Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

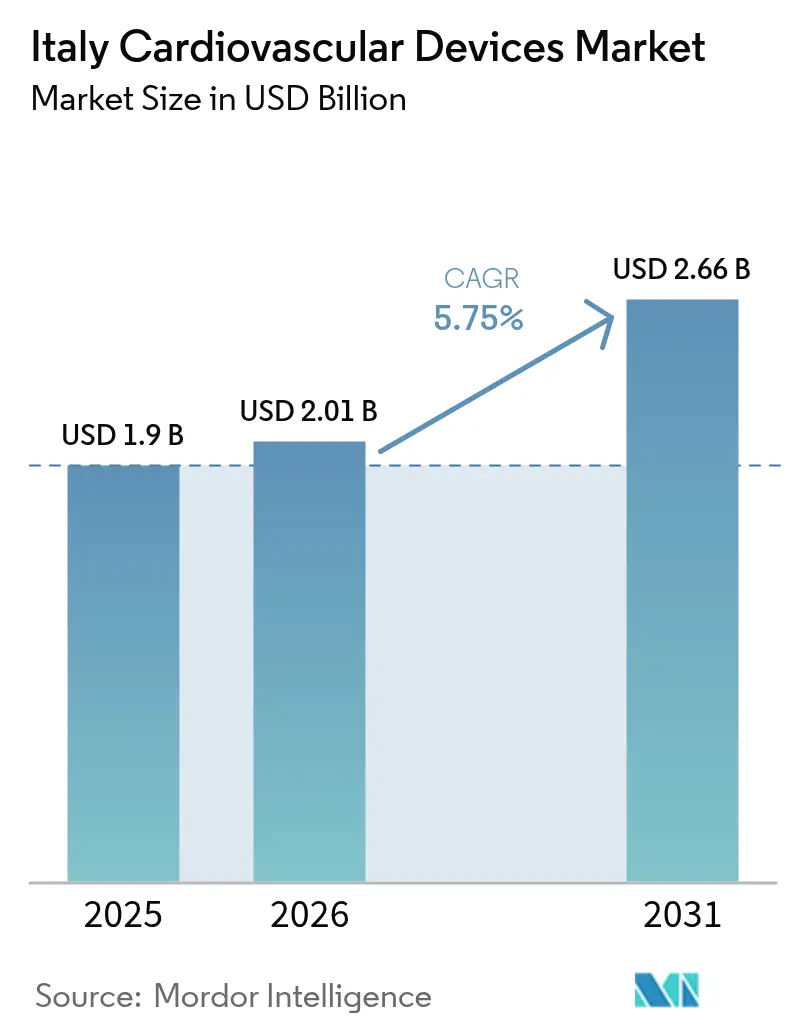

| Base Year Market Size (2025) | USD 1.9 Billion |

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

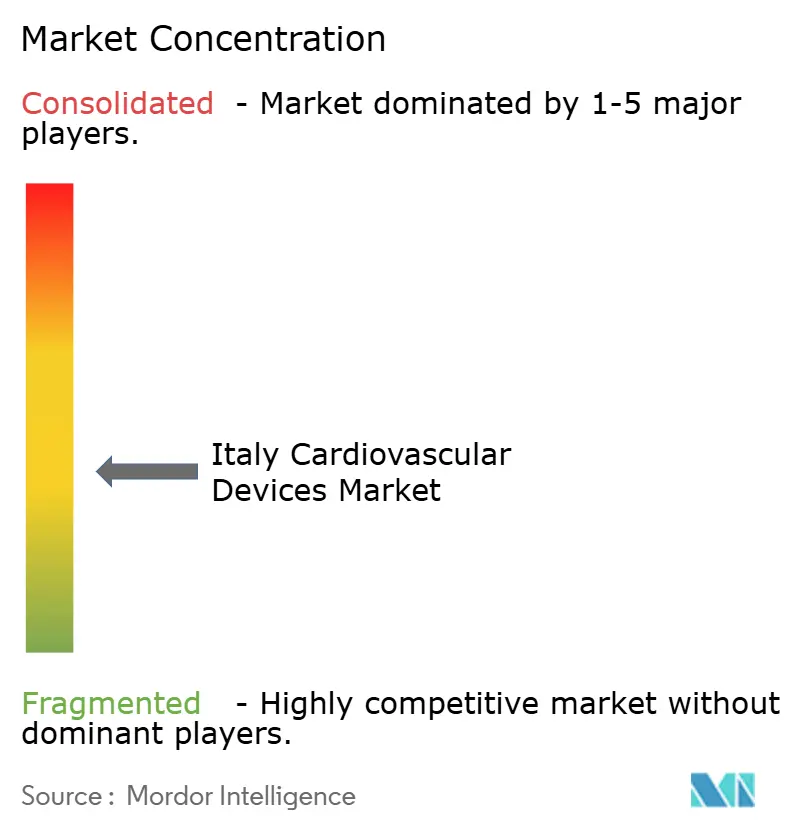

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Cardiovascular Devices Market Analysis by Mordor Intelligence

The Italy Cardiovascular Devices Market size is expected to grow from USD 1.9 billion in 2025 to USD 2.01 billion in 2026 and is forecast to reach USD 2.66 billion by 2031 at 5.75% CAGR over 2026-2031. The expansion is supported by population ageing, early-stage screening initiatives and swift uptake of minimally invasive technologies. Investments under the National Recovery and Resilience Plan are refreshing hospital equipment and widening access to specialty centers, while post-pandemic shifts toward shorter stays and outpatient care are driving preference for portable and home-based solutions[1]European Commission, "Italy’s recovery and resilience plan," commission.europa.eu. At the same time, tighter price caps on premium implants, combined with the ongoing European Union Medical Device Regulation transition, are reshaping go-to-market strategies and accelerating consolidation across the Italian cardiovascular devices market.

Key Report Takeaways

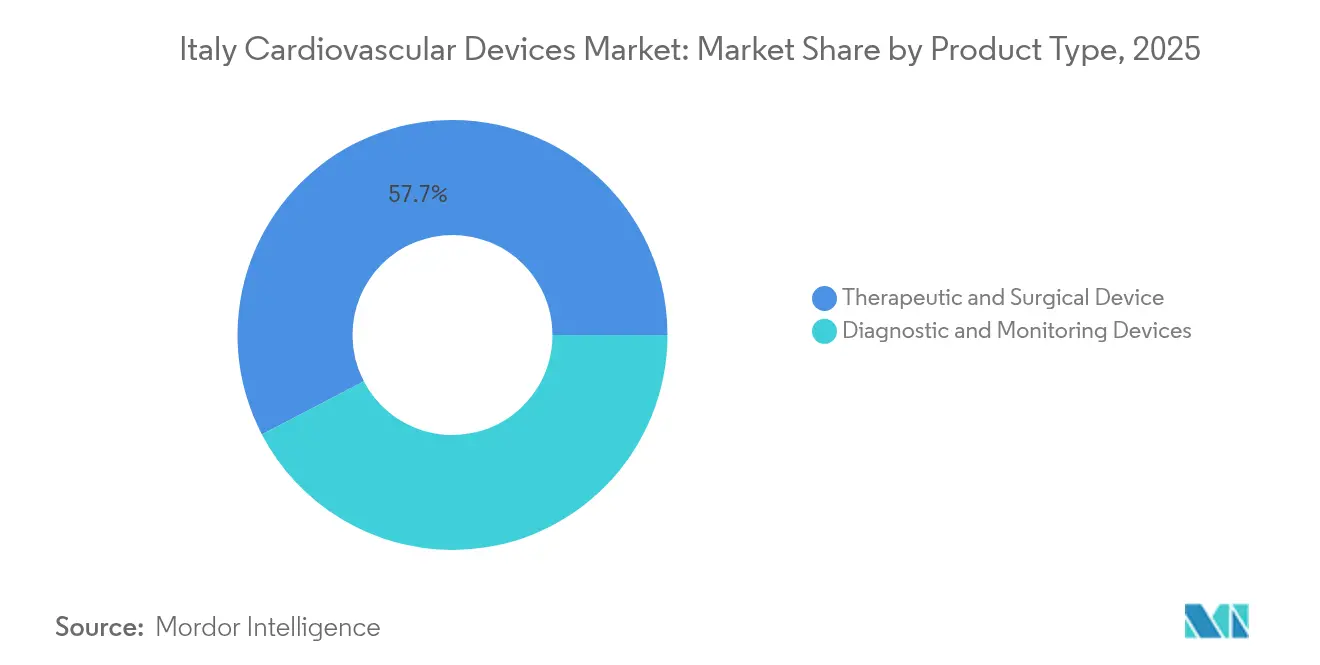

- By device type, therapeutic and surgical devices led with 57.65% of the Italian cardiovascular devices market share in 2025, while diagnostic and monitoring devices are forecast to expand at a 5.98% CAGR through 2031.

- By indication, coronary artery disease captured 49.10% share of the Italian cardiovascular devices market size in 2025; heart failure applications are projected to grow at a 7.04% CAGR between 2026 and 2031.

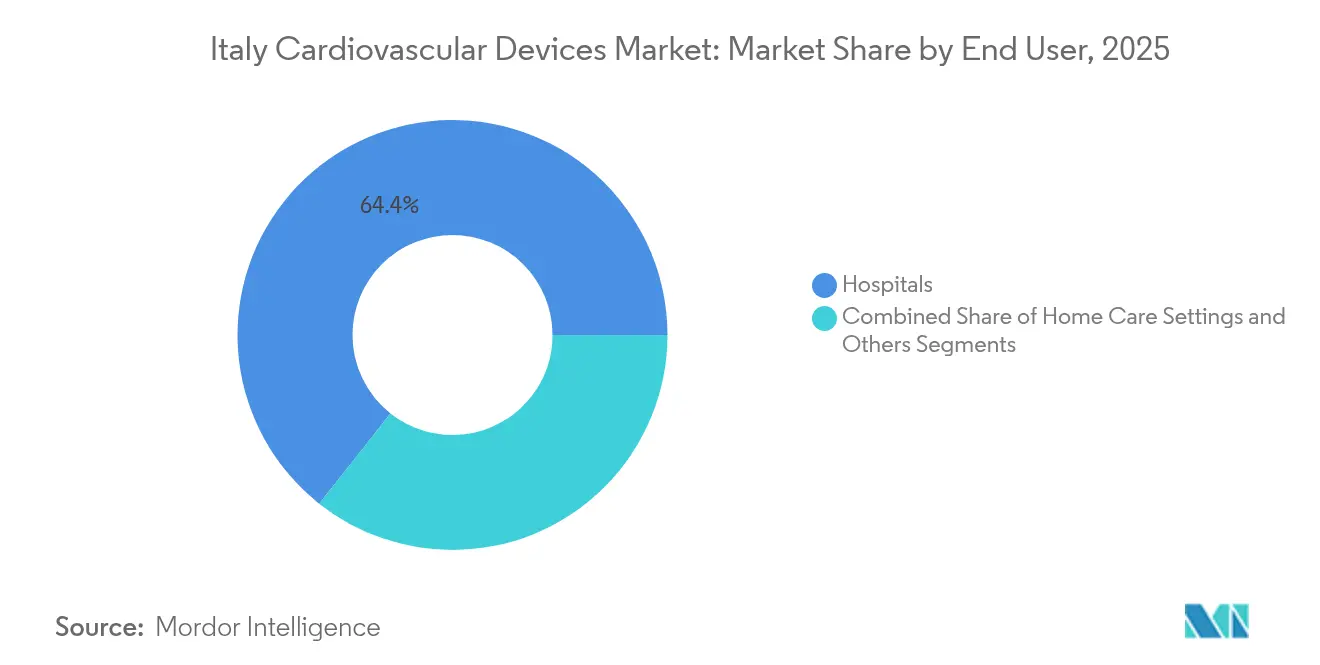

- By end user, hospitals accounted for 64.35% of the Italian cardiovascular devices market size in 2025, whereas home care settings are advancing at a 6.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National screening programs & rising coronary angiography volumes | +1.2% | Northern regions | Medium term (2–4 years) |

| Government incentives for early TAVI reimbursement under LEA | +1.5% | Urban centers | Short term (≤ 2 years) |

| Aging population-driven surge in PAD procedures | +0.8% | Southern regions | Long term (≥ 4 years) |

| Expansion of public–private cardiovascular centers | +0.7% | Northern and central regions | Medium term (2–4 years) |

| Rapid technological advances and minimally invasive procedures | +1.3% | Specialized centers nationwide | Medium term (2–4 years) |

| Increasing Adoption of Minimally Invasive Cardiac Procedures | +0.3% | Southern regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

National Screening Programs & Rising Coronary Angiography Volumes

Italy’s structured cardiovascular screening is uncovering previously undetected conditions in both athletes and the elderly, generating steady demand for diagnostic imaging and catheter-based tools. Coronary angiography volumes that dipped during the pandemic have returned to pre-crisis levels, with urgent post-surgical angiography now required in 1.83% of cardiac surgery cases. These patterns are stimulating investment in fractional flow reserve, optical coherence tomography and AI-enabled echocardiography platforms that improve lesion assessment and shorten procedure times. The Italian cardiovascular devices market benefits as hospital cath-lab managers refresh inventories to accommodate both routine and emergency cases.

Government Incentives for Early TAVI Reimbursement under LEA

The listing of Transcatheter Aortic Valve Implantation in the Essential Levels of Assistance has cut the median inpatient stay from 7 to 5 days, saving hospitals USD 565 per patient while broadening patient eligibility. Favorable funding, paired with Italy’s high‐risk patient profile, is advancing uptake of next-generation self-expanding and balloon-expandable valves. Device makers are responding with low-profile delivery systems and durability-enhanced leaflet materials, reinforcing momentum in the Italian cardiovascular devices market.

Aging Population-Driven Surge in Peripheral Artery Disease Procedures

With 23.8% of residents aged 65 or older, Italy holds one of Europe’s oldest populations [2]Eurostat, "Population Structure and Ageing," ec.europa.eu. The prevalence of peripheral artery disease in people with type 2 diabetes has reached 19–22%. National clinical guidelines now prioritize ankle-brachial index screening and embolic-protection devices to curb procedural complications. These shifts prompt hospitals to expand inventories of covered stents, drug-coated balloons and atherectomy devices, keeping the Italian cardiovascular devices market on a solid growth path.

Rapid Technological Advancements and Minimally Invasive Procedures

Robotic mitral valve surgery has trimmed total hospitalization costs by 20% and enabled earlier discharge relative to conventional minimally invasive approaches. Pairing Enhanced Recovery After Surgery protocols with smaller incisions further cuts length of stay by 21%. Artificial intelligence is now matching expert echocardiographers in detecting wall-motion abnormalities. Together, these innovations are tilting physician preference toward less invasive techniques, reinforcing double-digit growth pockets inside the Italian cardiovascular devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Consip price caps for stents & TAVI | −1.0% | Nationwide | Medium term (2–4 years) |

| EU-MDR re-certification delays | −1.2% | Small and medium manufacturers | Short term (≤ 2 years) |

| Regional disparities in device access across public hospitals | −0.8% | Southern regions | Long term (≥ 4 years) |

| Budgetary constraints in public healthcare spending | −0.7% | Northern and central regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

National Consip Price Caps Compressing ASPs for Stents & TAVI

Italian procurement authority Consip imposes ceiling prices that have narrowed margins on drug-eluting stents and valve implants. A 2024 tender awarded to a new entrant underscored intensifying competition and price pressure in TAVI. Hospitals, reimbursed via diagnosis-related groups, increasingly look for bundled-service offers that link device supply to clinical outcomes. Manufacturers must therefore justify performance with head-to-head evidence while revising contracting terms, dampening immediate revenue growth in the Italian cardiovascular devices market.

EU-MDR Re-certification Delays Causing Catheter Supply Shortages

Only 8,120 of the required MDR applications were submitted by late 2024, leaving thousands of legacy certificates to lapse. Italian hospitals have reported intermittent catheter shortages, prompting urgent substitution with higher-priced imports. Small domestic producers, which account for 94% of the country’s device firms, face steep documentation costs that postpone innovation cycles. These factors trim near-term growth, although firms that complete certification stand to gain share in the Italian cardiovascular devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Devices Drive Revenue Leadership

Therapeutic and surgical devices command 57.65% of the Italian cardiovascular devices market, anchored by sustained implant volumes for drug-eluting stents, cardiac rhythm management systems and Transcatheter Aortic Valve Implantation. The Italian cardiovascular devices market size for therapeutic systems is projected to expand at 5.3 2Source: AdvaMed, “Global Medical Device Recall Index,” advamed.org307" class="citation-tooltip" aria-label="Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com"> 1Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com% CAGR, supported by hospital upgrades and aging-driven procedure counts. Demand tilts toward platforms that shorten procedure time, such as rapid-exchange angioplasty balloons and single-access vascular closure devices, which improve throughput in busy cath labs.

Diagnostic and monitoring solutions, despite a smaller base, are forecast to rise at a 5.98% CAGR. Fractional flow reserve consoles, ECG-gated CT scanners and AI-powered echocardiography suites are seeing the fastest growth as physicians seek functional data to refine treatment plans. Portable Holter monitors and insertable cardiac monitors with six-year battery life further broaden remote-care capabilities.

By Indication: Heart Failure Emerges as the Fastest Climber

Coronary artery disease retains 49. 2Source: AdvaMed, “Global Medical Device Recall Index,” advamed.org307" class="citation-tooltip" aria-label="Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com"> 1Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com0% of the Italian cardiovascular devices market share thanks to entrenched screening and treatment pathways. Coronary computed tomography angiography, recently validated as a non-inferior alternative to invasive angiography in selected patients, strengthens noninvasive work-ups .

Meanwhile, the Italian cardiovascular devices market size linked to heart failure therapies is accelerating at 7.04% CAGR. Telemonitoring programs that lower rehospitalizations are stimulating adoption of sensor-equipped leads and algorithm-based remote monitoring hubs. In structural heart, transcatheter mitral and tricuspid repair systems such as the PASCAL platform are achieving high clinical success, widening eligibility criteria.

By End User: Hospitals Dominate, Home Care Gains Traction

Public hospitals absorb 64.35% of device demand, reflecting their role in complex surgery and acute interventions. Recovery-plan funding of EUR 2Source: AdvaMed, “Global Medical Device Recall Index,” advamed.org307" class="citation-tooltip" aria-label="Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com"> 1Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com. 2Source: AdvaMed, “Global Medical Device Recall Index,” advamed.org307" class="citation-tooltip" aria-label="Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com"> 1Emergo by UL, “Notified Body Survey: MDR Certification Numbers,” emergobyul.com8 billion is earmarked for replacement of aging capital equipment, ensuring steady renewal cycles within the Italian cardiovascular devices market. Hospitals also benefit from close collaboration with national cardiology societies, which issue adoption-guideline updates influencing purchasing patterns.

Integrated home care services, however, are the fastest-growing channel. The Italian cardiovascular devices market now sees brisk demand for Bluetooth-enabled sphygmomanometers, single-lead ECG patches and cloud-linked rhythm monitors that permit cardiologists to adjust therapy remotely.

Geography Analysis

Northern Italy captures the lion’s share of the Italian cardiovascular devices market, buoyed by dense networks of academic hospitals and private centers equipped for advanced interventions. Regions such as Lombardy and Emilia-Romagna host early adopters of AI-assisted imaging and robotic surgery platforms, reinforcing premium-equipment turnover.

Central Italy, anchored by Lazio and Tuscany, is experiencing an uptick in device procurement as public–private partnerships finance hybrid operating rooms and structural-heart programs. These projects leverage recovery-plan grants to introduce shared service models, thus broadening patient access to cutting-edge procedures.

Southern Italy continues to report higher cardiovascular risk profiles yet historically lower device utilization. Targeted recovery-plan allocations for telemedicine and portable diagnostics are beginning to bridge gaps, while national STEMI networks promote uniform protocol adoption for primary PCI. As digital literacy improves, the Italian cardiovascular devices market is poised for above-average growth in the south, narrowing historical disparities.

Competitive Landscape

Competitive Landscape

Global multinationals, including Medtronic, Abbott, Boston Scientific and Edwards Lifesciences, occupy leading positions in the Italian cardiovascular devices market through comprehensive portfolios and service-based contracting. Their strategies increasingly revolve around bundled pricing, remote-therapy support and data analytics that align with value-based purchasing models. Recent CE-mark approval of the Sapien 3 Ultra RESILIA valve demonstrates ongoing product refreshment to combat price compression.

Domestic manufacturers, mainly small and medium enterprises, succeed in niche hardware and custom components, leveraging local clinical ties and rapid prototyping. EU-MDR compliance costs have prompted some to seek distribution alliances or pursue specialization in low-volume, high-complexity devices. The Italian cardiovascular devices market logged 153 recall notices in Q4 2024, underscoring regulators' close watch and the competitive advantage of robust quality systems.

SMT's national TAVI tender win challenges incumbents by offering cost-constrained hospitals an alternative valve system. Edwards Lifesciences' planned integration of JenaValve positions it to serve patients with aortic regurgitation once EU approval materializes. Boston Scientific introduced the DIRECTSENSE thermal-monitoring module to improve ablation precision in electrophysiology labs.

Italy Cardiovascular Devices Industry Leaders

-

Abbott Laboratories

-

Boston Scientific Corporation

-

GE Healthcare

-

Medtronic PLC

-

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: SMT secured a two-year national tender to supply the Hydra TAVI system to Italian hospitals.

- March 2024: Abbott received European approval for its six-year battery Jot Dx insertable cardiac monitor.

- May 2024: Abbott received European approval for its six-year battery Jot Dx insertable cardiac monitor.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every diagnostic, monitoring, therapeutic, and surgical device deployed to detect or treat cardiac and peripheral vascular disorders in Italian patients, including ECG monitors, cardiac CT and ultrasound systems, remote telemetry hubs, stents, valves, pacemakers, implantable cardioverter-defibrillators, ventricular assist devices, grafts, and interventional catheters.

Scope Exclusion: Pharmaceuticals, standalone software without a hardware component, and veterinary cardiovascular equipment are excluded.

Segmentation Overview

-

By Device

-

Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

-

Therapeutic & Surgical Devices

-

Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

-

Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

-

Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

-

Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

-

Coronary Stents

-

Diagnostic & Monitoring Devices

-

By Indication

- Coronary Artery Disease

- Arrhythmia

- Heart Failure

- Valvular Heart Disease

-

By End User

- Hospitals

- Home care Settings

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with interventional cardiologists, catheter-lab managers, procurement leads, and home-care clinicians across the North, Center, and South.

These discussions validated average selling prices, replacement cycles, and the impact of Consip price ceilings.

Quick polls with distributors then gauged supply gaps linked to EU-MDR recertification delays.

Desk Research

We began with procedure and mortality files from ISTAT, Eurostat, and the Italian Ministry of Health, paired with import and export tallies from UN Comtrade and device approvals logged in EUDAMED.

Insights from the European Heart Network, national cardiology registries, and peer-reviewed journals shaped adoption curves.

Paid datasets, chiefly D&B Hoovers for company splits and Dow Jones Factiva for price trends, refined revenue allocations.

The sources named illustrate, not exhaust, our desk inputs.

Market-Sizing & Forecasting

A top-down model rebuilt demand from national angioplasty, valve, and rhythm-device procedure counts, layered with penetration ratios and device mix.

Supplier roll-ups and sampled ASP × volume checks supplied a bottom-up reality check, closing visible gaps.

Key drivers in the multivariate regression include 65-plus population growth, elective-surgery backlog clearance, home telemetry uptake, average Consip discounts, and euro-dollar shifts.

Where primary data were thin, conservative substitution anchored estimates before final triangulation.

Data Validation & Update Cycle

Outputs face automated variance flags, peer review, and senior sign-off.

Models refresh annually, with interim tweaks when reimbursement rules, major recalls, or macro shocks alter demand.

Why Mordor's Italy Cardiovascular Devices Baseline Commands Reliability

Published values differ because firms slice the market, apply unique price decks, and refresh models on different clocks. We show our scope, inputs, and checks so clients can trace every number.

Key gap drivers include certain studies that bundle imaging capital equipment, others that omit diagnostic ECG and home telemetry; some still rely on 2022 exchange rates or locked ASPs, which skews totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.9 billion (2025) | Mordor Intelligence | - |

| USD 2.0 billion (2024) | Regional Consultancy A | Adds imaging systems and service contracts |

| €1.2 billion (2025) | Trade Journal B | Excludes diagnostics, uses fixed 2022 fx |

| €1.5 billion (2023) | Global Consultancy C | Factory shipments only |

These contrasts show that our disciplined scope, multilevel checks, and yearly refresh supply a balanced, repeatable baseline for confident planning.

Key Questions Answered in the Report

What is the current Italy Cardiovascular Devices Market size?

The Italy Cardiovascular Devices Market is projected to register a CAGR of 5.75% during the forecast period (2026-2031)

Who are the key players in Italy Cardiovascular Devices Market?

Abbott Laboratories, Boston Scientific Corporation, GE Healthcare, Medtronic PLC and Siemens Healthineers AG are the major companies operating in the Italy Cardiovascular Devices Market.

What years does this Italy Cardiovascular Devices Market cover?

The report covers the Italy Cardiovascular Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Italy Cardiovascular Devices Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: