Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

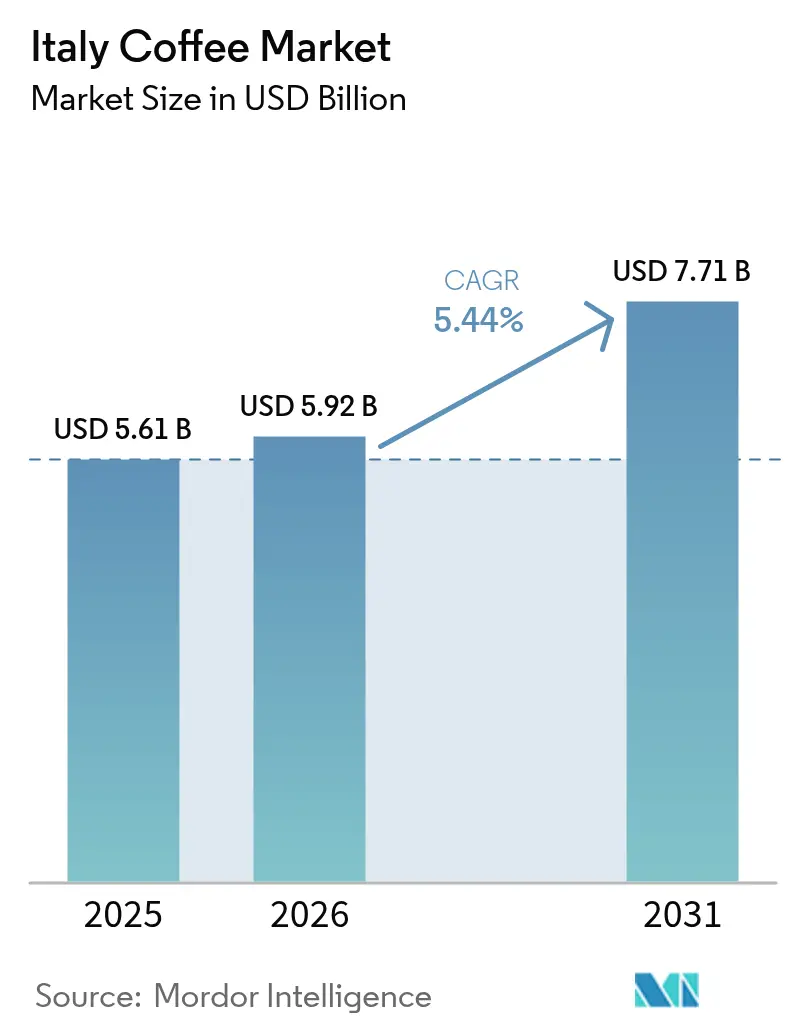

| Base Year Market Size (2025) | USD 5.61 Billion |

| Market Size (2026) | USD 5.92 Billion |

| Market Size (2031) | USD 7.71 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

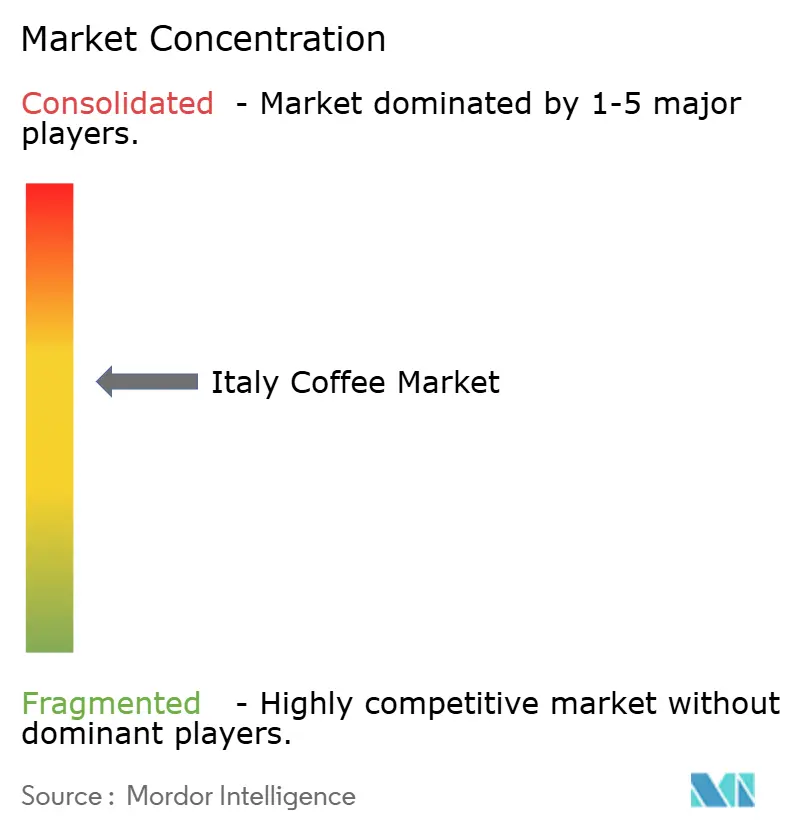

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Coffee Market Analysis by Mordor Intelligence

Italian coffee market size in 2026 is estimated at USD 5.92 billion, growing from 2025 value of USD 5.61 billion with 2031 projections showing USD 7.71 billion, growing at 5.44% CAGR over 2026-2031. Coffee consumption remains integral to Italy's cultural heritage and daily lifestyle, maintaining consistent demand across market segments. Ground coffee dominates the market share, supported by the country's strong espresso culture. However, segments including coffee pods, capsules, specialty coffee, and ready-to-drink beverages are experiencing significant growth due to convenience and premium offerings. The market's expansion is supported by increasing consumer interest in sustainable and ethically sourced products. The integration of technology, including smart brewing systems and e-commerce platforms, is enhancing market accessibility and consumer engagement. While market saturation and traditional consumption habits present certain limitations, the combination of cultural significance, premium product development, and changing consumer preferences continues to drive market growth.

Key Report Takeaways

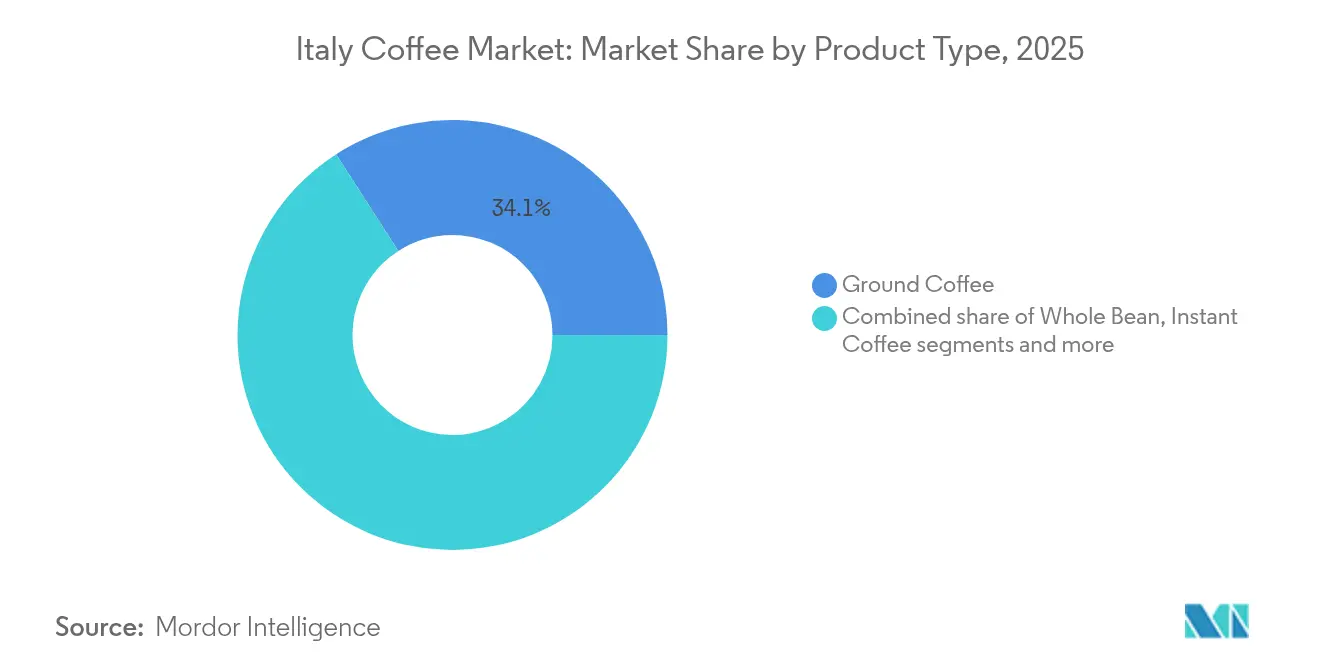

- By product type, ground coffee led with 34.10% of the Italian coffee market share in 2025, while pods and capsules are projected to grow at a 6.31% CAGR through 2031.

- By flavor, plain variants accounted for 78.20% of the Italian coffee market size in 2025, whereas flavored offerings are advancing at a 7.02% CAGR to 2031.

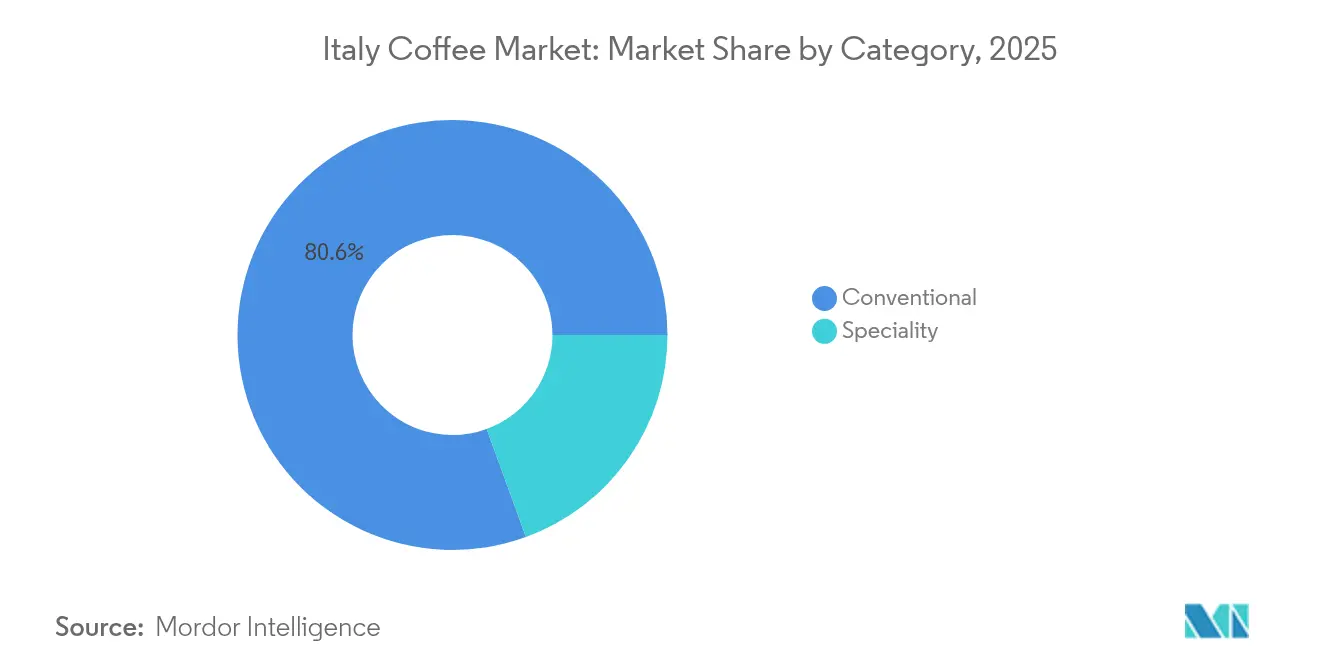

- By category, conventional lines held 80.55% share of the Italy coffee market size in 2025; specialty coffee is forecast to expand at an 7.63% CAGR over the period.

- By bean type, Arabica occupied 61.90 of % Italy coffee market share in 2025, while Robusta is set to rise at a 5.95% CAGR through 2031.

- By distribution channel, off-trade commanded 79.30% of the Italy coffee market size in 2025, whereas on-trade is rebounding at a 5.66% CAGR as hospitality recovers post-pandemic.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong cultural heritage of coffee | +1.2% | National, concentrated in Northern and Central Italy | Long term (≥ 4 years) |

| Product innovation fuel market development | +0.9% | National, with early adoption in Milan, Rome, Turin | Medium term (2-4 years) |

| Sustainability and ethical sourcing | +0.6% | National, with premium positioning in Northern Italy | Long term (≥ 4 years) |

| Convenience and ready-to-drink (RTD) coffees | +0.7% | National, with higher penetration in urban centers | Short term (≤ 2 years) |

| Rising cafe culture and social coffee consumption | +0.8% | National, with spillover to Southern regions | Medium term (2-4 years) |

| Influence of coffee chains and retail expansion | +0.5% | National, with concentration in metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong cultural heritage of coffee

Italy's deep-rooted coffee culture is a primary driver of its coffee market growth. The country's traditional coffee customs, integrated into daily routines and social interactions, maintain a steady demand for premium coffee products. Italy's established espresso culture, café customs, and distinct regional preferences shape a market where coffee represents both a beverage and a cultural cornerstone. This cultural foundation supports various coffee formats, from traditional to modern, maintaining consumer loyalty and market expansion. According to the European Coffee Federation (ECF), coffee sales in Europe increased from EUR 2,456 million in 2022 to EUR 2,571 million in 2023, demonstrating growth sustained by strong consumption patterns in key markets like Italy [1]Source: European Coffee Federation (ECF), "European Coffee Report 2023/2024", ecf-coffee.org. These figures highlight how Italy's coffee culture influences both domestic consumption and broader European market dynamics, positioning the country as an influential force in the European coffee industry.

Product innovation fuel market development

Product innovation drives the development of the Italy coffee market. While Italian consumers maintain strong ties to traditional coffee culture, they show increasing receptivity to innovative coffee products that combine heritage with modern preferences. New developments in coffee formulations, brewing methods, and flavor combinations expand market appeal beyond traditional offerings. These innovations attract both younger consumers seeking novel experiences and established customers exploring premium and specialty segments, contributing to market expansion. For instance, in February 2023, Starbucks introduced its Oleato olive oil coffee range in Italy. The Oleato line features products including a latte, cold brew, and the Oleato Deconstructed, combining coffee with olive oil to create distinct flavor profiles. This launch demonstrates how international companies adapt their offerings to align with local tastes and cultural elements, supporting market growth and diversification. These innovations enhance market dynamics by addressing evolving consumer preferences while preserving connections to Italian coffee traditions.

Sustainability and ethical sourcing

The expansion of the Italy coffee market is primarily attributed to the increasing consumer emphasis on sustainable and ethically sourced products. Italian consumers demonstrate heightened awareness regarding the environmental and social implications of their coffee procurement decisions, resulting in increased demand for sustainably produced coffee. Market participants are implementing comprehensive measures, including environmentally conscious farming methodologies, equitable labor practices, and community development initiatives in coffee-producing regions. Lavazza Group exemplifies this strategic approach through the implementation of 29 agricultural and social inclusion projects across 18 countries, encompassing more than 137,000 growers to advance sustainable agriculture and enhance community welfare. These sustainability initiatives correspond directly with Italian consumer preferences, facilitating market expansion and product innovation. The prioritization of sustainable and ethical sourcing practices continues to be instrumental in shaping the trajectory of the Italian coffee market.

Convenience and ready-to-drink (RTD) coffees

The growth of the Italy coffee market is significantly influenced by convenience and Ready-to-Drink (RTD) coffees. The demand for convenient coffee options has increased due to modern lifestyles characterized by busy schedules and on-the-go consumption patterns. RTD coffees provide portable beverages that maintain quality and taste while eliminating the need for brewing equipment or preparation time. This category particularly attracts younger consumers and urban professionals who value efficiency and premium coffee experiences. For instance, in May 2024, Lavazza expanded its product portfolio by introducing a new RTD beverage line made from a 100% Arabica blend. These products enhance Lavazza's coffee offerings while addressing the growing demand for convenience. The positive market response to RTD products continues to drive investment and development in this segment, establishing convenience as a fundamental factor in Italy's coffee consumption patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative beverages | -0.8% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Climate change impact on supply | -1.1% | Global supply chain, affecting Italian importers | Long term (≥ 4 years) |

| Price volatility and supply chain disruptions | -0.9% | Global, with direct impact on Italian roasters | Medium term (2-4 years) |

| High operational and raw material costs | -0.7% | National, concentrated in manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from alternative beverages

The Italian beverage market is experiencing a shift as alternative drinks gain popularity, particularly among younger consumers who are open to non-coffee options during traditional coffee drinking times. Premium and functional teas are seeing increased consumption, while energy drinks are gaining market share during afternoon periods typically reserved for espresso. Major Italian cities are witnessing growth in specialty tea shops and bubble tea venues, which serve as social spaces competing with traditional coffee bars. Health-conscious consumers are increasingly choosing matcha, kombucha, and adaptogenic beverages as alternatives to coffee for energy and social occasions. Plant-based milk alternatives are becoming more common in coffee preparation and as standalone beverages. In response, Italian beverage companies are diversifying their product portfolios, with coffee manufacturers adding tea, functional drinks, and wellness products to utilize their existing distribution channels and brand recognition.

Climate change impact on supply

Climate change poses a significant restraint on the Italian coffee Market by impacting the global coffee supply chain and increasing uncertainties around raw material availability and cost stability. As Italy imports virtually all its green coffee beans, disruptions in major coffee-producing regions caused by climate change, such as altered rainfall patterns, rising temperatures, and increased incidence of pests and diseases, directly threaten the quality, yield, and reliability of coffee crops. These environmental stresses can reduce supply volumes and elevate raw coffee prices, squeezing profit margins for Italian roasters and limiting their pricing flexibility. Climate-related supply volatility challenges the ability of market players to maintain consistent product quality and fulfillment, creating risks around sourcing and inventory management. The need for sustainable agricultural practices and investments in climate-resilient coffee farming adds operational complexity and cost, which smaller producers and roasters may find difficult to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pods Drive Convenience Revolution

Ground Coffee dominates the Italian coffee Market with a 34.10% market share in 2025. This leadership position stems from Italy's established coffee culture and traditional brewing methods that emphasize ground coffee use in homes and cafés. Ground coffee remains integral to authentic Italian coffee preparation, with consumers preferring it for its optimal balance of convenience and flavor quality. The format enables users to create fresh brews that match professional café standards. Ground coffee's versatility accommodates various brewing methods, supporting daily consumption patterns from morning espressos to afternoon coffee breaks. The segment maintains its strong position through diverse product offerings, including multiple blends, roast levels, and brewing options that serve different consumer preferences.

Coffee Pods and Capsules represent the fastest-growing segment in the Italian Coffee Market, with a CAGR of 6.31% projected through 2031. This growth results from increasing consumer demand for convenience, consistent quality, and wider adoption of single-serve coffee machines in households and offices. Pods and capsules provide efficient brewing solutions while maintaining taste quality, attracting busy consumers and younger demographics who value modern coffee experiences. The segment's expansion continues through product innovations, including the development of cross-compatible capsules and new flavor varieties. In December 2024, Maurizio Distefano Licensing (MDL) demonstrated this trend by launching Baileys-branded coffee capsules and pads through Italian coffee brand Caffè Borbone.

By Flavor: Traditional Preferences Face Innovation

Plain coffee maintains a dominant market position in the Italian coffee Market, representing 78.20% market share in 2025. This significant market presence is attributed to Italian consumers' established preference for traditional, unadulterated coffee that emphasizes the inherent characteristics of premium coffee beans. The market preference for plain coffee demonstrates Italy's deep-rooted coffee heritage, which prioritizes superior bean quality, professional roasting techniques, and conventional brewing methodologies. Plain coffee accommodates diverse consumption patterns, from traditional morning espresso to structured coffee breaks, underscoring its cultural importance and consistent market demand.

Flavored coffee demonstrates substantial market momentum in the Italian coffee Market, exhibiting a projected CAGR of 7.02% through 2031. This market expansion indicates a transformation in consumer preferences, specifically among younger demographic segments and metropolitan consumers pursuing diversified taste experiences. Flavored coffee variants appeal to consumers seeking enhanced aromatic profiles and sweetness characteristics, incorporating specific spice combinations and flavor compounds. The segment's development is facilitated by systematic product innovation and strategic marketing initiatives from coffee manufacturers aiming to establish market presence within specialized segments of the mature coffee industry.

By Category: Specialty Coffee Gains Premium Ground

Conventional coffee maintains an 80.55% market share in the Italian coffee Market in 2025, demonstrating its predominant position among Italian consumers. This market leadership is attributed to Italy's deeply established coffee culture, which prioritizes traditional blends and methodical preparation techniques refined across generations. Conventional coffee's broad market acceptance is founded on its established flavor profiles, standardized quality parameters, and competitive price positioning, effectively serving diverse market segments from residential consumers to commercial establishments. The segment's market position is fortified by established Italian coffee manufacturers who maintain consumer retention through systematically developed roasting and blending processes.

Specialty coffee demonstrates superior growth dynamics in the Italian coffee Market, projecting a CAGR of 7.63% through 2031. This market expansion is primarily driven by increasing consumer demand for premium-grade, artisanal coffee products that emphasize geographical origin, distinctive flavor characteristics, and verified sustainable procurement practices. The segment primarily attracts younger demographic cohorts, urban populations, and higher-income consumers who demonstrate a willingness to invest in products with authenticated organic and fair-trade certifications. Market growth is additionally supported by the systematic expansion of specialized coffee establishments, contemporary coffee venues, and direct procurement channels between roasters and agricultural producers, enhancing product quality standards and consumer engagement metrics.

By Bean Type: Arabica Dominance Faces Robusta Challenge

Arabica beans constitute 61.90% market share in the Italian coffee Market in 2025. The preference for Arabica stems from its sophisticated flavor composition and comparatively reduced caffeine concentration. These beans generate refined taste characteristics, incorporating distinct fruit-forward notes, floral elements, and balanced acidity that conform to established Italian espresso blend specifications. The deeply rooted Italian espresso culture emphasizes these distinguished attributes, establishing Arabica as the predominant selection among consumers and industry professionals. The superior quality of these beans corresponds directly with the methodical roasting and precise blending techniques inherent in Italian coffee production.

Robusta coffee demonstrates a projected CAGR of 5.95% through 2031 in the Italian coffee Market. This expansion is attributed to Robusta's elevated caffeine composition and pronounced bitter flavor characteristics, which contribute to enhanced espresso blend properties, specifically in crema formation and body development. Manufacturing entities increasingly integrate Robusta varieties into their formulations to achieve intensified flavor profiles and optimal crema production. This trajectory indicates a significant market evolution, wherein established preferences coexist with increasing consumer demand for more robust coffee experiences.

By Distribution Channel: Off-Trade Dominance Meets On-Trade Recovery

Off-trade channels maintain market leadership in the Italian coffee Market, holding a 79.30% share in 2025. Italian consumers predominantly purchase coffee products through retail outlets, including supermarkets, hypermarkets, convenience stores, and specialty shops for home consumption. The off-trade segment's strength stems from extensive product availability across various coffee formats that meet diverse consumer preferences. The growth of e-commerce within the off-trade segment is transforming purchasing behaviors through direct-to-consumer sales and increased access to premium and niche products. Competitive pricing, promotional activities, and flexible purchasing options from single units to bulk quantities reinforce the off-trade channel's market position.

On-trade channels in the Italian coffee Market project a CAGR of 5.66% through 2031. This growth reflects increasing consumer preference for out-of-home coffee consumption in cafés, restaurants, hotels, and hospitality venues where coffee remains integral to social and cultural practices. The segment's expansion aligns with consumer demand for premium coffee experiences and convenient out-of-home consumption. According to the Italian National Institute of Statistics, household expenditure on food consumption outside the home in Italy increased by 4% in 2024 compared to 2023, reaching approximately EUR 96 billion . This trend highlights the hospitality and foodservice sectors' influence on coffee consumption patterns, with on-trade venues serving as key platforms for product innovation and premium coffee experiences.

Geography Analysis

Italy's coffee market demonstrates regional consistency with variations influenced by economic, cultural, and lifestyle factors. Northern Italy, including metropolitan centers like Milan and Turin, leads in specialty coffee adoption and premium product consumption. The region's higher disposable incomes and exposure to international coffee trends drive demand for premium coffee products. Northern Italy's concentrated industrial and business environment also creates substantial demand for office coffee solutions and convenient formats like pods and capsules, aligned with the urban professional lifestyle.

Central Italy, with Rome at its core, functions as a transitional market between traditional espresso culture and emerging coffee trends. The region bridges the innovation-focused North and tradition-oriented South. Consumers maintain their appreciation for classic espresso while showing growing interest in specialty coffees and modern consumption formats.

Southern Italy maintains traditional coffee preparation methods and flavor profiles, safeguarding Italy's coffee heritage. The younger demographic increasingly adopts modern formats such as pods, capsules, and ready-to-drink options, signaling a gradual shift toward convenience and diversification. Supporting Italy’s overall coffee market relevance, the Observatory of Economic Complexity (OEC) reports that in 2023, Italy imported coffee worth USD 2.47 billion, ranking as the world's 4th largest coffee importer . This volume reinforces Italy's significance as a coffee market, combining traditional practices with evolving consumer preferences across regions, sustaining a consistent coffee consumption pattern nationwide.

Regulatory Landscape

Coffee products sold in Italy fall under the EU food-law framework, including general food safety and traceability obligations under Regulation (EC) 178/2002, along with hygiene requirements under Regulation (EC) 852/2004. Product integrity also depends on compliance with EU contaminant limits, including monitoring requirements for contaminants such as ochratoxin A under Regulation (EC) 1881/2006, which can feed into roasting controls, supplier qualification, and incoming-bean testing.

Category-specific rules apply to coffee extracts through Italy's implementation of Directive 1999/4/EC (via D.P.R. 255/2000), covering composition, labeling, and product naming for extracts and soluble formats. For import and market access, operators also face expanding due-diligence requirements for deforestation-free supply chains under Regulation (EU) 2023/1115 (EUDR), with main obligations applying from 30 December 2026 for operators placing coffee on the EU market. This increases the need for origin traceability (including plot-level information) and for due-diligence statements that meet EU requirements.

Value Chain Analysis

Italy's coffee value chain is anchored in imported green coffee, where importers and green coffee traders coordinate sourcing, quality specifications, and risk management for roasters. Major logistics gateways such as the Port of Genoa and the Port of Trieste handle inflows, and roasting companies then convert green beans into branded retail packs and foodservice formats (ground coffee, whole bean, pods and capsules, instant, and RTD). Packaging suppliers and equipment manufacturers (professional and household machines) also shape how products are prepared, reinforcing the country's espresso-led consumption model.

Downstream, distribution splits between off-trade channels (supermarkets/hypermarkets, convenience and grocery, specialty retail, and online) and on-trade outlets (bars/cafes, restaurants, hotels, and travel hubs). Industry bodies such as Unione Italiana Food, through the Comitato Italiano del Caffe (representing over 65 companies and about 80% of the national coffee market), and associations like ALTOGA and GITC function as coordination points on trade, compliance, and operating standards. Their role is becoming more operationally critical as EUDR-driven due diligence adds additional data collection, verification, and documentation steps between origin suppliers, importers, and roasters.

Competitive Landscape

The Italian coffee market shows moderate concentration, with established domestic companies maintaining strong positions through their heritage, quality standards, and distribution networks. Market leaders like Lavazza exemplify this trend, with the group reporting revenues of EUR 3.35 billion in 2024, marking a 9.1% increase over the previous year. These companies maintain their market positions through continuous innovation and international expansion, operating in a competitive environment shaped by traditional brands and specialty roasters.

Companies differentiate themselves through technology adoption in the Italian coffee market. IoT-enabled brewing systems enable customized coffee preparation, while sustainable packaging innovations address environmental concerns. Companies also utilize e-commerce platforms to enhance customer relationships and improve operational efficiency, allowing quick responses to market changes.

The market presents growth opportunities in premium ready-to-drink (RTD) coffee, functional beverages, and sustainable packaging. These segments reflect consumer preferences for convenience, health benefits, and environmental responsibility, while building on Italy's manufacturing capabilities and brand heritage. New market entrants include specialty roasters offering single-origin and artisanal coffees, subscription-based services providing personalized experiences, and companies developing smart brewing technologies for customized coffee preparation.

Italy Coffee Industry Leaders

-

Luigi Lavazza S.p.A.

-

Nestlé S.A.

-

Kimbo S.p.A.

-

Starbucks Corporation

-

Gruppo Illy S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Single-serve innovation and capacity build-out are creating room for growth across pods, capsules, and other convenience-led formats. Ongoing moves include Lavazza's Tabli system (launched in April 2025), which uses coffee tabs without protective capsules, and Massimo Zanetti Beverage Group's April 2026 acquisition of On Caffe, aimed at scaling single-serve manufacturing capacity. Together, these actions indicate sustained competition around proprietary systems, compatible formats, and higher-throughput packaging.

Sustainability-linked sourcing and traceability are also becoming direct commercialization levers as EUDR timelines approach, shifting procurement toward data-verified supply. This is reinforced by active corporate programs and financing, including Lavazza's network of 29 agricultural and social inclusion projects across 18 countries involving more than 137,000 growers, and the company's April 2026 sustainability-linked financing agreement (EUR 900 million) tied to ESG targets. In this setup, opportunities cluster around compliance-grade traceability services, verified sustainable product lines (including specialty and origin-differentiated offerings), and packaging or format redesign that reduces material use while keeping espresso-quality positioning.

Recent Industry Developments

- June 2026: Lavazza began commercial launch activities for its Tablì single-serve espresso system in the United States, supported by a production facility in Gattinara, Italy. The move extends an Italian-developed single-serve format beyond the domestic market and adds manufacturing scale behind a capsule-alternative system.

- September 2025: illycaffe acquired an 80% stake in Capitani S.r.l., a coffee machine manufacturer. The deal deepens vertical integration into equipment, supporting tighter control over brewing technology and reinforcing illycaffe's premium positioning across home and professional channels.

- April 2024: Private equity firm QuattroR acquired a 50% stake in Massimo Zanetti Beverage Group via a capital increase. The investment injected growth capital into one of Italy's major coffee groups and underlined the role of financial sponsors in funding international expansion and portfolio development.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Italy coffee market is measured as the value of coffee sold and consumed in Italy across retail and foodservice, covering common formats like whole bean, ground, instant, pods, and capsules.

Scope exclusions: ready-to-drink coffee beverages, coffee-flavored dairy drinks, and standalone coffee machines and grinders are not counted in this market sizing.

Segmentation Overview

-

By Product Type

- Whole Bean

- Ground Coffee

- Instant Coffee

- Coffee Pods and Capsules

- Ready-to-Drink (RTD) Coffee

-

By Flavor

- Plain

- Flavored

-

By Category

- Conventional

- Speciality (Organic/Single-Origin)

-

By Bean Type

- Arabica

- Robusta

- Others

-

By Distribution Channel

- On-trade

-

Off-trade

- Supermarkets/Hypermarkets

- Convenience/ Grocery Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is used to set the structure of the market model and to sanity check country-level demand signals. We rely on public statistics and sector references such as ISTAT releases, Eurostat trade and consumption tables, FAOSTAT agricultural series, and customs tariff line guidance for coffee product codes. This is supported with coffee association publications, sustainability and certification summaries, and peer-reviewed papers that explain consumption patterns and channel shifts.

On top of that, we review company annual reports, investor presentations, and major retailer and foodservice announcements to understand pricing moves, format mix, and promotional intensity over time. Where helpful, a paid subscription for company financials and a shipment-level import and export database are used to cross-check reported revenues and coffee inflow trends against the demand picture. The desk sources listed here are illustrative only, and other public and paid references were used to fill gaps and confirm assumptions.

Primary Interviews and Surveys

Primary work is used to validate the split between at-home and out-of-home demand, and to pressure test pricing and mix assumptions that cannot be read directly from public tables. We interview and survey roasters, importers, distributors, retail channel experts, and foodservice operators across Italy so the model reflects how volumes, pack sizes, and pricing are actually moving. Input is also used to confirm how specialty and single-serve formats are counted, and where substitution between formats is happening.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | |

| Mid tier: 46% | Functional/Unit leaders: 35% | |

| Smaller Players: 20% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that reconstructs national coffee consumption using a mix of category splits and channel allocation, then converts that into value using observed price and mix signals. To keep the numbers realistic, we corroborate results with selective bottom-up checks such as sampled brand and private-label price points, retailer shelf observations, and a limited roll-up of supplier revenues where disclosures are available.

The key inputs in the model include per-person consumption direction, the share shift between on-trade and off-trade, the mix of ground versus pods and capsules, import and export movements for green and roasted coffee, and inflation-led unit price changes by pack format. Because pricing has been a major swing factor in recent years, average selling prices are not treated as a single flat number, and instead are aligned to format mix and channel behavior before totals are finalized.

For forecasting, scenario analysis is used, followed by a simple multivariate regression cross-check that links value growth to variables like inflation, foodservice traffic direction, and format penetration. When bottom-up checks are incomplete, for example small local roasters with limited disclosures, gaps are handled through conservative scaling based on observed channel share and regional distribution patterns discussed during interviews.

Data Validation & Update Cycle

Outputs are validated through multiple checks so large jumps are explained before sign-off. We compare the implied volumes and prices against trade flows, public consumption indicators, and the interview-led view of channel performance, and then recheck any mismatch at the assumption level. If a variance remains, the related inputs are revisited, and follow-up calls are triggered with the most relevant respondents.

Before publication, the model and write-up go through an internal multi-step review so definitions, math, and logic stay consistent across sections. Reports are refreshed annually, and interim updates are made when a material event changes pricing, supply availability, or channel dynamics. Right before delivery, a final pass is completed so clients receive the latest updated view that matches the most recent data cut.

Mordor Intelligence's Italy Coffee Market Size Compared With Other Published Estimates

Different publishers often land on different market sizes even when they use the same country name, because the counted products, channel coverage, and base year price logic are not always aligned. In coffee, the swing usually comes from whether single-serve formats are treated fully, how foodservice value is captured, and how inflation-driven price changes are applied in the base year.

Trade-flow direction for coffee beans and roasted coffee, combined with channel checks on retail pricing and on-trade consumption intensity, are the evidence points that keep Mordor Intelligence tied to a realistic Italy demand pool and the right format mix instead of a narrow retail-only view.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.61 B (2025) | |

| Industry Research Publisher A | USD 3.80 B (2025) | The total appears to be more conservative on value capture, and the scope can lean toward packaged retail coffee, which can undercount on-trade sales and the premium pricing seen in pods and capsules. |

| Market Research Publisher B | USD 4.03 B (2024) | Using an earlier base year can reduce the measured value in a period of fast price movement, and product definitions that emphasize beverages and cafe drinks can treat coffee formats differently from a format-based coffee category model. |

Across the table, the spread is mainly explained by base year timing and by how completely out-of-home consumption and single-serve value are counted. By keeping the inputs traceable to demand signals, channel splits, and format-specific pricing, the resulting number is easier to follow and to reproduce when assumptions are updated.

Key Questions Answered in the Report

How big is the italy coffee market in 2026?

It is valued at USD 5.92 billion in 2026 and is projected to reach USD 7.71 billion by 2031.

What is the expected CAGR for coffee sales in Italy?

Sales are forecast to advance at a 5.44% CAGR over 2026-2031.

Which product type is growing fastest in Italy?

Pods and capsules are projected to expand at a 6.31% CAGR through 2031.

Which bean type holds the largest share in Italian blends?

Arabica leads with a 61.90% share, though Robusta is growing at 5.95% CAGR due to cost and climate resilience advantages.

Page last updated on: