Home and Property Improvement

27th MayStrategic Expansion in the Russia Laundry Appliances Market

3 Min Read

The Italy Furniture Market Report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and More), Material (Wood, Metal, Plastic & Polymer, Other Materials), Price Range (Economy, Mid-Range, Premium), Distribution Channel (B2C/Retail, B2B/Project), and Geography (Northern Italy, Central Italy, Southern Italy & Islands). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

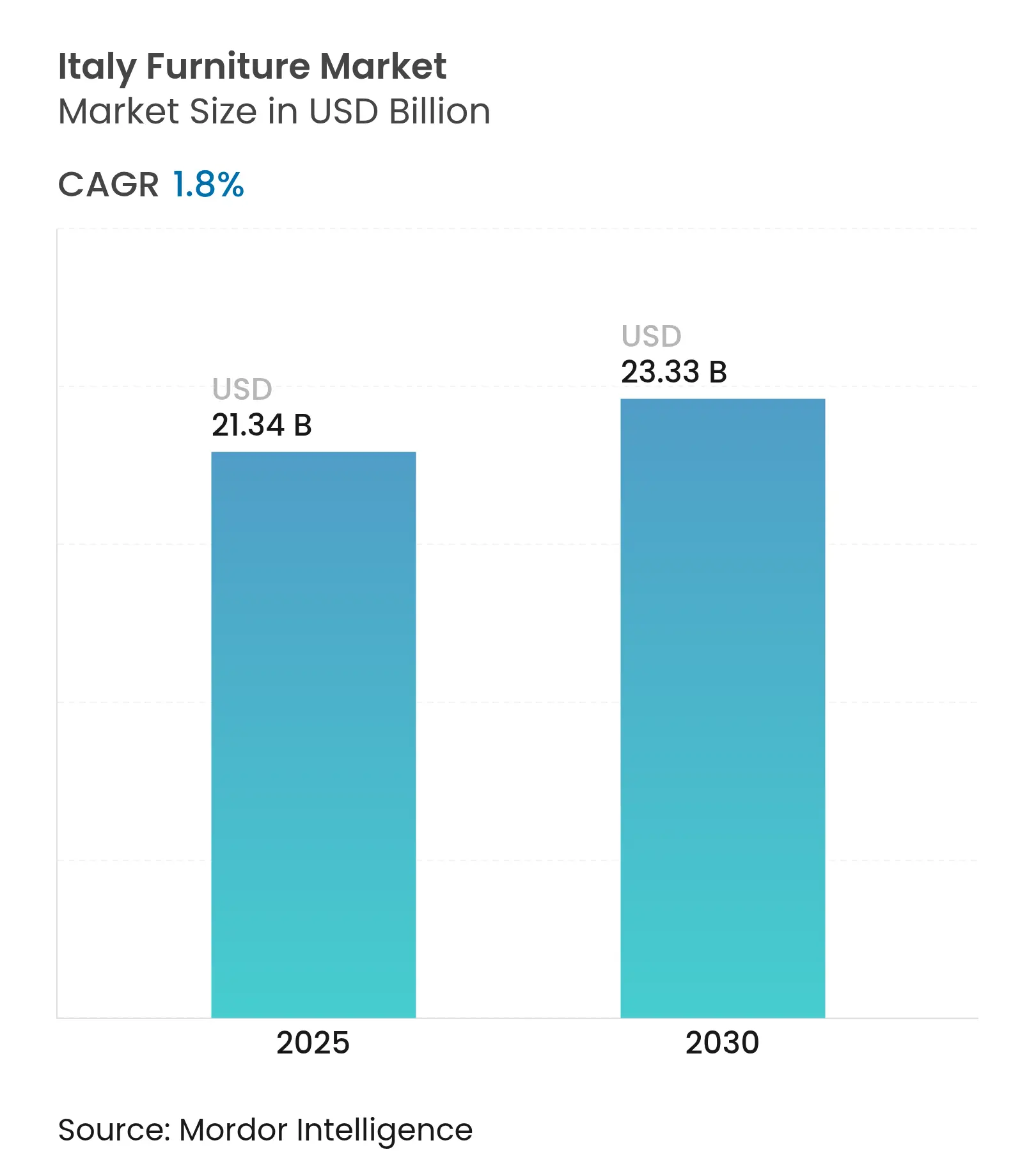

| Market Size (2025) | USD 21.34 Billion |

| Market Size (2030) | USD 23.33 Billion |

| Growth Rate (2025 - 2030) | 1.80 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Italy furniture market size stood at USD 21.34 billion in 2025 and is forecast to reach USD 23.33 billion by 2030, expanding at a 1.80% CAGR over the period. Steady growth reflects a pivot from stimulus-driven demand to durable fundamentals such as the reshoring of high-end production, tourism-led hospitality refurbishments, and deepening e-commerce penetration. The Italy furniture market benefits from the country’s position as Europe’s second-largest producer, with exports of EUR 19.4 billion (USD 20.76 billion) in 2024 despite a 2.10% decline that year[1]Il Sole 24 Ore, “Brianza, cuore del mobile italiano,” ilsole24ore.com.. Supply-side resilience is underwritten by industrial districts in Lombardy, Veneto, and Friuli-Venezia Giulia that have embraced Industry 4.0 to shorten cycle times by up to 35%, protecting margins against raw-material inflation. Demand fundamentals include a shift toward premium segments, an 18% online penetration rate that is expanding 8% annually, and tourism recovery that is reviving project-based hospitality orders.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Housing renovation tax credits

Housing renovation tax credits

| +0.4% | National; strongest in Northern and Central regions | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

+0.4%

|

Geographic Relevance

:

National; strongest in Northern and Central regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

Reshoring of high-end production

Reshoring of high-end production

| +0.3% | Northern industrial districts; spillover to Central regions | Medium term (2-4 years) | |||

E-commerce penetration in furniture & décor

E-commerce penetration in furniture & décor

| +0.2% | National; urban concentration in Milan, Rome, Turin | Medium term (2-4 years) | |||

Surge in tourist-driven hospitality refurbishments

Surge in tourist-driven hospitality refurbishments

| +0.2% | Major tourist destinations nationwide | Short term (≤ 2 years) | |||

Digitally enabled mass-customization

Digitally enabled mass-customization

| +0.1% | Northern clusters, expanding southward | Long term (≥ 4 years) | |||

Growing demand for certified circular-economy products

Growing demand for certified circular-economy products

| +0.1% | EU-wide; strongest in Northern Italy | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Housing Renovation Tax Credits (Superbonus 110%)

The transition from Superbonus 110% to reduced incentive rates creates a measured deceleration rather than a collapse in furniture demand, with the furniture bonus extending through 2025 at a 50% deduction up to EUR 5,000 (USD 5,350) per household. This policy evolution signals the government's recognition that furniture purchases represent discretionary spending requiring sustained support beyond construction completion. Companies like Nusco experienced revenue declines of 9.57% in 2024, directly attributable to incentive reduction, yet maintained EBITDA margins above 13% through operational efficiency gains. The geographic impact concentrates in regions with higher home ownership rates and renovation activity, particularly Northern and Central Italy where disposable income levels support continued furniture investment even with reduced subsidies. Market dynamics suggest a shift toward higher-value purchases as consumers optimize tax benefits, potentially accelerating premiumization trends across furniture categories.

Reshoring of High-End Furniture Production

Tax incentives reducing corporate income by up to 50% for relocated activities from outside the EU are accelerating the reshoring of high-end production to Italy[2]University of Brescia, “Reshoring strategies of Italian manufacturing companies,” unibs.it. . The Brianza district, comprising 2,754 specialized firms, leverages its proximity to design hubs to enable rapid prototyping and stringent quality control. This advantage supports the Italian market in maintaining "Made in Italy" price premiums, even amid rising labor costs. Reshoring is particularly prominent in the customizable luxury segment, which is driving growth in related industries. Component suppliers and technical service providers in Northern clusters are benefiting from these ecosystem spillovers. This trend underscores the strategic importance of localized production in sustaining competitive advantages in the global market.

E-commerce Penetration in Furniture & Décor

Online retail generated EUR 58.8 billion (USD 62.92 billion) in Italian e-commerce sales in 2024, with furniture accounting for 18% and rising 8% each year[3]DIY International, “Italy,” diyinternational.com. This penetration rate significantly exceeds traditional furniture retail growth, indicating structural channel migration rather than cyclical expansion. The shift proves particularly pronounced in urban markets where logistics infrastructure supports large-item delivery and consumers demonstrate higher digital adoption rates. However, the furniture category's tactile nature limits pure-play online models, driving hybrid strategies that combine digital discovery with physical showroom experiences. Companies investing in augmented reality visualization and virtual staging tools gain competitive advantages in converting online browsers to buyers, while traditional retailers integrating omnichannel capabilities capture market share from purely physical competitors.

Surge in Tourist-Driven Hospitality Refurbishments

Tourism recovery catalyses hospitality furniture demand as hotel investment reached EUR 1.4 billion (USD 1.50 billion) in 2023, with focus shifting toward luxury and boutique properties requiring distinctive furnishing solutions. This segment's growth trajectory exceeds general market expansion due to deferred maintenance during COVID-19 restrictions and evolving guest expectations for experiential accommodations. Italian manufacturers benefit from proximity to major tourist destinations and established relationships with hospitality designers, creating barriers to entry for international competitors. The geographic distribution spans traditional tourism centers and emerging destinations, with particular strength in coastal regions and historic city centers where property values support premium furniture investments. Contract furniture specialists gain market share through project-based sales models that bundle design services with product delivery.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Construction slowdown in Southern Italy

Construction slowdown in Southern Italy

| -0.3% | Southern regions and islands | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.3%

|

Geographic Relevance

:

Southern regions and islands

|

Impact Timeline

:

Medium term (2-4 years)

|

Rising raw-material import prices

Rising raw-material import prices

| -0.2% | National; heavier on high-volume producers | Short term (≤ 2 years) | |||

Ageing skilled‑craft workforce & apprenticeship gap

Ageing skilled‑craft workforce & apprenticeship gap

| – 0.2 % | Traditional furniture regions across Italy | Medium term (2–4 yr) | |||

Intensifying low‑cost imports from Eastern Europe &

Asia

Intensifying low‑cost imports from Eastern Europe &

Asia

| – 0.3 % | Nationwide—especially in mass‑market, volume‑sensitive segments | Short term (≤ 2 yr) | |||

| Source: Mordor Intelligence | ||||||

Construction Slowdown in Southern Italy

Regional economic disparities manifest in construction activity divergence, with Southern Italy experiencing weaker residential and commercial development that constrains furniture demand growth. While national construction output rose 6% year-over-year in February 2025, the increase concentrated in NRRP infrastructure projects rather than private housing development[4]Banca d’Italia, “Bollettino Economico n. 1 - 2025,” bancaditalia.it. Southern regions face structural challenges, including lower disposable income, limited access to construction financing, and demographic outmigration that reduces household formation rates. This geographic constraint particularly impacts volume-oriented furniture segments where price sensitivity limits premium product penetration. The restraint's medium-term timeline reflects the persistence of regional economic imbalances despite national recovery programs, suggesting furniture manufacturers must adapt distribution strategies and product portfolios to address varying regional purchasing power.

Rising Raw-Material (Wood & Metal) Import Prices

Input cost inflation creates margin pressure across Italy's furniture supply chain, with wood prices surging from EUR 25/m³ to EUR 90/m³ (USD 26.75/m³ to USD 96.30/m³) in 2025, while metal components face similar volatility. This cost escalation stems from global supply chain disruptions, energy price increases, and currency fluctuations affecting import-dependent manufacturers. The impact proves most severe for volume-oriented producers lacking pricing power to pass through cost increases, while premium manufacturers maintain margins through value-added positioning. Geographic relevance spans national boundaries but affects Northern Italy's manufacturing clusters most acutely due to higher production volumes and export orientation. Companies respond through vertical integration strategies, alternative material adoption, and supplier diversification, yet short-term margin compression remains unavoidable for most market participants.

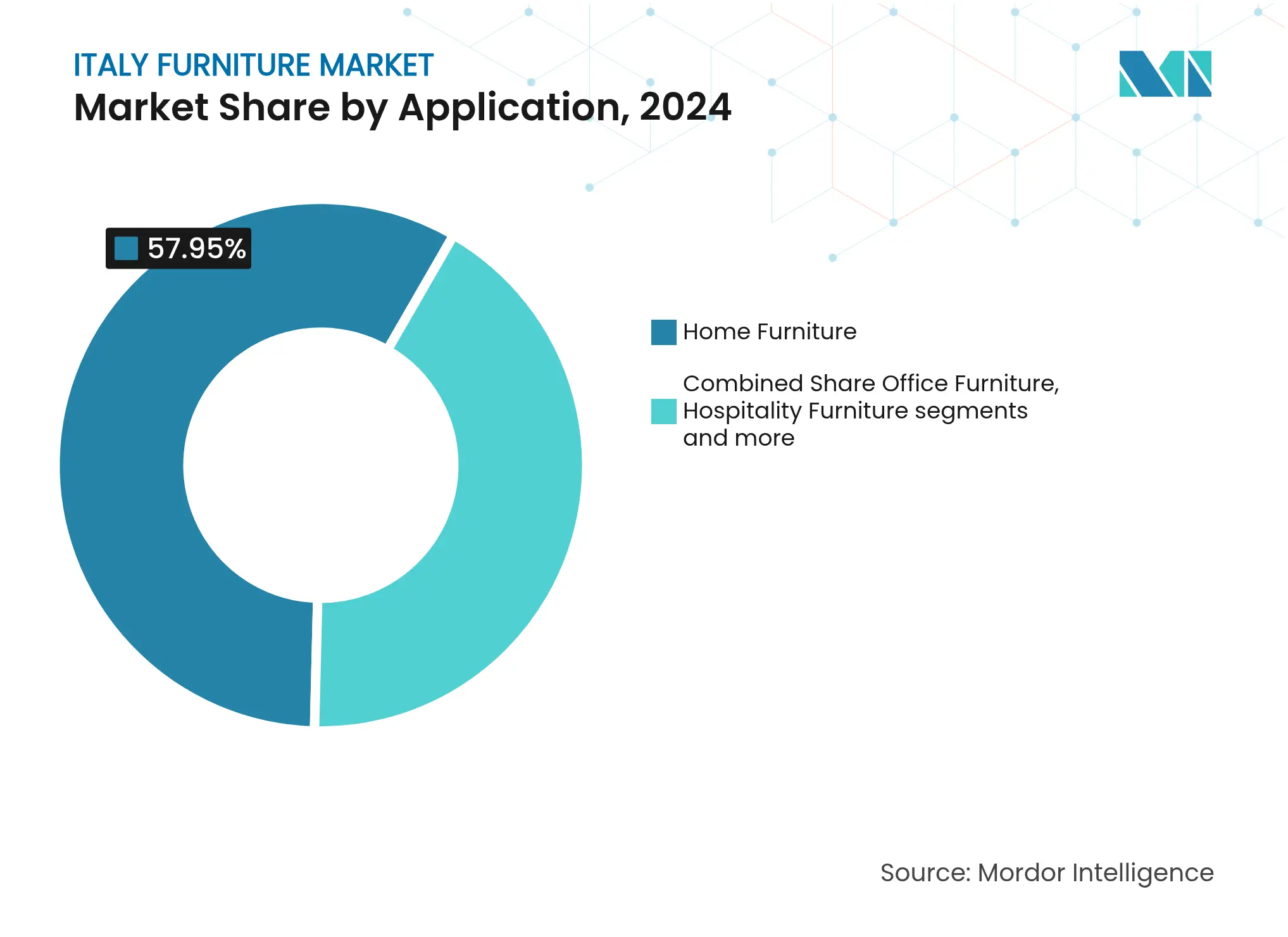

By Application: Home Furniture Dominates as Hospitality Accelerates

Home furniture generated 57.95% of Italy's furniture market size in 2024, reflecting strong domestic consumption and established export channels. Living room and bedroom products benefit from renovation incentives and consumer focus on multifunctional spaces. Hospitality, though smaller, is forecast to grow at a 2.93% CAGR as hoteliers refurbish properties to meet rising tourist expectations.

Demand for contract-grade pieces with stringent fire-safety and durability standards lifts margins and buffers cyclicality, helping the Italy furniture market diversify revenue streams. Office furniture lags due to hybrid work adoption, yet educational and healthcare installations rise on public funding. Specialist suppliers offering turnkey project management gain share across segments, and cross-selling opportunities emerge when homes, hotels, and co-working spaces converge in design aesthetics.

Note: Segment shares of all individual segments available upon report purchase

By Material: Wood Heritage Meets Polymer Innovation

Wood accounted for 61.85% Italy's furniture market share in 2024, underpinned by consumer preference for natural finishes and Italy’s artisanal legacy. FSC-certified panels and veneers help manufacturers command premiums in export markets. Plastic and polymer products, although smaller, are projected to grow at a 3.38% CAGR as recyclable resins and 3D printing enable mass customization and circular-economy designs.

Metal frames face cost volatility, driving interest in hybrid constructions that reduce steel content without compromising strength. Companies such as Fantoni achieve 80% recycled wood content in particleboard, signalling a shift from virgin materials toward sustainable composites. Continuous R&D in carbon-negative materials positions the Italy furniture market for future regulatory requirements and eco-label differentiation.

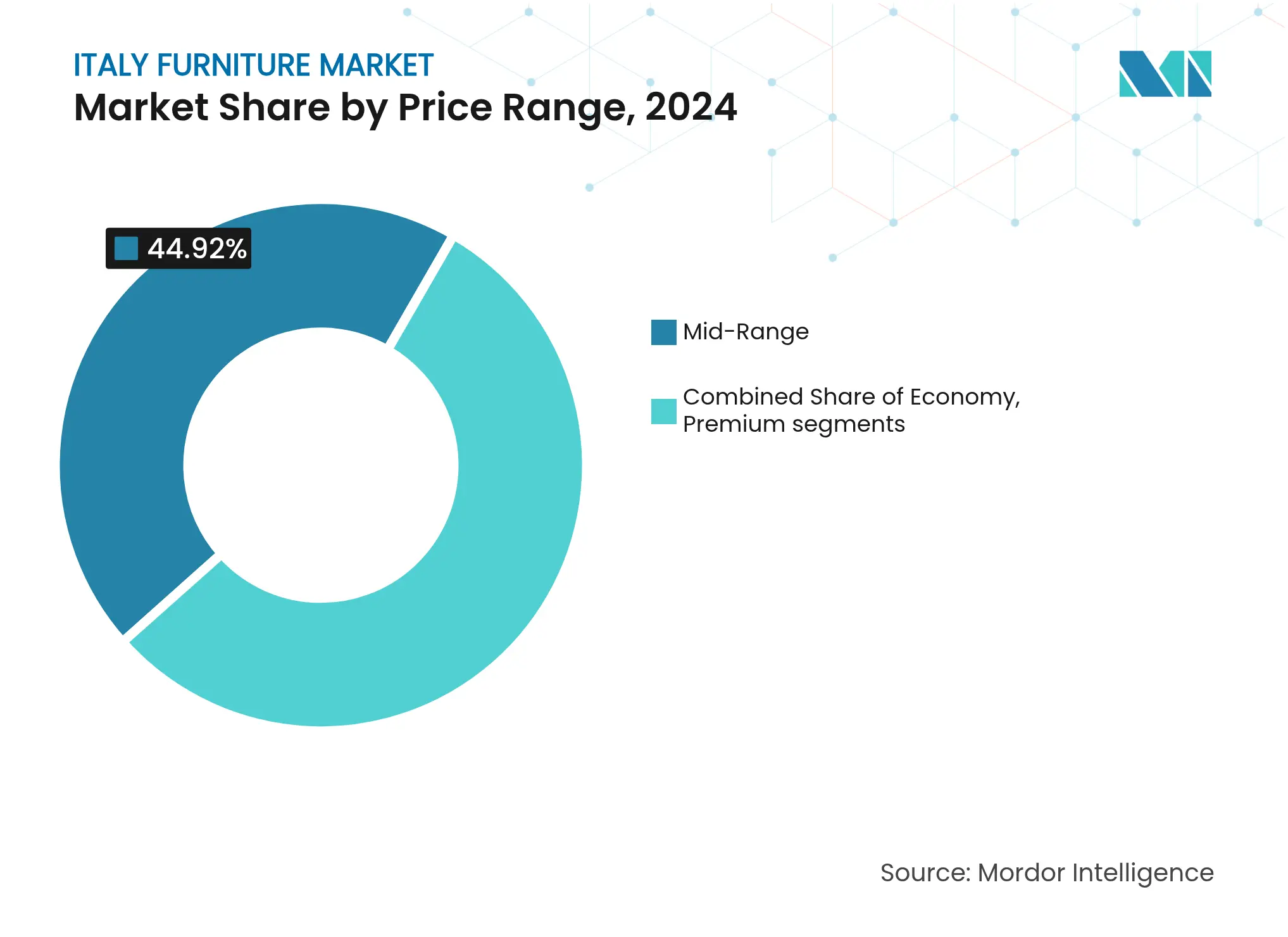

By Price Range: Premium Positioning Drives Expansion

In 2024, mid-range furniture accounted for 44.92% of the Italian furniture market, reflecting its significant contribution to the overall market size. However, the premium furniture segment is projected to grow at a faster pace, with a compound annual growth rate (CAGR) of 2.54% during the forecast period through 2030. This growth is driven by increasing consumer preference for high-quality, design-centric products that offer exclusivity and durability. Leading brands such as Poltrona Frau and B&B Italia capitalize on their strong design heritage and craftsmanship to justify premium price points. These attributes enable them to maintain differentiation and avoid commoditization, which is a key challenge in the competitive furniture market. Their ability to integrate traditional craftsmanship with modern design trends positions them favorably in both domestic and international markets.

The economy segment, on the other hand, faces intense competition from imports originating from Eastern Europe and Asia. These imports often offer lower price points, compelling Italian manufacturers in this segment to adopt strategies aimed at climbing the value chain. Key approaches include the use of superior materials, the introduction of limited-edition collections, and the provision of personalized finishes to enhance product appeal. Additionally, Italian furniture brands are leveraging integrated storytelling to strengthen their market positioning. This strategy is evident in flagship showrooms, where immersive brand narratives are used to engage consumers emotionally. Online configurators further complement this approach by offering customization options, which enhance the consumer experience and foster brand loyalty. The premiumization trend is gaining momentum across both domestic and international markets, supported by these strategic initiatives. Italian furniture manufacturers are increasingly focusing on creating a strong emotional connection with consumers, which is critical for sustaining growth in the premium segment. By aligning product offerings with evolving consumer preferences, these brands are well-positioned to capture a larger share of the growing premium furniture market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Retail Dominance with Digital Acceleration

B2C retail accounted for 68.33% of Italy furniture market size in 2024 and grow at a CAGR of 3.12%, supported by national chains, regional independents, and factory outlets. Omnichannel investments allow shoppers to preview products via augmented reality, schedule virtual design consultations, and complete purchases either online or in store. Online penetration reached 18% and is expanding at 8% annually, reflecting logistical improvements for last-mile delivery of bulky items.

B2B project sales play a pivotal role in securing large-scale contracts in the hospitality, office, and healthcare sectors within the Italian furniture market. These contracts often prioritize customization and volume discounts, making B2B sales a critical component of the value chain. The adoption of collaboration platforms has streamlined key processes, including specification, procurement, and installation. This efficiency has resulted in reduced project timelines, enabling faster execution of large projects. Additionally, these platforms have strengthened supplier relationships by fostering transparency and improving coordination. As a result, businesses can achieve both operational efficiency and long-term strategic partnerships in this competitive market.

Northern Italy held 34.12% Italy furniture market share in 2024, leveraging densely interconnected supply chains and advanced digital manufacturing. Lombardy’s integrated ecosystem supports quick design iterations and stringent quality control, enabling exporters to navigate tariff uncertainties in markets such as the United States. Veneto’s EUR 991 million (USD 1.06 billion) and Friuli-Venezia Giulia’s EUR 581 million (USD 621.67 million) first-quarter 2023 exports underscore diversification in product mix and destination markets, from Germany to the Middle East.

Central Italy shows the fastest 3.27% CAGR, draws on cultural heritage and a rebound in inbound tourism that fuels boutique hotel development. Artisanal workshops collaborate with design schools in Rome and Florence, marrying traditional techniques with contemporary aesthetics. NRRP-funded infrastructure upgrades improve logistics and attract private construction, creating a virtuous cycle of demand and supply expansion within the Italy furniture market.

Southern Italy and the islands remain constrained by lower disposable incomes and credit access, yet pockets of opportunity emerge in Sicily and Sardinia where high-end resorts seek locally inspired furnishings. Government initiatives aimed at stimulating SMEs and vocational training may gradually lift production capabilities. For now, southern manufacturers focus on mid-volume, cost-efficient lines while leveraging e-commerce to reach national consumers beyond regional borders.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

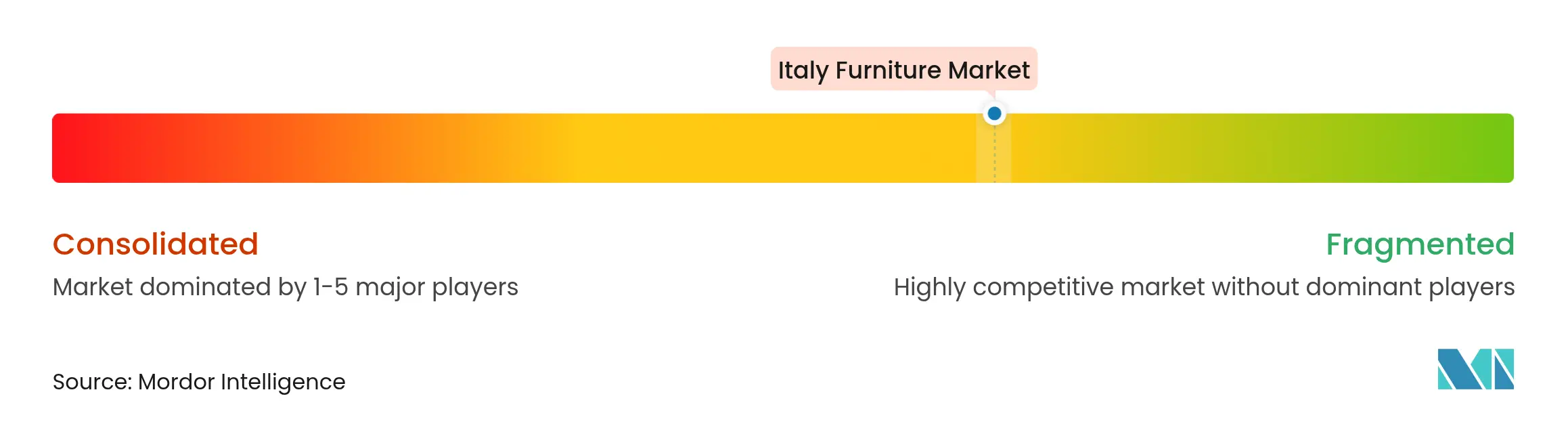

Market Concentration

The Italy furniture market is moderately fragmented, with leading companies holding a notable but not dominant position leaving significant room for consolidation. A diverse mix of family-owned businesses and regional specialists contributes to a rich landscape of niche brands that compete more on design creativity than on large-scale production efficiencies. Sustainability credentials are becoming decisive: Natuzzi has held FSC certification since 2016, while B&B Italia integrates recycled content in flagship ranges, differentiating products in premium tiers.

Technology adoption is leveling the playing field. Digital twins and real-time production tracking allow small manufacturers to custom-produce at competitive lead times. As Industry 4.0 spreads, cloud-based procurement platforms connect designers with factories, fostering collaborative innovation and lowering entry barriers.

M&A momentum is building. Salice acquired hardware specialist Atim in August 2024 to broaden component portfolios, and Visionnaire completed an acquisition in April 2024 to reinforce luxury positioning. Banks such as Intesa Sanpaolo finance supply-chain contracts worth over EUR 2 billion (USD 2.14 billion), facilitating upgrades and internationalization for more than 45,000 companies, evidence of institutional confidence in the Italy furniture market’s export potential.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value in USD)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

The Italy Furniture Market is segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and Other Furniture), by Material (Wood, Metal, Plastic, and Other Furniture), and by Distribution Channel (Home Centers, Flagship Stores, Specialty Stores, Online, and Other Distribution Channels). The report offers market size and forecasts for the Italy Furniture Market in value (USD) for all the above segments.

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Deep-Dive Analysis of Feed Probiotics Across Key Regions

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.