Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.73 Billion |

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

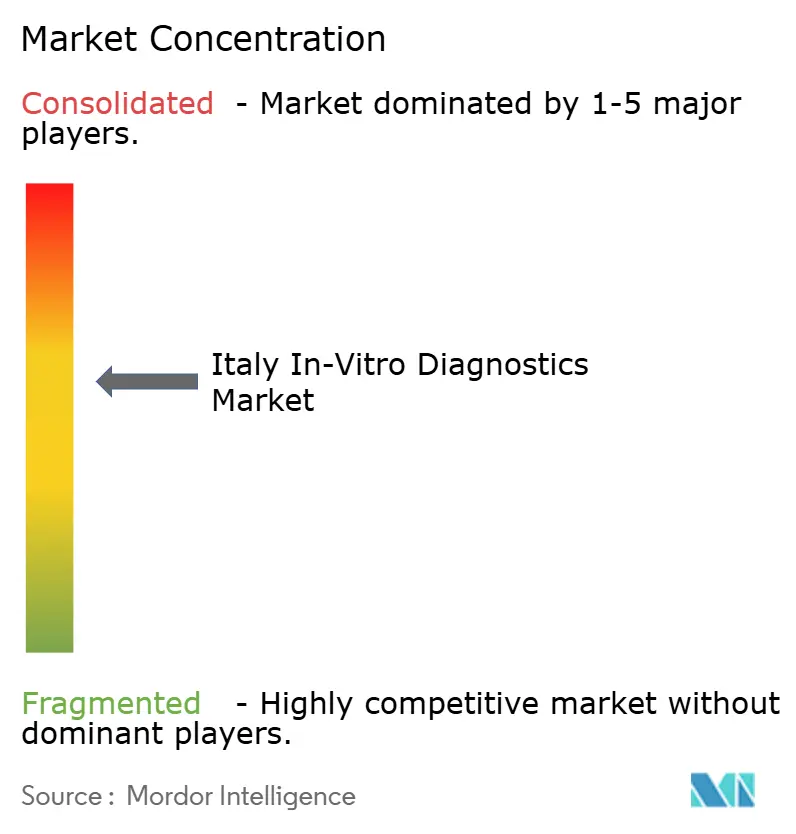

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Italy in vitro diagnostics market size was valued at USD 3.73 billion in 2025 and estimated to grow from USD 3.89 billion in 2026 to reach USD 4.82 billion by 2031, at a CAGR of 4.35% during the forecast period (2026-2031). Growth is sustained by the rising prevalence of chronic diseases, steady gains in preventive health screening, and rapid uptake of advanced molecular platforms that cut turnaround times and broaden test menus. Regulatory alignment with the EU IVDR is adding short-term certification costs yet is expected to improve product quality and patient safety over the forecast horizon. Technology convergence, particularly the pairing of microfluidics with artificial intelligence, continues to lower sample-volume requirements while boosting diagnostic accuracy, a trend most visible in oncology-focused liquid biopsy and multiplex PCR assays. Meanwhile, demand for point-of-care (POC) solutions is accelerating as regional authorities push diagnostics closer to primary-care and home settings to relieve capacity constraints in the hospital network.

Key Report Takeaways

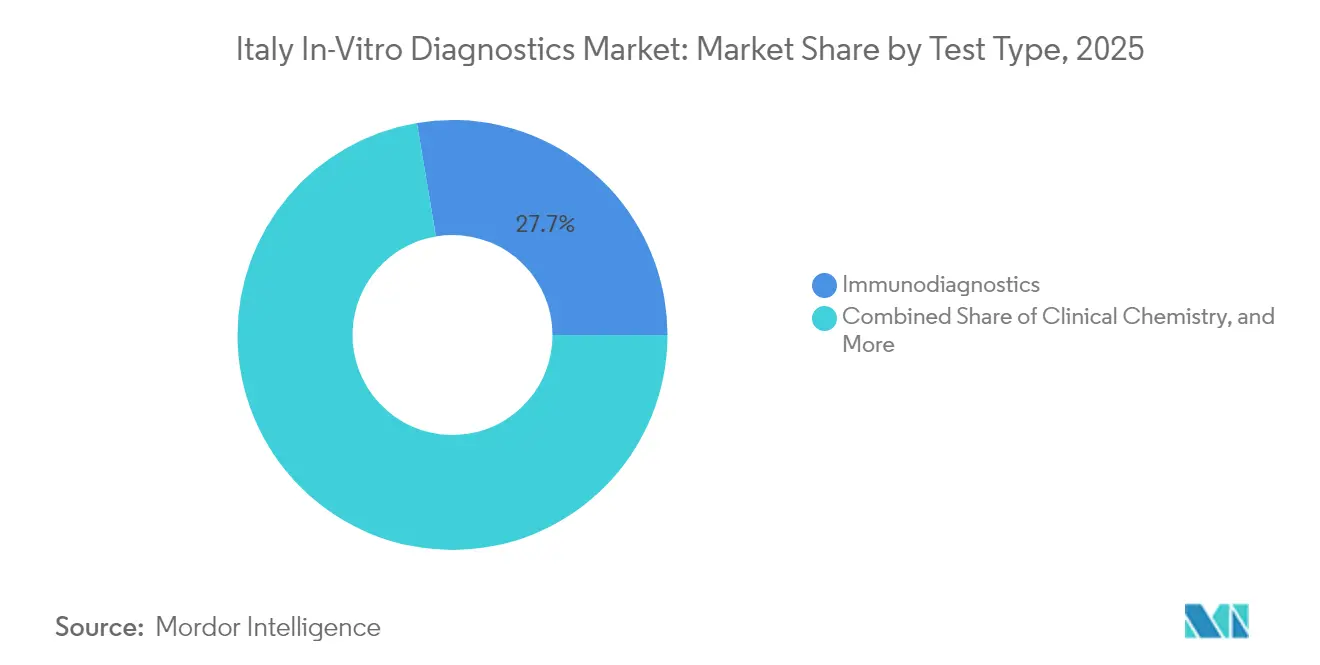

- By test type, immunodiagnostics led with 27.65% revenue share in 2025, while molecular diagnostics is projected to advance at a 7.66% CAGR through 2031.

- By product, reagents and consumables commanded 64.32% of the Italy in vitro diagnostics market size in 2025 and are growing at 5.78% CAGR to 2031.

- By usability, disposable devices held 71.18% of the market in 2025 and are expanding at 5.77% CAGR through 2031.

- By mode of testing, laboratory-based diagnostics accounted for 80.35% of the Italy in vitro diagnostics market share in 2025, whereas point-of-care platforms are rising at an 8.16% CAGR.

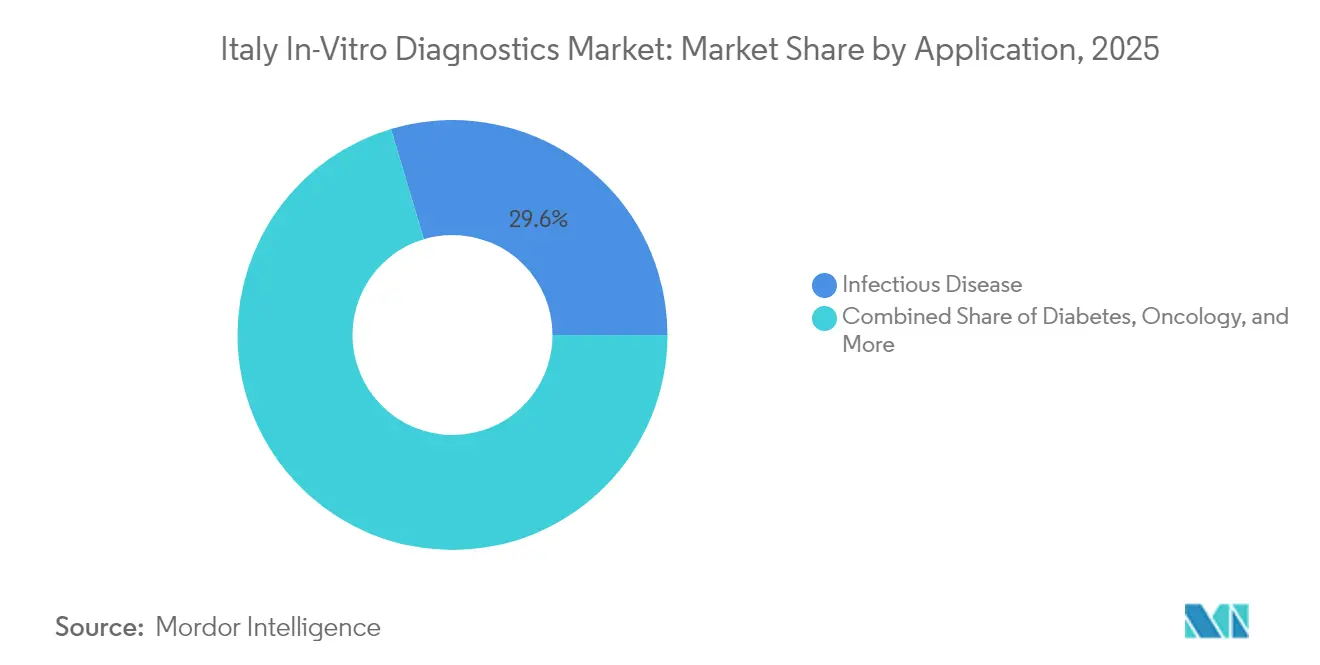

- By application, infectious-disease testing contributed 29.62% of 2025 revenue, while oncology diagnostics is the fastest-growing segment at an 7.96% CAGR.

- By end user, hospitals and clinics represented 51.55% of sales in 2025; independent diagnostic laboratories record the briskest growth at 6.09% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic & lifestyle diseases | +1.8% | National; higher prevalence in North | Long term (≥ 4 years) |

| Rapid technological innovation in molecular & immunodiagnostics | +1.2% | National; urban centers | Medium term (2-4 years) |

| Expansion of point-of-care testing | +0.9% | National; emphasis in South | Medium term (2-4 years) |

| Government & EU investment programs for digital lab modernization | +0.7% | National; early roll-out in North | Short term (≤ 2 years) |

| Growth of precision medicine & companion diagnostics | +0.5% | Northern regions & academic hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Lifestyle Diseases (Diabetes, CVD, Cancer)

Chronic conditions now affect a growing share of Italy’s population, with 3.9 million residents living with diabetes in 2024 and cardiovascular disease remaining the top cause of mortality[1]bioMérieux, “Universal Registration Document 2024,” biomerieux.com. Larger case volumes have spurred demand for continuous glucose-monitoring, high-sensitivity cardiac-marker assays, and multi-parameter panels that profile several risk factors in one run. Payers see diagnostics as a lever to curb treatment costs exceeding EUR 20 billion per year, fostering favorable reimbursement for early-detection tools. Laboratories increasingly deploy integrated platforms that simultaneously analyze metabolic and inflammatory markers, improving patient stratification while conserving reagents. This long-term epidemiological shift underpins steady increases in routine test volumes, thereby stabilizing reagent demand across the Italy in vitro diagnostics market.

Rapid Technological Innovation in Molecular & Immunodiagnostics

Next-generation sequencing and multiplex PCR have reached cost and throughput thresholds suited for routine use in tertiary centers, cutting time-to-result and enabling wider gene panels. Microfluidic cartridges now process smaller sample volumes, a crucial advantage in pediatrics and oncology biopsies. Italian labs are retrofitting COVID-era PCR instruments for oncology, sepsis, and antimicrobial-resistance panels, which lifts system utilization and lowers per-test costs. Immunodiagnostics benefit from chemiluminescent platforms that automate up to 240 tests per hour, expanding menus into fertility, thyroid, and autoimmune markers. As genomic and proteomic data converge, clinicians gain richer insights that feed into personalized-medicine protocols, sustaining above-market growth for molecular assays.

Expansion of Point-of-Care Testing Across Primary & Home Settings

POC uptake is strongest in underserved provinces of Southern Italy, where decentralized testing alleviates travel burdens for chronic-care patients. Handheld lateral-flow and isothermal-amplification devices now deliver influenza, RSV, and Streptococcus results in under 20 minutes, supporting rapid treatment decisions. Connectivity modules route encrypted data to regional laboratory hubs, ensuring quality oversight and creating longitudinal patient records. Smartphone-based readers exploit Italy’s 83% mobile-penetration rate to extend diagnostics into home care, a model embraced by community nurses tasked with monitoring elderly patients. Vendors with cloud dashboards gain a competitive edge by offering clinicians real-time population-level surveillance data.

Government & EU Investment Programs for Digital Lab Modernization

Through the National Recovery and Resilience Plan, Italy has earmarked EUR 15.63 billion (USD 17.85 billion) for health-system upgrades, a share of which finances total laboratory automation lines and middleware. Early beneficiary regions such as Lombardy report 25% higher daily throughput and 18% lower reagent waste after automation roll-outs. Parallel EU projects under the European Health Data Space aim to standardize data-exchange protocols, opening the door to cross-border tele-consults and pan-European disease registries. Manufacturers able to bundle instruments, reagents, AI analytics, and support services are increasingly preferred in tenders as procurement bodies favor full-solution offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent & evolving EU IVDR regulatory landscape | -0.7% | National; SMEs hit hardest | Medium term (2-4 years) |

| Regional reimbursement delays & budget constraints | -0.5% | More severe in South | Short term (≤ 2 years) |

| Shortage of skilled laboratory personnel & training gaps | -0.3% | National; rural deficit | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent & Evolving EU IVDR Regulatory Landscape

The IVDR recasts most assays into higher-risk classes that demand stricter clinical-evidence dossiers and ongoing post-market surveillance. Only 12 notified bodies were approved for IVDR certification by 2024, creating application backlogs that slow product launches[2]Confindustria Dispositivi Medici, “Challenges in Europe’s Medical Technology Regulatory Framework,” confindustradm.it. Compliance expenses can absorb 5–15% of annual revenue for smaller firms, prompting some to withdraw niche tests rather than fund new studies. Larger multinationals use this window to consolidate share by acquiring domestic peers struggling with documentation upgrades. Although transition deadlines stretch to 2029 for low-risk assays, market-access uncertainty weighs on near-term investment decisions.

Regional Reimbursement Delays & Budget Constraints

Italy’s 20 regions set their own reimbursement schedules, producing approval lags ranging from six to 18 months[3]Marcella Marletta, “Establishing a National HTA Program for Medical Devices in Italy,” researchgate.net. Post-pandemic spending reviews prioritized acute-care bed capacity, temporarily displacing funding for advanced diagnostics. The national HTA program aims to harmonize evaluation criteria, yet uneven staffing levels cause inconsistent adoption timelines. Vendors with robust regional-access teams and evidence packages tailored to local cost-effectiveness thresholds accelerate listing success, whereas newcomers face uphill entry barriers, particularly in Southern regions facing tighter budget ceilings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular innovation accelerates market diversification

Immunodiagnostics commanded 27.65% of 2025 revenue, underpinning routine panels for thyroid disorders, fertility, and infectious-disease serology. The stable reimbursement environment and broad installed base of chemiluminescent analyzers anchor segment growth at mid-single-digit rates. Molecular diagnostics, though starting from a smaller base, is charting a 7.66% CAGR as next-generation sequencing migrates from reference labs to tertiary hospitals, extending coverage into oncology minimal-residual-disease monitoring. The Italy in vitro diagnostics market size attributed to molecular assays is expected to double between 2025 and 2030, reflecting expanded syndromic respiratory panels and liquid biopsy uptake. Convergence trends see multiplex platforms combining nucleic-acid detection with immuno-capture technologies, enabling laboratories to consolidate instrument fleets while widening their menus.

COVID-19 infrastructure—high-throughput PCR cyclers and automated extractors—is now repurposed for sexually transmitted infections and antimicrobial-resistance testing, lifting utilization rates. Italian start-ups innovate in microfluidic chip fabrication that slashes reagent volumes, appealing to budget-conscious regional health systems. Immunodiagnostic suppliers respond with high-sensitivity assays targeting neurodegeneration and emerging zoonoses, while molecular vendors court oncology centers with bundled assay-plus-bioinformatics offerings. Such dynamics reinforce technology pluralism and foster cross-segment collaboration within the Italy in vitro diagnostics market.

By Product: Reagents retain revenue primacy amid instrument upgrades

Reagents and consumables generated 64.32% of turnover in 2025, a share driven by recurring demand patterns that stabilize cash flows for suppliers. Rising test volumes in chronic-disease monitoring lift lot sizes, helping laboratories negotiate bulk-purchase discounts. Still, the closed-system philosophy of many analyzers preserves vendor pricing power and sustains gross margins that often exceed 60%. Instruments and analyzers post a 6.37% CAGR as facilities modernize to automated track systems capable of 3,000 tubes per hour, mitigating staff shortages and lowering per-sample cost. Software and informatics solutions—ranging from middleware to AI-enabled decision support—emerge as the highest-margin category and are frequently bundled under reagent-rental contracts that shift capital expenditure into operating budgets.

Total-laboratory-automation lines gain favor in university hospitals, where they drive 20% reductions in manual handling errors. Cloud-delivered quality-control dashboards help regional health authorities monitor laboratory performance, a feature aligning well with new IVDR post-market surveillance rules. Open-platform advocates push for reagent interoperability to reduce costs, yet proprietary-reagent strategies remain prevalent as suppliers prioritize life-cycle revenue streams.

By Usability: Disposable formats extend reach beyond hospital walls

Disposable devices captured 71.18% of sales in 2025, buoyed by infection-control guidelines and ease-of-use in decentralized sites. Lateral-flow cartridges now screen not only pregnancy and influenza but also cardiac troponin and C-reactive protein, broadening their clinical utility. Innovations in biodegradable polymers address environmental concerns and comply with tightening waste-disposal rules in several Italian regions. Reusable platforms continue to dominate high-complexity testing such as hematology analyzers that rely on flow-cell optics difficult to miniaturize. Hybrid concepts pairing reusable optical readers with single-use nucleic-acid cartridges blur traditional boundaries and support on-demand testing in emergency departments.

Investment in eco-design also permeates reusable instruments, with sleep-mode energy savers and modular upgrades that extend life spans. Service contracts increasingly include sustainable-operation clauses focusing on reduced water and reagent consumption. The Italy in vitro diagnostics market share for disposable devices is predicted to inch higher as home-based chronic-care programs incorporate self-testing strips linked to telehealth portals. Nevertheless, reusable systems will continue to underpin high-throughput labs thanks to economies of scale and deeper analytic capabilities.

By Mode of Testing: Point-of-care momentum challenges laboratory primacy

Central laboratories still process 80.35% of diagnostic throughput thanks to economies of scale, comprehensive quality systems, and advanced automation. The Italy in vitro diagnostics market size linked to lab-based workflows is set to reach USD 3.77 billion by 2031 even as growth moderates. Total-laboratory-automation and track-management systems shorten sample dwell time by as much as 40%, mitigating personnel shortages and elevating consistency. Point-of-care testing, expanding at 8.16% CAGR, leverages handheld molecular readers that deliver CLIA-grade accuracy within 15 minutes, reshaping emergency and primary-care algorithms.

Regional programs in Calabria and Sicily deploy mobile POC vans equipped with multiplex respiratory panels, narrowing rural diagnostic gaps. Connectivity ensures that results flow into electronic health records and national surveillance networks, satisfying IVDR traceability mandates. Laboratory managers collaborate with POC coordinators to standardize quality controls, thereby integrating off-site testing into accreditation cycles. Vendors offering unified middleware that harmonizes data across instrument classes gain procurement preference.

By Application: Oncology outpaces infectious-disease incumbency

Infectious-disease assays contributed 29.62% of 2025 revenue, underpinned by routine respiratory panels and sexually transmitted infection testing. Multiplex syndromic cartridges capable of detecting up to 16 pathogens expedite treatment decisions in emergency departments, curbing empirical antibiotic use. Oncology, advancing at 7.96% CAGR, benefits from liquid-biopsy tests that analyze circulating tumor DNA to guide targeted therapy and monitor minimal residual disease. Companion-diagnostic requirements embedded in AIFA reimbursement policies have entrenched molecular profiling in standard oncology care pathways.

Diabetes and cardiology segments maintain relevance through point-of-care HbA1c and high-sensitivity troponin assays, respectively. Autoimmune panels grow on the back of rising awareness and improved assay specificity. Multi-analyte risk-assessment panels linking inflammatory and metabolic markers gain traction in preventive-cardiology clinics. The Italy in vitro diagnostics market continues to diversify as neurodegeneration markers and microbiome-profiling kits enter early-adopter centers, indicating future niches for expansion.

By End-User: Independent labs strengthen as outsourcing rises

Hospitals and clinics accounted for 51.55% of 2025 demand, owing to integrated care pathways and critical-care testing needs. Consolidation within regional health networks drives core-lab centralization, while satellite POC sites maintain rapid-response capabilities. Diagnostic laboratories, posting a 6.09% CAGR, absorb overflow testing and specialize in high-complexity services such as whole-exome sequencing, fueling competitive tendering for courier and data-integration contracts. Academic centers pioneer pilot programs in AI-assisted histopathology that later diffuse to public hospitals after cost-benefit validation.

Home-care initiatives rely on connected glucometers and coagulation monitors that transmit data to telehealth portals, reducing outpatient visits. Device makers bundle remote-monitoring software that alerts clinicians to threshold breaches, supporting reimbursement models based on avoided hospitalizations. The Italy in vitro diagnostics industry is thus broadening its customer base from traditional labs to include digital-health providers and primary-care consortia.

Geography Analysis

Northern Italy, led by Lombardy and Veneto, captures the lion’s share of spending owing to higher per-capita income, dense hospital networks, and early adoption of automation. Laboratories here often serve as reference hubs for neighboring regions, pulling in send-out testing volumes and driving scale advantages. Central regions such as Lazio and Tuscany focus investments on precision-medicine programs partnered with academic medical centers, thereby boosting demand for NGS oncology panels. Southern regions exhibit lower penetration rates but supply the fastest incremental growth as POC deployments and mobile units bridge infrastructure gaps.

Regional financing disparities shape procurement cycles: northern authorities allocate larger budgets for capital-intensive automation, whereas southern counterparts favor reagent-rental contracts that spread costs over multiple years. EU cohesion funds have financed digital-pathology pilots in Sardinia, proving the feasibility of tele-consultation workflows that link rural hospitals with mainland experts. Collaboration among regions through the National HTA program aims to harmonize evaluation metrics, yet reimbursement delays still average nine months longer in the South, slowing market entry for novel assays.

Cross-border patient flows with Switzerland, France, and Slovenia foster demand for multilingual lab information systems and standardized reporting formats, aligning with European Health Data Space objectives. The Italy in vitro diagnostics market benefits from medical-tourism inflows into Lombardy oncology centers, raising assay volumes in molecular pathology units. Conversely, emigration of healthcare professionals from the South to the North exacerbates personnel shortages, prompting southern authorities to emphasize automation and remote-support contracts to sustain lab operations.

Competitive Landscape

Five multinational and domestic leaders—Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, DiaSorin, and Menarini Diagnostics—jointly generated a significant market share of 2024 revenue. Roche maintains a comprehensive core-lab portfolio combined with digital middleware, reinforcing loyalty among large hospital customers. Abbott leverages strong positions in POC cardiology markers and immunoassays, while Siemens extends reach through total-lab-automation tracks integrated with its Atellica analyzers. DiaSorin capitalizes on immunodiagnostic expertise and the 2024 Luminex acquisition to diversify into molecular syndromic panels, strengthening its Italian base. Menarini focuses on hematology and hemoglobinopathy analyzers tailored to regional lab workflows.

Strategic thrusts center on technology integration: artificial-intelligence modules overlay image analysis in histopathology; cloud-based dashboards streamline quality control; and reagent-rental models lock in multi-year consumable revenue. Market-access capabilities differentiate players as regional tendering intensifies; vendors with in-house health-economic teams secure swift reimbursement listings. Partnerships between diagnostics and pharma proliferate, with co-development agreements for companion tests covering lung, breast, and gastrointestinal cancers.

White-space opportunities persist in neurodegenerative-disease biomarkers, microbiome analytics, and non-invasive prenatal testing. Domestic SMEs such as Sentinel Diagnostics carve niches through agile R&D and customization services, while AI start-ups collaborate with pathology networks to deploy cloud-native image-analytics pipelines. IVDR compliance pressures are accelerating acquisitions of smaller firms lacking certification resources, indicative of a consolidation trend that will reshape the Italy in vitro diagnostics market over the coming five years.

Italy In-Vitro Diagnostics Industry Leaders

Thermo Fischer Scientific Inc.

Abbott Laboratories

F. Hoffmann-La Roche AG

Siemens Healthineers AG

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Aiforia Technologies partnered with Sardinia’s regional health authority to extend AI pathology solutions, marking its third Italian regional contract.

- February 2025: Aiforia Technologies obtained IVDR certification for its cancer-diagnostic AI models, enabling CE-IVD marketing across Europe.

- January 2025: Aiforia Technologies was selected by Lombardy’s health authority to deploy AI-assisted analysis for breast, lung, and prostate cancer biopsies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian in-vitro diagnostics (IVD) market as all reagent kits, consumables, software, and analyzers cleared for human clinical testing that detect, monitor, or screen diseases using patient specimens processed in laboratories or point-of-care settings.

Scope Exclusion: Research-use-only platforms and veterinary diagnostics are kept outside the modeled universe.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immunodiagnostics

- Molecular Diagnostics

- Hematology

- Microbiology

- Coagulation

- Point-of-Care (POC) Tests

- By Product

- Instruments & Analyzers

- Reagents & Consumables

- Software & Services

- By Usability

- Disposable IVD Devices

- Reusable IVD Devices

- By Mode of Testing

- Laboratory-Based Testing

- Point-of-Care Testing

- By Application

- Infectious Disease

- Diabetes

- Oncology (Cancer)

- Cardiology

- Autoimmune Disorders

- Other Applications

- By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

- Home-Care / Ambulatory POC Settings

- Other End-Users

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews and online surveys with hospital lab managers, private diagnostic chains, regional health-authority buyers, reagent distributors, and regulatory consultants helped us validate usage rates, price erosion, and compliance costs across North, Central, and Southern Italy. These conversations filled blind spots left by secondary data and anchored our scenario assumptions.

Desk Research

We began with public datasets from ISTAT's health expenditure tables, the Ministry of Health's laboratory tariff schedules, OECD health statistics, and MedTech Europe's GDMS country panels; these sources framed utilization volumes and pricing envelopes. Trade association briefs from Confindustria Dispositivi Medici, peer-reviewed journals on molecular assay uptake, and EU IVDR dossiers enriched trend mapping. Paid assets such as D&B Hoovers for company splits and Dow Jones Factiva for deal tracking sharpened revenue attribution. A wider pool of annual reports, investor decks, and patent counts (Questel) completed the desk scan. This list is illustrative; many additional references fed triangulation and sanity checks.

Second-level desk work pulled in import codes for PCR reagents, reimbursement circulars, and hospital procurement notices, giving us unit flow estimates and benchmark average selling prices.

Market-Sizing & Forecasting

A top-down construct starts with national laboratory spend, COVID-related step-downs, and test-volume forecasts, which are then split by technology using penetration ratios gleaned from expert interviews. Sampled supplier roll-ups (reagents × ASP) serve as a bottom-up sense check before final alignment. Key variables include population aged 65+, diabetes prevalence, molecular test reimbursement tariffs, IVDR transition timeline, and hospital budget growth. A multivariate regression model links these drivers to historical IVD revenue, generating the 2025-2030 curve and enabling scenario tweaking when any driver shifts. Gap cells in bottom-up estimates are bridged by industry-standard reagent-to-instrument revenue multipliers vetted with respondents.

Data Validation & Update Cycle

Mordor analysts run variance screens versus MedTech Europe market totals, macro-economic indicators, and quarterly earnings. Outliers trigger peer review and, if needed, a respondent call-back. The model refreshes every 12 months; material events (e.g. tariff resets) prompt an interim patch before client delivery.

Why Our Italy In-Vitro Diagnostics Baseline Earns Decision-Maker Trust

Published estimates often diverge because each firm selects different base years, COVID adjustments, and scope filters.

Key gap drivers here include pandemic windfall carry-over, inclusion or exclusion of capital equipment, and currency-conversion practices that some publishers neglect to update once inflation cools.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.73 bn (2025) | Mordor Intelligence | - |

| USD 4.36 bn (2022) | Global Consultancy A | Elevated by one-off PCR surge and older base year |

| USD 2.89 bn (2024) | Regional Consultancy B | Omits instruments and LDT revenue streams |

| USD 3.83 bn (2023) | Industry Analyst C | Uses static ASPs and average 2023 FX without inflation reset |

These contrasts show that Mordor's disciplined scope, driver-linked forecasting, and annual refresh cadence give stakeholders a balanced, transparent baseline they can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the Italy in vitro diagnostics market and how large will it be by 2031?

The market is worth USD 3.89 billion in 2026 and is expected to reach USD 4.82 billion by 2031.

What compound annual growth rate (CAGR) is projected for Italy’s in vitro diagnostics market?

The overall market is forecast to expand at a 4.35% CAGR between 2026 and 2031.

Which test-type segment is growing the fastest?

Molecular diagnostics leads growth with a 7.66% CAGR, driven by wider use of next-generation sequencing and liquid biopsy assays.

How is the EU In Vitro Diagnostic Regulation (IVDR) influencing Italian market dynamics?

IVDR adds stricter clinical-evidence and surveillance requirements, raising compliance costs—especially for SMEs—and encouraging consolidation among manufacturers.

Why is point-of-care testing gaining traction in Italy?

Point-of-care devices are growing at an 8.16% CAGR as regional health authorities push diagnostics into primary-care and home settings to improve access and relieve hospital pressure.

Which product category generates the majority of recurring revenue?

Reagents and consumables account for 64.32% of 2025 sales, reflecting the recurring revenue model that underpins the industry’s profitability.

Page last updated on: