Iron Oxide Pigments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

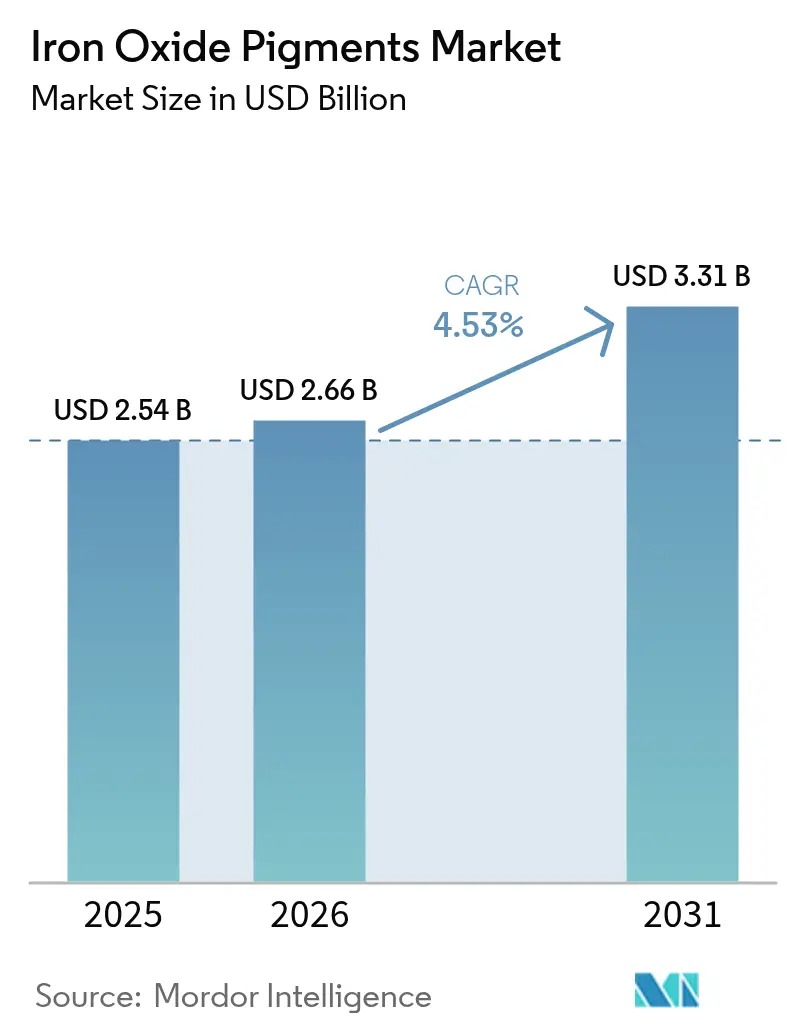

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 3.31 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iron Oxide Pigments Market Analysis by Mordor Intelligence

The Iron Oxide Pigments Market size was valued at USD 2.54 billion in 2025 and estimated to grow from USD 2.66 billion in 2026 to reach USD 3.31 billion by 2031, at a CAGR of 4.53% during the forecast period (2026-2031). Stable growth reflects reliable demand in construction, paints, plastics and regulated consumer products. Infrastructure stimulus in emerging economies, stricter global limits on toxic colorants and steady price relief in iron-ore feedstock jointly support expansion. Producers that can guarantee non-toxic, lead-free grades and carbon-efficient operations are capturing premium contracts, while vertical integration shelters margins from raw-material swings. Ongoing capacity consolidation is likely to accelerate technology upgrades and quality harmonization across the supply base.

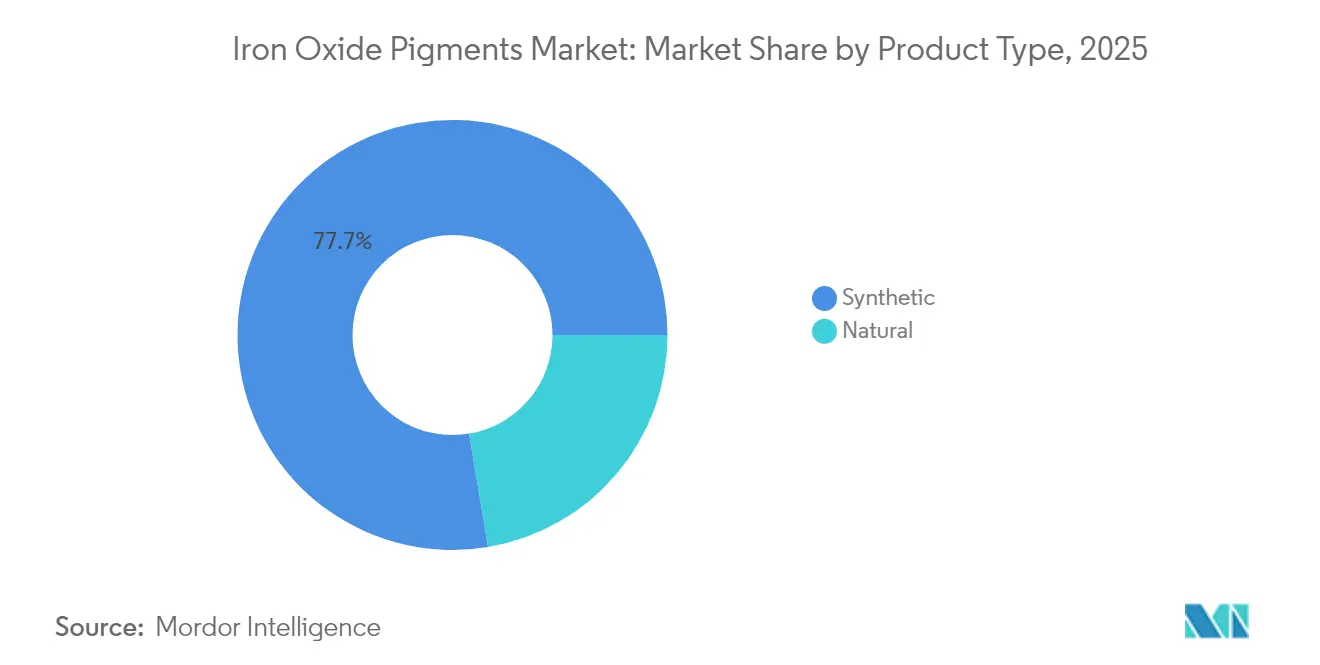

- By product type, synthetic grades commanded 77.65% of iron oxide pigments market share in 2025, while natural grades are projected to grow at 3.18% CAGR through 2031.

- By color, red pigments led with 43.82% revenue share in 2025; the yellow segment is forecast to expand at 4.98% CAGR to 2031.

- By form, powder accounted for 42.15% of the iron oxide pigments market size in 2025; liquid dispersions are advancing at 4.95% CAGR through 2031.

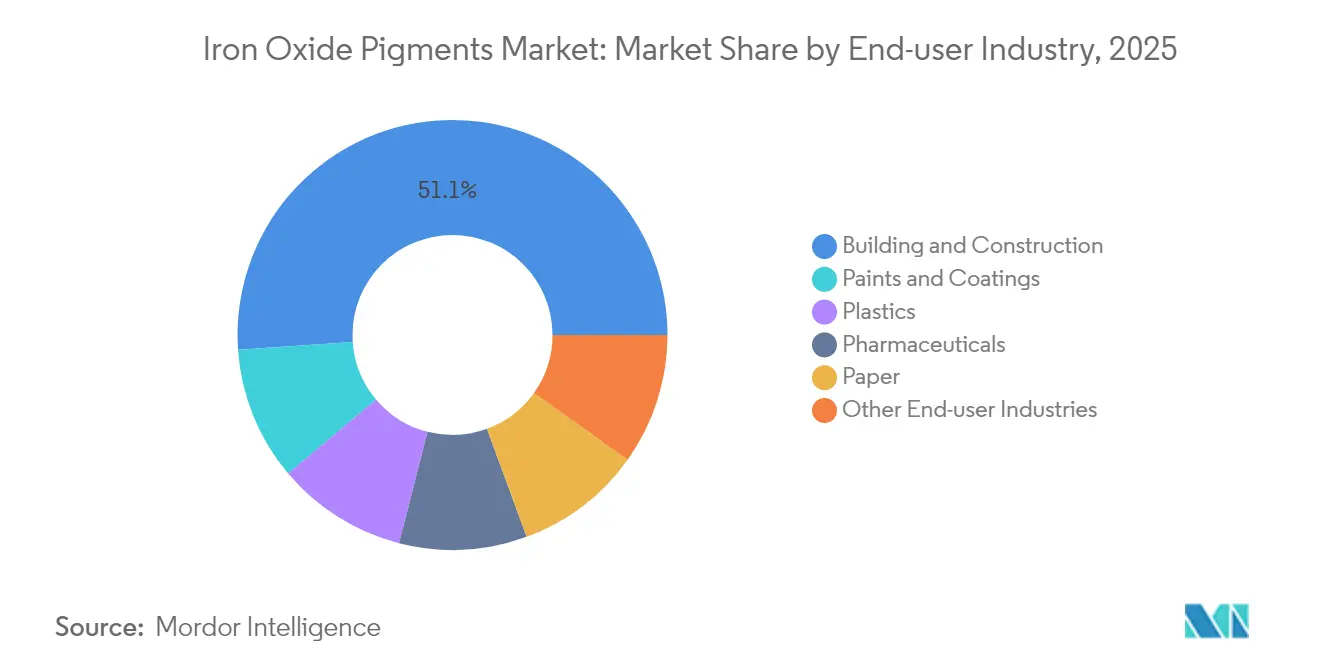

- By end-user industry, building and construction held 51.10% revenue share in 2025; paints and coatings record the highest projected CAGR at 5.05% through 2031.

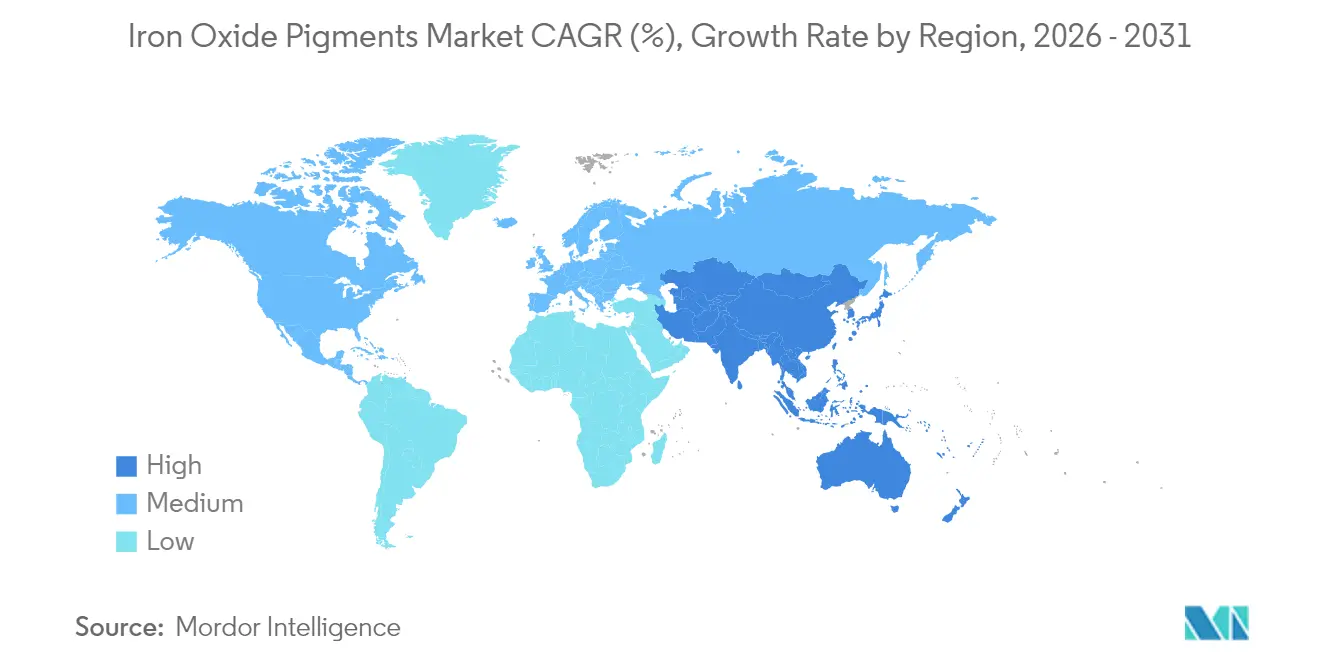

- By geography, Asia-Pacific dominated with 44.55% share in 2025 and is growing at 5.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Iron Oxide Pigments Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from building & construction | +1.2% | Global, focus on APAC | Medium term (2-4 years) |

| Expanding paints & coatings production capacity in APAC | +0.8% | APAC, spill-over to MEA | Short term (≤ 2 years) |

| Infrastructure stimulus in emerging economies | +0.7% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Regulatory shift toward lead-free colorants | +0.6% | North America & EU first | Medium term (2-4 years) |

| 3-D printing filament coloration needs | +0.2% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Building & Construction

Urbanization and government-funded infrastructure upgrades in Asia, Latin America and Africa increase concrete coloration needs. Synthetic grades prevail because precise particle size control promotes uniform tone and weather resistance in precast blocks, pavers and roofing tiles. India’s national highway program and China’s retrofit of aging residential stock are prominent pull factors. Many municipalities now require high-albedo surfaces that reduce heat-island effects, lifting use of iron oxide blends with near-infrared reflectance credentials[1]U.S. Department of Energy, “Cool Roofs,” energy.gov. Seasonal swings in site work create order volatility, so producers maintain modular kilns and flexible mixing stations that can ramp output efficiently.

Expanding Paints & Coatings Production Capacity in APAC

Southeast Asia posts double-digit gains in decorative paints volumes, and multinationals have shifted tinting-paste lines nearer to end-markets. Local sourcing of ready-to-use dispersions shortens lead times and reduces freight costs, advancing the iron oxide pigments market in Indonesia, Vietnam and Thailand. Water-borne coatings now exceed 60% of architectural sales in major Chinese cities, requiring finely milled pigment slurries with low-glycol carriers. LANXESS publishes Environmental Product Declarations for its Bayferrox series to satisfy eco-label audits and provincial green-building codes. Producers that certify VOC-free dispersions win tender preference from state-owned developers.

Infrastructure Stimulus in Emerging Economies

Budget allocations for rail, port and social-housing projects in Brazil, Nigeria and the Philippines raise baseline demand over multiyear horizons. Procurement rules often stipulate regional value addition, encouraging pigment milling in-country and lowering reliance on imports. Government bidders also request durability in monsoon, desert or marine climates, favoring high-purity grades with proven UV stability. Public-work planners increasingly embed CO₂ footprint thresholds in bid documents, so suppliers that document renewable-energy inputs gain an advantage.

Regulatory Shift Toward Lead-Free, Non-Toxic Colorants

The United States limits total lead in food uses to 5 mg/kg and pharmaceuticals to 10 mg/kg, compelling reformulation of capsules and confectionery coatings[2]U.S. Food and Drug Administration, “Guidance for Industry: Lead in Food, Foodwares, and Dietary Supplements,” fda.gov. Similar rules spread across the European Union, Canada and Australia, reinforcing adoption of synthetic iron oxides approved for human contact. Cosmetics brands specify hypoallergenic, trace-metal-free pigments in eye shadow and sunscreen lines to meet clean-beauty marketing claims. Medical-device coatings also convert to iron-oxide blends because they withstand gamma sterilization without color shift.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of iron ore & hydrochloric acid | −0.9% | Regions dependent on imports | Short term (≤ 2 years) |

| Tightening VOC / hazardous-waste regulations | −0.6% | North America & EU | Medium term (2-4 years) |

| Rise of nano-ceramic & hybrid high-chroma pigments | −0.4% | High-performance niches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Iron Ore & Hydrochloric Acid

Spot iron-ore dropped from USD 88–144 per ton in 2024 to USD 75–120 in 2025 yet price curves remain jagged due to logistical snags and project ramp-ups. Hydrochloric-acid producer price index reached 131.457 in March 2025, marking sustained input inflation. Producers without captive mining or acid recovery units face squeezed spreads. Long-term supply contracts or in-house regeneration plants buffer spikes but demand capital outlays. Regional concentration of ore in Australia and Brazil exposes Asian processors to freight disruptions during cyclone seasons.

Tightening VOC / Hazardous-Waste Regulations

Revised US EPA aerosol-coating rules push compliance to January 2027 and require lower solvent thresholds. European directives expand the list of substances of very high concern, adding administrative load for dossier updates. Factories built before 2000 often need scrubber retrofits and upgraded effluent-neutralization units to stay licensed. Waste disposal fees rise when iron-oxide sludge classifies as hazardous under local statutes, particularly in densely populated EU industrial clusters. These costs weigh heavier on small operators, prompting closures or acquisition by larger groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetic Dominance Reinforces Quality Standards

Synthetic grades held 77.65% of iron oxide pigments market share in 2025 as customers prioritize batch consistency for regulated uses. The iron oxide pigments market size attributed to synthetic output reached USD 1.97 billion in 2025 and is tracking a 4.78% CAGR to 2031. Precipitation and Laux routes allow narrow particle-size windows, giving uniform tint strength in coil-coating and plastic masterbatch. Pharmaceutical buyers specify low-arsenic and low-mercury grades, achievable only in controlled synthetic reactors. Vertical integration into sulfuric-acid recycling and calcining umbrellas energy costs and slashes Scope 1 emissions, pleasing ESG auditors.

Natural pigments draw value seekers in ceramics, art supplies and landscaping mulch. Annual global production clusters in India, Germany and Spain at 385,000 metric tons. Quality variation and trace-metal risk reduce applicability in food or personal-care items. Some governments offer tax credits for artisanal mining, but stringent EN71 toy-safety limits narrow adoption. Blending natural with synthetic inputs helps processors hit target chroma while optimizing cost, yet synthetic still captures the incremental volumes as exporters upgrade specifications.

By Color: Red Leadership Challenged by Yellow Growth

Red iron oxides occupied 43.82% revenue in 2025, underpinned by façade bricks, asphalt shingles and anti-corrosion primers. Formulators value the hematite-rich shade’s high hiding power and chemical inertness in alkaline cement. In contrast, yellow iron oxides deliver 4.98% CAGR thanks to vivid architectural coatings and plastic housings in consumer electronics. Technological advances yield goethite crystal morphologies that resist photobleaching in tropical climates, widening geographical reach.

Black iron oxides serve both coloration and functional roles. Magnetite-derived Fe₃O₄ enables electrostatic toner, magnetic recording media and electromagnetic-shielding films. Research into Fe₂O₃@TiO₂ core-shell structures shows near-infrared reflectance above 0.7, opening cool-roof applications. Brown, orange and blended earth tones satisfy ceramic glazes and cultured-stone panels. Color innovation remains vital as architects pursue customized palettes for brand differentiation.

By Form: Powder Dominance Faces Liquid Dispersion Challenge

Powder shipments totaled 42.15% of the iron oxide pigments market size in 2025, favored for ease of storage, long shelf life and compatibility with traditional high-speed mixers. Granular variants reduce dusting and improve free-flow in automated dosing but add processing steps. Liquid dispersions, although smaller, are climbing at 4.95% CAGR. Ready-to-use slurries cut milling time, lower respirable dust exposure by 90% and yield tighter batch-to-batch ΔE variations.

Aqueous dispersions dominate water-borne paints, while non-aqueous carriers target solvent-borne maintenance coatings. Producers refine rheology modifiers to keep viscosities below 1,000 cP over freeze-thaw cycles. Investment in inline high-pressure homogenizers accelerates throughput and energy savings. Dispersions integrate biocide systems meeting EU BPR rules, giving extended pot life without compromising worker safety. Powder suppliers respond with surface-treated micro-granulates that disperse in under 30 seconds, narrowing the convenience gap.

By End-user Industry: Construction Leadership Meets Coatings Growth

Building and construction retained 51.10% revenue in 2025, anchored by colored concrete, pavers and roofing granules. Infrastructure stimulus in Asia and MENA keeps baseline volume high. Yet the paints and coatings segment’s 5.05% CAGR through 2031 makes it the prime growth engine. Protective coil coatings for solar frames, wind towers and offshore platforms demand micronized iron oxides with tight particle-size cuts to assure gloss and corrosion resistance at thin film builds.

Plastics uptake benefits from the pigment’s thermal stability above 300 °C, suitable for polyolefin pipes and ABS housings. FDA conformity broadens usage in food-contact crates. Paper mills apply low-shade yellow iron oxides in décor laminates. Pharmaceuticals, despite small tonnage, deliver margins quadruple those in concrete colorants due to GMP documentation. This multi-industry spread cushions cyclical risk for suppliers and sustains investment in application labs.

Geography Analysis

Asia-Pacific controlled 44.55% of global revenue in 2025, driven by concentrated production hubs in eastern China and downstream demand growth in India and Southeast Asia. Stricter Chinese emissions codes forced small kilns offline, shifting share to compliant multinationals and large domestic groups with regenerative thermal oxidizers. India’s smart-city program finances mass-transit corridors and eco-housing that specify integral colored concrete, lifting bulk orders for red and yellow powders.

North America follows with technology-focused demand. Cool-roof mandates in California and energy-saving tax incentives nationwide stimulate consumption of near-infrared reflecting grades. Auto OEM coatings plants in the United States require high-purity black iron oxides for metallic styling colours. Regional suppliers differentiate through zero-waste acid recovery and renewable electricity procurement.

Europe accounts for a mature but innovation-rich customer base. REACH and CLP regulations drive early adoption of PFAS-free processing aids, compelling pigment vendors to re-engineer coatings compatibilizers. Germany leads high-chroma automotive finishes, while Spain pushes architectural color cards linked to heritage building codes. Circular-economy legislation promotes pigment recovery from demolition waste, an emerging specialty niche.

Latin America shows incremental opportunities tied to Brazilian port upgrades and Mexican appliance production. Currency volatility and import duties spur local finishing plants to seek on-shore milling partners. Middle East & Africa markets hinge on megaprojects such as Saudi Arabia’s NEOM and Nigeria’s rail network. Hot desert climates favor cool-roof and anti-chalk formulations, creating openings for technical collaboration.

Competitive Landscape

The iron oxide pigments market features a moderately consolidated profile in which the top five suppliers hold roughly 60% of global volume. DIC Corporation remains the scale leader, but October 2024 saw Sudarshan Chemical Industries acquire Heubach Group for EUR 127.5 million, vaulting the combined firm into the second position and expanding its European footprint. The deal adds Laux-process capacity and a diversified color portfolio, positioning the new entity to bid for global master-batch and construction accounts.

Innovation differentiates mid-tier contestants. LANXESS won the 2024 ICIS Award for a lithium-iron-phosphate battery pigment produced with waste-heat recovery, reducing CO₂ per ton by 25%. BASF’s “Sustainability Future Target Picture” road map outlines energy-optimized calcination kilns and carbon-border-adjustment readiness. Producers publish cradle-to-gate emissions data to gain preferred-supplier status under automotive OEM scorecards.

Regional specialists also reshape the landscape. Cathay Industries completed integration of Venator’s color business and rebranded as OXERRA in April 2023. The company pushes distributed manufacturing, placing small reactors near key construction zones to cut freight and lead time. Several Chinese operators upgrade hydrochloric-acid regeneration units to comply with national discharge norms, shifting exports from low-margin commodity powders toward value-added dispersions.

Iron Oxide Pigments Industry Leaders

Lanxess

BASF

Oxerra

Venator Materials PLC

Clariant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Sudarshan Chemical Industries closed its EUR 127.5 million acquisition of Heubach Group’s global pigment business, creating the world’s second-largest pigment supplier.

- April 2023: Cathay Industries completed the purchase of Venator’s color portfolio and rebranded the combined enterprise as OXERRA.

Global Iron Oxide Pigments Market Report Scope

Iron oxide pigments are made from iron and oxides. They can come from both natural and man-made sources. Naturally, these are made from umber, goethite, sienna, hematite, ochre, and magnetite. Similar to how they are produced naturally, they are produced synthetically through key procedures such as the thermal deposition of iron compounds, the precipitation of iron salts, and the reduction of organic compounds by iron.

The iron oxide pigments market is segmented by product type, color, end-user industry, and geography. By product type, the market is segmented into natural and synthetic. By color type, the market is segmented into red, yellow, black, and other colors. By end-user industry, the market is segmented into building and construction, paints and coatings, plastics, paper, pharmaceuticals, and other end-user industries. The report also covers the market size and forecasts for the iron oxide pigments market in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD).

| Natural |

| Synthetic |

| Red |

| Yellow |

| Black |

| Others |

| Powder |

| Granules |

| Liquid Dispersion |

| Building and Construction |

| Paints and Coatings |

| Plastics |

| Paper |

| Pharmaceuticals |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Natural | |

| Synthetic | ||

| By Color | Red | |

| Yellow | ||

| Black | ||

| Others | ||

| By Form | Powder | |

| Granules | ||

| Liquid Dispersion | ||

| By End-user Industry | Building and Construction | |

| Paints and Coatings | ||

| Plastics | ||

| Paper | ||

| Pharmaceuticals | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the iron oxide pigments market?

The iron oxide pigments market size is USD 2.66 billion in 2026 and is forecast to reach USD 3.31 billion by 2031.

Which region leads global demand?

Asia-Pacific holds 44.55% of global revenue and is also the fastest-growing region with a 5.18% CAGR through 2031.

Why are synthetic iron oxides preferred over natural grades?

Synthetic grades offer tighter particle-size control, higher purity and consistent color strength, which are essential for regulated applications like pharmaceuticals and architectural coatings.

How are environmental regulations influencing product development?

Stricter lead limits and VOC caps accelerate the shift to non-toxic, low-solvent formulations, pushing producers to publish Environmental Product Declarations and adopt closed-loop acid recovery.

Which end-use sector shows the strongest growth?

Paints and coatings record the highest projected CAGR at 5.05% as demand rises for durable architectural and industrial finishes.

Page last updated on: