Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

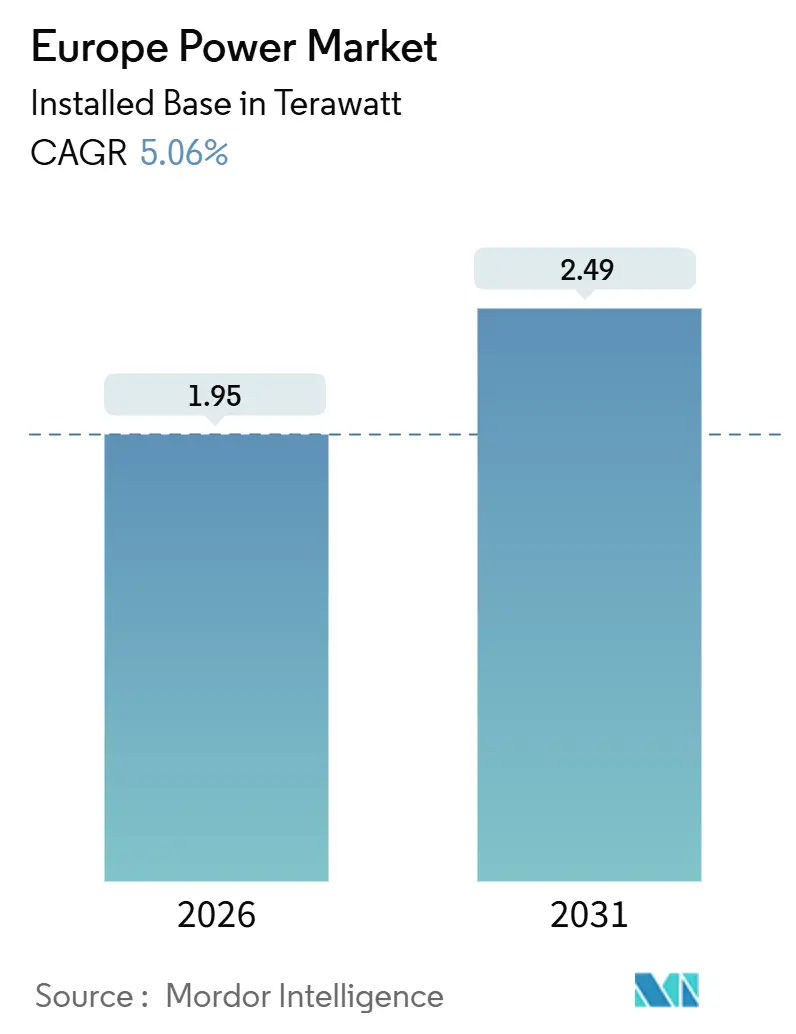

| Market Volume (2026) | 1.95 Terawatt |

| Market Volume (2031) | 2.49 Terawatt |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Power Market Analysis by Mordor Intelligence

The Europe Power Market size in terms of installed base is expected to grow from 1.95 Terawatt in 2026 to 2.49 Terawatt by 2031, at a CAGR of 5.06% during the forecast period (2026-2031).

Strong policy momentum under Fit-for-55 and REPowerEU is pushing utilities to replace retiring coal and nuclear plants with low-cost wind and solar, whose levelized costs dropped to EUR 35 per MWh and EUR 40 per MWh respectively in 2024. Offshore wind pipelines, hydrogen-ready gas retrofits, and AI-enabled grid upgrades are converging to neutralize intermittency concerns, while corporate power-purchase agreements (PPAs) give developers an additional funding channel that now rivals traditional utility procurement. Grid-edge technologies, including virtual power plants and residential batteries, are expanding the addressable flexibility pool and tempering wholesale price volatility. At a regional level, Germany remains the capacity heavyweight, yet Denmark’s acceleration toward 100% renewable electricity is reshaping the competitive balance.

Key Report Takeaways

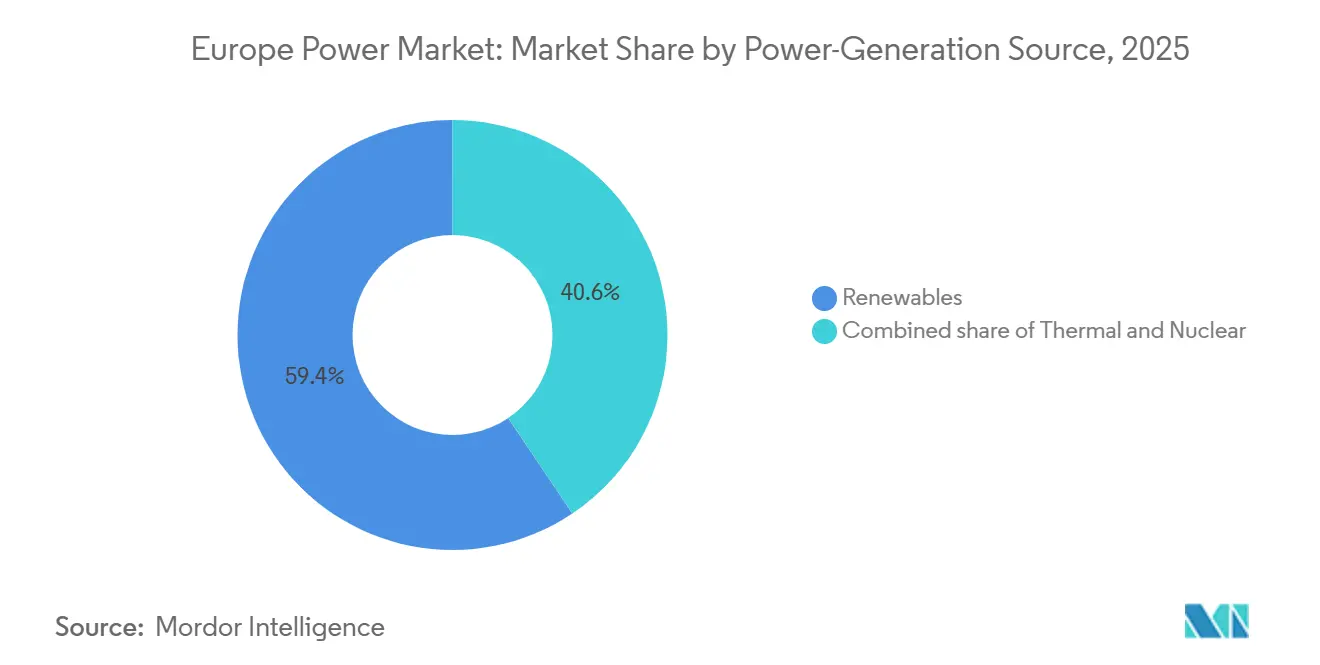

- By power-generation source, renewables captured 59.40% of Europe's power market share in 2025; offshore wind capacity is projected to advance at an 8.51% CAGR to 2031.

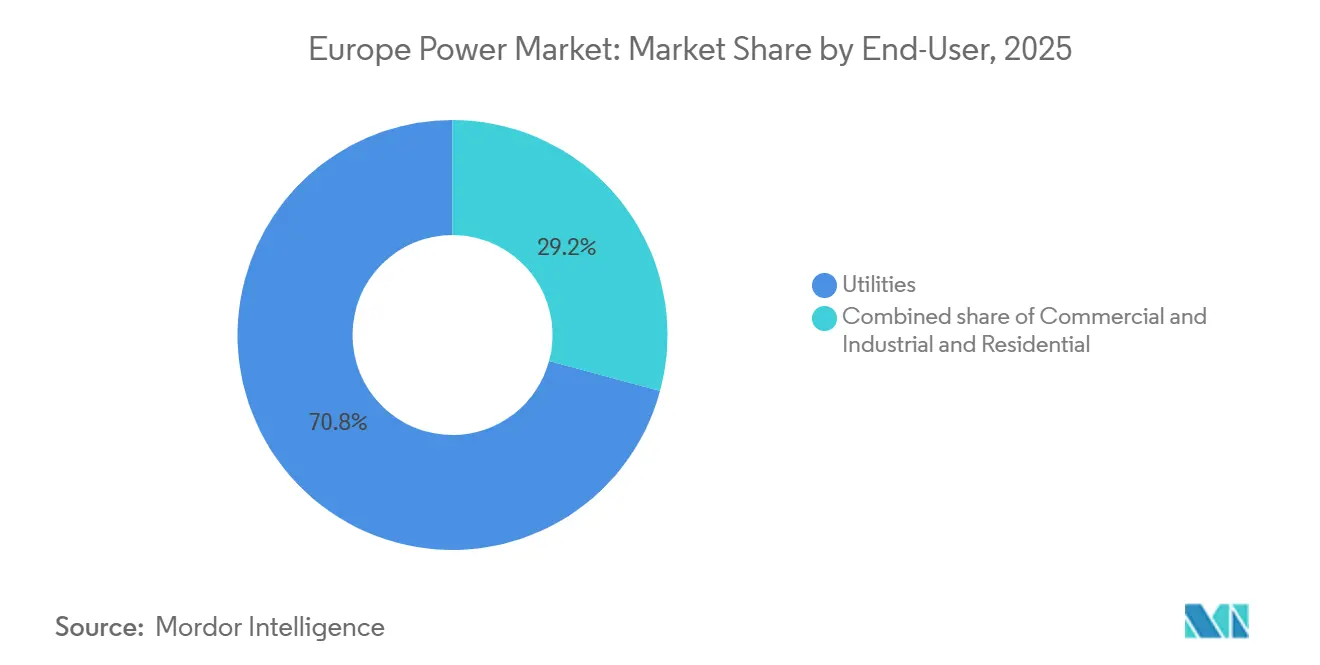

- By end-user, utilities commanded 70.8% of the European power market size in 2025, while the residential segment is expanding at a 10.4% CAGR through 2031.

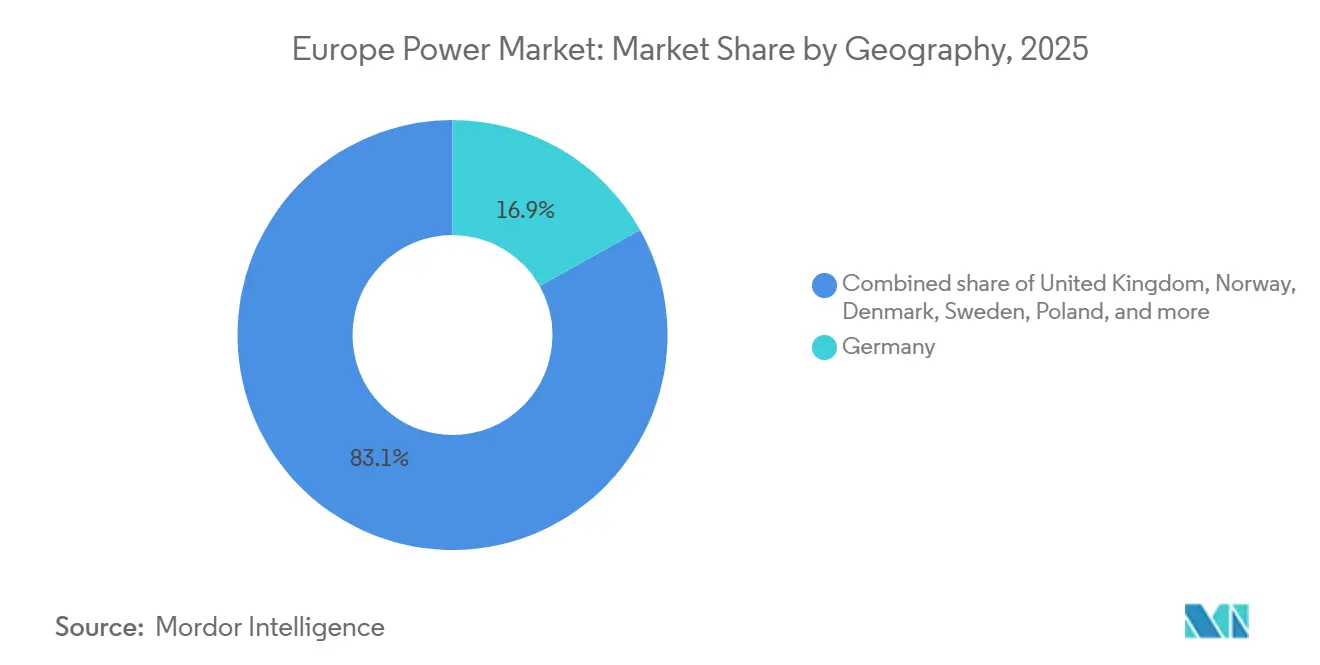

- By geography, Germany held 16.87% of the European power market in 2025; Denmark records the fastest forecast pace with a 9.5% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Fit-for-55 & REPowerEU decarbonization mandates | +1.2% | EU-wide, strongest in Germany, Denmark, Spain | Long term (≥ 4 years) |

| Record-low LCOE of onshore wind & utility-scale solar | +1.0% | Global, with highest impact in Spain, Germany, Nordics | Medium term (2-4 years) |

| Accelerated coal & nuclear phase-outs post-2025 | +0.8% | Germany, France, Poland, Belgium | Medium term (2-4 years) |

| Digitalisation of grids (AI-enabled predictive O&M) | +0.5% | UK, Germany, France, Netherlands | Short term (≤ 2 years) |

| Data-centre electricity demand surge (>20 TWh by 2030) | +0.7% | Ireland, Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| Hydrogen-ready CCGT retrofits unlocking flexible backup | +0.4% | Germany, Netherlands, UK, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Fit-for-55 & REPowerEU Decarbonization Mandates

Mandated renewable shares of 42.5% by 2030 and net-zero by 2050 have anchored long-term revenue visibility for developers, pushing annual solar additions in Germany to 15 GW and onshore wind to 10 GW, triple the 2020-2023 run-rate.[1]European Commission, “Renewable Energy Directive III,” ec.europa.eu Streamlined permitting that caps approvals at 12 months in priority zones is easing deployment backlogs that once stretched five years, while EUR 300 billion of REPowerEU funds redirects recovery spending toward grid reinforcement and battery co-location. Utility investment portfolios are shifting in tandem, allocating more than 50% of 2026 budgets to renewables and digital networks. Grid codes now reward fast-acting battery storage, spurring 10 GWh of additions in 2024. The taxonomy framework is equally influential because “do-no-significant-harm” rules favor projects with recycling or circular-economy plans, leading turbine makers to announce blade-recycling lines in France and Spain.

Record-Low LCOE of Onshore Wind & Utility-Scale Solar

Onshore wind at EUR 35 per MWh and utility solar at EUR 40 per MWh undercut 2024 coal and gas benchmarks by more than 50%, turning renewables into the default capacity choice. Efficiency gains are material: 6 MW onshore turbines yield 30% more output than 2020 machines, and bifacial panels raise solar yields by up to 15%.[2]IRENA, “Future of Solar Photovoltaic,” irena.org Spain’s 2024 tender cleared at EUR 28 per MWh, while the United Kingdom’s latest Contracts-for-Difference round delivered offshore wind at GBP 44 per MWh (USD 56). LCOE deflation has a price-paradox, though; high solar penetration in Denmark triggered midday negative wholesale prices on 42 days in 2024, accelerating power-to-X electrolyzer uptake that reached 2 GW that year. Project economics now embed ancillary-service revenue, adding new valuation levers for investors.

Accelerated Coal & Nuclear Phase-Outs Post-2025

Germany’s April 2023 nuclear exit and planned 2030 coal retirement strip 19 GW of baseload, requiring a doubling of annual renewable installations and grid-scale storage. France is rebalancing after fleet corrosion cut nuclear availability to 54% in 2022, while Poland committed to removing 5 GW of coal by 2030 under EU pressure. Life-extension decisions remain contentious: Belgium extended Doel 3 and Tihange 2 for ten years to safeguard winter adequacy. Flexible hydrogen-ready combined-cycle gas turbines (CCGTs) are bridging the gap, capturing capacity payments and ensuring inertia, with RWE planning 3 GW of retrofits through 2028. Net cross-border electricity imports into Germany rose to 15 TWh in 2024, signaling wider reliance on interconnectors during tight periods.

Digitalisation of Grids (AI-Enabled Predictive O&M)

Machine-learning platforms reduced unplanned outages by 20%-30% when National Grid rolled out predictive analytics across 7,000 transmission substations in 2024. Digital twins from Siemens are now in service with 15 transmission operators, allowing stress-testing of high-renewable dispatch scenarios and minimizing curtailment. Artificial-intelligence controls also unlock distributed flexibility; Germany aggregated 2 GW of residential batteries and EV chargers into frequency-response markets in 2024. Cyber-security oversight tightened through the NIS2 Directive, which imposes 24-hour incident reporting and EUR 10 million fines, pushing smaller utilities to adopt edge-computing designs that degrade gracefully under attack. Taken together, digitalisation is compressing operations and maintenance outlays by 15%-20%, freeing capital for new build.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Congested cross-border interconnector capacity | -0.6% | Germany-France, Iberia-France, Nordics-Continental Europe | Medium term (2-4 years) |

| Lengthy grid permitting & NIMBY opposition | -0.5% | Germany, UK, France, Spain | Long term (≥ 4 years) |

| Volatile wholesale prices eroding utility margins | -0.4% | EU-wide, most acute in Germany, Spain, Denmark | Short term (≤ 2 years) |

| Critical-mineral supply-chain exposure for renewables | -0.3% | Global, with highest impact on solar and battery projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Grid Permitting & NIMBY Opposition

Grid build-times average 7-10 years, with local challenges adding two to three years, evident in Germany’s 700 km SuedLink that will be 13 years old by first power in 2028. France’s TSO reports that 40% of projects face lawsuits, especially near coastal landing points for offshore wind connections. In the United Kingdom, a connection queue of 739 GW stretches out to 15 years for some projects, prompting new “first ready, first connected” rules. Spain cut approval windows to 18 months in designated zones, yet implementation lags in Catalonia and Andalusia, keeping uncertainty high. The delays stranded 12 GW of German wind and solar proposals between 2022 and 2024, equal to EUR 15 billion of stalled capital.

Congested Cross-Border Interconnector Capacity

Fourteen corridors highlighted by ACER’s 2025 monitoring report operate near saturation, suppressing efficient dispatch and inflating redispatch costs that hit EUR 4.2 billion in Germany during 2024.[3]Agency for the Cooperation of Energy Regulators, “Electricity Wholesale Market Monitoring Report 2025,” acer.europa.eu The France-Spain interconnector’s 2.8 GW ceiling prevents 15 GW of surplus Iberian solar from relieving French mid-day demand spikes. Nordic-to-Continental cables also choke during winter, curtailing Norwegian hydro exports and forcing the Baltic states toward pricier gas imports. The 1.4 GW Viking Link, finally commissioned in 2023 after an eight-year gestation, underscores the slow approval pipeline. Developers facing frequent negative pricing are curtailing output, trimming capacity factors by up to 8% in Spain and Denmark.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power-Generation Source: Renewables Dominate Capacity Additions

Renewables contributed 59.40% of the European power market in 2025, and their installed base is advancing at an 8.51% CAGR through 2031.[4]WindEurope, “Offshore Wind in Europe: Key Trends and Statistics 2024,” windeurope.org Offshore wind is taking the lead, with 5 GW installed in 2024 and a 25 GW construction queue led by Denmark’s 3.5 GW Hornsea Three and several North Sea clusters. Onshore wind added 12 GW in 2024, mainly in Spain, Germany, and Sweden, while utility solar added 18 GW, reflecting Spain’s record 6 GW contribution. Hydro remains steady at roughly 200 GW, though Austria’s 1 GW pumped-storage commissioning in 2024 highlighted renewed interest in long-duration storage. Biomass, waste-to-energy, geothermal, and tidal together stay below 5% of capacity but meet niche circular-economy and island-mode needs. The influx of low-variable-cost renewables is altering dispatch order, pushing thermal plants into peaker roles with 30%-40% capacity factors versus 60% in 2015.

Conventional generation still anchors system stability. Natural-gas turbines provide about 200 GW of flexible backup, and hydrogen-ready models are emerging to cut residual carbon. Nuclear remains prominent in France and the United Kingdom at 120 GW region-wide, despite Germany’s exit. Retiring coal blocks free emissions headroom but leave adequacy gaps until sufficient storage comes online. The Europe power market size for flexible backup technologies is therefore gaining investor attention, with pumped-storage, battery farms, and hydrogen-ready gas expected to command more than 15% of new-build spending by 2031.

By End-User: Residential Electrification Outpaces Utility Growth

Utilities still represented 70.8% of Europe's power market size in 2025. Their central role covers large-scale generation, transmission, and cross-border trade. Yet residential electrification is scaling quicker than any other end-user category at 10.4% CAGR, powered by more than 3.5 million heat pumps installed by 2023 and 8 GW of rooftop solar that came online in 2024. Residential EV charging is multiplying after 500,000 public chargers were added in 2024, and behind-the-meter batteries smooth evening peaks. These assets now participate in ancillary markets via aggregators, expanding income streams while deferring distribution upgrades.

Commercial and industrial customers are hedging volatility through long-term PPAs worth 12.7 GW in 2023, with tech multinationals dominating contract volumes. Factory-site solar and battery systems improve uptime in energy-intensive sectors, and the green-steel pivot is evident in Thyssenkrupp's on-site electrolyzer that trims emissions by 30%. Utilities are seeking stable earnings by overweighting regulated networks; Iberdrola reallocated 60% of 2024-2026 capex toward grids, up from 40% four years earlier. Consequently, European power industry players are realigning business models around data, digital services, and flexibility instead of pure commodity sales.

Geography Analysis

Germany, France, Spain, and the Nordics together contributed more than 50% of aggregate capacity in 2025, underlining the geographic concentration of dispatchable and variable generation assets. Germany’s grid congestion costs climbed to EUR 4.2 billion in 2024, a stark rise from EUR 1.5 billion in 2020, emphasizing the monetary strain of balancing a north-south renewables mismatch. Denmark, despite representing less than 2% of the European power market size, delivers outsize technology leadership in offshore wind design and hybrid interconnectors. France’s fleet modernization plan will extend 32 reactors by another decade, preserving 50 GW of nuclear baseload through 2040. Spain retains the lowest solar LCOEs in Europe, catalyzing corporate PPA demand and positioning the country as a merchant-solar exporter once interconnector limits ease.

In Northern Europe, Norway’s 33 GW of hydro and Sweden’s 16 GW offer the continent a strategic battery that fills supply gaps during wind lulls. The United Kingdom is marching toward 50 GW of offshore wind by 2030, and Crown Estate seabed auctions in 2024 released 8 GW of new zones. Ireland faces grid constraints as data-center demand already accounts for 31% of national load, prompting connection moratoria near Dublin. Poland’s transition dilemma underscores a broader Eastern European challenge: legacy coal fleets face rising EU Emissions Trading Scheme costs, yet financing for renewables and storage has lagged.

The rest of Europe, including Italy, the Netherlands, Belgium, Austria, and the Balkans, makes up roughly 35% of installed capacity. Italy leads in distributed solar at 25 GW, the Netherlands excels in North Sea wind at 3 GW, and Austria added the continent’s largest pumped-storage plant in 2024. Interconnection investments are beginning to stitch these disparate resources together, yet ACER warns that EUR 150 billion in new lines is still required by 2030 to unlock full regional synergies.

Competitive Landscape

The European power market exhibits moderate concentration: the top five utilities, EDF, Enel, Iberdrola, RWE, and Engie, control roughly 35% of installed capacity, leaving considerable headroom for regional specialists and technology disruptors. EDF channels EUR 50 billion into nuclear life extensions while simultaneously exploring hydrogen production on brownfield sites, whereas Enel and Iberdrola divest legacy fossil plants to finance solar-plus-storage portfolios. Ørsted expanded offshore wind holdings to 9 GW after Gode Wind 3’s 1.5 GW commissioning in January 2026, underscoring the growth of pure-play renewable developers. Transmission and system operators, TenneT, Terna, National Grid, and Red Eléctrica, compete for interconnector mandates that now garner regulatory priority, illustrated by TenneT’s EUR 20 billion financing for SuedLink.

Battery storage and virtual power plants present fertile white space. Fluence deployed 2 GWh of grid-scale batteries in 2024, and Next Kraftwerke aggregated 10 GW of distributed assets into real-time balancing markets. AI ranks as a strategic differentiator: utilities with predictive maintenance suites cut unscheduled downtime and narrow customer-churn risks, while laggards incur higher opex. M&A activity remains brisk; RWE’s USD 3.2 billion Northland Power acquisition raised its offshore wind pipeline to 10 GW, and Engie exited all coal generation in 2025 to pivot fully toward hydrogen and flexible gas. Retail disruption by Octopus Energy’s Kraken platform, which onboarded 5 million customers by 2024, exemplifies the competitive pressure now spilling over into customer-facing services.

Policy presents both challenges and opportunities. The EU Electricity Market Design reform formalizes capacity remuneration mechanisms that reward flexibility over traditional baseload, reshaping revenue models. Separate unbundling rules compel transmission owners to grant non-discriminatory access, further leveling the playing field for new entrants. As digital tools proliferate, market boundaries between generation, storage, and demand response blur, catalyzing partnerships that combine data analytics with hardware expertise.

Europe Power Industry Leaders

Electricité de France S.A. (E.D.F.)

Enel S.p.A.

Iberdrola SA

RWE AG

Engie SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Ingrid has partnered with Energiequelle GmbH to co-develop and deploy 200 MW of grid-scale Battery Energy Storage Systems (BESS) across Germany. In this collaboration, Energiequelle spearheads project development, whereas Ingrid takes charge of financing, operating, and optimizing the assets through its proprietary trading and optimization platform.

- October 2025: Apple unveiled plans to bolster its renewable energy endeavors across Europe. The tech giant is set to develop 650 MW of new solar and wind farms in Greece, Italy, Latvia, Poland, and Romania.

- March 2025: RWE and TotalEnergies sealed a landmark 15-year agreement. Under this deal, RWE will supply 30,000 tons of green hydrogen each year to TotalEnergies' Leuna refinery in Germany, commencing in 2030. The initiative aims to reduce emissions at the refinery by substituting gray hydrogen with green hydrogen.

- January 2025: Plenitude revealed a 400 MW boost to its renewable energy capacity in Spain, bringing its total to nearly 950 MW. This marks a more than twofold increase from its 2023 figures, encompassing both photovoltaic and wind power projects.

Europe Power Market Report Scope

Power is the generation of electricity through various primary sources such as coal, hydro, solar, thermal, etc. In utilities, it's a step prior to its delivery to end users. Transmission and distribution take place after the process. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) as per the requirements of the end user.

The European power market is segmented by power source, end user, and geography. By power source, the market is segmented into thermal, nuclear, and renewables. By end user, the market is segmented into utilities, commercial and industrial, and residential. By geography, the market is segmented into the United Kingdom, Germany, France, Spain, Norway, Denmark, Sweden, Poland, Russia, and the rest of Europe. For each segment, the market sizing and forecasts have been carried out on the basis of installed capacity, measured in gigawatts (GW).

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Norway |

| Denmark |

| Sweden |

| Poland |

| Russia |

| Rest of Europe |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Norway | |

| Denmark | |

| Sweden | |

| Poland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe power market in 2026?

The Europe power market size is 1.95 terawatt in 2026, and it is forecast to reach 2.49 terawatt by 2031.

What is driving capacity growth across Europe?

EU Fit-for-55 and REPowerEU mandates, record-low renewable costs, and accelerated coal and nuclear retirements are key growth catalysts.

Which segment is expanding fastest by end-user?

Residential demand grows at 10.4% CAGR because of heat pumps, rooftop solar, and EV charging, outpacing utility and industrial segments.

Why are interconnectors critical for the region?

Congested cross-border lines block surplus renewable power from moving between countries, raising redispatch costs and curtailing output.

Who are the leading companies?

EDF, Enel, Iberdrola, RWE, and Engie top the capacity rankings, while Ørsted and Statkraft dominate offshore wind and hydro niches.

Page last updated on: