Ireland Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

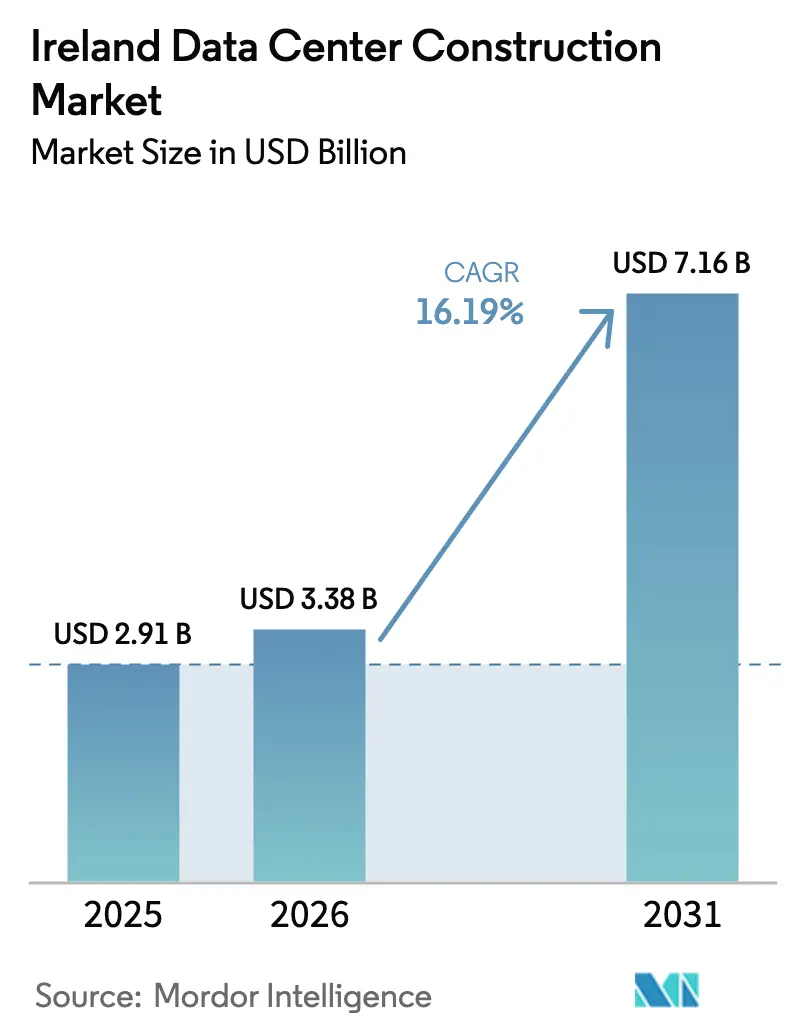

| Base Year Market Size (2025) | USD 2.91 Billion |

| Market Size (2026) | USD 3.38 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 16.19% CAGR |

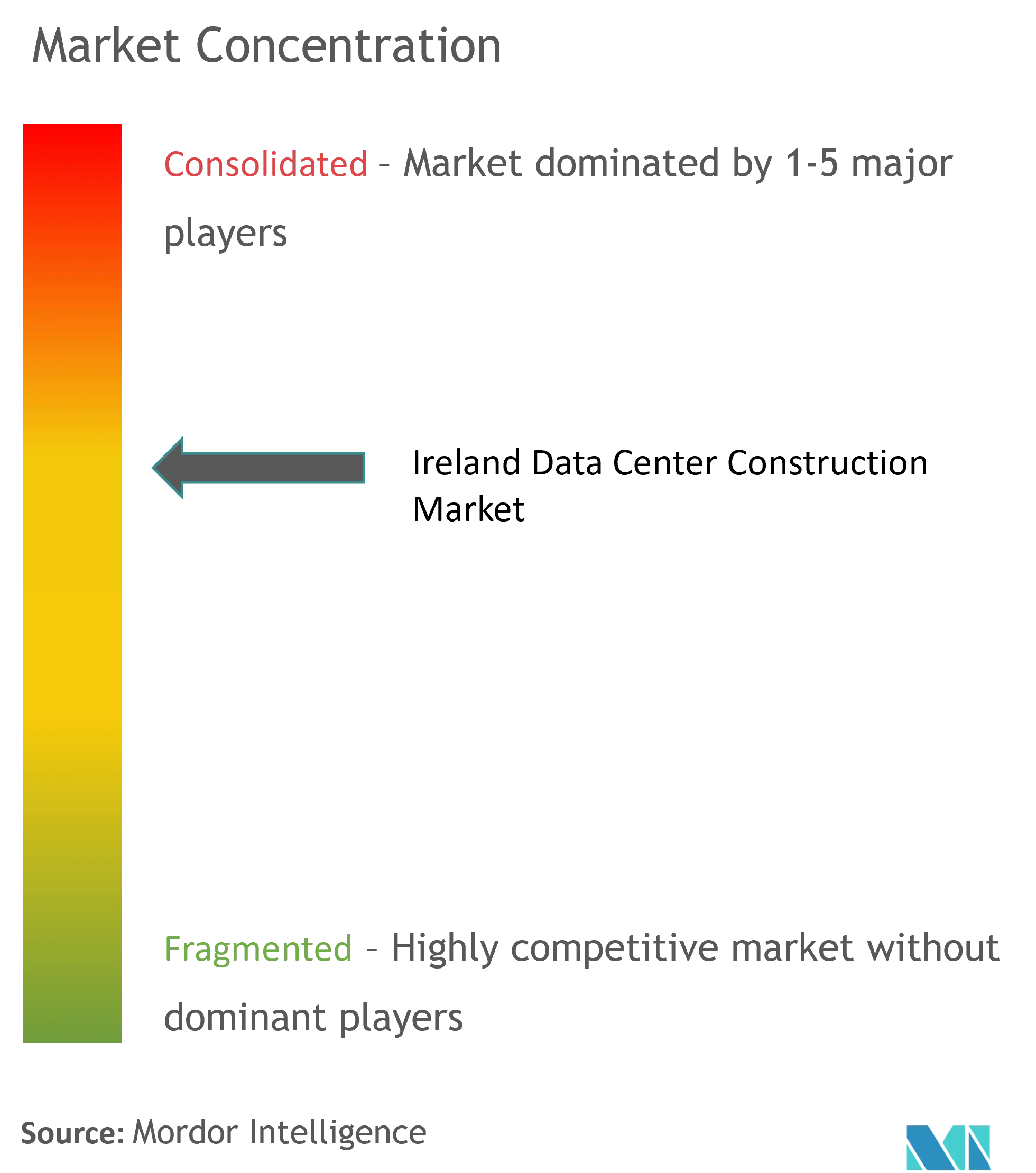

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Data Center Construction Market Analysis by Mordor Intelligence

The Ireland data center construction market size in 2026 is estimated at USD 3.38 billion, growing from 2025 value of USD 2.91 billion with 2031 projections showing USD 7.16 billion, growing at 16.19% CAGR over 2026-2031. This growth reflects Ireland’s role as a digital infrastructure hub, where hyperscale cloud operators and artificial-intelligence workloads drive demand for power-dense facilities, liquid cooling systems, and integrated on-site generation. Regulatory tension remains pronounced because data centers consumed 22% of Ireland’s electricity in 2024, intensifying the debate over grid capacity, renewable integration, and carbon targets. Developers are responding with modular builds, prefabricated electrical skids, and district-heating interfaces to secure planning approval while meeting aggressive delivery schedules. Consolidation among specialty contractors accelerates technical know-how, as seen in Turner Construction’s EUR 700 million acquisition of Dornan Engineering Group, which created the country’s largest mission-critical builder. Together, these forces sustain a market where advanced engineering capabilities, resilient power design, and sustainability credentials underpin competitive advantage.

Key Report Takeaways

- By tier type, Tier 3 facilities held 54.70% of Ireland's data center construction market share in 2025, while Tier 4 is projected to expand at a 16.38% CAGR to 2031.

- By data center type, colocation led with 58.40% revenue share in 2025; self-build hyperscaler deployments are forecast to grow at an 17.85% CAGR through 2031.

- By electrical infrastructure, power-distribution systems accounted for 51.80% share of the Ireland data center construction market size in 2025 and are advancing at a 16.18% CAGR to 2031.

- By mechanical infrastructure, cooling systems commanded a 46.60% share of the Ireland data center construction market size in 2025, whereas servers and storage components record the highest CAGR at 16.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ireland Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud and AI workload investment boom | +4.2% | National, concentrated in Dublin and Cork | Medium term (2-4 years) |

| Government digital-economy initiatives and tax incentives | +2.8% | National, with regional development focus | Long term (≥ 4 years) |

| 5G-enabled edge demand and new trans-Atlantic subsea cables | +3.1% | National, with Galway connectivity hub | Medium term (2-4 years) |

| Surplus-heat reuse mandates opening district-heating revenue | +1.9% | Dublin metropolitan area | Long term (≥ 4 years) |

| Green-bond financing momentum for sustainable facilities | +2.3% | National, emphasis on renewable energy regions | Medium term (2-4 years) |

| Modular prefab builds mitigating skilled-labour shortages | +1.5% | National, rural development priority | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud and AI Workload Investment Boom

Hyperscale and AI projects reshape specifications as rack power rises to 90-130 kW for model training, compelling liquid-cooling adoption, and 300 MW campus designs. Microsoft’s USD 500 million Grange Castle build shows how on-site generation circumvents Dublin’s grid moratorium and secures predictable energy. Investor appetite remains strong; Vantage Data Centers raised EUR 720 million via Europe’s first data-center securitization to fund Dublin capacity that relies on hydrotreated-vegetable-oil generators. These investments cascade across the Ireland data center construction market as contractors compete for GPU-ready cooling packages, high-frequency switchgear and resilient distribution paths. Supply-chain strain intensifies demand for prefabricated modules that shorten on-site schedules and guarantee component availability.

Government Digital-Economy Initiatives and Tax Incentives

Ireland’s enterprise policy highlights a EUR 7 billion (USD 8.06 billion) economic contribution from data centers since 2010 and prioritizes them as strategic assets.[1]Department of Enterprise, “Ireland’s Digital-Economy Strategy 2025,” enterprise.gov.ieThe Planning & Development Bill 2023 accelerates approvals for large sites while enforcing sustainability screening, pushing builders to integrate renewable sourcing and heat-recovery loops from day one. IDA Ireland’s grants steer construction toward regional towns such as Galway, where fast-track permitting and land support reduce soft costs idaireland.com. Tax relief for green-capex plus accelerated depreciation trims project budgets by 8-12%, improving return profiles for Tier 4 builds. Collectively, fiscal incentives preserve Ireland data center construction market momentum despite power-capacity headwinds.

5G-Enabled Edge Demand and New Trans-Atlantic Subsea Cables

The EUR 1.1 billion (USD 1.27 billion) Far North Fiber, a 15,000 km cable landing in Galway, positions Ireland as a trans-Pacific gateway.[2]Marine Institute, “Far North Fiber to Land in Galway,” marine.ie Low-latency applications linked to 5G require edge nodes within 20 km of users, prompting 1-5 MW modular sites across Cork, Limerick, and Waterford. Prefabricated steel frames, containerized chillers, and standardized bus ducts support 12-18 month delivery cycles—half that of conventional hyperscale campuses. Sub-marine landing stations introduce strict environmental criteria, so contractors with coastal engineering expertise secure premium margins. Edge proliferation diversifies the Ireland data center construction market while easing pressure on Dublin’s grid.

Surplus-Heat Reuse Mandates and District-Heating Revenue

Dublin’s heat-reuse rules create secondary revenue as Amazon’s Tallaght facility delivers 3 MW of thermal output, lowering emissions by 1,500 t annually.[3]Werner Vogels, “AWS Heat Reuse in Tallaght,” allthingsdistributed.comConstruction now embeds plate-exchangers, insulated pipework and metering for third-party heat offtake, adding 3-5% to capex yet boosting lifecycle returns 12-15%. Equinix’s Blanchardstown site proves scalability, integrating recovery systems during fit-out to avoid costly retrofits. Contractors skilled in thermal hydraulics gain bid advantages as heat-reuse shifts from optional to required for permits, reinforcing sustainability credentials across the Ireland data center construction market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-connection moratorium & Dublin power-capacity shortfall | -3.8% | Dublin metropolitan area | Short term (≤ 2 years) |

| Escalating electricity costs & carbon-pricing exposure | -2.1% | National, higher impact in urban areas | Medium term (2-4 years) |

| Long-lead HV switchgear & transformer supply bottlenecks | -2.9% | National, affecting all major projects | Short term (≤ 2 years) |

| Local opposition over groundwater & cooling-water abstraction | -1.4% | Regional, particularly rural developments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Moratorium and Dublin Capacity Shortfall

EirGrid’s suspension of new Dublin data-center connections until 2028 pushes developers toward on-site generation that lifts capex 15-20% while prolonging design cycles. The regulator now assesses applications case-by-case, prioritizing facilities able to shed load or island from the grid. Developers spend an extra 6-12 months securing gas turbines, battery farms and wastewater-sourced cooling to maintain schedules. The constraint bifurcates the Ireland data center construction market between grid-tied builds and hybrid projects with dedicated generation.

Long-Lead Transformer and HV Switchgear Bottlenecks

Global transformer scarcity stretches delivery beyond 100 weeks and raises prices, turning HV gear into the critical path of many Irish builds. AI-ready sites needing 300 kW-plus racks depend on specialized step-down units that few vendors supply at scale. Contractors such as Kirby Group Engineering invest in an EUR 8 million prefabrication plant to manufacture electrical skids and mitigate supply-chain risk. Those without secured gear face 6-18 month delays, eroding project IRR and straining customer commitments. Component stockpiling and early procurement now dominate bid strategies across the Ireland data center construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Shift Toward Fault-Tolerant Infrastructure

Tier 3 designs held 54.70% of the Ireland data center construction market in 2025 as a cost-efficient baseline for cloud hosting, yet Tier 4 facilities are on track for a 16.38% CAGR through 2031. This premium reflects AI training workloads demanding 99.995% availability and 2N+1 redundancy in power, cooling and network paths, forcing contractors to master concurrent-maintenance layouts and fault-tolerant switchgear.

High-complexity builds raise margins but also carry schedule risks; builders like Mercury Engineering deliver Tier 4 projects using off-site-fabricated MEP modules to compress fit-out by 20%. Financial institutions and semiconductor fabs co-locate AI clusters inside Tier 4 shells, anchoring long-term leases that stabilize cash flows. Green-bond investors favor Tier 4 because integrated renewable inputs and heat-recovery loops align with ESG criteria, reinforcing their dominance in the Ireland data center construction market. Lenders now discount Tier 1 and Tier 2 projects, deeming them obsolete for edge or 5G use-cases that also require high uptime.

By Data Center Type: Hyperscaler Self-Build Gains Pace

Colocation operators maintained 58.40% revenue in 2025, but self-build hyperscaler campuses are expanding at an 17.85% CAGR, reshaping the Ireland data center construction market size for owner-developed assets. Hyperscalers retain full design authority, enabling 480 V distribution, liquid-immersion cooling and custom AI accelerators without shared governance.

Turner-Dornan’s integration targets this segment, offering combined civil, electrical and process-piping capability to meet single-contractor procurement models. Meanwhile, colocation firms respond by pivoting to “build-to-suit” shells that accommodate 140 kW racks on shared backbones. Edge and enterprise micro-facilities also grow as sovereign-data laws and telecom 5G rollouts require distributed 1-5 MW nodes. Each archetype fuels unique supply-chain flows, widening participation in the Ireland data center construction market.

By Electrical Infrastructure: Distribution Systems Dominate Capex

Power-distribution assemblies captured 51.80% of Ireland data center construction market share in 2025 and will grow 16.18% annually, reflecting moves to 600 V buses, back-fed breakers and bus-duct topology. High-density racks propel demand for fast-switching static transfer units that isolate faults in microseconds, protecting GPU clusters valued at millions per row.

Transformer shortages prompt builders to pre-purchase gear two years out, locking prices and warehousing units close to site. To shorten installation, Kirby Group now ships pre-terminated busways from its Portlaoise factory, reducing field labor 30%. Backup systems evolve too; lithium-ion UPS blocks and hydrogen fuel cells appear in Tier 4 designs, although uptake stays limited to flagship campuses. Electrical scope thus remains the largest risk and profit lever in the Ireland data center construction market

By Mechanical Infrastructure: Cooling Technology Transforms Design

Cooling systems held 46.60% of the Ireland data center construction market size in 2025, yet servers and storage posted a faster 16.88% CAGR as hardware shifts to GPU-dense blades. Liquid technologies dominate specification lists, with direct-to-chip loops, rear-door heat exchangers and immersion tanks replacing legacy CRAC rows.

R&D from Irish start-ups like Nexalus recovers up to 80% of waste heat, aligning with district-heating mandates while driving PUE below 1.1. Facebook’s StatePoint deployment in Clonee exemplifies evaporative systems that cut water use by 30-40%. The mechanical package now intersects strongly with architectural design because chilled-water plants, pumps and plate exchangers define building massing. Mastering these interfaces differentiates contractors in the Ireland data center construction market, which increasingly resembles advanced manufacturing rather than commercial real-estate work.

Geography Analysis

Development remains Dublin-centric, with roughly 60% of operational facilities, owing to dense fiber rings, submarine-cable proximity and a deep subcontractor base. However, the grid-connection embargo redirects fresh capital toward counties with renewable headroom and receptive councils, diversifying the Ireland data center construction market.

Cork rises as the principal alternative, supported by legacy tech employers and better wind-farm linkage, enabling lower energy tariffs and streamlined permits. EMC’s planned expansion validates the city’s potential to anchor hyperscale clusters that siphon overflow from Dublin.

Galway’s relevance accelerates with the Far North Fiber landing that positions the region for latency-sensitive Asia-Europe routes, attracting edge clusters aimed at trans-Pacific content delivery. County Offaly and County Mayo also court investment by bundling brownfield industrial sites with grid capacity from local wind assets, shortening lead times.

As a result, regional contractors partner with national specialists to deliver standardized 5 MW modules, ensuring the Ireland data center construction market maintains momentum irrespective of Dublin restrictions.

Competitive Landscape

Market consolidation advances as specialty players command high-value mechanical and electrical scopes that traditional builders cannot match. Turner Construction’s EUR 700 million Dornan buyout produced a 1,000-person entity holding EUR 1.6 billion backlog concentrated 85% in advanced-technology projects.

Mercury Engineering, Collen Construction and BAM Ireland retain strong positions by offering design-build approaches with single-line accountability, an advantage prized by hyperscalers seeking rapid, repeatable deployment. Kirby Group Engineering, meanwhile, leverages its Portlaoise prefab plant and BIM library to deliver 25% of projects with factory-assembled skids, mitigating labor scarcities.

Competitive dynamics shift as green-bond investors and district-heating mandates favor contractors with demonstrable sustainability records. Firms that bundle low-carbon concrete, HVO generators and heat-recovery subsystems increasingly win bids. Consequently, technical depth and ESG compliance—not low price—govern contract awards across the Ireland data center construction market.

Ireland Data Center Construction Industry Leaders

Mercury Engineering

Jacobs Engineering Group

Arup

AECOM Ireland Ltd

Turner & Townsend

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vantage Data Centers secured EUR 720 million in Europe’s first data-center securitization, funding 64 MW of fully leased Irish capacity.

- January 2025: Turner Construction completed its EUR 700 million purchase of Dornan Engineering Group, creating Ireland’s largest data-center construction firm with a EUR 1.6 billion backlog.

- December 2024: Equinix acquired BT’s Irish data-center portfolio for EUR 59 million, adding two Dublin facilities with expansion headroom for AI workloads.

- November 2024: Kirby Group Engineering inaugurated an EUR 8 million off-site manufacturing hub in Portlaoise, enabling prefabrication for 25% of its projects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Ireland data center construction market as the annual spend, both greenfield and major brownfield, on civil works, electrical power distribution packages, mechanical cooling, and commissioning services required to bring new data center white space online across the Republic of Ireland. Conversions of legacy office blocks, modular edge pods, and hyperscale self-build campuses are all counted once the general contractor breaks ground.

Scope exclusion: routine facilities management, rack-level IT refreshes, and pure land acquisitions are outside the market.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

- Tier 1 and 2

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed Irish MEP service engineers, Tier III design consultants, and procurement leads at hyperscale operators across Dublin, Cork, and Galway. These conversations validated typical cost per megawatt, shift premiums, and lead times for 132 kV substations, then reconciled them with desk findings to close data gaps.

Desk Research

We began with public records from the Central Statistics Office, Commission for Regulation of Utilities, and EirGrid load connection files, which quantify construction cost indices, grid queue capacity, and regional power tariffs. Trade associations such as Host in Ireland and the European Data Centre Association provided baseline project pipelines, while company filings and planning permission portals in Dublin and Meath clarified individual site budgets. Paid libraries, including D&B Hoovers for contractor revenue splits and Dow Jones Factiva for project announcements, helped us date stamp spend profiles. The sources listed illustrate our approach; many additional feeds informed cross checks.

Market-Sizing & Forecasting

We applied a top-down investment pool reconstruction: published grid connection MW additions, multiplied by benchmark cost per MW, built the base year. Select bottom-up roll-ups of eight emblematic projects, civil, electrical, and mechanical packages, provided a reasonableness screen. Key variables like average floor area additions, median installed power density, exchange rate movements, contractor margin trends, and government moratorium scenarios drive the model. A multivariate regression with scenario overlays projects spend through 2030; where supplier quotes were missing, we prorated costs using historical €/m² relationships observed in comparable EU builds.

Data Validation & Update Cycle

Outputs pass three-layer checks: variance against historic CAPEX/MW norms, peer review among senior analysts, and final sign-off before publication. The model refreshes annually, with interim updates triggered by large project announcements or policy shifts.

Why Our Ireland Data Center Construction Baseline Commands Reliability

Published figures often diverge because firms select different cost elements, FX treatments, and refresh cadences.

Key gap drivers include exclusion of retrofit electrical works, use of announced, not executed, budgets, or single year exchange rates that ignore inflation pass-throughs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.91 B (2025) | Mordor Intelligence | - |

| USD 1.70 B (2024) | Global Consultancy A | omits mechanical retrofits and applies 2024 only grid projects |

| EUR 2.51 B (2025) | Trade Journal B | relies on planned spend without adjusting for deferred builds and uses constant 1:1 FX |

These comparisons show that by aligning spend to confirmed ground-breaking dates, adjusting every line for inflation and currency, and revisiting assumptions each year, Mordor Intelligence delivers the balanced baseline decision makers can trust.

Key Questions Answered in the Report

What is the current value of the Ireland data center construction market?

The market stands at USD 3.38 billion in 2026 and is projected to reach USD 7.16 billion by 2031.

Why are Tier 4 facilities growing faster than other tiers?

AI training workloads require 99.995% uptime and 2N+1 redundancy, prompting hyperscalers to favor Tier 4 designs that can support 90-130 kW racks.

How is Dublin’s grid-connection moratorium affecting new projects?

Developers must add on-site generation or shift builds to Cork, Galway and rural counties, extending schedules by up to 12 months in some cases.

Which infrastructure segment captures the largest share of project budgets?

Power-distribution equipment leads with 51.80% share in 2025 because AI-ready facilities need 600 V bus ducts, redundant switchgear and fast-transfer units.

Page last updated on: