Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

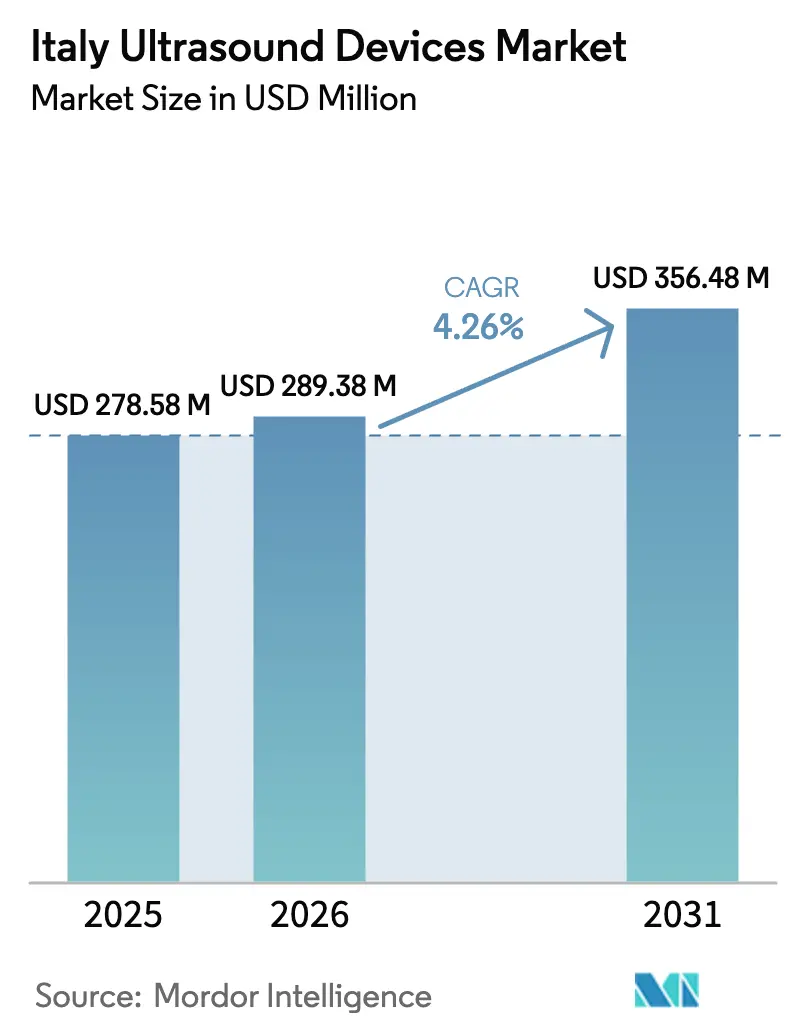

| Base Year Market Size (2025) | USD 278.58 Million |

| Market Size (2026) | USD 289.38 Million |

| Market Size (2031) | USD 356.48 Million |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Ultrasound Devices Market Analysis by Mordor Intelligence

The Italy Ultrasound Devices Market size is expected to grow from USD 278.58 million in 2025 to USD 289.38 million in 2026 and is forecast to reach USD 356.48 million by 2031 at 4.26% CAGR over 2026-2031.

Public-sector orders placed under the Piano Nazionale di Ripresa e Resilienza (PNRR) are standardizing equipment specifications, while point-of-care and handheld scanners reshape purchasing criteria. Vendor competition pivots on artificial-intelligence automation, tele-ultrasound readiness, and green-procurement compliance, with multi-year framework contracts defining regional access dynamics. Operators in the Italian ultrasound devices market now balance capital refresh cycles for stationary consoles with the need to equip emergency departments, intensive care units, and home health teams with portable alternatives. Reimbursement certainty under the Servizio Sanitario Nazionale (SSN) supports consistently high examination volumes, yet North-South funding gaps, Medical Device Regulation (MDR) conformity delays, and workforce shortages temper growth headroom.

Key Report Takeaways

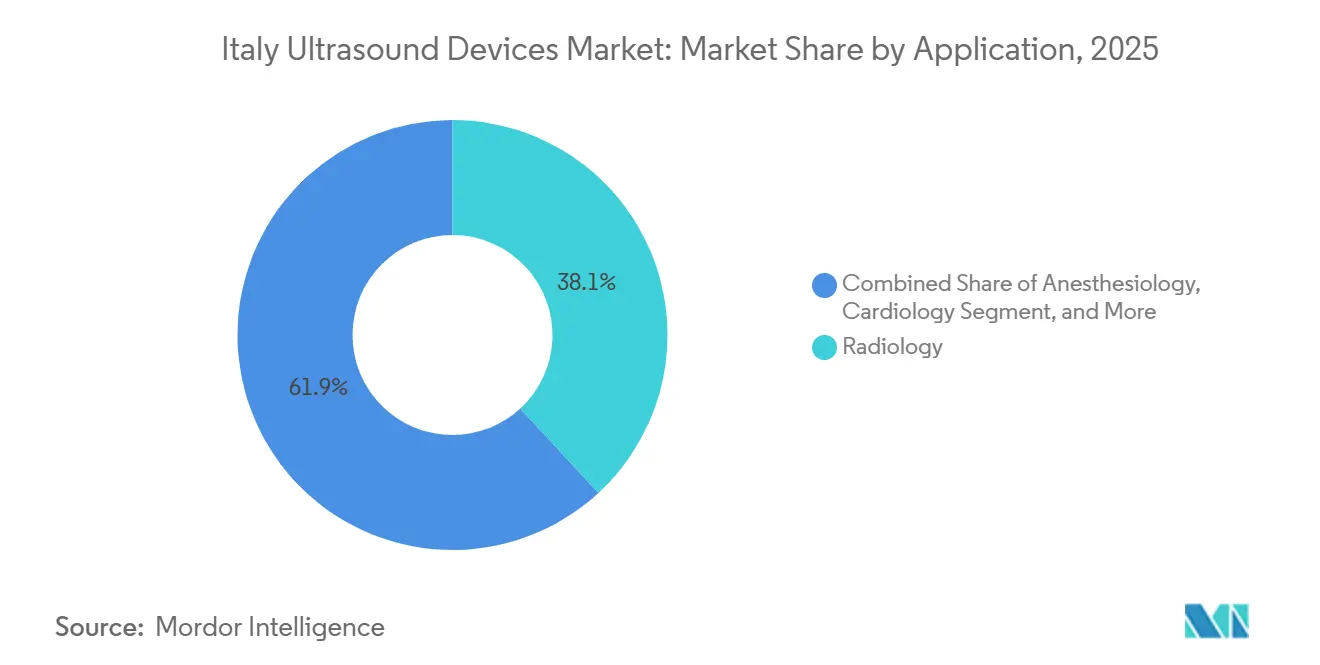

- By application, radiology led with 38.13% revenue share in 2025, while critical care is advancing at a 5.83% CAGR through 2031.

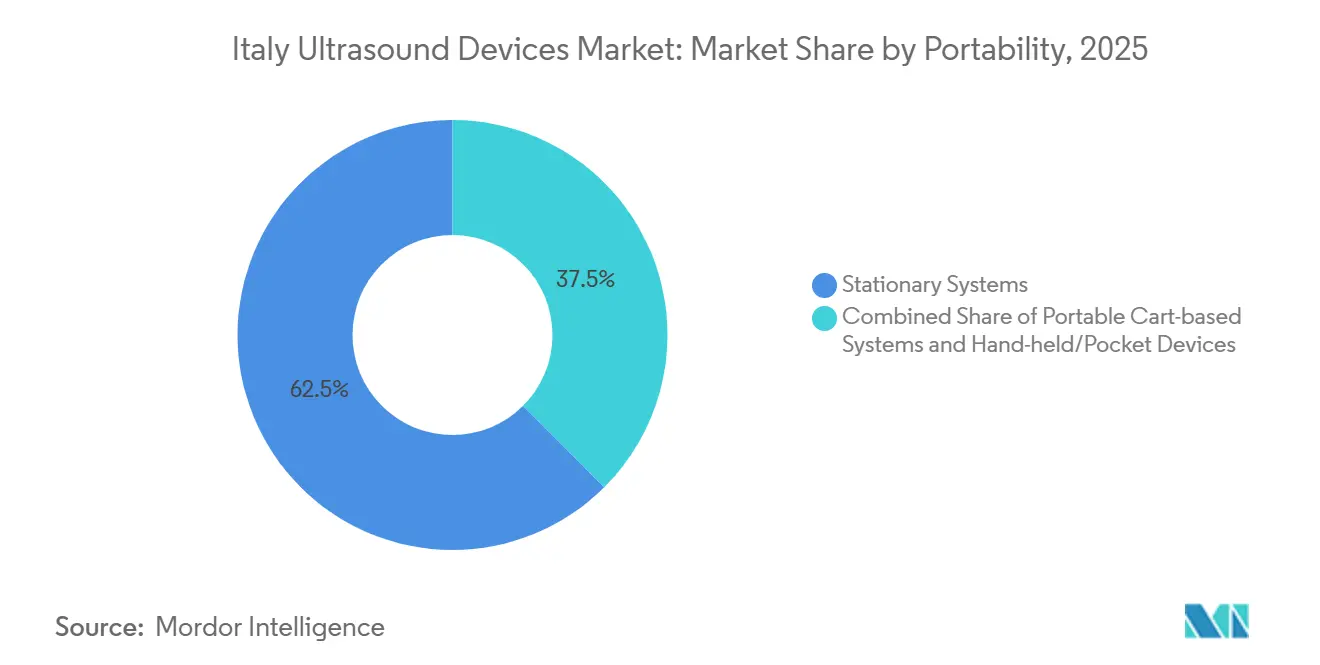

- By portability, stationary systems held 62.47% of the Italian ultrasound devices market share in 2025, yet handheld and pocket units are projected to expand at a 7.18% CAGR to 2031.

- By technology, 3D and 4D imaging accounted for 41.87% of 2025 revenue, whereas high-intensity focused ultrasound is the fastest-growing segment with a 5.33% CAGR through 2031.

- By end user, hospitals captured 54.64% of 2025 revenue, while the home healthcare segment is forecast to expand at a 6.68% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Population & Chronic-Disease Burden Escalation | +0.8% | National, higher in northern regions | Long term (≥ 4 years) |

| Technology Shift to 3D/4D & AI-Enabled Imaging | +0.9% | National, early adoption in Milan, Rome, Bologna | Medium term (2-4 years) |

| Rapid Adoption of Point-Of-Care Ultrasound | +1.0% | National, strongest in EDs and ICUs | Short term (≤ 2 years) |

| Favorable SSN Reimbursement for Ultrasound Procedures | +0.6% | National | Medium term (2-4 years) |

| Tele-Ultrasound Integration Backed by PNRR Funds | +0.7% | National, focus on rural and southern areas | Medium term (2-4 years) |

| EU Green-Procurement Push for Energy-Efficient Scanners | +0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Chronic-Disease Burden Escalation

Italy’s population aged ≥ 65 continues to expand, elevating demand for ultrasound in cardiology, musculoskeletal, and vascular care.[1]World Health Organization, “Noncommunicable Diseases Country Profiles – Italy,” who.int Hospitals prefer ultrasound over ionizing imaging for frail patients because it is bedside-ready, cost-efficient, and radiation-free. Geriatric wards increasingly rely on cart-based consoles for pleural-effusion checks and bladder scanning, while adding handheld probes for ward rounds. Stable reimbursement under the SSN assures high utilization, sustaining the replacement cycle for legacy fleets and reinforcing the trajectory of the Italy ultrasound devices market.

Technology Shift to 3D/4D & AI-Enabled Imaging

3D and 4D ultrasound dominate value, as obstetrics departments follow the protocols of the Società Italiana di Ecografia Ostetrica e Ginecologica, which mandate detailed anatomy scans. AI modules such as GE HealthCare’s SonoLyst trim examination time by 65%, while cardiac departments validate handheld AI tools that approximate MRI-derived ejection fraction. Hospitals justify the premium by quantifying throughput gains and consistent measurements, prompting vendors to monetize software upgrades across installed bases.

Rapid Adoption of Point-Of-Care Ultrasound

Point-of-care protocols became routine after COVID-19. National surveys show 79% physician uptake of lung investigations and 78% handheld device usage. Emergency and critical-care teams use handheld probes for trauma triage, serial hemodynamic checks, and gastric residual estimation, displacing computed tomography in selected pathways. The SSN now lists point-of-care ultrasound as a billable code, catalyzing decentralized procurement that is pulling the Italian ultrasound devices market toward rugged, battery-powered formats.

Favorable SSN Reimbursement for Ultrasound Procedures

Ultrasound tariffs safeguard hospital margins compared with CT or MRI, especially for obstetric scans covered at three gestational milestones and for cardiology’s full echocardiography suite.[2]Governo Italiano, “Piano Nazionale di Ripresa e Resilienza – Missione 6 Salute,” governo.it Tele-ultrasound rules reimburse both image acquisition and off-site interpretation, fuelling growth in home health and rural clinics. Predictable cash flows encourage regional authorities to prioritize ultrasound in capital budgets, strengthening the outlook for the Italy ultrasound devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition & Maintenance Costs | -0.5% | National, acute in southern regions | Medium term (2-4 years) |

| Shortage of Skilled Sonographers | -0.4% | National, rural and southern areas | Long term (≥ 4 years) |

| MDR Conformity-Assessment Delays | -0.3% | National | Short term (≤ 2 years) |

| North-South Healthcare Funding Disparities | -0.3% | Southern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Maintenance Costs

Premium 3D/4D consoles list at EUR 100,000-150,000, with annual service at 8-12% of purchase price, challenging hospitals in Calabria, Campania, and Sicily, where per-capita health spending trails the national mean. PNRR tenders favor mid-tier platforms costing EUR 82,000, but leasing and pay-per-use models remain scarce. Cost pressure accelerates the 7.18% CAGR for handheld devices priced at EUR 5,000-10,000 and influences the modality mix throughout the Italy ultrasound devices market.

Shortage of Skilled Sonographers

Professional bodies report persistent workforce gaps. Emergency and critical-care settings expanded the scope of ultrasound, yet residency programs graduate fewer than 200 emergency physicians a year, insufficient for the 500+ departments nationwide. AI guidance mitigates but does not eliminate operator dependency; limited off-shift staffing constrains scanner utilization and lengthens waiting lists in southern provinces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Surges as POCUS Embeds in ICU Workflows

Critical-care ultrasound is projected to post a 5.83% CAGR, outpacing all other uses. The Italian ultrasound devices market for this segment benefits from 79% physician adoption of lung and cardiac protocols, serial hemodynamic monitoring, and bedside-guided procedures. Radiology still accounts for the largest slice at 38.13% of 2025 revenue, but its lower growth reflects competition from CT and MRI in complex cases. Parallel demand persists in cardiology, obstetrics-gynecology, musculoskeletal, and vascular clinics, each supported by specialty society guidelines that mandate ultrasound at defined intervals.

Radiology departments continue to purchase feature-rich consoles equipped with advanced Doppler and elastography, while ICUs and emergency rooms procure portable or handheld units optimized for infection-control and battery runtime. This bifurcation deepens channel specialization: purchasing teams increasingly split tenders by clinical domain to match device attributes with workflow needs. As a result, the Italy ultrasound devices market share for critical-care applications steadily rises within hospital budgets.

By Technology: HIFU Gains Clinical Traction in Oncology and Orthopedics

Three- and four-dimensional imaging captured 41.87% of 2025 technology revenue driven by obstetric and cardiac demand, yet high-intensity focused ultrasound (HIFU) is set to expand at a 5.33% CAGR. Oncology and orthopedics centers in Milan, Bologna, and L’Aquila now ablate bone metastases, osteoid osteoma, and uterine fibroids with MR-guided systems, supporting incremental procedure volumes. Broader SSN reimbursement could unlock applications for prostate and pancreatic cancers.

Doppler and conventional 2D remain essential for vascular mapping and abdominal exams, ensuring a diversified modality mix. Vendors court HIFU prospects by offering pay-per-treatment finance packages to offset capital outlays of EUR 1-2 million. Consequently, the Italy ultrasound devices market size for HIFU, while still small, exhibits outsized momentum relative to legacy modalities.

By Portability: Handheld Devices Disrupt Cart-Based Workflows

Stationary consoles accounted for 62.47% of the Italian ultrasound device market share in 2025, yet handheld units are expanding at a 7.18% CAGR on the back of point-of-care adoption. Emergency departments in Turin cut CT utilization by 18% after equipping triage nurses with smartphone-connected probes. Home-health teams leverage the lightweight form factor for bladder, lung, and lower-limb checks during domiciliary visits.

Despite resolution trade-offs, AI-driven gain optimization and automated measurements narrow the quality gap. Hospitals increasingly deploy mixed fleets of radiology consoles, portable OR carts, and handheld devices for bedside care, securing interoperability through vendor-neutral DICOM and cloud gateways. This tiered approach anchors sustainable growth across all portability classes in the Italy ultrasound devices market.

By End User: Home-Health Momentum Builds on Telemedicine Reimbursement

Hospitals accounted for 54.64% of 2025 revenue, but home healthcare is the fastest-growing sector at a 6.68% CAGR, backed by tele-ultrasound tariffs and Casa di Comunità funding. Visiting nurses and even patients themselves capture diagnostic clips with handheld probes and forward them to hub-hospital radiologists. Diagnostic centers protect share through extended hours and rapid turnaround, while ambulatory surgical centers deploy compact scanners for intraoperative guidance.

Equipment criteria vary sharply: hospitals seek versatility and durability, diagnostic centers focus on throughput, ambulatory sites prioritize footprint, and home-health operators demand long battery life and wireless upload. Vendors with modular product lines and unified software ecosystems address all four settings, widening their addressable base within the Italy ultrasound devices market.

Geography Analysis

Regional disparities define adoption patterns. Northern regions Lombardy, Emilia-Romagna, Veneto, and Lazio enjoy per-capita spending of EUR 2,300 and host 43 tertiary hubs equipped with premium 3D/4D consoles, fusion imaging, and AI analytics. Waiting times hover around 15 days. Southern regions allocate just EUR 1,800 per capita; spoke hospitals rely on portable systems, and queues exceed 60 days, steering patients to private centers or self-pay diagnostics. PNRR procurement of 928 mid-tier consoles many earmarked for the south narrows the gap but does not erase it.

Central regions sit between the two extremes, leveraging proximity to supply chains while facing fewer fiscal constraints than the south. Tuscany’s tele-orthopedic program exemplifies innovation diffusion: wearable tattoos ensure scan reproducibility, informing nationwide rollouts at Casa di Comunità. Insular regions contend with logistics: service crews must fly to Sardinia or ferry to Sicily, lengthening repair cycles and pushing facilities toward handheld devices with lower downtime risk.

Urban-rural splits compound inequity. Metropolitan hospitals in Milan and Rome secure vendor discounts through volume commitments, whereas rural hospitals in Abruzzo or Basilicata negotiate from weaker positions.

Competitive Landscape

The Italy ultrasound devices market is moderately concentrated. GE HealthCare, Koninklijke Philips, and Siemens Healthineers anchor high-end segments, while Genoa-based Esaote leverages domestic presence in musculoskeletal imaging. Asian makers Mindray, Samsung Medison, and Canon Medical gain traction in cost-sensitive tenders, particularly in the south, by pairing five-year warranties with Naples and Palermo service hubs. Disruptors Butterfly Network and Clarius Mobile Health reshape the handheld tier by pricing probes at EUR 5,000-10,000 and bundling cloud subscriptions.

Competition unfolds across three arenas: (1) premium consoles featuring AI tools like GE’s SonoLyst and Philips’s Auto Strain; (2) mid-tier carts aligned with PNRR’s EUR 82,000 reference price; and (3) handheld devices for decentralized care. MDR certification backlog raises entry barriers but also slows incumbent product refreshes, opening windows for agile startups that secure early compliance. Strategic responses include Siemens’s hybrid-OR bundles, Esaote’s fusion-ready MyLab E80, and GE’s budget-tier Versana Premier, each calibrated to distinct budget bands.

Italy Ultrasound Devices Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: The Catholic University of Rome announced the development of AI-based ultrasound software for childbirth decisions, achieving 94.5% accuracy in determining delivery methods and expected availability in delivery rooms by 2028, representing a significant advancement in obstetric care technology

- January 2024: Esaote, one of the leading Italian companies in medical imaging participated in Arab Health and launched two new ultrasound systems namely MyLabA50 and MyLab A7.

Italy Ultrasound Devices Market Report Scope

A diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They are being utilized for the assessment of various conditions in the kidney, liver, and other abdominal conditions. They are also widely used to treat chronic illnesses, which include ailments including diabetes, asthma, cancer, and heart disease. As a result, these devices have a variety of uses in the medical area, including both diagnostic imaging and therapeutic modality.

Italy's ultrasound devices market is segmented by application, technology and Type. By application, the market is segmented into anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, critical care, and other applications. By technology, market is segmented into 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging, and high-intensity focused ultrasound. By type, market is segmented into stationary ultrasound and portable ultrasound.

The report offers the value (in USD) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Centers |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| Other End Users |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Centers | |

| Ambulatory Surgical Centers | |

| Home Healthcare Settings | |

| Other End Users |

Key Questions Answered in the Report

How fast is demand growing for critical-care ultrasound in Italy?

Critical-care applications are projected to grow at a 5.83% CAGR to 2031, the fastest pace among all clinical uses of ultrasound.

Which portability class is expanding most rapidly?

Handheld and pocket scanners are forecast to post a 7.18% CAGR as emergency, primary care, and home health teams adopt point-of-care workflows.

What share of 2025 revenue did 3D/4D imaging hold?

3D and 4D technology captured 41.87% of 2025 revenue, driven by obstetrics and advanced cardiac imaging protocols.

How will PNRR funding influence regional adoption?

PNRR-financed purchases of 928 mid-tier consoles and funds for Casa di Comunità hubs, accelerating uptake in underserved southern regions.

Why are vendors emphasizing AI features?

AI modules shorten scan times, standardize measurements and reduce operator dependency, allowing hospitals to justify premium console prices under tight staffing.

What is the outlook for home-health ultrasound?

Supported by tele-ultrasound reimbursement, the home-health segment is projected to expand at 6.68% CAGR, outpacing hospital growth through 2031.

Page last updated on: