Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.99 Billion |

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.42 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Architectural Coatings Market Analysis by Mordor Intelligence

The Italy architectural coatings market size is expected to increase from USD 1.99 billion in 2025 to USD 2.06 billion in 2026 and reach USD 2.42 billion by 2031, growing at a CAGR of 3.28% over 2026-2031. Following the withdrawal of the 110% Superbonus, demand has stabilized, focusing on upgrades for owner-occupied homes, refurbishments in tourism-related hospitality, and a gradual renewal of housing built before 1970. As the European Union (EU) Ecolabel tightens emission limits, water-borne, low-VOC formulations are capturing a larger market share. However, the industry grapples with challenges: spikes in titanium dioxide costs and labor shortages are impacting profit margins and project timelines. Yet, buoyed by resilient data on building permits and construction output, the underlying activity remains strong. To bolster their competitive edge, multinationals are investing in color-automation laboratories, expanding powder-coating lines, and forming partnerships for bio-attributed resins. In contrast, domestic brands are capitalizing on their heritage and credentials in circular packaging.

Key Report Takeaways

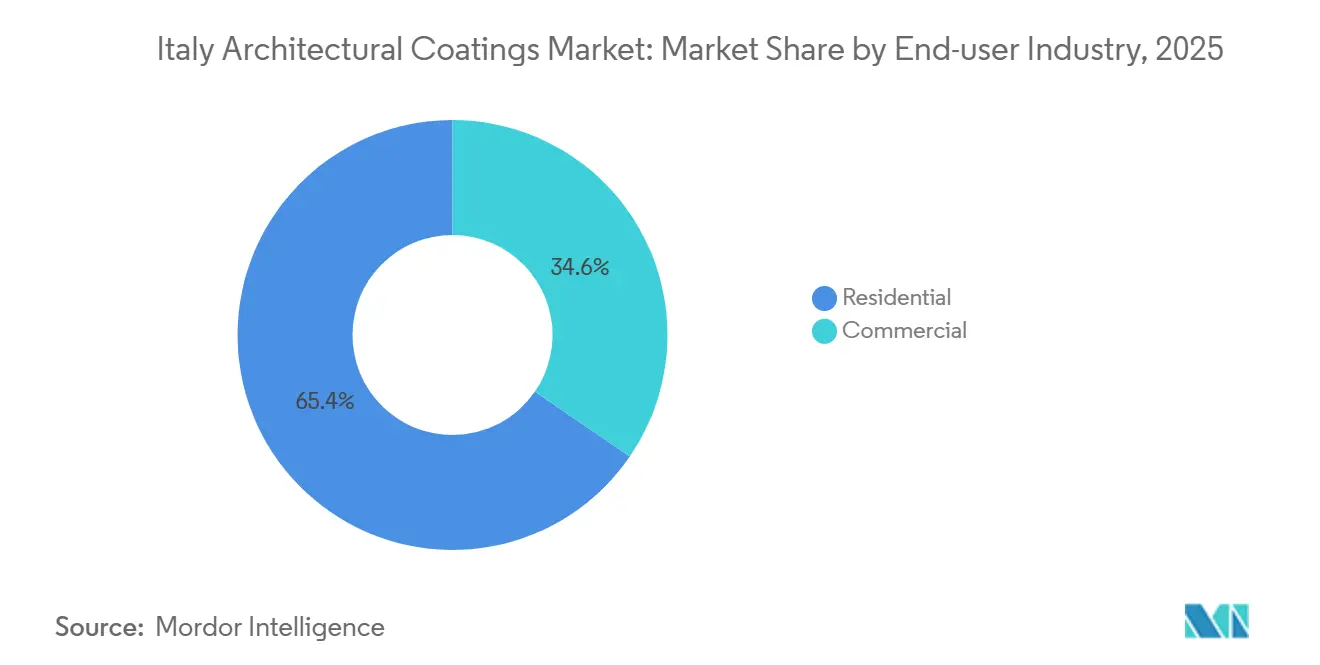

- By end-user industry, the residential segment held 65.44% of the Italy architectural coatings market share in 2025 and is projected to expand at a 3.84% CAGR from 2026 to 2031.

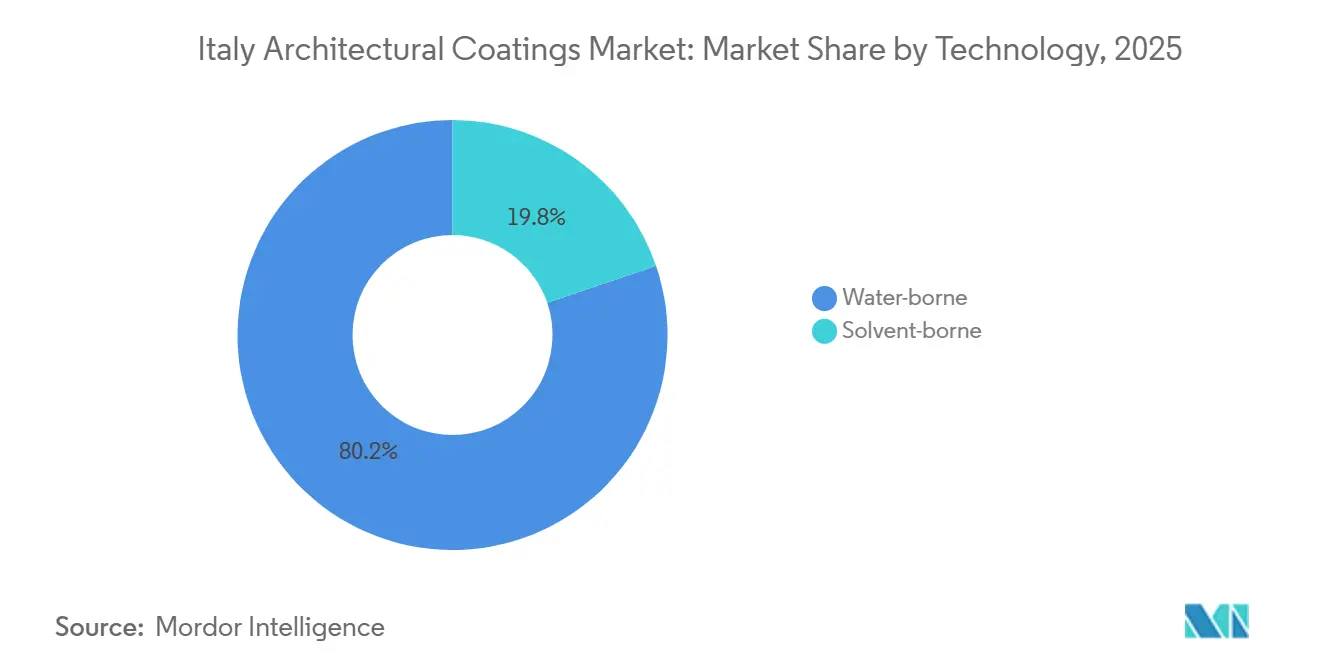

- By technology, water-borne coatings captured 80.22% of the Italy architectural coatings market size in 2025 and are advancing at a 4.04% CAGR from 2026 to 2031.

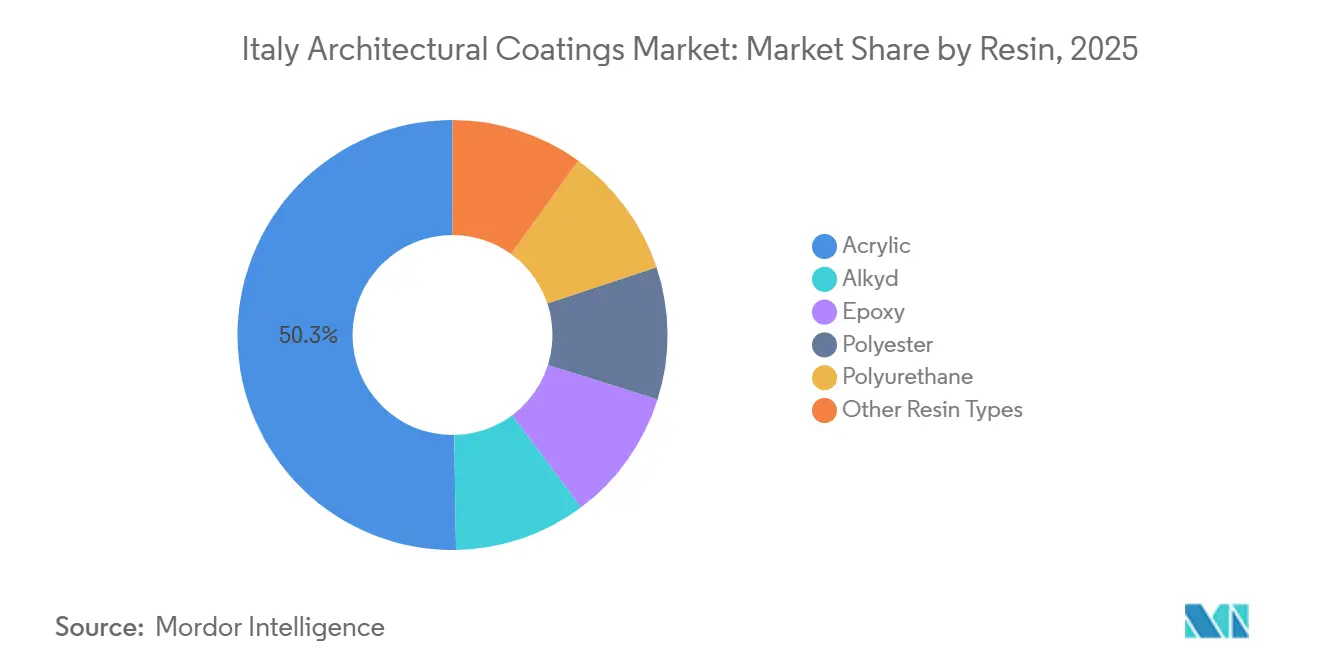

- By resin, acrylics commanded 50.26% of the Italy architectural coatings market share in 2025 and are set to grow at a 3.97% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid refurbishment of pre-1970 housing stock | +1.2% | National, with concentration in Lombardy, Piedmont, Veneto, Emilia-Romagna | Long term (≥ 4 years) |

| Growth of Italy's professional paint applicator networks | +0.6% | National, urban centers (Milan, Rome, Turin, Bologna) | Medium term (2-4 years) |

| Rebound in tourism-related construction (hotels, cultural sites) | +0.8% | National, with emphasis on Milan, Rome, Florence, Venice, coastal regions | Medium term (2-4 years) |

| Rising DIY culture fueled by e-commerce tutorials | +0.4% | National, suburban and rural areas | Short term (≤ 2 years) |

| Government "Superbonus 110%" extension for energy-efficient facades | +0.3% | National, owner-occupied principal residences | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Refurbishment of Pre-1970 Housing Stock

In Italy, nearly 70% of homes predate 1970, and over 70% fall short of energy class C standards[1]ENEA, “Rapporto Annuale Efficienza Energetica 2025,” enea.it. Despite the conclusion of the 110% incentive, a continued 50% deduction for primary residences makes energy upgrades appealing. This has driven regions like Lombardy, Piedmont, Veneto, and Emilia-Romagna to increasingly adopt breathable mineral renders, anti-damp systems, and acrylics compatible with insulation. The Organisation for Economic Co-operation and Development (OECD) projects a need of EUR 792 billion (USD 860 billion) to elevate the current housing stock to near-zero energy standards, creating sustained demand for premium façade and interior coatings.

Growth of Italy’s Professional Paint-Applicator Networks

The increasing demand for precise coating sequences in heat-pump installations and multilayer insulation systems is driving the growth of certified applicator networks in Milan, Rome, Turin, and Bologna. Manufacturers are offering onsite training, digital color-matching, and technical hotlines to support this growth. However, a gap in skilled labor continues to delay intricate façade projects, particularly those involving historic masonry. PPG's EUR 2 million laboratory in Milan, which can produce 100,000 color matches each year, highlights the support suppliers are providing to applicators[2]PPG, “PPG Opens Color Automation Laboratory in Milan,” ppg.com .

Rebound in Tourism-Related Construction (Hotels, Cultural Sites)

In Q3 2025, non-residential permits surged by 11.1% year-on-year, driven by hotels, restaurants, and cultural sites hastening refurbishments to seize the momentum of post-pandemic travel. Additionally, National Recovery and Resilience Plan (PNRR) funds are channeling investments into seismic safety and art-storage enhancements at venues like Matera and Venaria Reale. These upgrades necessitate specialized materials, including breathable mineral paints, anti-graffiti topcoats, and moisture-barrier primers. Meanwhile, escalating house prices in Genoa, Rome, and Turin are spurring increased private spending on decorative finishes.

Government Incentives for Energy-Efficient Façades

In 2025, projects that secured permits before mid-October 2024 will continue to benefit from a 65% deduction, bolstering the demand for façade coatings and external thermal insulation composite systems (ETICS). The deduction structure, adjusted from 36%-30% for 2025-2027, is heightened to 50%-36% specifically for owner-occupied homes, ensuring a steady demand for envelope upgrades. To qualify, products must be low-VOC and Ecolabel-compliant, which is hastening the industry's pivot towards water-borne acrylics and powder-coated architectural metals.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in titanium-dioxide prices | -0.5% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Strict VOC limits under EU Green Deal revisions | -0.3% | National, EU-wide compliance | Medium term (2-4 years) |

| Skilled labor shortage in building restoration trade | -0.4% | National, acute in Northern regions (Lombardy, Piedmont, Veneto) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Titanium-Dioxide Prices

Architectural coatings rely heavily on titanium dioxide, the leading white pigment, which constitutes a significant portion of raw material expenses. Prices for titanium dioxide have been volatile, a situation worsened by the EU's imposition of anti-dumping duties on imports. These duties along with energy surcharges and emissions-disclosure regulations have inflated pigment costs. This surge in costs has further squeezed margins for Italian formulators, who are already grappling with a tepid demand for renovations. While the JRC highlights titanium dioxide's dominance in environmental impact categories, a potential switch to zinc sulfide doesn't alleviate the challenges, leaving manufacturers vulnerable.

Strict VOC Limits Under EU Green Deal Revisions

In December 2025, the European Commission rolled out updated EU Ecolabel criteria for decorative paints and varnishes, setting a validity until December 31, 2032. These revisions introduce stricter thresholds for volatile organic compounds (VOC) and semi-volatile organic compounds (SVOC) content, tighten limits on preservatives, and update fitness-for-use criteria. Under Commission Decision 2025/2607, interior matt paints now face a VOC cap of 10 g/L, alongside a 28-day chamber emission limit of 300 µg/m³ for total volatile organic compounds (TVOC). This places significant restraints on high-solvent products. Furthermore, bans on per- and polyfluoroalkyl substances (PFAS), phthalates, and organotins necessitate significant R&D and re-engineering of preservatives, especially in light of the European Union's Classification, Labelling and Packaging's (CLP) reclassification of isothiazolinones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Owner-Occupied Homes Sustain Dominance

In 2025, the residential segment dominated Italy's architectural coatings market, capturing 65.44% of the market, and is projected to grow at a 3.84% CAGR through 2031. This growth is attributed to owner-occupiers utilizing deductions ranging from 50% to 36% for envelope improvements. The segment benefits from low mortgage penetration and consistent house price increases, encouraging cash-financed interior upgrades. Furthermore, energy-class improvements continue to drive demand for thermal-insulation coatings.

The commercial segment is experiencing growth due to increased activity in hotels, restaurants, and cultural venue renovations. Non-residential permits rose by 11.1% year-on-year in Q3 2025, reflecting this trend. AkzoNobel's expansion of powder coatings in Como highlights the rising demand for metal façades. This demand is particularly strong in tourism-related construction projects that require durable and color-stable finishes.

By Technology: Water-Borne Formulations Accelerate

In 2025, water-borne systems dominated Italy's architectural coatings market, capturing 80.22% of the market, and are projected to grow at a 4.04% CAGR through 2031, surpassing their solvent-borne counterparts. Meanwhile, Commission Decision 2025/2607 solidifies the lead of low-VOC options.

Lifecycle assessments reveal that water-based aerosol sprays produce up to 58% less CO₂ than their solvent-based counterparts, providing specifiers with a measurable sustainability advantage. With public procurement increasingly mandating Ecolabel compliance, suppliers are channeling their R&D efforts into flow-and-level water-borne acrylics and powder-coated metal systems, highlighting the segment's alignment with regulatory standards.

Although solvent-borne technology remains a choice for specific high-performance needs, like metal primers and industrial coatings, its market share is declining. This reduction is driven by mounting regulatory pressures and a growing emphasis on indoor air quality and environmental credentials among customers.

By Resin Type: Acrylics Retain the Lead

In 2025, acrylics commanded a 50.26% share of Italy's architectural coatings market. Forecasted to grow at a 3.97% CAGR through 2031, this growth is attributed to their low-VOC compatibility, color retention, and vapor permeability. Highlighting the industry's shift towards sustainability, AkzoNobel, in collaboration with Arkema and BASF, unveiled a super-durable powder coatings line, underscoring the use of bio-attributed monomers to reduce carbon footprints.

As solvent restrictions tighten, alkyds face a decline. Meanwhile, epoxy, polyurethane, and polyester resins carve out niche roles in the architectural coatings arena. These resins are predominantly employed in performance-driven applications, including floor coatings, anti-corrosion primers, and industrial metal finishes. Epoxy coatings, celebrated for their chemical resistance and abrasion durability, are the go-to choice for high-traffic commercial interiors and industrial floors. On the other hand, polyurethane topcoats shine in high-end architectural millwork and furniture, where resistance to scratches and marks is crucial.

Polyester resins, known for their outdoor durability and color stability, find their primary application in powder coatings for architectural metals. The acrylic segment's leading position is bolstered by its alignment with regulatory trends, sustainability mandates, and the technical demands of energy-retrofit projects, driving the growth of Italy's architectural coatings market.

Competitive Landscape

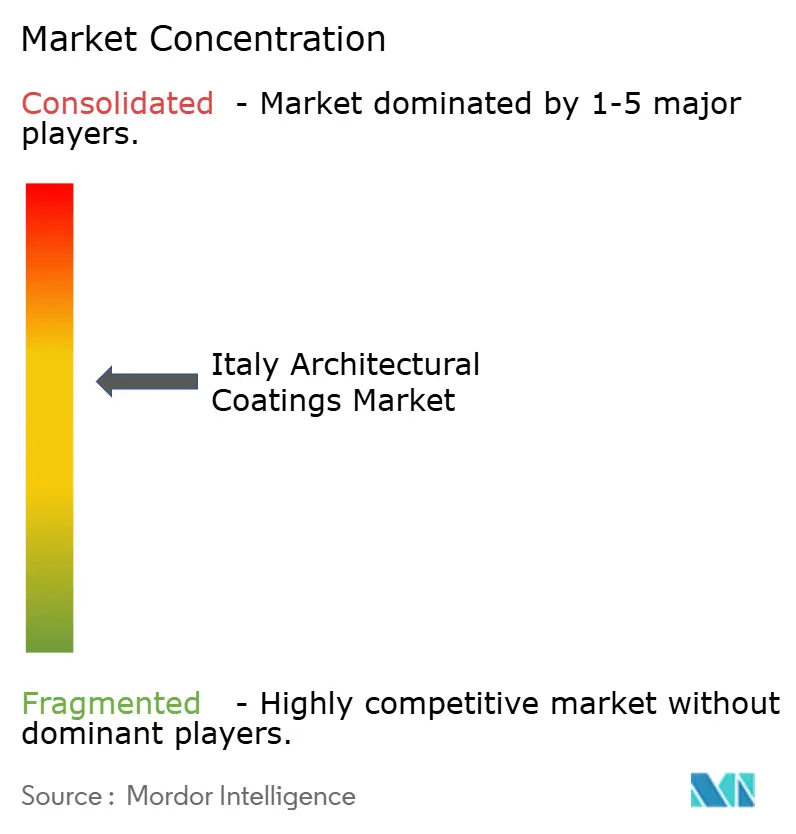

The Italy architectural coatings market is moderately fragmented. AkzoNobel, PPG, and Sherwin-Williams lead multinationals, while Boero, ICA, San Marco, Oikos, and Valpaint anchor national share. AkzoNobel’s EUR 21 million Como expansion added four powder-coating lines and bonding equipment, boosting supply chain resilience for façade and fenestration projects across.

PPG’s Milan color-automation lab, opened with a USD 2.1 million outlay, now produces 100,000 bespoke color matches annually, underpinning its color leadership with specifiers. Boero’s 53% PCR-plastic bucket achievement in 2025 positions it favorably for circular-economy contracts, while its CIN partnership expands geographic reach.

Strategic moves focus on low-carbon resins, circular packaging, and digital specification tools. Suppliers seek ISO 9001/14001/45001 certifications and Seveso III compliance to qualify for public tenders, creating a baseline of operational rigor that raises entry barriers for smaller competitors.

Italy Architectural Coatings Industry Leaders

AkzoNobel N.V.

DAW SE

PPG Industries, Inc.

San Marco Group S.p.A.

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The European Commission has adopted updated EU Ecolabel criteria for decorative paints, varnishes, and related products, valid until 31 December 2032.

- October 2025: Italy has ended the 110% Superbonus scheme, shifting towards significantly lower tax deductions for home renovations to reduce public spending. Under the 2026 budget law, deductions for building renovations and energy improvements will be lowered to 36%-30% by 2026/2027.

Italy Architectural Coatings Market Report Scope

Architectural coatings are protective and decorative finishes applied to stationary, on-site structures, such as residential, commercial, and industrial buildings. These products, including paints, stains, sealers, and varnishes, are designed for both exterior and interior surfaces to offer durability, aesthetics, and resistance to environmental damage.

The Italy Architectural Coatings market is segmented by end-user industry, technology and resin. By end-user industry, the market is segmented into commercial and residential. By technology, the market is segmented into solvent-borne and water-borne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. For each segment, market sizing and forecasts are provided in terms of value (USD).

By End-User Industry

| Commercial |

| Residential |

By Technology

| Solvent-borne |

| Water-borne |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| By End-User Industry | Commercial |

| Residential | |

| By Technology | Solvent-borne |

| Water-borne | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms