IT Outsourcing (ITO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

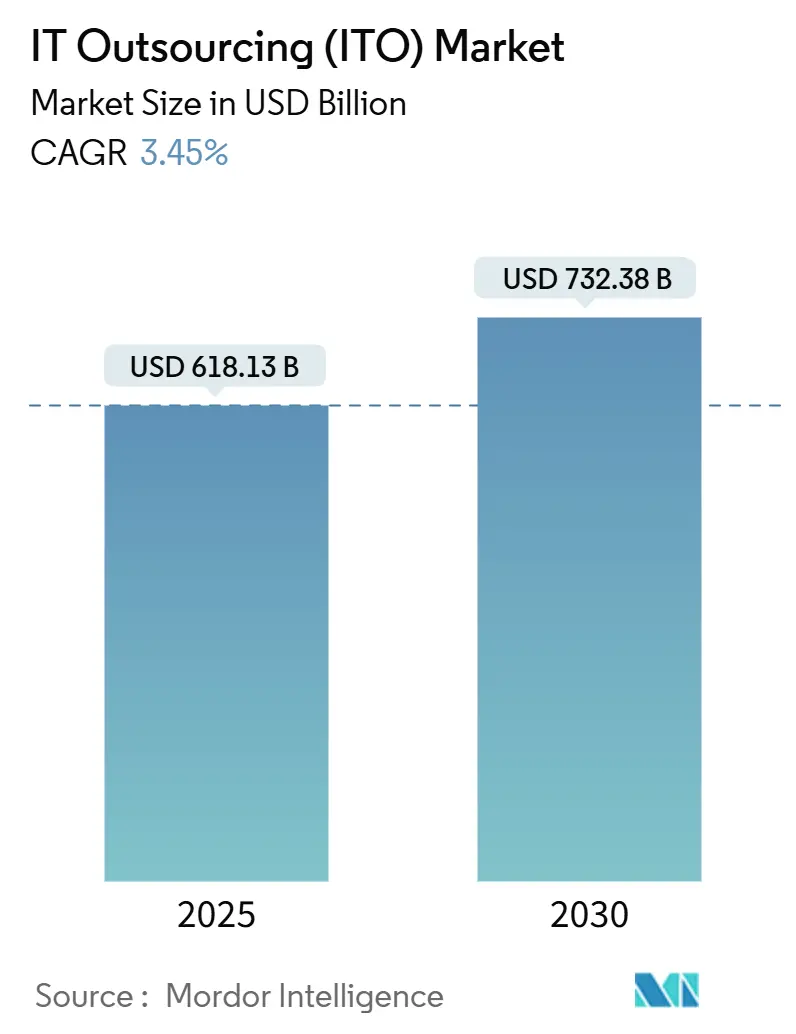

| Market Size (2025) | USD 618.13 Billion |

| Market Size (2030) | USD 732.38 Billion |

| Growth Rate (2025 - 2030) | 3.45% CAGR |

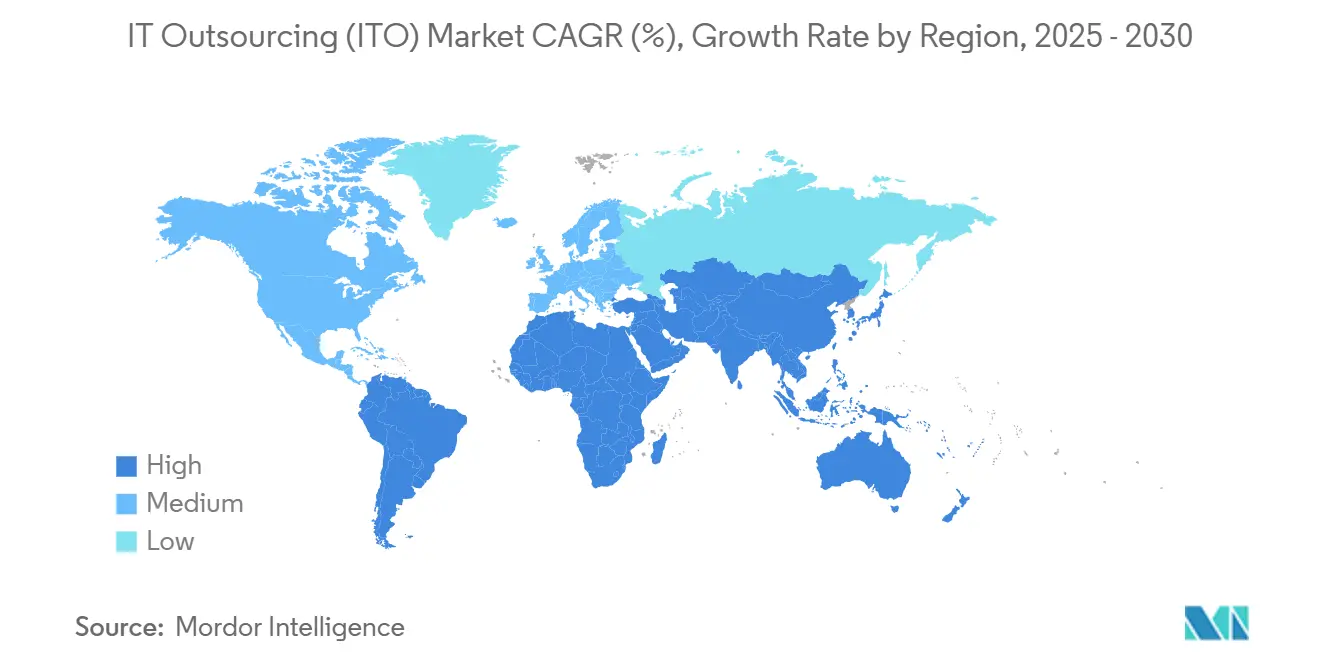

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

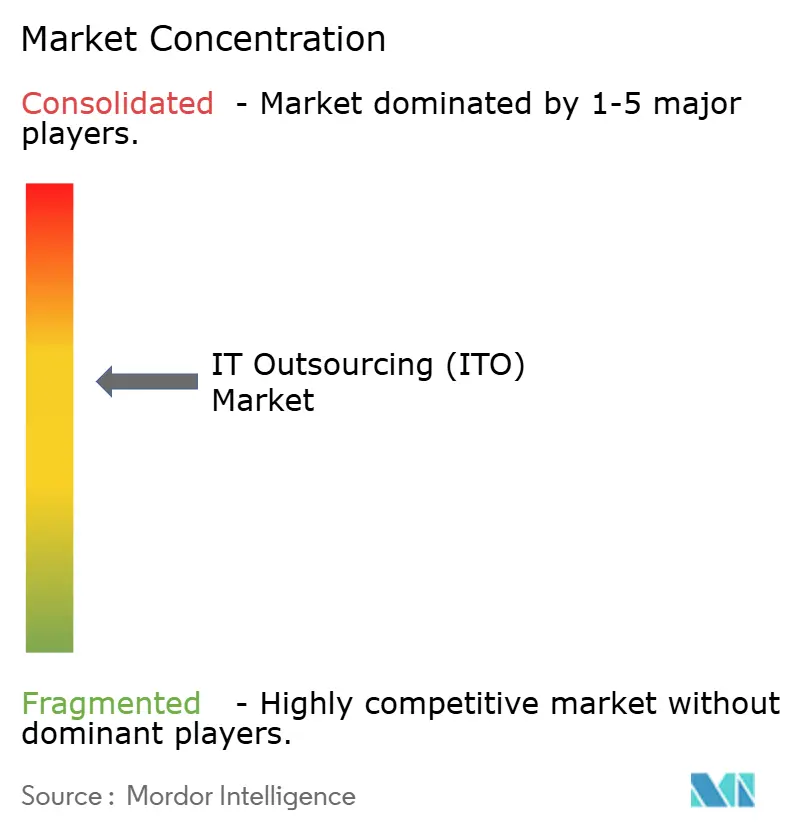

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

IT Outsourcing (ITO) Market Analysis by Mordor Intelligence

The IT outsourcing market size is estimated at USD 618.13 billion in 2025 and is forecast to attain USD 732.38 billion by 2030, reflecting a 3.45% CAGR during the period. The measured trajectory mirrors the sector’s maturation as generative AI automation reshapes labor-intensive delivery models, spurring new AI-enabled services while compressing traditional headcount-driven contracts. Geopolitical tensions are prompting enterprises to diversify sourcing footprints in response to sovereign-cloud mandates and data-residency rules, leading many buyers to blend offshore, nearshore, and onshore centers for risk mitigation. The cybersecurity talent shortfall of 4.8 million positions worldwide is creating premium demand for managed detection and response offerings. Consolidation is accelerating: recent deals such as Cognizant’s USD 1.3 billion Belcan purchase and Capgemini’s negotiations to acquire WNS illustrate how scale players absorb niche specialists to deepen AI capabilities and broaden portfolios. Cloud-managed services are gaining prominence as enterprises struggle to govern hybrid, multicloud estates, while outcome-based pricing gains favor for its alignment with measurable business results.

Key Report Takeaways

By service type, infrastructure outsourcing led with 45.7% of IT outsourcing market share in 2024; cloud-managed services is projected to expand at a 3.5% CAGR through 2030.

By organization size, large enterprises accounted for 67.9% share of the IT outsourcing market size in 2024, whereas SMEs are advancing at a 4.1% CAGR to 2030.

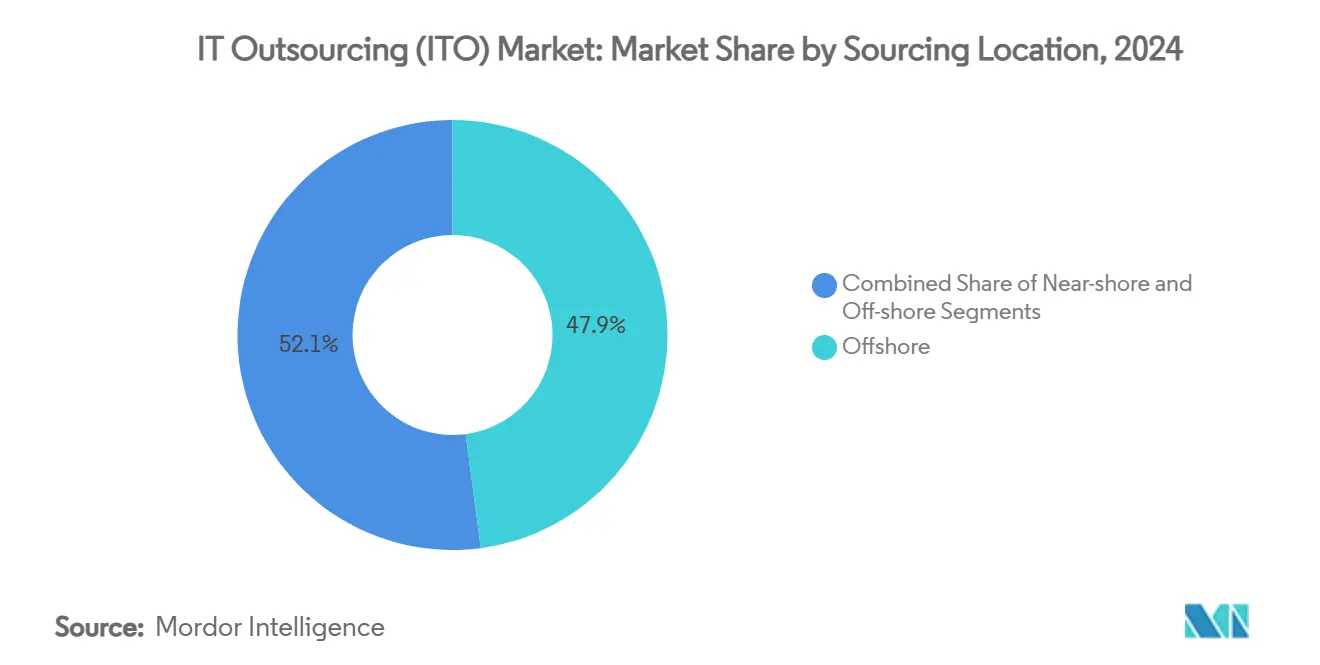

By sourcing location, offshore centers held 47.9% share of the IT outsourcing market size in 2024; nearshore arrangements are progressing at a 5.3% CAGR through 2030.

By end-user industry, BFSI captured 25.6% of IT outsourcing market share in 2024, while healthcare and life sciences is set to rise at a 5.7% CAGR to 2030.

By geography, North America accounted for 24.5% share of the IT outsourcing market size in 2024, whereas Asia-Pacificis set to rise at a 3.7% CAGR to 2030.

Global IT Outsourcing (ITO) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native application modernisation demand | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| GenAI-enabled service-desk automation | +0.6% | Global, early adoption in North America and Asia-Pacific | Short term (≤ 2 years) |

| Integration of AI and automation in DevOps outsourcing | +0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Talent-scarcity in cybersecurity and observability | +0.4% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Rise of sovereign-cloud and data-residency mandates | +0.3% | Europe, Asia-Pacific, with spillover to other regions | Long term (≥ 4 years) |

| Vendor shift to outcome-based pricing models | +0.2% | Global, early adoption in North America | Medium term (2-4 years) |

Source: Mordor Intelligence

Cloud-native Application Modernization Demand

Enterprises are re-architecting monolithic systems into microservices, containers, and serverless functions, which opens sizable engagements for platform engineering, Kubernetes orchestration, and event-driven design. Providers increasingly deliver outcome-based contracts that guarantee performance, cost targets, and scalability rather than billing for effort, particularly in highly regulated verticals such as financial services and healthcare where compliance adds complexity.[1]SHRM Editorial, “Geopolitical Tensions Are Shifting Global Talent Strategies,” shrm.org Cultural change management complements the technical shift, and external partners frequently guide agile processes that internal teams cannot easily instill.

GenAI-enabled Service-desk Automation

Generative AI is cutting Level 1 ticket volumes by up to 40% and trimming mean-time-to-resolution by 25% through intelligent routing and self-healing scripts. Virtual assistants now grasp context across multiple systems, drive personalized responses, and predict incidents before users notice disruption. Providers must, however, pair automation with human oversight for complex security issues that demand contextual judgment.

Integration of AI and Automation in DevOps Outsourcing

Machine-learning models embedded in CI/CD pipelines automate code review, testing, and infrastructure provisioning, allowing service partners to promise faster releases with predictive failure analysis and intelligent rollback. AI-driven infrastructure-as-code optimizes resource allocation across multicloud estates, while autonomous observability pinpoints root causes and triggers remediation without manual intervention.

Talent-scarcity in Cybersecurity and Observability

Premium skills in zero-trust frameworks, cloud security architecture, and AI-based threat hunting remain scarce, driving managed security service contracts that blend human experts with AI orchestration to achieve scale.[2]ISC2, “2024 Cybersecurity Workforce Study,” isc2.orgObservability follows a parallel path as enterprises outsource complex telemetry management to ensure full-stack visibility across hybrid environments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geopolitical tensions disrupting offshore delivery centers | -0.4% | Global, concentrated impact on US-China, EU-Russia corridors | Medium term (2-4 years) |

| Escalating IP-theft and ransomware insurance costs | -0.3% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Volatility in hyperscaler egress pricing | -0.2% | Global, affecting multi-cloud strategies | Short term (≤ 2 years) |

| AI-enabled code-generation reducing outsourcing scope | -0.2% | Global, early impact in North America and Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Escalating IP-theft and Ransomware Insurance Costs

Increasing cyber incidents raise premiums and narrow coverage, forcing enterprises to add encryption, access monitoring, and segregated development zones that inflate project costs EY. Buyers now demand providers carry higher insurance limits and submit to regular penetration tests, a hurdle that disadvantages smaller vendors and fuels consolidation.

Rising Geopolitical Tensions Disrupting Offshore Delivery Centers

Data localization laws, export controls, and trade restrictions are pushing 37% of multinationals to diversify delivery footprints beyond single-country dependencies, lengthening procurement cycles and driving preference for shorter, flexible contracts.[3]Accenture, Beyond Uptime: Fueling innovation with infrastructure management,” accenture.comProviders respond by expanding nearshore and onshore hubs, but this adds capital expenditure and erodes historical cost advantages.

Segment Analysis

By Service Type: Infrastructure Dominance Faces Cloud Disruption

Infrastructure outsourcing commanded 45.7% of the IT outsourcing market in 2024 due to enterprises’ reliance on resilient data center operations that need continuous monitoring and regulatory compliance. Cloud-managed services, however, are pacing the field with a 3.5% CAGR as organizations confront the complexity of hybrid estates spanning AWS, Azure, Google Cloud, and private environments. Providers now bundle unified management platforms that sequence workloads by cost, latency, and compliance preferences, challenging the boundaries between traditional infrastructure management and emerging multicloud orchestration.

Demand for application development and maintenance is being reshaped by low-code and AI-assisted development, pushing vendors to differentiate through domain knowledge and integration expertise. Edge computing and AI model lifecycle services sit in the “Others” bucket and represent nascent yet high-margin opportunities. As cloud adoption rises, incumbents pivot to automated site-reliability-engineering services that deliver guaranteed service-level objectives using AI-driven self-healing, thereby protecting infrastructure revenue streams against price compression.

Note: Segment shares of all individual segments available upon report purchase

By Organization Size: SME Acceleration Challenges Enterprise Dominance

Large enterprises retained 67.9% of spending in 2024 as their complex legacy estates require deep architectural know-how, yet SMEs are expanding faster at a 4.1% CAGR. Outcome-based contracts resonate with smaller firms because they align IT spending to tangible business outcomes instead of headcount. Cloud-native vendors lower entry barriers with self-service portals and automated provisioning, giving SMEs on-demand access to AI, analytics, and cybersecurity capabilities once exclusive to Fortune 500 budgets. This democratization of technology widens the total addressable IT outsourcing market and pressures established providers to create modular, standardized offerings that scale down economically without compromising margin.

By Sourcing Location: Nearshore Gains Amid Offshore Resilience

Offshore hubs like India and the Philippines preserved 47.9% of 2024 revenue owing to labor cost advantages of up to 60% over onshore options. Nearshore centers, however, are growing at 5.3% CAGR as enterprises seek time-zone alignment and cultural affinity. Mexico, Costa Rica, and Colombia benefit from United States–Mexico–Canada Agreement provisions, which streamline data transfer and intellectual-property protections, fostering real-time agile collaboration.

Hybrid sourcing models now distribute workloads according to risk tolerance and talent availability. Critical security functions may stay onshore, customer experience platforms shift nearshore for language alignment, and scalable engineering tasks continue offshore. Providers invest in delivery-center diversification to counter geopolitical shocks, while automation reduces sensitivity to wage inflation in high-cost jurisdictions.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Healthcare Surge Challenges BFSI Leadership

BFSI accounted for 25.6% of IT outsourcing market revenue in 2024 as core banking, insurance policy administration, and regulatory reporting require 24/7 uptime and bulletproof security. The sector’s sophisticated demands sustain premium pricing for providers with deep domain credentials. This growth stems from stringent data-protection laws such as HIPAA and evolving clinical-trial digitization norms. Retail, manufacturing, and media also present opportunities as they embed IoT, smart-factory analytics, and content-personalization engines into business models. Providers capturing vertical expertise differentiate through accelerators, regulatory toolkits, and pre-configured data models, driving cross-sell potential across industry portfolios.

Geography Analysis

North America’s 24.5% share confirms its status as the prime adopter of AI and cloud modernization initiatives that demand seasoned providers. United States enterprises are renegotiating legacy contracts toward outcome-based terms that stipulate cost-per-transaction or revenue uplift metrics, reducing labor-arbitrage exposure. Canadian firms prioritize zero-trust security frameworks and sovereign cloud instances to comply with stringent privacy acts. Mexican nearshore centers expand agile pods and DevOps capabilities, reducing project latency and enhancing cultural alignment for US clients.

Asia-Pacific’s 3.7% CAGR stems from India’s continued dominance and rising contributions from ASEAN economies. Vietnam, Indonesia, and Malaysia are nurturing engineering talent pipelines through government incentives and academic partnerships, positioning themselves as secondary hubs for application development and testing. Japan and South Korea outsource next-generation network operations and edge-cloud orchestration to compensate for local workforce gaps, and Australia increases demand for managed cybersecurity and cloud FinOps services.

Europe combines stringent data-protection mandates with an appetite for digital sovereignty. Local providers form alliances with hyperscalers to launch region-specific sovereign cloud zones. Germany, France, and the Netherlands drive sectoral cloud migration while insisting on in-country data processing. The United Kingdom, despite Brexit, remains a hub for financial-services outsourcing, emphasizing resilience testing and operational-risk controls. Eastern Europe’s software-engineering clusters offer high-end R&D outsourcing but navigate geopolitical uncertainty through diversification agreements with Western European clients.

Competitive Landscape

Global revenue concentration is moderate as the top 10 vendors control nearly 40% of spending. Accenture, TCS, and Infosys exploit global delivery centers, expansive portfolios, and automation platforms to anchor multiyear transformation programs. Cognizant, through its Belcan acquisition, adds aerospace-engineering depth and AI-driven digital-product design services, while Capgemini’s pursuit of WNS signals a push into domain-rich business-process management.

Cloud hyperscalers expand professional services arms, blending infrastructure consumption with advisory offerings that squeeze traditional integrators. Meanwhile, niche players such as EPAM Systems, Globant, and Endava use agile product studios and design thinking to win digital-native clients. Providers stake competitive advantage on proprietary AI platforms that automate delivery, with some claiming productivity gains exceeding 30%. Sustainability credentials and transparent carbon reporting are emerging differentiators as European buyers embed environmental criteria into RFPs.

Acquisition velocity is set to persist as firms seek scarce cybersecurity skills and regional delivery footprints. Private-equity investment is rising in mid-tier MSPs, signaling confidence in margin expansion via automation and vertical specialization. White-space opportunities include quantum-computing readiness assessments, edge-AI lifecycle management, and green-IT optimization services that help clients achieve net-zero commitments without sacrificing performance.

IT Outsourcing (ITO) Industry Leaders

-

IBM Corporation

-

DXC Technologies

-

Accenture PLC

-

NTT Corporation

-

Infosys Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cognizant Technology Solutions secured a USD 1 billion contract with a major US healthcare company, underscoring healthcare’s pivot toward AI-enabled IT services.

- April 2025: Capgemini opened advanced talks to acquire WNS Holdings, aiming to deepen BPM and analytics breadth for global clients.

- April 2025: Tata Consultancy Services launched sovereign cloud networks for the Indian market, with India now contributing USD 2.6 billion, or 8.6%, to total revenue.

- March 2025: Citigroup outlined plans to cut external IT contractors from 50% to 20%, signaling a shift toward in-house capability development that may affect long-standing vendor relationships.

- January 2025: Infosys filed a counterclaim against Cognizant alleging anti-competitive practices, highlighting intensifying legal skirmishes among top vendors.

Global IT Outsourcing (ITO) Market Report Scope

IT outsourcing involves a contractual arrangement where IT service providers take complete ownership and control over the client's IT infrastructure. The growing emphasis on operational efficiency and cost-effectiveness led to increased demand for outsourcing to offshore companies. The study tracks the regional and country-level market demand for IT outsourcing and provides detailed coverage of the major end-user trends affecting adoption.

The IT outsourcing market is segmented by organization size (small and medium enterprises and large enterprises), end-user vertical (BFSI, healthcare, media and telecommunication, retail and e-commerce, manufacturing, and other end-user verticals), by geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Italy, Spain, The Nordics, Benelux, Poland, and Rest of Europe), Asia-Pacific (China, India, Japan, Indonesia, Vietnam, Malaysia, South Korea, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Colombia, and Rest of Latin America), Middle East and Africa (GCC, South Africa, Turkey, and Rest of Middle East and Africa)).

The market sizes and forecasts are provided in USD for all the above segments.

| By Service Type | Infrastructure Outsourcing | |||

| Application Development and Maintenance | ||||

| Cloud-Managed Services | ||||

| Others | ||||

| By Organization Size | Small and Medium Enterprises | |||

| Large Enterprises | ||||

| By Sourcing Location | On-shore | |||

| Near-shore | ||||

| Off-shore | ||||

| By End-user Industry | BFSI | |||

| Healthcare and Life-Sciences | ||||

| Media and Telecommunications | ||||

| Retail and E-commerce | ||||

| Manufacturing | ||||

| Others | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| South Korea | ||||

| India | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| Infrastructure Outsourcing |

| Application Development and Maintenance |

| Cloud-Managed Services |

| Others |

| Small and Medium Enterprises |

| Large Enterprises |

| On-shore |

| Near-shore |

| Off-shore |

| BFSI |

| Healthcare and Life-Sciences |

| Media and Telecommunications |

| Retail and E-commerce |

| Manufacturing |

| Others |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the IT outsourcing market?

The IT outsourcing market is valued at USD 618.13 billion in 2025 and is projected to reach USD 732.38 billion by 2030.

Which service segment is growing the fastest?

Cloud-managed services lead growth with a projected 3.5% CAGR through 2030 as enterprises grapple with hybrid multicloud complexity.

Why are nearshore locations gaining traction?

Nearshore centers offer time-zone overlap, cultural affinity, and reduced geopolitical risk while maintaining meaningful cost advantages.

How is generative AI influencing outsourcing contracts?

GenAI automates service-desk functions and DevOps tasks, enabling outcome-based contracts that tie provider fees to tangible business results.

Which industry vertical shows the highest outsourcing growth potential?

Healthcare and life sciences is expected to grow at a 5.7% CAGR thanks to telehealth demand, AI-enabled diagnostics, and strict compliance requirements.

What primary challenge threatens continued outsourcing growth?

Escalating cybersecurity insurance costs and heightened data-protection regulations increase delivery complexity and may slow contract expansion.