Coal Trading Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.37 Billion |

| Market Size (2031) | USD 16.64 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

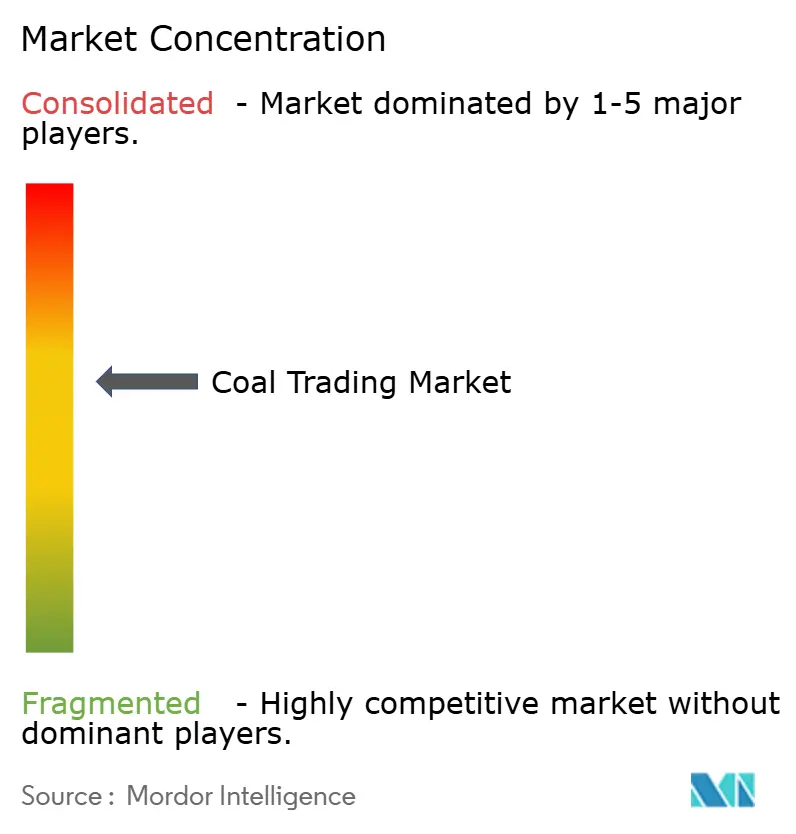

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coal Trading Market Analysis by Mordor Intelligence

The Coal Trading Market size is projected to expand from USD 12.72 billion in 2025 and USD 13.37 billion in 2026 to USD 16.64 billion by 2031, registering a CAGR of 4.47% between 2026 to 2031.

Strong Asian utility procurement, European hedging against natural-gas volatility, and widening metallurgical-coal premiums over thermal grades sustain this measured expansion.[1]Reuters, “China Coal Imports Hit Record 548 Million Tonnes in 2024,” REUTERS.COM Long-term freight costs linked to IMO 2030 carbon-intensity rules have restored the appeal of fixed-price supply contracts, while port-capacity upgrades at Richards Bay and Qinhuangdao ease demurrage pressures and release stranded tonnage. Digital bill-of-lading platforms now settle 12% of seaborne trades, lowering working-capital needs for counterparties that can verify cargo quality in real time. Although renewable build-out in OECD economies crimps steam-coal demand, high-grade coking coal remains irreplaceable for blast-furnace steelmaking, giving the global coal trading market durable multi-segment demand diversity.[2]World Steel Association, “Global Steel Production and Coking Coal Demand 2024,” WORLDSTEEL.ORG

Key Report Takeaways

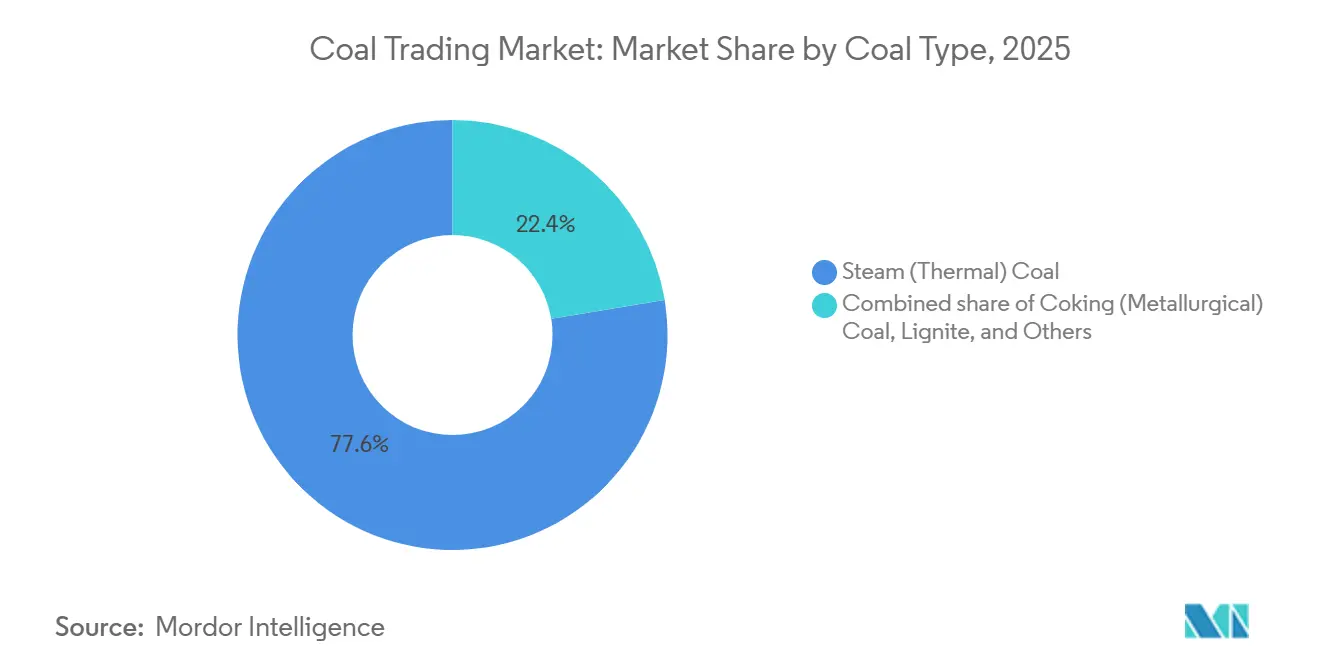

- By coal type, steam coal led with a 77.6% share of the global coal trading market in 2025, while coking coal is forecast to post the fastest 5.1% CAGR to 2031.

- By trader mechanism, long-term contracts held 60.5% of the global coal trading market in 2025, and this segment is projected to expand at a 6.7% CAGR through 2031.

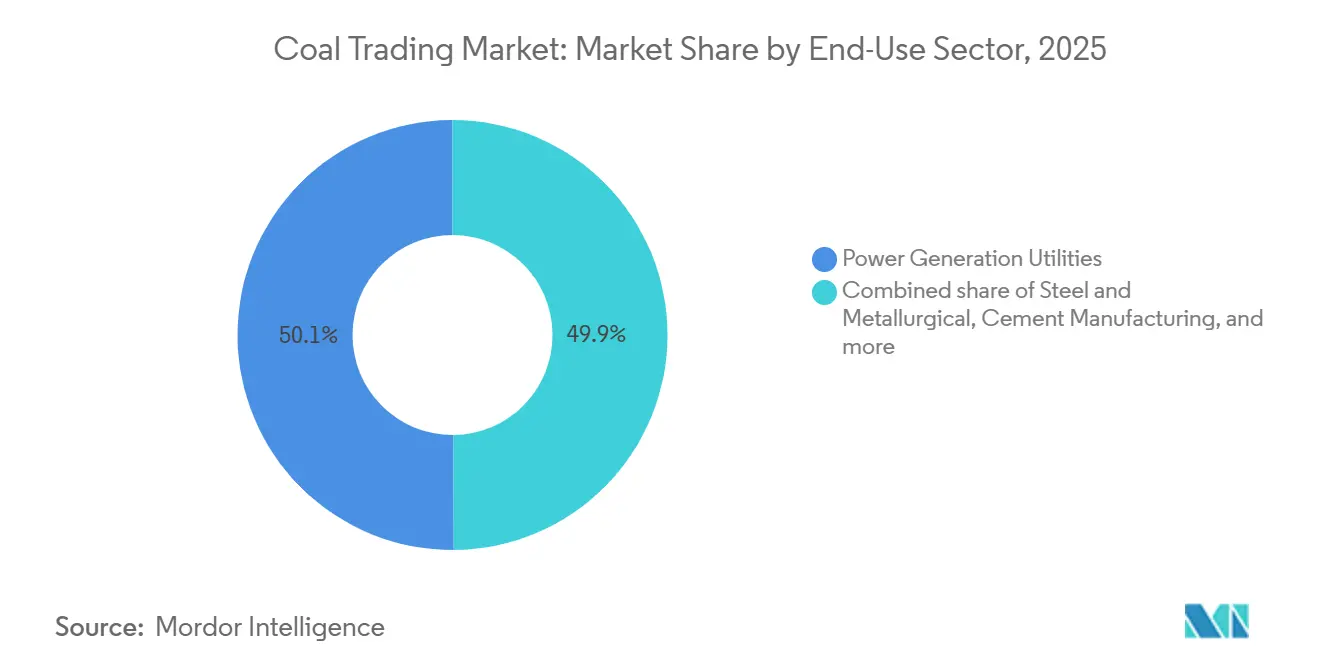

- By end-use sector, power generation commanded 50.1% of value in 2025; the steel segment is advancing at the highest 5.4% CAGR between 2026 and 2031.

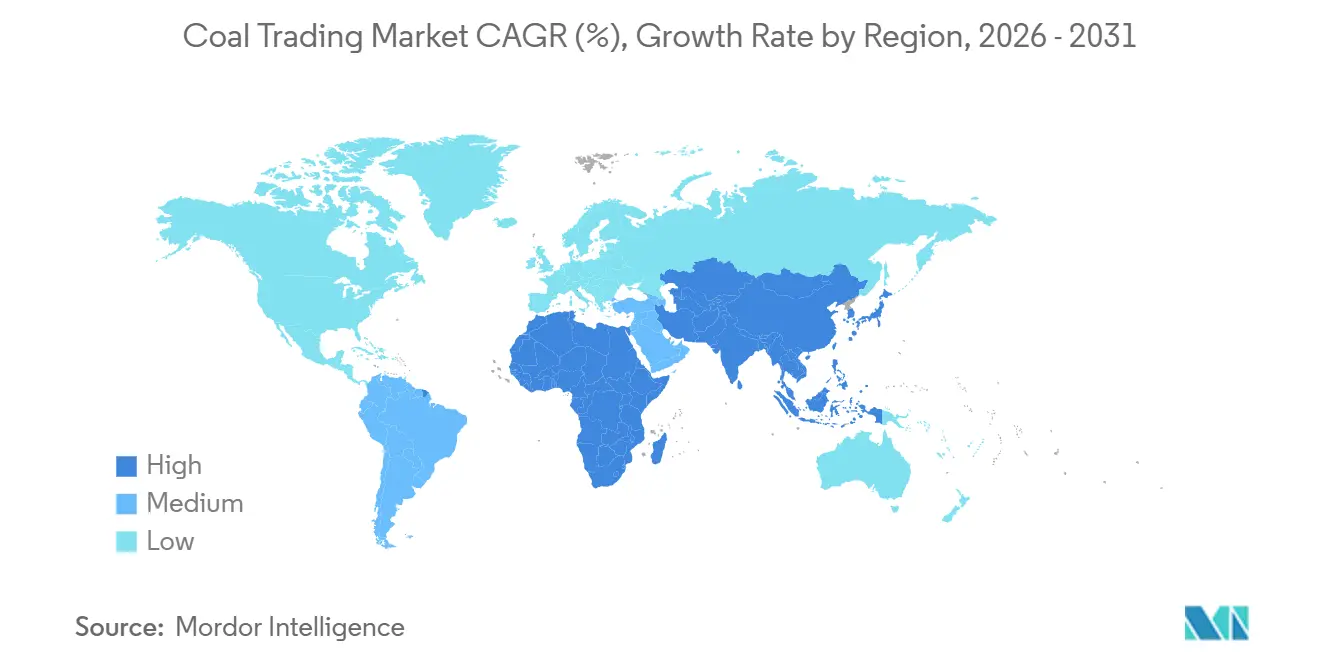

- By geography, Asia-Pacific captured 66.9% revenue in 2025 and is expected to record a 4.9% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coal Trading Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Asian demand for sub-bituminous coal imports | +1.2% | Asia-Pacific core, spillover to Oceania exporters | Medium term (2-4 years) |

| Expansion of merchant coal-fired plants in emerging SE Asia | +0.8% | ASEAN | Long term (≥ 4 years) |

| Infrastructure bottleneck relief at Richards Bay & Qinhuangdao ports | +0.6% | South Africa and China export corridors | Short term (≤ 2 years) |

| Digitization of physical coal trading platforms & blockchain B/Ls | +0.4% | Global, early adoption in Singapore and Rotterdam hubs | Medium term (2-4 years) |

| India’s coastal shipping incentives for bulk cargo | +0.5% | India, secondary effects on Indonesian and Australian exporters | Short term (≤ 2 years) |

| Resurgence of European coal burn amid gas-price volatility | +0.7% | Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Asian Demand for Sub-Bituminous Coal Imports

Chinese and Indian utilities purchased 793 million t of imported coal in 2024, up 13% year-on-year, favoring low-sulfur Indonesian grades that avoid flue-gas desulfurization retrofits.[3]International Energy Agency, “Coal 2024: Analysis and Forecast to 2030,” IEA.ORG Sub-bituminous cargoes captured 65% of India’s thermal-coal imports because lower ash content reduces boiler maintenance intervals, extending turbine life and cutting outage risk. ASEAN power producers added 18 GW of coal capacity between 2020 and 2024, underpinning steady demand for 4,200–5,000 kcal/kg material that balances lower calorific value against sub-0.8% sulfur specifications. Indonesian dominance in this niche concentrates supply risk; Jakarta’s 25% domestic-market obligation has already withheld 18 million t from export channels during 2024 demand spikes, forcing Chinese buyers to diversify toward Russian Far-East coal.[4]Reuters, “China Coal Imports Hit Record 548 Million Tonnes in 2024,” REUTERS.COM

Expansion of Merchant Coal-Fired Plants in Emerging SE Asia

Independent power producers commissioned 12 GW of merchant coal plants across Vietnam, the Philippines, and Indonesia in 2024, sourcing fuel via quarterly tenders rather than decade-long utility contracts. These generators arbitrage between Indonesian 4,200 kcal/kg coal and Australian 5,500 kcal/kg grades, increasing spot-market turnover and stimulating regional coal brokerage desks. Merchant operators, lacking captive mines, procure all requirements on the open market, creating incremental demand for flexible blending and inventory-financing services that large traders can monetize. Vietnam’s Vinh Tan 4 extension and the Philippines’ Atimonan One Energy facilities illustrate this model, collectively importing 2.4 million t per quarter in 2025 contract tenders.

Infrastructure Bottleneck Relief at Richards Bay & Qinhuangdao Ports

Richards Bay Coal Terminal lifted throughput to 52.08 million t in 2024 after a ZAR 2.5 billion conveyor upgrade raised nameplate capacity to 77 million t. Qinhuangdao processed 208.83 million t the same year, aided by automated stacking systems that cut vessel waits by eight hours. Reduced congestion trims demurrage costs, historically USD 5–8/t during peak seasons, and frees traders to cycle vessels faster, effectively expanding fleet productivity. South Africa’s new 375 km rail bypass ensures coal trains avoid general freight bottlenecks, pointing export volumes toward 60 million t by 2026.

Digitization of Physical Coal Trading Platforms & Blockchain B/Ls

A 2024 Trafigura-ING blockchain pilot cut bill-of-lading processing from seven days to 24 hours and lowered financing margins by 15 basis points. Mercuria’s AI-enabled quality-monitoring network predicts ash and calorific value before berth, letting buyers reject off-spec cargo at load port, which curtails costly arbitration cycles. Blockchain consortia such as Komgo and Contour now clear 12% of coal trades by value, drawing smaller counterparties unable to post traditional collateral. Faster settlement unlocks working capital, enabling traders to scale volumes without balance-sheet strain, and collectively bolsters the global coal trading market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating renewable build-out under REPowerEU & IRA | –1.1% | North America & EU, spillover to APAC supply chains | Long term (≥ 4 years) |

| Stricter coal financing restrictions by OECD ECAs | –0.6% | Global, acute in Africa and Latin America | Medium term (2-4 years) |

| IMO 2030 carbon-intensity rules raising dry-bulk freight costs | –0.8% | Global, highest on Australia–Europe routes | Short term (≤ 2 years) |

| Mandatory domestic-market-obligation caps in Indonesia | –0.7% | Asia-Pacific importers dependent on Indonesian supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Renewable Build-Out Under REPowerEU & IRA

REPowerEU targets 750 GW of renewables by 2030, displacing 120 million t of coal demand each year once wind and solar exceed 50% of generation in Germany, Spain, and Denmark. The U.S. Inflation Reduction Act funnels USD 369 billion into clean-energy credits, adding 40 GW of wind and solar annually and accelerating coal-to-gas switching across 15 GW of remaining coal capacity. China’s 217 GW solar build in 2024 alone signals that coal’s domestic generation share will slip to 45% by 2030. When wind and solar undercut coal’s levelized costs in eight months of the year, utilities curtail baseload coal units, trimming global seaborne steam-coal demand.

IMO 2030 Carbon-Intensity Rules Raising Dry-Bulk Freight Costs

The IMO’s Carbon Intensity Indicator, tightening annually to 2030, punishes high-emission Capesize vessels with lower charter ratings, forcing speed cuts or retrofits that translate into USD 3–5/t higher freight costs. Australia-to-Europe rates rose 22% in 2024 as owners passed through compliance expenses, wiping out traditional price advantages of distant suppliers. Delivered costs to Rotterdam increased USD 8/t during 2024 solely from freight surcharges, squeezing arbitrage margins for traders. Older vessels risk premature scrapping; fleet retirements will tighten capacity and keep freight elevated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coal Type: Metallurgical Grades Gain Momentum

Coking coal’s 5.1% forecast CAGR outpaces steam coal’s 4.2% as Indian and ASEAN blast-furnace expansions add 225 million t of crude-steel capacity by 2031. Although steam coal controlled 77.6% of the global coal trading market share in 2025, its growth moderates as renewables displace baseload coal in OECD regions. Lignite contributed just 3.8% of trade value and remains limited to intra-regional flows due to high moisture content.

Tight metallurgical supply widened premiums to USD 180/t over thermal coal in 2024 after Australian floods curtailed output, prompting Indian mills to import record volumes. The global coal trading market size tied to metallurgical grades is poised to expand further as steelmakers lock in multi-year contracts that secure consistent 65% fixed-carbon material. Steam-coal stability hinges on the successful deployment of carbon-capture retrofits across 20 GW of U.S. and EU capacity; absent these installations, steam-coal volumes will see a gradual decline after 2028.

By Trader Mechanism: Contracting Regains Primacy

Long-term agreements covered 60.5% of 2025 volume and are growing at 6.7% as buyers hedge IMO-linked freight volatility. Spot trading, while still liquid, expands at a slower 4.1% because rapid freight swings erode short-term arbitrage gains. Japanese utilities signed 5-year deals indexed to Newcastle plus USD 5/t that transfer freight risk to sellers.

Steel mills favor multi-year coking-coal contracts; power utilities now mix contract and spot cargoes to optimize monthly burn profiles. Contract sales settle within 15 days of discharge, freeing cash compared with 45-day spot cycles, and this efficiency is attracting capital-constrained traders. Consequently, the portion of the global coal trading market size tied to long-term contracts should exceed two-thirds by 2031.

By End-Use Sector: Steel Outpaces Power

Power generation still accounted for 50.1% of the value in 2025, yet a 3.9% CAGR trails the steel segment’s projected 5.4% growth. Integrated mills in India alone will import 28 million t of coking coal annually by 2031, sustaining metallurgical demand even as electric-arc furnace adoption remains nascent. Cement and chemicals grow at intermediate rates, anchored by Southeast Asian infrastructure programs and China’s coal-to-chemicals builds.

Power-sector coal demand is increasingly price elastic; India’s NTPC cut coal burn by 8 million t in 2024 by dispatching solar during daylight and cycling coal to evenings. Conversely, blast-furnace operations cannot tolerate quality variability, locking the steel supply chain into high-grade coal. These contrasts reinforce the global coal trading market’s dual-track outlook: steady if slower volumes in power and faster growth in metallurgical niches.

Geography Analysis

Asia-Pacific dominated the global coal trading market with a 66.9% share in 2025 and will grow at 4.9% through 2031. Within the region, China’s imports plateau near 550 million t by 2028 as domestic mines scale productivity, whereas India targets a reduction from 245 million t in 2024 to 180 million t by 2031 on rising local output. ASEAN demand climbs 6.2% yearly, underpinned by Vietnam’s 18 GW coal pipeline and the Philippines’ 55% coal share in Luzon grid generation.

Europe held 12.4% in 2025, experiencing a temporary 2.8% annual uptick until 2027 as gas prices remain volatile; thereafter, coal demand contracts 4.5% annually once REPowerEU renewable targets suppress dispatch economics. Germany’s imports reached 32 million t in 2024 but will trend to zero by 2038 under the legislated phase-out.

North America’s 8.7% share is export-oriented; the U.S. shipped 65 million t of mostly metallurgical coal in 2024, while importing only niche volumes for Appalachian steel mills. South America’s 6.2% portion revolves around Colombian exports that face community-driven output caps, shrinking 2.1% annually. Middle East & Africa captured 5.8%; Richards Bay’s capacity upgrades may lift South African exports to 60 million t by 2026, yet Transnet rail limits further growth.

Competitive Landscape

The global coal trading market is moderately concentrated; Glencore, Vitol, Trafigura, Mercuria, and China Shenhua handled about 40% of seaborne volumes in 2025 but exercise limited sway over price indices set by independent assessors. Vitol’s USD 208.9 million purchase of Noble Resources added 15 million t of origination and Indonesian storage, while Trafigura’s acquisition of Puma Energy’s desk secured African utility off-takes, illustrating consolidation among mid-tier platforms.

Glencore divested its 33.3% Cerrejón stake for USD 588 million, signaling a pivot from mining toward pure trading to redeploy capital into LNG and transition metals. Chinese SOEs such as China Shenhua and China Coal produced 304.3 million t and 120 million t respectively in 2024 and now extend into export channels, leveraging state-owned port access to challenge incumbent Western traders.

Blockchain adoption remains uneven; Singapore and Rotterdam clear 12% of coal trades digitally, yet Latin American and African cargoes still rely on paper documents that add a week to settlement. Rising freight costs and OECD finance curbs will likely winnow the active number of global coal desks from 25 in 2024 to fewer than 15 by 2031, further concentrating the competitive field.

Coal Trading Industry Leaders

Trafigura Group Pte. Ltd.

Glencore Plc.

Mercuria Energy Group

Vitol Holding B.V

China Shenhua Energy Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: China Shenhua Energy has acquired 12 assets from China Energy Investment Group for CNY 133 billion (USD 18.9 billion), increasing its total assets to over CNY 200 billion. The acquisition includes coal production, power generation, coal chemicals, and logistics, expanding operations into Xinjiang and Inner Mongolia as coal power faces a gradual decline in the world's largest coal market.

- February 2025: Peabody Energy reported USD 181.5 million adjusted EBITDA on higher Australian metallurgical sales and launched a USD 150 million share-buyback program.

- September 2024: PT Adaro Energy signed a 5-year 15 million tpa off-take with India’s NTPC, indexed to the Indonesian Coal Index.

- August 2024: Vitol closed the USD 208.9 million Noble Resources purchase, boosting coal volumes to 80 million t annually.

Global Coal Trading Market Report Scope

The trading of coal pertains to the purchase and sale of coal as a commodity among nations, corporations, or individuals. Coal is a fossil fuel primarily utilized for generating electricity and industrial applications. It originates from the remnants of plants that thrived and perished millions of years ago, and it is located in underground deposits. The coal trade encompasses the extraction of coal from mines or open pits, its transport to processing facilities or ports, and its subsequent dissemination to end-users. This trade can assume diverse manifestations, such as internal trade within a nation and cross-border trade between countries.

The coal trading market is segmented by type of coal, end-use sector, and geography. By type of coal, the market is segmented into steam coal, coking coal, and lignite. By end-use sector, the market is segmented into power generation, steel, cement, chemical, and others. The report also covers the market size and forecasts for the coal trading market across major regions, such as North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion) for all the above segments.

| Steam (Thermal) Coal |

| Coking (Metallurgical) Coal |

| Lignite |

| Others |

| Spot Trading |

| Long-term Contracts |

| Power Generation Utilities |

| Steel and Metallurgical |

| Cement Manufacturing |

| Chemical/Industrial Heating |

| Others (Residential, Commercial, Transport) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Coal Type | Steam (Thermal) Coal | |

| Coking (Metallurgical) Coal | ||

| Lignite | ||

| Others | ||

| By Trader Mechanism | Spot Trading | |

| Long-term Contracts | ||

| By End-use Sector | Power Generation Utilities | |

| Steel and Metallurgical | ||

| Cement Manufacturing | ||

| Chemical/Industrial Heating | ||

| Others (Residential, Commercial, Transport) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global coal trading market?

The global coal trading market size stood at USD 13.37 billion in 2026 and is projected to reach USD 16.64 billion by 2031.

Which coal type is growing fastest in international trade?

Coking coal is forecast to register the highest 5.1% CAGR between 2026 and 2031, driven by new blast-furnace capacity in India and ASEAN.

Why are long-term contracts gaining share in coal trading?

Rising freight volatility linked to IMO 2030 rules makes fixed-price supply agreements attractive, pushing long-term contracts to 60.5% of 2025 volume and a 6.7% growth trajectory.

How will renewable energy targets affect coal demand in Europe?

REPowerEU's 750 GW renewable goal is expected to cut European coal burn after 2027, causing regional demand to decline 4.5% annually from 2028 onward.

Which region dominates global coal trade?

Asia-Pacific accounted for 66.9% of 2025 value and is projected to grow at a 4.9% CAGR through 2031.

What is the level of market concentration among coal traders?

The top five traders handle roughly 40% of seaborne volumes, indicating moderate concentration.

Page last updated on: