Dishwashing Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 26.06 Billion |

| Market Size (2031) | USD 30.79 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

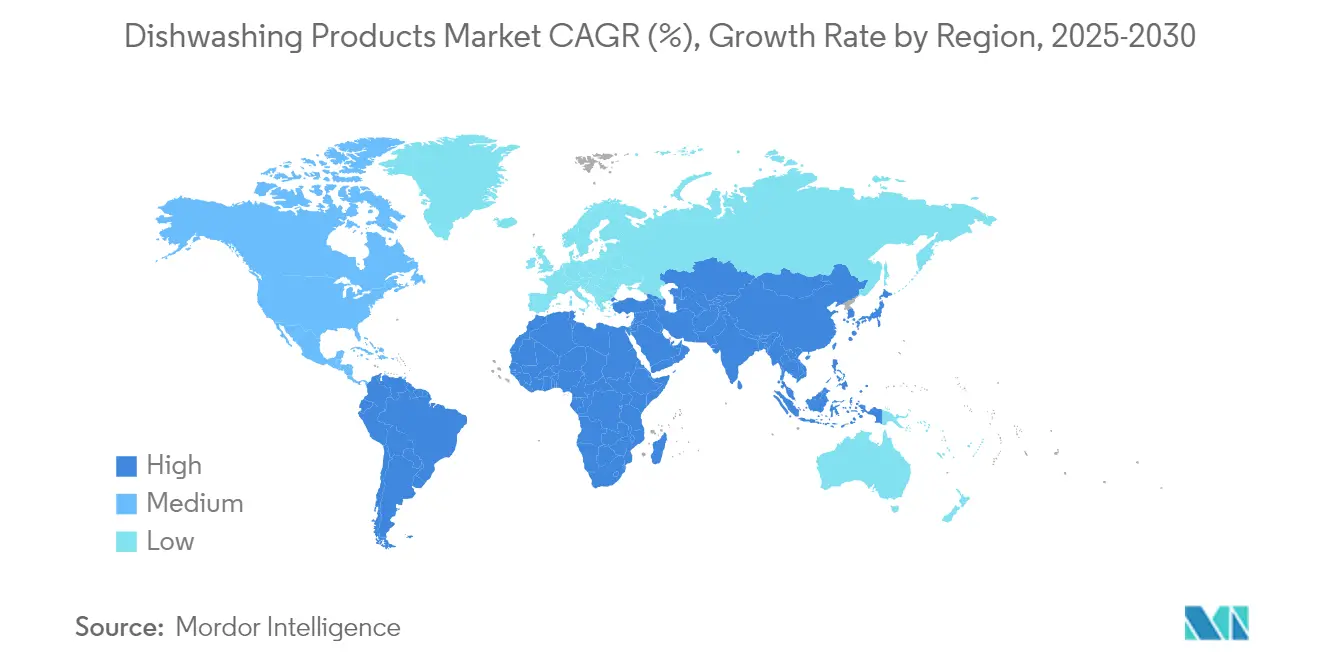

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

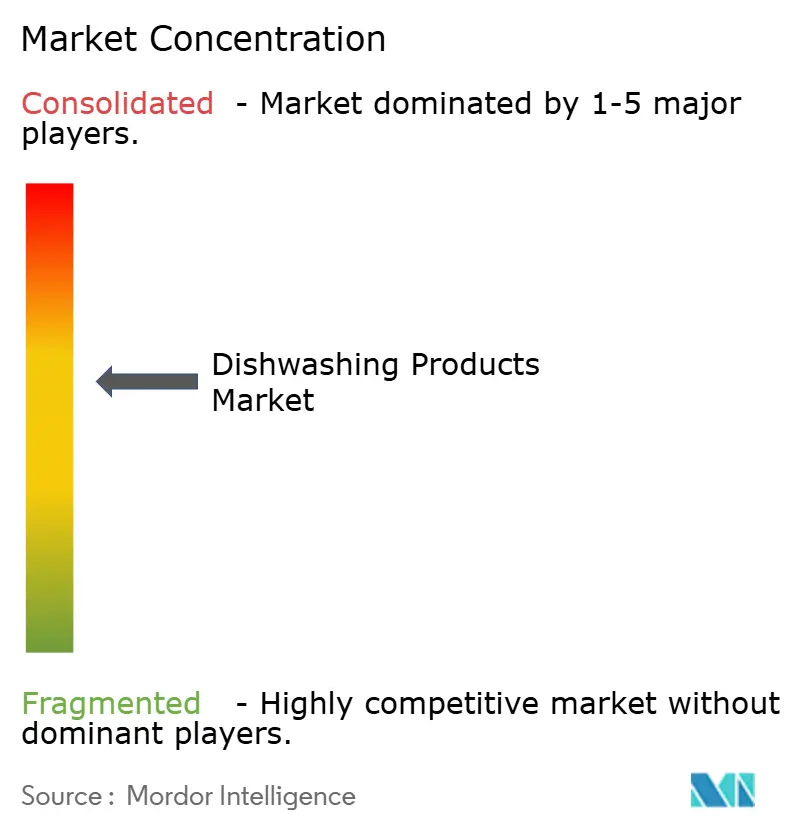

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dishwashing Products Market Analysis by Mordor Intelligence

Dishwashing products market size in 2026 is estimated at USD 26.06 billion, growing from 2025 value of USD 25.21 billion with 2031 projections showing USD 30.79 billion, growing at 3.39% CAGR over 2026-2031. Market growth is driven by rising hygiene awareness, health consciousness, and social media endorsements. Emerging economies show steady growth, while mature regions face slower expansion due to high household penetration. Liquid dishwashing products dominate, but concentrated pods and organic options are gaining popularity due to health and eco-friendly trends. Adults drive most demand, with growing interest in child-friendly products. Supermarkets and hypermarkets remain key sales channels, though online sales are rapidly increasing due to convenience. Sustainable packaging, like refill pouches, is becoming popular. In Europe, strict environmental regulations are driving investments in sustainable product design and packaging. The market is moderately concentrated, with Procter & Gamble, Unilever, and Reckitt leveraging strong brands, procurement networks, and research and development to stay competitive.

Key Report Takeaways

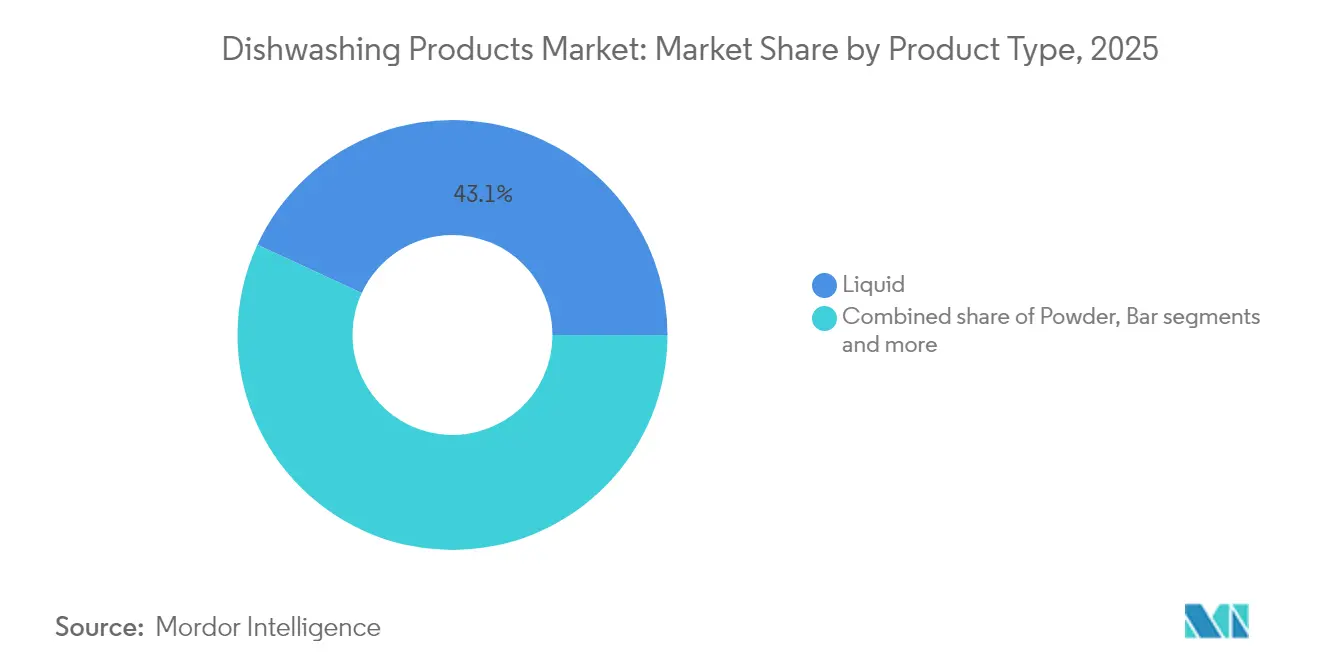

- By product type, liquid cleaners held 43.10% of the dishwashing products market share in 2025, are set to post the fastest 3.55% CAGR through 2031.

- By ingredient profile, conventional products retained 82.10% revenue share in 2025; natural and organic alternatives are forecast to expand at a 3.86% CAGR to 2031.

- By end user, adults accounted for 94.40% of demand in 2025, yet formulations for children are growing at a 4.12% CAGR on the back of skin-sensitive positioning.

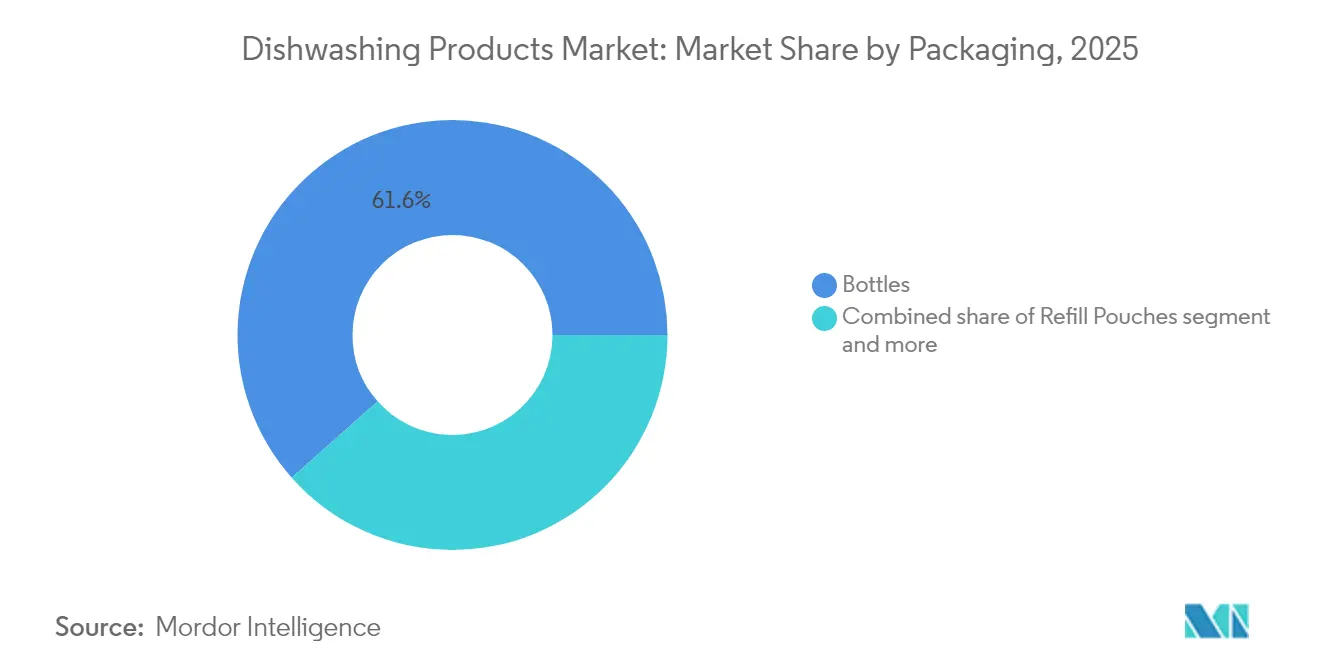

- By packaging format, bottles dominated with 61.55% share in 2025; refill pouches are the fastest-growing format at a 4.61% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets controlled 44.90% of 2025 sales, whereas online retail stores are on track for a 4.87% CAGR to 2031.

- By geography, Europe led with 32.10% revenue share in 2025, while Asia-Pacific is projected to grow the quickest at 5.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dishwashing Products Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hygiene awareness and health consciousness | +0.8% | Global, with stronger impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Innovation in eco-friendly formulations and packaging | +0.6% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in dishwashing products | +0.5% | Global, led by developed markets | Long term (≥ 4 years) |

| Travel and convenience-driven consumption | +0.4% | Europe and North America primarily | Medium term (2-4 years) |

| Social media influence and endorsements | +0.3% | Global, strongest in urban markets | Short term (≤ 2 years) |

| Increasing adoption of dishwashers | +0.7% | Asia-Pacific core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising hygiene awareness and health consciousness

Hygiene awareness and health consciousness are driving the dishwashing products market. Consumers prefer premium products with antimicrobial benefits and safer, clearly labeled ingredients. In response to 2024 P&G research identifying dishwashing as a disliked chore, Dawn launched Dawn PowerSuds, offering double the suds to trap grease and reduce residue transfer. Brands like Ecover are adopting plant-based surfactants for effective cleaning without harsh chemicals. Advancements in biological cleaning agents are enhancing germ protection, boosting multifunctional product demand. As of 2024, with 55% of the global population in urban areas (projected to reach 68% by 2050, per the United Nations), urban consumers favor convenient formats like pods and sprays [1]Source: Urban Population, "68% of the world population is projected to live in urban areas by 2050, says the UN",un.org. Products such as Finish Quantum Ultimate and Method Dish Spray are gaining popularity for their ease of use and transparent marketing.

Innovation in eco-friendly formulations and packaging

In Europe, strict sustainability regulations are driving rapid growth in eco-friendly dishwashing products and packaging. Companies are investing in research and development to develop 100% bio-based products, such as Sunlight’s 2024 plant-based product line. Brands like Ecover and Seventh Generation are adopting concentrated refills and recyclable packaging, reducing plastic waste and shipping emissions while supporting recycling programs. Enzyme technologies from companies like Novozymes enable effective cleaning at lower temperatures and shorter wash cycles, saving energy and water. Products like Finish Eco Dishwasher Tablets and Method’s Plant-Based Dish Soaps reflect this trend. These practices help brands secure premium shelf space and align with circular economy goals, though smaller manufacturers face challenges due to high transition costs.

Technological advancements in dishwashing products

Advanced technologies are enhancing dishwashing products, improving effectiveness and convenience. Innovations like enzymatic blends, microbial boosters, and water-hardness stabilizers boost compact pod performance. For instance, the 2024 launch of Finish Quantum Infinity Shine offers precise dosing and easy storage. Fragrance innovation is also a focus, with products like Cascade Platinum Plus featuring advanced scent-release technologies. Eco-friendly options, such as Sunlight dishwashing liquid, deliver excellent cleaning using 100% plant-based, renewable, and biodegradable ingredients. These advancements meet consumer demands for convenience, effectiveness, and sustainability, keeping brands competitive.

Travel and convenience-driven consumption

With busy lifestyles and frequent travel becoming more common, there is a growing need for dishwashing products that are easy to carry and use. According to the United Nations, in 2024, international tourism saw a significant rebound, with approximately 1.4 billion people traveling internationally [2]Source: International Tourism, "International tourism recovers pre-pandemic levels in 2024", unwto.org. Compact options like small sachets, pre-measured pods, and portable sprays are gaining traction for their lightweight nature and ease of fitting into bags or luggage. These products cater especially to travelers, be it backpackers, campers, or families on road trips, by saving space and simplifying dish cleaning on the go. For example, small sachets serve as a perfect solution for short trips, camping, or picnics. They're particularly beneficial for solo travelers seeking a quick dishwashing solution while traveling. In countries such as India and Indonesia, where affordability and daily purchases are the norm, brands have rolled out these budget-friendly and travel-friendly small sachets and compact refill packs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for traditional alternatives | -0.4% | Global, stronger in rural and developing markets | Medium term (2-4 years) |

| Availability of counterfeit products | -0.3% | APAC and MEA primarily, emerging in online channels | Short term (≤ 2 years) |

| High production costs | -0.5% | Global, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Price fluctuation in raw material | -0.6% | Global, with regional supply chain variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products

Counterfeit dishwashing products remain a significant challenge in the market. UNCTAD reports that as of 2025, 44% of its member countries lack adequate consumer-safety regulations, enabling counterfeit detergents to spread across physical stores and online platforms [3]Source: Consumer Product Safety, "Emerging trends and challenges in consumer product safety", unctad.org. These products often mimic reputable brands but contain substandard or harmful ingredients, endangering consumer health and damaging trusted manufacturers' reputations. The presence of counterfeits also forces legitimate companies to lower prices, disrupting market equilibrium. To address this, companies like Procter & Gamble and Henkel are implementing measures such as unique product codes, tamper-proof packaging, and QR codes for authenticity verification. Additionally, brands are educating consumers through websites and social media, urging them to buy only from authorized retailers. These efforts aim to protect consumers and uphold market integrity.

Consumer preference for traditional alternatives

In rural and semi-urban areas, families often rely on homemade cleaning solutions made from natural ingredients like citrus extracts, coconut oil, aloe vera, and ash. These options are seen as safer, more natural, and more affordable compared to commercial dishwashing products. This preference is strongly tied to cultural traditions, where natural cleaning methods have been passed down through generations and are valued for their simplicity and perceived health benefits. As a result, branded dishwashing products face challenges in gaining acceptance and achieving widespread use in these regions. To address this, companies need to design marketing strategies that respect and acknowledge these local cleaning habits. By educating consumers about the additional benefits of modern products, such as better hygiene, ease of use, and time-saving features, manufacturers can gradually build trust and encourage people to try these products. Without such efforts, it will remain difficult for companies to expand their presence and increase adoption in these markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Leadership and Pod Convenience

In 2025, liquid cleaners dominated the dishwashing products market, capturing 43.10% of the revenue share and projected to grow at a CAGR of 3.55% through 2031. Their versatility across varying water hardness levels and widespread consumer familiarity, both for manual and machine dishwashing, bolsters their steady demand amidst the rise of new product formats. Emerging contenders like concentrated pods, dissolvable film powders, and spray-on pre-treatments are gaining traction. Marketed as mess-free, eco-friendly, and easy to store, these formats resonate with urban consumers valuing convenience. The inclusion of biological additives enables these products to excel in cold washes, positioning pods as a premium choice.

In response to the pod trend, liquid cleaner brands are enhancing their offerings with potent formulas, appealing fragrances, and initiatives like recyclable bottle programs to combat plastic waste. A case in point: Ecover unveiled its concentrated liquid dish soap line, packaged in 100% recycled plastic bottles topped with 50% recycled caps, merging eco-friendliness with superior cleaning. In regions grappling with hard water, powders retain their significance due to their stain-removing alkaline properties. On the other hand, environmentally-conscious consumers gravitate towards bar soaps for their minimal packaging. This product diversification strategy not only broadens the customer base but also solidifies the supremacy of liquid cleaners, suggesting a harmonious coexistence of product types in the market.

By Ingredients: Conventional Scale Meets Natural Momentum

Conventional synthetic formulations accounted for the largest market share of 82.10% in 2025. Their popularity is driven by their well-established supply chains and proven ability to clean tough grease and heavily soiled cookware effectively. Consumers widely trust these products for their consistent performance. However, natural and organic products are gaining traction, with a projected CAGR of 3.86%. Stricter European regulations, such as the ban on phosphates, and the increasing demand for private-label products in North America, fuel this growth. To meet these changing demands, leading brands are now incorporating sugar-based surfactants and coconut-derived foaming agents while gradually eliminating phosphates to align with sustainability goals.

Advancements in product development are helping natural products improve their cleaning performance, although they still face challenges in handling heavy grease and adapting to different water hardness levels. Hybrid formulations, which combine plant-based ingredients with enzyme boosters, are emerging as a practical solution. These products offer strong cleaning power while being environmentally friendly, making them appealing to eco-conscious consumers. Additionally, brands are sourcing local ingredients like coconut oil and aloe vera in regions such as India and Southeast Asia to cater to regional preferences and reduce costs. Looking ahead, clear labeling of ingredients and certifications, such as eco-friendly or organic seals, are expected to play a more significant role in influencing consumer buying decisions.

By End User: Adult Stability and Children-Focused Growth

Adults are the primary users of dishwashing products, accounting for 94.40% of total consumption in 2025. This is because adults typically handle household shopping and kitchen cleaning tasks. They prefer products that are effective at removing grease and leave behind pleasant scents like citrus or lavender. For example, brands like Dawn and Palmolive cater to these needs by offering powerful grease-fighting formulas with fresh, appealing fragrances. These products are designed to make cleaning faster and easier, which is especially important for busy households. Additionally, the availability of concentrated formulas and refill packs from these brands adds convenience and cost-effectiveness, making them even more popular among adult users.

In contrast, the children’s segment is smaller but growing steadily, with an expected CAGR of 4.12%. This growth is driven by parents who prioritize safer and gentler dishwashing options for their children, such as hypoallergenic or dye-free liquids and foams. For instance, brands like Babyganics and Dapple focus on creating child-friendly products with tear-free and non-toxic formulations. Companies are also introducing features like ergonomic pumps and colorful packaging to make these products easier and safer for kids to use. Claims such as "gentle on skin" or "dermatologist-tested" are particularly appealing to parents concerned about skin sensitivity. While these products are more common in developed markets, awareness is increasing in emerging economies.

By Packaging: Bottles Dominate as Refills Rise

Bottles made up 61.55% of the revenue in 2025 due to their convenience and ease of use. They are practical for dispensing liquids and work well with existing filling systems. Many consumers prefer bottles because they allow better control over the amount of product used, thanks to improved cap designs. For instance, Fairy’s Platinum Plus dishwashing liquid introduced a “no-mess dosing cap” that dispenses the exact amount needed for each wash. This feature helps households avoid wasting product, saving money while being environmentally friendly. Bottles remain a popular choice for their functionality and user-friendly designs, making them a staple in the dishwashing products market.

On the other hand, refill pouches are gaining popularity, growing at a CAGR of 4.61%, as more consumers look for eco-friendly and cost-effective options. These pouches help reduce plastic waste and are often promoted by retailers through in-store refill stations, where customers can reuse durable containers. This aligns with the growing zero-waste movement. For example, brands like Method and Ecover offer refill pouches that allow consumers to refill their bottles at home, reducing the need for single-use plastics. Additionally, innovations like water-soluble wrappers for powder tablets and lightweight, recyclable pumps are becoming more common. Companies like Grove Collaborative, which acquired Grab Green in February 2025, are investing in sustainable packaging solutions that not only reduce environmental impact but also maintain a premium look on store shelves.

By Distribution Channel: Store Strength and Online Acceleration

Supermarkets and hypermarkets continue to dominate as the main sales channels, holding a 44.90% market share in 2025. These outlets are popular because they offer a wide variety of products, attractive promotional displays, and the convenience of immediate purchase. For example, stores like Walmart and Carrefour often feature discounts or bundle deals on dishwashing products, encouraging bulk purchases. The ability to physically inspect products before buying makes these stores a preferred choice for many consumers. Seasonal sales during holidays or special events, like Christmas or Black Friday, further boost sales in these stores. The availability of well-known brands and the ease of access make supermarkets and hypermarkets a go-to option for many consumers.

On the other hand, online retail is growing rapidly, with an expected CAGR of 4.87% through 2031. This growth is driven by the convenience of home delivery and the rise of subscription services that ensure automatic restocking of dishwashing products. For instance, platforms like Amazon and Instacart allow customers to easily compare prices and access niche, eco-friendly brands that may not be available in physical stores. Hybrid models, such as click-and-collect services offered by retailers like Target, combine the ease of online shopping with the option to pick up products in-store. These strategies are helping manufacturers and retailers expand their reach while providing consumers with more flexible shopping options.

Geography Analysis

In 2025, Europe captured 32.10% of the revenue share, driven by strict eco-design regulations, high dishwasher ownership, and consumer demand for sustainable products. Circular-economy laws are pushing companies to use recyclable materials and low-carbon processes. Brands like Finish and Ecover have introduced eco-friendly packaging and biodegradable formulas. In Western Europe, saturated markets are focusing on unique fragrances and skin-friendly claims. Regional material sourcing is helping manufacturers reduce costs and stay competitive in price-sensitive markets.

The Asia-Pacific region is set to grow at the highest CAGR of 5.25%, fueled by rising disposable incomes, a growing younger middle class, and urbanization in countries like China, India, and Vietnam. Smaller households and fast-paced lifestyles are driving demand for dishwashers and ready-to-use solutions. In 2024, the dishwasher sector recorded CNY 11 billion in annual retail sales, with a 2.9% penetration rate, highlighting growing adoption and detergent demand . In price-sensitive markets like India, manufacturers are offering affordable options such as concentrated sachets and small-pack refills.

North America shows stable sales and a growing preference for premium, plant-based dishwashing pods. Potential plastic taxes and producer responsibility policies may impact packaging strategies, with brands like Seventh Generation adopting sustainable packaging. South America and Africa, though smaller markets, are growing, driven by urbanization and retail modernization. Challenges like limited infrastructure and counterfeit products persist, prompting companies to partner with trusted distributors and run educational campaigns promoting hygienic dishwashing products over traditional methods.

Competitive Landscape

The dishwashing products market is moderately consolidated, led by Procter & Gamble, Unilever, and Reckitt. These companies rely on strong brands, large-scale production, and R&D investments to maintain their positions but face competition from private-label brands and eco-friendly startups like Dropps and Blueland. Private-label brands benefit from retailer partnerships, while startups attract consumers with sustainable products like plastic-free pods. To stay competitive, established firms are focusing on eco-friendly technologies, digital marketing, and acquiring niche brands to meet the preferences of environmentally conscious consumers.

Technology is a key differentiator in the dishwashing products market. Novozymes provides enzymes for biodegradable detergents with effective grease removal, while innovations like fragrance microcapsules enable premium products with lasting freshness. E-commerce analytics help brands like Procter & Gamble and Unilever run targeted campaigns, boosting customer loyalty and promoting complementary products like rinse aids. Procter & Gamble uses data-driven strategies to enhance its online presence and sales.

Merger and acquisition activities are reshaping the market. First Quality acquired Henkel’s private-label business to strengthen its retailer brand segment, while Grove Collaborative purchased Grab Green to expand its eco-friendly offerings. Reckitt is considering selling its Essential Home division to focus on healthcare. Large companies benefit from cost advantages in packaging and enzyme sourcing, while mid-sized innovators adapt to environmental regulations and offer sustainable solutions like refillable packaging and plant-based cleaners, driving growth among eco-conscious consumers.

Dishwashing Products Industry Leaders

-

The Procter & Gamble Company

-

Unilever Plc

-

Henkel AG & Co. KGaA

-

Reckitt Benckiser Group PLC

-

Colgate-Palmolive Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cascade launches its upgraded Platinum Plus detergent, designed to remove up to 100% of food and deliver a near-spot-free shine, addressing concerns like stuck-on residue and tough grease.

- February 2025: Dawn introduced its most effective liquid dish soap yet, featuring double the suds. The new Dawn PowerSuds formula creates twice as many bubbles, which trap grease and prevent residue from spreading across dishes.

- October 2024: Unilever SA, a leading dishwashing detergent manufacturer, rolled out Sunlight’s 100% plant-based technology across multiple markets.

- October 2024: Dropps, a certified B Corporation and a leader in home care innovation, introduced its new UltraWash Plus Biobased Power Dishwasher Detergent Pods. This product is the first multi-chamber dishwasher detergent pod that combines advanced cleaning technology with a USDA Certified Biobased formulation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global dishwashing products market as liquids, powders, bars, gels, and tablets formulated to remove food soils from household and institutional crockery, cookware, and cutlery. Values capture only consumables and are expressed in current US dollars.

Scope exclusion: Automatic dishwashers, scouring tools, brushes, and rinse aids are outside this valuation.

Segmentation Overview

-

By Product Type

- Powder

- Liquid

- Bar

- Other Product types

-

By Ingredients

- Conventional

- Natural and Organic

-

By End User

- Adult

- Kids/Children

-

By Packaging

- Bottles

- Refill Pouches

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Others Distribution Channel

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interview formulation chemists, supermarket buyers, private-label procurement heads, and regional distributors across Asia-Pacific, Europe, and the Americas. Their insights fine-tune usage frequency, eco-label traction, channel mix, and prevailing selling prices, closing gaps flagged during desk work.

Desk Research

Mordor analysts begin with hard numbers released by public bodies. We map HS-3402 trade flows from UN Comtrade, production volumes from Eurostat PRODCOM, and consumer price files from the US Bureau of Labor Statistics. Usage cues arrive from the American Cleaning Institute and AISE. Company 10-Ks, investor decks, and patent logs accessed through Questel reveal innovation pivots, while news indexed on Dow Jones Factiva and shipment traces on Volza cross-check regional supply shifts. These references are illustrative; many additional open records inform our master sheet.

Market-Sizing & Forecasting

Modeling opens with a top-down consumption build that links household counts, dish-cleaning frequency, and spend per wash to produce regional demand pools. Selective bottom-up roll-ups of supplier revenues and sampled average prices then test the totals. Key drivers, such as dishwasher penetration, disposable income, liquid-to-tablet substitution, raw-material cost curves, surfactant regulation, and e-commerce share, feed a multivariate regression that projects demand to 2030. When supplier splits remain patchy, we apply rolling three-year averages before final triangulation.

Data Validation & Update Cycle

Every model passes variance scans, multi-analyst review, and leadership sign-off. Reports refresh once a year, and interim updates trigger when raw-material spikes or demand shocks cross preset thresholds.

Why Mordor's Dishwashing Products Baseline Commands Solid Decision Reliability

Published estimates often differ because some publishers bundle accessories, apply one global price, or freeze exchange rates for long periods. Our disciplined scope, quarterly FX updates, and annual refresh narrow that drift.

Key gap drivers include the inclusion of brushes and rinse aids by certain publishers, aggressive dishwasher uptake curves, and untested price-lift assumptions; Mordor keeps strictly consumables, moderates penetration paths, and recalibrates core variables each cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.21 Bn (2025) | Mordor Intelligence | |

| USD 43.67 Bn (2025) | Global Consultancy A | Adds accessories, uses single global price |

| USD 47.34 Bn (2025) | Industry Think Tank B | Expects rapid dishwasher uptake with no moderation |

| USD 24.60 Bn (2025) | Trade Journal C | Uses historic FX rates and limited primary checks |

Together, the comparison shows our clear variables, steady refresh cadence, and transparent steps deliver a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the dishwashing products market?

The dishwashing products market is valued at USD 26.06 billion in 2026 and is forecast to reach USD 30.79 billion by 2031.

Which product type dominates global sales?

Liquid formulations lead with 43.10% share, owing to their versatility across hand and machine washing.

Which region is expanding the quickest?

Asia-Pacific is projected to grow at a 5.25% CAGR, driven by urbanization, rising incomes and higher dishwasher penetration.

How are brands responding to stricter environmental rules?

Manufacturers invest in plant-based surfactants, enzyme boosters and recyclable packaging to comply with evolving regulations and meet consumer expectations

Page last updated on: