ISO Tank Container Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

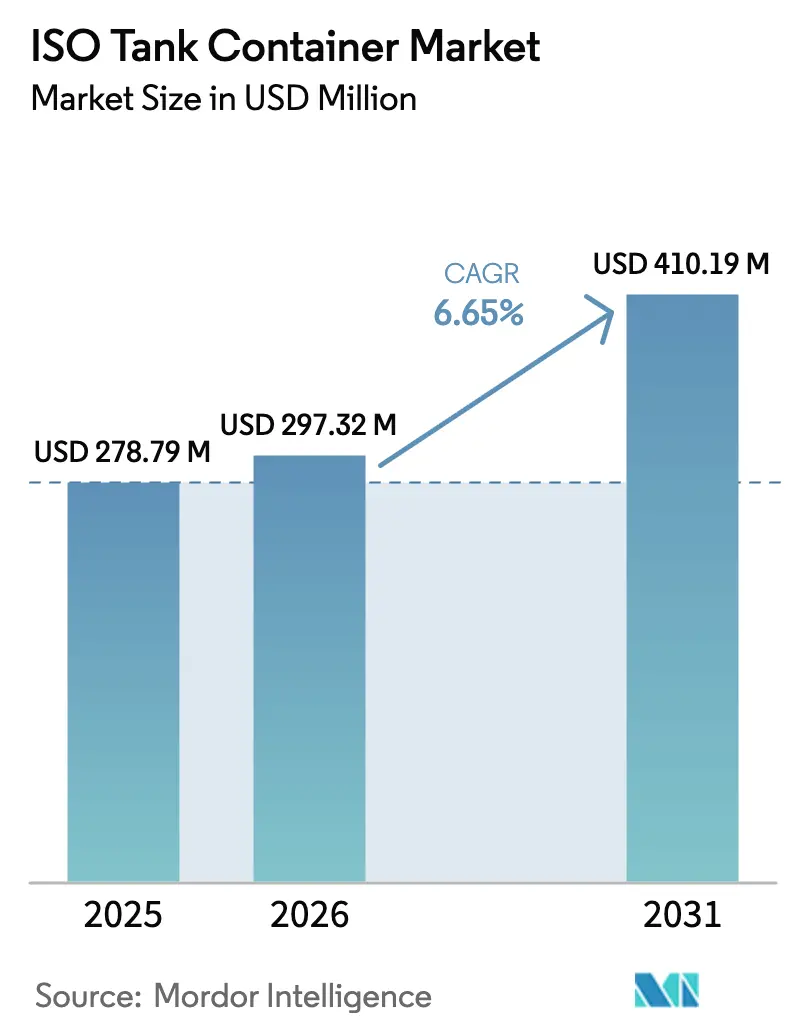

| Market Size (2026) | USD 297.32 Million |

| Market Size (2031) | USD 410.19 Million |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

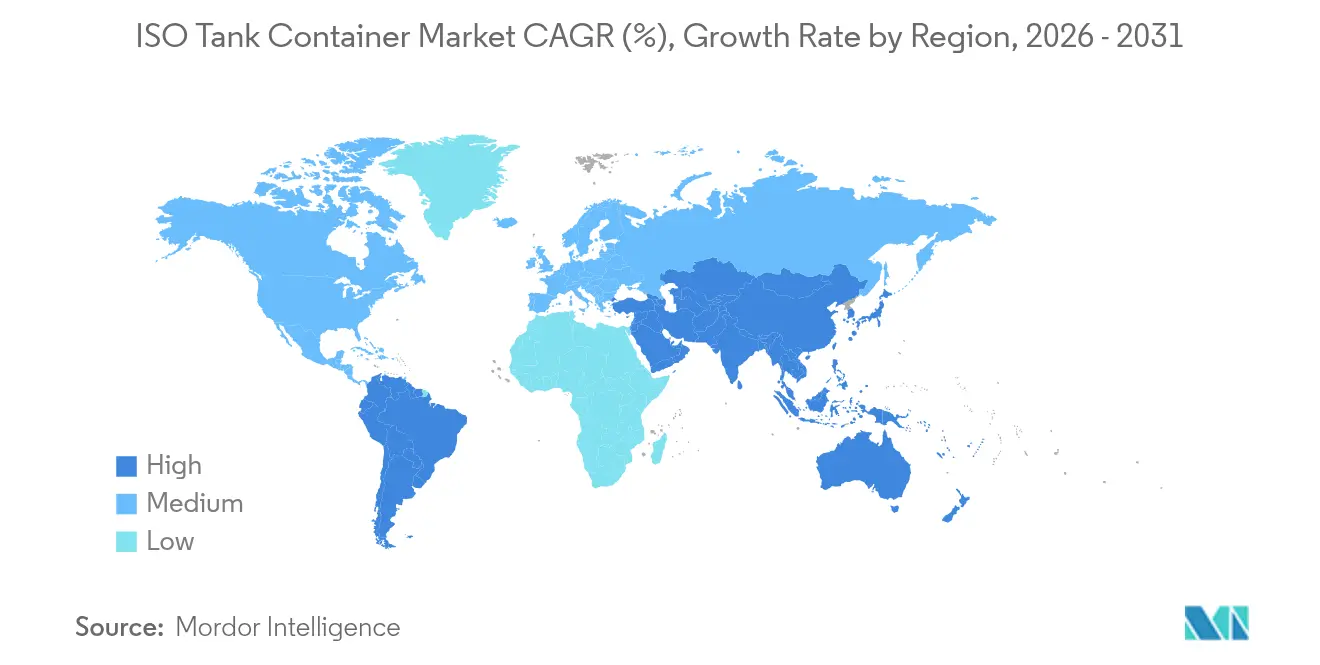

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

ISO Tank Container Market Analysis by Mordor Intelligence

The ISO tank container market size was valued at USD 278.79 million in 2025 and estimated to grow from USD 297.32 million in 2026 to reach USD 410.19 million by 2031, at a CAGR of 6.65% during the forecast period (2026-2031). The expansion is underpinned by steady liquid-bulk trade, stricter global safety rules, and rapid hydrogen infrastructure roll-outs that favor cryogenic equipment. Integrated telematics, multi-compartment designs, and leasing platforms are reshaping fleet economics while stainless steel price swings and depot shortages pressure smaller operators. Asia-Pacific dominates volumes on the back of manufacturing growth and intermodal upgrades, whereas Europe sets the regulatory tone with new ADR and IMDG amendments. Consolidation continues as logistics majors and lessors acquire specialized fleets to secure capacity and embed end-to-end services.

Key Report Takeaways

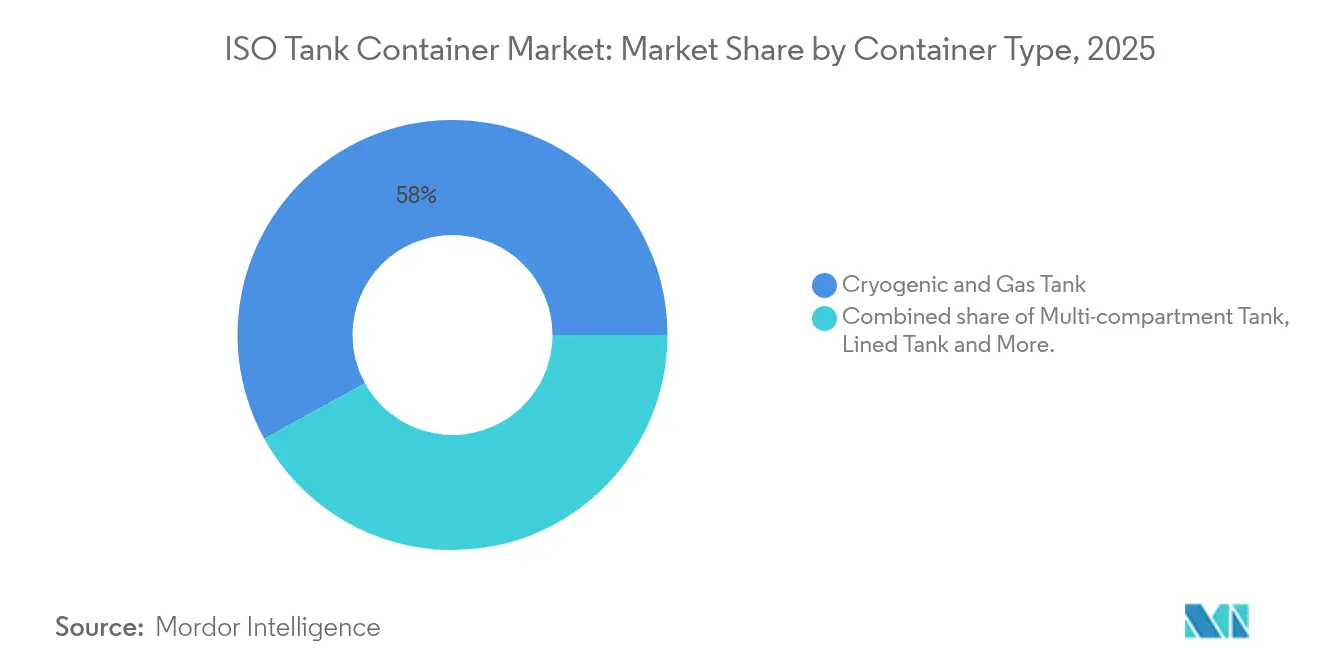

- By container type: Cryogenic and Gas units led with 58.02% ISO tank container market share in 2025, while Multi-compartment designs are projected to expand at a 9.65% CAGR through 2031.

- By end-use industry: Chemicals held 44.01% revenue share of the ISO tank container market size in 2025; Industrial Gas is advancing at a 9.22% CAGR to 2031.

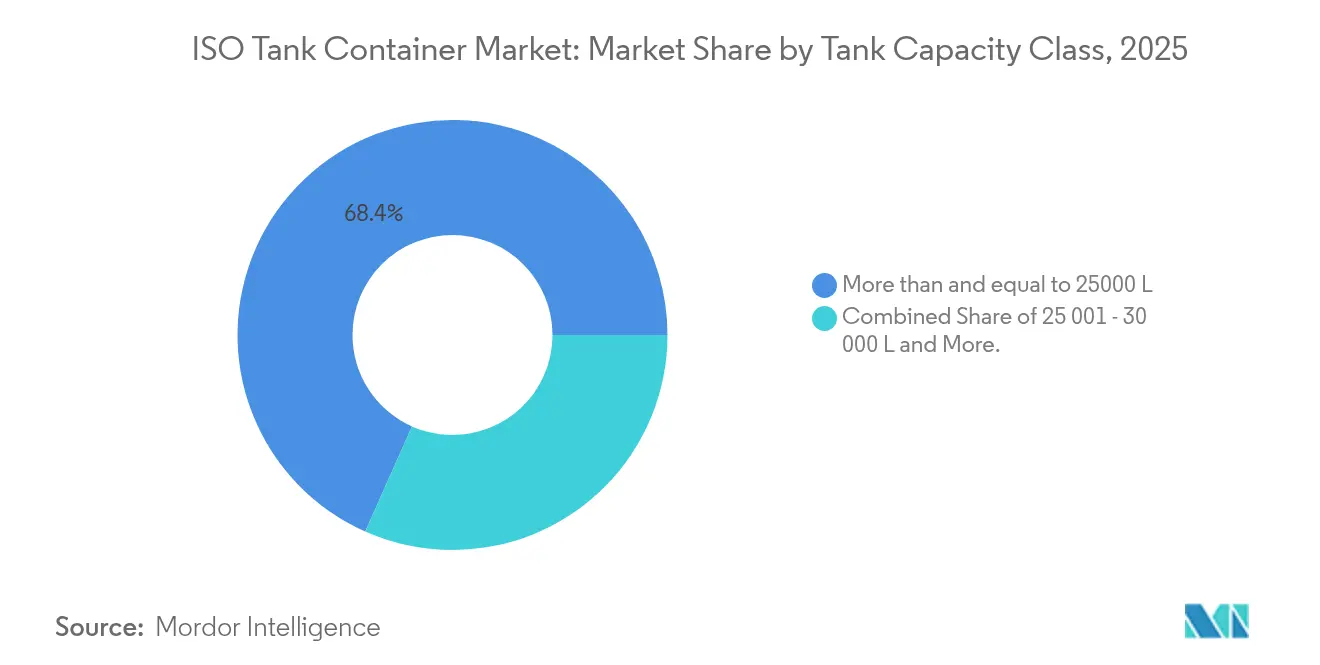

- By tank capacity: Units ≤25,000 L captured 68.35% share in 2025; tanks >30,000 L are forecast to rise at a 9.41% CAGR through 2031.

- By ownership model: Operator-owned fleets accounted for 49.78% revenue in 2025, whereas leasing is set to grow at 9.76% CAGR through 2031.

- By geography: Asia-Pacific commanded 42.02% revenue share in 2025 and is progressing at a 9.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global ISO Tank Container Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for chemical and liquid bulk transport | +2.1% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| Shift from drums/flexitanks to ISO for cost and safety | +1.8% | Global, with early adoption in North America and EU | Short term (≤ 2 years) |

| Rapid expansion of food-grade and pharma cold-chain trade | +1.5% | Global, led by Asia-Pacific emerging markets | Medium term (2-4 years) |

| Stricter UN/IMO safety and environmental regulations | +1.2% | Global maritime routes, strongest in EU and North America | Long term (≥ 4 years) |

| Intermodal network upgrades in emerging economies | +0.9% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Hydrogen and LNG bunkering driving cryogenic ISO uptake | +0.6% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Chemical and Liquid Bulk Transport

Chemical industry consolidation drives specialized transport requirements as manufacturers seek cost-effective solutions for hazardous and non-hazardous liquid cargo. The German chemical sector, generating EUR 200 billion (USD 226 billion) in annual revenues, faces logistics costs of EUR 10 billion (USD 11.3 billion), creating pressure for transport optimization. Den Hartogh's collaboration with Sun Chemical exemplifies this trend, where customized ISO tanks achieved 72% reduction in road mileage and 19% payload capacity increase through improved insulation design. Nova Chemicals' implementation of advanced planning systems demonstrates how chemical manufacturers integrate tank container logistics with production scheduling to optimize supply chain efficiency. The shift toward just-in-time delivery models requires tank containers with enhanced tracking capabilities, as evidenced by Den Hartogh's telematics implementation across its 24,100-unit fleet for continuous monitoring of location, temperature, and pressure parameters.

Shift from Drums/Flexitanks to ISO for Cost and Safety

Traditional packaging methods face increasing scrutiny as companies prioritize safety and environmental compliance over initial cost savings. The International Tank Container Organisation's technical guidance emphasizes ISO tanks' superior safety profile compared to drums and flexitanks, particularly for hazardous materials requiring specific gravity considerations and thermal expansion accommodation. KriCon Group's flexitank division, launched in 2022, acknowledges this limitation by restricting flexitank use to non-hazardous liquids only, while recommending traditional tank containers for hazardous materials due to their stability and structural integrity. The economic advantage becomes apparent in cross-contamination prevention, where ISO tanks eliminate the need for single-use packaging and reduce waste disposal costs. Quality Carriers' 2024 patent for domestic tank container design specifically addresses intermodal efficiency improvements, enabling seamless transitions between rail, road, and sea transport modes. Container utilization rates improve significantly as ISO tanks eliminate empty repositioning requirements inherent in flexitank operations, reducing overall logistics costs and carbon footprint.

Rapid Expansion of Food-Grade and Pharma Cold-Chain Trade

Temperature-controlled pharmaceutical logistics experiences unprecedented growth as the sector transitions from 30% to 70% utilization of reusable temperature-controlled packaging systems. SkyCell's introduction of the 1500X Hybrid container with 270-hour independent runtime addresses critical pharmaceutical transport requirements, ensuring product integrity during extended transit periods. The Asia-Pacific food packaging market demonstrates remarkable expansion at 12.60% CAGR, with India experiencing 200% increase in packaging consumption over the past decade due to urbanization and changing consumer preferences. Cold Chain Technologies' establishment of a new manufacturing facility in Breda, Netherlands, reflects European market expansion for thermal packaging solutions targeting life sciences applications. Modal shift from air to sea transport gains momentum as pharmaceutical companies seek to reduce CO2 emissions, with ocean shipping generating significantly lower greenhouse gas emissions than airfreight while requiring careful inventory planning due to longer shipping times.

Stricter UN/IMO Safety and Environmental Regulations

The International Maritime Organization's IMDG Code Amendment 42-24, effective January 2025, introduces enhanced safety requirements for dangerous goods transport, directly impacting tank container specifications and operational procedures. The United Nations Economic Commission for Europe's ADR 2025 and ADN 2025 agreements establish comprehensive frameworks for dangerous goods transport by road and inland waterways, requiring tank container operators to meet stringent construction and testing standards [1]United Nations Economic Commission for Europe. "ADR 2025 - Agreement concerning the International Carriage of Dangerous Goods by Road." January 2, 2025. https://unece.org/adr-2025-files..Russia's energy export requirements and emerging markets in Eastern Europe present growth opportunities despite geopolitical challenges.

North America benefits from established intermodal infrastructure and regulatory frameworks, with the Intermodal Association of North America reporting 7.9% year-over-year volume increase in Q2 2024, driven by 13.3% growth in international containers. DP World's A$400 million (USD 280 million) investment with NSW Ports to expand rail capacity at Sydney's Port Botany demonstrates infrastructure commitment to container transport efficiency. The United States leads in regulatory development with EPA's PFAS National Primary Drinking Water Regulation affecting tank container lining materials and cleaning procedures [2]Federal Register. "PFAS National Primary Drinking Water Regulation." April 26, 2024. https://www.federalregister.gov/documents/2024/04/26/2024-07773/pfas-national-primary-drinking-water-regulation..

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and specialised maintenance costs | -1.4% | Global, particularly affecting smaller operators | Short term (≤ 2 years) |

| Limited depot/cleaning infrastructure at secondary ports | -0.9% | Emerging markets, secondary port locations | Medium term (2-4 years) |

| Stainless-steel price volatility squeezing margins | -0.7% | Global manufacturing hubs, Asia-Pacific focus | Short term (≤ 2 years) |

| Tightening PFAS-lining rules constraining tank supply | -0.5% | North America and EU regulatory jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Specialised Maintenance Costs

Tank container manufacturing requires substantial capital investment, with specialized stainless steel grades and precision engineering driving unit costs significantly above standard dry containers. Damstahl's November 2024 market analysis reveals challenging conditions in the stainless steel industry, with stable nickel prices around USD 16,000 per ton but high ferromolybdenum prices at USD 50,000 per ton creating cost pressures for manufacturers. The complexity of multi-compartment tank designs further escalates manufacturing costs, as these units require additional internal structures, specialized valves, and enhanced safety systems. Maintenance requirements extend beyond standard container servicing, demanding specialized cleaning facilities, pressure testing equipment, and certified technicians familiar with hazardous materials handling protocols. The COTAC depot reopening in Houston exemplifies infrastructure investment needs, as specialized cleaning facilities require significant capital for equipment and regulatory compliance. Smaller operators face particular challenges in justifying capital expenditure for specialized equipment, leading to market consolidation as larger players acquire assets and expertise to achieve economies of scale.

Limited Depot/Cleaning Infrastructure at Secondary Ports

Secondary port locations often lack adequate tank container cleaning and maintenance infrastructure, creating operational bottlenecks and increased repositioning costs. Heniff Transportation's strategic acquisitions, including TechnoPort for international ISO tank services, highlight industry efforts to expand depot networks and address infrastructure gaps. The development of specialized cleaning facilities requires substantial investment in wastewater treatment systems, vapor recovery equipment, and regulatory compliance infrastructure. Quantix's opening of a new tank cleaning location in Port Allen, Louisiana, and Stolt's Houston facility upgrades demonstrate ongoing industry investment in cleaning capabilities. Methanol butterworthing technology emerges as a revolutionary tank cleaning method, utilizing methanol to enhance cleaning efficiency while reducing greenhouse gas emissions during operations. The challenge intensifies in emerging markets where regulatory frameworks for hazardous waste handling remain underdeveloped, limiting the establishment of compliant cleaning facilities and constraining market growth in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Container Type: Cryogenic Dominance Drives Hydrogen Economy

Cryogenic and Gas Tank containers maintain market leadership with 58.02% share in 2025, benefiting from accelerating hydrogen infrastructure development and LNG bunkering applications. DB Cargo's introduction of a multi-element gas container (MEGC) for rail transport of gaseous hydrogen, developed with Hexagon Purus and other partners, demonstrates technological advancement in this segment. The container, approved for 500 bar pressure and capable of carrying 1,223 kg of hydrogen, replaces up to 52 trucks while reducing CO₂ emissions by over 80%. CIMC's hydrogen revenue surge to 1 billion yuan (USD 139 million) in 2024, with expectations to double by 2025, reflects growing demand for hydrogen storage and transport solutions. Multi-compartment Tank containers emerge as the fastest-growing segment at 9.65% CAGR, driven by chemical industry requirements for segregated transport and operational efficiency improvements. These containers enable simultaneous transport of multiple products while preventing cross-contamination, reducing the number of shipments required and optimizing logistics costs. Lined Tank containers serve specialized applications requiring chemical compatibility, while Reefer Tank containers support temperature-sensitive cargo transport. Swap-Body Tank containers, primarily used in European intermodal operations, facilitate efficient rail-road transfers through standardized lifting systems and corner fittings compatible with European railway infrastructure.

By End-use Industry: Chemical Leadership Amid Industrial Gas Acceleration

The Chemicals sector dominates with 44.01% market share in 2025, supported by Germany's chemical industry generating EUR 200 billion (USD 226 billion) in annual revenues and facing logistics costs of EUR 10 billion (USD 11.3 billion). Den Hartogh's case study with Sun Chemical demonstrates sector innovation, where customized ISO tanks achieved 72% reduction in road mileage through improved insulation design and self-heating systems. The Petrochemicals segment benefits from integrated supply chain optimization as refiners seek cost-effective transport solutions for intermediate products and finished goods.

Industrial Gas applications represent the fastest-growing segment at 9.22% CAGR, propelled by hydrogen economy expansion and alternative fuel adoption. CIMC Enric's record deal for 1,000 dual 1,500L LNG on-vehicle cylinders, marking the largest single order in China, reflects growing demand for gas transport solutions.

By Tank Capacity Class: Smaller Tanks Dominate Amid Large-Capacity Growth

Containers with ≤ 25,000 L capacity command 68.35% market share in 2025, reflecting demand for flexible, cost-effective transport solutions suitable for diverse cargo types and intermodal operations. These smaller tanks offer operational advantages including easier handling, reduced capital investment, and compatibility with standard container handling equipment at ports and terminals. The 25,001 – 30,000 L segment serves mid-range applications where cargo volume justifies larger capacity while maintaining operational flexibility.Containers with > 30,000 L capacity emerge as the fastest-growing segment at 9.41% CAGR, driven by bulk chemical transport optimization and economies of scale in high-volume applications. Large-capacity tanks reduce per-unit transport costs for bulk liquids while minimizing the number of containers required for major shipments. GTT's ballast-split design for LNG carriers demonstrates technological advancement in large-capacity applications, optimizing operations by partitioning ballast tanks to reduce liquid motion and improve boil-off rates. The design addresses challenges in partial cargo loading, particularly in the 10 to 40% tank height range, leading to lower hull and containment system costs. Regulatory compliance becomes increasingly complex for larger tanks, requiring enhanced safety systems and specialized handling procedures.

By Ownership / Service Model: Leasing Gains Momentum

Operator-Owned (Logistics Firms) maintains the largest share at 49.78% in 2025, reflecting integrated logistics providers' preference for asset control and operational flexibility. Major logistics companies invest in tank container fleets to ensure equipment availability and maintain service quality standards. Den Hartogh's fleet of 24,100 tank containers exemplifies this model, enabling comprehensive global transport services with integrated telematics and tracking capabilities.Lessor-Owned (Leasing) emerges as the fastest-growing segment at 9.76% CAGR, driven by capital efficiency and operational flexibility benefits. Peacock Container's successful closure of a USD 350 million debt facility extension supports fleet growth and demonstrates investor confidence in the leasing model. Container xChange's launch of a free leasing marketplace in January 2025 facilitates transparent, accessible container leasing transactions .

Geography Analysis

Asia-Pacific dominates the ISO Tank Container Market with 42.02% share in 2025 and leads growth at 9.68% CAGR through 2031, driven by manufacturing expansion, infrastructure development, and trade volume increases. China's position as the world's largest container manufacturer, with CIMC reporting hydrogen-related revenues of 1 billion yuan (USD 139 million) in 2024, reinforces the region's manufacturing leadership. India's food packaging market demonstrates remarkable growth at 12.60% CAGR, with 200% increase in packaging consumption over the past decade due to urbanization and changing consumer preferences. CJ Logistics' initiation of South Korea's first liquefied hydrogen transportation, utilizing regulatory sandbox approval from the Ministry of Trade, Industry, and Energy, establishes industry standards for hydrogen logistics. CJ Logistics' initiation of South Korea's first liquefied hydrogen transportation, utilizing regulatory sandbox approval from the Ministry of Trade, Industry, and Energy, establishes industry standards for hydrogen logistics

Europe maintains significant market presence through technological innovation and regulatory leadership, with companies like Vopak reporting strong FY 2024 results including EUR 376 million (USD 425 million) net profit and EUR 1,170 million (USD 1.32 billion) proportional EBITDA .Germany's chemical industry, generating EUR 200 billion (USD 226 billion) in annual revenues, drives regional demand for specialized transport solutions DACHSER. The United Kingdom's maritime expertise and France's chemical manufacturing base contribute to market development, while regulatory frameworks like ADR 2025 and ADN 2025 establish comprehensive safety standards for dangerous goods transport UNECE. Russia's energy export requirements and emerging markets in Eastern Europe present growth opportunities despite geopolitical challenges. North America benefits from established intermodal infrastructure and regulatory frameworks, with the Intermodal Association of North America reporting 7.9% year-over-year volume increase in Q2 2024, driven by 13.3% growth in international containers. DP World's A$400 million (USD 280 million) investment with NSW Ports to expand rail capacity at Sydney's Port Botany demonstrates infrastructure commitment to container transport efficiency . The United States leads in regulatory development with EPA's PFAS National Primary Drinking Water Regulation affecting tank container lining materials and cleaning procedures. Canada's intermodal terminal network and Mexico's nearshoring benefits, with 22.6% rise in Mexican intermodal traffic compared to Q2 2023, support regional growth.

Competitive Landscape

The ISO Tank Container Market demonstrates moderate consolidation with intensifying competition among established players and emerging regional manufacturers. Market concentration increases through strategic acquisitions, as evidenced by Heniff Transportation's purchase of TechnoPort for international ISO tank services expansion and TITAN Containers' acquisition of ALPHA Containers in Denmark. Leading manufacturers differentiate through technological innovation, with CIMC's hydrogen revenue surge to 1 billion yuan (USD 139 million) demonstrating successful diversification into alternative fuel.

Strategic patterns focus on vertical integration and service expansion, with companies like Den Hartogh implementing telematics across 24,100 tank containers to enhance monitoring capabilities and customer insights. Leasing companies gain prominence through capital efficiency models, with Peacock Container securing USD 350 million debt facility extension and Container xChange launching a free leasing marketplace. White-space opportunities emerge in hydrogen transport infrastructure, specialized food-grade applications, and emerging market depot development. Quality Carriers' U.S. patent for domestic tank container design indicates ongoing innovation in intermodal capabilities, while DB Cargo's multi-element gas container for hydrogen rail transport demonstrates technological advancement in alternative fuel applications.

ISO Tank Container Industry Leaders

-

Intermodal Tank Transport

-

Bertschi AG

-

Bulkhaul Limited

-

Royal Den Hartogh Logistics

-

HOYER GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Container xChange launched a free leasing marketplace aimed at enhancing container leasing efficiency by connecting container owners with lessees through a transparent, accessible platform that streamlines leasing transactions and improves market liquidity.

- January 2025: DP World and NSW Ports announced a co-investment of A$400 million (USD 280 million) to expand rail capacity at Sydney's Port Botany, enhancing container transport efficiency and supporting the growing intermodal market in Australia.

- December 2024: Heniff Transportation completed the acquisition of TechnoPort, expanding its international ISO tank services capabilities and strengthening its position in the global tank container market through enhanced service offerings.

- November 2024: CEVA Logistics reported that pharmaceutical industry utilization of reusable temperature-controlled packaging is expected to increase from 30% to 70%, driven by sustainability initiatives and cost efficiency improvements in cold chain logistics.

Global ISO Tank Container Market Report Scope

ISO tank containers are standardized, large containers designed for the safe and efficient transportation of bulk liquids and gases. Built to comply with International Organization for Standardization (ISO) standards, they facilitate seamless movement across sea, road, and rail transport modes.

The study tracks the revenue accrued through the sale of the ISO tank container market by various players across the globe. it also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The ISO tank container market is segmented by container type (multi-compartment tank, lined tank, reefer tank, cryogenic & gas tanks, and swap body tank), transport mode (road, rail, and marine), end-use industry (chemicals, petrochemicals, food & beverage, pharmaceuticals, industrial, and others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Multi-compartment Tank |

| Lined Tank |

| Reefer Tank |

| Cryogenic and Gas Tank |

| Swap-Body Tank |

| Chemicals |

| Petrochemicals |

| Food and Beverage |

| Pharmaceuticals |

| Industrial Gas |

| Other End-use Industry |

| Less than and equal to 25000 L |

| 25001 - 30000 L |

| More than 30000 L |

| Lessor-Owned (Leasing) |

| Operator-Owned (Logistics Firms) |

| Shipper-Owned |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Container Type | Multi-compartment Tank | ||

| Lined Tank | |||

| Reefer Tank | |||

| Cryogenic and Gas Tank | |||

| Swap-Body Tank | |||

| By End-use Industry | Chemicals | ||

| Petrochemicals | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Industrial Gas | |||

| Other End-use Industry | |||

| By Tank Capacity Class | Less than and equal to 25000 L | ||

| 25001 - 30000 L | |||

| More than 30000 L | |||

| By Ownership / Service Model | Lessor-Owned (Leasing) | ||

| Operator-Owned (Logistics Firms) | |||

| Shipper-Owned | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the ISO tank container market by 2031?

The ISO tank container market is forecast to reach USD 410.19 million by 2031, growing at a 6.65% CAGR.

Which container type currently leads the ISO tank container market?

Cryogenic and Gas tank containers dominate with 58.02% share, driven by hydrogen and LNG demand.

Why are leasing models growing rapidly in ISO tanks?

Leasing offers capital efficiency and fleet flexibility; it is expanding at a 9.76% CAGR, supported by debt-financed fleet growth and digital marketplaces.

Which region is expected to record the fastest growth?

Asia-Pacific will advance at a 9.68% CAGR to 2031, fueled by manufacturing expansion and hydrogen pilots.

How are new regulations influencing tank design?

IMDG 42-24, ADR 2025, and EPA PFAS rules are tightening safety and lining standards, prompting investment in advanced materials and monitoring systems.

Page last updated on: