Italy Construction Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

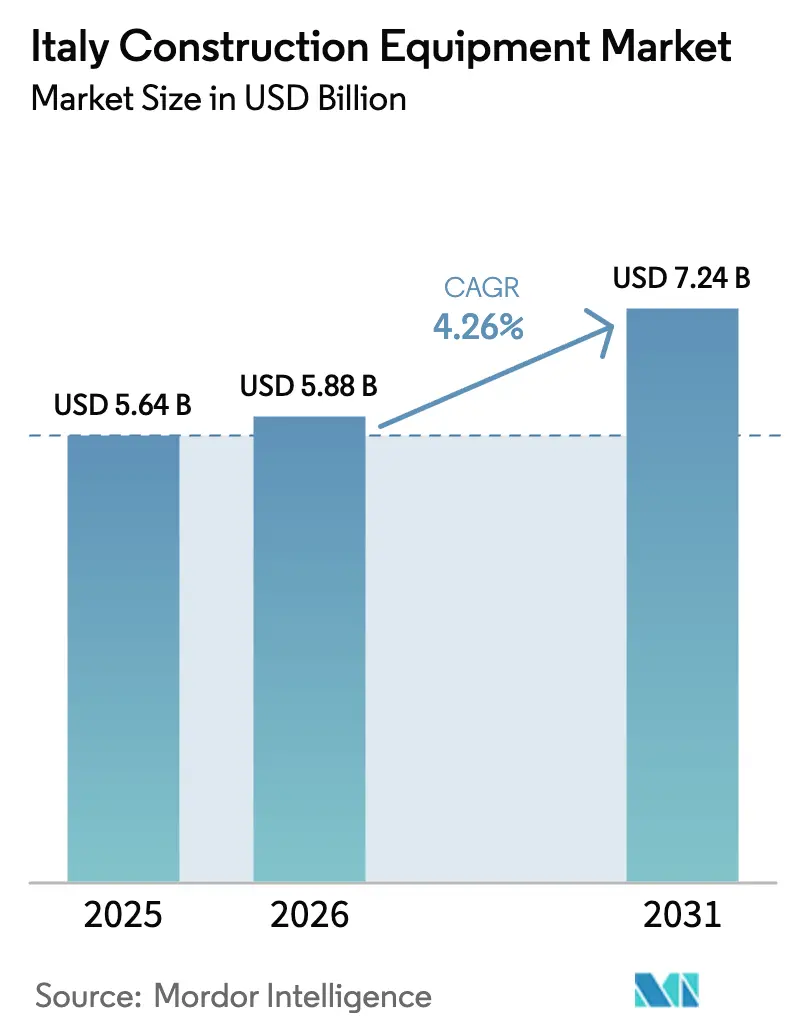

| Base Year Market Size (2025) | USD 5.64 Billion |

| Market Size (2026) | USD 5.88 Billion |

| Market Size (2031) | USD 7.24 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Construction Equipment Market Analysis by Mordor Intelligence

The Italy construction equipment market size in 2026 is estimated at USD 5.88 billion, growing from 2025 value of USD 5.64 billion with 2031 projections showing USD 7.24 billion, growing at 4.26% CAGR over 2026-2031. Rising public-sector infrastructure spending under the National Recovery and Resilience Plan (PNRR), the push toward greener propulsion technologies, and mandatory digital-building procedures underpin this steady expansion[1]“Italia Domani – Home,” Italian Government, italiadomani.gov.it. Demand also benefits from the lingering impact of residential renovation incentives and a rebound in private industrial projects, while tighter Stage V emission norms accelerate fleet renewal. Competitive intensity remains moderate, allowing mid-tier brands to gain ground through electrified models and niche applications. Regional investment rebalancing and precision agriculture requirements further widen the addressable base for specialized equipment.

Key Report Takeaways

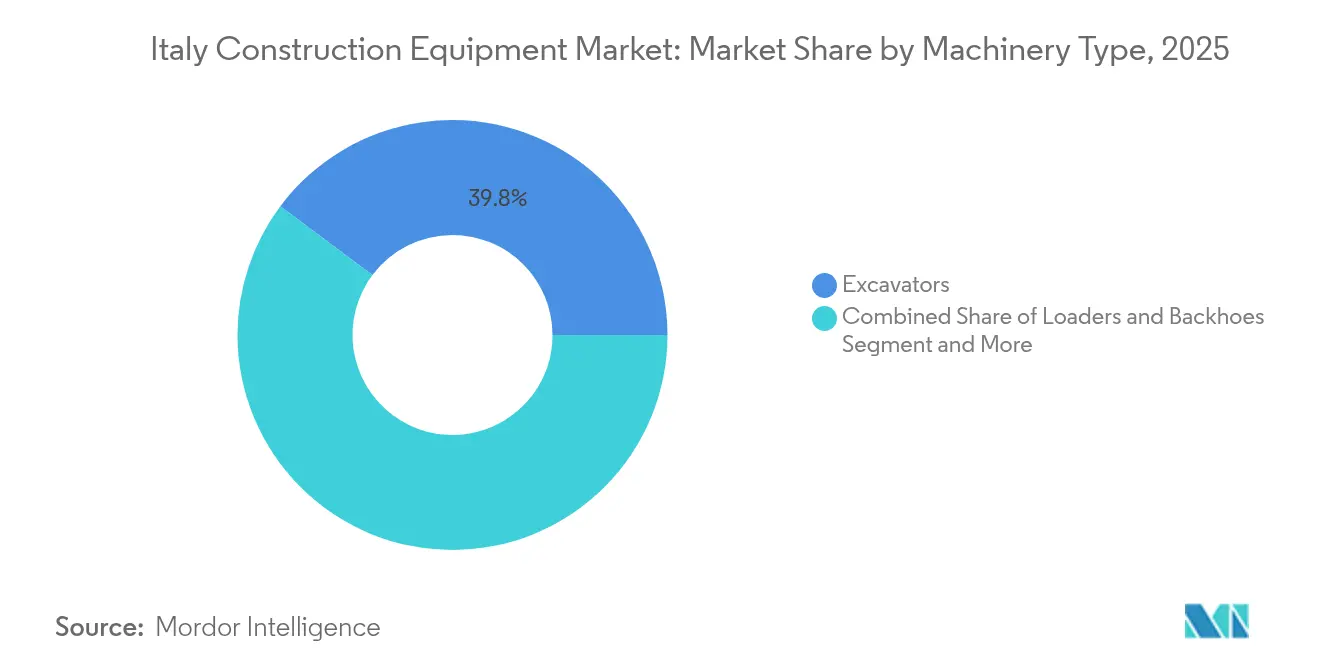

- By machinery type, excavators led with a 39.78% share of the Italy construction equipment market in 2025, whereas telescopic handlers are forecast to expand at a 6.25% CAGR to 2031.

- By propulsion, internal combustion units held 82.61% of the Italy construction equipment market share in 2025; electric models post the fastest growth at 13.86% CAGR through 2031.

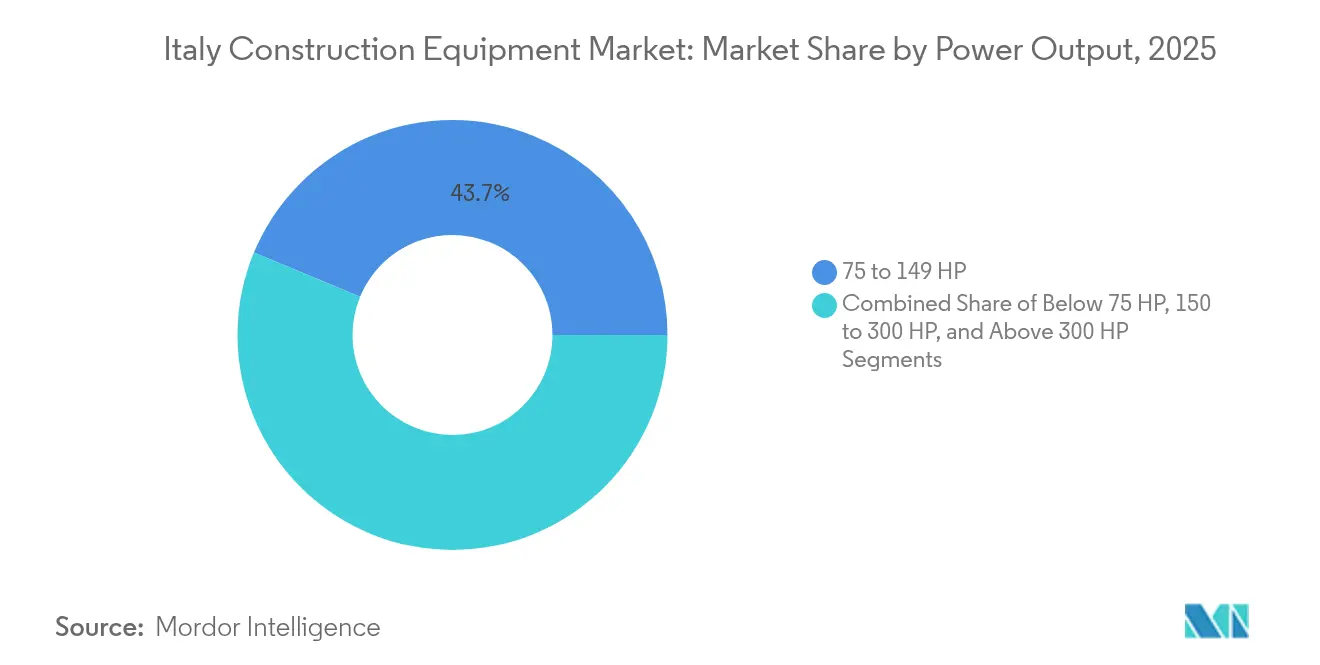

- By power output, the 75–149 HP bracket accounted for 43.74% of the Italy construction equipment market size in 2025, while equipment below 75 HP is set to rise at 15.5% CAGR over the forecast horizon.

- By application, infrastructure represented 46.62% of the Italy construction equipment market size in 2025, whereas agriculture and forestry is advancing at 6.12% CAGR to 2031.

- By region, Northern Italy commanded 52.12% of the Italy construction equipment market size in 2025; Southern Italy and the Islands accelerated at 7.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Plan and EU Recovery Fund Outlays | +1.8% | Lombardy, Veneto, Lazio, Campania | Medium term (2-4 years) |

| Residential Renovation Incentives | +1.2% | Lombardy, Lazio, Veneto, Emilia-Romagna | Short term (≤ 2 years) |

| Digitalization Mandates Boosting Smart Machinery | +0.8% | Lombardy, Piedmont, Veneto, Tuscany | Long term (≥ 4 years) |

| OEM Electrification Roadmaps | +0.6% | Apulia, Lombardy, Piedmont, Veneto | Long term (≥ 4 years) |

| Vineyard and Orchard Automation | +0.4% | Tuscany, Veneto, Piedmont, Sicily | Medium term (2-4 years) |

| Circular-Economy Policies | +0.3% | Lombardy, Veneto, Emilia-Romagna, Lazio | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Infrastructure Plan and EU Recovery Fund Outlays

The PNRR commits EUR 194.4 billion to transport, energy and digital corridors, with 39% earmarked for climate action, making it the single largest catalyst for heavy equipment demand nationwide[2]“Italy's National Recovery and Resilience Plan: Latest state of play,” European Parliament, europarl.europa.eu. High-speed rail corridors exceeding 280 km and highway upgrades stimulate extensive orders for excavators, graders and tunneling rigs. Rolling disbursements, EUR 11 billion approved in 2024 alone, create a dependable multiyear project pipeline, smoothing revenue visibility for dealers and rental fleets. As projects observe strict environmental criteria, contractors increasingly favor low-emission models, accelerating electrification across sizeable public tenders. The multiplier effect of logistics improvements also lowers supply-chain costs for OEMs and parts suppliers, reinforcing local assembly footprints.

Residential Renovation Incentives (Superbonus 110%)

Fiscal deductions that once peaked at 110% unleashed a EUR 219 billion renovation boom, driving record utilization rates for mini-excavators, skid-steer loaders and concrete pumps. Nearly 496,000 energy-upgrade projects registered by May 2024 created scheduling backlogs that pushed contractors toward rental fleets to meet delivery dates. While the 2025 budget cuts incentives to 50% for principal dwellings, a transitional surge persists as homeowners rush to lock in higher rebates. This near-term spike boosts aftermarket parts and maintenance revenue but also prompts contractors to rebalance toward infrastructure and commercial jobs once the program tapers.

Digitalization Mandates (BIM) Boosting Smart Machinery

From January 2025, public contracts above EUR 1 million must adopt Building Information Modeling (BIM), transforming site workflows and equipment procurement criteria. Although less than half of public agencies currently exploit BIM beyond design, mandatory use will broaden demand for telematics-ready excavators, intelligent compaction rollers and payload-monitoring loaders. Integration of BIM with geographic data, piloted at Catania Airport, illustrates productivity gains that justify premium prices for smart machines. Digital workflows shorten bid cycles and reduce rework, compelling rental houses to refresh fleets with IoT-enabled units to remain competitive.

OEM Electrification Roadmaps Lower Total Cost of Ownership (TCO)

A new production line for electric compact wheel loaders inaugurated in Lecce underscores the shift from prototype to serial manufacturing. OEMs highlight lifecycle fuel and maintenance savings to offset higher upfront prices, resonating with contractors operating in noise-sensitive city centers and indoor logistics hubs. The Italian goal of sourcing 39.4% of energy from renewables by 2030 dovetails with silent, zero-tailpipe-emission machinery on public works, reinforcing policy alignment. Early adopters also leverage emissions-related bonus points in tender evaluations, further tilting demand toward battery-powered units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Rental Equipment | -0.9% | Lombardy, Veneto, Lazio, Piedmont | Short term (≤ 2 years) |

| Stricter Stage V Emission Norms | -0.7% | Lombardy, Piedmont, Veneto, Emilia-Romagna | Medium term (2-4 years) |

| Fragmented SME Contractor Base | -0.5% | Southern Italy, Sicily, Sardinia, Calabria | Long term (≥ 4 years) |

| Volatile Steel Prices | -0.4% | Lombardy, Piedmont, Veneto, Apulia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Rental Equipment Industry

Double-digit fleet growth among national rental firms offers contractors flexible access to new technology without balance-sheet strain. For OEMs, this means larger but more concentrated customers who negotiate harder on price and refresh cycles, compressing equipment margins. Smaller dealers pivot toward service packages and certified used-equipment programs to offset lower wholesale volumes. While rentals uplift utilization of advanced telematics, they delay outright ownership in the SME segment, moderating net new unit sales in the short run.

Stricter Stage V Emission Norms Raising Capex

Complex after-treatment hardware inflates list prices, especially for engines above 130 kW, prompting some buyers to postpone replacements or shift to the rental channel. Maintenance technicians also require retraining, adding hidden costs for fleet operators. The regulation, however, speeds adoption of hybrid and electric options that circumvent diesel particulate requirements, effectively redefining product-mix dynamics by mid-decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Lead Infrastructure Modernization

Excavators generated 39.78% of the Italy construction equipment market in 2025 as large-scale rail and road corridors demanded robust earthmoving capacities. Crawler variants dominate heavy civil lots, whereas mini-excavators thrive in dense city-center refits backed by heritage preservation codes. Telescopic handlers, the fastest climber at 6.25% CAGR, support warehouse automation, farm logistics and modular construction, reflecting diversification away from purely civil works. Loaders and backhoe units serve municipal maintenance and aggregates handling, holding steady despite slower housing starts. Cranes see selective demand peaks in high-rise schemes in Milan and Rome, yet longer replacement cycles limit their headline growth.

A parallel transition in attachment ecosystems further spurs excavator turnover, as tiltrotators, quick-couplers and 3D machine-control kits become standard inclusions. Contractors increasingly weigh digital job-site integration and operator safety aids over raw horsepower. As a result, premium-priced models with integrated grade-assist achieve quicker payback, reinforcing brand loyalty and raising barriers for low-cost import challengers.

By Propulsion: Electric Surge Challenges ICE Dominance

Internal combustion engines still accounted for 82.61% of the Italy construction equipment market in 2025 due to entrenched refueling networks and established service know-how. Yet electric variants compound at 13.86% CAGR, targeting compact loaders, mini-excavators and access platforms where daily cycles align with overnight charging. Battery density improvements and the rollout of fast-charge depots at major worksites narrow productivity gaps versus diesel peers.

Hybrid drivetrains provide an interim step, cutting fuel burn 15–20% in stop-start duty without range anxiety. Stage V compliance costs continue to erode ICE price superiority, accelerating total cost-of-ownership parity as early as 2028 on urban projects with idle-reduction clauses. OEM announcements of dedicated battery Pack-As-a-Service options also lower entry barriers for smaller fleets exploring pilot deployments.

By Power Output: Compact Equipment Drives Market Evolution

Machines in the 75–149 HP band delivered 43.74% of 2025 revenue, balancing versatility with transport ease across mid-scale infrastructure and commercial builds. Contractors favor this class for trenching, loading and site prep where duty cycles fluctuate. The below-75 HP bracket, poised for a 15.5% CAGR, leverages lightweight designs compatible with battery propulsion and low ground pressure, ideal for renovation inside medieval cores and vineyards alike.

Manufacturers channel R&D into modular battery packs and quick-swap systems, enabling continuous shifts with minimal downtime. Conversely, the 150 HP and above segments remains essential for quarry and highway projects but exhibits slower renewal due to high capital outlay and specialization.

By Application: Infrastructure Investment Drives Market Leadership

Infrastructure works retained 46.62% of the Italy construction equipment market size in 2025, anchored by high-speed rail, port deepening and energy-grid upgrades. Long tunnel sections and viaducts elevate demand for high-tonnage excavators, pavers and piling rigs. Agriculture and forestry, the fastest-rising application at 6.12% CAGR, reflect mechanization of premium vineyards and orchard operations in central and southern provinces. Specialized narrow-gauge harvesters, low-profile telehandlers and mulchers expand OEM addressable niches. Commercial and logistics facilities sustain loader and access-platform volumes given robust e-commerce throughput, while residential renovation plateaus at lower incentive rates yet maintains a floor for compact machinery.

Geography Analysis

Northern Italy captured 52.12% of 2025 turnover, propelled by Lombardy’s industrial belt and Veneto’s export-driven manufacturing hubs. This dominance stems from robust private-sector capital expenditure, dense motorway networks and advanced manufacturing ecosystems that consistently consume heavy machinery. Lombardy, anchored by Milan, oversees urban redevelopment nodes including rail-station overbuilds and mixed-use clusters that demand high-tonnage cranes and foundation rigs. Veneto supplements volumes with port expansions and logistics hubs serving Adriatic trade lanes, while Piedmont sources equipment for cross-alpine tunnel projects linking to France and Switzerland.

Southern Italy and Islands, expanding at 7.44% CAGR, benefit from PNRR stipulations allocating at least 40% of territorial funds southward. Large-scale renewable energy parks spanning wind and solar dictate specialized lifting equipment, cable-laying crawlers and terrain-adaptive platforms suited to hilly or coastal topographies. Regional contractors increasingly form joint ventures with northern peers to access technical expertise, widening the customer base for advanced telematics and predictive maintenance tools. Enhanced motorway corridors and intermodal terminals further tie the southern supply chain to European freight flows, reinforcing sustained machinery demand post-2030.

Central Italy maintains a balanced portfolio of state-funded institutional buildings, transport links and tourism infrastructure. Rome’s metro extensions and Florence’s airport upgrade underpin steady orders for rail-maintenance machines, excavators with interchangeable road-rail undercarriages and low-emission airport service equipment. Restoration of heritage assets in Umbria and Marche favors compact, vibration-controlled mini-loaders that protect fragile masonry.

Competitive Landscape

The market features global marques alongside local specialists. The differentiation hinges less on scale than on propulsion innovation, digital integration and dealer service quality. The recent launch of an electric compact loader line in Apulia showcases how incumbent players anchor new technology domestically to capture emerging demand clusters and secure government support. Competitors respond with hybrid excavator variants, extended warranty programs and subscription-based telematics dashboards to foster lifecycle ties.

Midsize brands exploit white-space niches, vineyard automation, urban renovation, recycling systems, to win contracts where agility and custom engineering outweigh volume procurement. Partnerships between equipment makers and energy providers to bundle charging infrastructure with machine sales illustrate ecosystem thinking that can erode traditional barriers. Simultaneously, rental majors amass bargaining power by rotating fleets every four years, compelling OEMs to design residual-value-friendly platforms and integrate over-the-air diagnostics that cut maintenance down-time.

Autonomous operation prototypes progress from controlled environment pilots to highway consortium trials, with early commercialization likely in quarry haulage before broader urban deployment. Software-centric challengers enter via guidance retrofits and safety-zone geofencing, but entrenched brands leverage established parts networks and operator training centers to retain preference among risk-averse contractors.

Italy Construction Equipment Industry Leaders

Liebherr Group

CNH Industrial N.V.

AB Volvo

Caterpillar Inc.

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Mecalac Group unveiled its all-electric eS900tele swing-arm telescopic loader, offering up to eight hours of continuous duty on a single charge.

- July 2024: CNH Industrial inaugurated a new electric compact wheel loader production line at its Lecce, following EUR 13 million in facility upgrades that cement Italy’s role in European zero-emission machinery manufacturing.

Italy Construction Equipment Market Report Scope

Construction equipment is defined as any type of equipment used for the execution, completion, erection, operation, or maintenance of any construction project or work. Construction equipment is also used in earthmoving works during the construction of roads, bridges, and dams. Some types of construction equipment, like excavators and wheel loaders, are also used in mining.

Italy's construction equipment market is segmented by machinery type and drive type. By machinery type, the market is segmented into cranes, telescopic handlers, excavators, loaders and backhoes, motor graders, and other machinery types. By drive type, the market is segmented into internal combustion engines and electric and hybrid.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Excavators | Crawler Excavators |

| Wheeled Excavators | |

| Mini/Compact Excavators | |

| Loaders and Backhoes | Wheel Loaders |

| Skid-Steer Loaders | |

| Backhoe Loaders | |

| Cranes | Tower Cranes |

| Mobile Cranes | |

| Telescopic Handlers | |

| Motor Graders | |

| Asphalt Pavers and Compactors | |

| Drilling and Piling Rigs |

| Internal Combustion Engine |

| Electric |

| Hybrid |

| Below 75 HP |

| 75 to 149 HP |

| 150 to 300 HP |

| Above 300 HP |

| Residential Construction |

| Commercial Construction |

| Industrial and Manufacturing |

| Infrastructure (Road, Rail, Ports, Airports) |

| Mining and Quarrying |

| Agriculture and Forestry |

| Northern Italy | Lombardy |

| Veneto | |

| Piedmont | |

| Emilia-Romagna | |

| Central Italy | Lazio |

| Tuscany | |

| Marche | |

| Umbria | |

| Southern Italy and Islands | Campania |

| Apulia | |

| Sicily | |

| Sardinia | |

| Calabria |

| By Machinery Type | Excavators | Crawler Excavators |

| Wheeled Excavators | ||

| Mini/Compact Excavators | ||

| Loaders and Backhoes | Wheel Loaders | |

| Skid-Steer Loaders | ||

| Backhoe Loaders | ||

| Cranes | Tower Cranes | |

| Mobile Cranes | ||

| Telescopic Handlers | ||

| Motor Graders | ||

| Asphalt Pavers and Compactors | ||

| Drilling and Piling Rigs | ||

| By Propulsion | Internal Combustion Engine | |

| Electric | ||

| Hybrid | ||

| By Power Output | Below 75 HP | |

| 75 to 149 HP | ||

| 150 to 300 HP | ||

| Above 300 HP | ||

| By Application | Residential Construction | |

| Commercial Construction | ||

| Industrial and Manufacturing | ||

| Infrastructure (Road, Rail, Ports, Airports) | ||

| Mining and Quarrying | ||

| Agriculture and Forestry | ||

| By Region | Northern Italy | Lombardy |

| Veneto | ||

| Piedmont | ||

| Emilia-Romagna | ||

| Central Italy | Lazio | |

| Tuscany | ||

| Marche | ||

| Umbria | ||

| Southern Italy and Islands | Campania | |

| Apulia | ||

| Sicily | ||

| Sardinia | ||

| Calabria | ||

Key Questions Answered in the Report

What is the current size of the Italy construction equipment market?

The Italy construction equipment market stands at USD 5.88 billion in 2026 and is set to reach USD 7.24 billion by 2031.

Which machinery category holds the largest share?

Excavators lead with 39.78% of 2025 revenue, reflecting their critical role in large rail and road projects.

How fast is electric equipment growing in Italy?

Electric models register a 13.86% CAGR through 2031, the fastest among propulsion types as Stage V norms and urban emission limits gain traction.

Which Italian region is growing the quickest for equipment demand?

Southern Italy and the Islands region grow at 7.44% CAGR, buoyed by targeted PNRR investments and port modernization schemes.

What impact do rental companies have on equipment sales?

Rapid rental fleet expansion trims unit sales in the short term by offering contractors OPEX flexibility, reducing direct ownership among SMEs.

What is the outlook for compact equipment under 75 HP?

Compact machines below 75 HP are projected to rise at 15.5% CAGR, thanks to urban renovation needs and suitability for battery propulsion.

Page last updated on: