveraging advanced multimedia databases for more efficient identification and interception of counterfeit goods. Penalties for intellectual property infringement have been heightened, introducing stricter prison sentences and elevated fines as deterrents. These concerted efforts underscore Italy's commitment to safeguarding its luxury goods market and mitigating the broader economic impacts of counterfeiting.

Lesser Demand from Price-Sensitive Consumers

Italian consumers are changing how they spend on luxury goods due to economic challenges, inflation, and higher living costs. This change is most noticeable among middle-income and aspirational buyers, who are now more focused on price and value. Ultra-high-net-worth individuals (UHNWI) still buy luxury items but are becoming more selective, preferring experiences over products. To adapt, Italian luxury brands are emphasizing their storytelling, heritage, and craftsmanship to maintain their premium image. They are avoiding discounts to protect their brand value. For example, Brunello Cucinelli follows a "humanistic capitalism" approach, focusing on "fair pricing" instead of growing sales volume. However, many consumers, especially new luxury buyers, are unhappy with frequent price increases and question how sustainable this approach is. To address this, Italian brands are introducing new strategies like unique retail experiences, limited-edition collections, and personalized direct-to-consumer services to enhance value without raising prices. Still, it is uncertain if these efforts will successfully balance exclusivity with price sensitivity in the long run.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clothing Dominance Meets Watch Innovation

In 2025, clothing and apparel lead Italy's luxury goods market with a 47.85% share. This reflects Italy's strong fashion heritage and global reputation for craftsmanship. The country is a key supplier for European luxury brands and a production hub for top global fashion houses like Gucci, Prada, and Valentino. These brands maintain Italy's premium fashion status through traditional craftsmanship and steady consumer demand. The fashion industry is both a cultural symbol and a major economic contributor, employing millions and significantly boosting the national GDP.

Watches are the fastest-growing segment in Italy's luxury market, with a projected CAGR of 3.75% from 2026 to 2031. Their growth is driven by their appeal as investment assets and status symbols. Watches consistently achieve higher transaction values than other luxury items, showing their aspirational value. The second-hand watch market is expanding rapidly, especially among younger consumers who value the affordability, exclusivity, and prestige of pre-owned pieces. Neo-vintage models and independent watchmakers are gaining popularity, reflecting a shift toward unique and personalized luxury. These trends highlight the watch segment's strong growth potential and innovation.

By End User: Men Drive Growth Momentum

In 2025, women dominate the Italian luxury goods market, holding a commanding 58.45% share. This surge is fueled by strong demand across apparel, leather goods, jewelry, and beauty sectors. Renowned Italian brands, including Gucci, Prada, and Valentino, seamlessly blend traditional craftsmanship with modern aesthetics. The women's segment is thriving, driven by evolving consumer values that prioritize high-quality, sustainable, and ethically produced goods. Additionally, the rise of experiential retail, personalized shopping, and omnichannel engagement, especially on digital platforms, strengthens brand loyalty among female consumers. While growth in the women's luxury segment remains steady, it's firmly anchored in Italy's luxury landscape, supported by consistent spending from both domestic and international buyers.

Conversely, the men's luxury segment is witnessing a robust ascent, with projections indicating a CAGR of 4.24% from 2026 to 2031. This growth highlights evolving gender norms, as men increasingly explore luxury categories like skincare, fine jewelry, and accessories, areas once predominantly associated with women. Acknowledging this shift, Italian luxury houses are making targeted innovations and strategic investments. For instance, Brioni is enhancing its menswear's artisanal touch by inaugurating a new tailoring school, emphasizing craftsmanship and cultivating future talent.

By Distribution Channel: Digital Transformation Reshapes Retail

In 2025, single-brand stores lead the Italian luxury goods market with a 39.53% share, giving brands strong control over customer interactions and brand image. These stores meet the luxury segment's needs by offering private shopping events, bespoke services, and exclusive product launches. Luxury companies are expanding in Italy by opening standalone stores in prime locations. For example, in July 2024, Chaumet opened its first Italian boutique in Rome, showcasing signature collections and premium jewelry. With stores in cities like Rome, Florence, and Milan, Chaumet aims to strengthen its connection with Italian customers.

Online platforms are the fastest-growing distribution channel, with a projected CAGR of 4.73% from 2026 to 2031. This growth reflects the shift to online shopping and the adoption of advanced digital technologies. Luxury brands are enhancing their online stores with interactive features and technologies like augmented reality to improve the shopping experience. The rise of mobile commerce highlights the need for seamless, mobile-friendly platforms, making digital channels essential for attracting younger, tech-savvy consumers.

Geography Analysis

Tax-free shopping in Italy is growing rapidly, driven by an increasing number of wealthy tourists from North America, Asia-Pacific, and the Middle East. American tourists are the biggest spenders, showing a strong interest in luxury goods. Ultra High Net Worth Individuals (UHNWI) also make up a significant part of these shoppers. This trend emphasizes the need for luxury retailers to offer personalized services and exclusive products to attract and retain these high-spending international customers.

At the same time, meeting the needs of local consumers is important to keep the market balanced. The recent introduction of a VAT rebate threshold of EUR 70 has made shopping easier for tourists. This change not only improves their shopping experience but also strengthens Italy’s reputation as a top destination for luxury shopping.

Italy’s regional luxury manufacturing hubs are key to its global leadership in craftsmanship and quality. The Brenta district and Tuscany are well-known for their skilled artisans, high-quality production, and strong traditions. However, these regions face challenges from globalization, changing consumer preferences, and the fast adoption of digital technologies. To tackle these issues, they are combining traditional craftsmanship with modern technology. This approach helps preserve Italy’s artisanal heritage while ensuring its luxury manufacturing sector can meet the demands of the global market. By balancing tradition with innovation, Italy continues to strengthen its position and ensure its luxury goods industry remains competitive and ready for the future.

Competitive Landscape

Italian luxury brands have established a strong global presence with a wide range of products. Major players like LVMH Moët Hennessy Louis Vuitton, Compagnie Financière Richemont SA, Kering, Prada SpA, and Rolex SA lead the market with significant shares. These companies are not only launching new products but also forming partnerships to expand their retail networks and strengthen their market position. With the rise of digital platforms, they are heavily investing in online channels, including e-commerce websites and their own online stores. To stay ahead, Italian luxury brands are focusing on ethical production, sustainable sourcing, and using social media to reach a larger audience.

In the first half of 2024, Italian luxury brands performed better than their French competitors. Prada reported a 17% increase in net revenues, reaching EUR 2.55 billion. This growth was mainly driven by a 93% rise in Miu Miu's retail sales and strong demand in key regions such as Asia Pacific, Europe, Japan, and the Middle East. On the other hand, LVMH saw a modest 2% revenue growth, reaching EUR 41.7 billion, while Kering experienced an 11% drop in revenues, totaling EUR 9 billion. These results highlight the strength and adaptability of Italian luxury brands in the global market.

Sustainability and digital innovation are becoming key strategies for standing out in the market. Brands are using advanced technologies like AI and blockchain to improve supply chain transparency and provide better customer experiences. Additionally, the unique quality of Italian craftsmanship is being officially recognized through initiatives like the state seal for Italian-made goods. This seal helps distinguish authentic Italian luxury products from similar items made elsewhere, reinforcing the value of Italian luxury in the global market.

Italy Luxury Goods Industry Leaders

-

Prada SpA

-

Moncler SpA

-

Giorgio Armani SpA

-

OTB Group

-

Ermenegildo Zegna

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kering Eyewear and Google established a strategic collaboration to develop smart glasses utilizing the Android XR platform. The partnership integrates Kering's luxury design expertise with Google's extended reality technology to manufacture functional smart eyewear.

- May 2025: Dolce & Gabbana and Havaianas are releasing their second and final collaborative footwear collection for summer 2025. The collection enhances the traditional sandal design with premium elements, distinct colors, and established patterns including leopard, zebra, Banano, and florals. Select models incorporate faux fur or handcrafted macramé straps. The three primary designs feature gold metallic Havaianas logos and Dolce & Gabbana pins. The limited-edition collection will be distributed through both brands' retail locations and e-commerce platforms.

- May 2025: Bvlgari established its flagship retail location in Milan's premium commercial district on Via Montenapoleone. Situated in the historic Taverna Radice Fossati building, the 750-square-meter retail space operates across three floors, integrating Roman architectural elements with Milanese design characteristics. The establishment presents the company's core product lines, including Serpenti, B.zero1, Divas' Dream, and Octo. The location houses the "Tubogas & Beyond" exhibition, featuring historical artifacts such as the original 1941 Tubogas bracelet and a Monete Tubogas choker formerly in the possession of Frank and Barbara Sinatra.

- June 2024: Cartier established its first retail location at Rome's Fiumicino Airport, marking its entry into the Italian airport market. The retail operation, launched in partnership with Italian luxury retailer ROCCA, commenced business on June 1st. The retail space, positioned in Terminal 3, features Cartier's complete product portfolio, encompassing jewelry, timepieces, leather goods, fragrances, and accessories.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Italy's luxury goods market as retail sales of high-end apparel, footwear, leather goods, eyewear, jewelry, watches, and premium beauty items that command prestige pricing and brand equity among domestic residents and inbound tourists.

Scope Exclusions: Cars, yachts, fine art, and real-estate investments remain outside this review.

Segmentation Overview

-

By Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Leather Goods

- Jewelry

- Watches

- Beauty and Personal Care

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Single Brand Stores

- Multi Brand Stores

- Online Stores

Detailed Research Methodology and Data Validation

Primary Research

Store managers in Milan's Quadrilatero, luxury e-commerce merchandisers, artisan guild heads, and affluent shoppers across Rome, Florence, and Venice share hard numbers on unit throughput, average selling prices, and seasonality swings. Insights from these interviews refine assumptions drawn from desk work and help us triangulate growth signals across consumer cohorts.

Desk Research

We first gather baseline figures from publicly available, high-credibility sources such as ISTAT retail statistics, Bank of Italy card-spend and tourist-refund data, Confindustria Moda trade briefs, Italian Customs tariff files, and European Commission VAT datasets. Company filings and select paid repositories, including D&B Hoovers and Dow Jones Factiva, supply brand-level revenue clues and channel commentary. These references illustrate but do not exhaust the wider document set our analysts mine; many other publications underpin data checks and clarifications.

Market-Sizing & Forecasting

A top-down demand pool build combines household disposable-income tiers with tourist duty-free receipts, which are then benchmarked against retail turnover indices. Results are stress tested through selective bottom-up roll-ups of sampled ASP × volume data from flagship stores, department chains, and online platforms. Key model inputs include inbound leisure arrivals, VAT-refund slip counts, median ticket price shifts, store footprint additions, and digital-channel penetration. Multivariate regression, supplemented by scenario analysis for macro swings, drives the 2025-2030 forecast. Assumption gaps in bottom-up samples are bridged by weighted averages from nearest known peers.

Data Validation & Update Cycle

Mordor analysts run variance and anomaly screens, compare outputs with external luxury confidence barometers, and escalate any outliers for senior review. Reports refresh each year, with interim revisions triggered by material events, such as currency jolts, tax rule changes, or mergers. A final pre-publication audit ensures clients receive the most current view.

Why Mordor's Italy Luxury Goods Baseline Holds Firm Ground

Published estimates frequently diverge because firms apply different product scopes, currency bases, and refresh cadences. Our disciplined variable selection and dual-path modeling yield a balanced midpoint that decision-makers can retrace.

Key gap drivers include scope carve-outs (e.g., some studies drop beauty or eyewear), unadjusted gray-market flows, and one-off tourist spikes baked into base years. Mordor's annual refresh and category-level filters smooth these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.85 B (2025) | Mordor Intelligence | |

| USD 22.14 B (2024) | Global Consultancy A | Excludes premium cosmetics; blends travel-retail receipts with domestic sell-in |

| USD 22.00 B (2024) | Industry Research Firm B | Allocates global brand revenues to Italy without netting gray-market exports |

| USD 12.26 B (2024) | Analytics Provider C | Covers personal luxury only, omitting footwear and eyewear segments |

Taken together, the comparison shows that while other publishers swing wide due to selective category cuts or opaque allocations, Mordor's carefully documented scope and recurrent validation steps deliver a transparent, dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the Italy luxury goods market?

The sector generates USD 20.15 billion in 2026 revenue and is on course to reach USD 24.07 billion by 2031.

Which product segment is growing fastest?

Watches lead growth at a 3.75% CAGR for 2026-2031, supported by rising demand for collectible timepieces and authenticity certification.

Why are online sales important for luxury brands in Italy?

Online stores are expanding at a 4.73% CAGR because mobile commerce already accounts for half of Italian e-commerce spending, and omnichannel buyers spend more per transaction.

What policy changes will shape sustainability in Italy luxury Goods Market?

EU-mandated Digital Product Passports, due by 2030, will require every luxury item to display detailed environmental data, pushing brands to trace materials and disclose emissions.

Page last updated on: