Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

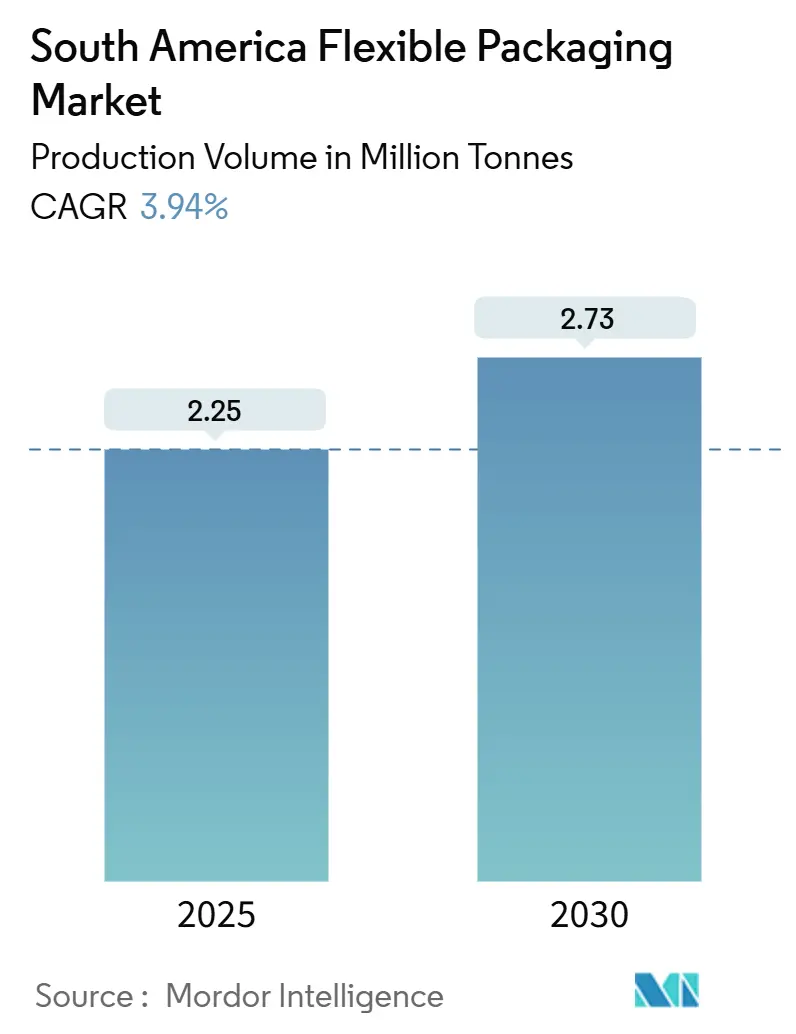

| Market Volume (2025) | 2.25 Million tonnes |

| Market Volume (2030) | 2.73 Million tonnes |

| Growth Rate (2025 - 2030) | 3.94% CAGR |

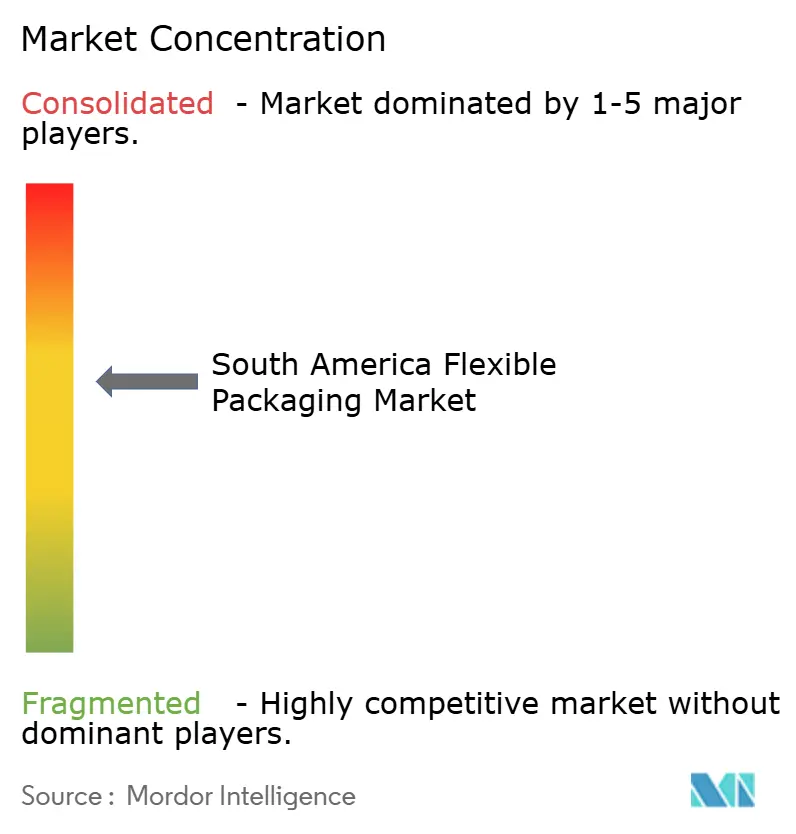

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Flexible Packaging Market Analysis by Mordor Intelligence

The South America flexible packaging market size stood at 2.25 million tonnes in 2025 and is projected to reach 2.73 million tonnes by 2030 at a 3.94% CAGR. E-commerce growth, premium pet nutrition trends, and region-specific recyclability mandates support this measured expansion. Plastics retain their dominance thanks to an entrenched converting base, yet paper solutions are gaining traction as consumer-packaged-goods (CPG) owners trial mono-material formats to meet forthcoming recycled-content targets. In product terms, stand-up pouches outperform because they travel well through last-mile networks and meet the rising expectations for barrier performance in food, pharmaceutical, and pet care channels. Brazil’s leadership is secure on the back of its advanced regulatory framework and large consumer base, while Argentina supplies the fastest incremental volumes as macro-economic reforms foster renewed investment. Consolidation accelerates as large multinationals seek to scale and secure post-consumer-recycled (PCR) supply chains to navigate tightening regulations across Brazil, Chile, and the Pacific Alliance bloc.

Key Report Takeaways

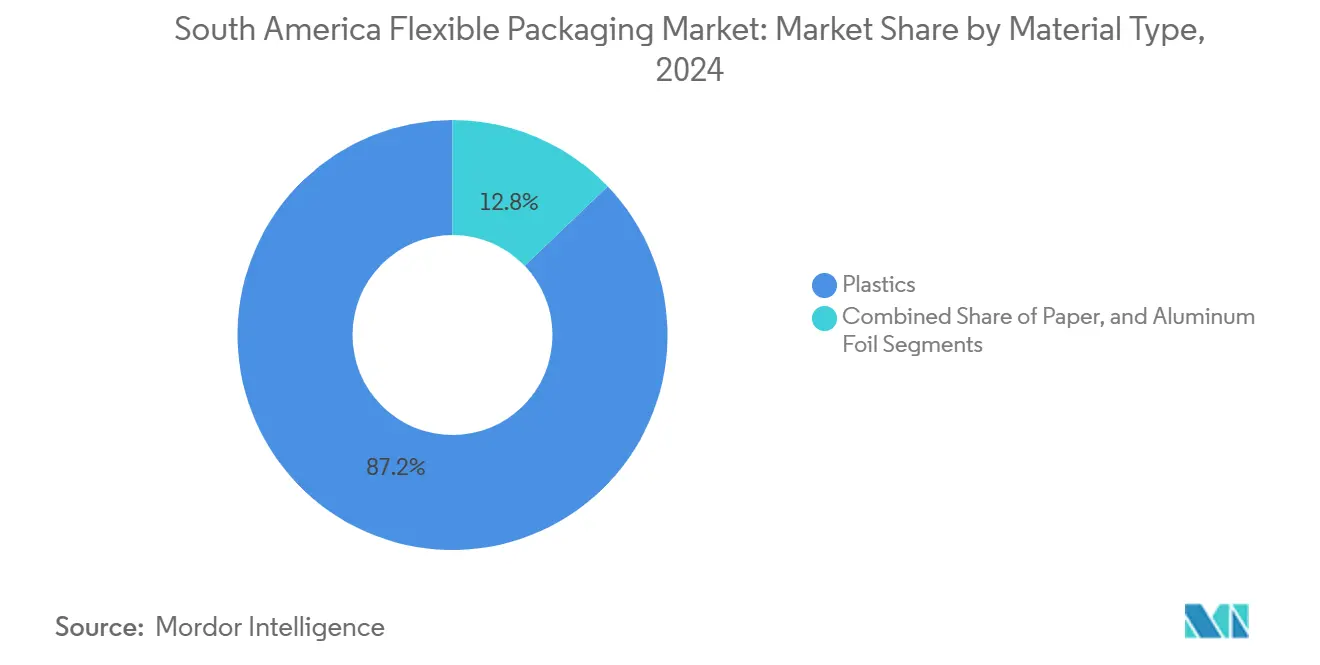

- By material type, plastics led with 87.16% of South America's flexible packaging market share in 2024; paper is forecast to expand at a 4.78% CAGR to 2030.

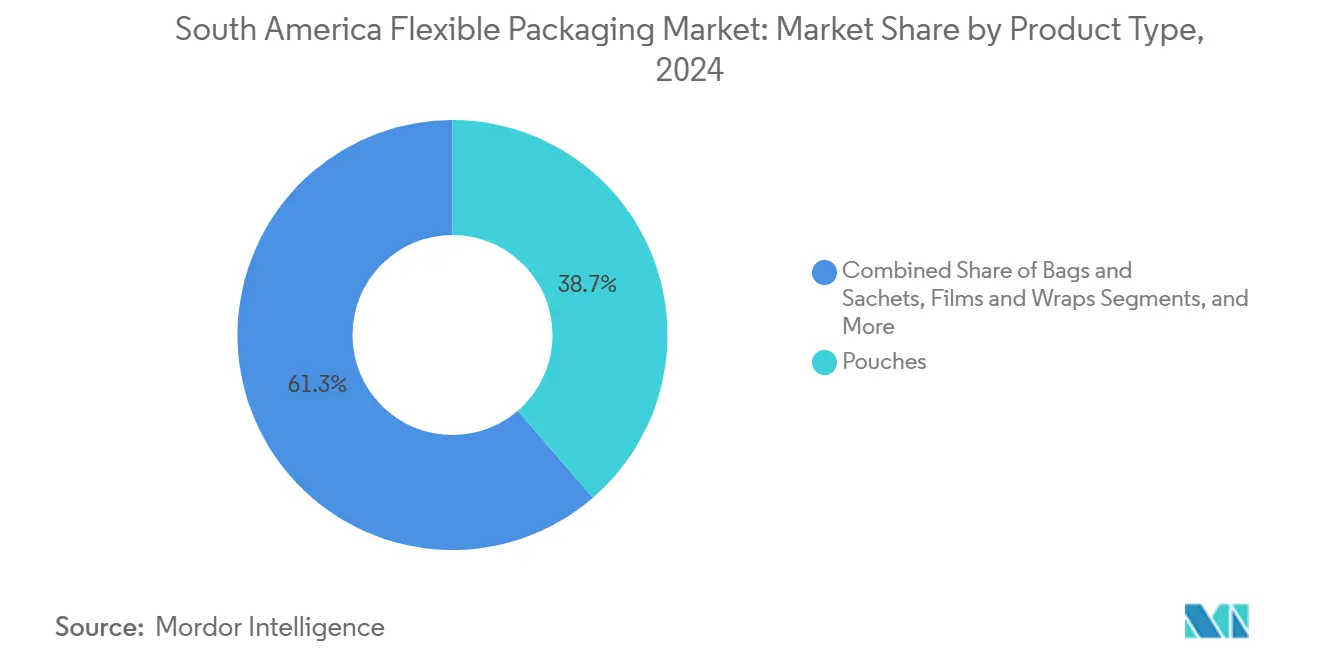

- By product type, pouches commanded a 38.67% share of the South America flexible packaging market size in 2024 and are projected to advance at a 4.36% CAGR through 2030.

- By end-user industry, food applications accounted for a 55.29% share of the South America flexible packaging market size in 2024, while pharmaceuticals and medical devices are projected to grow at a 4.52% CAGR from 2024 to 2030.

- By country, Brazil held 35.54% of the South America flexible packaging market share in 2024; Argentina is projected to record the highest CAGR at 4.43% through 2030.

South America Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in e-commerce fulfilment packaging | +1.2% | Brazil, Mexico, Colombia | Medium term (2-4 years) |

| Rising demand for high-barrier snack pouches | +0.8% | Brazil core, spill-over to Argentina, Chile | Short term (≤ 2 years) |

| Mandatory recycled-content quotas in Brazil and Chile | +0.6% | Brazil and Chile | Long term (≥ 4 years) |

| Cold-chain expansion for fresh produce exports | +0.5% | Colombia, Argentina, Chile | Medium term (2-4 years) |

| Adoption of mono-material PE/PP laminates by CPGs | +0.4% | Brazil, Mexico | Medium term (2-4 years) |

| Booming premium pet-food segment | +0.3% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Boom in E-commerce Fulfilment Packaging

Regional digital-commerce sales continue to rise as consumers migrate toward online grocery and meal-delivery platforms, generating higher parcel volumes that favor lightweight flexible formats. World Bank economists expect South America and the Caribbean GDP to grow 2.5% in 2025, up from 2.2% in 2024, a trend that underpins household consumption.[1]World Bank Prospects Group, “Global Economic Prospects,” worldbank.org Large converters, such as Berry Global, reported modest volume gains in South American consumer films in fiscal 2024, crediting pantry-loading and grocery channel shifts. Mexico’s USD 2.5 billion food-delivery sector generated more than 300,000 tons of packaging waste in 2024, yet less than 10% of it entered recycling streams, highlighting an urgent need for lighter, easier-to-recycle flexible options. Brands now specify recyclable mono-material mailer films and high-barrier pouches for ambient foods to cut freight weight and carbon footprints while protecting contents during erratic last-mile handling. The e-commerce channel, therefore, adds a predictable baseline of multi-SKU demand to the South America flexible packaging market.

Rising Demand for High-Barrier Snack Pouches

Convenience-oriented consumers favor resealable snack, treat, and premium pet foods that require oxygen- and moisture-barrier structures to preserve quality in warm, humid climates. Brazil’s pet population of 139.3 million animals generated more than BRL 15 billion (USD 0.18 billion) in 2018, and the segment grew 8.5% annually between 2011 and 2018, cementing a durable use-case for high-barrier laminates. Sealed Air’s food division delivered 3% sales growth in Q4 2024, attributing out-performance to retail meat and specialty snack conversions into advanced pouch designs. Converter investments in EVOH-layered co-extrusions and metallized films now target both human and pet snack brands seeking shelf-life parity with cans while maintaining a premium look. The resulting migration lifts the average value per tonne and reinforces the South America flexible packaging market as a solution for high-margin categories.

Mandatory Recycled-Content Quotas in Brazil and Chile

Governments pursue circular-economy outcomes by obligating brand owners to incorporate PCR into packaging. Chile requires beverage containers to include 15% recycled material by 2025, with the percentage incrementally rising to 70% by 2060. Brazil’s reverse-logistics decree mandates shared responsibility across the value chain and has already attracted 3,475 public-consultation comments, signalling strong enforcement intent. Flexible converters with integrated wash, sort, and extrude lines gain preferential supplier status as multinational CPGs scramble to secure food-grade PCR. Smaller firms that lack access to consistent feedstock face margin squeeze or exit, accelerating consolidation across the South America flexible packaging industry.

Cold-Chain Expansion for Fresh Produce Exports

Colombia, Argentina, and Chile are expanding refrigerated logistics corridors to transport avocados, berries, and citrus to North American and European supermarkets. World Bank studies show that an inadequate cold chain can double export costs for perishables, prompting governments to co-finance containerization upgrades. Trade agency ProColombia highlights modified-atmosphere liners and anti-fog produce bags as cost-effective tools to extend shelf life during multi-day voyages. Flexible suppliers that engineer gas-transmission-rate-optimized films capture incremental tonnage as produce exporters standardize pack formats.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict single-use-plastic bans in Mexico City and Bogotá | −0.9% | Mexico and Colombia | Short term (≤ 2 years) |

| Shortage of domestic PCR resin supply | −0.7% | Brazil, Argentina | Medium term (2-4 years) |

| Currency volatility inflating polymer import costs | −0.6% | Argentina, Brazil | Short term (≤ 2 years) |

| Rising adoption of fiber-based flexibles in beverages | −0.4% | Brazil, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Single-Use-Plastic Bans in Mexico City and Bogotá

Urban ordinances restrict traditional take-out bags, straws, and cutlery, directly trimming high-volume single-serve flexible demand. Mexico City’s ban coincides with the city’s 300,000-tonne annual food-delivery plastic waste problem, of which under 10% is recycled. Bogotá’s enforcement escalates import permit scrutiny, with U.S. Department of Agriculture reports noting an increase in shipment detentions in early 2025. Food-service apps and quick-commerce players are trialing reusable or compostable systems, further curbing the flow of conventional plastics. Flexible suppliers must pivot toward compliant bio-based substrates or risk volume loss in densely populated capitals that set national policy precedents.

Shortage of Domestic PCR Resin Supply

Despite Brazil achieving a 55% PET collection rate, food-grade recycled pellets remain scarce because cheap virgin imports depressed recycled polymer prices by 28% in 2024.[2]Sustainable Plastics, “PET Recycling in Brazil,” sustainableplastics.comValgroup’s 4,000-tonne-per-month bottle-to-bottle plant covers only half the current brand-owner demand, forcing converters to import PCR at currency-linked premiums. Argentina’s inflation and trade controls add further friction, deterring investment in advanced sortation. Limited feedstock availability hampers producers' ability to meet mandated recycled-content thresholds, slowing certain high-volume conversions across the South America flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Maintain Scale While Paper Accelerates

Plastics contributed 87.16% of South America's flexible packaging market share in 2024, as PE, BOPP, and CPP lines operated near nameplate capacity to serve food and personal-care customers.[3]Sonoco Products Company, “2023 Annual Report,” sonoco.com The material suite benefits from Orbia’s USD 2.7 billion polymer revenue stream and a projected 3.6% increase in PVC demand from 2024 to 2030. The South America flexible packaging market size for plastics still expands, albeit at a moderating clip, as regulators target virgin content.

Paper alternatives post the segment’s fastest 4.78% CAGR because CPG owners seek kerbside-recyclable mono-material sachets and wraps. Sonoco’s EnviroFlex Paper roll-out across snacks and condiments validates technical feasibility and provides converters with a lower-barrier route to meet upcoming EPR fees. Aluminum foil remains a niche layer in pharmaceutical blister stock and high-barrier pouches, but cost and limited recycling channels restrain volume growth. Over the forecast period, plastics retain primary status, yet paper’s share uptick signals a broadened competitive palette that reshapes raw-material procurement strategies.

By Product Type: Pouches Capture Preference in Omni-Channel Retail

Pouches accounted for 38.67% of South America's flexible packaging market size in 2024 and are forecasted to have a 4.36% CAGR as stand-up formats accommodate both shelf merchandising and e-commerce dimensional-weight targets. Rigid-to-flexible conversions in dry pet food and powdered beverages support sustained order books.

Sachets and bags retain relevance in value-tier foods and agricultural inputs, although their growth trails that of pouches because governments scrutinize multi-layer laminations that lack recovery pathways. Shrink sleeves and labels gain traction in beverage multipacks, while fiber-based cartons begin to cannibalize certain use cases. Films and wraps serve as pallet protection and over-wrap roles, but volumes flatten where municipal bans curb the use of secondary plastic. Across all formats, automated filling and sealing investments converge on pouch lines, reinforcing their centrality to the South America flexible packaging market.

By End-User Industry: Food Dominates While Pharma Outpaces

Food retained a 55.29% revenue stake in 2024, riding on South America’s strong cattle, poultry, and fruit supply chains. Sealed Air’s food division captured 3% organic growth in Q4 2024 on the back of retail meat and cheese demand that depends on modified-atmosphere pouches. The South America flexible packaging industry also benefits from rising frozen produce exports enabled by expanded cold-storage networks.

Pharmaceutical and medical products are expected to mark the fastest growth rate of 4.52% CAGR as ANVISA enforces new e-labeling and device sterility rules. Drug-delivery sachets, IV-bag over-pouches, and test-kit laminates call for high-barrier, low-leachable films that few regional converters can supply at scale. Household and personal-care segments benefit from e-commerce subscription models, while beverage flexibility is tempered by fiber-based pouch pilots among multinational soft drink bottlers.

Geography Analysis

Brazil remains the epicenter of the South America flexible packaging market with a 35.54% share in 2024. Its reverse logistics decree engages manufacturers, importers, and consumers in collection networks, enabling 3,475 stakeholder comments that shaped the final legislation.[4]Ministério do Meio Ambiente, “Consulta Pública,” gov.brANVISA’s 2024-2025 agenda tightens device-sterility and e-labeling norms, positioning Brazil as the most stringent regulatory environment, which benefits converters with ISO 13485-certified cleanrooms. Pet food dynamics contribute to structural volume, as 139.3 million animals consume premium treats that require high-barrier pouches.

Argentina records the fastest 4.43% CAGR outlook. World Bank economists cite improving debt sustainability and trade openness as catalysts for packaging demand in meat and dairy exports. However, polymer imports face periodic surcharges and currency fluctuations that challenge the cash flows of converters. Investors nonetheless reassess project pipelines as inflation expectations cool under proposed fiscal frameworks.

Elsewhere, Chile is pioneering a 15% recycled-content mandate, beginning in 2025, which will ramp up to 70% by 2060, compelling brand owners to secure PCR supply or redesign products into fiber alternatives. Mexico’s mega metro single-use bans reshape food-delivery packaging, nudging platforms toward reusable container pilots. Colombia’s stricter import-permit rules complicate raw-material sourcing; however, avocado and mango exporters adopt advanced breathable films to sustain cold-chain integrity, thereby securing flexible demand despite administrative bottlenecks. The mosaic of policy and economic conditions keeps supply chains regionalized and spurs the development of adaptive product portfolios across the South America flexible packaging market.

Competitive Landscape

Strategic mergers sharpen scale advantages. Amcor’s USD 24 billion all-stock merger with Berry Global, announced in January 2025, is projected to yield USD 650 million in annual cost synergies and unite complementary healthcare, food-service, and South American operations. The deal catapults the combined company to unrivaled extrusion capacity, which is critical for meeting PCR mandates and ensuring multi-market compliance. Mondi earmarks EUR 1.2 billion (USD 1.39 billion) for corrugated and flexible packaging expansion, which includes kraft-paper lines attractive to CPGs pursuing mono-material claims.

Portfolio rationalization proceeds in parallel. Sonoco divested its USD 1.3 billion thermoformed and flexible packaging arm to TOPPAN for USD 1.8 billion in December 2024, redeploying the proceeds toward high-margin protective segments and acquiring Brazilian converter Inapel Embalagens to deepen its local reach. Sealed Air’s CTO2Grow program targets USD 140-160 million savings by 2025 through plant automation, supporting price-cost management in an inflationary resin environment.

Technology roadmaps emphasize circularity and automation. Integrated suppliers invest in chemical recycling trials, digital watermarks for pack sorting, and variable data printing for track-and-trace compliance under ANVISA. Smaller converters face capital constraints, accelerating a shift toward contract manufacturing or exit. Consequently, the South America flexible packaging market gravitates toward a mid-concentration profile in which the top five players still control a decisive share of installed capacity.

South America Flexible Packaging Industry Leaders

Amcor plc

Mondi plc

Sealed Air Corporation

Coveris Management GmbH

Grupo Oben Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Brazil, Argentina, and Chile are increasingly adopting post-consumer recycled (PCR) content and bioplastics, driven by tighter regulations on single-use plastics and a growing consumer environmental consciousness.

- January 2025: Amcor and Berry Global have announced an all-stock merger valued at USD 24 billion, aiming to form a global packaging leader with USD 650 million in potential synergies.

- December 2024: Sonoco closed the USD 1.8 billion sale of its Thermoformed and Flexibles Packaging business to TOPPAN Holdings.

- November 2024: Berry Global reported FY 2024 net sales of USD 12.3 billion, with the flexible-packaging unit posting 2% organic volume growth and resilience in South America.

South America Flexible Packaging Market Report Scope

By Material Type

| Plastics | Polyethylene (PE) |

| Biaxially-Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Polyvinyl Chloride (PVC) | |

| Ethylene-Vinyl Alcohol (EVOH) | |

| Paper | |

| Aluminum Foil |

By Product Type

| Pouches |

| Bags and Sachets |

| Films and Wraps |

| Shrink Sleeves and Labels |

| Other Formats |

By End-user Industry

| Food | Frozen Food |

| Dairy Products | |

| Fruits and Vegetables | |

| Meat, Poultry and Seafood | |

| Baked Goods and Snacks | |

| Confectionery | |

| Other Foods | |

| Beverage | |

| Pharmaceutical and Medical | |

| Household and Personal Care | |

| Industrial and Chemical |

By Country

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Material Type | Plastics | Polyethylene (PE) |

| Biaxially-Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Ethylene-Vinyl Alcohol (EVOH) | ||

| Paper | ||

| Aluminum Foil | ||

| By Product Type | Pouches | |

| Bags and Sachets | ||

| Films and Wraps | ||

| Shrink Sleeves and Labels | ||

| Other Formats | ||

| By End-user Industry | Food | Frozen Food |

| Dairy Products | ||

| Fruits and Vegetables | ||

| Meat, Poultry and Seafood | ||

| Baked Goods and Snacks | ||

| Confectionery | ||

| Other Foods | ||

| Beverage | ||

| Pharmaceutical and Medical | ||

| Household and Personal Care | ||

| Industrial and Chemical | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected volume for flexible packaging in South America by 2030

It is expected to reach 2.73 million tonnes, growing at a 3.94% CAGR from 2025.

Which product format is expanding the quickest in the region?

Stand-up pouches lead with a 4.36% CAGR because they balance shelf appeal and e-commerce handling performance.

How are recycled-content mandates shaping supplier strategy?

Brazil and Chile require rising PCR levels, so converters invest in in-house recycling and secure long-term PCR contracts to stay compliant.

Why is Argentina considered a growth hot-spot?

Economic reforms and export-oriented food sectors fuel a 4.43% CAGR despite currency volatility.

Which end-user segment offers the highest incremental growth?

Pharmaceuticals and medical devices expand at 4.52% CAGR, driven by stricter ANVISA sterilization and e-labeling standards.

How will the Amcor–Berry merger influence regional dynamics?

The combined entity’s scale and PCR capabilities will pressure smaller players on price and compliance, accelerating market consolidation.

Page last updated on: