Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

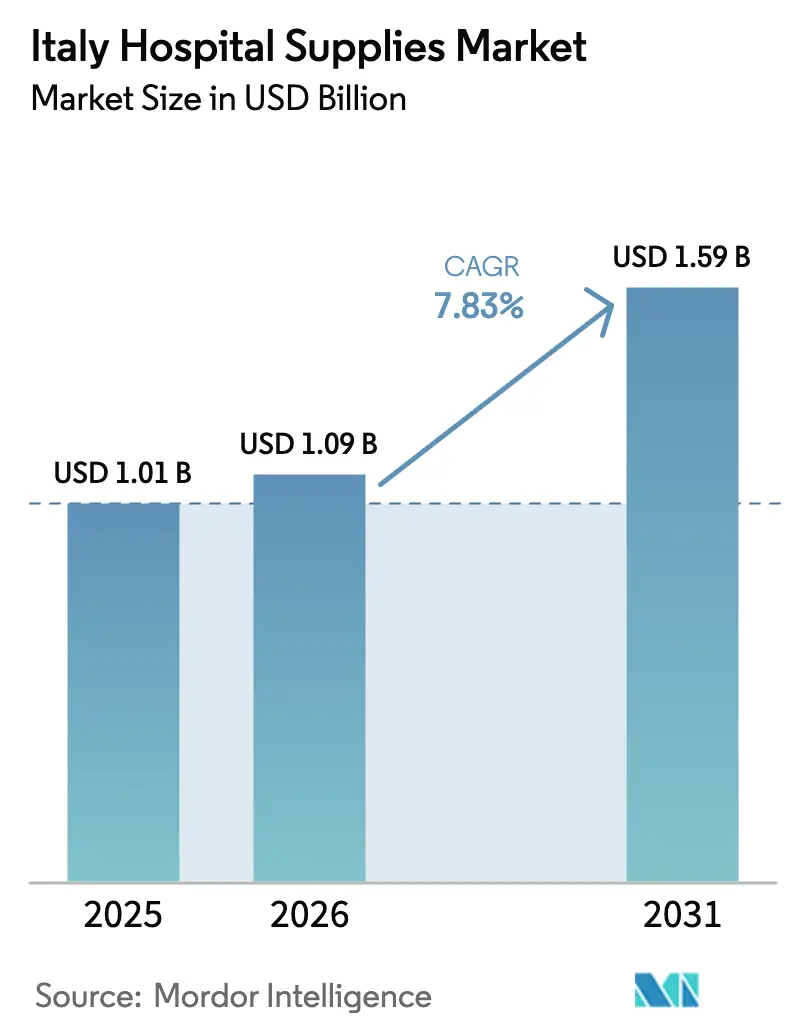

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Hospital Supplies Market Analysis by Mordor Intelligence

The Italy Hospital Supplies Market size was valued at USD 1.01 billion in 2025 and is estimated to grow from USD 1.09 billion in 2026 to reach USD 1.59 billion by 2031, at a CAGR of 7.83% during the forecast period (2026-2031).

The Italian hospital supplies market is undergoing a significant transformation, driven by rising demand for single-use consumables aimed at reducing hospital-acquired infections, alongside a substantial EUR 15.63 billion allocation under the PNRR Mission 6. Rapid digitalization of clinical workflows is further influencing procurement strategies. Hospitals are increasingly prioritizing large imaging and robotic surgical systems with workflow-automation features to address operational challenges, including a projected shortfall of 63,000 nurses. However, growth is constrained by regional payment delays of up to 120 days, MDR-related certification costs, and fragmented tendering processes in Southern regions. Vendors offering CONSIP-qualified portfolios and efficient e-commerce fulfillment capabilities are well-positioned to capitalize on the growing demand in this market.

Key Report Takeaways

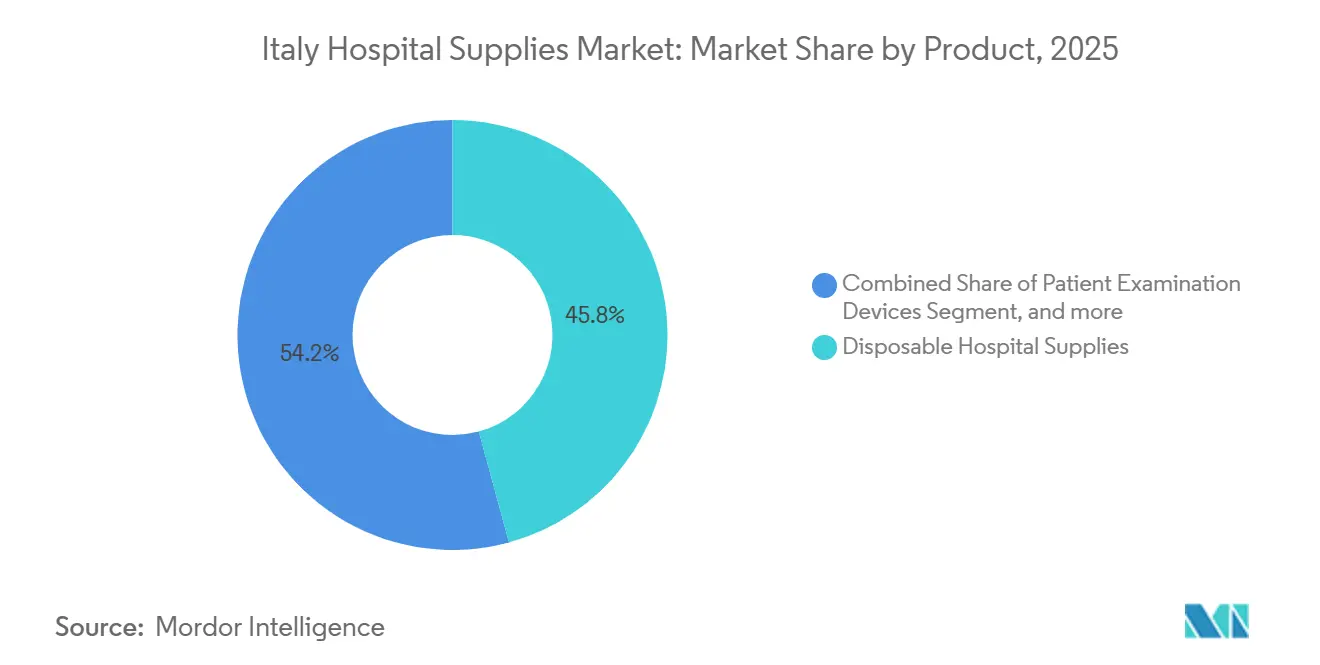

- By product category, disposable hospital supplies led with 45.76% of the Italy hospital supplies market share in 2025. Operating Room Equipment is forecast to expand at an 8.43% CAGR through 2031.

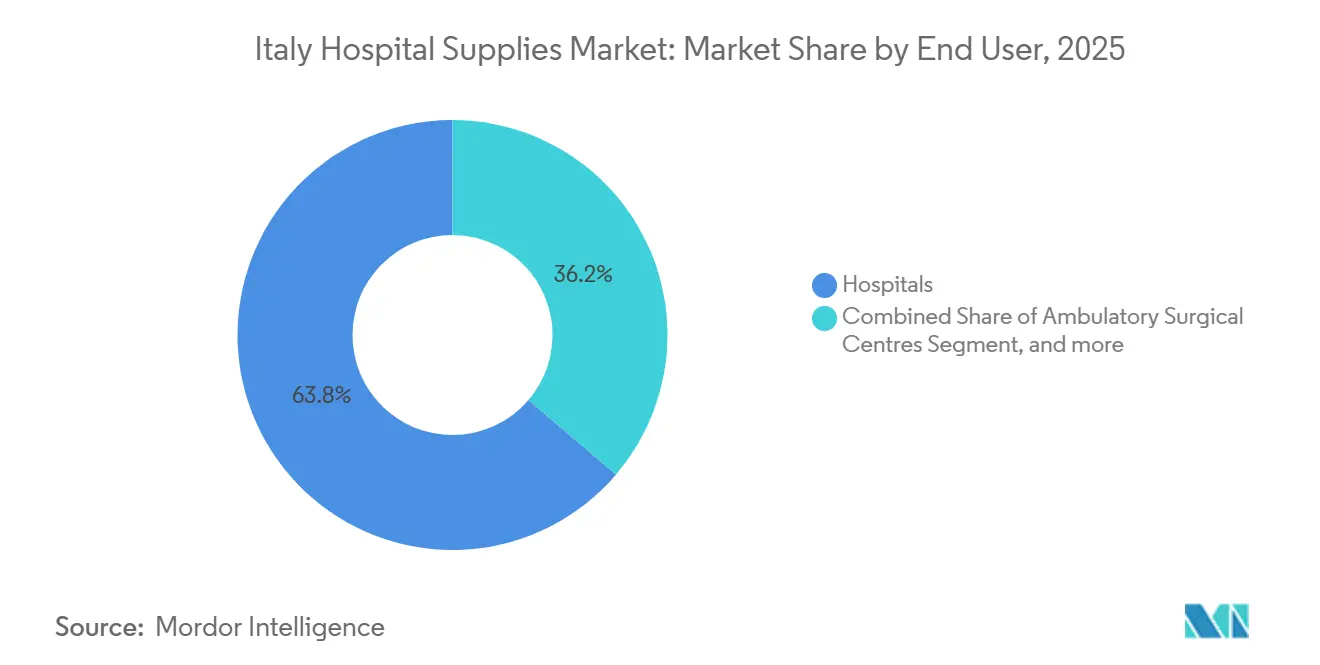

- By end user, hospitals accounted for 63.76% of the Italy hospital supplies market in 2025. Ambulatory Surgical Centres are advancing at an 8.67% CAGR to 2031.

- By distribution channel, direct tender and bulk procurement accounted for 72.74% of 2025 orders in the Italy hospital supplies market. E-Commerce and GPO Platforms are growing at a 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Recovery-Plan Capital Investments | +2.1% | National, highest in Campania, Sicily, Calabria | Medium term (2-4 years) |

| Expanding Chronic-Disease Burden | +1.8% | National, stronger in Lombardy, Veneto, Emilia-Romagna | Long term (≥ 4 years) |

| Rapid Digitalization of Hospital Infrastructure | +1.3% | National, early uptake in Lombardy, Lazio, Piedmont | Medium term (2-4 years) |

| Heightened Hospital-Infection Awareness | +1.0% | National, acute-care hospitals and ASCs | Short term (≤ 2 years) |

| Shift Toward Outpatient & Home-Care Models | +0.9% | National, accelerated in Milan, Rome, Turin, Naples | Short term (≤ 2 years) |

| Emergence of Value-Based Procurement Practices | +0.7% | National, pilot tenders in Northern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Chronic-Disease Burden

In 2022, 23.8% of Italy's population was aged 65 and above, a figure expected to reach 34% by 2050. This demographic trend ensures a stable demand for medical supplies such as syringes, glucose meters, and wound-care dressings[1]ISTAT, “Report on Elderly Population,” istat.it. Cardiovascular diseases, responsible for 31% of deaths, along with 40.9% of the population reporting at least one chronic condition, have led hospitals to adopt multi-year CONSIP frameworks for bulk procurement of patient-examination devices. The rising incidence of diabetes is driving repeat purchases of continuous glucose monitors, particularly those integrated with electronic health records. Between 2019 and 2021, mental health diagnoses for anxiety and depression increased by 19.8% and 17.3%, respectively, fueling demand for telepsychiatry kits that connect community facilities with tertiary care centers. Suppliers offering bundled chronic-care kits, which effectively reduce hospital readmissions, are gaining competitive advantages in value-based tenders across Italy's hospital supplies market.

Government Recovery-Plan Capital Investments

The PNRR earmarked EUR 15.63 billion (USD 17.19 billion) for health spending, including EUR 4.05 billion for hospital technology upgrades and EUR 1.67 billion for digital infrastructure[2]Ministry of Economy and Finance, “PNRR Mission 6 Allocations,” mef.gov.it. Procurement targets encompass 3,100 CT, MRI, and angiography systems and 84 hospital seismic retrofits. Execution delays in 2024 require a sevenfold acceleration to meet 2026 milestones, compressing tender windows and favoring incumbents with CONSIP credentials. Southern regions receive disproportionate allocations, yet limited administrative capacity postpones approvals, intensifying a two-speed dynamic inside the Italy hospital supplies market.

Rapid Digitalization of Hospital Infrastructure

FSE 2.0 has 25.4 million patient consents, 6.5 million active users, and 139,000 physicians onboard, but only 28% of citizens accessed their records in 2024, underscoring interoperability gaps. PNRR funding channels EUR 1.67 billion into cloud data exchange, telemedicine, and IoT-enabled devices. Hospitals in Lombardy, Lazio, and Piedmont contract Philips, Siemens Healthineers, and GE Healthcare for connected imaging suites that transmit diagnostics into cloud dashboards. ISO 27001 and GDPR mandates raise entry barriers, shifting preference toward vendors with cyber-secure portfolios inside the Italy hospital supplies market.

Shift Toward Outpatient and Home-Care Models

Decree 77/2022 prescribes one community house for every 40,000-50,000 residents and shifts elective procedures into ambulatory centers. ASCs, expanding at 8.67% CAGR, now handle cataract and hernia operations in same-day models. Home-health programs absorb oxygen concentrators, infusion pumps, and remote monitoring kits reimbursed under telemedicine tariffs, stimulating e-commerce procurement. Centralized warehouses must now supply hundreds of micro-sites, a logistical realignment that leans on GPOs and just-in-time inventory solutions in the Italy hospital supplies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory & Tender Compliance | −0.7% | National, heavier in Lazio and Campania | Medium term (2-4 years) |

| Healthcare Workforce Shortages | −0.6% | National, most acute in Southern regions | Short term (≤ 2 years) |

| Regional Budgetary Constraints | −0.5% | Calabria, Sicily, Molise, Basilicata | Long term (≥ 4 years) |

| Global Supply-Chain Vulnerabilities | −0.4% | National, highest risk for import-dependent disposables | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Tender Compliance

CONSIP handled EUR 28.3 billion in centralized procurement during 2024, yet 24-36-month framework contracts lock in pricing, squeezing margins when raw-material costs rise[3]CONSIP, “Annual Report 2024,” consip.it. EU MDR imposes rigorous clinical-evaluation and UDI labeling duties, raising compliance costs by 20-30% for midsize producers. Fragmented tenders in Lazio and Campania extend award cycles by up to nine months, pressuring vendor cash flow. Multinationals absorb these hurdles with specialized regulatory teams, while smaller Italian manufacturers exit segments such as sterilization and mobility aids, subtly consolidating the Italy hospital supplies market.

Regional Budgetary Constraints

Per-capita health spending is EUR 2,300 in Lombardy but EUR 1,800-1,900 in Calabria and Sicily, reflecting chronic underfunding. Southern hospitals defer payments for 90-120 days, dissuading suppliers from high-value bids and confining purchases to commodity disposables. PNRR aims to close the gap, yet Southern regions had absorbed only 40% of allocated health funds by mid-2025 versus 65% uptake in the North. Budget rigidity also limits adoption of robotic surgery and AI diagnostics, maintaining a two-tier structure inside the Italy hospital supplies market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Disposables Anchor Infection-Control Protocols

Disposable Hospital Supplies captured 45.76% of 2025 demand as 530,000 hospital-acquired infections and 34% MRSA prevalence forced single-use workflows. The Italy hospital supplies market for disposables is forecast to reach USD 21.7 billion by 2031, supported by antimicrobial-resistant strains, including 27% of Klebsiella pneumoniae strains that are carbapenem-resistant. Operating Room Equipment will post an 8.43% CAGR, fueled by EUR 4.05 billion in PNRR funds for 3,100 large devices and by surgeon preference for robotic-assisted platforms. Value-based tenders award points for lifecycle services and predictive maintenance, elevating the portfolios of B. Braun, Stryker, and Medtronic.

Patient Examination Devices cater to 40.9% of citizens with chronic conditions and integrate Bluetooth links to FSE 2.0 dashboards. Mobility Aids gain traction among the elderly, while Sterilization equipment upgrades focus on automated cycle-logging to satisfy MDR post-market audits. Syringe and needle demand remains steady, yet safety-engineered retractable designs see faster uptake, encouraged by EU Directive 2010/32/EU.

By End User: Hospitals Dominate, ASCs Surge

Hospitals held 63.76% of 2025 procurement, supported by 210,000 beds across 1,050 facilities. The Italy hospital supplies market share for hospitals is projected to decline marginally as Decree 77/2022 steers low-complexity cases toward ASCs, which are now expanding at a 8.67% CAGR. Nurse shortages delay elective procedures, pushing hospitals to automate anesthesia records and instrument tracking. Community Houses and Diagnostic Centres grow under the same reform, demanding portable ultrasound, ECG, and point-of-care testing units.

Home health settings absorb oxygen concentrators and wound care supplies under telemedicine reimbursements. Specialty Clinics, particularly orthopedic and oncology hubs, are pursuing robotic platforms to differentiate their private-pay services. Distributors must now service a patchwork of micro-sites, shifting truckload logistics toward parcel-level fulfillment—an operational pivot defining competition in the Italyhospital supplies market.

By Distribution Channel: Tenders Persist, Digital Platforms Emerge

Direct Tender and Bulk Procurement accounted for 72.74% of 2025 volumes, with CONSIP’s EUR 28.3 billion annual frameworks covering everything from gloves to CT scanners. The Italy hospital supplies market size handled through tenders will still exceed USD 30 billion by 2031, yet growth tilts toward digital platforms. Distributor sales cover private clinics and aftermarket service, shielding vendors from tender-based price ceilings. E-commerce and GPO portals grow at 7.54% CAGR as buyers log into MePA for small orders or join private GPOs that aggregate ASC demand. However, fixed-term framework agreements limit online penetration to non-tendered SKUs in the Italy hospital supplies market.

Competitive Landscape

The Italy hospital supplies market is characterized by moderate fragmentation. Leading global players such as B. Braun, Baxter, Cardinal Health, Medtronic, Johnson & Johnson, and Stryker utilize value-based bundles and IoT telemetry to secure CONSIP lots. Companies like Philips, Siemens Healthineers, and GE Healthcare establish proprietary ecosystems within hospitals through cloud analytics and long-term service agreements. Local firms, including DE LAMA and Favero Health Projects, leverage shorter lead times and PNRR subsidies to win sterilization and furniture tenders, although expanding beyond regional markets remains a significant challenge.

Multinational companies address the 90-day payment delays prevalent in Southern markets by offering vendor-managed inventory and financing solutions. Smaller brands such as ConvaTec and Smith & Nephew concentrate on wound care and outpatient orthopedics, deploying clinical educators to improve tender scores by meeting training criteria. Additionally, EU MDR compliance has increased acquisition opportunities, as under-capitalized local manufacturers attract global players seeking expedited market entry.

Italy Hospital Supplies Industry Leaders

General Electric Company (GE Healthcare)

Invacare Corporation

DE LAMA S.P.A.

Althena Medical

Baxter International (Hill-Rom Services)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Italy, in partnership with the EU and Spain delivered advanced medical equipment to six Ethiopian hospitals to strengthen Ethiopia's healthcare system. The initiative aims to improve medical services and support progress toward universal health coverage.

- August 2025: Ningbo Medelast Co., Ltd., one of the leading medical bandages and disposables manufacturers, launched its Sterile Finger Bandage with Foam in Italy. This expansion aligns with the company's strategy to offer quality wound care globally, capitalizing on its product development expertise.

Italy Hospital Supplies Market Report Scope

As per the scope of the report, hospital supplies are medical or surgical items that are consumable, expendable, disposable, or non-durable and that are used for the treatment or diagnosis of a patient's specific illness, injury, or condition in hospital settings.

The Italy Hospital Supplies Market is Segmented by Product (Patient Examination Devices, Operating Room Equipment, Mobility Aids & Transportation Equipment, Sterilisation & Disinfectant Equipment, Disposable Hospital Supplies, Syringes & Needles, and Other Products), End User (Ambulatory Surgical Centres, Diagnostic Centres, Home-Health-Care Settings, Hospitals, Specialty Clinics, and Other End Users), and Distribution Channel (Direct Tender / Bulk Procurement, Distributor & Dealer Sales, and E-Commerce & GPO Platforms). The report offers the value (in USD million) for the above segments.

By Product

| Patient Examination Devices |

| Operating Room Equipment |

| Mobility Aids & Transportation Equipment |

| Sterilisation & Disinfectant Equipment |

| Disposable Hospital Supplies |

| Syringes & Needles |

| Other Products |

By End User

| Ambulatory Surgical Centres |

| Diagnostic Centres |

| Home-Health-Care Settings |

| Hospitals |

| Specialty Clinics |

| Other End Users |

By Distribution Channel

| Direct Tender / Bulk Procurement |

| Distributor & Dealer Sales |

| E-Commerce & GPO Platforms |

| By Product | Patient Examination Devices |

| Operating Room Equipment | |

| Mobility Aids & Transportation Equipment | |

| Sterilisation & Disinfectant Equipment | |

| Disposable Hospital Supplies | |

| Syringes & Needles | |

| Other Products | |

| By End User | Ambulatory Surgical Centres |

| Diagnostic Centres | |

| Home-Health-Care Settings | |

| Hospitals | |

| Specialty Clinics | |

| Other End Users | |

| By Distribution Channel | Direct Tender / Bulk Procurement |

| Distributor & Dealer Sales | |

| E-Commerce & GPO Platforms |

Key Questions Answered in the Report

How large is the Italy Hospital Supplies market in 2026?

The Italy hospital supplies market size reached USD 34.62 billion in 2026.

What is the expected CAGR for hospital supplies sales in Italy through 2031?

Sales are projected to grow at a 6.53% CAGR between 2026 and 2031.

Which product segment leads spending?

Disposable hospital supplies led with 45.76% of sales in 2025.

Why are Ambulatory Surgical Centres growing quickly?

Decree 77/2022 shifts elective surgeries to outpatient settings, driving an 8.67% CAGR for ASC demand.

How is digital health influencing procurement?

FSE 2.0 and EUR 1.67 billion in PNRR digital funds are boosting demand for IoT-enabled devices that integrate with electronic health records.

What challenges affect smaller Italian manufacturers?

EU MDR compliance costs and fixed-price CONSIP frameworks compress margins and lengthen tender cycles.

Page last updated on: