France Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

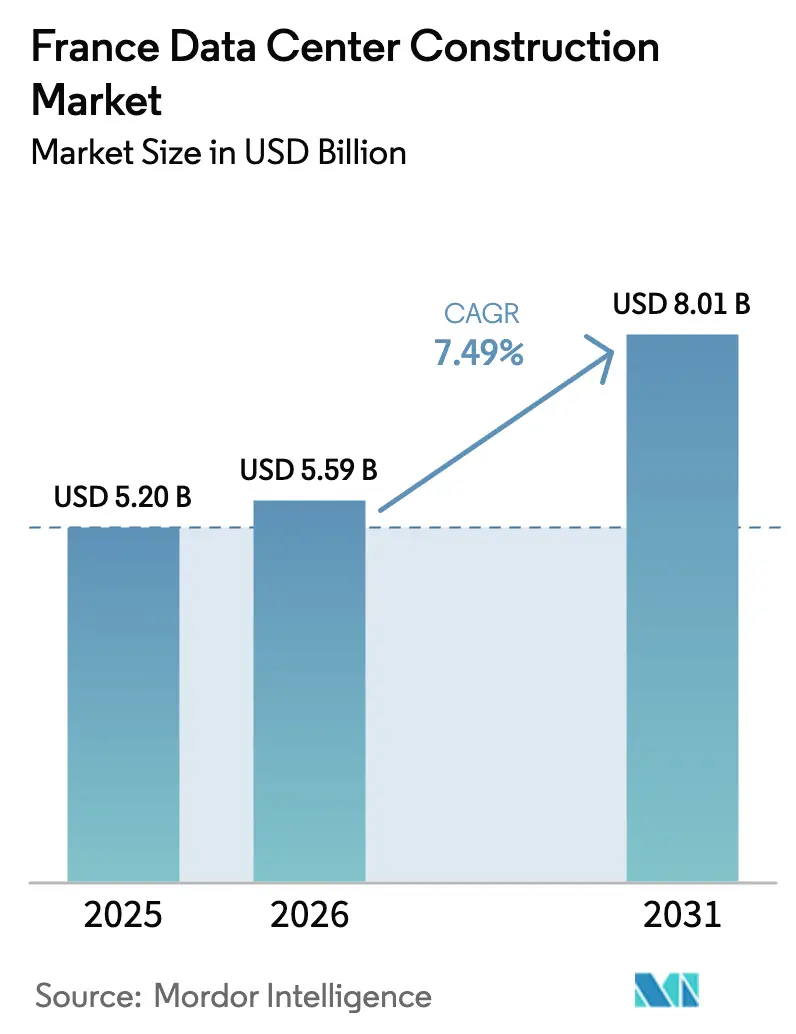

| Base Year Market Size (2025) | USD 5.20 Billion |

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 8.01 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Data Center Construction Market Analysis by Mordor Intelligence

The France data center construction market size is expected to grow from USD 5.20 billion in 2025 to USD 5.59 billion in 2026 and is forecast to reach USD 8.01 billion by 2031 at 7.49% CAGR over 2026-2031. Ready-to-use land parcels, an extensive nuclear-powered grid, and strategic submarine-cable links are accelerating project pipelines. Replacement demand is robust because as much as 80% of installed capacity cannot support high-density AI loads. Competitive intensity is increasing as domestic builders partner with international operators to combine local permitting expertise with global scale. Nevertheless, rising labor and material costs are trimming project margins and shifting activity toward secondary metros.

Key Report Takeaways

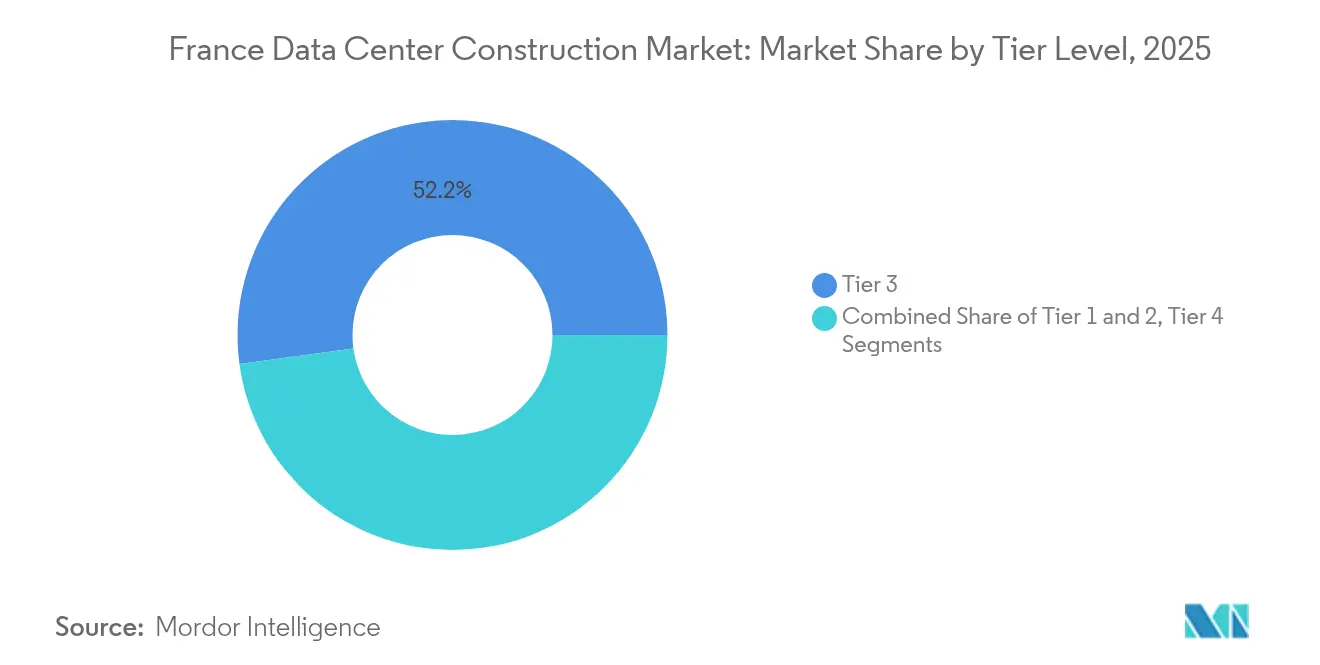

- By tier classification, Tier 3 facilities led with 52.15% of France data center construction market share in 2025, while Tier 4 is projected to post an 7.87% CAGR through 2031.

- By data-center type, the colocation category captured 56.60% revenue share in 2025; hyperscaler self-builds are set to expand at a 9.65% CAGR to 2031.

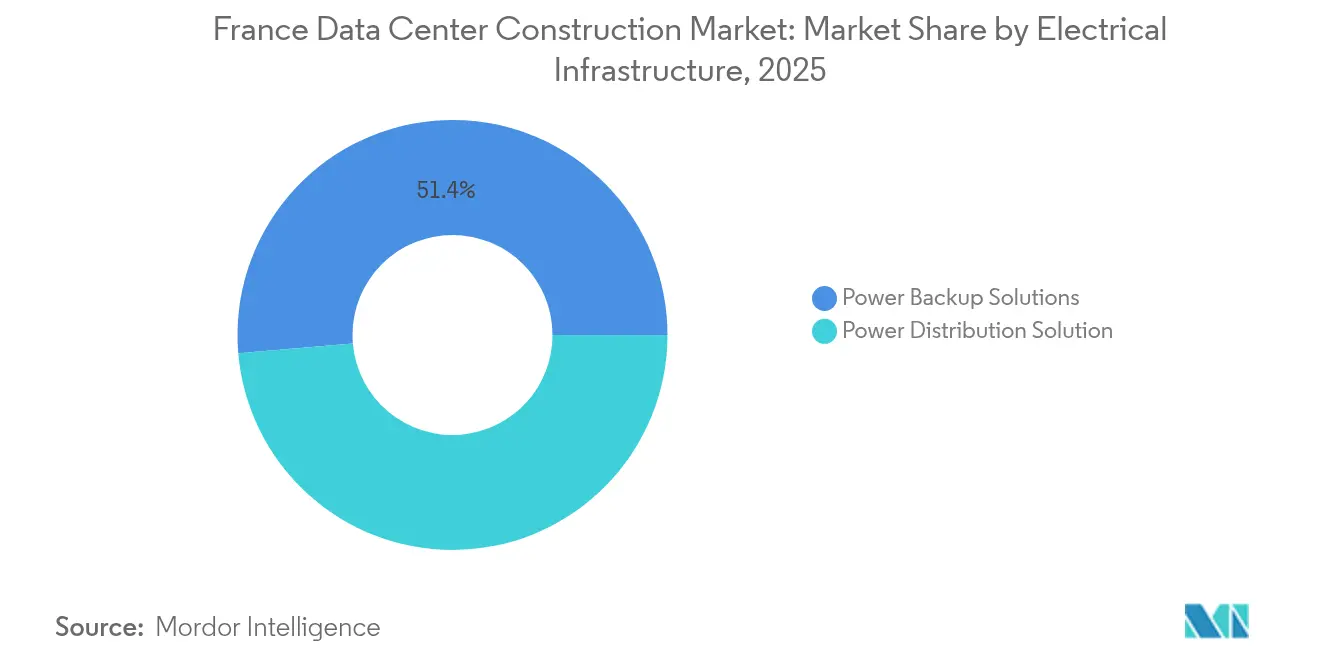

- By electrical infrastructure, power-backup systems accounted for a 51.35% share of the France data center construction market size in 2025, whereas power-distribution solutions are forecast to grow at a 8.92% CAGR.

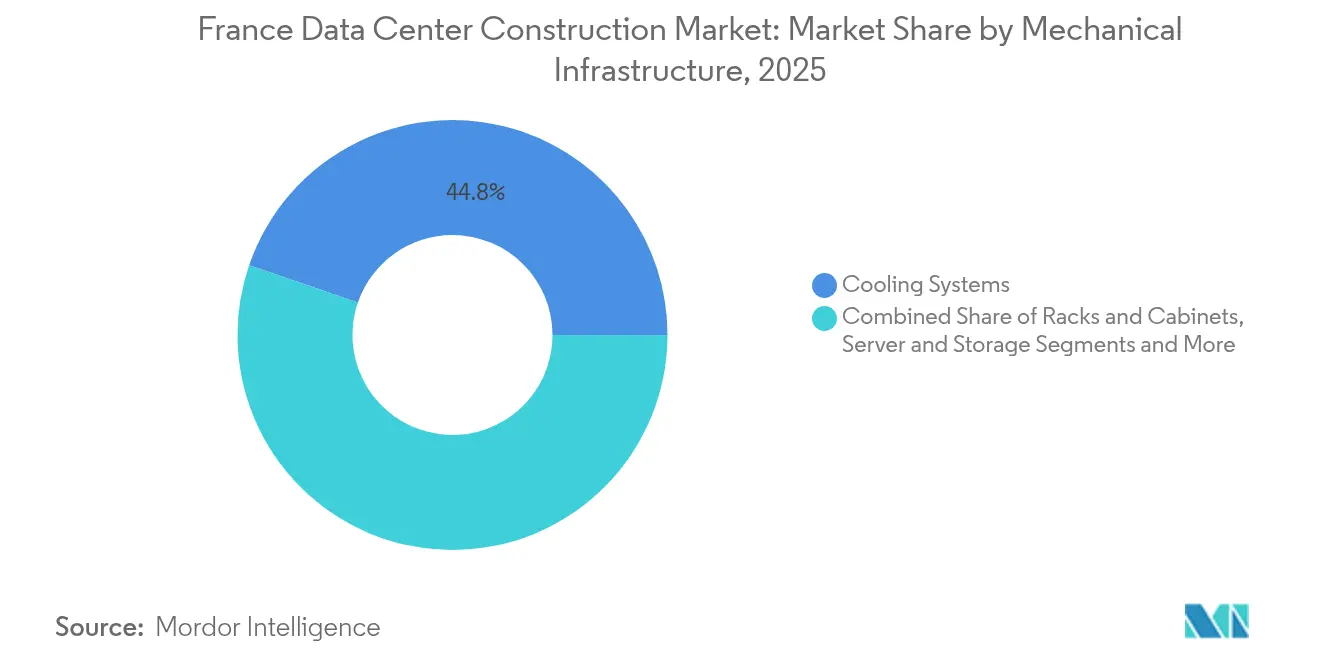

- By mechanical infrastructure, cooling systems dominated with a 44.75% share in 2025, while servers and storage are expected to advance at an 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation and managed-cloud demand | +1.2% | National, concentrated in Paris-Lyon-Marseille corridor | Medium term (2-4 years) |

| 5G roll-out and edge-computing densification | +0.8% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Government AI and digital-sovereignty investment surge | +1.5% | National, with focus on strategic sites | Long term (≥ 4 years) |

| Availability of low-carbon nuclear-backed electricity | +0.9% | National, particularly attractive for hyperscale facilities | Long term (≥ 4 years) |

| Fast-track "national-interest" permit regime | +0.6% | National, streamlining major projects | Medium term (2-4 years) |

| Edge data-center growth for AI/IoT low-latency workloads | +0.7% | Metropolitan areas, industrial zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Transformation and Managed-Cloud Demand

Enterprises are replacing on-premises hardware with hybrid-cloud architectures that need low-latency links to public-cloud regions and specialised colocation halls. Sector-specific compliance is reshaping specifications; healthcare operators seek ISO 13485 halls, while gaming and lottery operators commission multi-site audits before moving workloads. The managed-services layer compels builders to integrate staging space for edge appliances and AI inference clusters. Demand for sovereign-hosted environments is anchoring capacity inside national borders to meet European data-protection rules.

5G Roll-Out and Edge-Computing Densification

Widespread 5G coverage is pushing computing clusters closer to streets and factory floors. Municipal projects, such as the Istres private 5G rollout, embed micro-data centers into civic infrastructure to support real-time video analytics, creating opportunities for contractors versed in high-density electrical layouts that fit inside refurbished utility rooms. Manufacturers deploying 5G on production lines are requesting ruggedised edge enclosures paired with liquid cooling that withstand industrial heat and vibration.[1]Ericsson, "Istres launches Private 5G Network for enhanced urban connectivity,"ericsson.com

Government AI and Digital-Sovereignty Investment Surge

Paris has packaged land banks, pre-approved power licences, and accelerated permits into a single policy toolkit. The offer has lured cross-border capital, exemplified by a EUR 30–50 billion (USD 34.54-57.57 billion) UAE partnership to build a 1-gigawatt AI campus and by Brookfield’s EUR 20 billion(USD 23.03 billion) allocation that will triple Data4’s national footprint. Public-sector orders are steady; the City of Paris is funding its own cloud facility to safeguard confidential datasets, while sovereign-cloud ventures such as Orange-Capgemini Bleu mandate hardened halls with intrusion-detection zoning.[2]Jean-Paul Legendre, “France Readies 35 Plots for Data Center Megaprojects,” Bat info, batinfo.com

Availability of Low-Carbon Nuclear-Backed Electricity

Roughly 70% of French electricity is nuclear-generated, giving operators predictable energy prices and a low-carbon marketing edge. EDF has earmarked four grid-connected plots for hyperscale parks and offers direct-to-reactor power agreements that shorten energisation schedules. Fluidstack’s planned EUR 10 billion (USD 11.51 billion) AI supercomputer will tap this baseload to run power-hungry model-training clusters around the clock without renewable-intermittency constraints.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Paris-region land and build-cost inflation | -0.8% | Paris metropolitan area, spillover to surrounding regions | Short term (≤ 2 years) |

| Stringent 2025 energy-efficiency disclosure law (ICPE) | -0.4% | National, affecting all facilities above 500kW | Medium term (2-4 years) |

| Localised grid-capacity bottlenecks in FLAP sub-markets | -0.5% | Paris, Lyon, Amsterdam, Frankfurt connectivity corridors | Medium term (2-4 years) |

| Tightening water-usage regulations for cooling systems | -0.3% | Water-stressed regions, particularly southern France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Paris-Region Land and Build-Cost Inflation

Limited industrial plots inside the A86 ring road have pushed average site prices beyond EUR 300(USD 345.51) per square meter, while steel and switchgear costs continue to rise at 5–7% annually. Hourly labour rates advanced from EUR 112.80 (USD 129.88) to EUR 121.02 (USD 139.34) during 2025, squeezing contractor margins. Developers are diverting pipelines to Lyon, Bordeaux and Marseille, where land is cheaper and municipal incentives are available. To offset cost pressures, builders are adopting factory-prefabricated modules that cut on-site labour hours and reduce exposure to price-volatile commodities.

Stringent 2025 Energy-Efficiency Disclosure Law (ICPE)

From 2025, facilities above 500 kW must report actual PUE, water consumption and recovery of waste heat. Operators are incorporating indirect-evaporative or liquid cooling to meet mandated thresholds and future-proof designs. Compliance adds metering, telemetry and data-visualisation systems during construction, raising upfront capex but lowering operating expenses. Projects unable to implement heat-reuse loops risk permitting delays, driving investment toward campuses with adjacent district-heating schemes.[3]Kevin Dalton, “Interxion Implements River Cooling at Marseille Site,” interxion.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

Tier 3 halls retained 52.15% of France data center construction market share in 2025 because most enterprise applications require high but not fault-tolerant uptime. The France data center construction market size for Tier 3 builds is forecast to continue expanding steadily yet below the overall industry CAGR. Tier 4, by contrast, is projected to grow 7.87% annually through 2031 as AI model training, fintech clearing and critical national infrastructure workloads need 99.995% availability.

Tier 4 projects entail 2N power trains, dual fibre paths and concurrent maintainability across mechanical subsystems, prompting larger electrical rooms and more sophisticated building-management software. The Thésée DataCenter campus, recognised as the nation’s first Uptime Tier IV colocation site, integrates AI-based cooling optimisation that trims energy consumption without compromising redundancy. Suppliers are therefore seeing heightened demand for AI-driven environmental controls, arc-flash-resistant switchgear and predictive-maintenance sensors that feed reliability dashboards.

By Data Center Type: Hyperscaler Self-Build Accelerates Market Transformation

Colocation operators commanded 56.60% of France data center construction market share in 2025, since enterprises prefer an opex-based capacity that can be contracted flexibly. Self-built hyperscaler halls, however, will record a 9.65% CAGR to 2031 as public-cloud providers seek cost control and guaranteed rack availability.

Hyperscaler campuses employ template-based designs with 54–60 MW blocks that replicate across regions, letting constructors gain repeatability benefits on materials and timelines. Microsoft’s EUR 4 billion (USD 4.61 billion) pledge is channelled into such cookie-cutter shells that accelerate commissioning. Enterprise and edge projects remain relevant where data-sovereignty rules or millisecond latency targets override economies of scale, prompting construction of micro-facilities inside factories, hospitals, and smart-city districts.

By Electrical Infrastructure: Power Distribution Innovation Leads Growth

Power-backup systems, including static UPS and diesel generators, held 51.35% of segment revenue in 2025 because uptime contracts still stipulate no-break transfer. Power-distribution units and busways are forecast to expand 8.92% annually, reflecting the shift to rack densities exceeding 40 kW for AI accelerators. The France data center construction market size allocated to advanced distribution gear will approach USD 1.63 billion in 2031.

Next-generation switchboards embed real-time analytics that balance phase loads and predict breaker wear. Socomec’s sensor-rich UPS topology supports edge sites by combining lithium-ion batteries with remote-management APIs, reducing truck-roll visits. Builders increasingly integrate grid-interactive battery energy-storage systems that provide both backup and frequency-regulation revenues, helping owners defray capex while meeting sustainability reporting obligations.

By Mechanical Infrastructure: Servers Drive Density Revolution

Cooling systems remained the largest mechanical slice with 44.75% share in 2025 because every new watt of compute demands roughly equal thermal removal. Servers and storage are poised for the fastest 8.25% CAGR as AI nodes drive exponential growth in GPU trays and NVMe arrays. High-density racks can exceed 100 kW, making direct-to-chip liquid cooling mainstream.

Immersion cooling loops deliver up to 20% longer hardware life and 39% carbon-emission cuts versus raised-floor air, attracting clients with net-zero commitments. 2CRSi’s USD 610 million hardware contract illustrates how server vendors package bespoke chassis, cold-plates and monitoring firmware as a single deal, compelling constructors to coordinate tightly with OEMs during design. Mechanical rooms likewise evolve, housing fluid loop pumps, heat exchangers and redundant dry coolers sized for hotter summer peaks.

Geography Analysis

Paris remains the core location for the France data center construction market because it hosts the bulk of financial trading, government clouds, and internet exchanges. Digital Realty operates 13 interconnected halls offering 932,500 ft² and dark-fibre links that guarantee sub-millisecond latency to La Défense financial district. Land scarcity and tightening acoustic regulations, however, are pushing expansions outward along express rail corridors.

Marseille is emerging as Europe’s southern gateway thanks to 14 submarine-cable terminations delivering 660 Tbps of capacity. Digital Realty’s recent EUR 280 million (USD 322.38 million) MRS5 build adds 22 MW on reclaimed industrial land, while Interxion converted a WWII submarine dock into a chilled-water-cooled facility that funnels waste heat into a district-heating grid.

Lyon, Bordeaux, and Strasbourg form a second-ring constellation that balances cost, power, and seismic resilience. Lyon leverages its position at the confluence of national fibre backbones and hosts SFR’s carrier-neutral Netcenter with Tier III certification. Bordeaux has welcomed Equinix’s BX1, signalling hyperscaler interest in the Atlantic coast. Rural municipalities are also courting projects; Sisteron’s planned green data center will recycle mountain-water cooling and infuse jobs into Provence. This geographic dispersion diversifies risk for clients and cushions the France data center construction market against localised policy changes.

Competitive Landscape

Domestic engineering conglomerates such as Bouygues Energies and Services, Eiffage Énergie Systèmes, and Vinci Energies capitalise on long-standing relationships with French utilities and regulators. Bouygues recently delivered a 28 MW UK facility that demonstrated agile phased hand-overs, while Eiffage modernised Telehouse Paris hubs without downtime, showcasing retrofit skill. These credentials help local firms secure state-sponsored and enterprise contracts that emphasise compliance documentation and union labour agreements.

International operators introduce capital depth and global best practice to the France data center construction market. Digital Realty and Equinix pursue campus-based expansion that pre-positions substations and liquid-cooling loops for AI tenants. They often employ design-build subsidiaries, tightening feedback loops between operations and construction. Data4, majority-owned by Brookfield, is scaling modular 6 MW blocks across its campuses, ordering identical electrical rooms to shave procurement lead times.

France Data Center Construction Industry Leaders

-

Bouygues Construction

-

Eiffage

-

Vinci Energies

-

Equans (formerly Engie Solutions)

-

CAP INGELEC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: UAE and France announced a EUR 30–50 billion (USD 34.54-57.57 billion) joint plan to build a 1 GW AI data-center campus.

- February 2024: Brookfield Asset Management committed EUR 20 billion (USD 23.03 billion) to French AI infrastructure, allocating EUR 15 billion (USD 17.27 billion) to Data4 expansions.

- February 2025: Fluidstack signed a EUR 10 billion (USD 11.51 billion) memorandum with the French government to erect a decarbonised AI supercomputer site targeting 1 GW by 2026.

- February 2025: The government published a list of 35 shovel-ready data-center plots with planned high-capacity grid links.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every euro spent within France on site preparation, shell erection, electrical and mechanical fit-outs, fire and security systems, and commissioning services for brand-new colocation, hyperscale, enterprise, and edge facilities. Expenses linked to IT hardware refresh, facilities management, or renovation of operating halls sit outside this construction pool, letting buyers compare clean capital-spend numbers across years.

Scope Exclusions: Operating expenditure, IT equipment purchases, and minor retrofit works are not modeled.

Segmentation Overview

-

By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

-

By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

-

By Infrastructure

-

By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

-

By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service (Design and Consulting, Integration, Support and Maintenance)

-

By Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with contractors, design engineers, utility planners, and colocation procurement leads across Île-de-France, Provence-Alpes-Côte d'Azur, and Grand Est helped us validate average build times, turnkey price bands, and power-density shifts, while a short survey of hyperscale real-estate teams clarified likely phasing for campuses announced after July 2025.

Desk Research

Mordor analysts pulled project pipelines from building permits published by data.gouv.fr, cross-checked power-access terms in RTE's grid-connection registry, and mapped submarine fiber landings using ARCEP's open-data portal. We then layered in construction cost indices from INSEE, trade insights from the European Data Centre Association, and public tender notices captured in Dow Jones Factiva and Tenders Info. D&B Hoovers supplied contractor revenue splits that anchored company-level roll-ups. The sources named here illustrate, not exhaust, the wider pool we tapped during desk work.

Market-Sizing & Forecasting

We began with a top-down spend reconstruction that multiplies commissioned IT load (MW) by region-specific cost per megawatt, which is itself trended from INSEE materials indices and labor-rate trackers. Select bottom-up checks, sampling recent EPC contracts and capex disclosures, fine-tuned totals. Key drivers in the model include Paris land inflation, average PUE targets, nuclear-grid availability, edge traffic growth, and Tier 4 adoption rates. A multivariate regression with these variables underpins the 2025-2030 forecast, and scenarios were stress-tested with interview feedback where data gaps arose.

Data Validation & Update Cycle

Before sign-off, outputs face variance checks against historical outturns, peer ratios, and customs data on generator imports. Annual refreshes are standard; interim updates trigger when grid tariffs, zoning laws, or ≥50 MW of new capacity announcements materially shift assumptions.

Why Our France Data Center Construction Baseline Commands Reliability

Published figures often diverge because some firms fold in IT racks, others quote pledged investments instead of actual outlays, and refresh cadences differ.

Mordor's scope sticks to bricks and mortar capex, applies uniform euro-to-dollar conversion at the publication date, and benefits from mid-year interviews that catch late-breaking campus phases.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.20 B (2025) | Mordor Intelligence | - |

| USD 6.23 B (2024) | Global Consultancy A | Includes IT hardware and fit-out upgrades |

| EUR 4.81 B (2025) | Industry Analytics B | Uses announced budgets, not spend realized |

| USD 6.00 B (2024) | Regional Consultancy C | Combines construction and five-year O&M estimates |

Mordor's disciplined scope selection and dual validation steps give decision-makers a balanced, reproducible baseline that sits between inflated announcement totals and narrower refurbish-only counts.

Key Questions Answered in the Report

What is the market size of the France data center construction market in 2026?

The industry is valued at USD 5.59 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 7.49% CAGR, reaching USD 8.01 billion by 2031.

Which tier classification is growing the quickest?

Tier 4 builds are projected to grow at 7.87% annually because AI and fintech workloads demand fault-tolerant designs.

Why are hyperscalers increasing self-build activity in France?

Low-carbon nuclear power, shovel-ready plots and strict data-sovereignty rules encourage cloud providers to own facilities and secure long-term capacity.

Page last updated on: