Italy Location-Based Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

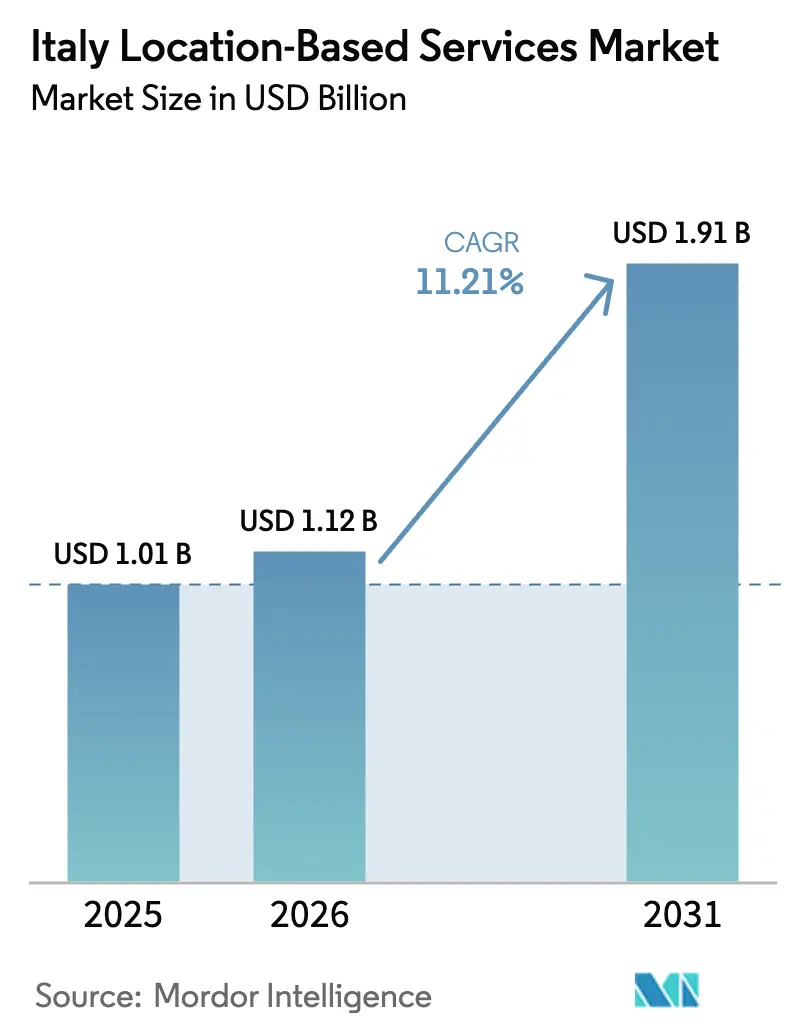

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

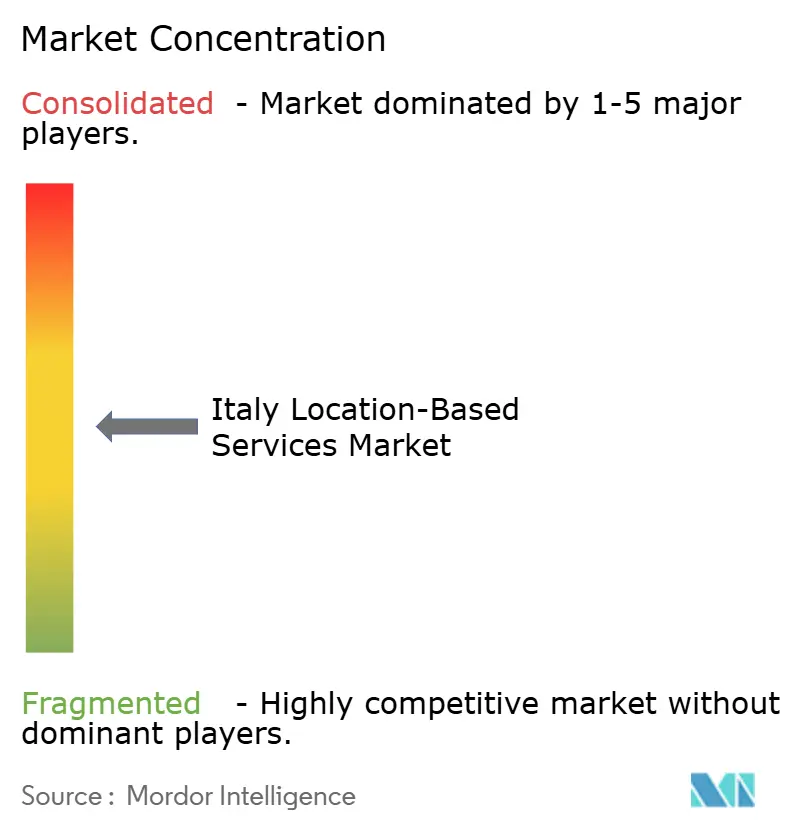

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Location-Based Services Market Analysis by Mordor Intelligence

The Italy Location-Based Services Market size in 2026 is estimated at USD 1.12 billion, growing from 2025 value of USD 1.01 billion with 2031 projections showing USD 1.91 billion, growing at 11.21% CAGR over 2026-2031. Growth is propelled by rapid 5G and NB-IoT roll-outs, sizeable National Recovery and Resilience Plan (PNRR) allocations for smart mobility, and rising enterprise demand for real-time asset visibility. Northern Italy’s industrial cluster, sustained investments from WindTre, TIM, and Fastweb+Vodafone, and mounting retail appetite for proximity advertising create immediate revenue upside. At the same time, strict GDPR enforcement stimulates privacy-first European providers, while technology fragmentation inside facilities restrains large-scale indoor deployments. Intensifying competition pushes vendors toward edge intelligence, ultra-low-power beacons, and verticalized software as differentiators in an increasingly sophisticated buyer landscape.

Key Report Takeaways

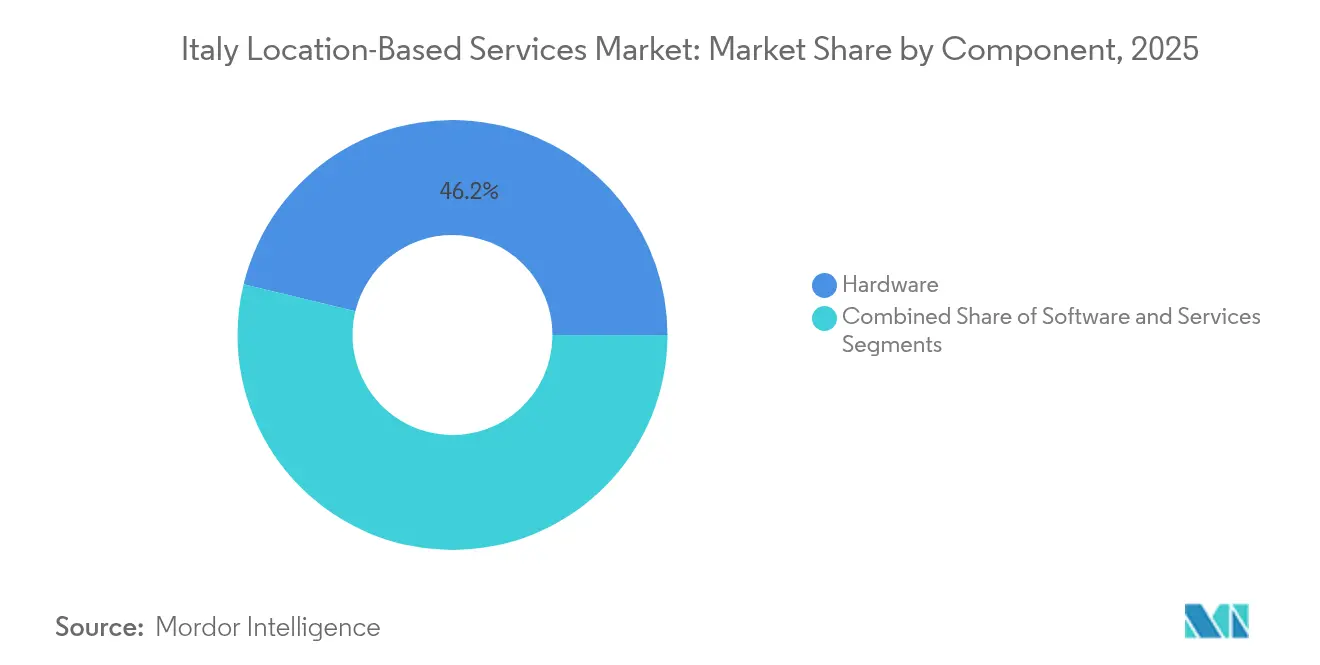

- By component, hardware led with 46.20% revenue share in 2025, whereas software posted the fastest 13.77% CAGR to 2031.

- By technology, GPS/GNSS captured 39.65% of the Italy location-based services market share in 2025, while cellular (5G, LTE, NB-IoT) is forecast to expand at a 14.04% CAGR through 2031.

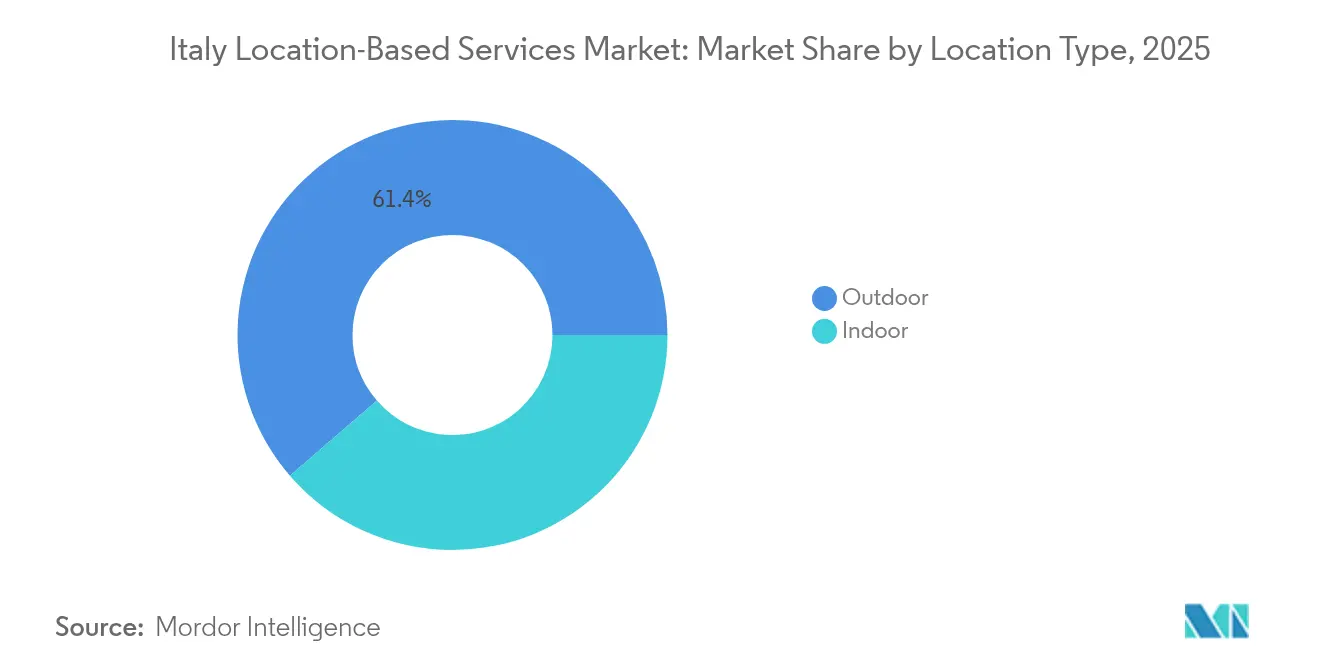

- By location type, outdoor solutions held 61.35% share of the Italy location-based services market size in 2025; indoor positioning is advancing at a 14.65% CAGR to 2031.

- By deployment mode, cloud platforms accounted for 54.85% revenue share in 2025, yet edge/fog computing records the highest 13.48% CAGR to 2031.

- By application, mapping and navigation commanded a 33.05% share, while asset tracking and fleet management posted a 13.58% CAGR between 2026-2031.

- By end-user vertical, transportation and logistics led with a 26.25% share in 2025; retail and e-commerce are projected to grow at a 13.46% CAGR.

- By region, Northern Italy dominated with a 49.70% share in 2025, whereas Southern Italy and the Islands registered the fastest 13.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy participates in a competitive field that extends beyond its own borders. The market landscape in the global location based services industry outlined by Mordor Intelligence covers that wider structure.

Italy Location-Based Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G and NB-IoT rollout boosts sub-meter accuracy | +2.8% | National, with early gains in Milan, Rome, Turin | Medium term (2-4 years) |

| EU Digital Markets Act catalyzes app-level LBS interoperability | +1.9% | National, aligned with EU-wide implementation | Long term (≥ 4 years) |

| National PNRR funds for smart mobility and ITS projects | +2.1% | National, concentrated in Southern Italy development | Medium term (2-4 years) |

| Retailers' surge in location-based advertising spend | +1.7% | National, with higher concentration in Northern commercial centers | Short term (≤ 2 years) |

| Industry 4.0 demand for indoor positioning in factories and hospitals | +1.5% | Northern Italy manufacturing belt, major healthcare centers | Medium term (2-4 years) |

| Open-data ecosystems (OpenStreetMap, EU Data Spaces) lower entry barriers | +1.0% | National, supporting SME adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G and NB-IoT Rollout Boosts Sub-Meter Accuracy

Italian operators blanket cities with dense small-cell grids and NB-IoT overlays, enabling precision location services that now reach sub-meter performance in live trials. TIM covers 5,000 municipalities with NB-IoT, while WindTre’s 5G network delivers 1.6 Gbps peak speeds that support high-definition positioning flows. [1]WINDTRE, “Caratteristiche della nostra rete veloce 5G,” windtre.it The EUR 97.7 million #Roma5G project alone installed 2,200 small cells and 1,800 IoT sensors across the capital, illustrating how public-private consortiums accelerate coverage. [2]Boldyn Networks, “City of Rome and Boldyn Networks kick off #Roma5G,” boldyn.com Research at Politecnico di Torino confirms 3.2 cm accuracy when ultra-wideband systems interwork with 5G edge nodes, reducing the need for stand-alone beacons. EOLO’s mmWave stand-alone network further trims latency for industrial use cases that demand deterministic positioning.

EU Digital Markets Act Catalyzes App-Level LBS Interoperability

The Act enforces open APIs and data portability, dismantling vendor lock-in that long hampered Italian municipalities. Platforms such as TIM Urban Genius now merge cellular telemetry, IoT feeds, and third-party apps into a cohesive smart-city canvas. Indoor-positioning specialist Nextome leverages the new rules to link its SDK seamlessly with external analytics engines, broadening addressable markets beyond hospitals and factories. Bolzano’s MaaS pilot, funded with EUR 2.3 million, shows how standardised interfaces let mobility operators stitch together buses, bikes, and parking into a single location-aware service. In turn, rising platform interoperability intensifies competition, lowering switching costs for enterprises and pushing suppliers toward differentiated analytics rather than proprietary data silos.

National PNRR Funds for Smart Mobility and ITS Projects

Italy earmarks EUR 191.5 billion for digital transformation, with smart mobility among the earliest spending lines. The European Investment Bank has already injected EUR 500 million into a tourism-focused thematic fund that prioritises location intelligence for seamless visitor movement. Southern regions gain the most: Puglia’s EUR 170 million Active Network integrates smart grids with EV charging guided by live geospatial analytics. TIM secured EUR 750 million in advance government contracts to extend fibre backhaul into underserved municipalities, effectively preparing rural areas for industrial LBS deployments. More than 1,000 smart-city schemes now run nationwide, each embedding traffic, environment, or citizen-service layers underpinned by location data.

Retailers’ Surge in Location-Based Advertising Spend

Hyperlocal marketing budgets swell as Italian chains witness tangible footfall gains. Stellantis &You registered 48% more dealership visits after tailoring campaigns to micro-zones around showrooms. Start-ups such as Blimp feed real-time pedestrian counters into demand-side platforms, letting retailers bid dynamically on foot-traffic hotspots. Content platforms like ZonzoFox catalogue 1,400 parks and 1,500 beaches, selling context-rich ad slots to hospitality brands keen on inbound tourist spend. A growing pool of case studies demonstrates click-through rates that surpass national digital averages, convincing more merchants to allocate incremental budgets to geofencing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-driven privacy sanctions on geo-tracking | -2.3% | National, with stricter enforcement in major cities | Short term (≤ 2 years) |

| Fragmented indoor-positioning technology standards | -1.8% | National, affecting enterprise adoption | Medium term (2-4 years) |

| High capex of UWB/BLE beacon roll-outs for SMEs | -1.2% | National, particularly affecting smaller enterprises | Medium term (2-4 years) |

| Multipath signal distortion in dense historical city cores | -0.9% | Historical city centers (Rome, Florence, Venice, Naples) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Privacy Sanctions on Geo-Tracking

Italy’s regulator imposes hefty fines on companies mishandling location data, exemplified by a EUR 2.6 million penalty levied on Foodinho for non-transparent rider tracking. [3]Garante per la protezione dei dati personali, “Order against Foodinho S.r.l.,” garanteprivacy.it The authority’s ban on Google Analytics over trans-Atlantic transfers magnifies compliance anxiety for global providers. Local law further compels explicit, revocable consent for all geo-tracking, elevating administrative overhead for app developers. Resulting cost pressure nudges enterprises toward Europe-based vendors able to guarantee regional data residency, though smaller firms sometimes delay LBS roll-outs until legal clarity improves.

Fragmented Indoor-Positioning Technology Standards

Hospitals, factories, and malls struggle with incompatible protocols across UWB, BLE, Wi-Fi, and hybrid tags. A Siena hospital project required triple-technology integration to satisfy accuracy goals, illustrating the engineering burden. Komete markets a plug-and-play real-time locating system but still faces customisation hurdles when linking with legacy MES or BMS suites. Researchers at Politecnico di Torino pursue self-calibrating UWB radios that auto-correct range errors, yet commercial maturity remains years away. Until clear industry profiles emerge, large multi-site buyers hesitate to commit capital, slowing deployments across healthcare and manufacturing estates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Infrastructure Drives Current Deployments

Hardware investments anchor today’s Italy location-based services market, accounting for 46.20% revenue in 2025 on the back of dense beacon networks within factories and transit systems. The FCA Cento plant’s 350-beacon roll-out trimmed downtime costs by USD 500 per minute, illustrating the clear payback that hardware-led projects still deliver. Rome’s metro deployed guard-tracking sensors that halve emergency response time, underscoring safety-driven adoption in public infrastructure. Nevertheless, software platforms are growing faster at 13.77% CAGR as AI analytics migrate decision logic to the edge, lowering latency and bandwidth outlays without sacrificing insight depth.

Edge-native stacks from SECO couple low-power modules with a cloud orchestration layer, allowing real-time triangulation and historical pattern mining inside the same console. Services, while the smallest slice, underpin complex projects that blend RF surveys, GDPR audits, and application configuration. Vendors, therefore, bundle managed services to de-risk deployments for resource-constrained SMEs. Collectively, the hardware base is shifting toward energy-harvesting tags and multi-band antennas, laying the foundation for scalable retrofits once software sophistication matures further within the Italy location-based services market.

By Technology: Cellular Networks Accelerate Growth Through 5G Integration

GPS/GNSS remains the workhorse of outdoor navigation, securing 39.65% market share in 2025 across ride-hailing, automotive telematics, and consumer apps. Yet the Italy location-based services market size attached to cellular positioning grows quickest at 14.04% CAGR, catalysed by operator commitments to stand-alone 5G and NB-IoT. TIM’s nationwide NB-IoT layer facilitates decade-long battery life for smart-meter tags, whereas LTE-M options satisfy mid-tier bandwidth use cases in asset monitoring. UWB and BLE overlap grows within warehouses, with research confirming a 3.2 cm mean error in live industrial environments.

Hybrid engines that dynamically select RF paths now surface in pilot projects. Siena’s hospital spatial-intelligence suite fused magnetic fingerprinting with Wi-Fi sniffers and BLE anchors to meet clinical precision thresholds. Such multi-modal architectures exemplify how accuracy, power, and cost trade-offs can be balanced per asset. Consequently, vendors embed software-defined radios inside tags to future-proof against emerging spectrum allocations, a trend likely to sustain technology churn within the Italy location-based services market.

By Location Type: Indoor Positioning Gains Momentum Through Industry 4.0 Adoption

Outdoor solutions still produced 61.35% revenue in 2025, dominated by navigation, fleet scheduling, and public-safety deployments. However, indoor systems outpace with 14.65% CAGR as manufacturers pursue digital-twin workflows and hospitals chase workflow optimisation. The Italy location-based services market share for indoor-ready tags rises as beacon costs fall and accuracy climbs into the sub-decimetre realm. In Turin, TIM, Ericsson, and Comau orchestrate 5G-sliced networks wherein collaborative robots self-locate in real time, elevating throughput and enabling predictive maintenance cycles.

Healthcare showcases socially impactful use cases. At “Il Paese Ritrovato,” Bluetooth arrays monitor Alzheimer’s patients, improving activity scheduling and caregiver response. Logistics operators such as CHIMAR meld motion capture with RTLS to reduce ergonomic strain, reinforcing the broader Industry 4.0 narrative. As return-on-investment data accumulates, SME hesitation lessens, pointing to sustained penetration across secondary cities within the broad Italy location-based services market.

By Deployment Mode: Cloud Platforms Enable Scalable Smart-City Solutions

Cloud delivery amassed 54.85% revenue share in 2025 as municipalities and enterprises preferred elastic compute for multi-tenant analytics. Venice’s adoption of Urban Genius demonstrates how a single cloud spine can intertwine traffic, parking, and waste-management sensors into one dashboard. Nevertheless, latency-sensitive robotics and public-safety feeds propel edge and fog architectures toward a 13.48% growth rate. Researchers achieved 40 cm accuracy from UWB nodes powered solely by indoor lighting, underscoring how low-power edge hardware pairs with real-time decisions at the network periphery.

Hybrid topologies dominate bid requests, mixing on-premise segments for sensitive data with cloud analytics for longitudinal insights. Vendors, therefore, package orchestration toolkits that push compute to where it yields net-present-value advantages. As GDPR enforcement tightens, sovereign cloud zones within Italy further boost domestic IaaS demand, reinforcing regional value creation in the Italy location-based services market size.

By Application: Asset Tracking Transforms Industrial Operations

Mapping and navigation delivered 33.05% of 2025 revenue, anchored by consumer usage and transport routing. Asset tracking now emerges as the fastest-growing slice, placing the Italy location-based services market size for this sub-segment on a 13.58% CAGR trajectory. Factories integrate RTLS with ERP and MES to cut search times and anticipate bottlenecks. Research documents unit-handling efficiency gains exceeding 20% in live plant environments when UWB tags feed predictive algorithms.

Retail and advertising blend geofencing with real-time engagement tactics. Campaigns run by Sekel Tech deliver click-through rates above national benchmarks, encouraging expansion beyond flagship malls to regional shopping streets. Business-intelligence overlays synthesise location feeds with sales, producing context-aware dashboards. Emergency responders exploit floor-level tracking to enhance evacuation drills, reflecting the widening mission-critical footprint of the Italy location-based services market.

By End-user Vertical: Retail Sector Accelerates Digital Transformation

Transportation and logistics retained a 26.25% share in 2025 through fleet, container, and cold-chain monitoring. Yet retail and e-commerce see the steepest 13.46% CAGR as omnichannel leaders pair shopper profiles with proximity triggers. Automotive showrooms use micro-segment targeting powered by live traffic sensors to boost test-drive bookings, proving spend efficiency at scale. Healthcare gains momentum through patient-flow mapping and medical-asset traceability that cuts equipment loss.

Manufacturing invests in location-enabled digital twins to simulate workflows, as witnessed in the CANTINA 5.0 winery project, where IoT sensors oversee barrel conditions. Government projects expand with PNRR-funded smart-city pilots, often bundled with environmental and mobility services. Hospitality leverages tour-path analytics to optimise staffing and upsell local experiences. BFSI uptake stays nascent, limited to fraud detection and foot-traffic modelling around branches. Collectively, sectoral breadth cements the Italy location-based services market as a horizontal enabler of digital transformation rather than a niche technology silo.

Geography Analysis

Northern Italy held 49.70% revenue in 2025, anchored by the Milan-Turin-Genoa corridor’s dense manufacturing and research ecosystem. Politecnico di Milano’s UWB testbeds feed a pipeline of spin-offs, while Comau’s 5G factory pilots draw global attention to Turin’s industrial prowess. High purchasing power fuels rapid consumer uptake of navigation apps and in-store proximity services, cementing the region’s lead within the Italy location-based services market.

Central Italy benefits from Rome’s expansive #Roma5G deployment that seeds ubiquitous network endpoints across cultural heritage zones. Government agencies leverage the same infrastructure for traffic orchestration ahead of Jubilee 2025, while tourism operators integrate augmented-reality guides into historical venues. Hospital modernisation in Tuscany and Lazio, exemplified by Siena’s indoor navigation project, further diversifies demand.

Southern Italy and the Islands achieve the fastest 13.68% CAGR to 2031, lifted by outsized PNRR grants channelled into connectivity and smart grids. Puglia’s PAN initiative intertwines EV charging with geospatial demand forecasting, exemplifying region-specific innovation. Cities like Messina deploy sensor meshes that monitor air quality and parking occupancy, attracting small vendors eager to prove scalable deployments. The resulting jump in digital infrastructure narrows historical disparities and unlocks fresh addressable revenue for the broader Italy location-based services market.

Mordor Intelligence provides coverage of the location based services market across other key regional markets, including Middle East and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Germany, Spain, United Arab Emirates, Nigeria, France, Canada, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

The market shows moderate fragmentation. Global platforms such as Google Maps and Apple Maps dominate consumer navigation, yet indoor and vertical applications tilt toward domestic innovators like Nextome, Komete, and TapMyLife. Telecom incumbents wield network reach to bundle location APIs with connectivity. WindTre’s EUR 485 million OpNet acquisition secures 75% population coverage for stand-alone 5G, creating end-to-end propositions that rival OTT players.

Strategic moves cluster around edge analytics and industry specialisation. SECO merges modular hardware with AI-enabled orchestration, presenting a differentiated stack for latency-critical workloads. Fastweb+Vodafone leans on joint spectrum assets to push NB-IoT services into utilities and agriculture. Rising compliance hurdles propel European contenders offering privacy-by-design frameworks, positioning them favorably against US-based rivals scrutinised by the regulator.

M&A interest remains high as incumbents fill capability gaps in indoor navigation, computer vision, and ultra-wideband chipsets. Yet price sensitivity among SMEs sustains a viable long-tail of niche providers who capture contracts through domain expertise and turnkey delivery. The collective result is a rich ecosystem in which collaboration, rather than outright consolidation, defines competitive advantage within the Italy location-based services market.

Italy Location-Based Services Industry Leaders

Google LLC

Apple Inc.

HERE Technologies

TomTom N.V.

Esri Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: WindTre completed the EUR 485 million acquisition of OpNet, gaining Italy’s first 5G stand-alone network with 3,000 base stations.

- May 2025: Fastweb+Vodafone recorded EUR 202 million in enterprise value-added services revenue and reached 78% 5G coverage.

- May 2025: TIM posted EUR 3.3 billion total revenue in Q1 2025, a 2.7% year-over-year rise, with enterprise cloud services at EUR 0.8 billion.

- April 2025: Boldyn Networks and the City of Rome launched the EUR 97.7 million #Roma5G project, deploying over 2,200 small cells.

- March 2025: SECO S.p.A. unveiled a unified edge-fog-cloud AI architecture enabling location-aware applications.

- February 2025: The Italian Data Protection Authority maintained its ban on Google Analytics, underscoring continued GDPR vigilance.

- January 2025: BagBnb secured EUR 2.5 million to scale its location-based luggage-storage app.

- December 2024: EOLO partnered with Nokia to roll out Europe’s first 5G stand-alone mmWave network in Italy.

Italy Location-Based Services Market Report Scope

Location-based services (LBSs) are computer or mobile applications that provide information based on the device's location and the user, primarily through mobile portable devices, such as smartphones and mobile networks. The precision of the location services primarily depends on the hardware and software used in the mobile communication system, along with the positioning server.

Italy's location-based services market is segmented by component (hardware, software, services), location (indoor and outdoor), application (mapping and navigation, business intelligence and analytics, location-based advertising, social networking, entertainment, and other applications), and end-user (transportation and logistics, IT and telecom, healthcare, government, BFSI, hospitality, manufacturing, and other end-user).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| GPS/GNSS |

| Wi-Fi |

| Bluetooth LE and UWB |

| Cellular (5G, LTE, NB-IoT) |

| Hybrid and Others |

| Indoor |

| Outdoor |

| On-premise |

| Cloud |

| Edge/Fog |

| Mapping and Navigation |

| Business Intelligence and Analytics |

| Location-based Advertising |

| Social Networking and Entertainment |

| Emergency and Public Safety |

| Asset Tracking and Fleet Management |

| Other Applications |

| Transportation and Logistics |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| BFSI |

| Hospitality and Tourism |

| Manufacturing and Industrial |

| Retail and E-commerce |

| Other End-user Verticals |

| Northern Italy |

| Central Italy |

| Southern Italy and Islands |

| By Component | Hardware |

| Software | |

| Services | |

| By Technology | GPS/GNSS |

| Wi-Fi | |

| Bluetooth LE and UWB | |

| Cellular (5G, LTE, NB-IoT) | |

| Hybrid and Others | |

| By Location Type | Indoor |

| Outdoor | |

| By Deployment Mode | On-premise |

| Cloud | |

| Edge/Fog | |

| By Application | Mapping and Navigation |

| Business Intelligence and Analytics | |

| Location-based Advertising | |

| Social Networking and Entertainment | |

| Emergency and Public Safety | |

| Asset Tracking and Fleet Management | |

| Other Applications | |

| By End-user Vertical | Transportation and Logistics |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Government and Public Sector | |

| BFSI | |

| Hospitality and Tourism | |

| Manufacturing and Industrial | |

| Retail and E-commerce | |

| Other End-user Verticals | |

| By Region | Northern Italy |

| Central Italy | |

| Southern Italy and Islands |

Key Questions Answered in the Report

What is the current size of the Italy location-based services market?

The market generated USD 1.12 billion in 2026 and is projected to reach USD 1.91 billion by 2031.

Which segment is growing fastest within the market?

Indoor positioning systems lead growth with a 14.65% CAGR, driven by Industry 4.0 deployments and hospital modernisation.

How significant is 5G to location-based services in Italy?

5G and NB-IoT roll-outs add about 2.8 percentage points to the forecast CAGR by supplying sub-meter accuracy and low-latency coverage nationwide.

Which region in Italy offers the highest growth potential?

Southern Italy and the Islands exhibit the fastest 13.68% CAGR thanks to substantial PNRR-funded digital infrastructure projects.

How do privacy regulations affect market participants?

Strict GDPR enforcement raises compliance costs and fines for non-conforming geo-tracking, prompting enterprises to favour European privacy-centric service providers.

What role do telecom operators play in the competitive landscape?

Operators such as TIM, WindTre and Fastweb+Vodafone combine nationwide 5G coverage with cloud and edge services, positioning themselves as end-to-end location-based service enablers.

Page last updated on: