Italy Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

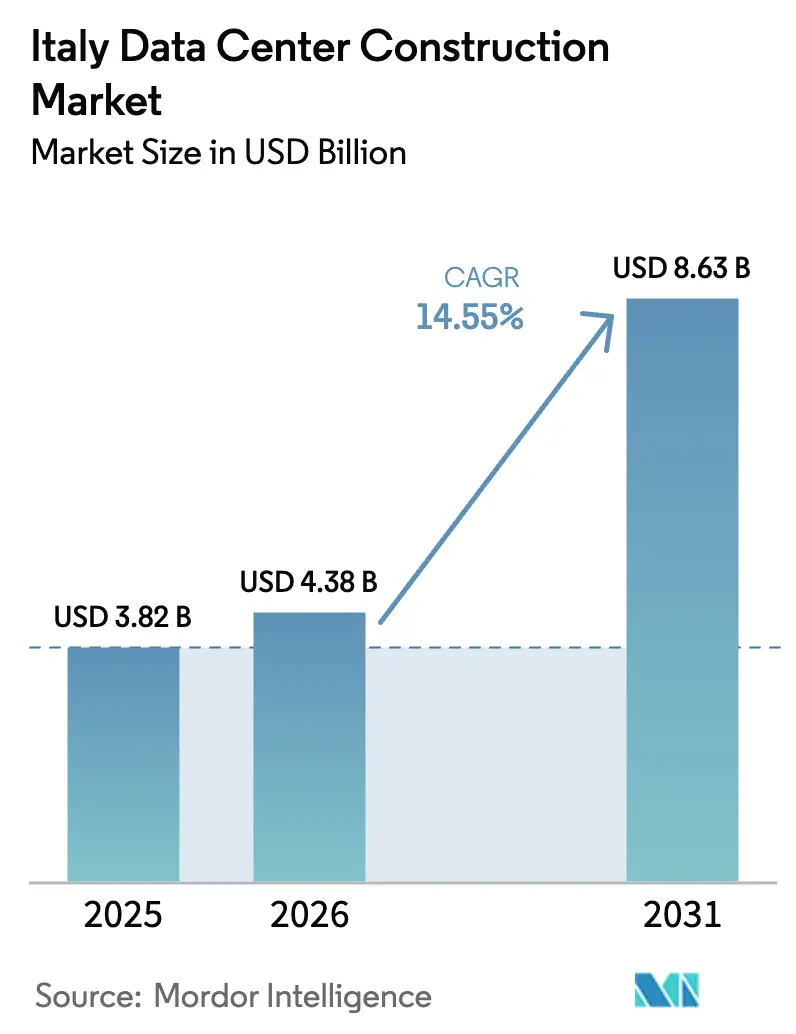

| Base Year Market Size (2025) | USD 3.82 Billion |

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 8.63 Billion |

| Growth Rate (2026 - 2031) | 14.55% CAGR |

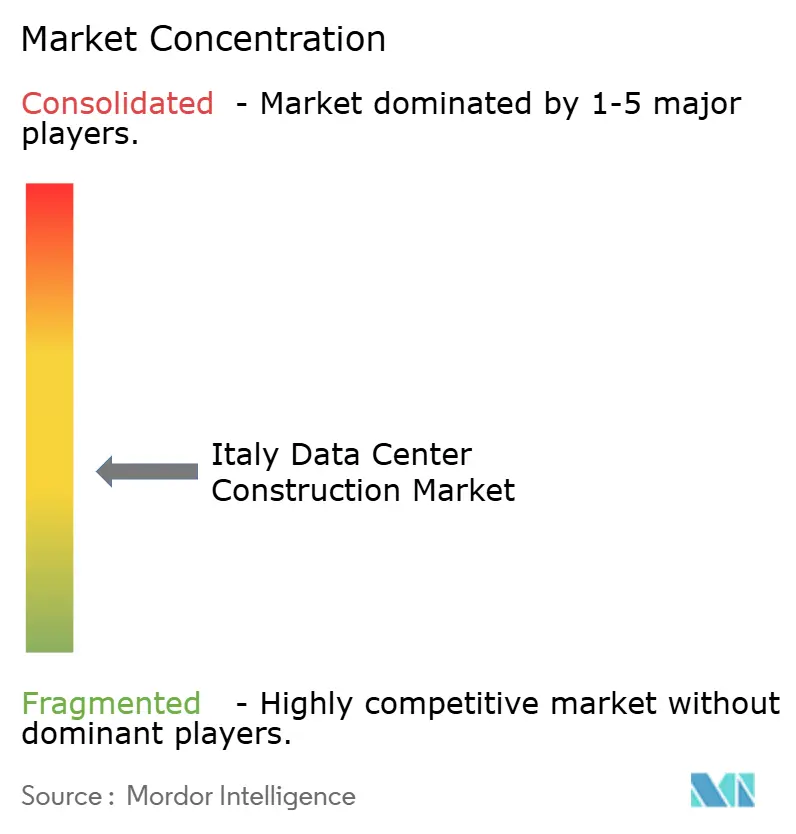

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Data Center Construction Market Analysis by Mordor Intelligence

Italy data center construction market size in 2026 is estimated at USD 4.38 billion, growing from 2025 value of USD 3.82 billion with 2031 projections showing USD 8.63 billion, growing at 14.55% CAGR over 2026-2031. Steady capital inflows from hyperscalers, strong government backing, and Italy’s geographic role as a Mediterranean connectivity node form the foundation of this rapid scale-up. Power connection requests have already eclipsed installed grid capacity, yet sustained investment plans by Terna and a wave of new submarine cable landings keep investor sentiment positive. Microsoft, AWS, Google Cloud, and Oracle continue to anchor fresh builds, while domestic operators such as TIM and Aruba blend local expertise with global best practice to accelerate delivery. Rising sustainability mandates, 5G rollout, and the build-to-lease approach embraced by hyperscalers collectively shape the next phase of the Italy data center construction market.

Key Report Takeaways

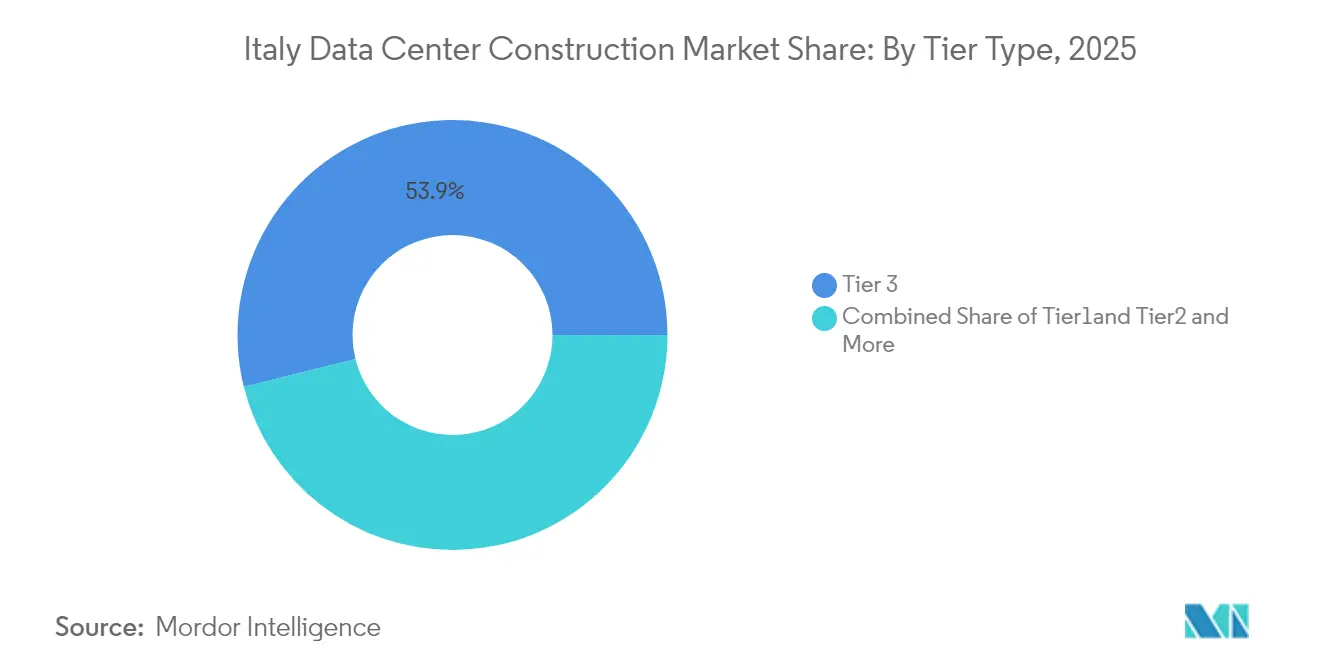

- By tier type, Tier 3 led with a 53.86% share of the Italy data center construction market in 2025, while Tier 4 facilities are expanding at a 17.48% CAGR through 2031.

- By data center type, colocation services held a 55.94% share of the Italy data center construction market size in 2025; self-build hyperscaler sites are growing 18.98% annually to 2031.

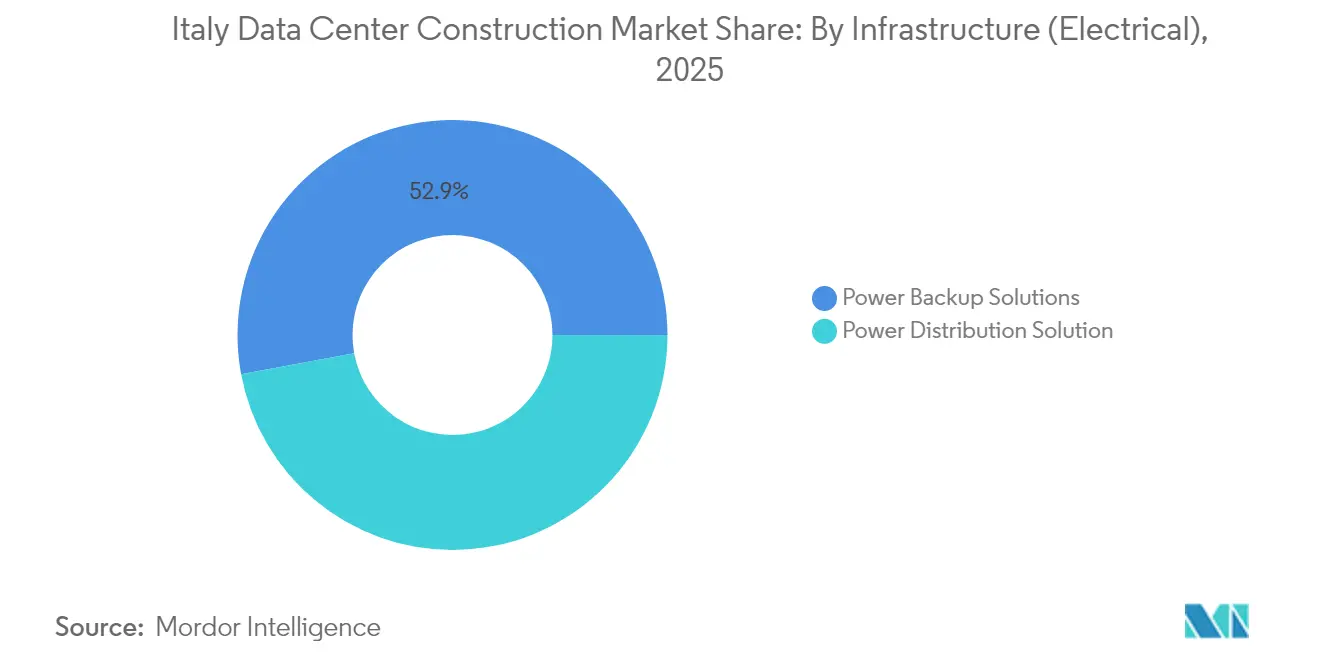

- By electrical infrastructure, power backup solutions accounted for 52.93% of the Italy data center construction market size in 2025, whereas power distribution solutions post the fastest 18.56% CAGR.

- By mechanical infrastructure, cooling systems captured 47.88% share of the Italy data center construction market size in 2025 and remain essential as servers and storage rise at a 16.13% CAGR.

- Regionally, Northern Italy commanded 61.58% of 2025 revenue; Sicily is forecast to post the highest 20.87% CAGR on the back of fresh cable landings.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G rollout accelerating edge and core builds | +2.8% | National, focused on Milan, Turin, Rome | Medium term (2-4 years) |

| Surging cloud and hyperscale demand | +3.2% | Northern and Central regions | Short term (≤ 2 years) |

| PNRR digital grants | +2.1% | Nationwide, underserved areas prioritized | Medium term (2-4 years) |

| Sustainability mandates and green energy sourcing | +1.9% | EU-wide, Italy leading Mediterranean uptake | Long term (≥ 4 years) |

| New subsea cable landings | +1.7% | Sicily, Genoa, Mediterranean coast | Long term (≥ 4 years) |

| Build-to-lease model | +1.5% | Northern Italy, moving southward | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G rollout accelerating edge and core builds

WindTre’s EUR 485 million purchase of OpNet’s standalone 5G assets unlocked 3,000 base stations serving 75% of Italy’s population, spurring immediate demand for micro-edge sites that reinforce traditional cores. TIM’s 2024-2026 plan maps 16 new data centers that dovetail with this national 5G push,[1]Telecom Italia, “TIM 2024-2026 Plan Accelerates 5G and Cloud,” telecomitalia.com and Phoenix Tower International’s 1,900-site program further underlines the need for low-latency capacity. Because 5G splits workloads between radio, edge, and core, facility planners now prioritize smaller footprints near population clusters, advanced liquid-assisted cooling, and resilient distribution paths to meet stringent latency targets.

Surging cloud and hyperscale demand

Google Cloud, Microsoft, AWS, and Oracle continue to earmark multi-billion-euro budgets for Italian expansion, often in partnership with TIM or other local carriers. The Milan-Turin corridor has become the epicenter, yet secondary cities are quickly absorbing projects as prime sites tighten. Hyperscale investment not only enlarges the Italy data center construction market but also boosts local employment, with University of Turin research projecting 65,000 jobs by 2025 from the Google ecosystem alone.[2]Google Cloud, “Introducing Google Cloud Regions in Milan and Turin,” cloud.google.com Partnerships shorten permitting cycles, ensure compliance with digital-sovereignty rules, and allow carriers to cross-sell edge services.

Government “PNRR” digital grants

Italy’s PNRR allocates EUR 32.5 billion to digital objectives,[3]European Commission, “Recovery and Resilience Facility: Italy Country Factsheet,” europa.eu and cloud-first directives in public administration are creating demand visibility that de-risks private capital. Piano Transizione 5.0 adds EUR 12.7 billion of tax credits to companies that lower energy use by at least 3%, directly supporting efficient builds. Municipal funding envelopes earmark EUR 500 million for cloud enablement in underserved areas, nudging operators to distribute capacity beyond the Milan-Turin core and thereby broadening the Italy data center construction market.

Rising sustainability mandates and green energy sourcing

From September 2024, EU rules require operators to disclose energy KPIs, driving efficiency upgrades and renewable sourcing. Italy’s Energy Decree trims permitting timelines for solar and wind projects that feed data centers, while leaders such as Aruba power entire campuses with hydro and PV. Retelit’s Avalon 3 recovers waste heat for district networks, illustrating how environmental rules spur technical innovation and adjacent revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power scarcity and volatile prices | -3.1% | Nation-wide, severe in industrial north | Short term (≤ 2 years) |

| Specialised labour shortage | -2.2% | Major metropolitan areas | Medium term (2-4 years) |

| Seismic-zone engineering costs | -1.8% | Central and Southern seismic belts | Long term (≥ 4 years) |

| Limited reclaimed water for cooling | -1.4% | Arid industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-power scarcity and volatile energy prices

Connection requests topped 42 GW in March 2025—almost triple available headroom—forcing operators to queue as long as three years for new feeds. Terna’s EUR 23 billion grid plan will ease congestion but not before late decade. Meanwhile, some hyperscalers buy retired Enel power assets to avoid delays. Rising spot prices complicate budgeting, and construction cost indices have risen 20% since the pandemic, squeezing margins for developers across the Italy data center construction market.

Shortage of specialised data-center construction labour

Italy shares a global shortfall of skilled technicians who understand high-density power, advanced cooling, and seismic design. Temporary booms from the Superbonus scheme distorted the labour pool, leaving fewer qualified crews for Tier 4 builds. Training pipelines exist but need two-plus years to flow, placing upward pressure on delivery timelines and wages and restraining the overall Italy data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Drives Premium Reliability

Tier 3 facilities controlled 53.86% of the Italy data center construction market share in 2025 as enterprises sought balanced uptime and cost. Nevertheless Tier 4 sites, required by finance, government, and AI workloads, expand 17.48% each year to 2031. This segment commands higher CAPEX due to dual power paths, concurrent maintainability, and seismic hardening. Vertiv’s CoolLoop Trim Cooler, compliant with impending EU F-GAS rules, cuts cooling energy 70%, making it attractive to Tier 4 builders seeking compliance and savings. Aruba’s IT4 in Rome exemplifies this trend with five duplicate buildings, 30 MW IT load, and renewable power.

Growth momentum also ripples down to Tier 1 and Tier 2 for edge or cost-sensitive projects. Yet as business continuity rises on boardroom agendas, these lower tiers are yielding share to fault-tolerant designs. The Italy data center construction market therefore shows a clear shift toward premium reliability, with operators positioning modular Tier 4 capacity along seismic lines to minimize disruption risk.

By Data Center Type: Hyperscalers Reshape Construction Patterns

Despite colocation’s 55.94% 2025 base, self-build hyperscaler projects rise 18.98% per year. Microsoft’s EUR 4.3 billion investment in Northern Italy, paired with AI-ready architecture, typifies this pivot. Google Cloud blends self-build and outsource by leasing space from TIM in Milan and Turin, illustrating hybrid forms that optimize speed and compliance. This wave enlarges the Italy data center construction market size for hyperscale to an estimated USD 2.39 billion by 2031, equal to 27.65% of total value.

Edge and enterprise builds grow moderately but still anchor regional diversification. The build-to-lease model lowers capital-heavy lifting for hyperscalers: Oracle’s Turin region runs inside a TIM campus, meeting uptime and sovereignty goals without direct land ownership. Pension and infrastructure funds are eager landlords, turning predictable 20-year hyperscale leases into bond-like returns, and thereby injecting new capital into the Italy data center construction industry.

By Infrastructure, Electrical Type: Power Distribution Innovation Accelerates

Power backup systems own 52.93% of spending today, a testament to uninterruptible uptime needs. Still, power distribution gear posts the quickest 18.56% CAGR as racks climb from 5-10 kW to 40-50 kW. The Italy data center construction market size for distribution is set to double by 2031, propelled by AI clusters like iGenius’s southern campus featuring 80 Nvidia servers. Terna’s smart-grid upgrades dedicate EUR 3.4 billion to data-center-oriented substations, enabling real-time load management.

Advanced busways, solid-state transformers, and on-site battery energy storage now appear in RFPs as standard. Operators are also pre-wiring for future fuel-cell integration. These investments streamline commissioning timelines while satisfying KPIs set by the EU’s forthcoming sustainability scorecard.

By Mechanical Infrastructure: Cooling Systems Face AI Challenge

Cooling ruled 47.88% of spend in 2025, but servers and storage—climbing 16.13% annually—now dictate mechanical design. Liquid immersion, rear-door heat exchangers, and heat-recovery loops shift facility layouts. Leonardo’s DaTEG system delivers 30% better chip performance at lower wattage, proving advanced thermal management’s ROI. The Italy data center construction market must also adapt cabinet structures for heavier liquid lines and denser gear while ensuring seismic integrity.

Operators capture new revenue by selling recovered heat to district utilities, as Retelit’s Avalon 3 does for 1,250 homes. Such innovations not only align with EU climate targets but also mitigate grid strain by offsetting regional heating demand.

Geography Analysis

Northern Italy remains the epicenter, with Lombardy and Piedmont accounting for roughly 61.58% of 2025 spend thanks to dense fibre routes, renewables access, and a seasoned supply chain. Milan hosts major campuses from Aruba, Data4, Microsoft, and AWS, while Turin gained momentum after Oracle and Google Cloud established sovereign cloud zones. This cluster effect accelerates lead-times but risks grid-capacity saturation, prompting operators to scout Central and Southern parcels.

Sicily’s Palermo, bolstered by Sparkle’s Sicily Hub and the 240 Tbps BlueMed cable, positions the island as a tri-continent gateway. Genoa adds a second landing point that slashes latency for North Africa and Middle East traffic, enlarging the Italy data center construction market potential along the Ligurian coast. Bologna’s “Data Valley,” centered on the Leonardo supercomputer, attracts HPC-heavy tenants and research consortia, diversifying demand beyond commercial cloud.

Southern regions leverage abundant solar and wind, lower land costs, and PNRR incentives. iGenius’s USD 1 billion project illustrates this pivot, integrating renewable power and AI supercomputing. Yet seismic engineering inflates CAPEX, triggering use of the Sismabonus tax break to recover up to 50% of reinforcement spend. Despite higher upfront outlays, operators value location diversity for disaster recovery and carbon-free energy procurement, broadening the Italy data center construction market footprint.

Competitive Landscape

Competition balances between legacy telcos (TIM, WindTre), pure-play providers (Aruba, Retelit), and hyperscalers with voracious capacity needs. TIM commands the largest domestic footprint through 16 data centers and cloud pacts with Google and Oracle. Aruba differentiates via 100% renewable portfolios, Rating 4 certifications, and heat-recovery pilots, drawing sustainability-focused tenants. Microsoft, AWS, and Google underpin the bulk of greenfield work, often through land-lease or powered-shell partnerships that de-risk local execution.

Private equity and infra funds are amplifying firepower: Bain Capital’s 80% stake in AQ Compute and InfraVia’s 50% purchase of Iliad’s OpCore unlock billions for expansion. Strategic moves include Phoenix Tower’s edge-ready mast acquisition, Vantage Data Centers’ EUR 1.4 billion EMEA allocation, and Terna’s escalated capex to safeguard grid resilience. The Italy data center construction market thus sees rising M&A pace, vendor consolidation, and heavier emphasis on ESG compliance as a competitive differentiator.

Italy Data Center Construction Industry Leaders

AECOM

Arup Group Limited

DPR Construction, Inc.

Schneider Electric SE

Fortis Construction, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: iGenius confirmed its USD 1 billion southern Italy campus will go live by summer 2025 with 80 Nvidia servers running on renewables.

- February 2025: Stantec won the EUR 3.2 billion design contract for Silicon Box’s semiconductor test facility in Northern Italy, underpinning AI and data center ecosystems.

- March 2025: Terna lifted Q1 2025 grid capex by 16.4% to EUR 562.1 million, earmarking funds for high-capacity data center interconnects.

- May 2025: CyrusOne unveiled plans for a 54 MW Milan site powered entirely by renewables and closed-loop cooling.

- June 2025: Apto announced Italy’s largest campus in Lacchiarella near Milan, investing EUR 3 billion across 228,000 m².

- December 2024: InfraVia closed on 50% of Iliad’s OpCore platform, forming a pan-European hyperscale venture.

- October 2024: Bain Capital bought 80% of AQ Compute to finance sustainable colocation rollouts across Europe, with Italy high on the list.

- August 2024: Retelit launched Italy’s first data-center heat-recovery scheme at Avalon 3, heating 1,250 homes and cutting 3,300 tons of CO₂ annually.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the Italy data center construction market as the yearly capital expenditure devoted to designing, engineering, and erecting new or expanded carrier-neutral, enterprise, and hyperscale facilities within Italian borders. This spend covers electrical and mechanical packages, general construction, security, and integration tasks and is expressed in constant-2024 US dollars.

Scope exclusion: We exclude day-to-day operations, refresh-only IT hardware replacements, and lease-driven colocation revenues.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed design engineers, electrical OEMs, and facility operators spread across Lombardy, Emilia-Romagna, Lazio, and Sicily. These discussions validated per-megawatt build costs, probability-weighted project timelines, and the mix shift toward liquid cooling, filling key gaps left by open data.

Desk Research

We began by mapping permit activity and grid-tie applications filed with ARERA, cross-checking these with Eurostat's construction cost indices and Gestore Servizi Energetici's renewable capacity registry. To size regional pipelines, we tapped public releases by the Associazione Italiana Data Center, city planning portals for Milan and Rome, and ENEA's energy-efficiency bulletins, which clarify cooling technology adoption.

Company filings, environmental-impact assessments, and land-registry deeds were then mined to benchmark site footprints, while D&B Hoovers provided contractor revenue clues and Dow Jones Factiva supplied news on hyperscaler build contracts. The sources listed illustrate, not exhaust, the wider desk research pool consulted.

Market-Sizing & Forecasting

A top-down model converts announced IT-power additions into spend by applying city-specific $/MW build factors, which are then reconciled with bottom-up samples from supplier price lists and channel checks. Variables such as rack density migration, copper and aluminum price trends, PPA tariffs, land costs, 5G subscriber growth, and hyperscaler region launches feed the model. Multivariate regression links these drivers to annual CAPEX, while scenario analysis adjusts for grid-power availability shocks. Where supplier granularity is thin, we impute costs by analog facility benchmarks and flag the variance for review.

Data Validation & Update Cycle

Outputs undergo anomaly scans, senior-analyst review, and variance tests against independent indicators like crane-hour demand and imported HVAC shipments. Reports refresh each year, with interim updates triggered by material project announcements. Before release, an analyst re-runs the latest data pull so clients receive an up-to-date view.

Why Mordor's Italy Data Center Construction Baseline Figures Inspire Confidence

Published estimates often diverge because firms fold in different spending buckets, use varied build-cost assumptions, or refresh figures on uneven cadences.

Key gap drivers in this market include whether refurbishments are counted, how pipeline probabilities are treated, and the currency inflation factor chosen; this is where Mordor Intelligence insists on probability-weighted pipelines, constant-currency baselines, and an annual refresh, producing a steadier benchmark for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.82 B (2025) | Mordor Intelligence | - |

| USD 4.09 B (2024) | Regional Consultancy A | Mixes hardware OPEX and maintenance spend with new-build CAPEX |

| USD 3.13 B (2024) | Trade Journal B | Counts every announced project at full value without probability discounting |

| USD 4.00 B (2024) | Global Consultancy C | Inflates totals by converting euro contracts at spot rather than constant rates |

The comparison shows that when scope, probability weighting, and currency treatment are harmonized, gaps narrow considerably. This disciplined approach is why, according to Mordor Intelligence, our baseline remains the most transparent and repeatable yardstick for Italy's data center construction outlook.

Key Questions Answered in the Report

What is the current Italy Data Center Construction Market size?

The Italy Data Center Construction Market is projected to register a CAGR of 14.55% during the forecast period (2026-2031)

Who are the key players in Italy Data Center Construction Market?

AECOM, Arup Group Limited, Legrand, Daikin Applied and STULZ are the major companies operating in the Italy Data Center Construction Market.

What years does this Italy Data Center Construction Market cover?

The report covers the Italy Data Center Construction Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Italy Data Center Construction Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: