Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

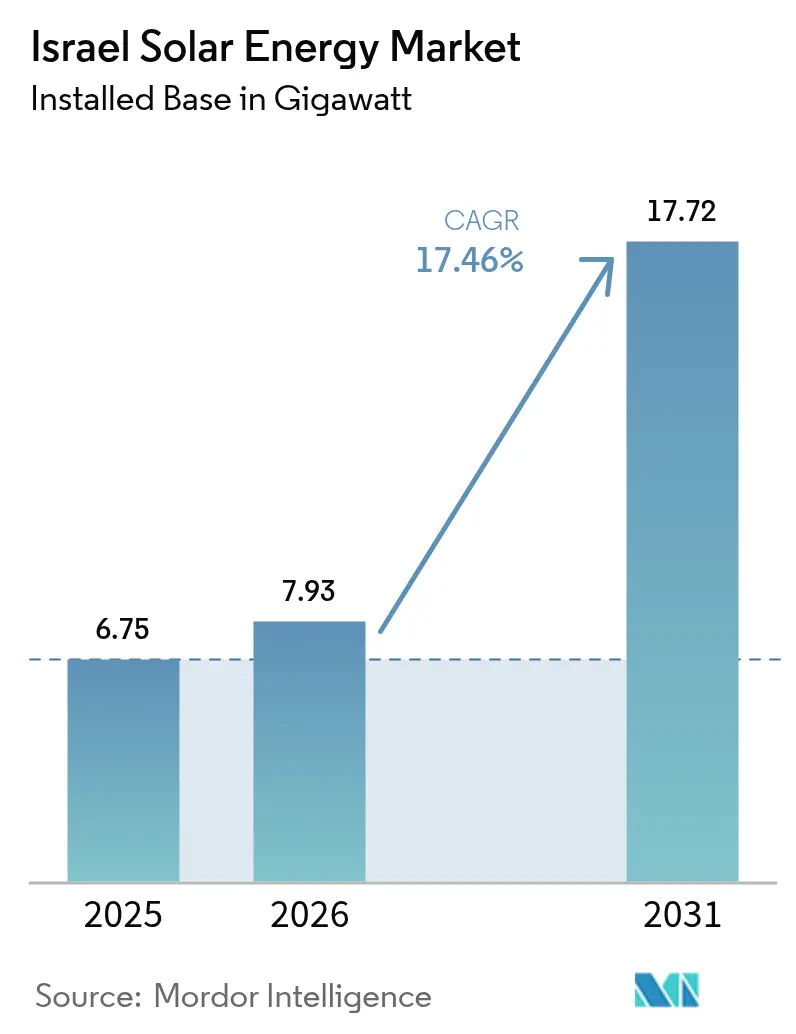

| Base Year Market Size (2025) | 6.75 gigawatt |

| Market Volume (2026) | 7.93 gigawatt |

| Market Volume (2031) | 17.72 gigawatt |

| Growth Rate (2026 - 2031) | 17.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Solar Energy Market Analysis by Mordor Intelligence

Israel Solar Energy Market size in 2026 is estimated at 7.93 gigawatt, growing from 2025 value of 6.75 gigawatt with 2031 projections showing 17.72 gigawatt, growing at 17.46% CAGR over 2026-2031.

The Israel solar energy market's growth trajectory reflects an accelerated pivot from natural gas toward renewable baseload generation, supported by Israel's 2023 Climate Law, bi-annual competitive tenders, and record-low power purchase agreement (PPA) prices. Utility-scale developers benefit from module costs below USD 0.10 per watt, while rooftop installers enjoy tariff reforms that shorten residential payback to seven–nine years. Meanwhile, declining lithium-ion prices are catalyzing the deployment of four-hour storage systems, signaling a shift toward hybrid PV-plus-battery configurations. Grid upgrades, rooftop mandates, and emerging agrivoltaic pilots collectively widen the addressable demand pool even as geopolitical risk premiums and transmission bottlenecks temper short-term build-out.

Key Report Takeaways

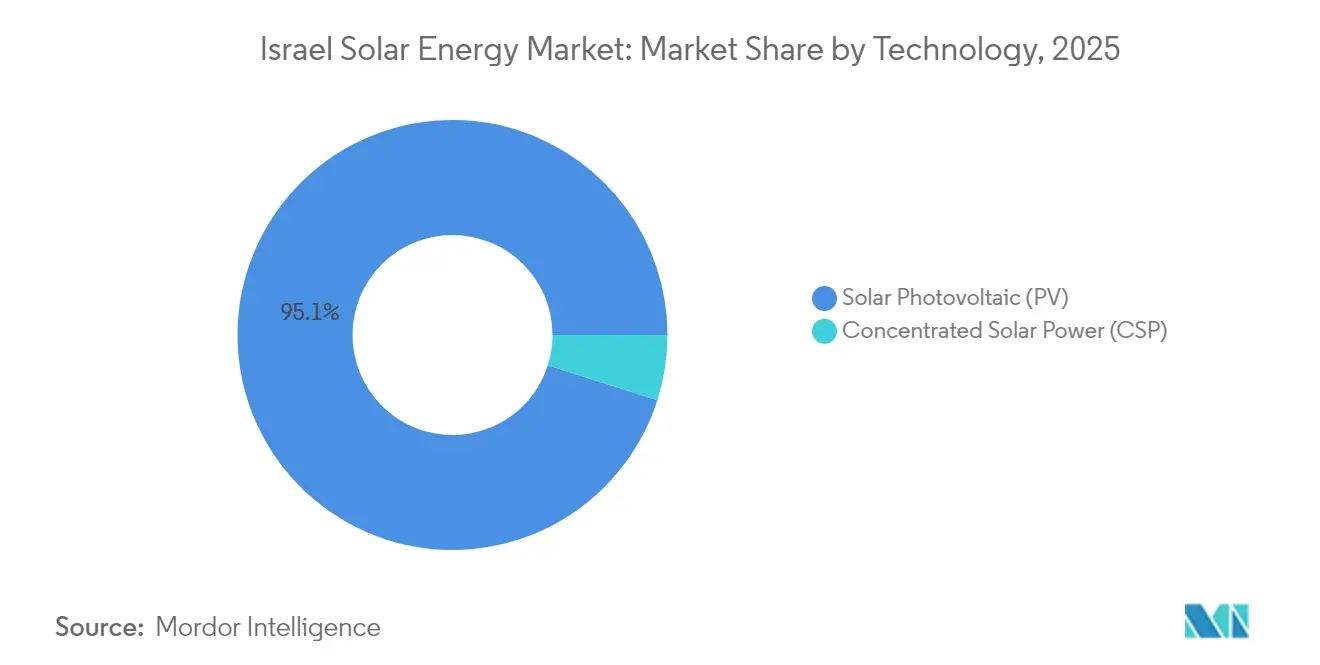

- By technology, Solar Photovoltaic commanded 95.10% of % Israel solar energy market share in 2025; Concentrated Solar Power remains a niche with dispatchable thermal storage.

- By grid type, On-Grid assets accounted for 98.55% of capacity in 2025, whereas Off-Grid installations are projected to expand at a 19.25% CAGR through 2031.

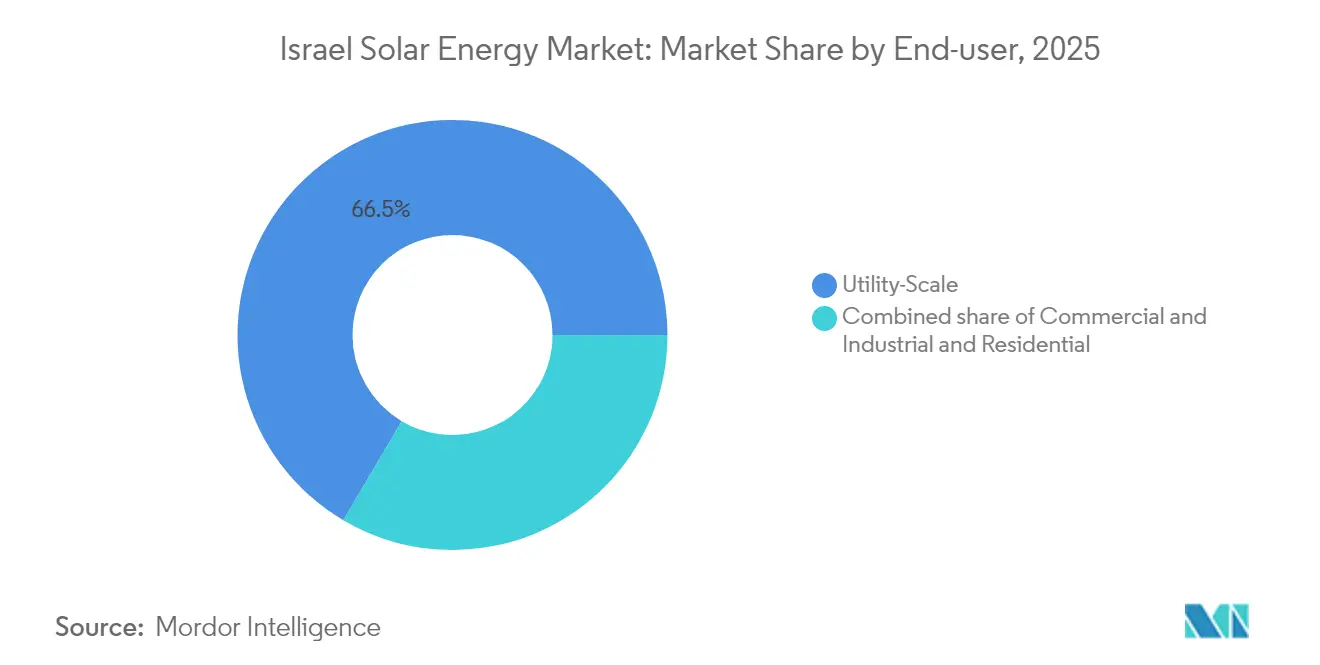

- By end-user, utility-scale plants held 66.52% of the Israel solar energy market size in 2025; the residential segment is forecast to grow fastest at 18.74% CAGR to 2031.

- By region, the Negev and Arava Valley captured 71.30% of installed capacity in 2025, while Tel Aviv metropolitan rooftops recorded the highest incremental additions.

- Enlight Renewable Energy, Doral, Nofar Energy, Shikun & Binui, and EDF Renewables controlled about 54.35% of installed capacity in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government FITs & competitive tenders | 4.20% | National, Negev & Arava zones | Short term (≤ 2 years) |

| High solar irradiance in Negev Desert | 3.10% | Negev, Arava Valley | Long term (≥ 4 years) |

| 2050 decarbonization & gas-to-RES transition | 5.30% | National | Long term (≥ 4 years) |

| Declining PV & battery costs | 3.80% | Nationwide | Medium term (2-4 years) |

| Mandatory rooftop-PV code (2024) | 2.90% | Urban metros | Medium term (2-4 years) |

| Agrivoltaics & desal-coupling initiatives | 1.40% | Negev farms, coastal plants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government FITs & Competitive Tenders Reshape Utility Economics

Competitive auctions replaced static feed-in tariffs, pushing PPA prices to ILS 0.07 per kWh in 2024 and establishing subsidy-free grid parity for the Israel solar energy market.[1]Israel Electricity Authority, “Tender Results July–August 2024,” electricity-authority.gov.il A February 2025 award covering 1.5 GW of four-hour storage further underscores policy commitment to firming variable solar output. Local-content clauses now embedded in tender rules are carving out work for domestic engineering firms even as modules remain import-dependent. Bi-annual auction cadence targeting 2 GW per year through 2027 sustains a robust pipeline, although smaller cooperatives face consolidation pressure as low bids favor developers with balance-sheet depth.

High Solar Irradiance in Negev Desert Anchors Utility-Scale Concentration

Annual irradiance of 2,200–2,500 kWh/m² in the Negev enables PV capacity factors above 23% and concentrates most future capacity south of Be’er Sheva. Single-axis tracking, bifacial modules, and TOPCon cells optimize harvests and soften land-use footprints. Despite the headline 250 MW Ashalim CSP complex, PV-plus-battery hybrids dominate new project design because they deliver similar evening dispatch at one-sixth the capital cost. Environmental safeguards, wildlife corridors, and soil-preservation measures add permitting complexity but have not derailed large-scale tenders.

2050 Decarbonization & Gas-to-RES Transition Drives Policy Commitment

Israel’s Climate Law targets 50% emission cuts by 2030 and net-zero by 2050, positioning the Israel solar energy market as the primary replacement for gas-fired generation that supplied 63% of 2024 electricity.[2]Israel Meteorological Service, “Annual Solar Irradiance Data,” ims.gov.il The “Yellow Pathway” projects 77% solar penetration and 108 GW of PV by mid-century, implying a trebling of annual build rates and extensive grid-scale storage. Corporate PPAs are accelerating as EU carbon-border measures threaten exporters, while municipal targets such as Tel Aviv’s 100% clean power pledge amplify local demand.

Declining PV & Battery Costs Compress Payback Periods

Polysilicon prices fell to USD 6.50 /kg by late 2024, driving modules below USD 0.10 /W and pushing Israel's solar energy market size projects under USD 750 /kW for fixed-tilt arrays.[3]BloombergNEF, “2024 Solar and Storage Price Survey,” about.bnef.com Lithium-ion packs averaged USD 139 /kWh in 2024 and are on track for USD 113 /kWh in 2025, turning four-hour batteries into mainstream complements for peak shaving and ancillary services. Silicon-carbide inverters and waterless cleaning robotics further reduce operating costs, though SolarEdge's restructuring shows price competition is intense even for domestic technology champions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & limited transmission capacity | −3.7% | Negev & southern grid | Short term (≤ 2 years) |

| Land-use & environmental permitting hurdles | −2.4% | Negev Desert corridors | Medium term (2-4 years) |

| Geopolitical security-risk premium on financing | −1.8% | Nationwide | Short term (≤ 2 years) |

| Import-dependency for modules & BOS | −1.3% | National supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Limited Transmission Capacity Constrain Deployment

Solar additions slowed to 900 MW in 2024 from 1.1 GW in 2023 as Negev interconnection queues lengthened. A NIS 20 billion (USD 5.4 billion) IEC plan to build 3,000 km of high-voltage lines by 2030 will ease constraints, yet four- to six-year construction timelines imply curtailment persists through 2027. Dynamic connection agreements mitigate risk but raise finance costs.

Land-Use & Environmental Permitting Hurdles Extend Project Timelines

Environmental-impact assessments, Bedouin land claims, and wildlife-corridor protections stretch utility-scale permitting to two–four years and add up to USD 50 /kW in extra costs. Water-use scrutiny for panel cleaning has accelerated the adoption of robotic systems that carry higher opex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominates as CSP Remains a Dispatchable Niche

Solar Photovoltaic accounted for 95.10% Israel's solar energy market share in 2025 and will grow 17.83% CAGR to 2031 on unbeatable capex and continuous efficiency gains. Concentrated Solar Power's 250 MW Ashalim showcase validates six-hour dispatchability yet sits at USD 4,500 /kW, far above PV-battery hybrids. Bifacial and TOPCon modules now underpin most new bids, while perovskite-silicon tandem pilots explore 33% plus efficiencies for post-2028 rollouts.

Israel's solar energy market size for CSP is projected to stagnate below 1.05 GW through 2031 unless capacity payments emerge. Conversely, floating PV on reservoirs and wastewater ponds offers land-neutral expansion, delivering 5-8% higher yields from evaporative cooling despite pricier interconnections.

By Grid Type: On-Grid Still Commands, Off-Grid Advances for Resilience

On-Grid plants represented 98.55% of installed capacity in 2025 thanks to competitive tenders and streamlined PPA bankability. Off-Grid systems, encompassing IDF bases, kibbutz microgrids, and agricultural pumps, will expand 19.25% CAGR to 2031 as security and fuel-savings targets intensify. Lithium-ion pack prices under USD 113 /kWh by 2025 are critical for four-hour autonomy, while regulatory clarity on islanded microgrids remains a gap.

By End-User: Utility-Scale Leads as Residential Rooftop Gains Momentum

Utility-scale assets captured 66.52% of Israel's solar energy market size in 2025, leveraged by headline PPAs of ILS 0.07 /kWh. Residential rooftop growth accelerates under the 2024 mandate and tariff reform, with Tel Aviv residents installing systems 20% larger than the minimum to maximize tax rebates. Commercial & Industrial rooftops report sub-five-year paybacks, yet installer shortages and financing barriers for middle-income households could temper the steep 18.74% CAGR outlook.

Geography Analysis

The Negev-Arava belt hosts 71.30% of capacity in 2025 due to world-class irradiance and low land costs, but also endures the heaviest curtailment and permitting scrutiny. Coastal desalination corridors pursue solar-powered reverse-osmosis to hedge against volatile gas pricing. Urban centers in Tel Aviv, Jerusalem, and Haifa lead rooftop penetration, aided by expedited permits and property-tax incentives. Northern border regions deploy hybrid microgrids to trim diesel reliance, reflecting defense and resilience priorities.

Regulatory Landscape

Israel's solar deployment is governed primarily by the Public Utility Authority (Electricity Authority) through tariff-setting, tender design, and grid-connection rules, with competitive auctions displacing legacy feed-in tariffs and driving record-low awarded prices (ILS 0.07/kWh in 2024). A major policy anchor is the 2024 mandatory rooftop-PV building code, with regulations taking effect on December 11, 2025 for new residential and large non-residential buildings (roof area above 250 sqm), shifting incremental capacity toward urban centers where land is constrained.

In 2026, planning and land-use rules further expanded the compliance framework for new solar build-out. The National Planning and Building Council approved agrivoltaics rules (February 2026), setting dual-use requirements such as maximum panel coverage and minimum installation heights by crop type. This creates a clearer path for PV on agricultural land, while adding measurable performance and monitoring obligations. In parallel, the Ministry of Energy and Infrastructure published its Renewable Energy 2035 strategic plan (May 2026), and government-led digital streamlining progressed with a renewable portal launched in July 2026 to centralize permitting requirements and guide project owners and developers through approvals.

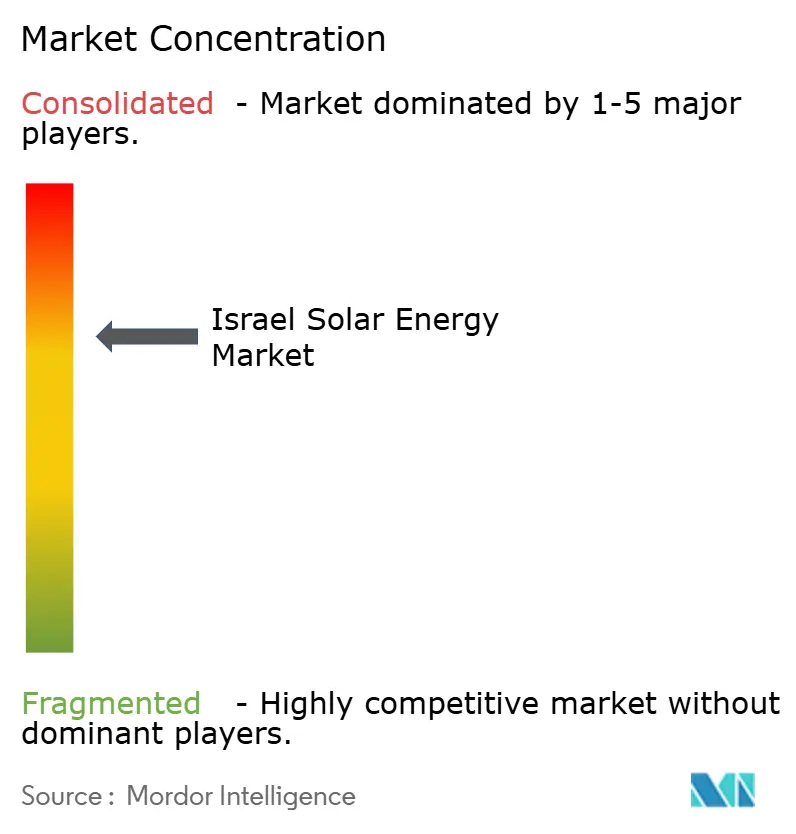

Competitive Landscape

The Israel solar energy market is moderately concentrated: Enlight, Doral, Nofar, Shikun & Binui, and EDF Renewables together hold 55% of installed capacity. International entrants such as Greencells and BELECTRIC compete aggressively on EPC pricing, driving PPA rates to historic lows. Early adoption of bifacial and TOPCon technologies differentiates cost leaders, while SolarEdge retains a 40% share in the residential hardware segment despite a 64% revenue slump in 2024. Agrivoltaic pilots and desal-coupled projects present new white-space opportunities for both domestic developers and equipment makers.

Israel Solar Energy Industry Leaders

Shikun & Binui Ltd

EDF Renewables

Enlight Renewable Energy

Doral Energy

Nofar Energy

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Israel's updated policy and financing activity in 2026 highlights near-term whitespace in segments that reduce land and grid constraints, while improving dispatchability. The Ministry of Energy and Infrastructure's May 2026 Renewable Energy 2035 plan frames a larger pipeline across agrivoltaics, dual-use installations (rooftops, parking canopies, and other built assets), and ground-mounted fields, reinforcing demand for EPC, grid-connection services, and hybrid integration capabilities that can align solar output with evening peaks. The February 2026 agrivoltaics rules also provide a defined route for dual-use land projects, creating opportunity for developers and investors able to meet agricultural-output and monitoring requirements.

Hybrid PV-plus-storage is moving from an optional design choice to a baseline approach for large projects and tender participation, supporting spend on four-hour BESS, controls, and grid services. Market evidence is visible in 2026 financing and project progress, with EDF Renewables reaching financial close for a 265 MW solar plant near Dimona under a PPP structure (May 2026), and Shikun and Binui Energy advancing a 150 MW Ashalim project paired with 460 MWh of storage through financing arrangements (June 2026). On the distributed side, the mandatory rooftop-PV code effective in December 2025 expands the addressable base for residential and commercial rooftops. In addition, the government's 2026 direction to replace solar water heaters with PV integrated with heat pumps in new construction creates additional pull-through for rooftop PV, smart inverters, and building-energy integration services.

Recent Industry Developments

- June 2026: Shikun & Binui Energy and the Noy Infrastructure & Energy Fund completed financial closing for the 150 MW Ashalim PV project with 460 MWh of energy storage, supported by ILS 577 million in financing from Bank Leumi. The transaction moves a large PV-plus-storage asset toward execution in the Negev, reinforcing the market shift toward firmed solar capacity that can better fit grid constraints and evening demand.

- May 2026: EDF Renewables reached financial close for a 265 MW solar power plant near Dimona after winning the project through a public-private partnership tender. Securing financing for a multi-hundred-megawatt facility strengthens the utility-scale pipeline at record-low auction economics and adds scale in the Negev-Arava corridor where most capacity is concentrated.

- February 2025: Israel Electricity Authority awarded a 1.5 GW tender for four-hour lithium-ion energy storage. The award expanded the bankable volume of grid-scale storage tied to solar build-out, supporting hybrid project designs and creating procurement demand for batteries, inverters, EPC, and integration services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as solar power capacity in Israel that is installed and grid connected or operating, measured in gigawatts. The scope includes solar photovoltaic (PV) and concentrated solar power (CSP) additions, and the resulting installed base across utility scale and customer sited systems.

Scope exclusions: We exclude non solar renewable sources, stand alone solar equipment trading that does not result in installed capacity, and unrelated grid infrastructure spend unless it is inseparable from solar project commissioning.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of Israel power demand, installed generation mix, and policy direction, since solar capacity is strongly guided by grid availability and regulation. We rely on public sources such as Israel government energy publications and regulator updates, Israel Electric Corporation planning materials and grid connection notices, IEA and IRENA statistical series, and peer reviewed journal articles that describe irradiance, performance ratios, and curtailment impacts.

To avoid over counting, project pipelines are screened using tender award notices, permitting disclosures, and reputable press coverage on commissioning timelines, followed by cross checks against utility interconnection queues where available. Company filings, investor presentations, and audited financial statements are used mainly to sanity check project execution pace and EPC activity. For consistency, we also use paid subscriptions for company financials and intelligence, patent databases, and shipment level import export records when equipment inflow trends help validate build rates. The sources named here are illustrative, and many other public documents were referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is actually getting built and connected, and to test assumptions on execution delays, grid constraints, and expected utilization once projects go live. We speak with a mix of developers, EPC and O&M teams, equipment distributors, utilities and grid related stakeholders, and large C&I solar buyers, which helps us align the pipeline view with on the ground commissioning reality in Israel.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 17% | Managers: 49% | Americas: 23% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where national capacity statistics, tendered volumes, and grid connection milestones are reconstructed into annual installed base additions and retirements. To keep the numbers grounded, we corroborate totals with selective bottom-up checks such as sampled project level MW roll ups from public announcements, channel checks on module and inverter inflows, and a few sanity checks using typical MW per site for rooftop programs.

Key inputs that shape the sizing include awarded capacity under government programs, connection and commissioning schedules, curtailment and grid congestion signals, rooftop versus utility scale build mix, and typical capacity factor and performance ratio ranges used by market participants. When data gaps appear for smaller installations, we handle them by applying adoption rates tied to rooftop permitting activity and historic installation run rates, then validating the implied totals with expert feedback. For forecasting, we use scenario analysis with a simple regression overlay that links annual additions to policy targets, expected grid readiness, and project pipeline maturity. The final trajectory is then adjusted after reconciling interview consensus on timing risks.

Data Validation & Update Cycle

Validation is done in several passes so that outliers do not slip into the final series. We compare model outputs with independent signals such as national installed capacity releases, project commissioning news, and import activity trends, then review any variance to determine whether it is a one time event or a persistent shift.

Before sign off, assumptions and calculations are rechecked by another analyst, and we re contact sources when a pipeline change or policy update materially shifts expected commissioning. Reports are refreshed annually, and interim updates are made when large tenders, tariff changes, or grid access rules meaningfully alter the outlook. Right before delivery, a final freshness pass is completed so clients receive the most current view available.

Mordor Intelligence's Israel Solar Energy Market Size Measured Against Other Published Estimates

Published estimates for Israel solar energy often spread out because the unit of measurement is not always the same, and some sources mix installed capacity with revenue metrics such as equipment or project spend. Timing also matters, since some numbers reflect end of year commissioned MW while others include projects that are awarded but not yet connected.

The refresh cadence and the date used for currency conversion can move the final figure, especially when inputs like equipment pricing and commissioning delays are updated mid year. Differences also come from how rooftop additions are treated, how off grid systems are counted, and whether curtailment and grid bottlenecks are used as a practical cap on near term realizations. This is why the update cycle and validation checks used by Mordor Intelligence can lead to a different capacity path than sources that mainly track policy targets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.75 B (2025) | |

| Industry Publisher A | USD 1.19 B (2020) | Uses a single year installed capacity datapoint anchored to an earlier base year, and it can understate the current market when later rooftop and utility additions are not rolled forward into an updated installed base. |

| Trade Analyst B | USD 7.93 B (2026) | Treats the next year capacity estimate as the main reference number, which can overstate the current year if commissioning slippage and grid connection constraints are not applied as timing adjustments. |

Looking across the table, most of the spread is explained by base year selection and whether pipeline capacity is counted before it is commissioned. By keeping the scope tied to installed capacity and by rechecking assumptions when new connection and tender signals appear, the final number stays traceable to clear build rates rather than optimistic target language.

Key Questions Answered in the Report

How fast is installed capacity expected to grow in the Israel solar energy market?

Capacity is projected to climb from 7.93 GW in 2026 to 17.72 GW by 2031, reflecting a 17.46% CAGR.

Why are PPA prices in Israel now among the lowest globally?

Competitive auctions, high solar irradiance, and falling module costs pushed 2024 PPA bids to ILS 0.07 /kWh (USD 0.019 /kWh).

Which segment will expand the quickest through 2031?

Residential rooftop systems are forecast to grow at 18.74% CAGR, boosted by the 2024 mandatory-PV building code and higher net-metering rates.

What is the main obstacle to faster utility-scale build-out?

Grid congestion in the Negev and Arava regions delays connections and caused 4.2% curtailment of potential generation in 2024.

How are battery prices influencing project economics?

Lithium-ion pack prices dropped to USD 139 /kWh in 2024 and are projected to hit USD 113 /kWh in 2025, making four-hour storage viable for peak shaving and ancillary services.

Which technologies are developers favoring for new projects?

Bifacial TOPCon PV modules paired with four-hour lithium-ion batteries dominate current bids due to higher yield and lower levelized cost of energy.

Page last updated on: